Recording Business Transactions: Impact of COVID-19 Analysis

VerifiedAdded on 2023/01/03

|15

|2615

|25

Homework Assignment

AI Summary

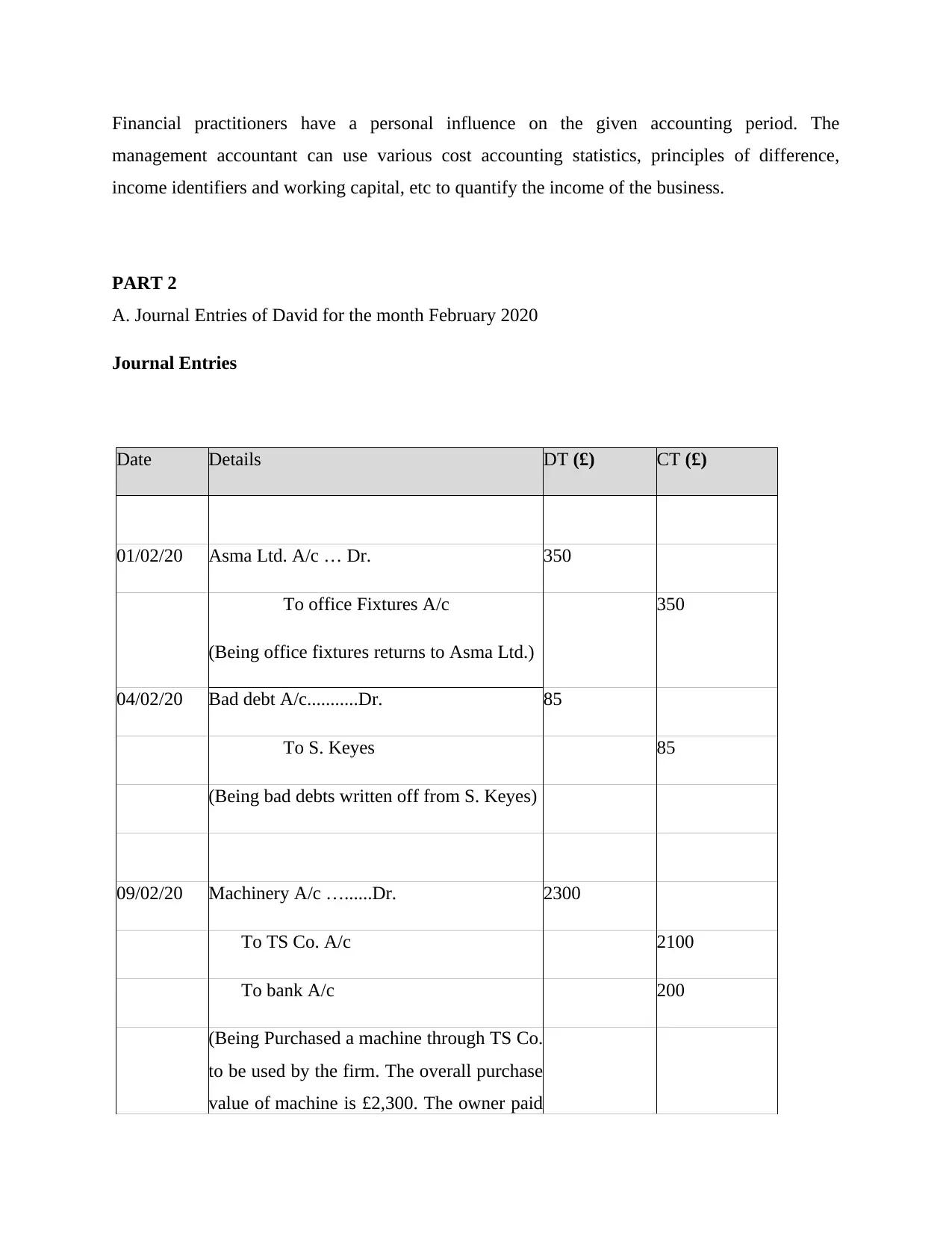

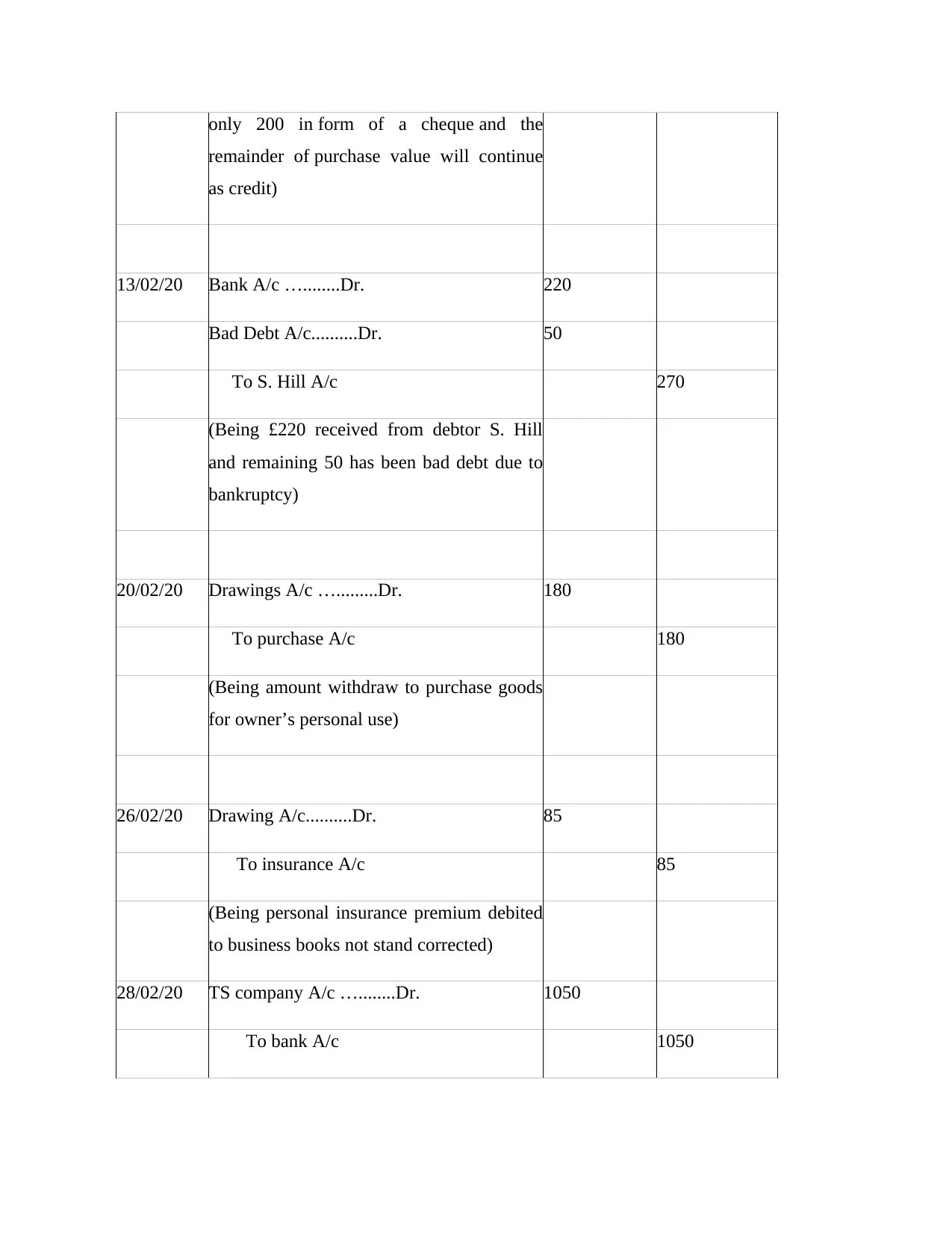

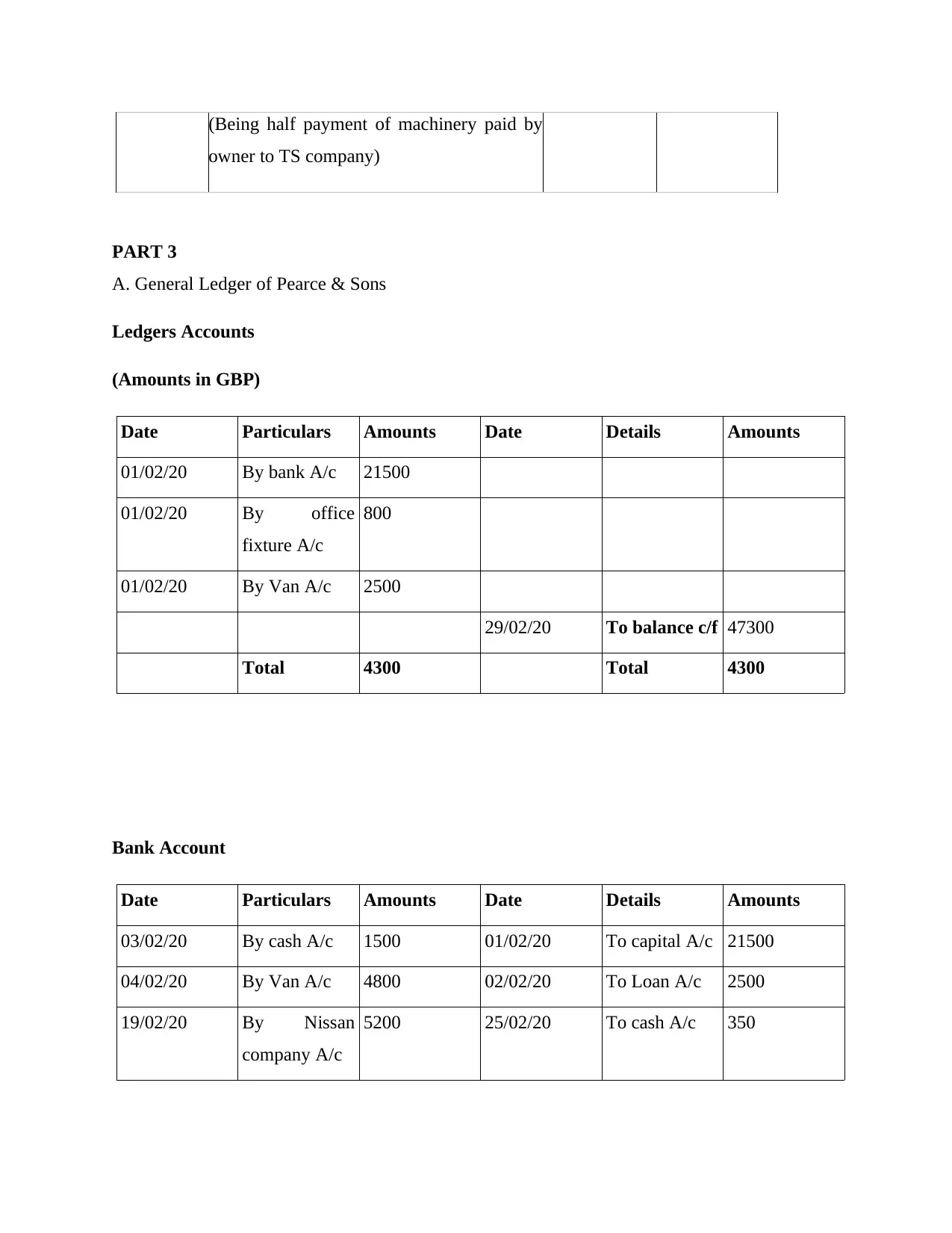

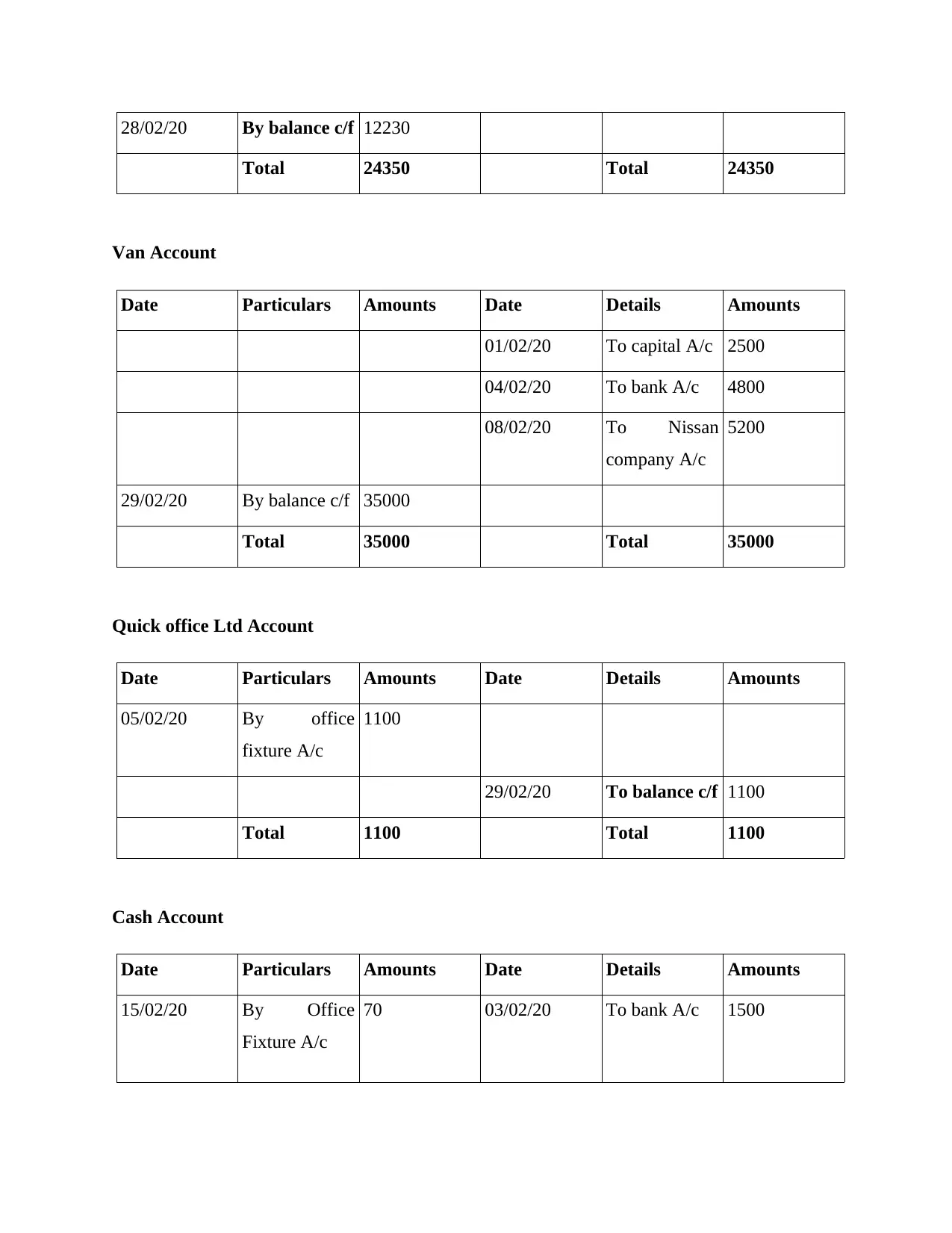

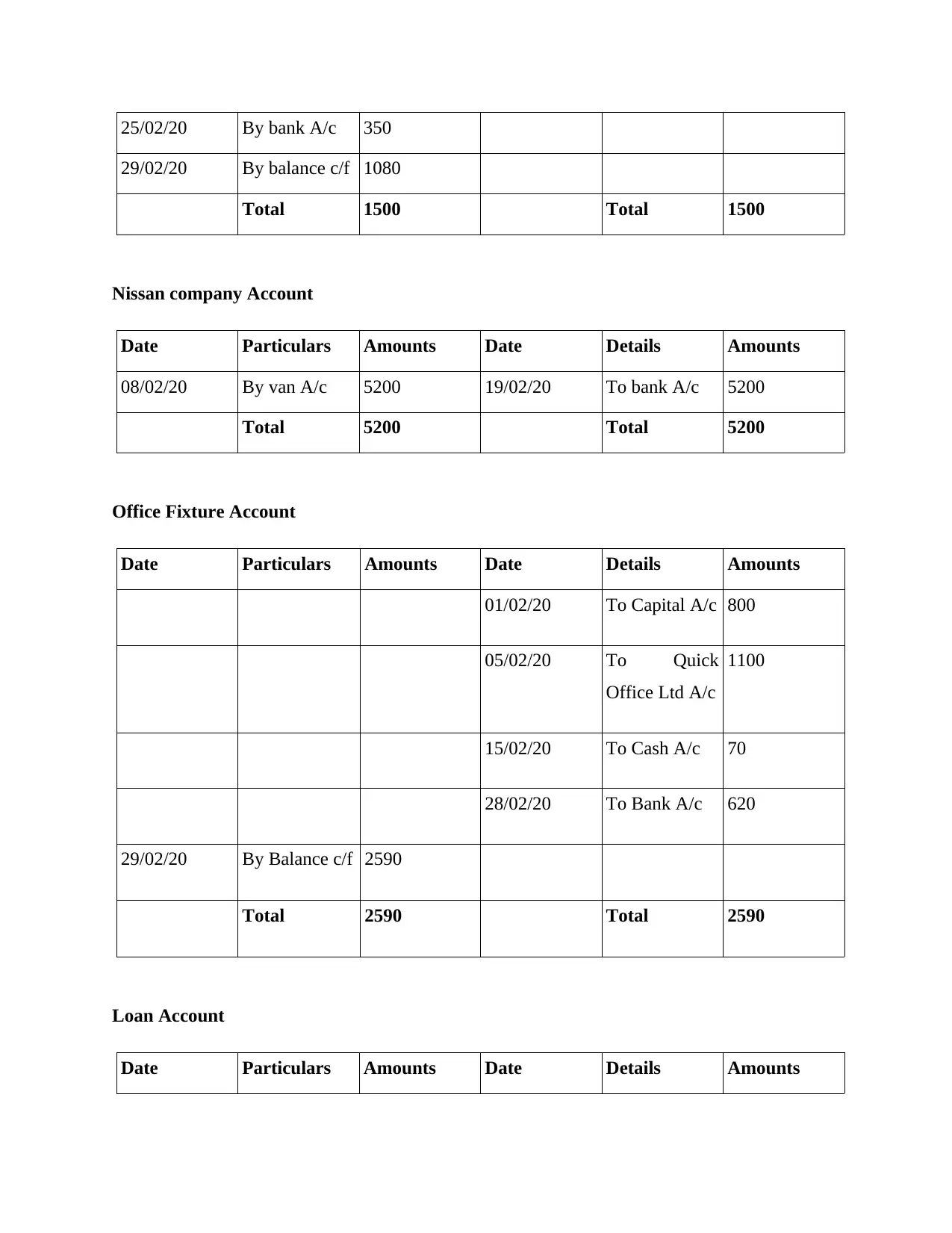

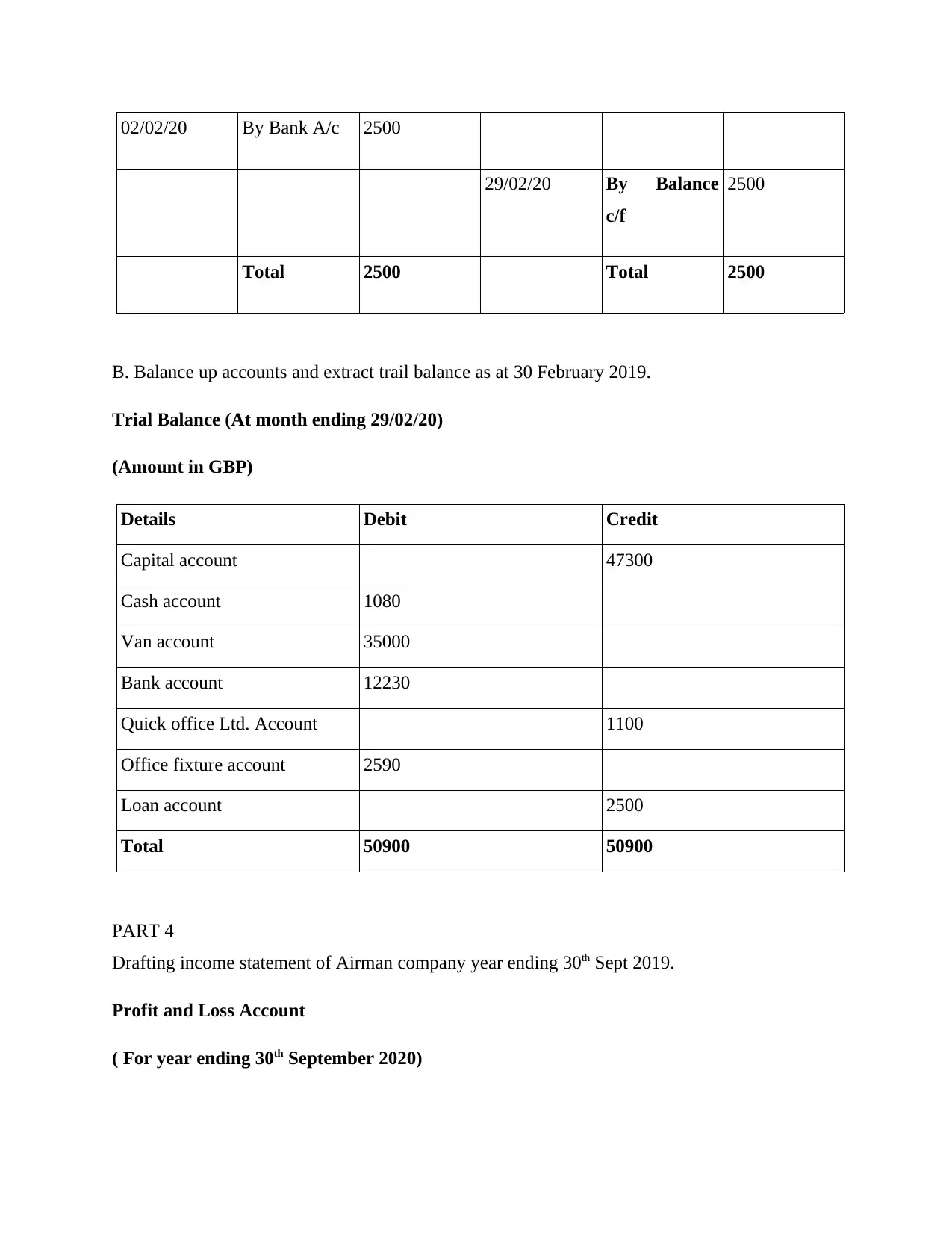

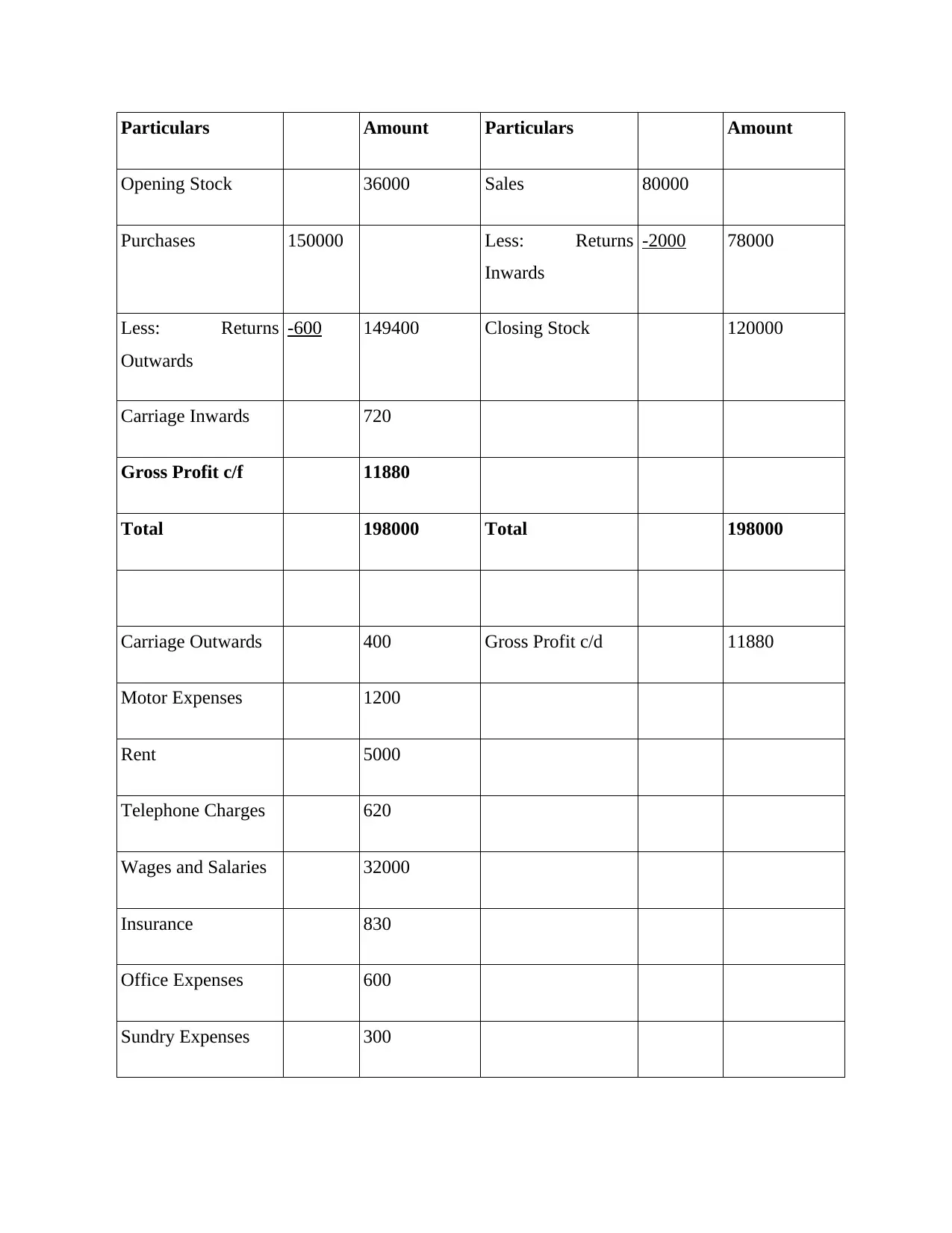

This assignment delves into the core principles of financial accounting, focusing on the meticulous process of recording business transactions. It begins with an introduction to the concept of accounting and its significance in financial reporting, followed by an exploration of the decision-makers who rely on accounting information and their specific needs. The assignment then presents a detailed examination of journal entries, general ledgers, and trial balances, using examples to illustrate the practical application of these accounting tools. Furthermore, the assignment covers the preparation of an income statement and concludes with an insightful analysis of the impact of the COVID-19 pandemic on financial statements, highlighting the challenges and considerations businesses faced during this period. The solution provides a comprehensive understanding of accounting principles and their practical application in analyzing business performance and financial decision-making.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.