Recording Business Transactions and Financial Analysis (Toy Shop)

VerifiedAdded on 2022/12/29

|11

|2547

|48

Project

AI Summary

This project presents a detailed financial analysis of a newly established toy shop in Oxford, focusing on the month of October 2020. It begins by documenting the business transactions through journal entries, followed by the creation of ledger accounts and a trial balance to identify any posting errors. The project then constructs an income statement to assess profitability and a statement of financial position (balance sheet) to evaluate the business's financial health. Furthermore, the project includes the calculation and comparison of various financial ratios to gauge the toy shop's performance against industry standards and competitors. The analysis covers net profit margin, gross profit margin, current ratio, acid test ratio, accounts receivable collection period, and accounts payable payment period. The project concludes with insights into the company's financial standing and future growth prospects, using the financial statements as the basis for its assessment.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

PART A...........................................................................................................................................1

b) Ledger accounts for the month of October 2020 of toy shop in Oxford:-...............................1

c) Trial balance as at 31st October 2020:-...................................................................................4

d) Income Statement for the period ended 31st October 2020:-..................................................4

e) Statement of Financial Position as at 31st October 2020:-......................................................5

f) Meaning of drawings account:-................................................................................................5

PART B............................................................................................................................................6

i) Calculation of ratios:-...............................................................................................................6

ii) Comparison of ratios:-.............................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

PART A...........................................................................................................................................1

b) Ledger accounts for the month of October 2020 of toy shop in Oxford:-...............................1

c) Trial balance as at 31st October 2020:-...................................................................................4

d) Income Statement for the period ended 31st October 2020:-..................................................4

e) Statement of Financial Position as at 31st October 2020:-......................................................5

f) Meaning of drawings account:-................................................................................................5

PART B............................................................................................................................................6

i) Calculation of ratios:-...............................................................................................................6

ii) Comparison of ratios:-.............................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

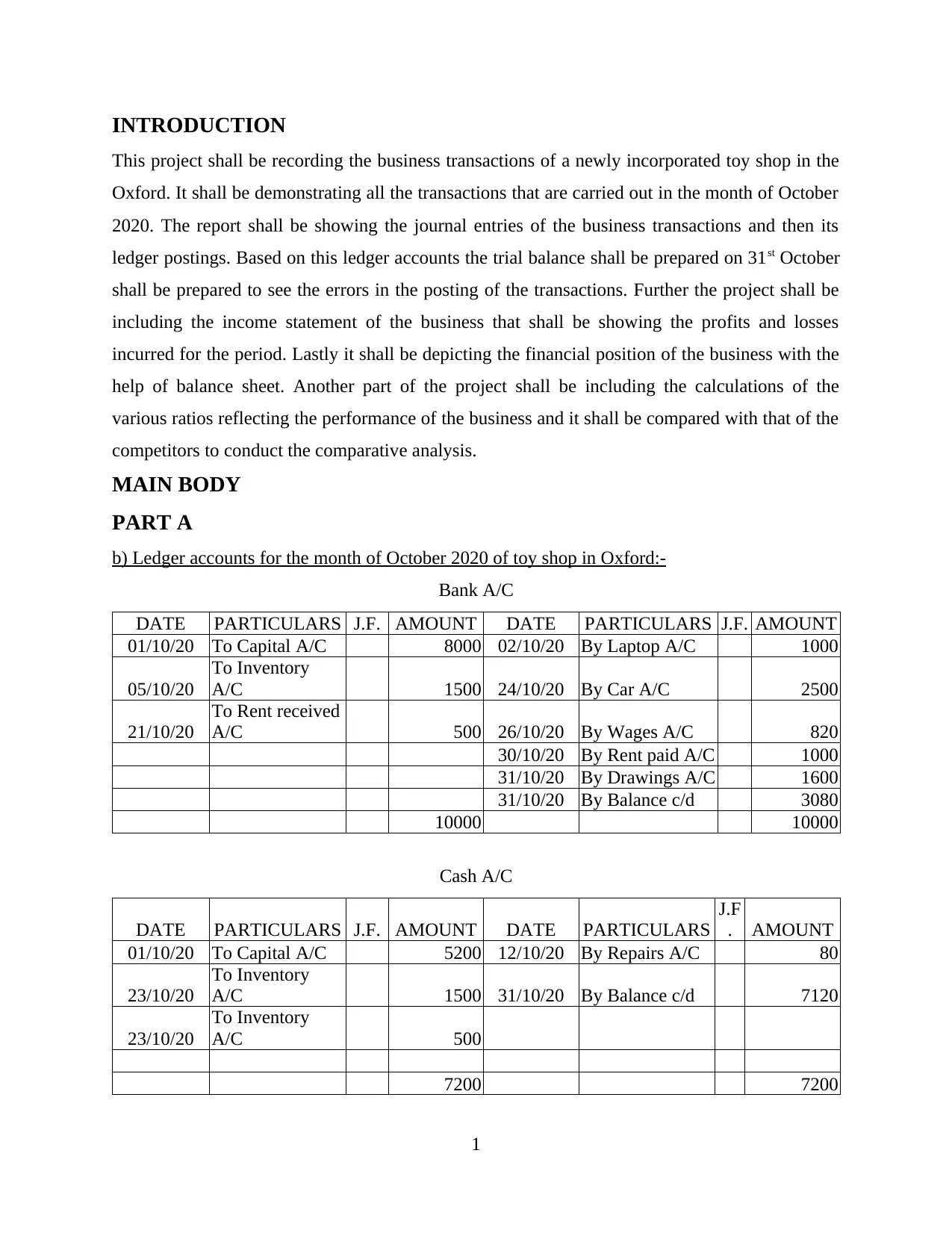

INTRODUCTION

This project shall be recording the business transactions of a newly incorporated toy shop in the

Oxford. It shall be demonstrating all the transactions that are carried out in the month of October

2020. The report shall be showing the journal entries of the business transactions and then its

ledger postings. Based on this ledger accounts the trial balance shall be prepared on 31st October

shall be prepared to see the errors in the posting of the transactions. Further the project shall be

including the income statement of the business that shall be showing the profits and losses

incurred for the period. Lastly it shall be depicting the financial position of the business with the

help of balance sheet. Another part of the project shall be including the calculations of the

various ratios reflecting the performance of the business and it shall be compared with that of the

competitors to conduct the comparative analysis.

MAIN BODY

PART A

b) Ledger accounts for the month of October 2020 of toy shop in Oxford:-

Bank A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

01/10/20 To Capital A/C 8000 02/10/20 By Laptop A/C 1000

05/10/20

To Inventory

A/C 1500 24/10/20 By Car A/C 2500

21/10/20

To Rent received

A/C 500 26/10/20 By Wages A/C 820

30/10/20 By Rent paid A/C 1000

31/10/20 By Drawings A/C 1600

31/10/20 By Balance c/d 3080

10000 10000

Cash A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS

J.F

. AMOUNT

01/10/20 To Capital A/C 5200 12/10/20 By Repairs A/C 80

23/10/20

To Inventory

A/C 1500 31/10/20 By Balance c/d 7120

23/10/20

To Inventory

A/C 500

7200 7200

1

This project shall be recording the business transactions of a newly incorporated toy shop in the

Oxford. It shall be demonstrating all the transactions that are carried out in the month of October

2020. The report shall be showing the journal entries of the business transactions and then its

ledger postings. Based on this ledger accounts the trial balance shall be prepared on 31st October

shall be prepared to see the errors in the posting of the transactions. Further the project shall be

including the income statement of the business that shall be showing the profits and losses

incurred for the period. Lastly it shall be depicting the financial position of the business with the

help of balance sheet. Another part of the project shall be including the calculations of the

various ratios reflecting the performance of the business and it shall be compared with that of the

competitors to conduct the comparative analysis.

MAIN BODY

PART A

b) Ledger accounts for the month of October 2020 of toy shop in Oxford:-

Bank A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

01/10/20 To Capital A/C 8000 02/10/20 By Laptop A/C 1000

05/10/20

To Inventory

A/C 1500 24/10/20 By Car A/C 2500

21/10/20

To Rent received

A/C 500 26/10/20 By Wages A/C 820

30/10/20 By Rent paid A/C 1000

31/10/20 By Drawings A/C 1600

31/10/20 By Balance c/d 3080

10000 10000

Cash A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS

J.F

. AMOUNT

01/10/20 To Capital A/C 5200 12/10/20 By Repairs A/C 80

23/10/20

To Inventory

A/C 1500 31/10/20 By Balance c/d 7120

23/10/20

To Inventory

A/C 500

7200 7200

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

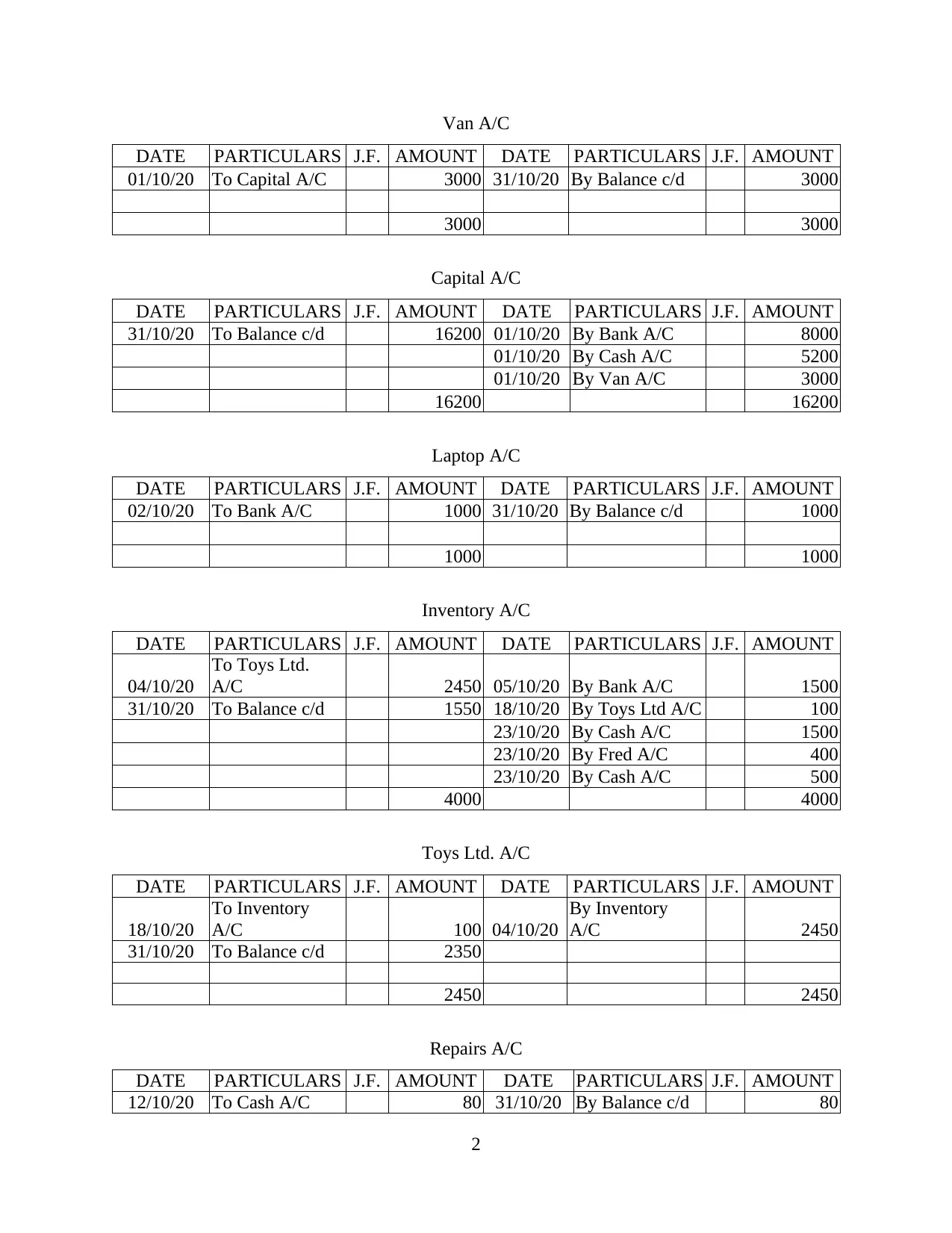

Van A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

01/10/20 To Capital A/C 3000 31/10/20 By Balance c/d 3000

3000 3000

Capital A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

31/10/20 To Balance c/d 16200 01/10/20 By Bank A/C 8000

01/10/20 By Cash A/C 5200

01/10/20 By Van A/C 3000

16200 16200

Laptop A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

02/10/20 To Bank A/C 1000 31/10/20 By Balance c/d 1000

1000 1000

Inventory A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

04/10/20

To Toys Ltd.

A/C 2450 05/10/20 By Bank A/C 1500

31/10/20 To Balance c/d 1550 18/10/20 By Toys Ltd A/C 100

23/10/20 By Cash A/C 1500

23/10/20 By Fred A/C 400

23/10/20 By Cash A/C 500

4000 4000

Toys Ltd. A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

18/10/20

To Inventory

A/C 100 04/10/20

By Inventory

A/C 2450

31/10/20 To Balance c/d 2350

2450 2450

Repairs A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

12/10/20 To Cash A/C 80 31/10/20 By Balance c/d 80

2

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

01/10/20 To Capital A/C 3000 31/10/20 By Balance c/d 3000

3000 3000

Capital A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

31/10/20 To Balance c/d 16200 01/10/20 By Bank A/C 8000

01/10/20 By Cash A/C 5200

01/10/20 By Van A/C 3000

16200 16200

Laptop A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

02/10/20 To Bank A/C 1000 31/10/20 By Balance c/d 1000

1000 1000

Inventory A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

04/10/20

To Toys Ltd.

A/C 2450 05/10/20 By Bank A/C 1500

31/10/20 To Balance c/d 1550 18/10/20 By Toys Ltd A/C 100

23/10/20 By Cash A/C 1500

23/10/20 By Fred A/C 400

23/10/20 By Cash A/C 500

4000 4000

Toys Ltd. A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

18/10/20

To Inventory

A/C 100 04/10/20

By Inventory

A/C 2450

31/10/20 To Balance c/d 2350

2450 2450

Repairs A/C

DATE PARTICULARS J.F. AMOUNT DATE PARTICULARS J.F. AMOUNT

12/10/20 To Cash A/C 80 31/10/20 By Balance c/d 80

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

80 80

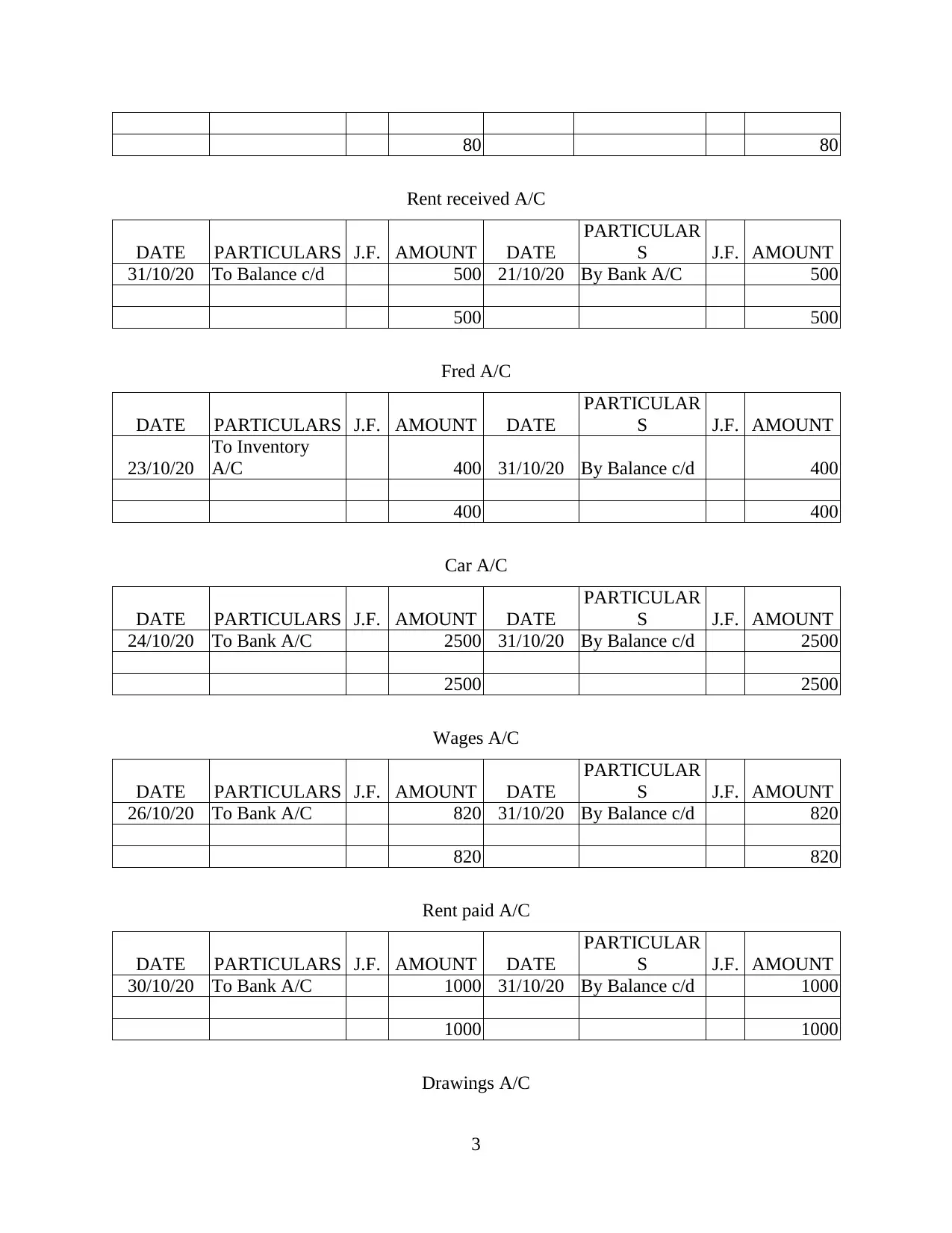

Rent received A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

31/10/20 To Balance c/d 500 21/10/20 By Bank A/C 500

500 500

Fred A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

23/10/20

To Inventory

A/C 400 31/10/20 By Balance c/d 400

400 400

Car A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

24/10/20 To Bank A/C 2500 31/10/20 By Balance c/d 2500

2500 2500

Wages A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

26/10/20 To Bank A/C 820 31/10/20 By Balance c/d 820

820 820

Rent paid A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

30/10/20 To Bank A/C 1000 31/10/20 By Balance c/d 1000

1000 1000

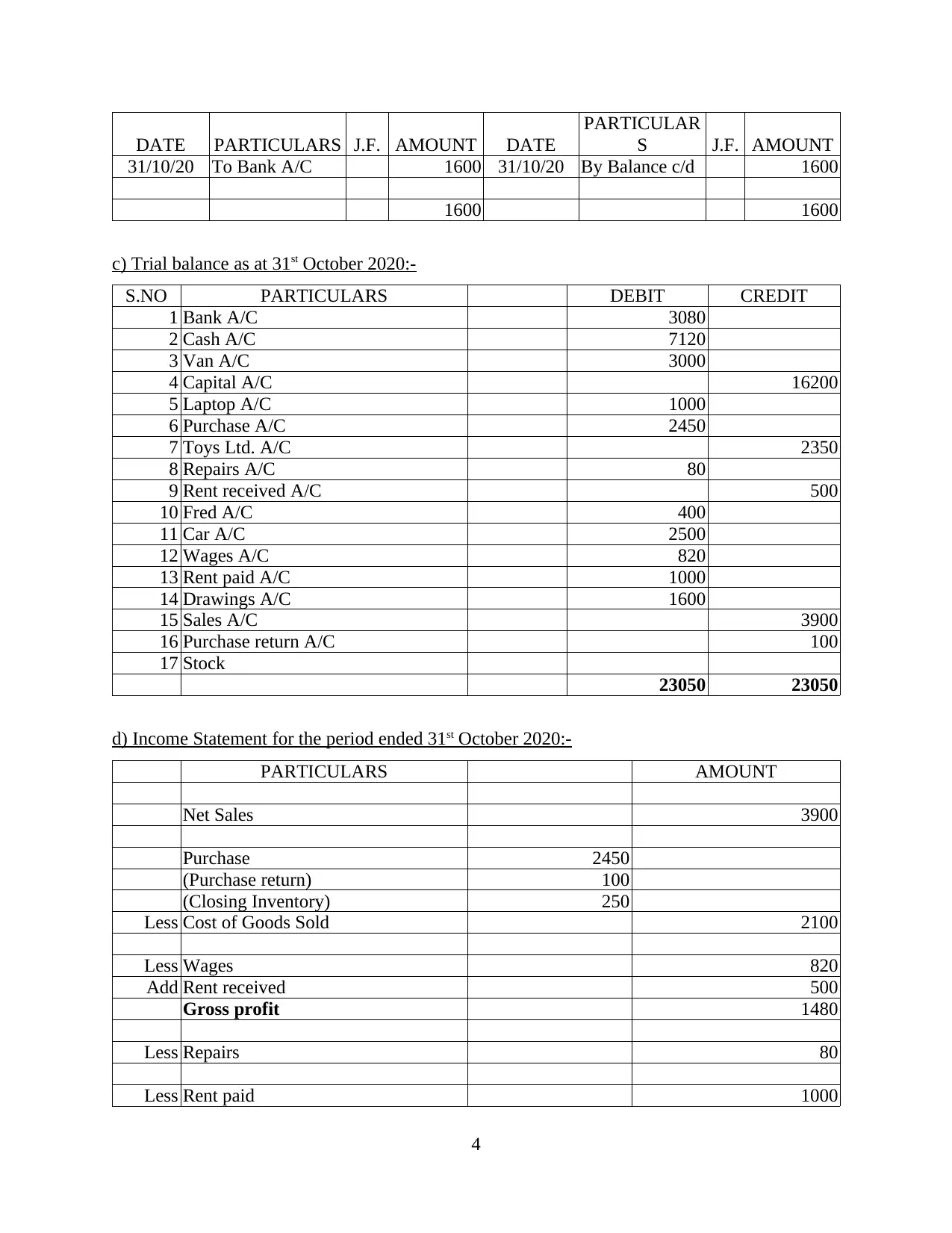

Drawings A/C

3

Rent received A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

31/10/20 To Balance c/d 500 21/10/20 By Bank A/C 500

500 500

Fred A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

23/10/20

To Inventory

A/C 400 31/10/20 By Balance c/d 400

400 400

Car A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

24/10/20 To Bank A/C 2500 31/10/20 By Balance c/d 2500

2500 2500

Wages A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

26/10/20 To Bank A/C 820 31/10/20 By Balance c/d 820

820 820

Rent paid A/C

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

30/10/20 To Bank A/C 1000 31/10/20 By Balance c/d 1000

1000 1000

Drawings A/C

3

DATE PARTICULARS J.F. AMOUNT DATE

PARTICULAR

S J.F. AMOUNT

31/10/20 To Bank A/C 1600 31/10/20 By Balance c/d 1600

1600 1600

c) Trial balance as at 31st October 2020:-

S.NO PARTICULARS DEBIT CREDIT

1 Bank A/C 3080

2 Cash A/C 7120

3 Van A/C 3000

4 Capital A/C 16200

5 Laptop A/C 1000

6 Purchase A/C 2450

7 Toys Ltd. A/C 2350

8 Repairs A/C 80

9 Rent received A/C 500

10 Fred A/C 400

11 Car A/C 2500

12 Wages A/C 820

13 Rent paid A/C 1000

14 Drawings A/C 1600

15 Sales A/C 3900

16 Purchase return A/C 100

17 Stock

23050 23050

d) Income Statement for the period ended 31st October 2020:-

PARTICULARS AMOUNT

Net Sales 3900

Purchase 2450

(Purchase return) 100

(Closing Inventory) 250

Less Cost of Goods Sold 2100

Less Wages 820

Add Rent received 500

Gross profit 1480

Less Repairs 80

Less Rent paid 1000

4

PARTICULAR

S J.F. AMOUNT

31/10/20 To Bank A/C 1600 31/10/20 By Balance c/d 1600

1600 1600

c) Trial balance as at 31st October 2020:-

S.NO PARTICULARS DEBIT CREDIT

1 Bank A/C 3080

2 Cash A/C 7120

3 Van A/C 3000

4 Capital A/C 16200

5 Laptop A/C 1000

6 Purchase A/C 2450

7 Toys Ltd. A/C 2350

8 Repairs A/C 80

9 Rent received A/C 500

10 Fred A/C 400

11 Car A/C 2500

12 Wages A/C 820

13 Rent paid A/C 1000

14 Drawings A/C 1600

15 Sales A/C 3900

16 Purchase return A/C 100

17 Stock

23050 23050

d) Income Statement for the period ended 31st October 2020:-

PARTICULARS AMOUNT

Net Sales 3900

Purchase 2450

(Purchase return) 100

(Closing Inventory) 250

Less Cost of Goods Sold 2100

Less Wages 820

Add Rent received 500

Gross profit 1480

Less Repairs 80

Less Rent paid 1000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Profit 400

e) Statement of Financial Position as at 31st October 2020:-

£ £

ASSETS LIABILITIES

Current Assets Current Liabilities

Bank 3080 Toys Ltd. 2350

Cash 7120

Stock 250 Non- current liabilities

Fred 400 Capital 16200

Drawings 1600

Fixed Assets Profit 400

Van 3000 15000

Laptop 1000

Car 2500

Total Assets 17350 Total Liabilities 17350

The trial balance of the company is used to check the balances of the accounts at the end of the

year. The debit and credit side of the trial balance matches.

The income statement of the company shows the profitability of the company.

The balance sheet shows the financial position of the company.

f) Meaning of drawings account:-

Drawings are the types of accounts which shows the money or the asset that is withdrawn

by the owner of the business for personal use (Chow and Schoenbaum, 2020). The expenses by

the owner apart from the business purpose are treated as drawings. This amount is further

deducted from the capital in the balance sheet which has been brought in the business by the

owner. As the concept of separate legal entity justifies that the owners and the business are two

separate persons, so the amount withdrawn from the business for private use cannot be an

expense for the business. This account work yearly wherein the previous years balance is

adjusted in the owners equity and next year a separate account is opened (Warren, Jonick and

Schneider, 2020).

5

e) Statement of Financial Position as at 31st October 2020:-

£ £

ASSETS LIABILITIES

Current Assets Current Liabilities

Bank 3080 Toys Ltd. 2350

Cash 7120

Stock 250 Non- current liabilities

Fred 400 Capital 16200

Drawings 1600

Fixed Assets Profit 400

Van 3000 15000

Laptop 1000

Car 2500

Total Assets 17350 Total Liabilities 17350

The trial balance of the company is used to check the balances of the accounts at the end of the

year. The debit and credit side of the trial balance matches.

The income statement of the company shows the profitability of the company.

The balance sheet shows the financial position of the company.

f) Meaning of drawings account:-

Drawings are the types of accounts which shows the money or the asset that is withdrawn

by the owner of the business for personal use (Chow and Schoenbaum, 2020). The expenses by

the owner apart from the business purpose are treated as drawings. This amount is further

deducted from the capital in the balance sheet which has been brought in the business by the

owner. As the concept of separate legal entity justifies that the owners and the business are two

separate persons, so the amount withdrawn from the business for private use cannot be an

expense for the business. This account work yearly wherein the previous years balance is

adjusted in the owners equity and next year a separate account is opened (Warren, Jonick and

Schneider, 2020).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In this business Linda is the owner of the toy shop who has taken a week long holiday in Florida

and pays the expenses from the bank account of the business. And the expense is made in order

to relieve the stress of the business. This amount shall be considered as Linda's drawings from

the business and cannot be considered as the business expense. Since the holiday is taken for

personal purposes and is not related to the business operations it cannot be debited to the expense

account. Indeed, it has to be deducted from the capital account of Linda at the end of the year.

In the above financial statements of the business the effect of the drawings can be seen. A

separate ledger is prepared to post the drawings made by the owner of the business. Apart from

that it is being deducted in the liability side of the balance sheet where owners equity is

mentioned (Dai and Vasarhelyi, 2017).

PART B

i) Calculation of ratios:-

Net Profit 400

Sales 3900

1 NET PROFIT MARGIN Net Profit / Sales *100

10.2564

102564

Gross Profit 980

Sales 3900

2 GROSS PROFIT MARGIN Gross Profit / Sales *100

25.1282

051282

Current Assets 10850

Current Liabilities 2350

3 CURRENT RATIO

Current Assets / Current

Liabilities

4.61702

12766

Current Assets 10850

Inventory 250

Current Liabilities 2350

4 ACID TEST RATIO

Current Assets – Inventory /

Current Liabilities

4.51063

82979

Accounts Receivable 400

Sales 3900

5

ACCOUNTS RECEIVABLE

COLLECTION PERIOD

Accounts Receivable / Sales

*365

37.4358

974359

Accounts Payable 2350

6

and pays the expenses from the bank account of the business. And the expense is made in order

to relieve the stress of the business. This amount shall be considered as Linda's drawings from

the business and cannot be considered as the business expense. Since the holiday is taken for

personal purposes and is not related to the business operations it cannot be debited to the expense

account. Indeed, it has to be deducted from the capital account of Linda at the end of the year.

In the above financial statements of the business the effect of the drawings can be seen. A

separate ledger is prepared to post the drawings made by the owner of the business. Apart from

that it is being deducted in the liability side of the balance sheet where owners equity is

mentioned (Dai and Vasarhelyi, 2017).

PART B

i) Calculation of ratios:-

Net Profit 400

Sales 3900

1 NET PROFIT MARGIN Net Profit / Sales *100

10.2564

102564

Gross Profit 980

Sales 3900

2 GROSS PROFIT MARGIN Gross Profit / Sales *100

25.1282

051282

Current Assets 10850

Current Liabilities 2350

3 CURRENT RATIO

Current Assets / Current

Liabilities

4.61702

12766

Current Assets 10850

Inventory 250

Current Liabilities 2350

4 ACID TEST RATIO

Current Assets – Inventory /

Current Liabilities

4.51063

82979

Accounts Receivable 400

Sales 3900

5

ACCOUNTS RECEIVABLE

COLLECTION PERIOD

Accounts Receivable / Sales

*365

37.4358

974359

Accounts Payable 2350

6

Sales 3900

6

ACCOUNTS PAYABLE PAYMENT

PERIOD Accounts Payable / Sales *365

219.935

8974359

ii) Comparison of ratios:-

Ratios are the effective tools that are used to facilitate comparison of the business either

with its past performance or with that of the competitors. The financial status of the company can

be known by comparing any two elements of the business and based on that calculating the

ratios.

Ratio is used to analyse the profitability of company for measuring the results of carrying

out the business. The net profit margin of company is 10.25% where of the competitors is 31%

and it shows that the ratio of company is very low from the industry standards. Lower net profit

means that existing strategies and policies of the company are not effective and also not helping

it to derive the adequate profits from the business (Christensen, Cottrell and Budd, 2016). It is

required that it analyses the current scenarios so that it could frame more effective policies that

will help it to increase the profits. Lower profit margins will affect the confidence of investors in

company and they will tend to move towards competitors giving higher returns.

Gross profit margin reflects the efficiency of management in earning adequate margins

from the main business. It includes trading and manufacturing costs and expenses. Gross margin

should be higher so that company has enough money to carry out the further expenses of the

business. The gross margin of competitors is 54% where of company is 25% only which is very

low (Easton and et.al. 2018). It could be evaluated from the ratio that management is required to

implement more cost effective strategies that will help to increase the gross margins. It is also

required to increase the sales so that it has adequate funds to meet the expenses of business. It

could increase the gross profits by undertaking cost control measures and also adopting

promotional measures that will increase he sales of company.

Current ratio- The current ratio of the business shall be depicting its capacity to pay the

short term obligations of the company (Palepu and et.al. 2020). It shall be comparing the current

assets with the current liabilities with which the liquidity position of the business in the period of

one year shall be seen. The current ratio of the toy business is very good as its current assets are

7

6

ACCOUNTS PAYABLE PAYMENT

PERIOD Accounts Payable / Sales *365

219.935

8974359

ii) Comparison of ratios:-

Ratios are the effective tools that are used to facilitate comparison of the business either

with its past performance or with that of the competitors. The financial status of the company can

be known by comparing any two elements of the business and based on that calculating the

ratios.

Ratio is used to analyse the profitability of company for measuring the results of carrying

out the business. The net profit margin of company is 10.25% where of the competitors is 31%

and it shows that the ratio of company is very low from the industry standards. Lower net profit

means that existing strategies and policies of the company are not effective and also not helping

it to derive the adequate profits from the business (Christensen, Cottrell and Budd, 2016). It is

required that it analyses the current scenarios so that it could frame more effective policies that

will help it to increase the profits. Lower profit margins will affect the confidence of investors in

company and they will tend to move towards competitors giving higher returns.

Gross profit margin reflects the efficiency of management in earning adequate margins

from the main business. It includes trading and manufacturing costs and expenses. Gross margin

should be higher so that company has enough money to carry out the further expenses of the

business. The gross margin of competitors is 54% where of company is 25% only which is very

low (Easton and et.al. 2018). It could be evaluated from the ratio that management is required to

implement more cost effective strategies that will help to increase the gross margins. It is also

required to increase the sales so that it has adequate funds to meet the expenses of business. It

could increase the gross profits by undertaking cost control measures and also adopting

promotional measures that will increase he sales of company.

Current ratio- The current ratio of the business shall be depicting its capacity to pay the

short term obligations of the company (Palepu and et.al. 2020). It shall be comparing the current

assets with the current liabilities with which the liquidity position of the business in the period of

one year shall be seen. The current ratio of the toy business is very good as its current assets are

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4.6 times the amount of its liabilities. In comparison to the competitor also its liquidity position

is better than its current ratio is almost double from that of the competitor (AREAS, 2018).

Acid test ratio- Acid test ratio of the business shall be measuring the highly liquid assets

that the company has to meet its liabilities within one year. The highly liquid assets shall include

the assets which are money or equivalent to the money. It shall not include the stock and the

prepaid expenses. The toy business is highly liquid and efficient as its acid test ratio proves that

it has liquid assets up-to 4.5 times than the short term liabilities. It has excess funds and can

employ them in other activities (Marsha and Murtaqi, 2017). Also, it can be said that the

liquidity position can be a competitive edge over the competitor whose acid test ratio is just 1.35.

Accounts receivable collection period shows the time taken to collect the amount from

the debtors of the business to whom goods were sold on credit. The lesser such time is the better

it is for the company as they shall receive money soon and can employ in the business working

cycle to get benefited from it (Abolfathi and Taebi, 2020). The business takes 37 days to recover

its debts whereas its competitor takes 50 days for the same.

Accounts payable payment period shows the time taken to payback the creditors from

whom we have purchased goods on credit. The higher such time the better it is for the business

as we get leverage in making the payments. The company has very high payable period of 220

days and the competitor has it only for 72 days.

CONCLUSION

The project concludes that the preparation of the financial statements of the company in

order the ascertain its profitability, position and the future growth prospects. Such financial

statements prove to be very crucial for the stakeholders of the business like the owners,

managers, investors, customers, creditors and the government bodies. These stakeholders use

these financial statements to analyse and make decisions. The report depicts the complete

process of accounting wherein firstly journal is prepared and based on that ledger posting and the

trial balance is formed. Post this preparation the profitability shall be known by the income

statement and the financial position shall be known by the balance sheet of the company. To

analyse the position in comparison with other competitors ratios are calculated and the

inefficiencies are known.

8

is better than its current ratio is almost double from that of the competitor (AREAS, 2018).

Acid test ratio- Acid test ratio of the business shall be measuring the highly liquid assets

that the company has to meet its liabilities within one year. The highly liquid assets shall include

the assets which are money or equivalent to the money. It shall not include the stock and the

prepaid expenses. The toy business is highly liquid and efficient as its acid test ratio proves that

it has liquid assets up-to 4.5 times than the short term liabilities. It has excess funds and can

employ them in other activities (Marsha and Murtaqi, 2017). Also, it can be said that the

liquidity position can be a competitive edge over the competitor whose acid test ratio is just 1.35.

Accounts receivable collection period shows the time taken to collect the amount from

the debtors of the business to whom goods were sold on credit. The lesser such time is the better

it is for the company as they shall receive money soon and can employ in the business working

cycle to get benefited from it (Abolfathi and Taebi, 2020). The business takes 37 days to recover

its debts whereas its competitor takes 50 days for the same.

Accounts payable payment period shows the time taken to payback the creditors from

whom we have purchased goods on credit. The higher such time the better it is for the business

as we get leverage in making the payments. The company has very high payable period of 220

days and the competitor has it only for 72 days.

CONCLUSION

The project concludes that the preparation of the financial statements of the company in

order the ascertain its profitability, position and the future growth prospects. Such financial

statements prove to be very crucial for the stakeholders of the business like the owners,

managers, investors, customers, creditors and the government bodies. These stakeholders use

these financial statements to analyse and make decisions. The report depicts the complete

process of accounting wherein firstly journal is prepared and based on that ledger posting and the

trial balance is formed. Post this preparation the profitability shall be known by the income

statement and the financial position shall be known by the balance sheet of the company. To

analyse the position in comparison with other competitors ratios are calculated and the

inefficiencies are known.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abolfathi, E. and Taebi, P., 2020. Modern Analysis of Financial Statements: Pharmaceutical

companies in Iran. Journal of management and accounting studies. 8(2).

AREAS, B., 2018. Financial analysis. growth, 30, p.10.

Chow, D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Christensen, T. E., Cottrell, D. M. and Budd, C., 2016. Advanced financial accounting. NY

McGraw-Hill/ Irwin,.

Dai, J. and Vasarhelyi, M. A., 2017. Toward blockchain-based accounting and

assurance. Journal of Information Systems. 31(3). pp.5-21.

Easton, P. D. and et.al. 2018. Financial statement analysis & valuation. Boston, MA: Cambridge

Business Publishers.

Marsha, N. and Murtaqi, I., 2017. The effect of financial ratios on firm value in the food and

beverage sector of the IDX. Journal of Business and Management, 6(2), pp.214-226.

Palepu, K. G. and et.al. 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

9

Books and Journals

Abolfathi, E. and Taebi, P., 2020. Modern Analysis of Financial Statements: Pharmaceutical

companies in Iran. Journal of management and accounting studies. 8(2).

AREAS, B., 2018. Financial analysis. growth, 30, p.10.

Chow, D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Christensen, T. E., Cottrell, D. M. and Budd, C., 2016. Advanced financial accounting. NY

McGraw-Hill/ Irwin,.

Dai, J. and Vasarhelyi, M. A., 2017. Toward blockchain-based accounting and

assurance. Journal of Information Systems. 31(3). pp.5-21.

Easton, P. D. and et.al. 2018. Financial statement analysis & valuation. Boston, MA: Cambridge

Business Publishers.

Marsha, N. and Murtaqi, I., 2017. The effect of financial ratios on firm value in the food and

beverage sector of the IDX. Journal of Business and Management, 6(2), pp.214-226.

Palepu, K. G. and et.al. 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.