Financial Accounting: Journal, Ledger, and Financial Statements

VerifiedAdded on 2022/12/29

|14

|2632

|199

Homework Assignment

AI Summary

This assignment provides a comprehensive overview of recording business transactions, starting with journal entries and progressing through ledger accounts, trial balances, income statements, and balance sheets. The solution uses a case study of a new business, detailing each step in the accounting cycle. It includes the creation of a journal, the posting of entries to a ledger, and the preparation of financial statements. Furthermore, the assignment calculates and analyzes various financial ratios, such as net profit margin, gross profit margin, current ratio, quick ratio, accounts receivable collection period, and accounts payable payment period, comparing the business's performance to that of its competitors. The analysis includes the treatment of owner's drawings and their impact on financial statements, ensuring a thorough understanding of the accounting principles involved.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

JOURNAL...................................................................................................................................3

LEDGER......................................................................................................................................4

Trial Balance as on 31 October 2020...........................................................................................6

Income Statement for the period ending 31 October 2020..........................................................7

Balance Sheet as at 31 October 2020...........................................................................................7

REFERENCES................................................................................................................................1

CONCLUSION................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

JOURNAL...................................................................................................................................3

LEDGER......................................................................................................................................4

Trial Balance as on 31 October 2020...........................................................................................6

Income Statement for the period ending 31 October 2020..........................................................7

Balance Sheet as at 31 October 2020...........................................................................................7

REFERENCES................................................................................................................................1

CONCLUSION................................................................................................................................1

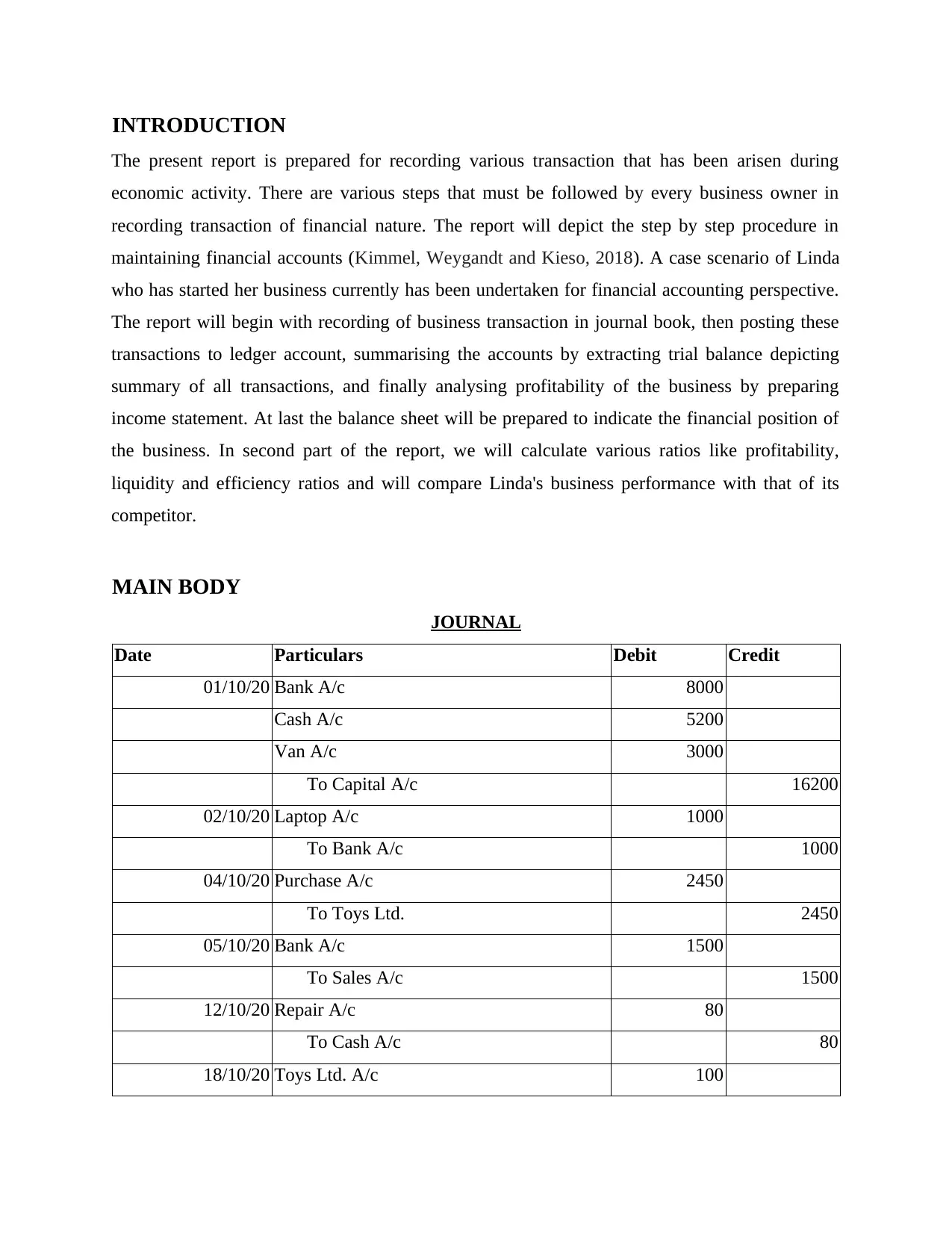

INTRODUCTION

The present report is prepared for recording various transaction that has been arisen during

economic activity. There are various steps that must be followed by every business owner in

recording transaction of financial nature. The report will depict the step by step procedure in

maintaining financial accounts (Kimmel, Weygandt and Kieso, 2018). A case scenario of Linda

who has started her business currently has been undertaken for financial accounting perspective.

The report will begin with recording of business transaction in journal book, then posting these

transactions to ledger account, summarising the accounts by extracting trial balance depicting

summary of all transactions, and finally analysing profitability of the business by preparing

income statement. At last the balance sheet will be prepared to indicate the financial position of

the business. In second part of the report, we will calculate various ratios like profitability,

liquidity and efficiency ratios and will compare Linda's business performance with that of its

competitor.

MAIN BODY

JOURNAL

Date Particulars Debit Credit

01/10/20 Bank A/c 8000

Cash A/c 5200

Van A/c 3000

To Capital A/c 16200

02/10/20 Laptop A/c 1000

To Bank A/c 1000

04/10/20 Purchase A/c 2450

To Toys Ltd. 2450

05/10/20 Bank A/c 1500

To Sales A/c 1500

12/10/20 Repair A/c 80

To Cash A/c 80

18/10/20 Toys Ltd. A/c 100

The present report is prepared for recording various transaction that has been arisen during

economic activity. There are various steps that must be followed by every business owner in

recording transaction of financial nature. The report will depict the step by step procedure in

maintaining financial accounts (Kimmel, Weygandt and Kieso, 2018). A case scenario of Linda

who has started her business currently has been undertaken for financial accounting perspective.

The report will begin with recording of business transaction in journal book, then posting these

transactions to ledger account, summarising the accounts by extracting trial balance depicting

summary of all transactions, and finally analysing profitability of the business by preparing

income statement. At last the balance sheet will be prepared to indicate the financial position of

the business. In second part of the report, we will calculate various ratios like profitability,

liquidity and efficiency ratios and will compare Linda's business performance with that of its

competitor.

MAIN BODY

JOURNAL

Date Particulars Debit Credit

01/10/20 Bank A/c 8000

Cash A/c 5200

Van A/c 3000

To Capital A/c 16200

02/10/20 Laptop A/c 1000

To Bank A/c 1000

04/10/20 Purchase A/c 2450

To Toys Ltd. 2450

05/10/20 Bank A/c 1500

To Sales A/c 1500

12/10/20 Repair A/c 80

To Cash A/c 80

18/10/20 Toys Ltd. A/c 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To Purchase A/c 100

21/10/20 Bank A/c 500

To Rent for premises A/c 500

23/10/20 Cash A/c 1500

Fred A/c 400

To Sales A/c 1900

23/10/20 Cash A/c 500

To Sales A/c 500

24/10/20 Second-hand car 2500

To Bank A/c 2500

26/10/20 Wages A/c 820

To Bank A/c 820

30/10/20 Rent A/c 1000

To Bank A/c 1000

31/10/20 **Drawings A/c 1600

To Bank A/c 1600

Total 30150 30150

**Note: The trip to Florida undertaken by Linda and its associated expenses will be considered

as business expenses as the question is silent about the cause of the trip. So the given expenses

made by Linda out of her business account will not be treated as business expense and rather

than that, this will be treated as Drawings made by her out of her own capital (Li, 2018).

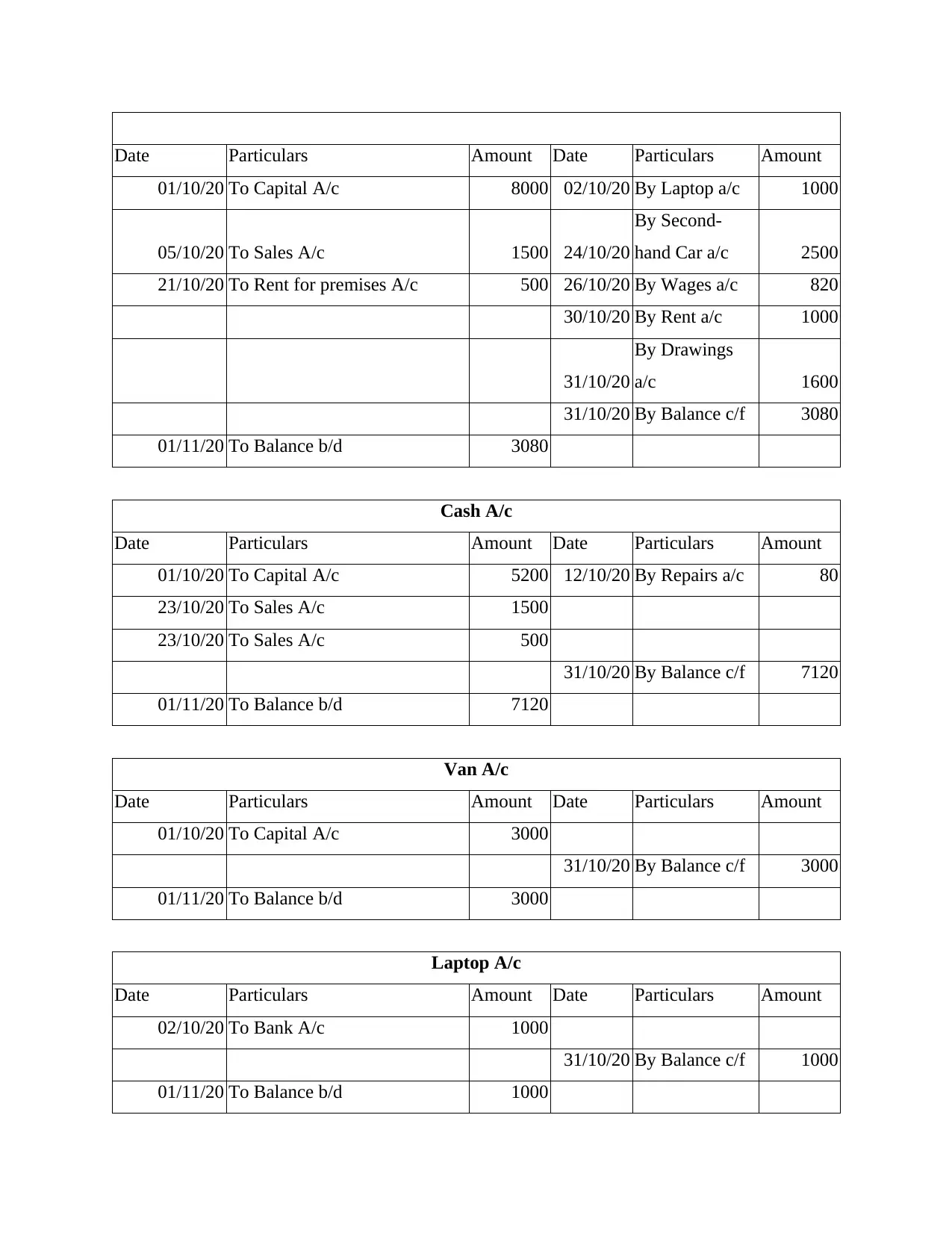

LEDGER

Capital A/c

Date Particulars Amount Date Particulars Amount

31/10/20 To Drawings a/c 1600 01/10/20 By Bank a/c 8000

By Cash a/c 5200

By Van a/c 3000

31/10/20 To Balance c/f 14600

01/11/20 By Balance b/d 14600

Bank A/c

21/10/20 Bank A/c 500

To Rent for premises A/c 500

23/10/20 Cash A/c 1500

Fred A/c 400

To Sales A/c 1900

23/10/20 Cash A/c 500

To Sales A/c 500

24/10/20 Second-hand car 2500

To Bank A/c 2500

26/10/20 Wages A/c 820

To Bank A/c 820

30/10/20 Rent A/c 1000

To Bank A/c 1000

31/10/20 **Drawings A/c 1600

To Bank A/c 1600

Total 30150 30150

**Note: The trip to Florida undertaken by Linda and its associated expenses will be considered

as business expenses as the question is silent about the cause of the trip. So the given expenses

made by Linda out of her business account will not be treated as business expense and rather

than that, this will be treated as Drawings made by her out of her own capital (Li, 2018).

LEDGER

Capital A/c

Date Particulars Amount Date Particulars Amount

31/10/20 To Drawings a/c 1600 01/10/20 By Bank a/c 8000

By Cash a/c 5200

By Van a/c 3000

31/10/20 To Balance c/f 14600

01/11/20 By Balance b/d 14600

Bank A/c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars Amount Date Particulars Amount

01/10/20 To Capital A/c 8000 02/10/20 By Laptop a/c 1000

05/10/20 To Sales A/c 1500 24/10/20

By Second-

hand Car a/c 2500

21/10/20 To Rent for premises A/c 500 26/10/20 By Wages a/c 820

30/10/20 By Rent a/c 1000

31/10/20

By Drawings

a/c 1600

31/10/20 By Balance c/f 3080

01/11/20 To Balance b/d 3080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/10/20 To Capital A/c 5200 12/10/20 By Repairs a/c 80

23/10/20 To Sales A/c 1500

23/10/20 To Sales A/c 500

31/10/20 By Balance c/f 7120

01/11/20 To Balance b/d 7120

Van A/c

Date Particulars Amount Date Particulars Amount

01/10/20 To Capital A/c 3000

31/10/20 By Balance c/f 3000

01/11/20 To Balance b/d 3000

Laptop A/c

Date Particulars Amount Date Particulars Amount

02/10/20 To Bank A/c 1000

31/10/20 By Balance c/f 1000

01/11/20 To Balance b/d 1000

01/10/20 To Capital A/c 8000 02/10/20 By Laptop a/c 1000

05/10/20 To Sales A/c 1500 24/10/20

By Second-

hand Car a/c 2500

21/10/20 To Rent for premises A/c 500 26/10/20 By Wages a/c 820

30/10/20 By Rent a/c 1000

31/10/20

By Drawings

a/c 1600

31/10/20 By Balance c/f 3080

01/11/20 To Balance b/d 3080

Cash A/c

Date Particulars Amount Date Particulars Amount

01/10/20 To Capital A/c 5200 12/10/20 By Repairs a/c 80

23/10/20 To Sales A/c 1500

23/10/20 To Sales A/c 500

31/10/20 By Balance c/f 7120

01/11/20 To Balance b/d 7120

Van A/c

Date Particulars Amount Date Particulars Amount

01/10/20 To Capital A/c 3000

31/10/20 By Balance c/f 3000

01/11/20 To Balance b/d 3000

Laptop A/c

Date Particulars Amount Date Particulars Amount

02/10/20 To Bank A/c 1000

31/10/20 By Balance c/f 1000

01/11/20 To Balance b/d 1000

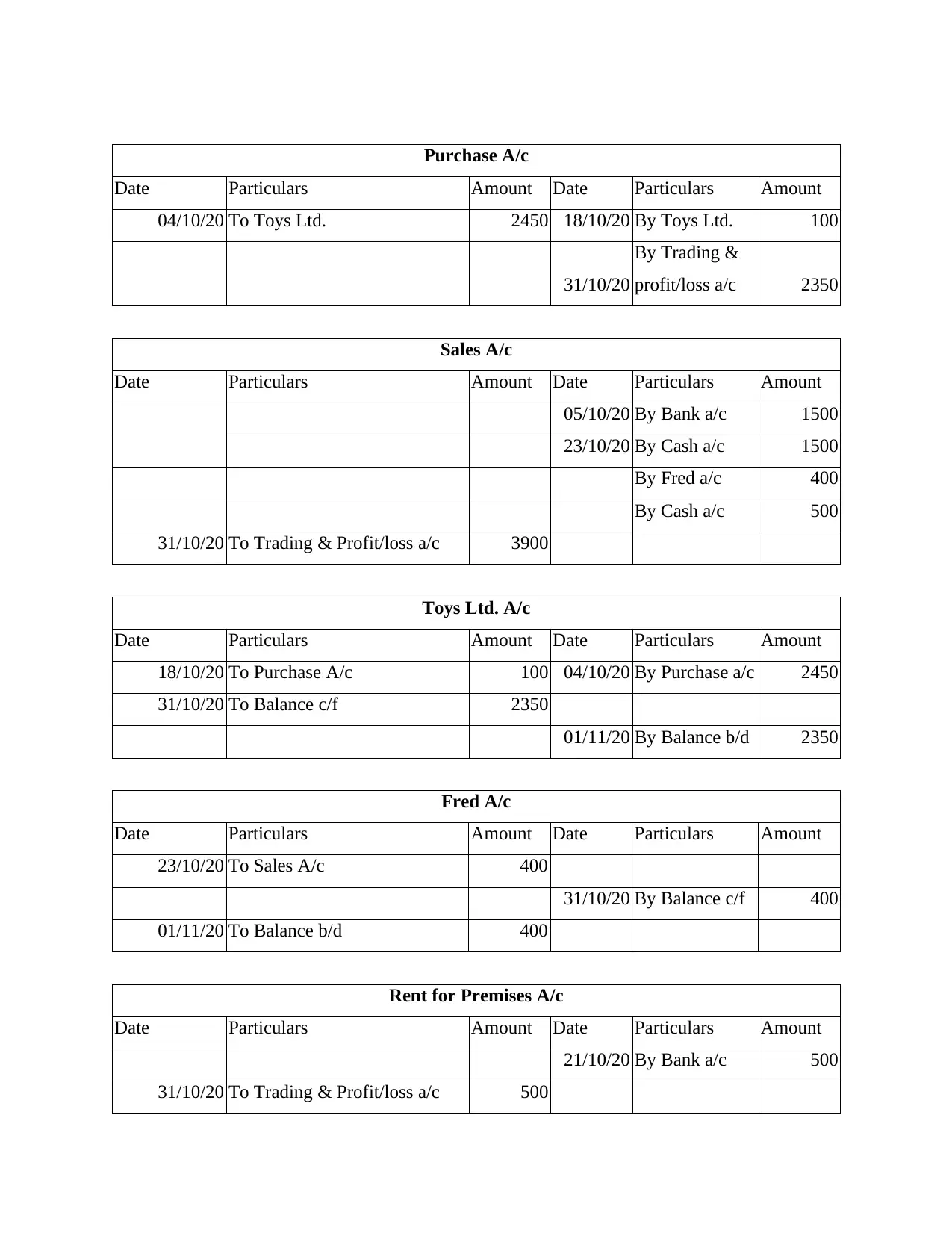

Purchase A/c

Date Particulars Amount Date Particulars Amount

04/10/20 To Toys Ltd. 2450 18/10/20 By Toys Ltd. 100

31/10/20

By Trading &

profit/loss a/c 2350

Sales A/c

Date Particulars Amount Date Particulars Amount

05/10/20 By Bank a/c 1500

23/10/20 By Cash a/c 1500

By Fred a/c 400

By Cash a/c 500

31/10/20 To Trading & Profit/loss a/c 3900

Toys Ltd. A/c

Date Particulars Amount Date Particulars Amount

18/10/20 To Purchase A/c 100 04/10/20 By Purchase a/c 2450

31/10/20 To Balance c/f 2350

01/11/20 By Balance b/d 2350

Fred A/c

Date Particulars Amount Date Particulars Amount

23/10/20 To Sales A/c 400

31/10/20 By Balance c/f 400

01/11/20 To Balance b/d 400

Rent for Premises A/c

Date Particulars Amount Date Particulars Amount

21/10/20 By Bank a/c 500

31/10/20 To Trading & Profit/loss a/c 500

Date Particulars Amount Date Particulars Amount

04/10/20 To Toys Ltd. 2450 18/10/20 By Toys Ltd. 100

31/10/20

By Trading &

profit/loss a/c 2350

Sales A/c

Date Particulars Amount Date Particulars Amount

05/10/20 By Bank a/c 1500

23/10/20 By Cash a/c 1500

By Fred a/c 400

By Cash a/c 500

31/10/20 To Trading & Profit/loss a/c 3900

Toys Ltd. A/c

Date Particulars Amount Date Particulars Amount

18/10/20 To Purchase A/c 100 04/10/20 By Purchase a/c 2450

31/10/20 To Balance c/f 2350

01/11/20 By Balance b/d 2350

Fred A/c

Date Particulars Amount Date Particulars Amount

23/10/20 To Sales A/c 400

31/10/20 By Balance c/f 400

01/11/20 To Balance b/d 400

Rent for Premises A/c

Date Particulars Amount Date Particulars Amount

21/10/20 By Bank a/c 500

31/10/20 To Trading & Profit/loss a/c 500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Second-hand Car A/c

Date Particulars Amount Date Particulars Amount

24/10/20 To Bank A/c 2500

31/10/20 By Balance c/f 2500

01/11/20 To Balance b/d 2500

Wages A/c

Date Particulars Amount Date Particulars Amount

26/10/20 To Bank A/c 820

31/10/20

By Trading &

profit/loss a/c 820

Drawings A/c

Date Particulars Amount Date Particulars Amount

31/10/20 To Bank A/c 1600 31/10/20 By Capital a/c 1600

Rent A/c

Date Particulars Amount Date Particulars Amount

30/10/20 To Bank A/c 1000 31/10/20

By Trading &

profit/loss a/c 1000

Repairs A/c

Date Particulars Amount Date Particulars Amount

12/10/20 To Cash A/c 80 31/10/20

By Trading &

profit/loss a/c 80

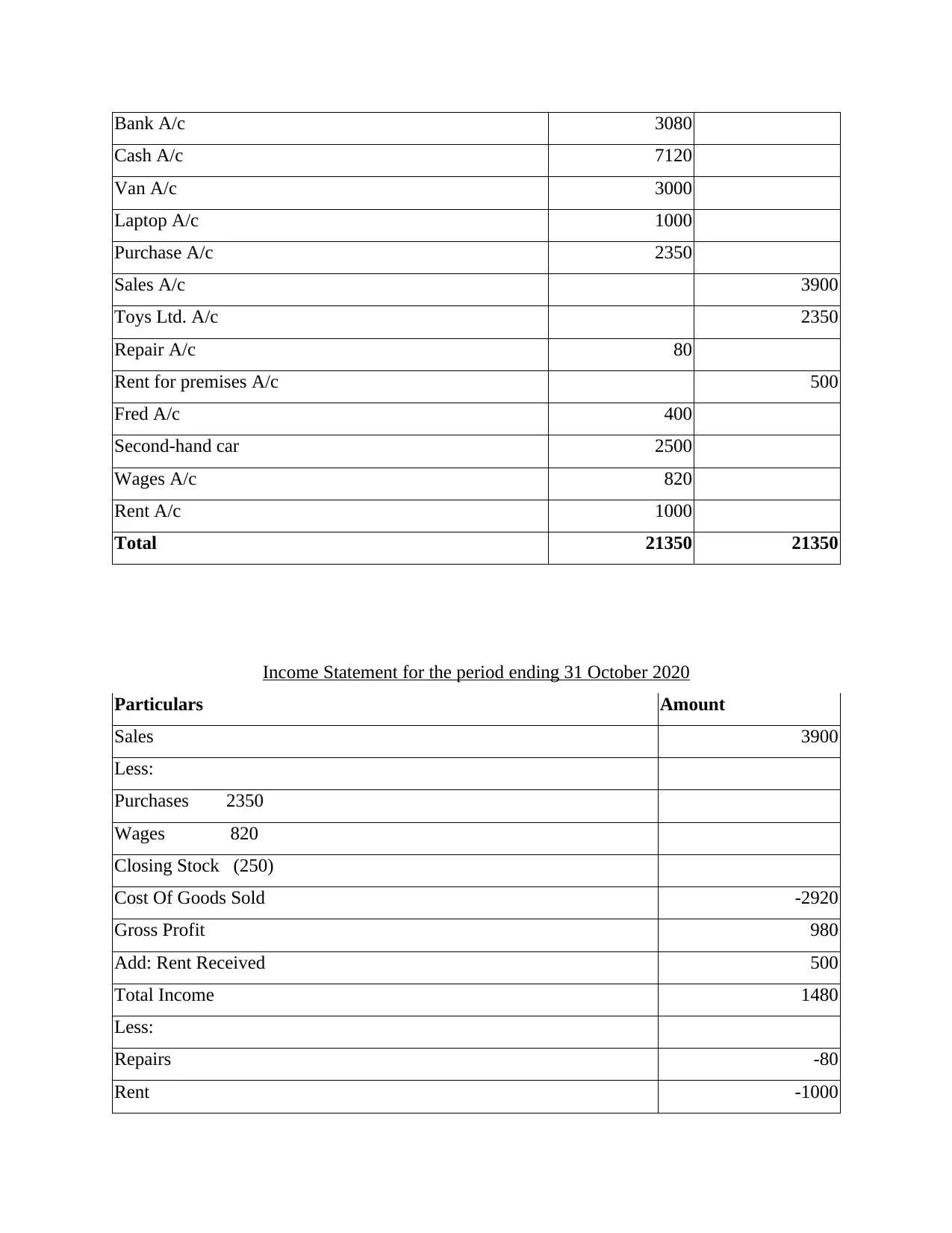

Trial Balance as on 31 October 2020

Particulars Debit Credit

Capital 14600

Date Particulars Amount Date Particulars Amount

24/10/20 To Bank A/c 2500

31/10/20 By Balance c/f 2500

01/11/20 To Balance b/d 2500

Wages A/c

Date Particulars Amount Date Particulars Amount

26/10/20 To Bank A/c 820

31/10/20

By Trading &

profit/loss a/c 820

Drawings A/c

Date Particulars Amount Date Particulars Amount

31/10/20 To Bank A/c 1600 31/10/20 By Capital a/c 1600

Rent A/c

Date Particulars Amount Date Particulars Amount

30/10/20 To Bank A/c 1000 31/10/20

By Trading &

profit/loss a/c 1000

Repairs A/c

Date Particulars Amount Date Particulars Amount

12/10/20 To Cash A/c 80 31/10/20

By Trading &

profit/loss a/c 80

Trial Balance as on 31 October 2020

Particulars Debit Credit

Capital 14600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank A/c 3080

Cash A/c 7120

Van A/c 3000

Laptop A/c 1000

Purchase A/c 2350

Sales A/c 3900

Toys Ltd. A/c 2350

Repair A/c 80

Rent for premises A/c 500

Fred A/c 400

Second-hand car 2500

Wages A/c 820

Rent A/c 1000

Total 21350 21350

Income Statement for the period ending 31 October 2020

Particulars Amount

Sales 3900

Less:

Purchases 2350

Wages 820

Closing Stock (250)

Cost Of Goods Sold -2920

Gross Profit 980

Add: Rent Received 500

Total Income 1480

Less:

Repairs -80

Rent -1000

Cash A/c 7120

Van A/c 3000

Laptop A/c 1000

Purchase A/c 2350

Sales A/c 3900

Toys Ltd. A/c 2350

Repair A/c 80

Rent for premises A/c 500

Fred A/c 400

Second-hand car 2500

Wages A/c 820

Rent A/c 1000

Total 21350 21350

Income Statement for the period ending 31 October 2020

Particulars Amount

Sales 3900

Less:

Purchases 2350

Wages 820

Closing Stock (250)

Cost Of Goods Sold -2920

Gross Profit 980

Add: Rent Received 500

Total Income 1480

Less:

Repairs -80

Rent -1000

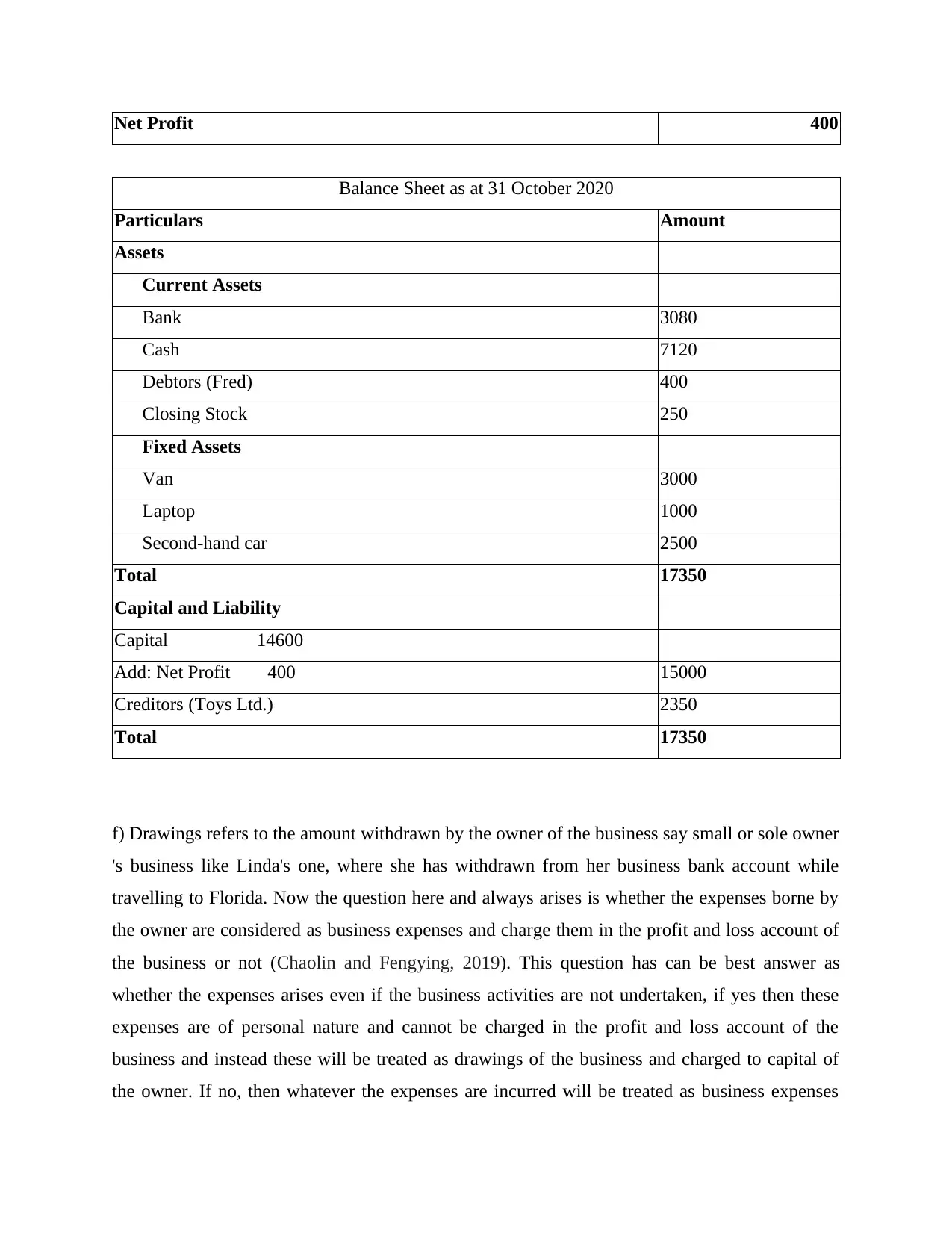

Net Profit 400

Balance Sheet as at 31 October 2020

Particulars Amount

Assets

Current Assets

Bank 3080

Cash 7120

Debtors (Fred) 400

Closing Stock 250

Fixed Assets

Van 3000

Laptop 1000

Second-hand car 2500

Total 17350

Capital and Liability

Capital 14600

Add: Net Profit 400 15000

Creditors (Toys Ltd.) 2350

Total 17350

f) Drawings refers to the amount withdrawn by the owner of the business say small or sole owner

's business like Linda's one, where she has withdrawn from her business bank account while

travelling to Florida. Now the question here and always arises is whether the expenses borne by

the owner are considered as business expenses and charge them in the profit and loss account of

the business or not (Chaolin and Fengying, 2019). This question has can be best answer as

whether the expenses arises even if the business activities are not undertaken, if yes then these

expenses are of personal nature and cannot be charged in the profit and loss account of the

business and instead these will be treated as drawings of the business and charged to capital of

the owner. If no, then whatever the expenses are incurred will be treated as business expenses

Balance Sheet as at 31 October 2020

Particulars Amount

Assets

Current Assets

Bank 3080

Cash 7120

Debtors (Fred) 400

Closing Stock 250

Fixed Assets

Van 3000

Laptop 1000

Second-hand car 2500

Total 17350

Capital and Liability

Capital 14600

Add: Net Profit 400 15000

Creditors (Toys Ltd.) 2350

Total 17350

f) Drawings refers to the amount withdrawn by the owner of the business say small or sole owner

's business like Linda's one, where she has withdrawn from her business bank account while

travelling to Florida. Now the question here and always arises is whether the expenses borne by

the owner are considered as business expenses and charge them in the profit and loss account of

the business or not (Chaolin and Fengying, 2019). This question has can be best answer as

whether the expenses arises even if the business activities are not undertaken, if yes then these

expenses are of personal nature and cannot be charged in the profit and loss account of the

business and instead these will be treated as drawings of the business and charged to capital of

the owner. If no, then whatever the expenses are incurred will be treated as business expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and accordingly will be charged in profit and loss account (Schroeder, Clark and Cathey, 2019).

Here Linda must treat her withdrawal from business bank account during Florida Travel as

drawing made by her out her business capital account which will reduce her capital balance by

that amount.

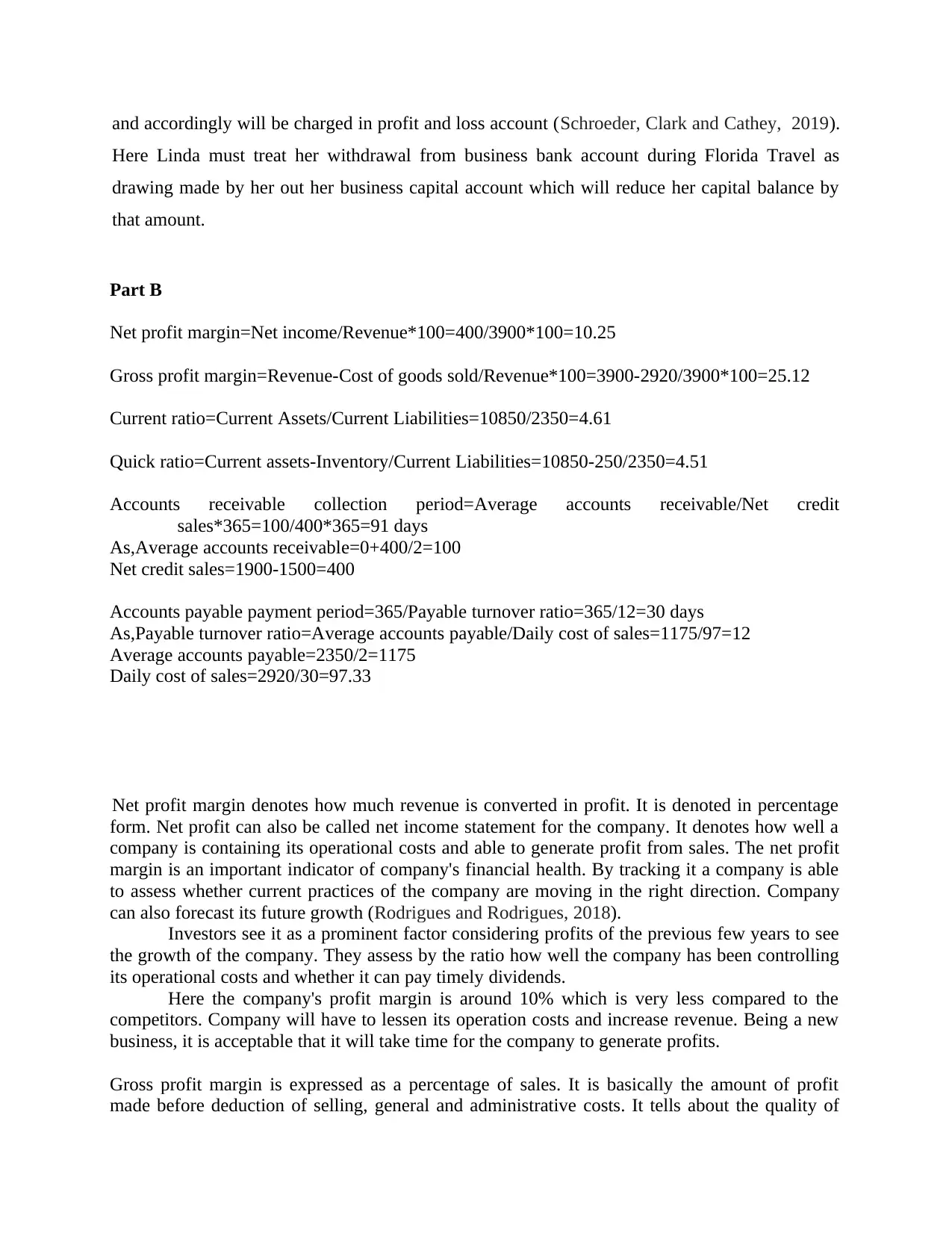

Part B

Net profit margin=Net income/Revenue*100=400/3900*100=10.25

Gross profit margin=Revenue-Cost of goods sold/Revenue*100=3900-2920/3900*100=25.12

Current ratio=Current Assets/Current Liabilities=10850/2350=4.61

Quick ratio=Current assets-Inventory/Current Liabilities=10850-250/2350=4.51

Accounts receivable collection period=Average accounts receivable/Net credit

sales*365=100/400*365=91 days

As,Average accounts receivable=0+400/2=100

Net credit sales=1900-1500=400

Accounts payable payment period=365/Payable turnover ratio=365/12=30 days

As,Payable turnover ratio=Average accounts payable/Daily cost of sales=1175/97=12

Average accounts payable=2350/2=1175

Daily cost of sales=2920/30=97.33

Net profit margin denotes how much revenue is converted in profit. It is denoted in percentage

form. Net profit can also be called net income statement for the company. It denotes how well a

company is containing its operational costs and able to generate profit from sales. The net profit

margin is an important indicator of company's financial health. By tracking it a company is able

to assess whether current practices of the company are moving in the right direction. Company

can also forecast its future growth (Rodrigues and Rodrigues, 2018).

Investors see it as a prominent factor considering profits of the previous few years to see

the growth of the company. They assess by the ratio how well the company has been controlling

its operational costs and whether it can pay timely dividends.

Here the company's profit margin is around 10% which is very less compared to the

competitors. Company will have to lessen its operation costs and increase revenue. Being a new

business, it is acceptable that it will take time for the company to generate profits.

Gross profit margin is expressed as a percentage of sales. It is basically the amount of profit

made before deduction of selling, general and administrative costs. It tells about the quality of

Here Linda must treat her withdrawal from business bank account during Florida Travel as

drawing made by her out her business capital account which will reduce her capital balance by

that amount.

Part B

Net profit margin=Net income/Revenue*100=400/3900*100=10.25

Gross profit margin=Revenue-Cost of goods sold/Revenue*100=3900-2920/3900*100=25.12

Current ratio=Current Assets/Current Liabilities=10850/2350=4.61

Quick ratio=Current assets-Inventory/Current Liabilities=10850-250/2350=4.51

Accounts receivable collection period=Average accounts receivable/Net credit

sales*365=100/400*365=91 days

As,Average accounts receivable=0+400/2=100

Net credit sales=1900-1500=400

Accounts payable payment period=365/Payable turnover ratio=365/12=30 days

As,Payable turnover ratio=Average accounts payable/Daily cost of sales=1175/97=12

Average accounts payable=2350/2=1175

Daily cost of sales=2920/30=97.33

Net profit margin denotes how much revenue is converted in profit. It is denoted in percentage

form. Net profit can also be called net income statement for the company. It denotes how well a

company is containing its operational costs and able to generate profit from sales. The net profit

margin is an important indicator of company's financial health. By tracking it a company is able

to assess whether current practices of the company are moving in the right direction. Company

can also forecast its future growth (Rodrigues and Rodrigues, 2018).

Investors see it as a prominent factor considering profits of the previous few years to see

the growth of the company. They assess by the ratio how well the company has been controlling

its operational costs and whether it can pay timely dividends.

Here the company's profit margin is around 10% which is very less compared to the

competitors. Company will have to lessen its operation costs and increase revenue. Being a new

business, it is acceptable that it will take time for the company to generate profits.

Gross profit margin is expressed as a percentage of sales. It is basically the amount of profit

made before deduction of selling, general and administrative costs. It tells about the quality of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

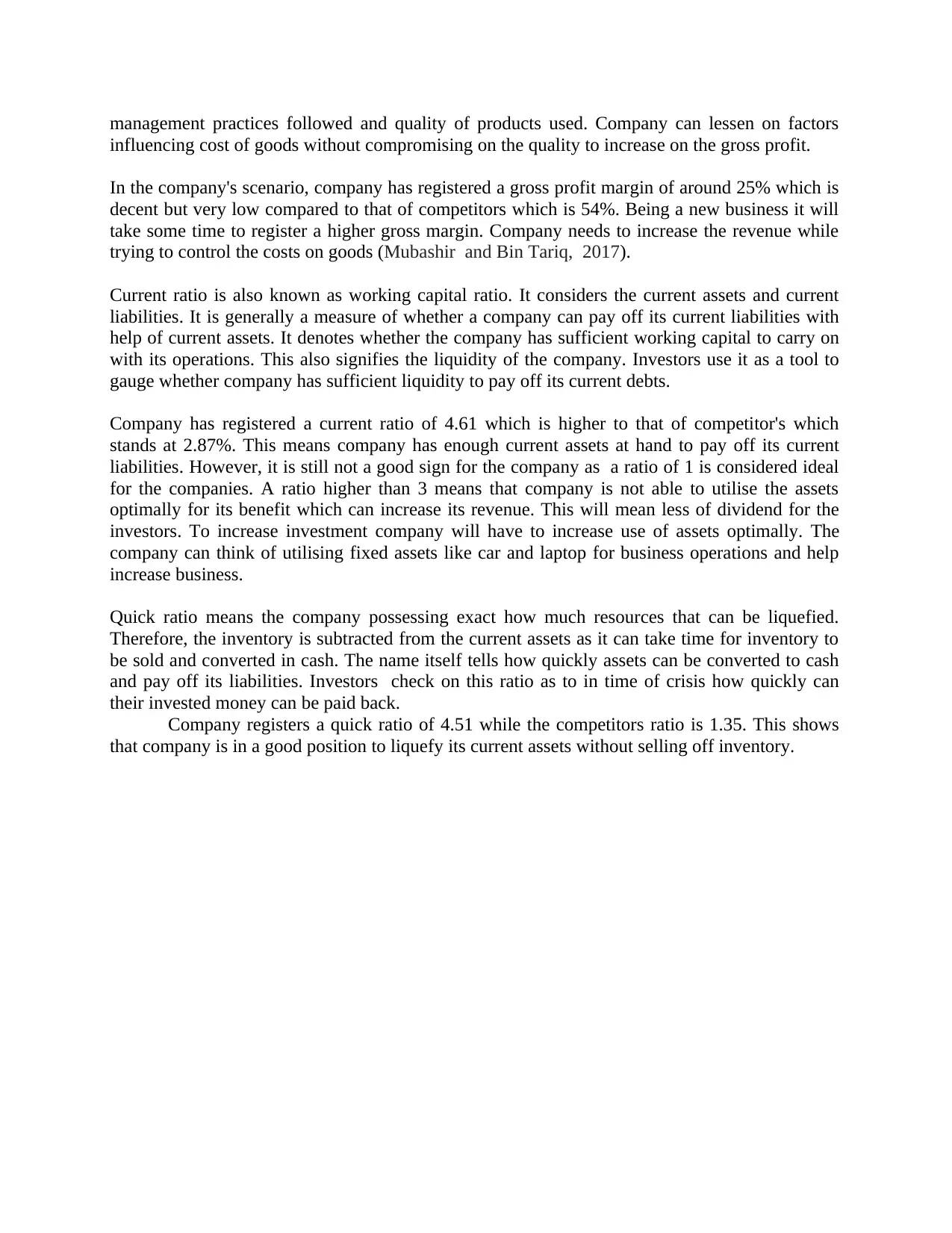

management practices followed and quality of products used. Company can lessen on factors

influencing cost of goods without compromising on the quality to increase on the gross profit.

In the company's scenario, company has registered a gross profit margin of around 25% which is

decent but very low compared to that of competitors which is 54%. Being a new business it will

take some time to register a higher gross margin. Company needs to increase the revenue while

trying to control the costs on goods (Mubashir and Bin Tariq, 2017).

Current ratio is also known as working capital ratio. It considers the current assets and current

liabilities. It is generally a measure of whether a company can pay off its current liabilities with

help of current assets. It denotes whether the company has sufficient working capital to carry on

with its operations. This also signifies the liquidity of the company. Investors use it as a tool to

gauge whether company has sufficient liquidity to pay off its current debts.

Company has registered a current ratio of 4.61 which is higher to that of competitor's which

stands at 2.87%. This means company has enough current assets at hand to pay off its current

liabilities. However, it is still not a good sign for the company as a ratio of 1 is considered ideal

for the companies. A ratio higher than 3 means that company is not able to utilise the assets

optimally for its benefit which can increase its revenue. This will mean less of dividend for the

investors. To increase investment company will have to increase use of assets optimally. The

company can think of utilising fixed assets like car and laptop for business operations and help

increase business.

Quick ratio means the company possessing exact how much resources that can be liquefied.

Therefore, the inventory is subtracted from the current assets as it can take time for inventory to

be sold and converted in cash. The name itself tells how quickly assets can be converted to cash

and pay off its liabilities. Investors check on this ratio as to in time of crisis how quickly can

their invested money can be paid back.

Company registers a quick ratio of 4.51 while the competitors ratio is 1.35. This shows

that company is in a good position to liquefy its current assets without selling off inventory.

influencing cost of goods without compromising on the quality to increase on the gross profit.

In the company's scenario, company has registered a gross profit margin of around 25% which is

decent but very low compared to that of competitors which is 54%. Being a new business it will

take some time to register a higher gross margin. Company needs to increase the revenue while

trying to control the costs on goods (Mubashir and Bin Tariq, 2017).

Current ratio is also known as working capital ratio. It considers the current assets and current

liabilities. It is generally a measure of whether a company can pay off its current liabilities with

help of current assets. It denotes whether the company has sufficient working capital to carry on

with its operations. This also signifies the liquidity of the company. Investors use it as a tool to

gauge whether company has sufficient liquidity to pay off its current debts.

Company has registered a current ratio of 4.61 which is higher to that of competitor's which

stands at 2.87%. This means company has enough current assets at hand to pay off its current

liabilities. However, it is still not a good sign for the company as a ratio of 1 is considered ideal

for the companies. A ratio higher than 3 means that company is not able to utilise the assets

optimally for its benefit which can increase its revenue. This will mean less of dividend for the

investors. To increase investment company will have to increase use of assets optimally. The

company can think of utilising fixed assets like car and laptop for business operations and help

increase business.

Quick ratio means the company possessing exact how much resources that can be liquefied.

Therefore, the inventory is subtracted from the current assets as it can take time for inventory to

be sold and converted in cash. The name itself tells how quickly assets can be converted to cash

and pay off its liabilities. Investors check on this ratio as to in time of crisis how quickly can

their invested money can be paid back.

Company registers a quick ratio of 4.51 while the competitors ratio is 1.35. This shows

that company is in a good position to liquefy its current assets without selling off inventory.

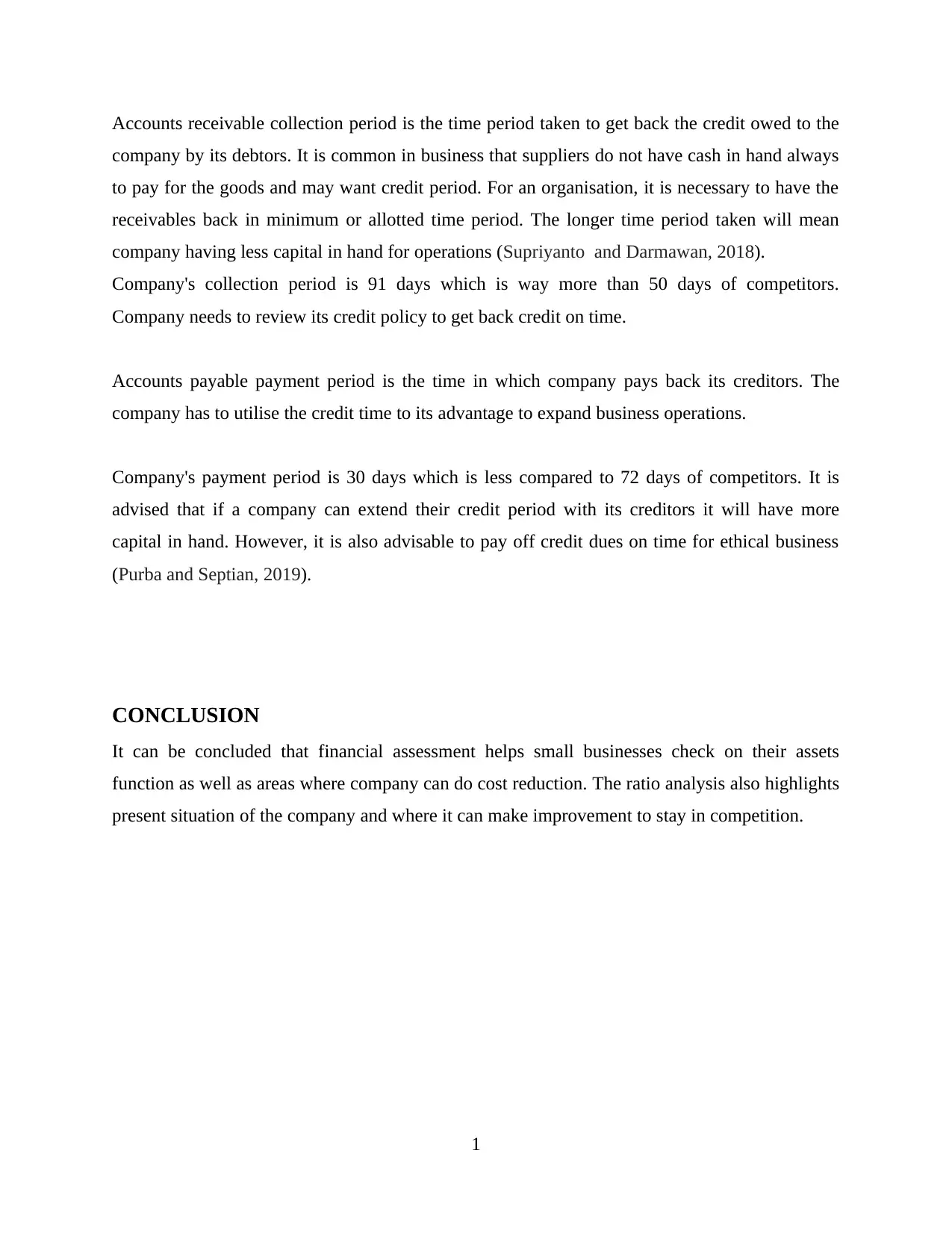

Accounts receivable collection period is the time period taken to get back the credit owed to the

company by its debtors. It is common in business that suppliers do not have cash in hand always

to pay for the goods and may want credit period. For an organisation, it is necessary to have the

receivables back in minimum or allotted time period. The longer time period taken will mean

company having less capital in hand for operations (Supriyanto and Darmawan, 2018).

Company's collection period is 91 days which is way more than 50 days of competitors.

Company needs to review its credit policy to get back credit on time.

Accounts payable payment period is the time in which company pays back its creditors. The

company has to utilise the credit time to its advantage to expand business operations.

Company's payment period is 30 days which is less compared to 72 days of competitors. It is

advised that if a company can extend their credit period with its creditors it will have more

capital in hand. However, it is also advisable to pay off credit dues on time for ethical business

(Purba and Septian, 2019).

CONCLUSION

It can be concluded that financial assessment helps small businesses check on their assets

function as well as areas where company can do cost reduction. The ratio analysis also highlights

present situation of the company and where it can make improvement to stay in competition.

1

company by its debtors. It is common in business that suppliers do not have cash in hand always

to pay for the goods and may want credit period. For an organisation, it is necessary to have the

receivables back in minimum or allotted time period. The longer time period taken will mean

company having less capital in hand for operations (Supriyanto and Darmawan, 2018).

Company's collection period is 91 days which is way more than 50 days of competitors.

Company needs to review its credit policy to get back credit on time.

Accounts payable payment period is the time in which company pays back its creditors. The

company has to utilise the credit time to its advantage to expand business operations.

Company's payment period is 30 days which is less compared to 72 days of competitors. It is

advised that if a company can extend their credit period with its creditors it will have more

capital in hand. However, it is also advisable to pay off credit dues on time for ethical business

(Purba and Septian, 2019).

CONCLUSION

It can be concluded that financial assessment helps small businesses check on their assets

function as well as areas where company can do cost reduction. The ratio analysis also highlights

present situation of the company and where it can make improvement to stay in competition.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.