Business Transactions and Financial Ratio Analysis Report

VerifiedAdded on 2023/01/03

|15

|2122

|32

Report

AI Summary

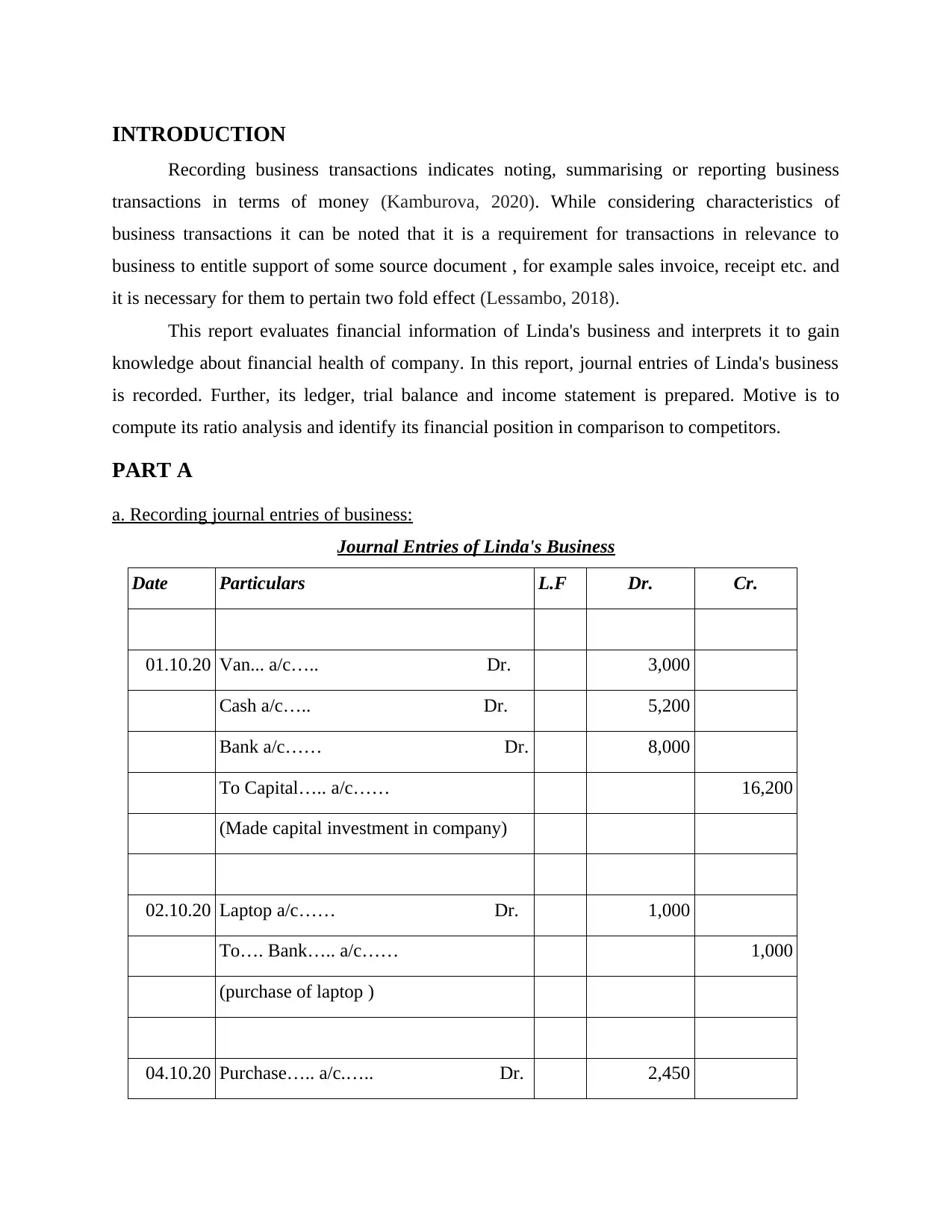

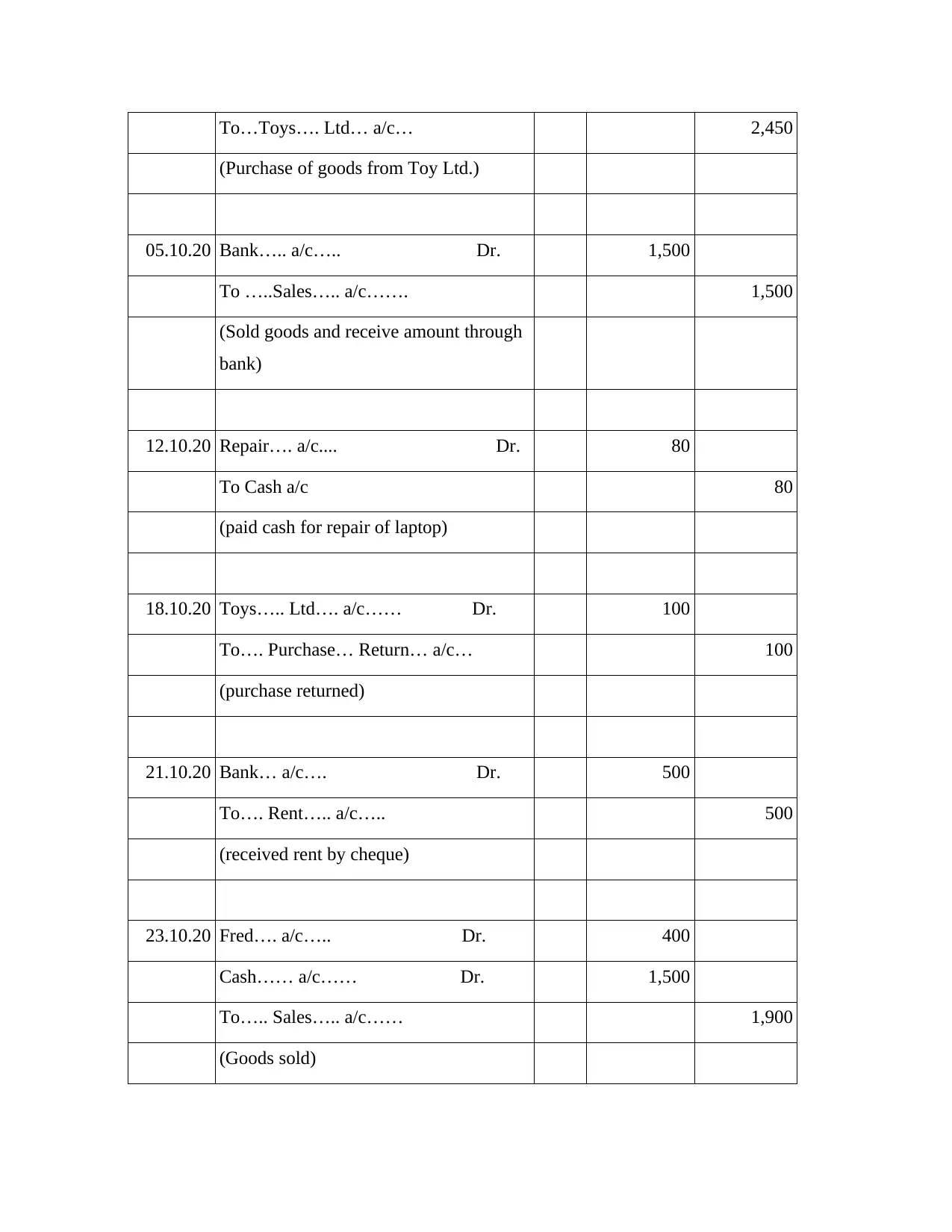

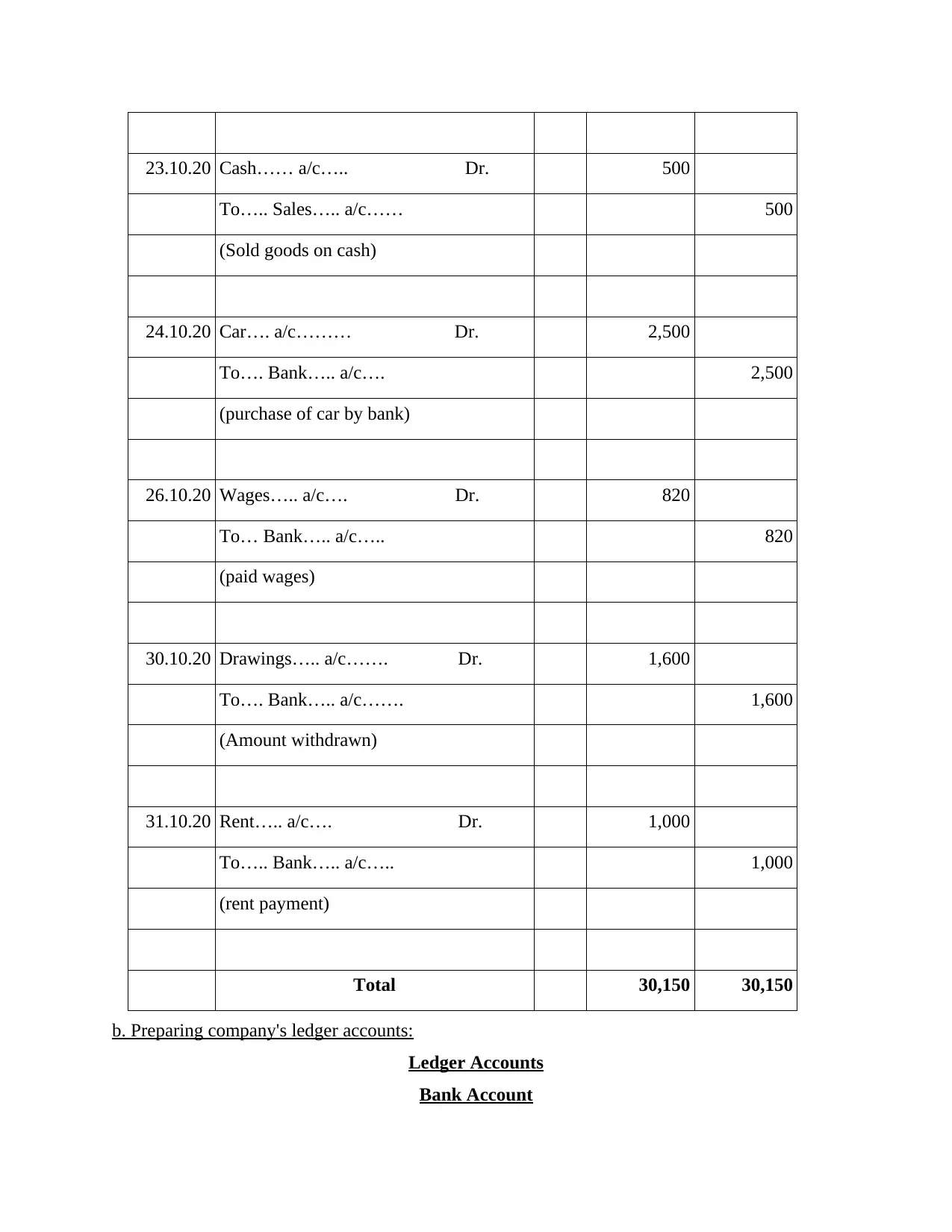

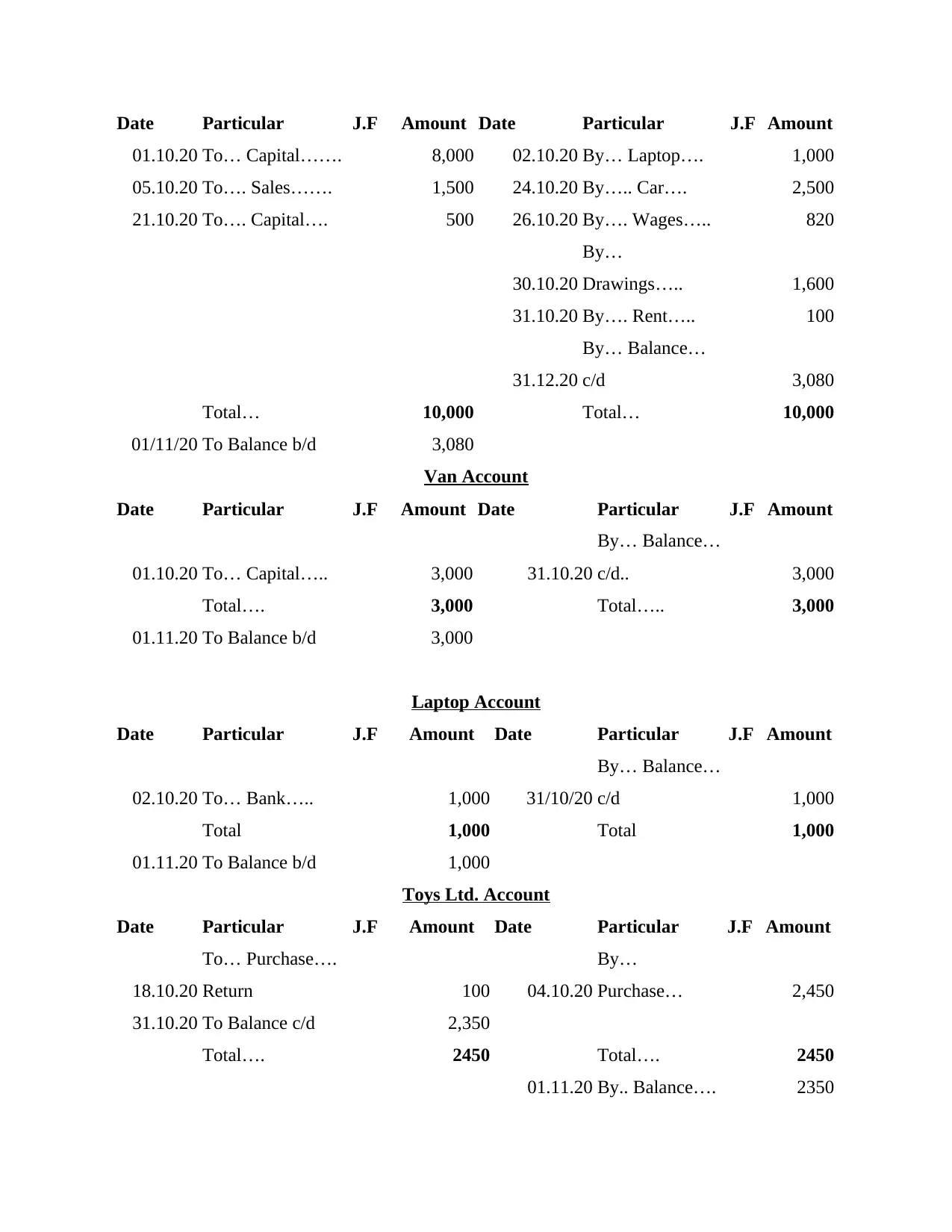

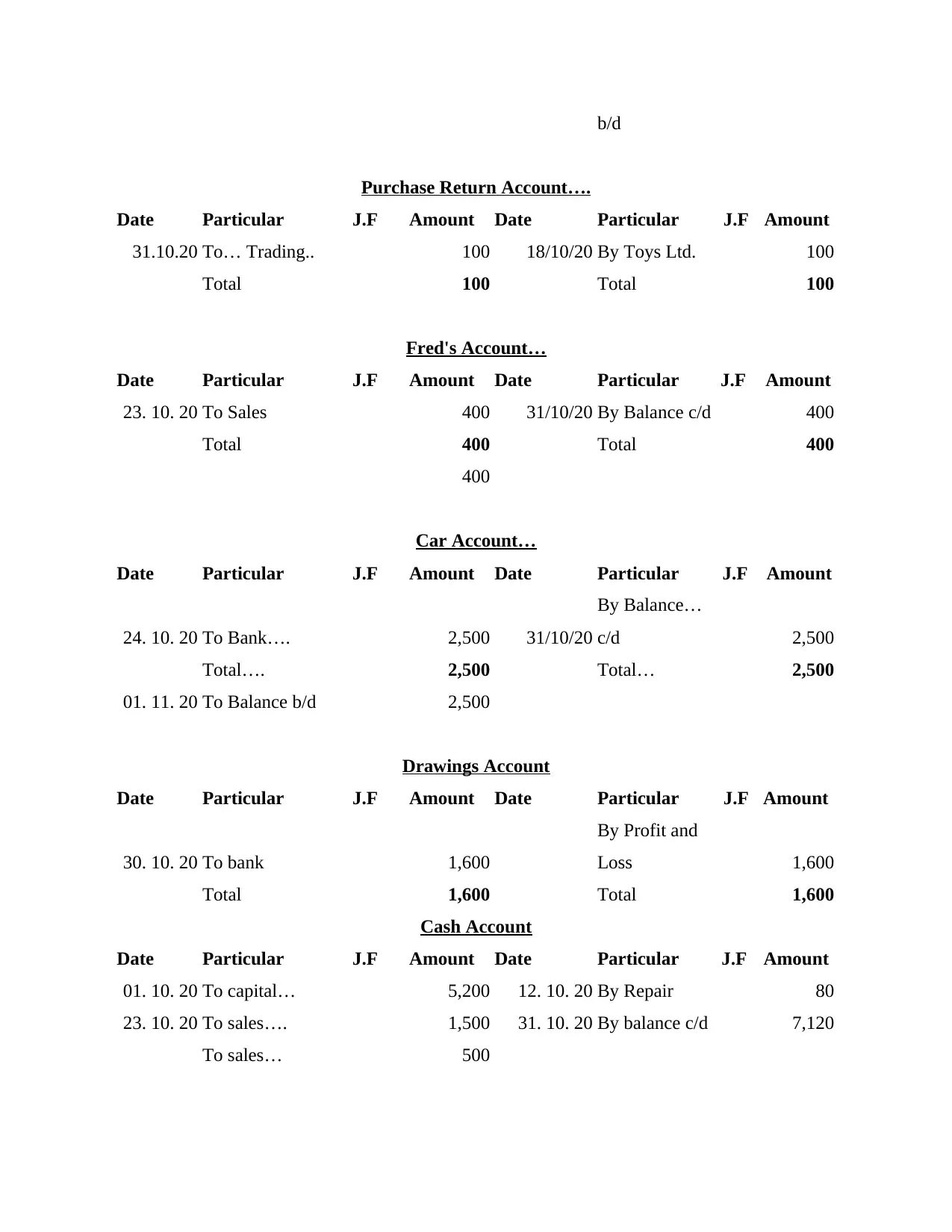

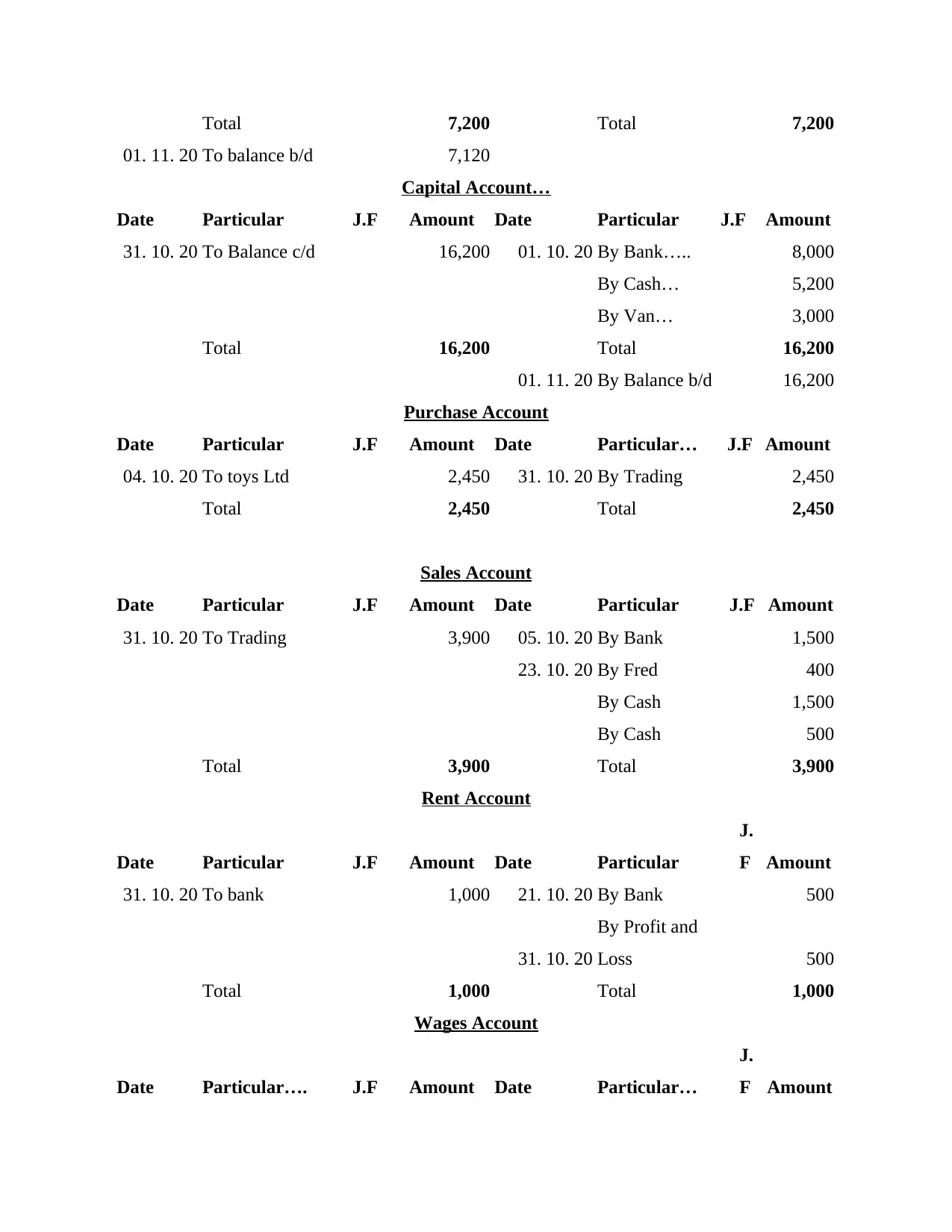

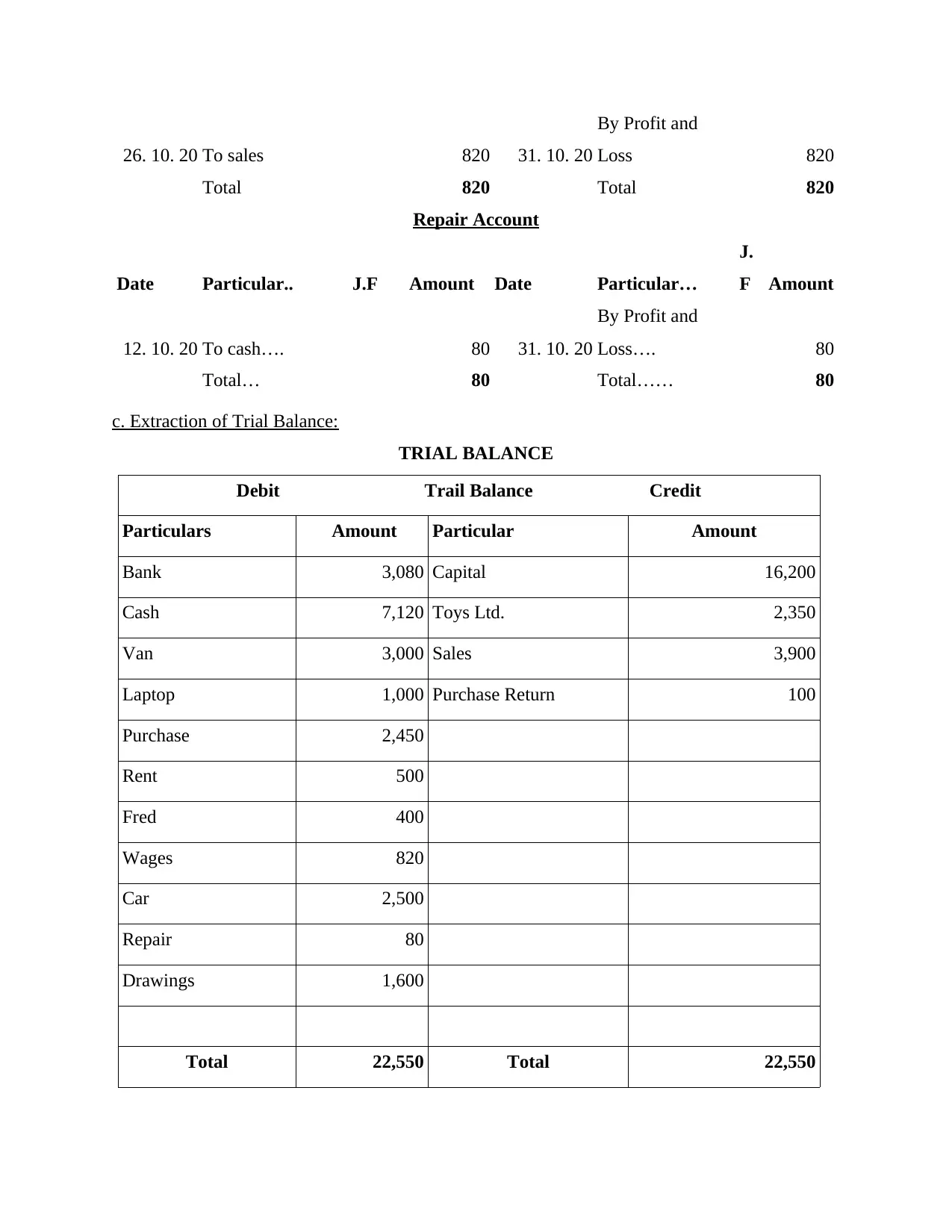

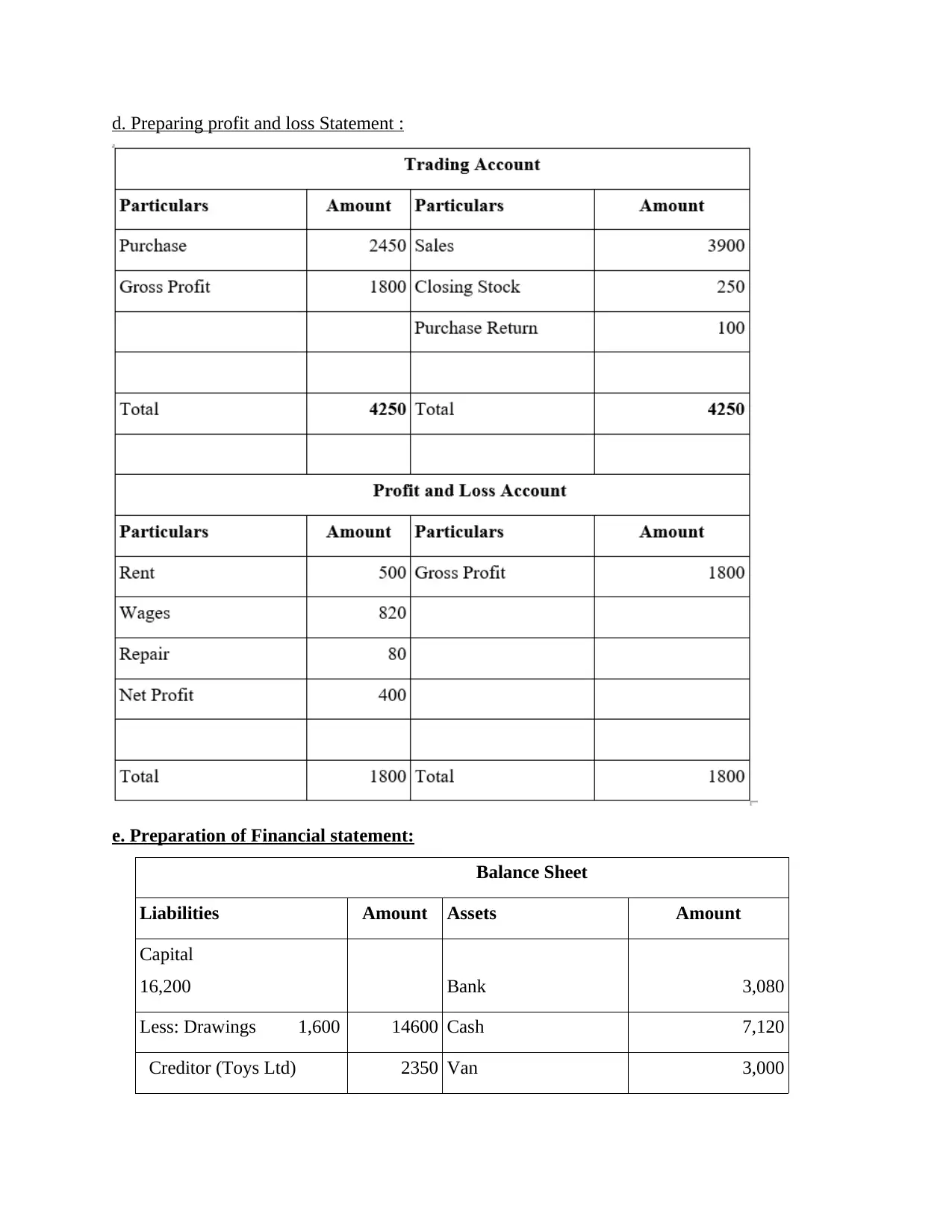

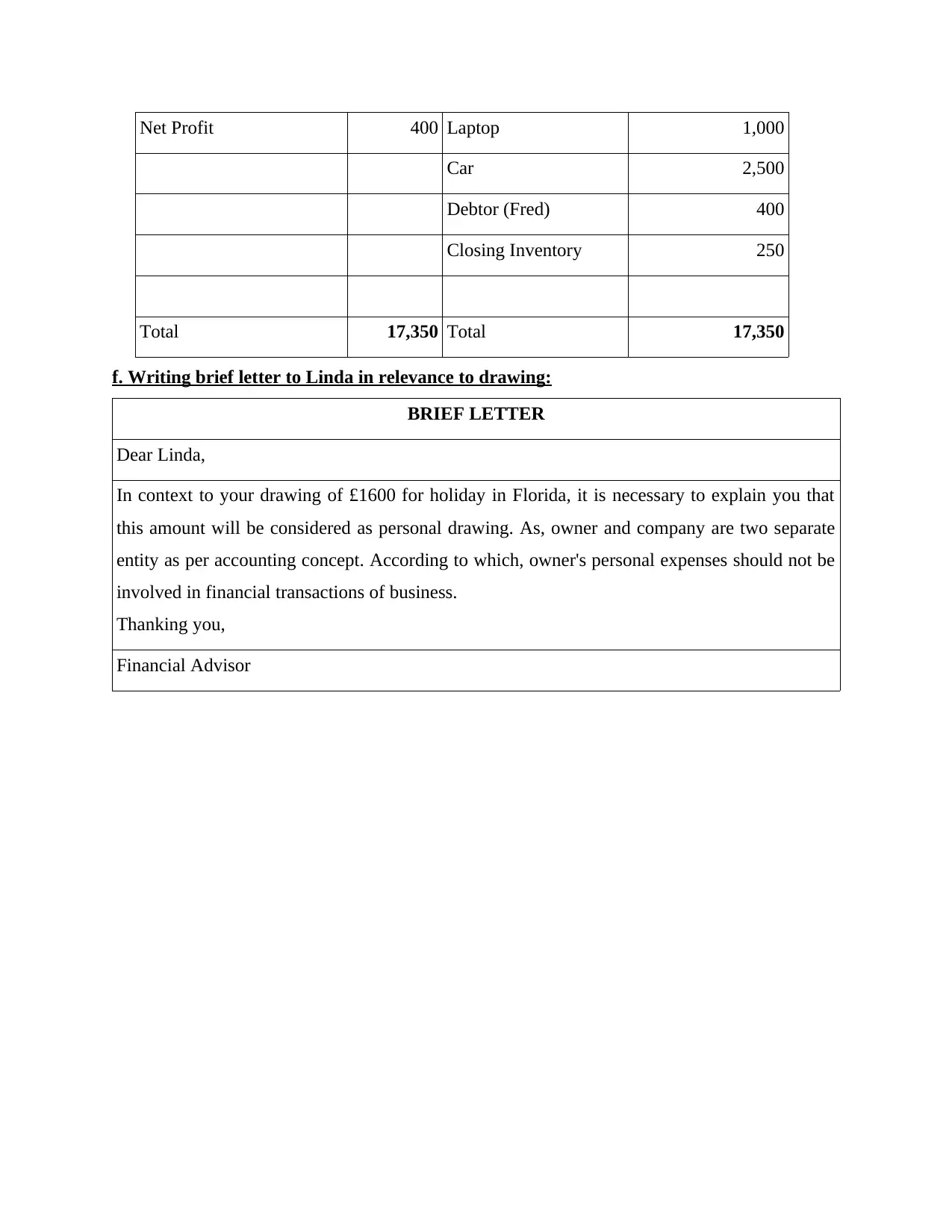

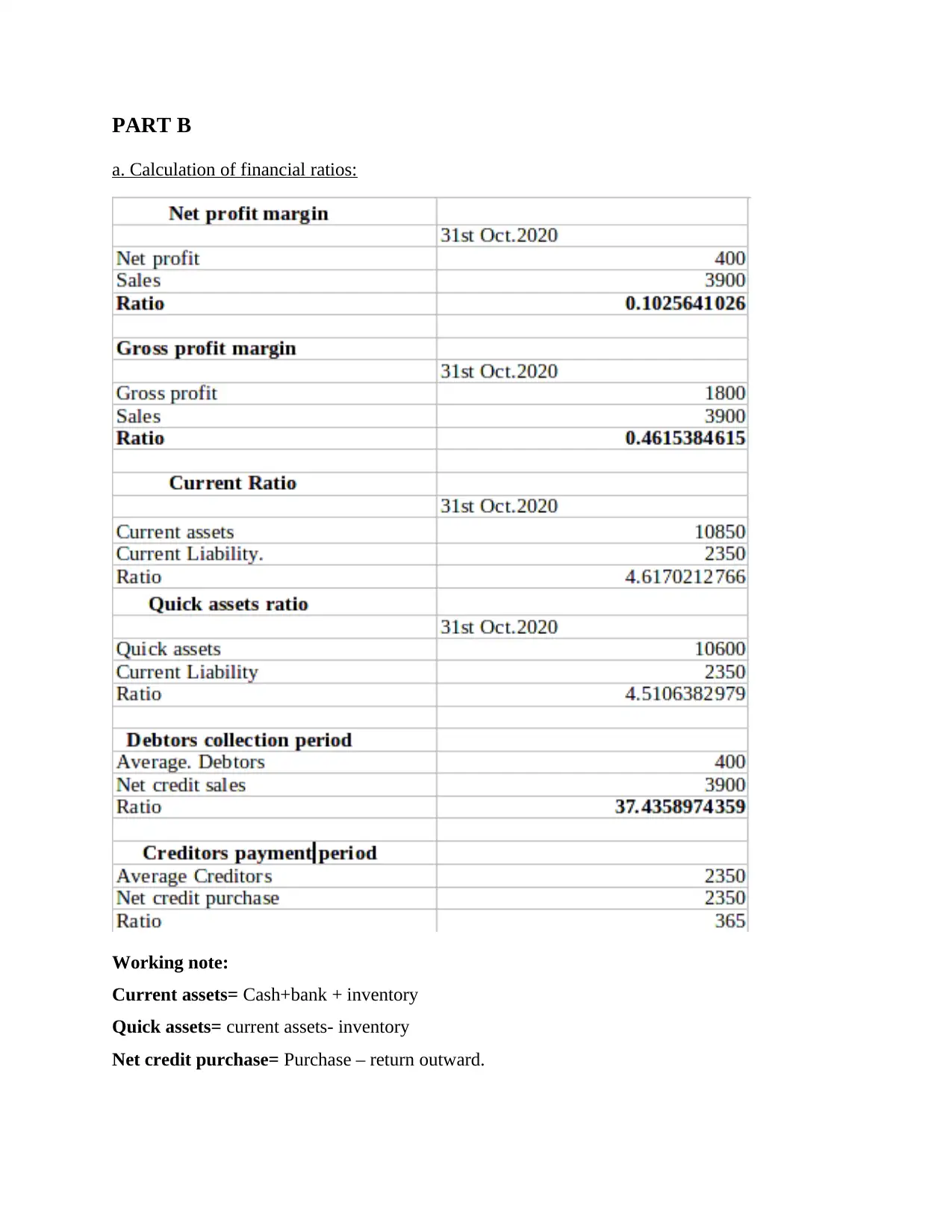

This report provides a comprehensive financial analysis of Linda's business, beginning with the recording of business transactions through journal entries, the creation of ledger accounts, and the extraction of a trial balance. The report then details the preparation of an income statement and balance sheet, presenting a clear view of the company's financial position. Furthermore, it delves into financial ratio analysis, calculating and interpreting key ratios to assess the company's performance, liquidity, and efficiency, comparing it to competitors. The report also includes a letter to Linda explaining the accounting treatment of personal drawings. The conclusion summarizes the findings, emphasizing the importance of financial reporting and analysis for informed decision-making.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.