Recording Business Transactions: Journal, Ledger, and Financials

VerifiedAdded on 2022/12/27

|14

|1809

|26

Homework Assignment

AI Summary

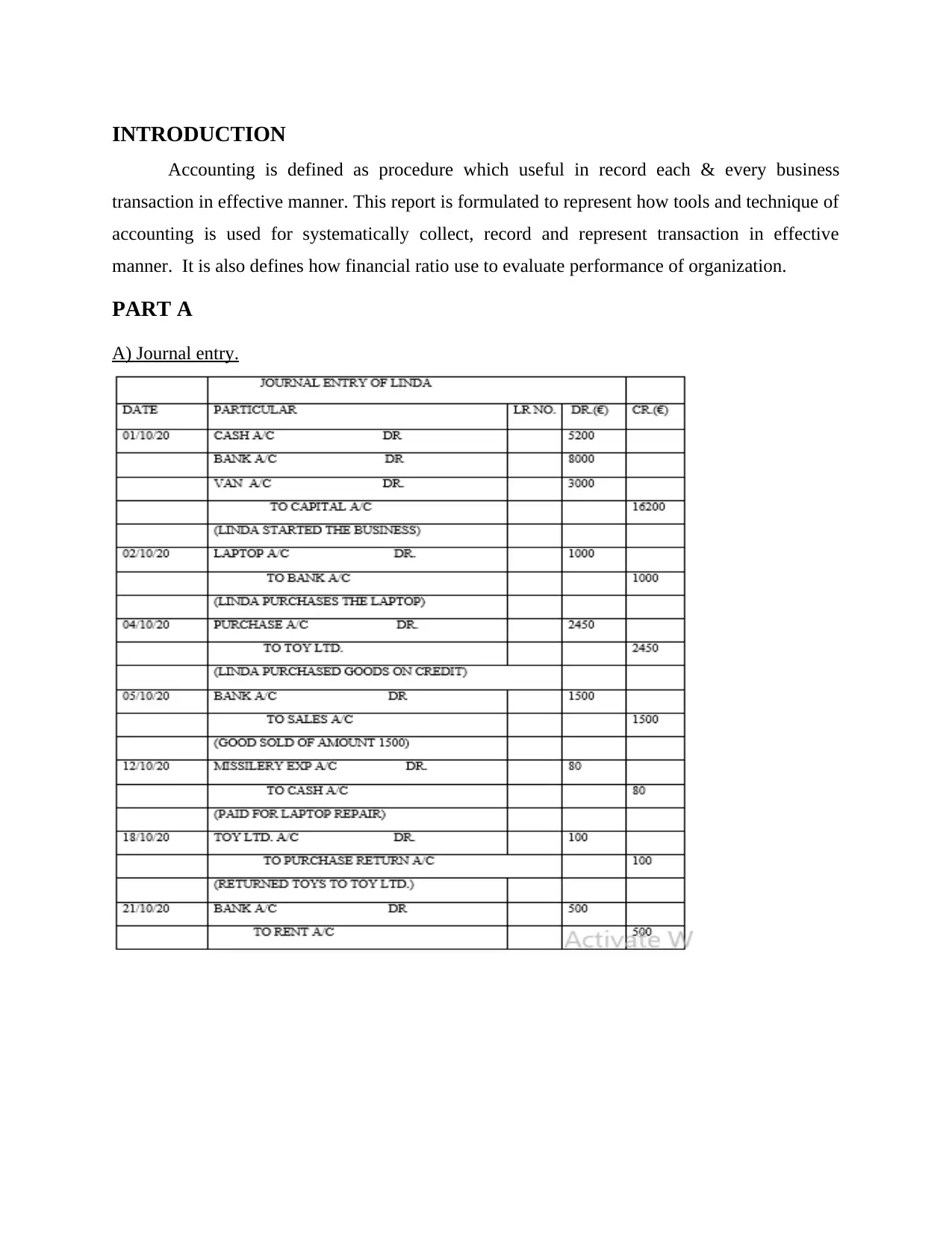

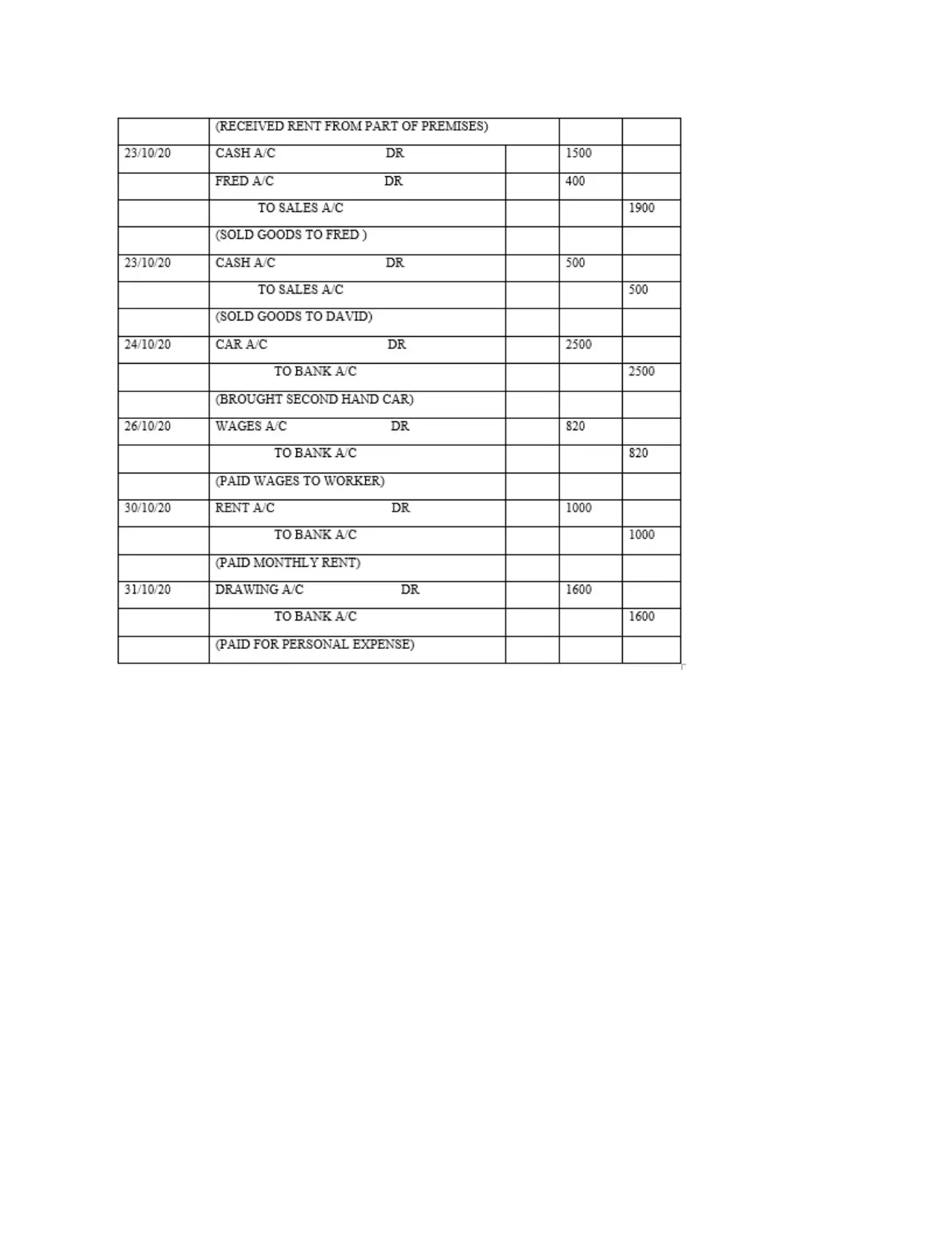

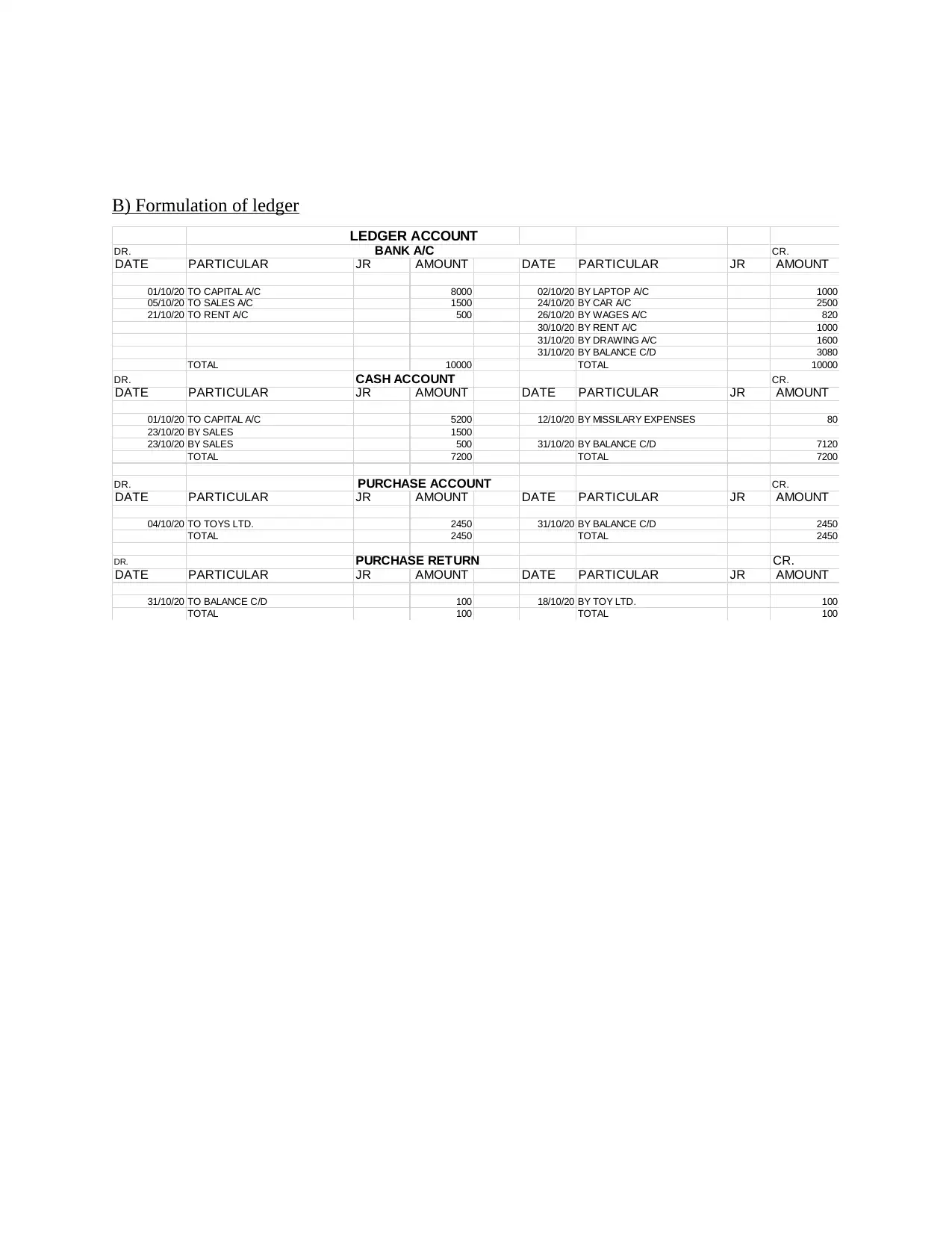

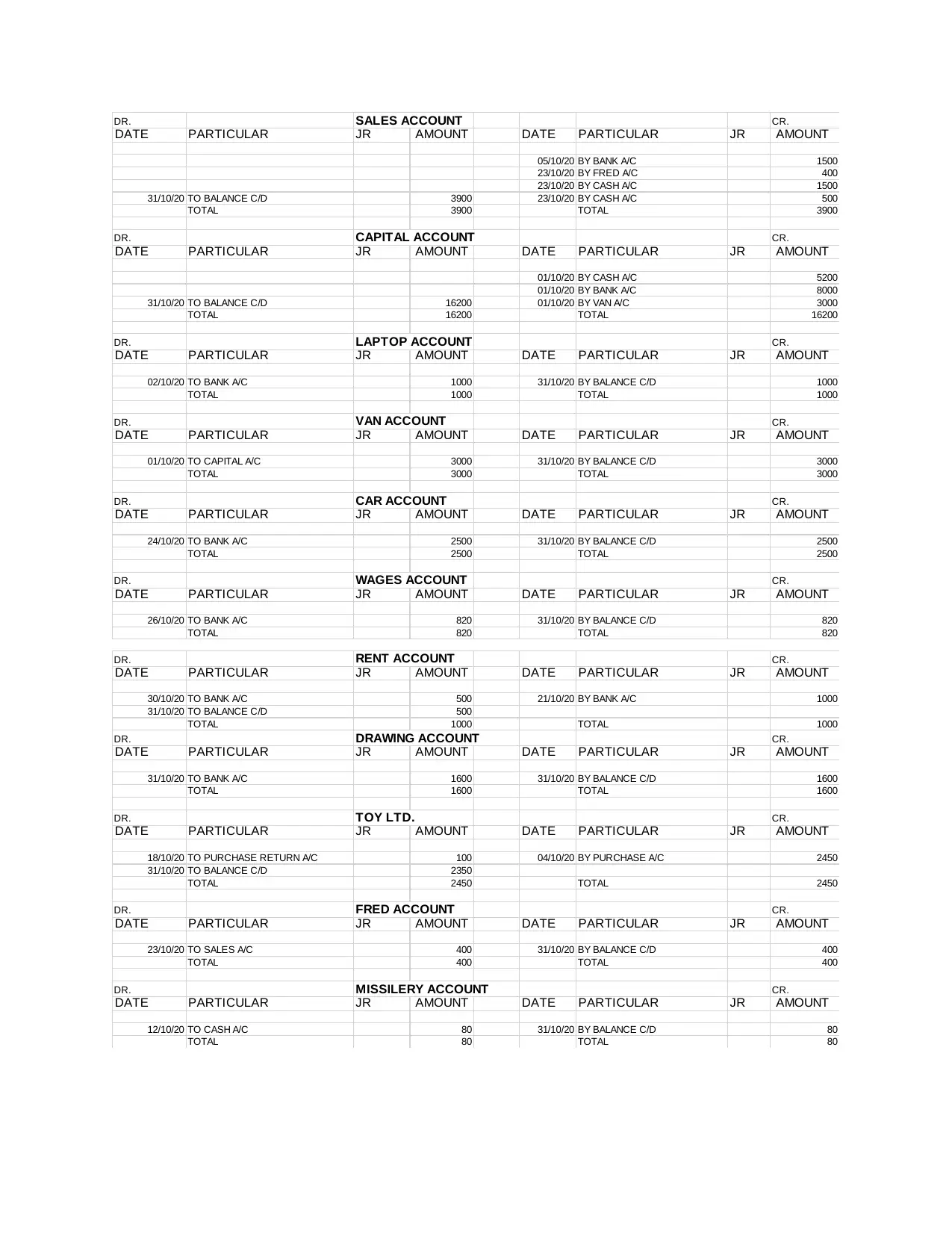

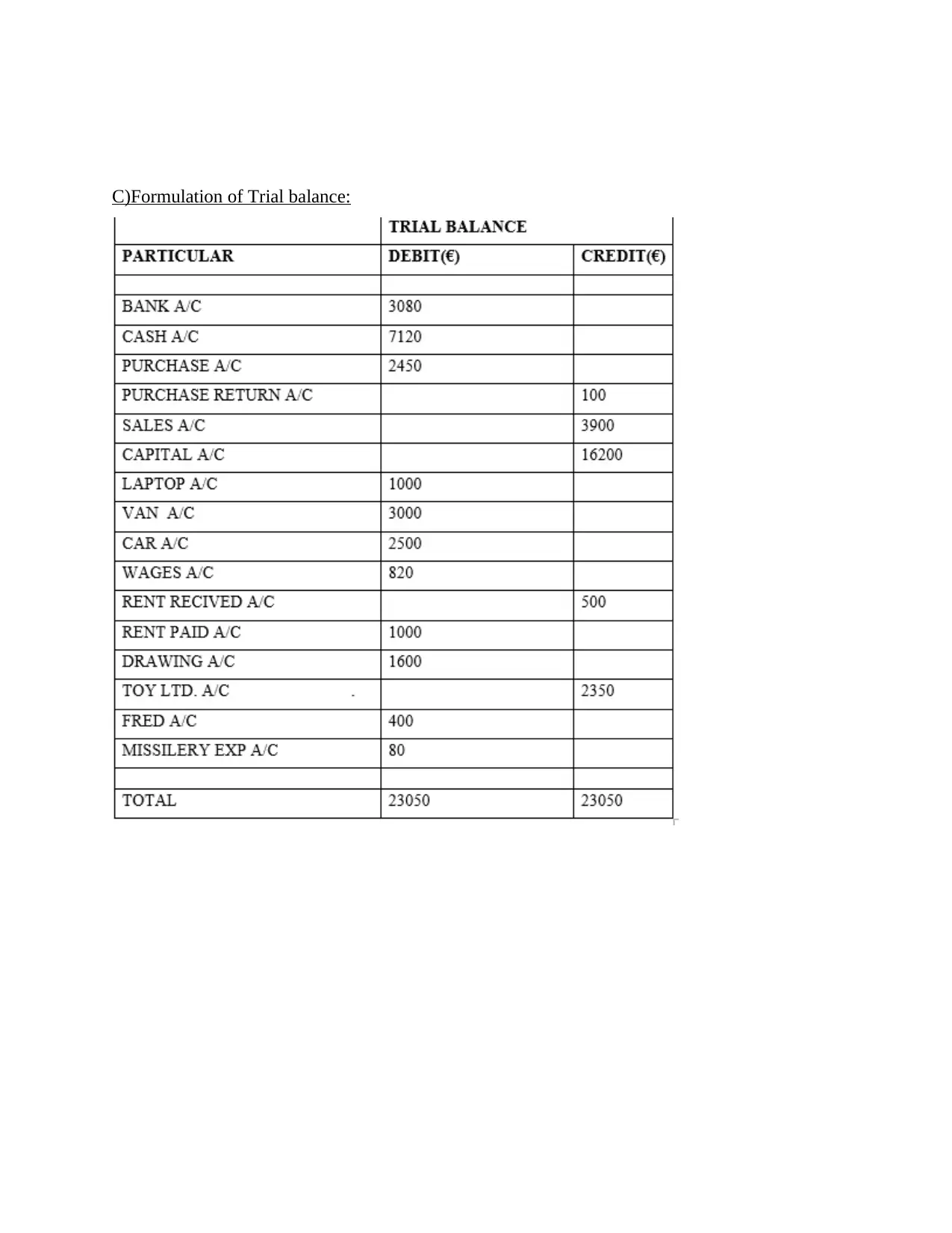

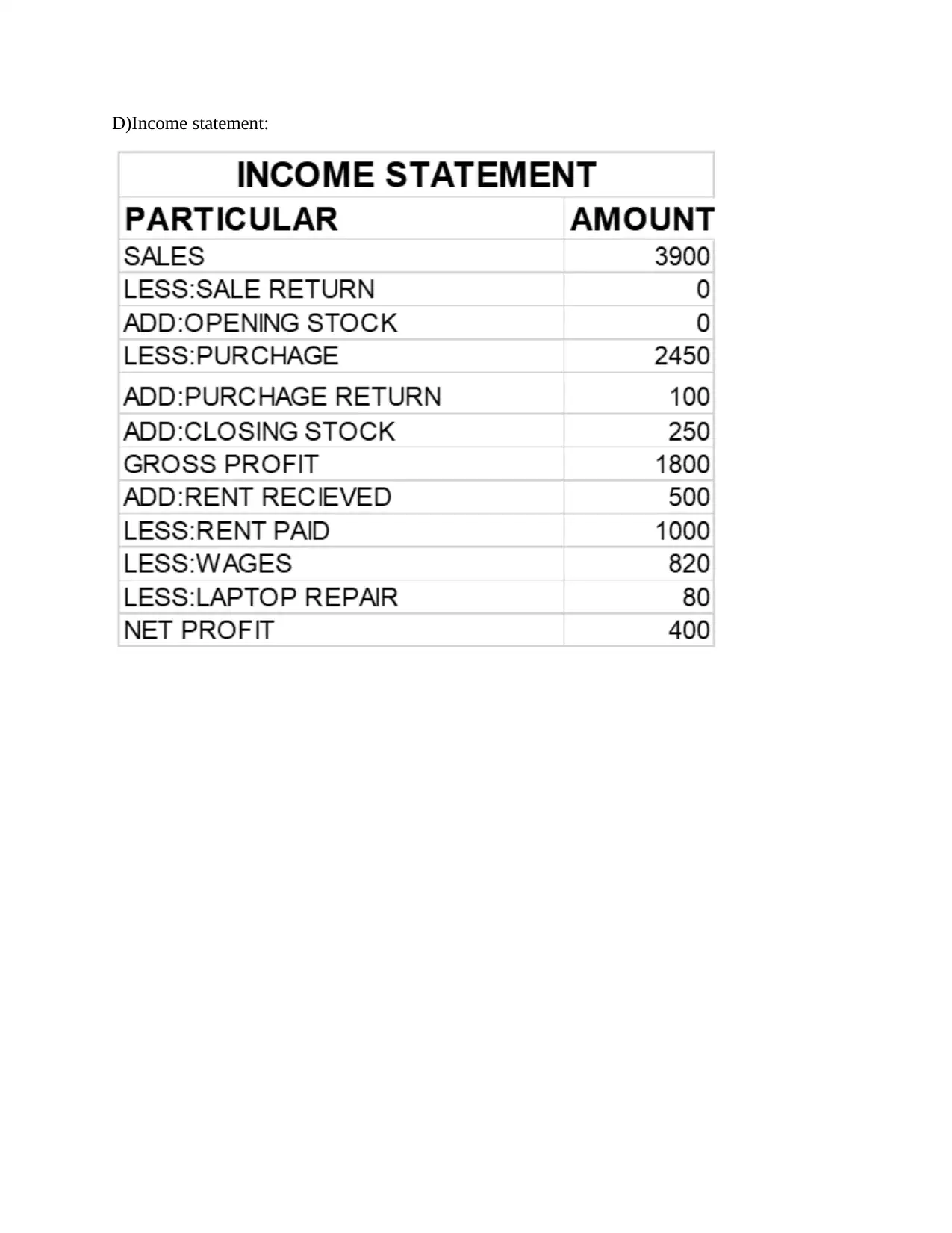

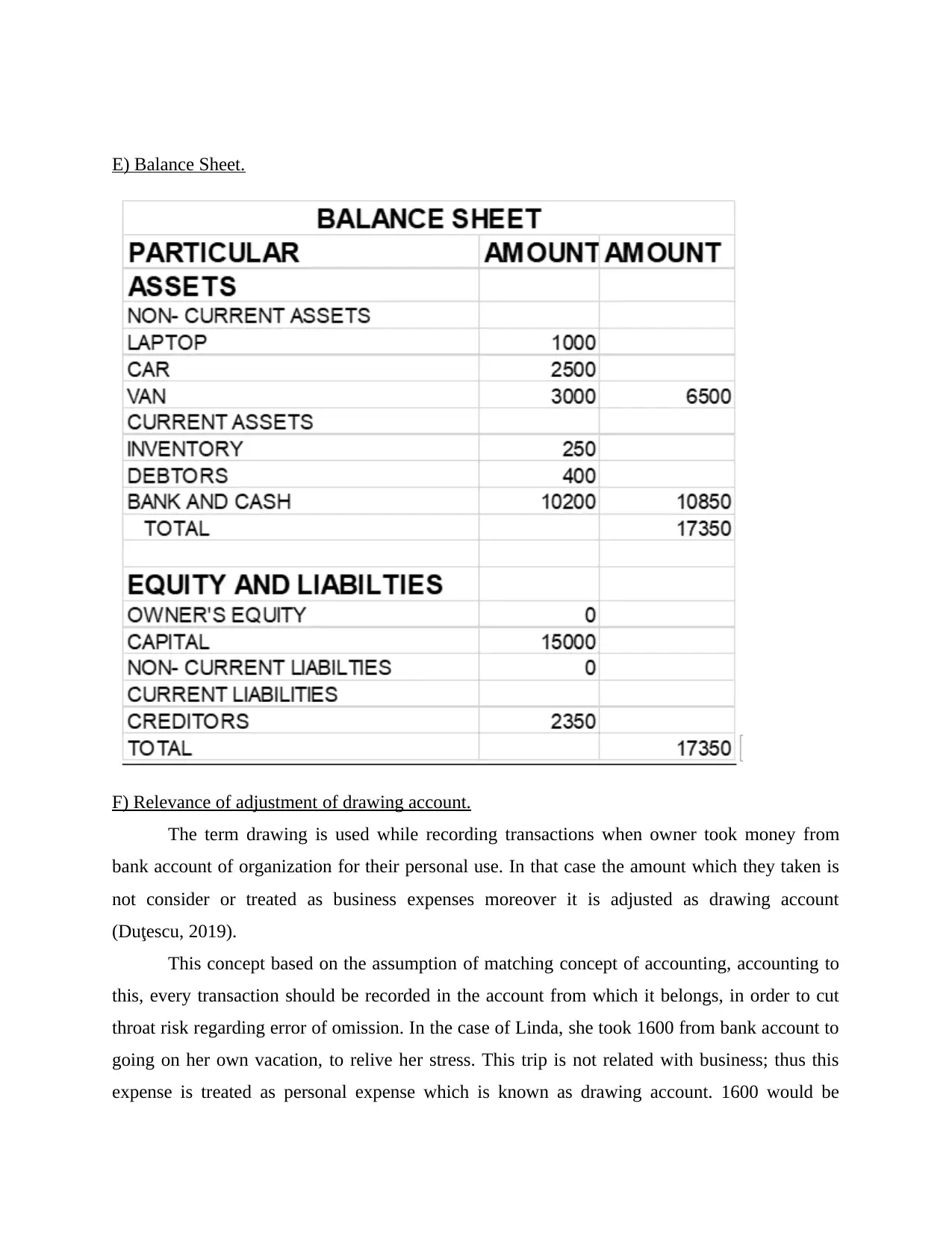

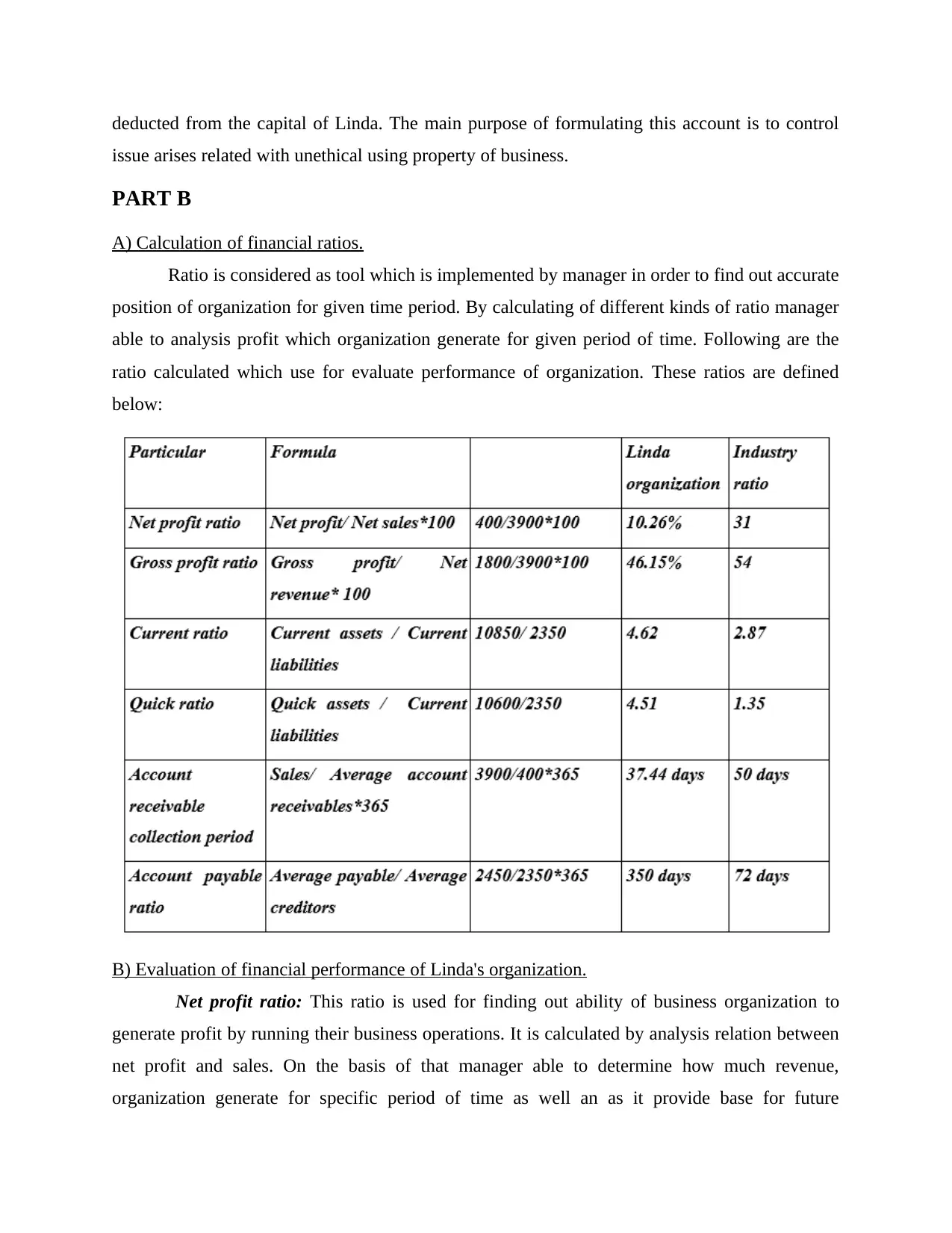

This assignment solution details the process of recording business transactions for Linda's toy business, starting from initial investments to the end-of-month financial statements. It includes the creation of journal entries, ledger accounts, and a trial balance to systematically record transactions. The solution then presents an income statement and balance sheet to assess the business's financial position. Furthermore, the assignment addresses the relevance of adjusting the drawing account, emphasizing that personal expenses are not business expenses. Part B involves calculating and evaluating various financial ratios, such as net profit ratio, gross profit ratio, current ratio, quick ratio, accounts receivable collection period, and accounts payable ratio, to assess Linda's organization's financial performance. The analysis reveals insights into the company's profitability, liquidity, and efficiency, comparing it to industry benchmarks and providing recommendations for improvement. The conclusion summarizes the importance of accounting tools for effective financial reporting and decision-making.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.