Business Transactions: Financial Statement Analysis & Recording

VerifiedAdded on 2023/06/14

|15

|1956

|157

Report

AI Summary

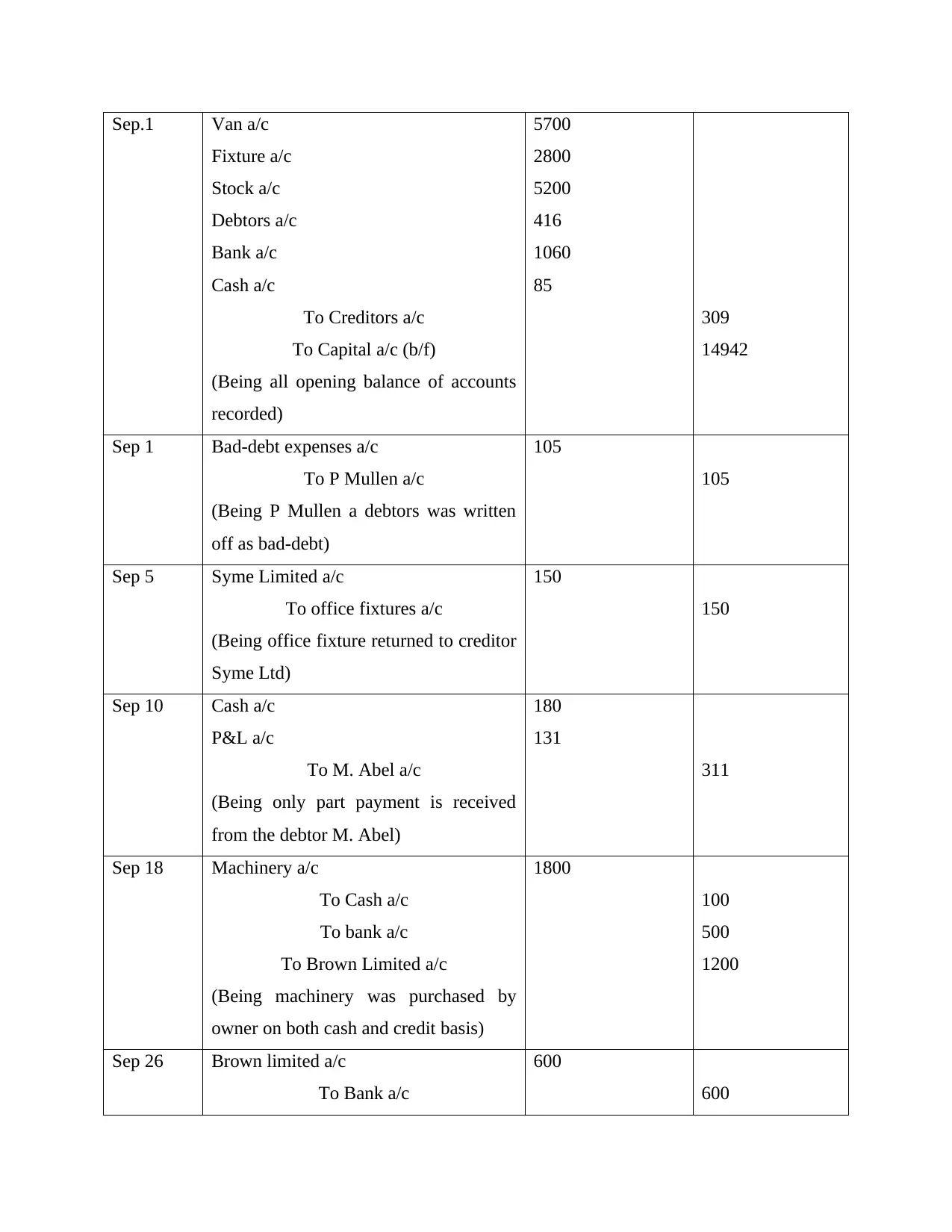

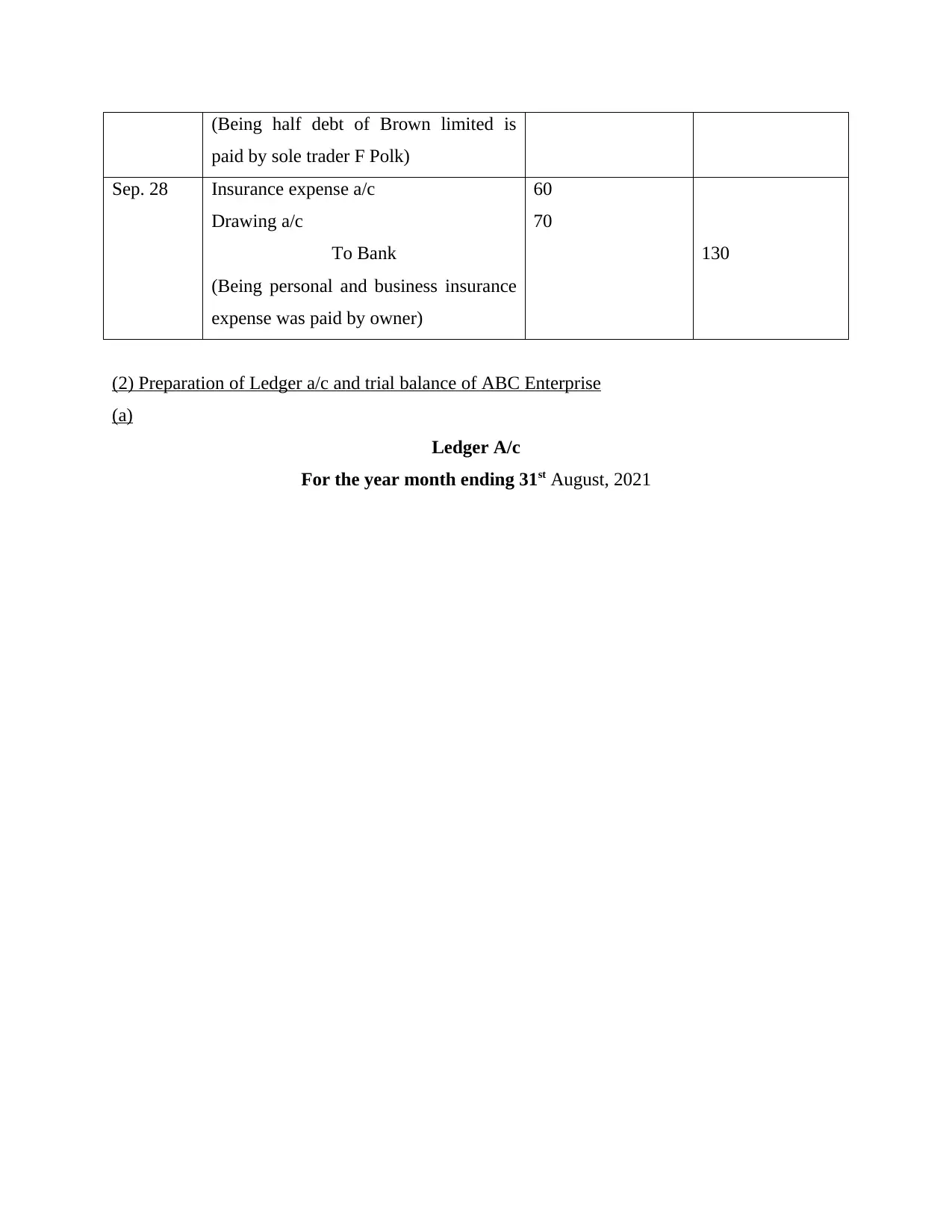

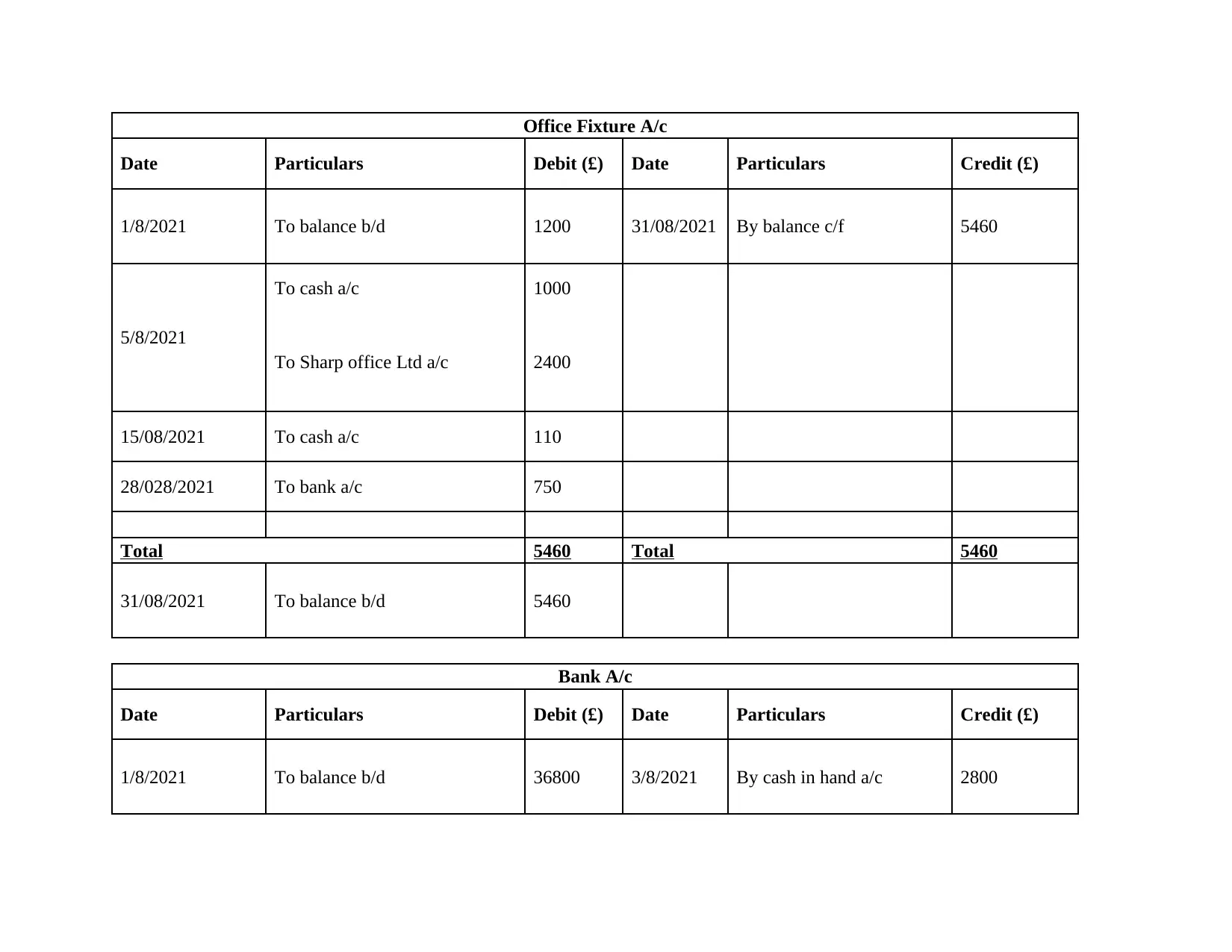

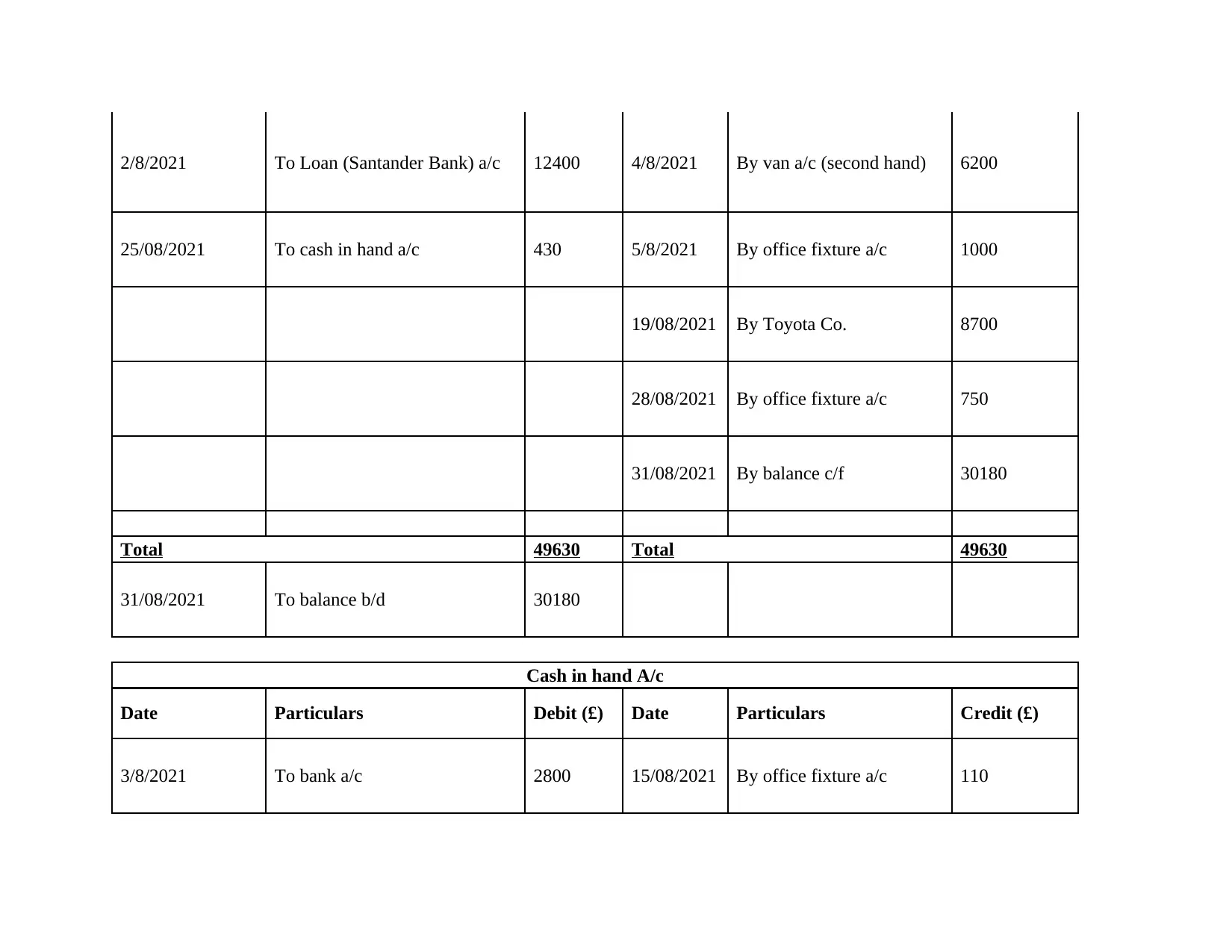

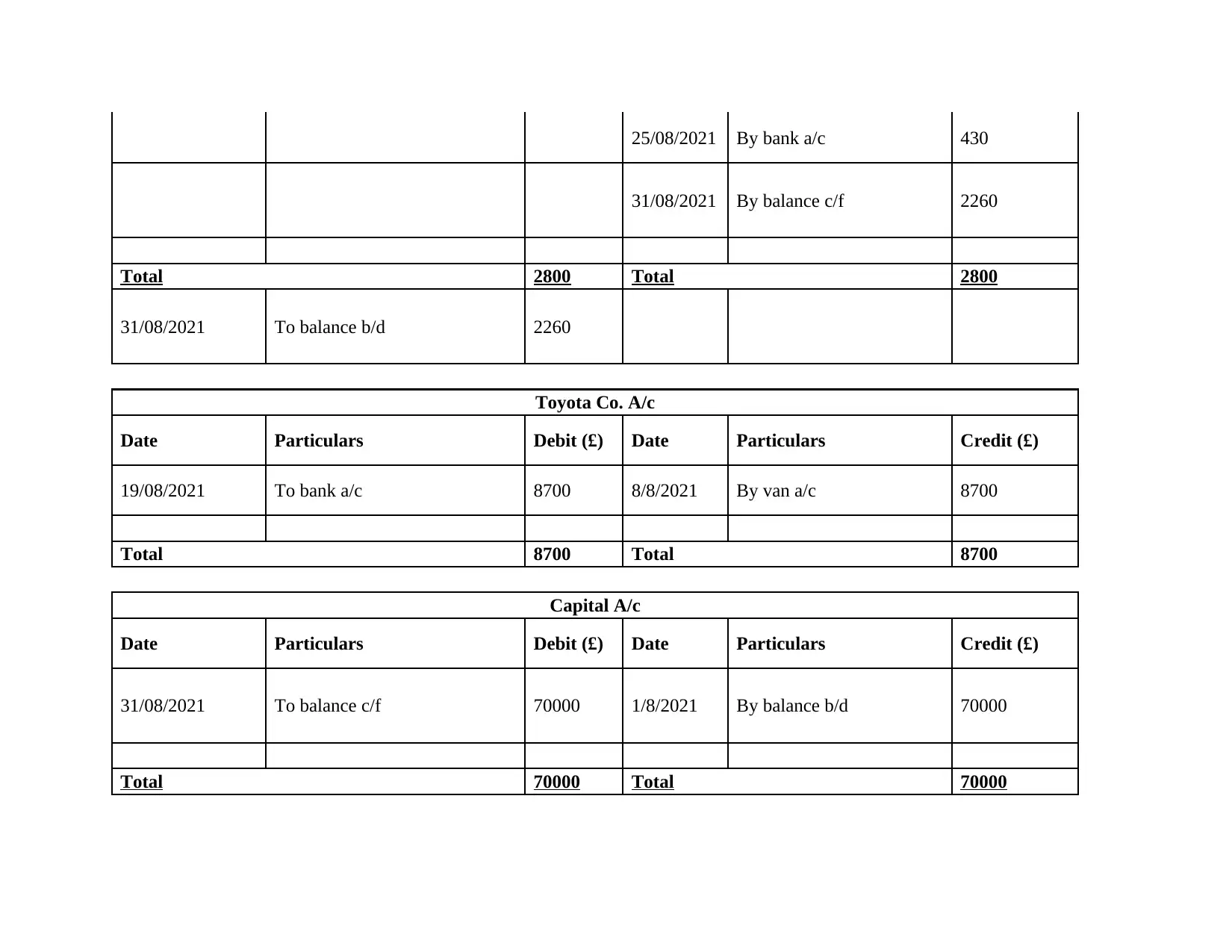

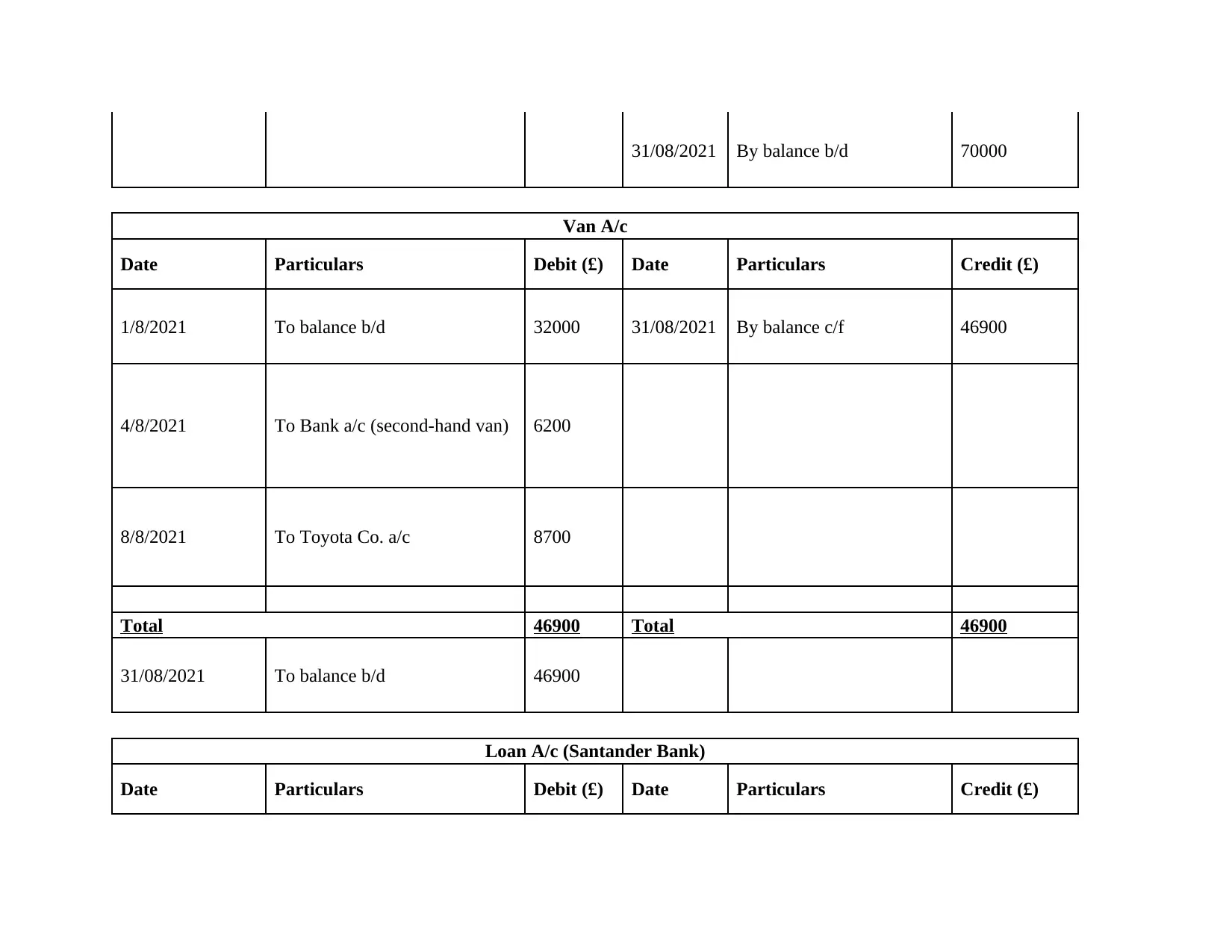

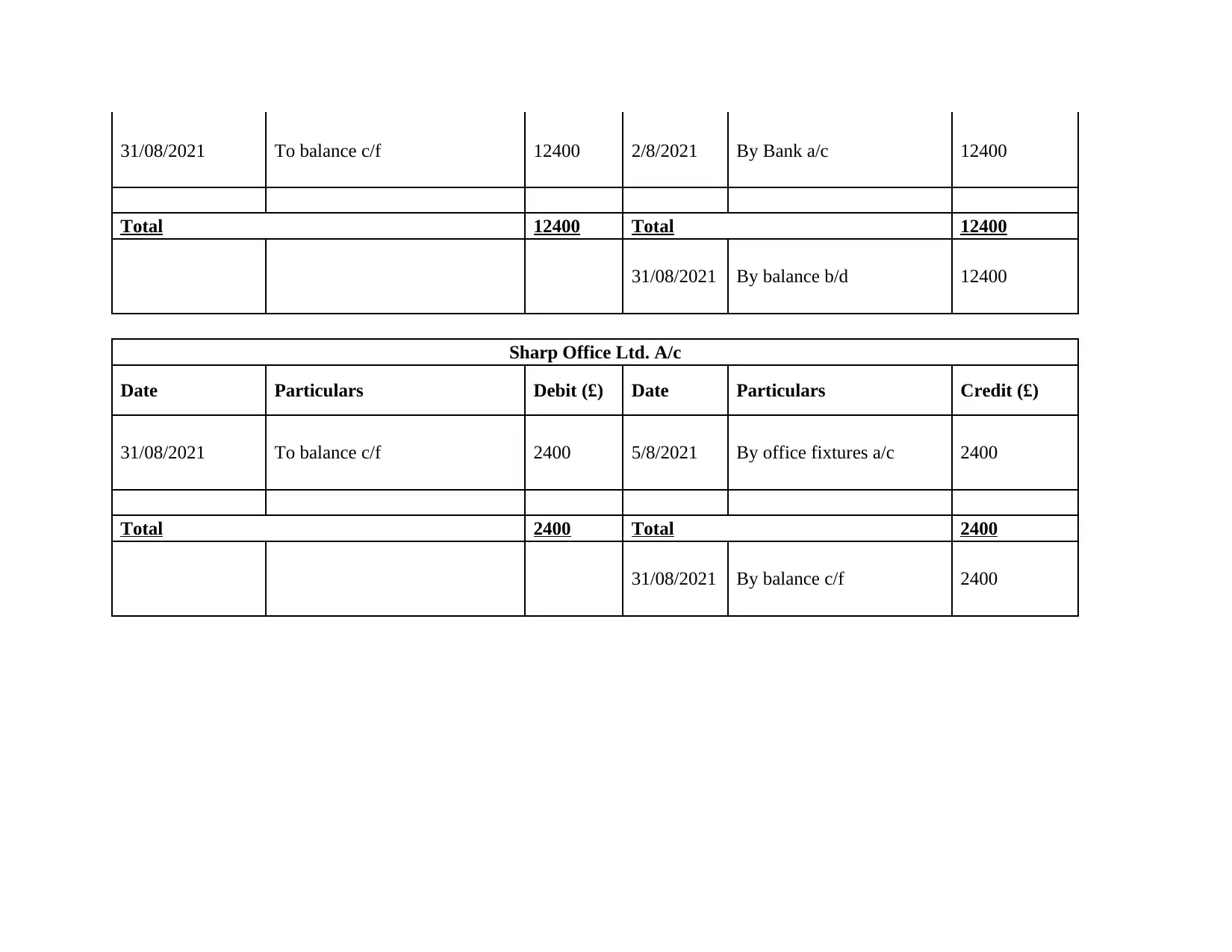

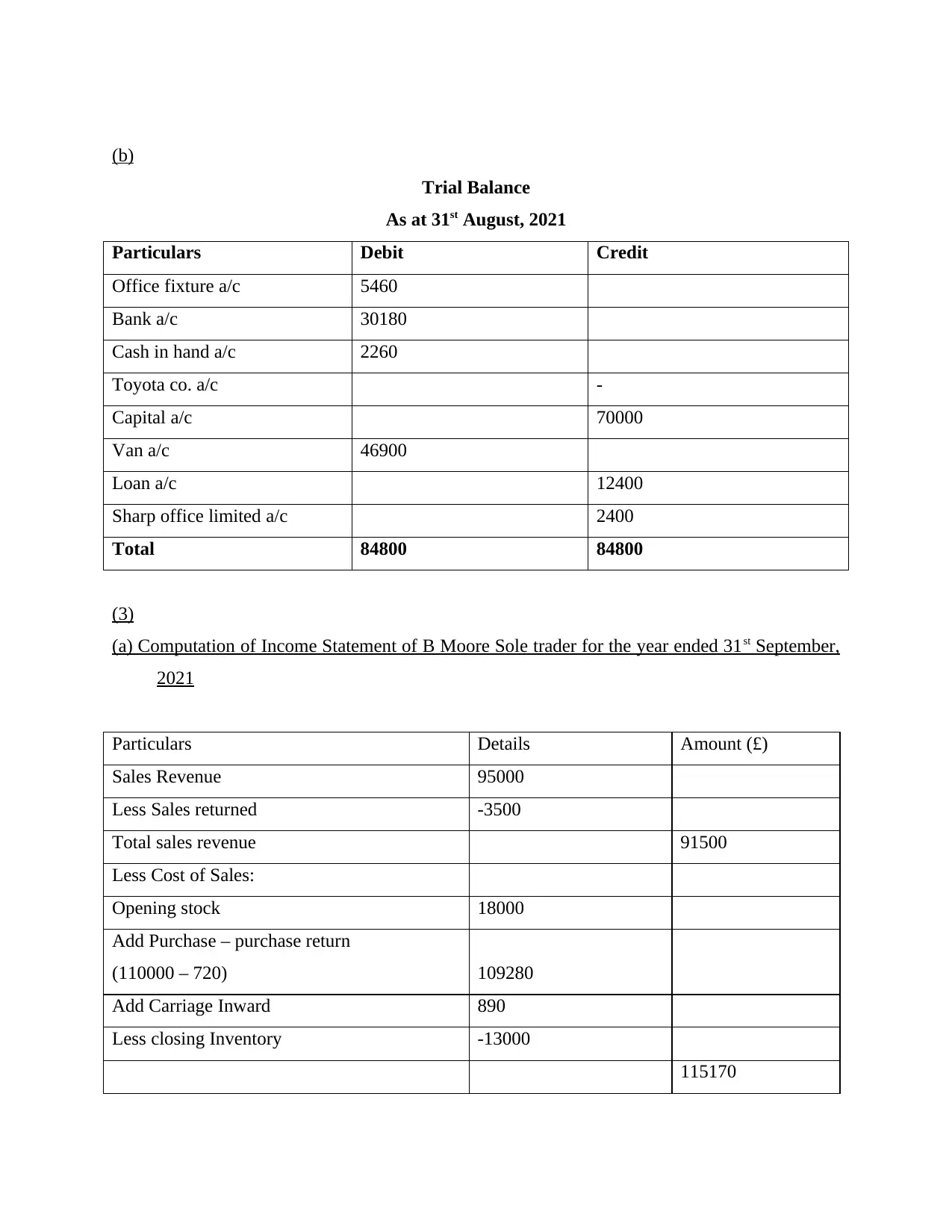

This report provides a detailed analysis of recording business transactions, starting with the steps to start a business in the UK decoration industry and identifying key decision-makers in a company like ASDA. It includes the preparation of journal entries, ledger accounts, and a trial balance for F Polk's business. Furthermore, the report computes the income statement for B Moore, a sole trader, for the year ended 31st September 2021, revealing a net loss. The analysis extends to a review of the company's profit/loss trend from 2013 to 2022, highlighting fluctuating performance and the impact of the pandemic on recent losses. The report concludes by emphasizing the importance of these accounting processes for understanding a business's financial health.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.