Analysis of Business Transactions, Decision Makers, and Accounting

VerifiedAdded on 2023/01/03

|15

|4216

|41

Homework Assignment

AI Summary

This assignment delves into the realm of financial accounting, focusing on recording and analyzing business transactions, and the crucial role of decision-makers. It examines the importance of accounting information for stakeholders like shareholders, CEOs, and board directors, highlighting how financial data influences their decisions. The assignment explores different business structures, including sole traders and partnerships, outlining their advantages and disadvantages from an accounting perspective. Furthermore, it touches upon the impact of accounting records on decision-making within companies like McDonald's and KFC. The assignment also requires an analysis of financial statements, particularly the income statement, identifying potential overspending issues and suggesting improvements. The analysis also includes the importance of financial data for BT, British Telecom, and how they use accounting information to make business decisions. The assignment provides a comprehensive overview of financial accounting principles and their practical application in various business contexts.

Student Name:

Unit Title: Recording Business Transaction

Table of Content

Unit Title: Recording Business Transaction

Table of Content

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Accounting refers to a process that includes recording, classification, analysis and

summarising of financial transaction of an individual within business unit and this is only

carried out with the help of accounting. Basically, accounting is a language of finance. Which

aids company to convert the working of a firm into tangible reports that can be differentiated.

All these records and reports is made in that form that aids in evaluation of financial

performance along with position of company (Neeraj and et.al., 2017). In which the present

assignment consist question that includes financial transaction of various company and need

to generate trail balance, along with income statement from that records. Further the benefits

and disadvantages in context of commercial business is discussed. Lastly the impact of

covid-19 on productivity and profitability of company is analysed.

Assessment 1: Part 1.

a)

Decision makers: All the individuals who are responsible for formulation of decisions

for a business are known as decision makers. For all the firms it is very important to make

sure that they are able to maintain interest of all of them so that the long term decisions

could be formulated. There are various types of decisions markers for the entities.

Discussion of all of them is as follows:

Shareholders: All the individuals or institutions which are legally owning specific

shares of an entity are known as shareholders. These are also known as members of

corporation (Wang, Lau and Mao, 2019). It is very important for all the businesses to

make sure that they are able to manage shareholders as it can help to carry out all

the operational activities in systematic manner. They are important for company

Accounting refers to a process that includes recording, classification, analysis and

summarising of financial transaction of an individual within business unit and this is only

carried out with the help of accounting. Basically, accounting is a language of finance. Which

aids company to convert the working of a firm into tangible reports that can be differentiated.

All these records and reports is made in that form that aids in evaluation of financial

performance along with position of company (Neeraj and et.al., 2017). In which the present

assignment consist question that includes financial transaction of various company and need

to generate trail balance, along with income statement from that records. Further the benefits

and disadvantages in context of commercial business is discussed. Lastly the impact of

covid-19 on productivity and profitability of company is analysed.

Assessment 1: Part 1.

a)

Decision makers: All the individuals who are responsible for formulation of decisions

for a business are known as decision makers. For all the firms it is very important to make

sure that they are able to maintain interest of all of them so that the long term decisions

could be formulated. There are various types of decisions markers for the entities.

Discussion of all of them is as follows:

Shareholders: All the individuals or institutions which are legally owning specific

shares of an entity are known as shareholders. These are also known as members of

corporation (Wang, Lau and Mao, 2019). It is very important for all the businesses to

make sure that they are able to manage shareholders as it can help to carry out all

the operational activities in systematic manner. They are important for company

because they provide funding to execute all the operations and facilitate the entity to

sustain in the market. If an entity will not be able to manage them then it may result in

issues for business in future.

CEO: A Chief Executive Officer is a person who is the highest ranking executive

within the organisation. The main responsibilities of a CEO include formulation of

corporate decisions, management of resources and operations and communicate

with board of directors and other corporates. For all the businesses CEOs are very

important as they fill the gap of communication between board of directors and other

employees of the organisation. If they will not be managed properly then it may result

in negative impacts upon functionality of business.

Board directors: A group which is responsible for supervising the whole

organisation is known as board of directors. This group is focused to conduct regular

meetings so that policies for executing operations of business could be formulated.

They are very important for businesses because they can facilitate an enterprise to

sustain in the market with the help of effective decision making of them. As they are

elected to represent the shareholders so they share detailed information of

requirements of them so that policies to retain the shareholders could be formulated

(Dolnicar, 2017).

Accounting information is very important for all the decision makers as it can help

them to analyse the actual position of business and then formulate future decisions for

betterment of business. Some of the decisions makers for the entities are CEO,

shareholders and board of directors. All of them need financial information and need of them

regarding the details could be analysed with the help of following discussion:

For all the decision makers accounting information is very important because it can

help them to determine that the business is able to perform all the operational

activities in systematic manner and reach to all the long term business goals.

Financial information is needed by CEO as it can help them to determine that the

business is performing appropriately or not. Apart from this, they can also analyse

that the financial position of the company is appropriate or not as compared to the

competitors.

The need of financial information for Board of Directors is very high because they are

working as the representatives of shareholders and in order to retain them for long

period they need to share proper and detailed information of company’s position. If

they will not be able to get the financial information, then it will be very difficult for

them to provide details of actual status of business to the shareholders (Götzer,

2018).

sustain in the market. If an entity will not be able to manage them then it may result in

issues for business in future.

CEO: A Chief Executive Officer is a person who is the highest ranking executive

within the organisation. The main responsibilities of a CEO include formulation of

corporate decisions, management of resources and operations and communicate

with board of directors and other corporates. For all the businesses CEOs are very

important as they fill the gap of communication between board of directors and other

employees of the organisation. If they will not be managed properly then it may result

in negative impacts upon functionality of business.

Board directors: A group which is responsible for supervising the whole

organisation is known as board of directors. This group is focused to conduct regular

meetings so that policies for executing operations of business could be formulated.

They are very important for businesses because they can facilitate an enterprise to

sustain in the market with the help of effective decision making of them. As they are

elected to represent the shareholders so they share detailed information of

requirements of them so that policies to retain the shareholders could be formulated

(Dolnicar, 2017).

Accounting information is very important for all the decision makers as it can help

them to analyse the actual position of business and then formulate future decisions for

betterment of business. Some of the decisions makers for the entities are CEO,

shareholders and board of directors. All of them need financial information and need of them

regarding the details could be analysed with the help of following discussion:

For all the decision makers accounting information is very important because it can

help them to determine that the business is able to perform all the operational

activities in systematic manner and reach to all the long term business goals.

Financial information is needed by CEO as it can help them to determine that the

business is performing appropriately or not. Apart from this, they can also analyse

that the financial position of the company is appropriate or not as compared to the

competitors.

The need of financial information for Board of Directors is very high because they are

working as the representatives of shareholders and in order to retain them for long

period they need to share proper and detailed information of company’s position. If

they will not be able to get the financial information, then it will be very difficult for

them to provide details of actual status of business to the shareholders (Götzer,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shareholders are the owners of business and financial information is also needed by

them as it can help them to analyse that the entity in which they have invested their

funds is able to sustain in the market. By using the information, they can formulate

decisions for future to provide funding to the entity to carry out operations.

The importance of having financial information for all the decisions makers is very

high as it can help them to make decisions for future to improve performance or

invest funds. If the information will not be gathered by them then it may result in long

term issues for them in future.

BT. British Telecom

Financial accounting involves recoding, analysing and summarising of all financial data in

that manner which can be used in reports. And these types of report which carries financial

information is useful for making effective plan and strategies related to finance and budget

(Berry, 2018). By this company will able to deal with their short outcomes in future. As well

as able to offer a better consumer service to end users. All the function starting from

recruiting to firing includes determination of sales target, planning of promotional activities

along with its budgeting and for choosing a specific techniques and software for performing

different function and operation. And all these decisions are taken by the senior executive

and managers of corporation. Responsibility of decision making within the firm depends on

the organisational structure of company for instance the in larger size company the

organisational structure that management team followed will be a hierarchical structure,

managed by top management or board of directors so that they will able to accomplish their

goal within stipulated time period. In relevance to this, a BT British telecom is a large size

organisation based on stock exchange and board of director managed by its CEO, Philip

Jansen and takes all strategic decision for the beneficial of company (Tong, Tao and Lifset,

2018). This firm follows hierarchical organisational structure which is the combination of

functional and divisional structure. In that all decision of company is taken by top level

management team on the basis of goal, objective, mission and vision of firm. For this all

obligation and roles are delegates to mangers of various departments as well as authorities

to carry out them.

them as it can help them to analyse that the entity in which they have invested their

funds is able to sustain in the market. By using the information, they can formulate

decisions for future to provide funding to the entity to carry out operations.

The importance of having financial information for all the decisions makers is very

high as it can help them to make decisions for future to improve performance or

invest funds. If the information will not be gathered by them then it may result in long

term issues for them in future.

BT. British Telecom

Financial accounting involves recoding, analysing and summarising of all financial data in

that manner which can be used in reports. And these types of report which carries financial

information is useful for making effective plan and strategies related to finance and budget

(Berry, 2018). By this company will able to deal with their short outcomes in future. As well

as able to offer a better consumer service to end users. All the function starting from

recruiting to firing includes determination of sales target, planning of promotional activities

along with its budgeting and for choosing a specific techniques and software for performing

different function and operation. And all these decisions are taken by the senior executive

and managers of corporation. Responsibility of decision making within the firm depends on

the organisational structure of company for instance the in larger size company the

organisational structure that management team followed will be a hierarchical structure,

managed by top management or board of directors so that they will able to accomplish their

goal within stipulated time period. In relevance to this, a BT British telecom is a large size

organisation based on stock exchange and board of director managed by its CEO, Philip

Jansen and takes all strategic decision for the beneficial of company (Tong, Tao and Lifset,

2018). This firm follows hierarchical organisational structure which is the combination of

functional and divisional structure. In that all decision of company is taken by top level

management team on the basis of goal, objective, mission and vision of firm. For this all

obligation and roles are delegates to mangers of various departments as well as authorities

to carry out them.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b)

Sole trader: A person who is running own business and responsible for bearing all

the risks and getting the profits is known as sole trader. All the profits or losses that will be

generated or faced by the enterprise in case this type of business will be the responsibility of

the owner. It is the cheapest and simplest structure of a business. In case of a sole trader

the decisions will be taken by the owner, no one can interfere in the decision making

process. In sole trading firms it is not compulsory to generate the accounting records as the

owner will be responsible to deal with profits and losses. Some of the advantages and

disadvantages of this type of business are as follows:

Advantages:

The process of formulating and winding up a sole trading business is very easy so

the owner will not have to be worry about the legal procedure in this case. It is an

advantage because it can help to reduce stress of owner to follow long processes for

business formulation.

Another advantage of sole trader is that the decision making process in this type of

business is quick as the owner does not have to ask for any type of approval in

decisions (Liu, 2019).

If a sole trading business will be operated by an individual, then it will be easy to

maintain the business secrets as there will be no one who can share the secrets with

outsiders in this type of firm.

Disadvantages:

The major disadvantage of a sole trading firm is related to resources which will be

limited. Due to this the owner will be able to spend limited amount on the development of

business.

The level of continuity in sole trading business is very low. For example, if the owner

will have to go to out of city then the business will not be carried out continuously and it may

affect the profitability.

The managerial expertise in sole trading business is very low and the owner will not

be able to ask for any type of guidance from others because there will be only one person

who will be running the business.

Partnership: It is a type of business in which an agreement is signed by two or more

parties to carry out business collaboratively. All the individuals who will be running the

business will be known as partners. The accounting process in partnership business will be

same as the rules that are made for the corporations (Uyar, Gungormus and Kuzey, 2017).

The profit and loss in this type of business will be segregated by partners equally or a

predetermined ratio. Advantages and disadvantages of this type of business are as follows:

Sole trader: A person who is running own business and responsible for bearing all

the risks and getting the profits is known as sole trader. All the profits or losses that will be

generated or faced by the enterprise in case this type of business will be the responsibility of

the owner. It is the cheapest and simplest structure of a business. In case of a sole trader

the decisions will be taken by the owner, no one can interfere in the decision making

process. In sole trading firms it is not compulsory to generate the accounting records as the

owner will be responsible to deal with profits and losses. Some of the advantages and

disadvantages of this type of business are as follows:

Advantages:

The process of formulating and winding up a sole trading business is very easy so

the owner will not have to be worry about the legal procedure in this case. It is an

advantage because it can help to reduce stress of owner to follow long processes for

business formulation.

Another advantage of sole trader is that the decision making process in this type of

business is quick as the owner does not have to ask for any type of approval in

decisions (Liu, 2019).

If a sole trading business will be operated by an individual, then it will be easy to

maintain the business secrets as there will be no one who can share the secrets with

outsiders in this type of firm.

Disadvantages:

The major disadvantage of a sole trading firm is related to resources which will be

limited. Due to this the owner will be able to spend limited amount on the development of

business.

The level of continuity in sole trading business is very low. For example, if the owner

will have to go to out of city then the business will not be carried out continuously and it may

affect the profitability.

The managerial expertise in sole trading business is very low and the owner will not

be able to ask for any type of guidance from others because there will be only one person

who will be running the business.

Partnership: It is a type of business in which an agreement is signed by two or more

parties to carry out business collaboratively. All the individuals who will be running the

business will be known as partners. The accounting process in partnership business will be

same as the rules that are made for the corporations (Uyar, Gungormus and Kuzey, 2017).

The profit and loss in this type of business will be segregated by partners equally or a

predetermined ratio. Advantages and disadvantages of this type of business are as follows:

Advantages:

A partnership firm is less formal with few obligation of legal authorities that can help

to execute all the operations in systematic manner. For example, as a limited

company is required to generate a confirmation statement but it will not be required in

partnership.

It is very easy to start a partnership business is the partners are agreeing to carry out

business collaboratively.

The burden of bearing losses and facing risks will be shared by all the partners and it

will not harm a single person or affect the profitability of business (Fitzgibbons, 2016).

Disadvantages:

The liabilities of all the partners in partnership firm will be unlimited and due to this

the partners may have to bear huge losses.

The access of partners in the capital is limited to the partners as they will not be able

to raise funds to grow the business easily as banks may refuse to provide funds to

operate business.

The possibility of potential differences and conflicts in partnership business is very

high because grievances may take place between partners at the time of decision

making.

Financial accounts represent all financial data with relation to company in brief that makes

viable and easy for the management team along with investors of company to use that

information in devising strategies. In which the financial accounts are prepared on the basis

of standard principles and guidance which are same throughout industry (Werner, 2017).

This aids them make differentiation from other competitors for standing across benchmark of

industry. It provides basis for management to take related to investment proposal like

whether these decisions are beneficial and economically feasible for company to take or not.

Further the projection and estimations are also relying on financial data within company and

for improvement according to the condition of marketplace. This is not only essential in terms

of comparison but also in forms of basis for extracting useful information from non-financial

data.

Mc Donald’s /KFC

A partnership firm is less formal with few obligation of legal authorities that can help

to execute all the operations in systematic manner. For example, as a limited

company is required to generate a confirmation statement but it will not be required in

partnership.

It is very easy to start a partnership business is the partners are agreeing to carry out

business collaboratively.

The burden of bearing losses and facing risks will be shared by all the partners and it

will not harm a single person or affect the profitability of business (Fitzgibbons, 2016).

Disadvantages:

The liabilities of all the partners in partnership firm will be unlimited and due to this

the partners may have to bear huge losses.

The access of partners in the capital is limited to the partners as they will not be able

to raise funds to grow the business easily as banks may refuse to provide funds to

operate business.

The possibility of potential differences and conflicts in partnership business is very

high because grievances may take place between partners at the time of decision

making.

Financial accounts represent all financial data with relation to company in brief that makes

viable and easy for the management team along with investors of company to use that

information in devising strategies. In which the financial accounts are prepared on the basis

of standard principles and guidance which are same throughout industry (Werner, 2017).

This aids them make differentiation from other competitors for standing across benchmark of

industry. It provides basis for management to take related to investment proposal like

whether these decisions are beneficial and economically feasible for company to take or not.

Further the projection and estimations are also relying on financial data within company and

for improvement according to the condition of marketplace. This is not only essential in terms

of comparison but also in forms of basis for extracting useful information from non-financial

data.

Mc Donald’s /KFC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In accounting all transaction are record and assess within a business are specific in nature

and all these are carried out on the basis of prescription of laws. In relevance to given two

firm Mc Donald and KFC some advantage and disadvantage with relation to maintenance of

accounting records are as follows:

Advantages:

Decision making: - In an organisation it is the responsibility of management team to

take effective decision related to finance and with the help of accounting they will able to

accomplish this goal by comparing financial records of present and past. In which accounting

books plays that role for business (Firmansyah, Arham and Nor, 2020). This provides

information about cash inflow and outflow along with income and expenses that makes easy

to forecast surplus or deficiency within funds and it need to be arranged timely. So, this aids

in developing responsibility and accountability fixation for preventing and detection of frauds.

In relevance to Mc Donald and KFC, this process of accounting provides a huge benefit to

them in making effective decision with relation to finance.

Evidence in legal matters: Accounting books in a business firm acts as business

record as all financial transaction are recorded in it. When any legal matter arises in relation

to finance or budget, that time these books will helpful, as a proof company can use this in

court. In context of Mc Donald and KFC they prepare accounting books on the basis of

specific format of act and then submit to registrar, once audited is done from independent

auditor. This makes them accountably and legally presented towards Tax authorities.

Disadvantage:

Record only financial aspects: In a business unit it has been find that it is one of

the prominent disadvantages of financial accounting as it only includes transaction and data

that are related with the finance nature only. For this context there are various non-financial

factors such as market conditions, political environments, policies, legal laws, social factors

and so on. All these puts significant impacts on business function and operations. As well as

all these are left out from being recorded in books of accounting. Due this it represents a

incomplete picture during devising strategy and making important decision of business. In

context of given tow firm, the mangers of company cannot take decision related to other

factors like environmental social etc. on the basis of this accounting book.

Historical nature: In books of accounts, amount is recorded on actual cost and

prices, fluctuations in cost will not be taken into consideration. Due to this it makes books of

accounts as a historical nature (Epstein, Buhovac and Yuthas, 2015). All these information

and data will be used as a base for future forecasting. It is not related with the time value of

money and changes that raise with this. With reference to KFC and Mc Donald, it is not

necessary that the estimation that makes on the basis of historical cost will be correct it

might go in wrong direction too for future activities.

and all these are carried out on the basis of prescription of laws. In relevance to given two

firm Mc Donald and KFC some advantage and disadvantage with relation to maintenance of

accounting records are as follows:

Advantages:

Decision making: - In an organisation it is the responsibility of management team to

take effective decision related to finance and with the help of accounting they will able to

accomplish this goal by comparing financial records of present and past. In which accounting

books plays that role for business (Firmansyah, Arham and Nor, 2020). This provides

information about cash inflow and outflow along with income and expenses that makes easy

to forecast surplus or deficiency within funds and it need to be arranged timely. So, this aids

in developing responsibility and accountability fixation for preventing and detection of frauds.

In relevance to Mc Donald and KFC, this process of accounting provides a huge benefit to

them in making effective decision with relation to finance.

Evidence in legal matters: Accounting books in a business firm acts as business

record as all financial transaction are recorded in it. When any legal matter arises in relation

to finance or budget, that time these books will helpful, as a proof company can use this in

court. In context of Mc Donald and KFC they prepare accounting books on the basis of

specific format of act and then submit to registrar, once audited is done from independent

auditor. This makes them accountably and legally presented towards Tax authorities.

Disadvantage:

Record only financial aspects: In a business unit it has been find that it is one of

the prominent disadvantages of financial accounting as it only includes transaction and data

that are related with the finance nature only. For this context there are various non-financial

factors such as market conditions, political environments, policies, legal laws, social factors

and so on. All these puts significant impacts on business function and operations. As well as

all these are left out from being recorded in books of accounting. Due this it represents a

incomplete picture during devising strategy and making important decision of business. In

context of given tow firm, the mangers of company cannot take decision related to other

factors like environmental social etc. on the basis of this accounting book.

Historical nature: In books of accounts, amount is recorded on actual cost and

prices, fluctuations in cost will not be taken into consideration. Due to this it makes books of

accounts as a historical nature (Epstein, Buhovac and Yuthas, 2015). All these information

and data will be used as a base for future forecasting. It is not related with the time value of

money and changes that raise with this. With reference to KFC and Mc Donald, it is not

necessary that the estimation that makes on the basis of historical cost will be correct it

might go in wrong direction too for future activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

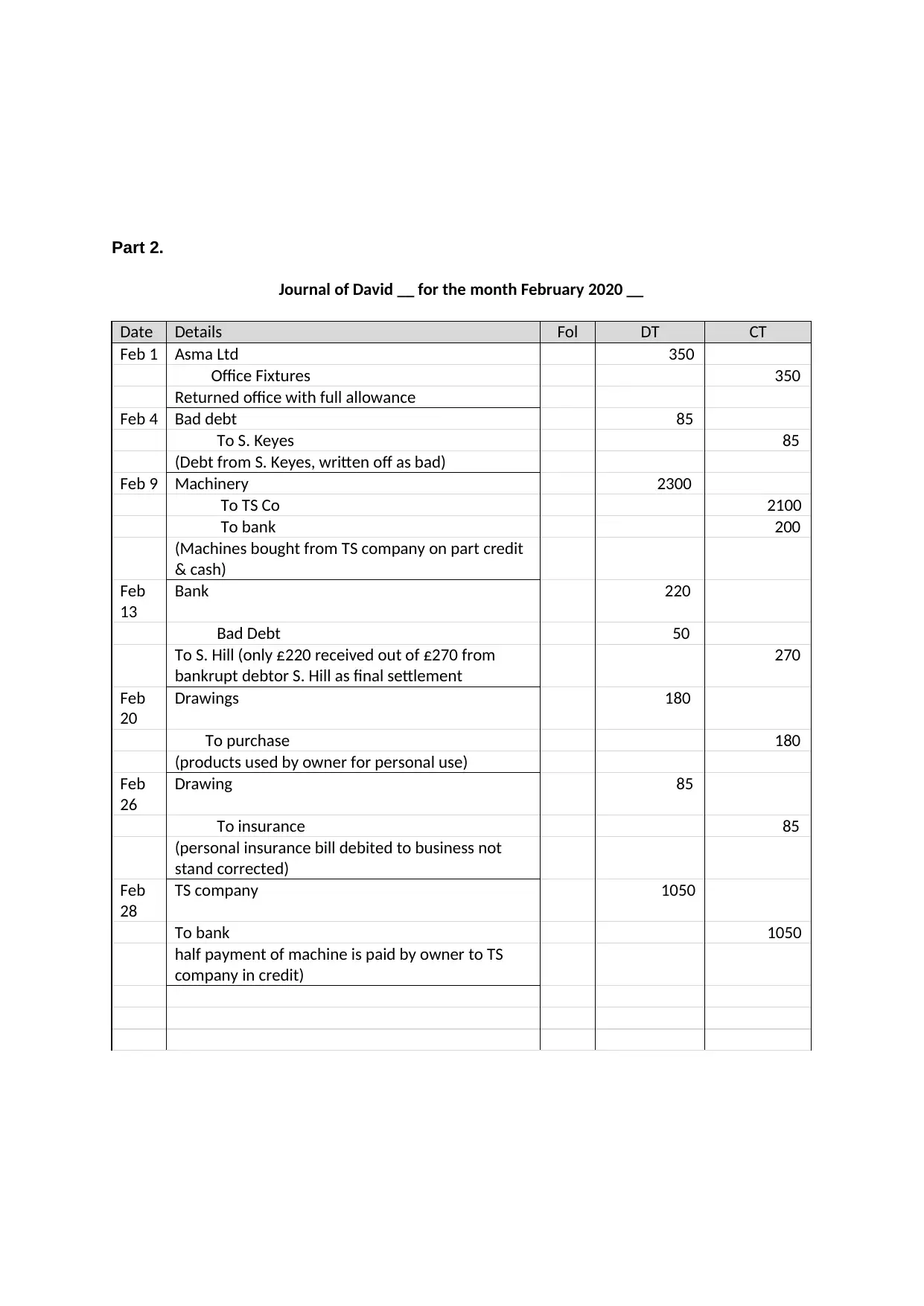

Part 2.

Journal of David __ for the month February 2020 __

Date Details Fol DT CT

Feb 1 Asma Ltd 350

Office Fixtures 350

Returned office with full allowance

Feb 4 Bad debt 85

To S. Keyes 85

(Debt from S. Keyes, written off as bad)

Feb 9 Machinery 2300

To TS Co 2100

To bank 200

(Machines bought from TS company on part credit

& cash)

Feb

13

Bank 220

Bad Debt 50

To S. Hill (only £220 received out of £270 from

bankrupt debtor S. Hill as final settlement

270

Feb

20

Drawings 180

To purchase 180

(products used by owner for personal use)

Feb

26

Drawing 85

To insurance 85

(personal insurance bill debited to business not

stand corrected)

Feb

28

TS company 1050

To bank 1050

half payment of machine is paid by owner to TS

company in credit)

Journal of David __ for the month February 2020 __

Date Details Fol DT CT

Feb 1 Asma Ltd 350

Office Fixtures 350

Returned office with full allowance

Feb 4 Bad debt 85

To S. Keyes 85

(Debt from S. Keyes, written off as bad)

Feb 9 Machinery 2300

To TS Co 2100

To bank 200

(Machines bought from TS company on part credit

& cash)

Feb

13

Bank 220

Bad Debt 50

To S. Hill (only £220 received out of £270 from

bankrupt debtor S. Hill as final settlement

270

Feb

20

Drawings 180

To purchase 180

(products used by owner for personal use)

Feb

26

Drawing 85

To insurance 85

(personal insurance bill debited to business not

stand corrected)

Feb

28

TS company 1050

To bank 1050

half payment of machine is paid by owner to TS

company in credit)

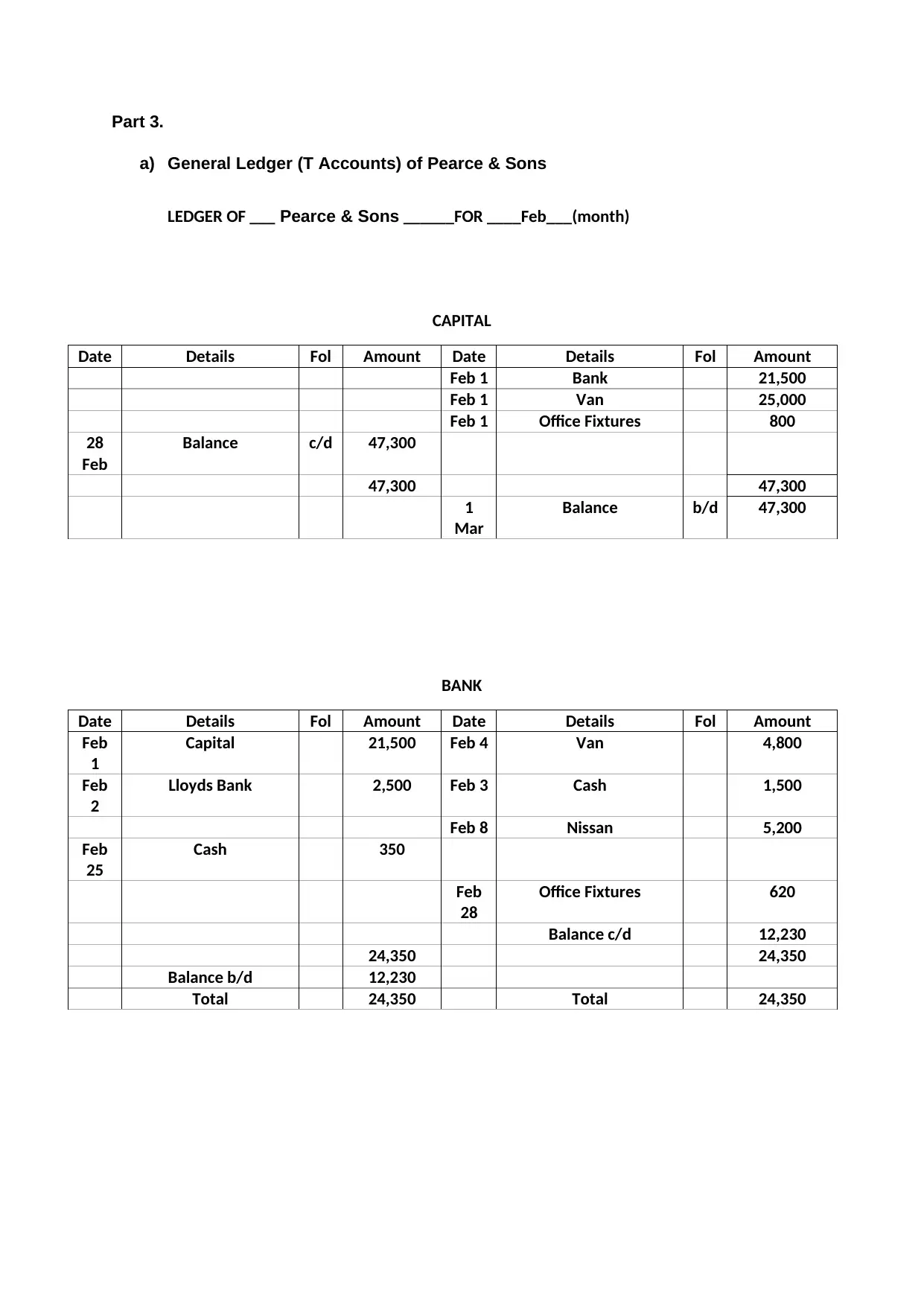

Part 3.

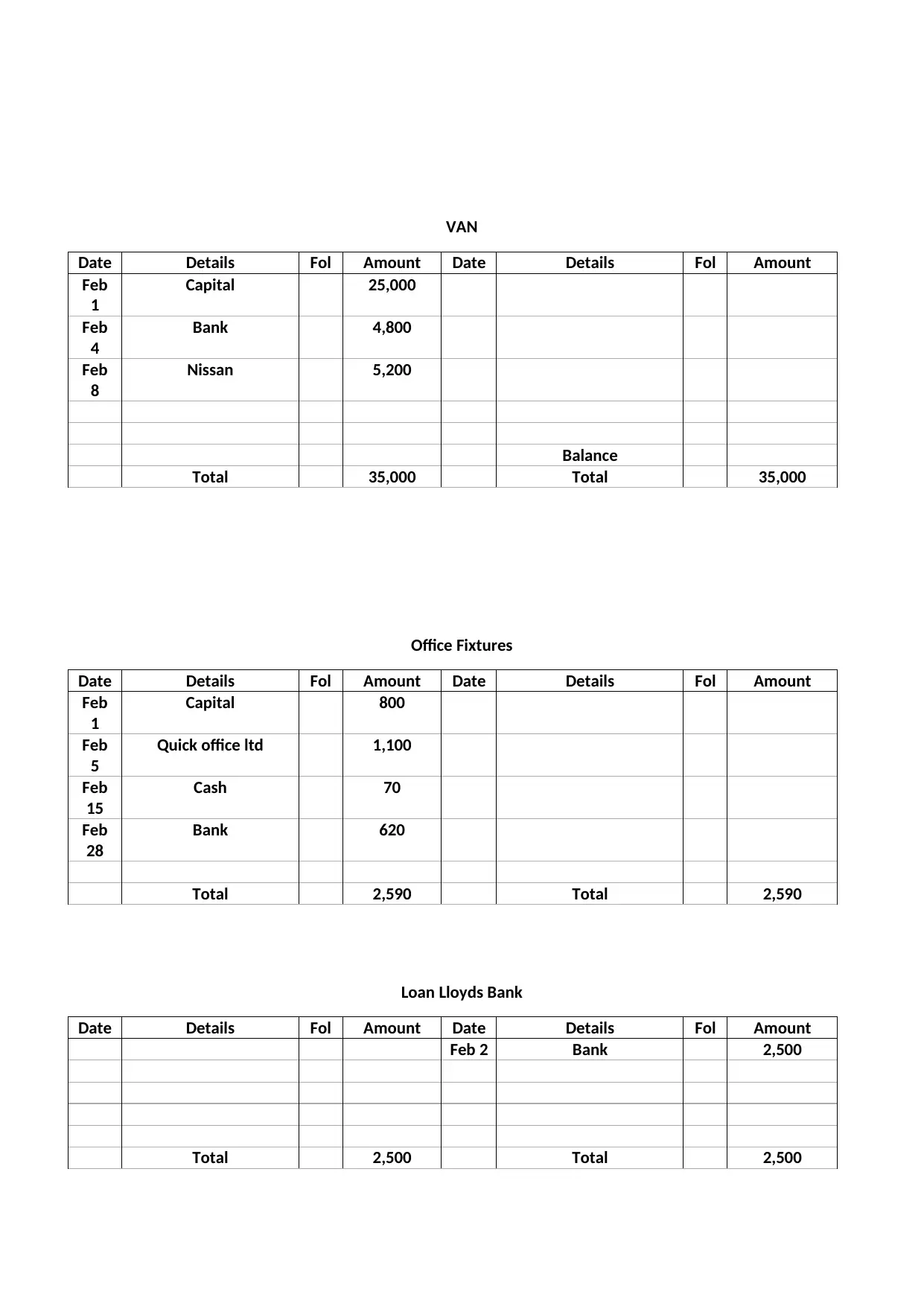

a) General Ledger (T Accounts) of Pearce & Sons

LEDGER OF ___ Pearce & Sons ______FOR ____Feb___(month)

CAPITAL

Date Details Fol Amount Date Details Fol Amount

Feb 1 Bank 21,500

Feb 1 Van 25,000

Feb 1 Office Fixtures 800

28

Feb

Balance c/d 47,300

47,300 47,300

1

Mar

Balance b/d 47,300

BANK

Date Details Fol Amount Date Details Fol Amount

Feb

1

Capital 21,500 Feb 4 Van 4,800

Feb

2

Lloyds Bank 2,500 Feb 3 Cash 1,500

Feb 8 Nissan 5,200

Feb

25

Cash 350

Feb

28

Office Fixtures 620

Balance c/d 12,230

24,350 24,350

Balance b/d 12,230

Total 24,350 Total 24,350

a) General Ledger (T Accounts) of Pearce & Sons

LEDGER OF ___ Pearce & Sons ______FOR ____Feb___(month)

CAPITAL

Date Details Fol Amount Date Details Fol Amount

Feb 1 Bank 21,500

Feb 1 Van 25,000

Feb 1 Office Fixtures 800

28

Feb

Balance c/d 47,300

47,300 47,300

1

Mar

Balance b/d 47,300

BANK

Date Details Fol Amount Date Details Fol Amount

Feb

1

Capital 21,500 Feb 4 Van 4,800

Feb

2

Lloyds Bank 2,500 Feb 3 Cash 1,500

Feb 8 Nissan 5,200

Feb

25

Cash 350

Feb

28

Office Fixtures 620

Balance c/d 12,230

24,350 24,350

Balance b/d 12,230

Total 24,350 Total 24,350

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VAN

Date Details Fol Amount Date Details Fol Amount

Feb

1

Capital 25,000

Feb

4

Bank 4,800

Feb

8

Nissan 5,200

Balance

Total 35,000 Total 35,000

Office Fixtures

Date Details Fol Amount Date Details Fol Amount

Feb

1

Capital 800

Feb

5

Quick office ltd 1,100

Feb

15

Cash 70

Feb

28

Bank 620

Total 2,590 Total 2,590

Loan Lloyds Bank

Date Details Fol Amount Date Details Fol Amount

Feb 2 Bank 2,500

Total 2,500 Total 2,500

Date Details Fol Amount Date Details Fol Amount

Feb

1

Capital 25,000

Feb

4

Bank 4,800

Feb

8

Nissan 5,200

Balance

Total 35,000 Total 35,000

Office Fixtures

Date Details Fol Amount Date Details Fol Amount

Feb

1

Capital 800

Feb

5

Quick office ltd 1,100

Feb

15

Cash 70

Feb

28

Bank 620

Total 2,590 Total 2,590

Loan Lloyds Bank

Date Details Fol Amount Date Details Fol Amount

Feb 2 Bank 2,500

Total 2,500 Total 2,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

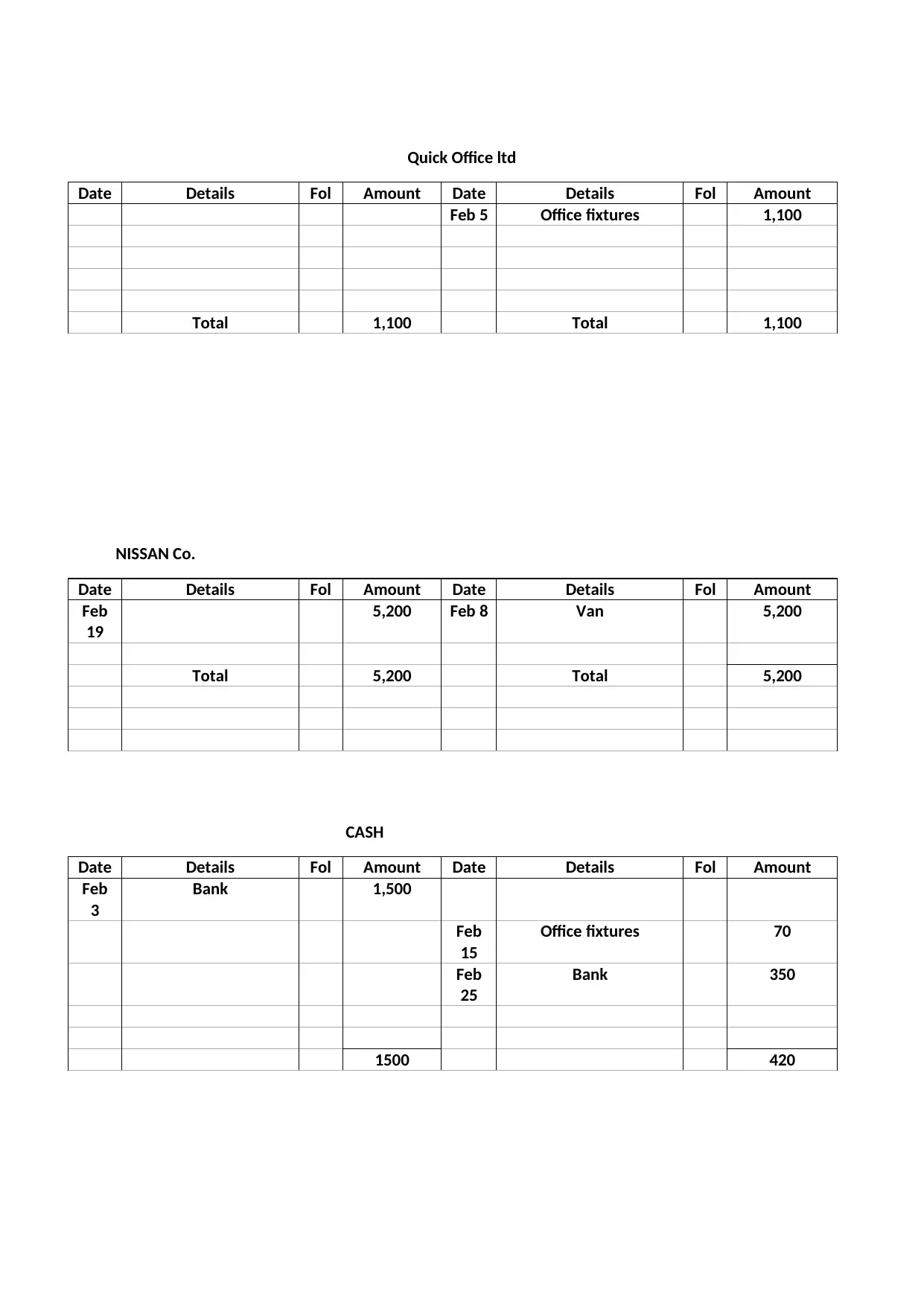

Quick Office ltd

Date Details Fol Amount Date Details Fol Amount

Feb 5 Office fixtures 1,100

Total 1,100 Total 1,100

NISSAN Co.

Date Details Fol Amount Date Details Fol Amount

Feb

19

5,200 Feb 8 Van 5,200

Total 5,200 Total 5,200

CASH

Date Details Fol Amount Date Details Fol Amount

Feb

3

Bank 1,500

Feb

15

Office fixtures 70

Feb

25

Bank 350

1500 420

Date Details Fol Amount Date Details Fol Amount

Feb 5 Office fixtures 1,100

Total 1,100 Total 1,100

NISSAN Co.

Date Details Fol Amount Date Details Fol Amount

Feb

19

5,200 Feb 8 Van 5,200

Total 5,200 Total 5,200

CASH

Date Details Fol Amount Date Details Fol Amount

Feb

3

Bank 1,500

Feb

15

Office fixtures 70

Feb

25

Bank 350

1500 420

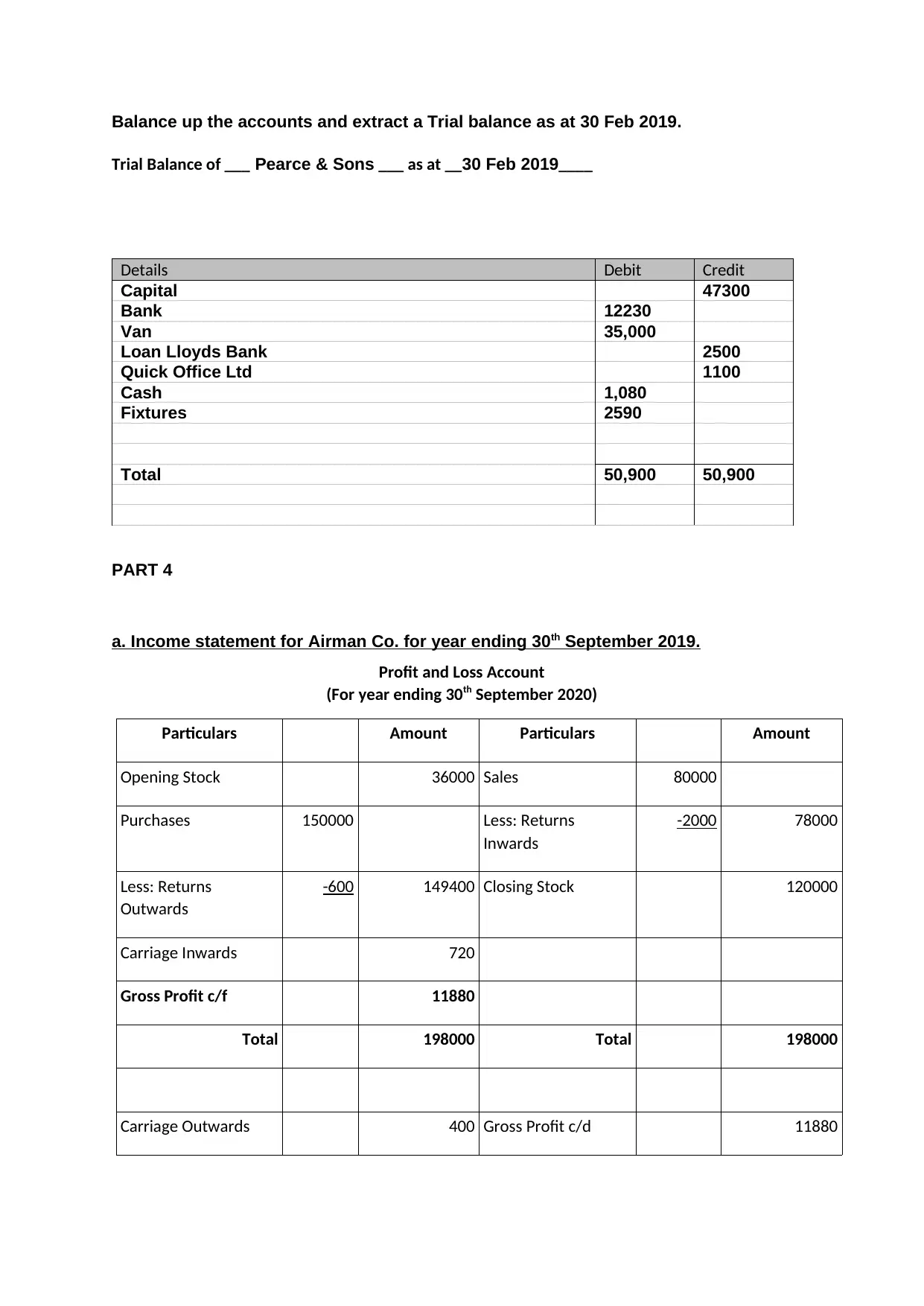

Balance up the accounts and extract a Trial balance as at 30 Feb 2019.

Trial Balance of ___ Pearce & Sons ___ as at __30 Feb 2019____

Details Debit Credit

Capital 47300

Bank 12230

Van 35,000

Loan Lloyds Bank 2500

Quick Office Ltd 1100

Cash 1,080

Fixtures 2590

Total 50,900 50,900

PART 4

a. Income statement for Airman Co. for year ending 30th September 2019.

Profit and Loss Account

(For year ending 30th September 2020)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns

Inwards

-2000 78000

Less: Returns

Outwards

-600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Trial Balance of ___ Pearce & Sons ___ as at __30 Feb 2019____

Details Debit Credit

Capital 47300

Bank 12230

Van 35,000

Loan Lloyds Bank 2500

Quick Office Ltd 1100

Cash 1,080

Fixtures 2590

Total 50,900 50,900

PART 4

a. Income statement for Airman Co. for year ending 30th September 2019.

Profit and Loss Account

(For year ending 30th September 2020)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns

Inwards

-2000 78000

Less: Returns

Outwards

-600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.