Recording Business Transactions: UWL BA30592E Assignment

VerifiedAdded on 2022/12/27

|17

|2493

|56

Homework Assignment

AI Summary

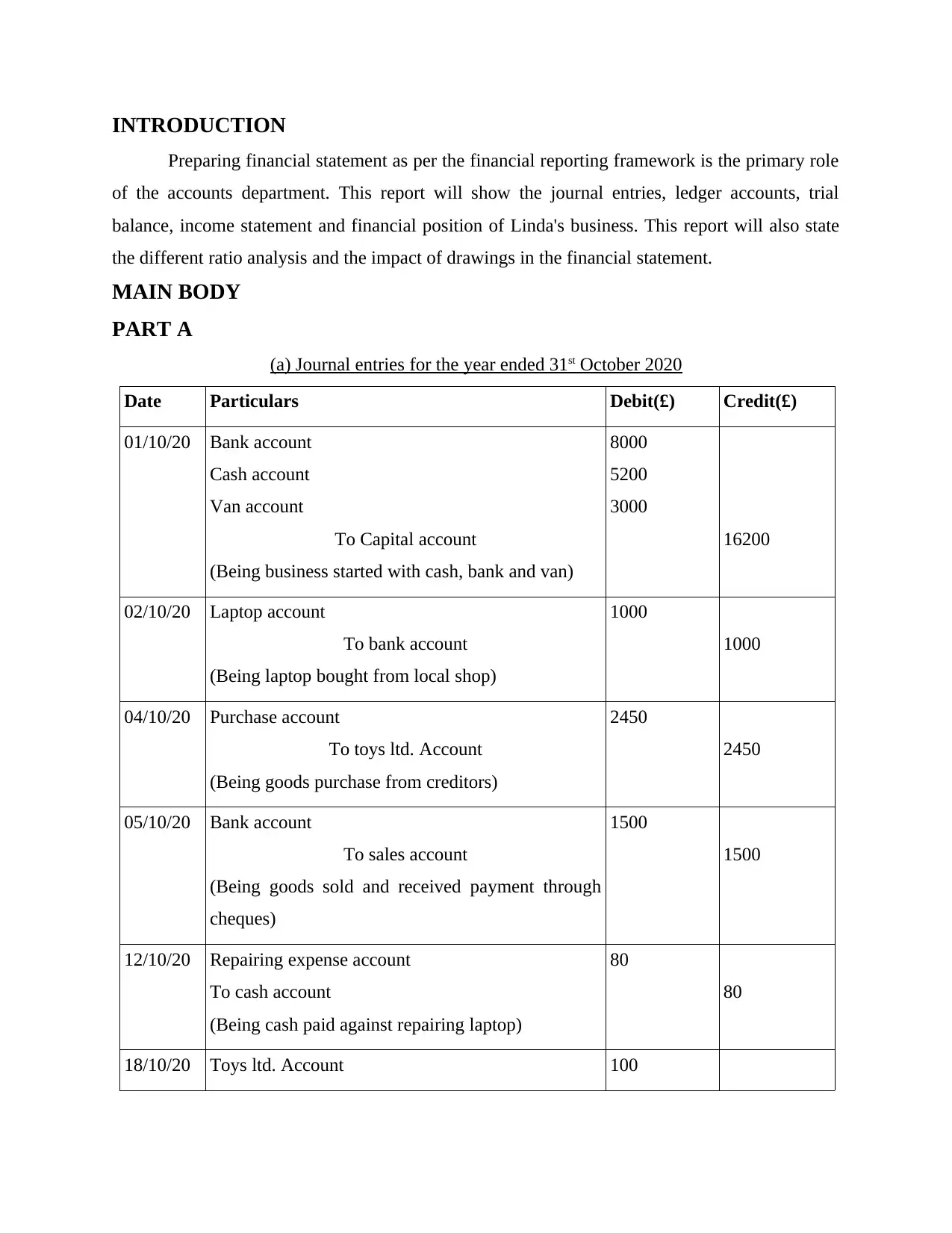

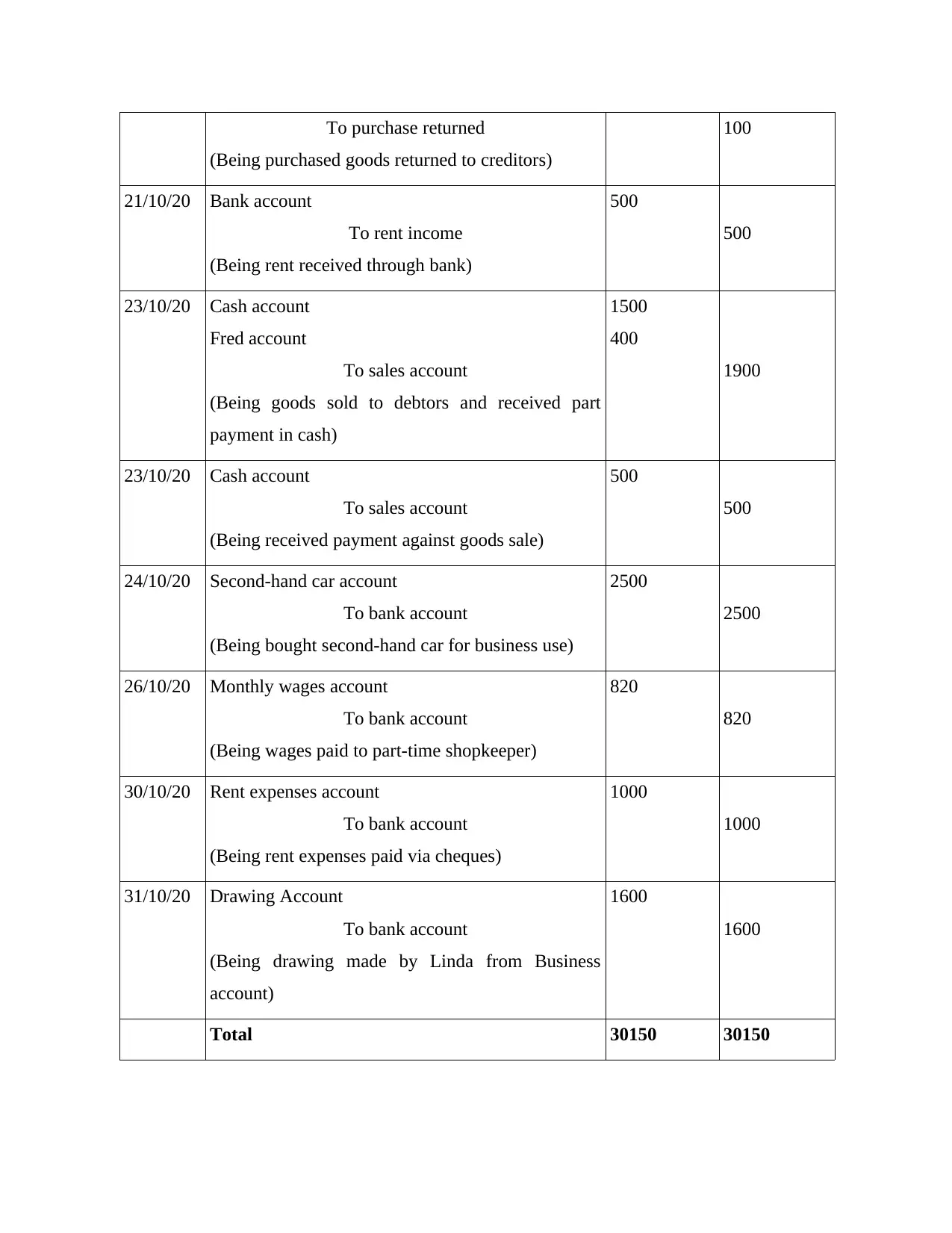

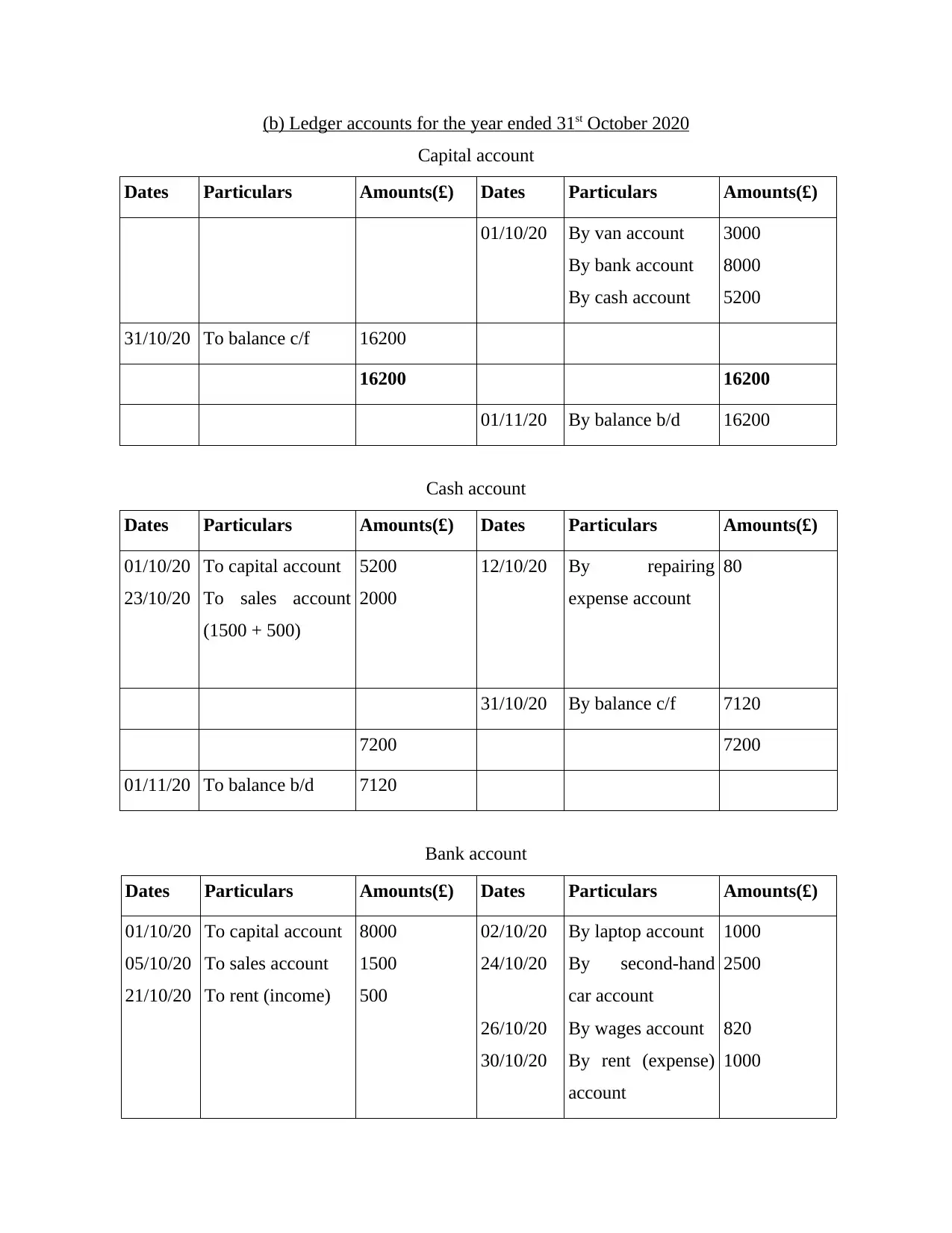

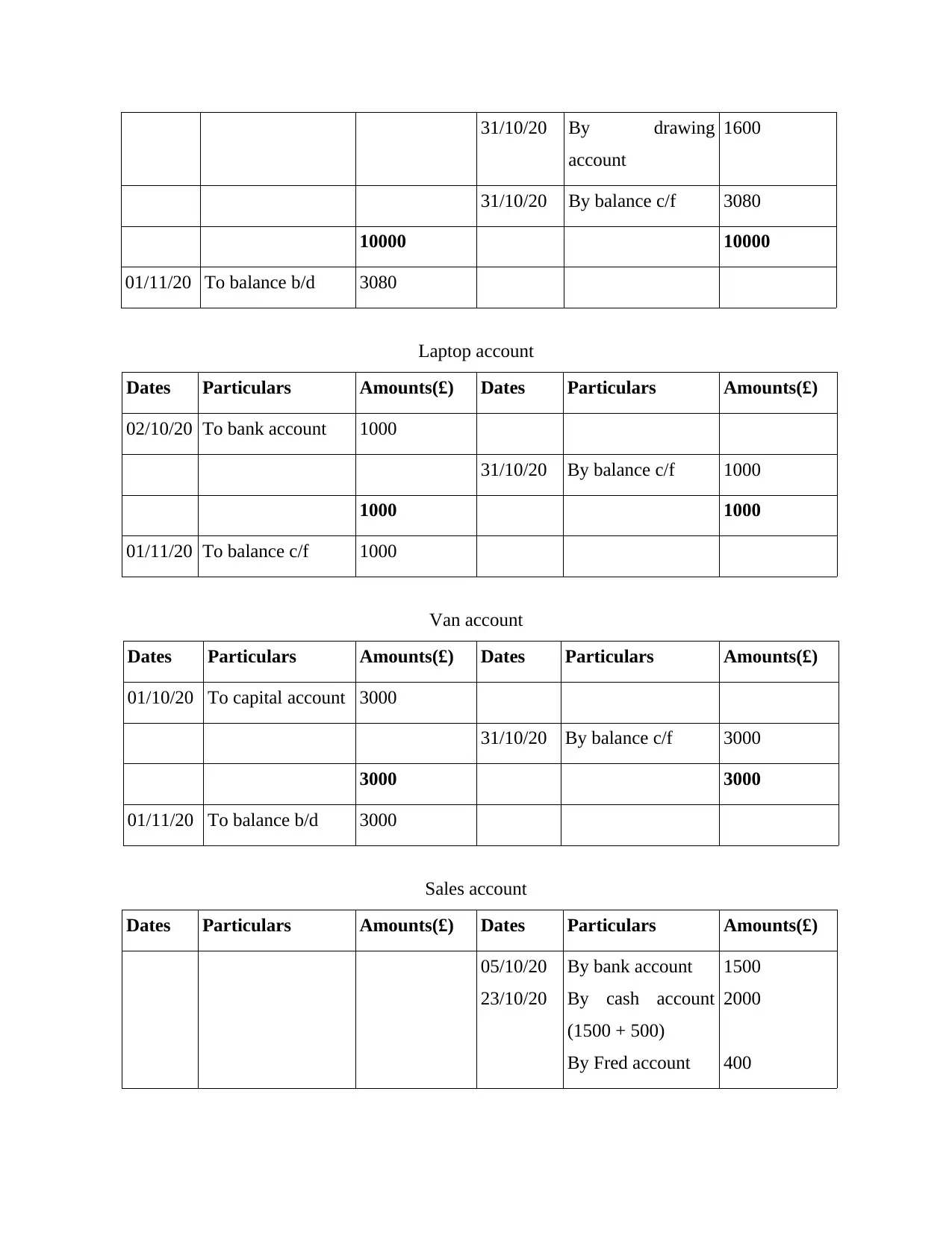

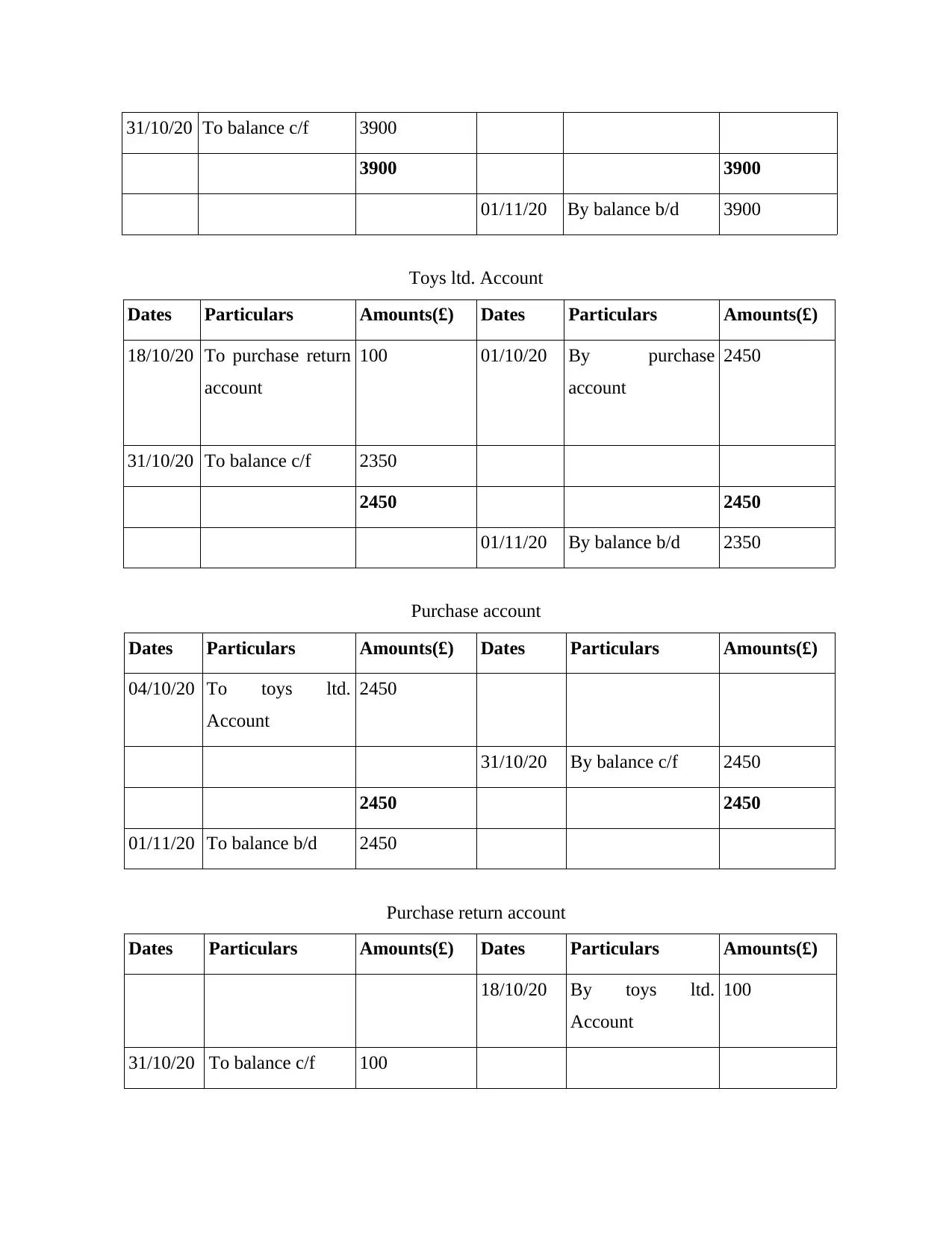

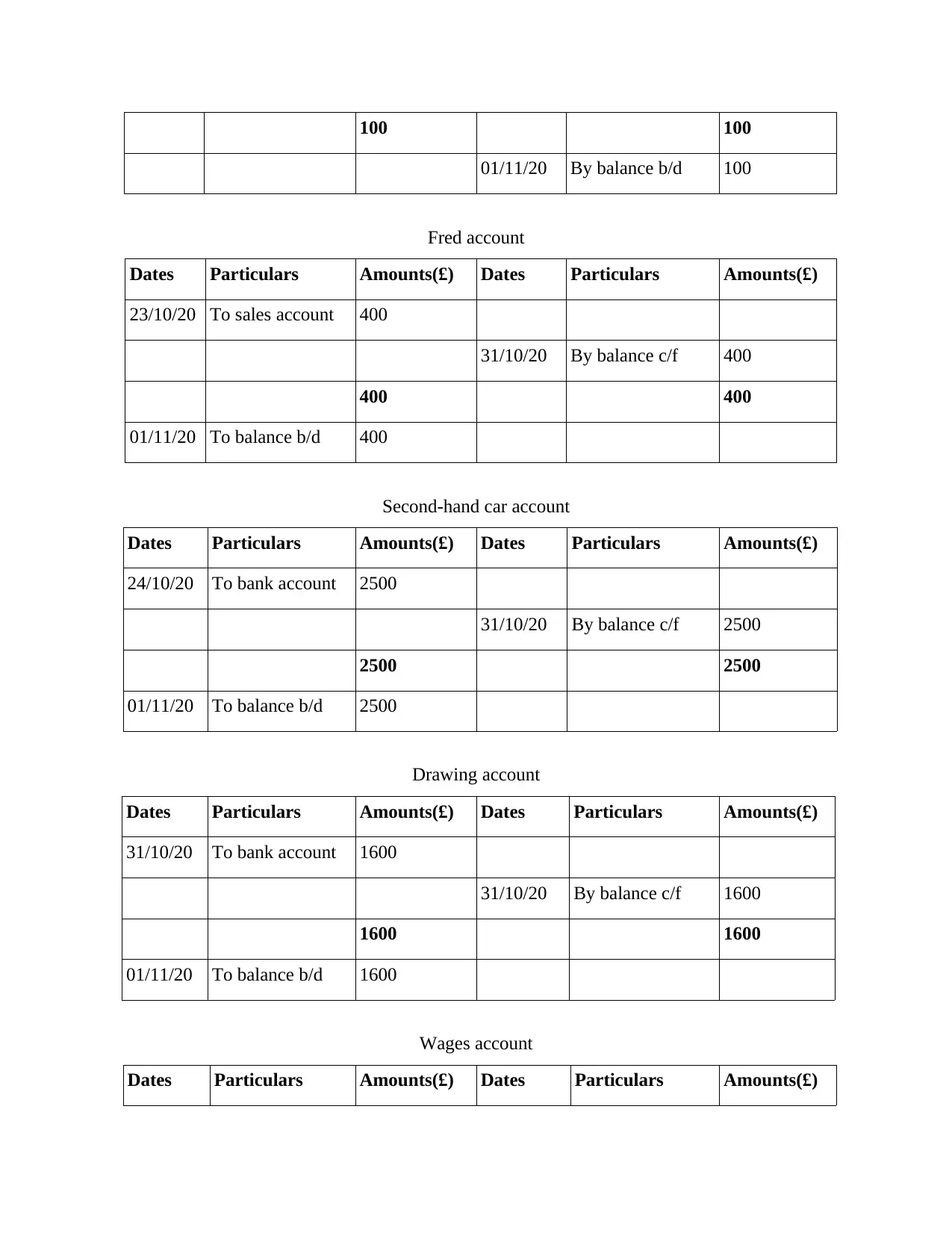

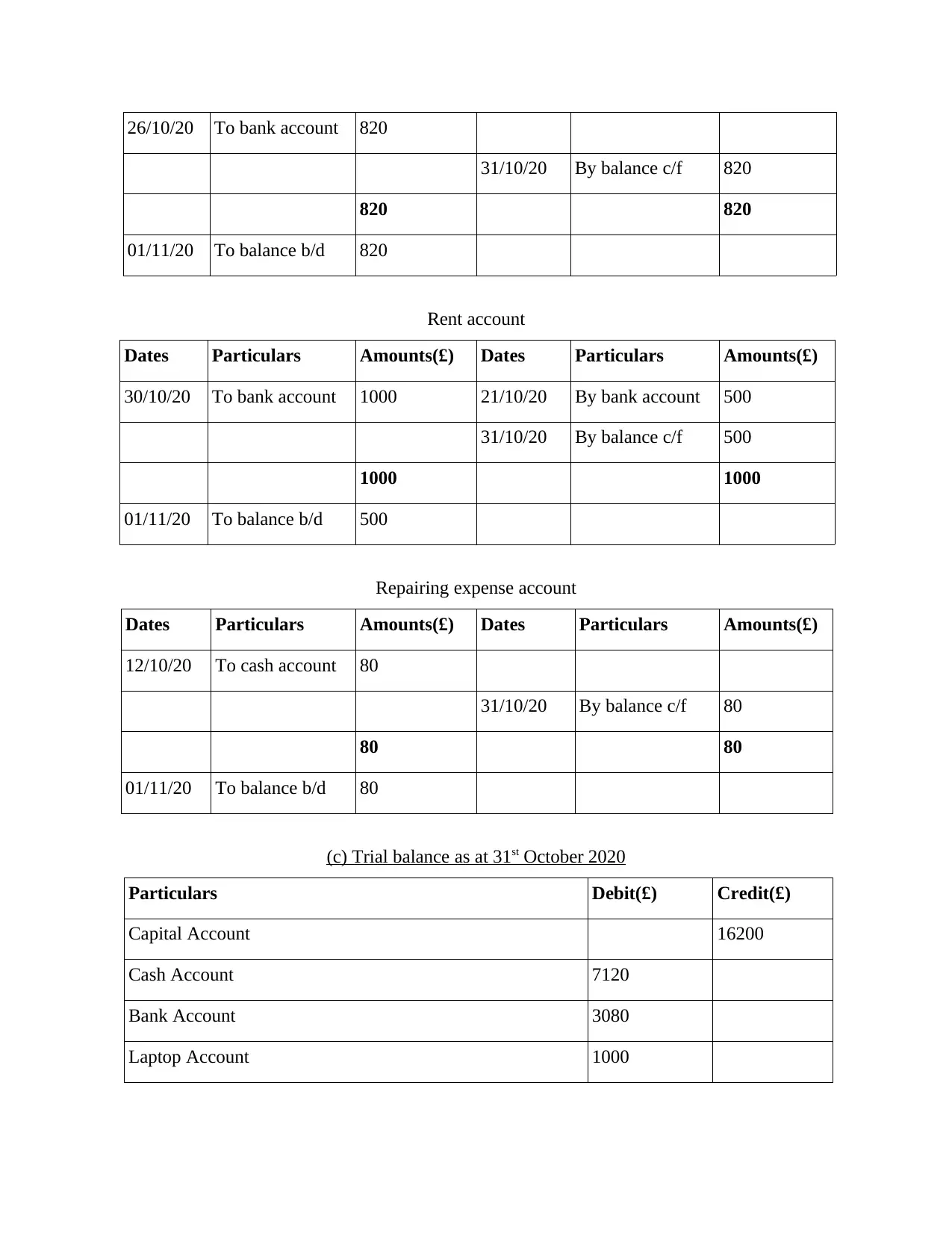

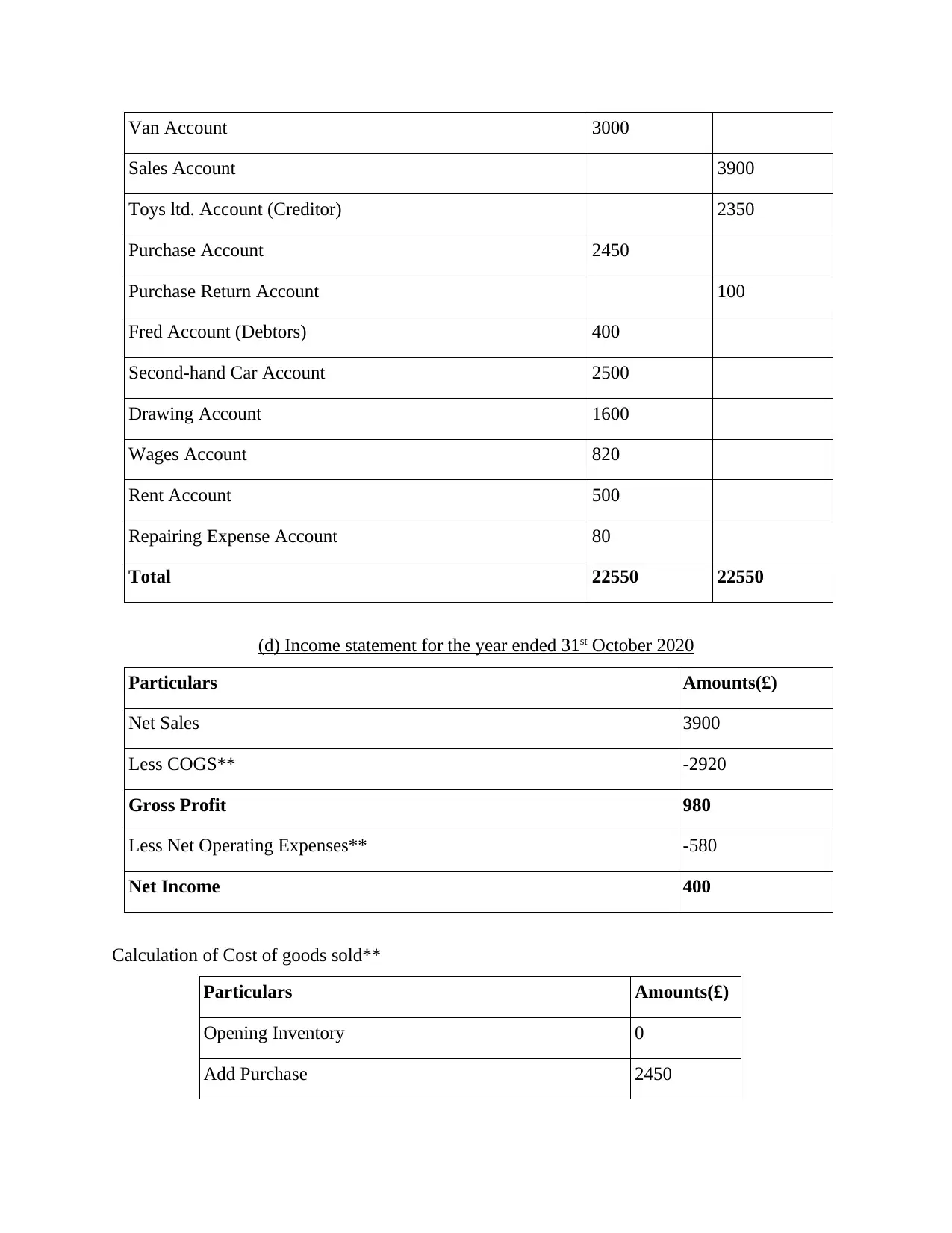

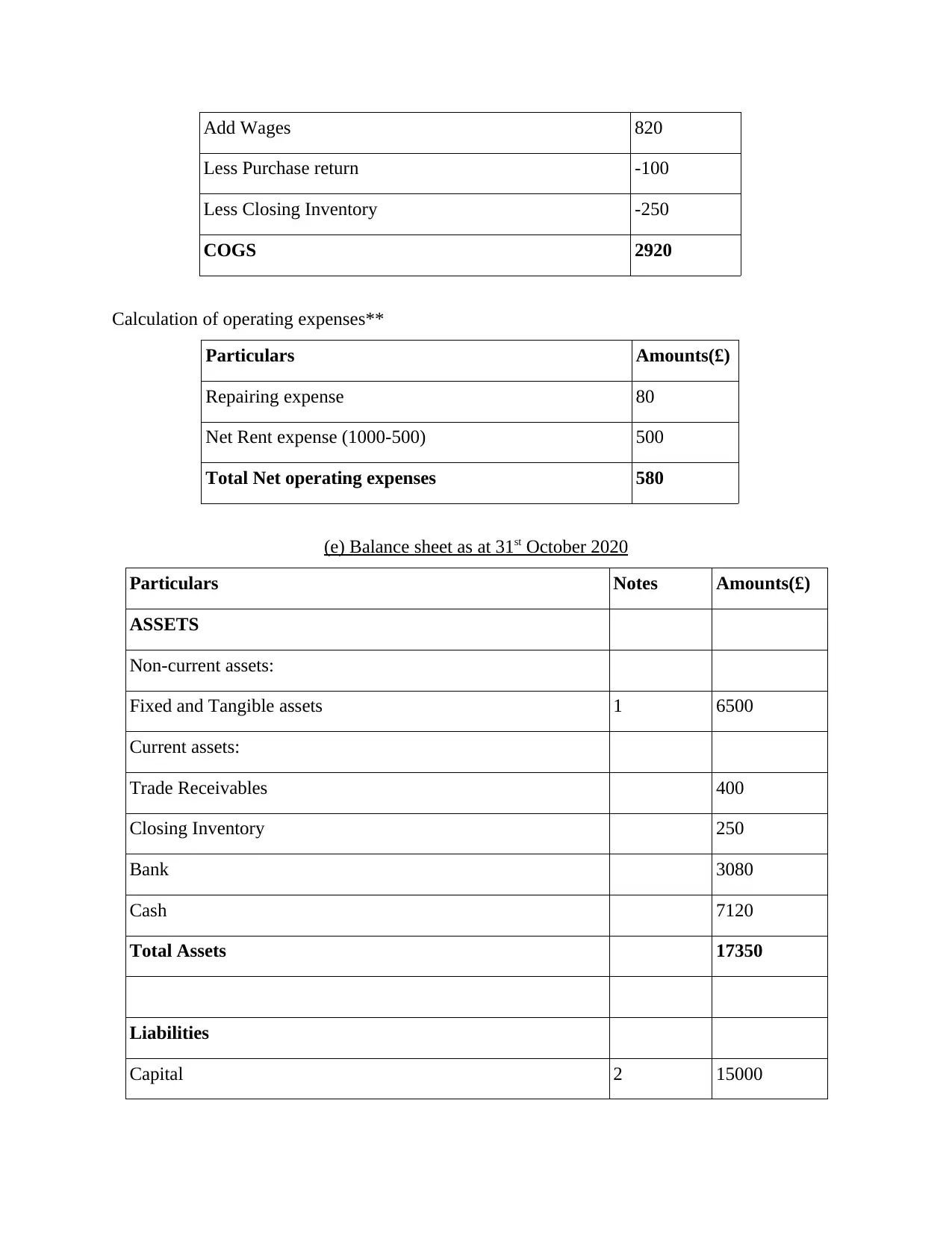

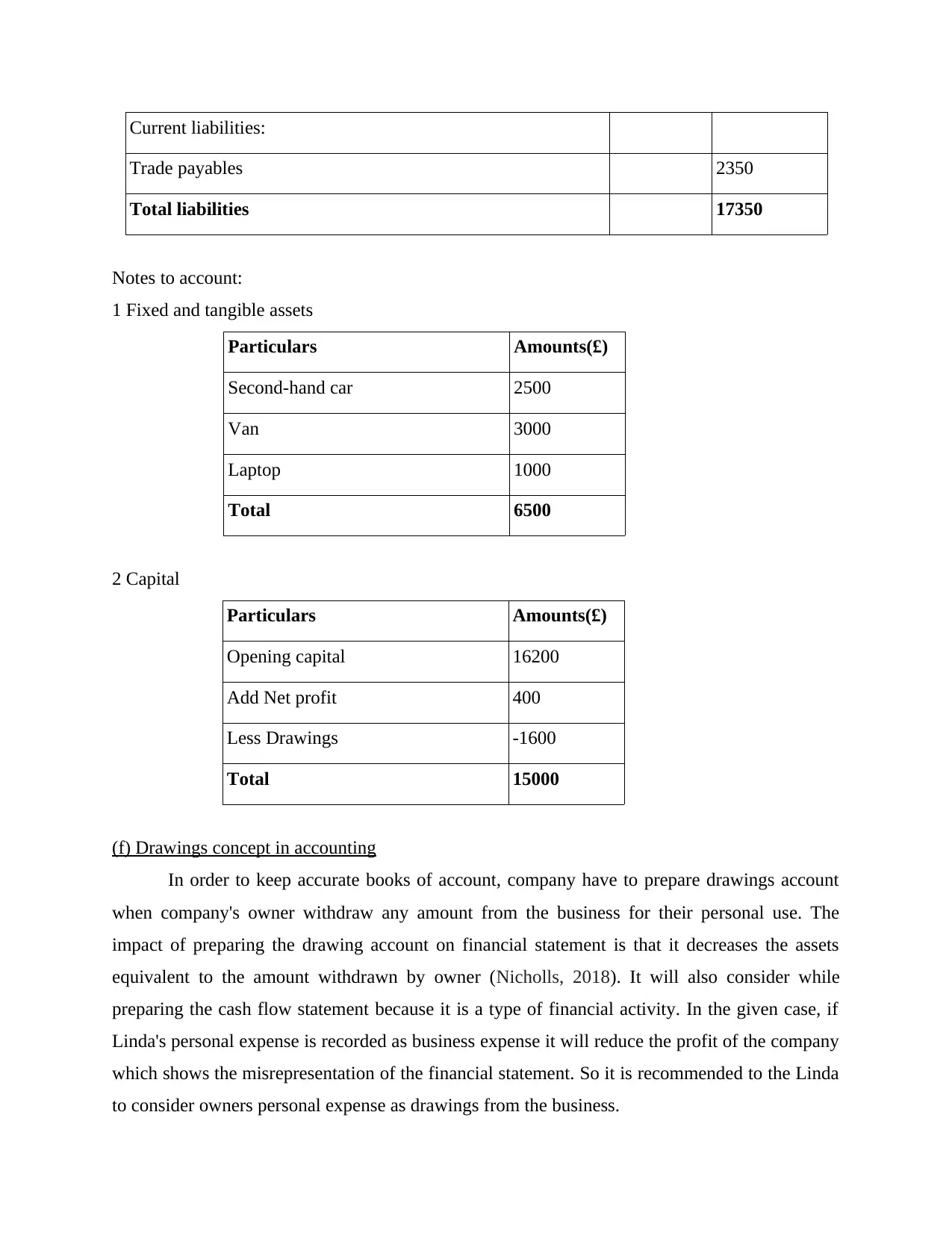

This assignment solution from a University of West London student focuses on recording business transactions for a toy business. It includes journal entries, ledger accounts, a trial balance, an income statement, and a balance sheet for the month of October 2020. The solution details the initial capital contribution, followed by transactions involving purchases, sales, expenses, and drawings. Part A presents the financial statements, while Part B delves into ratio analysis, comparing Linda's performance with competitors. The analysis covers profitability, liquidity, and efficiency ratios, offering insights into the business's financial health and recommendations for improvement. The assignment concludes with a discussion on the impact of drawings and a summary of the findings, referencing relevant accounting principles and literature.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.