Report on Business Transactions, Accounting Ledgers and Ratios

VerifiedAdded on 2023/06/15

|15

|1857

|173

Report

AI Summary

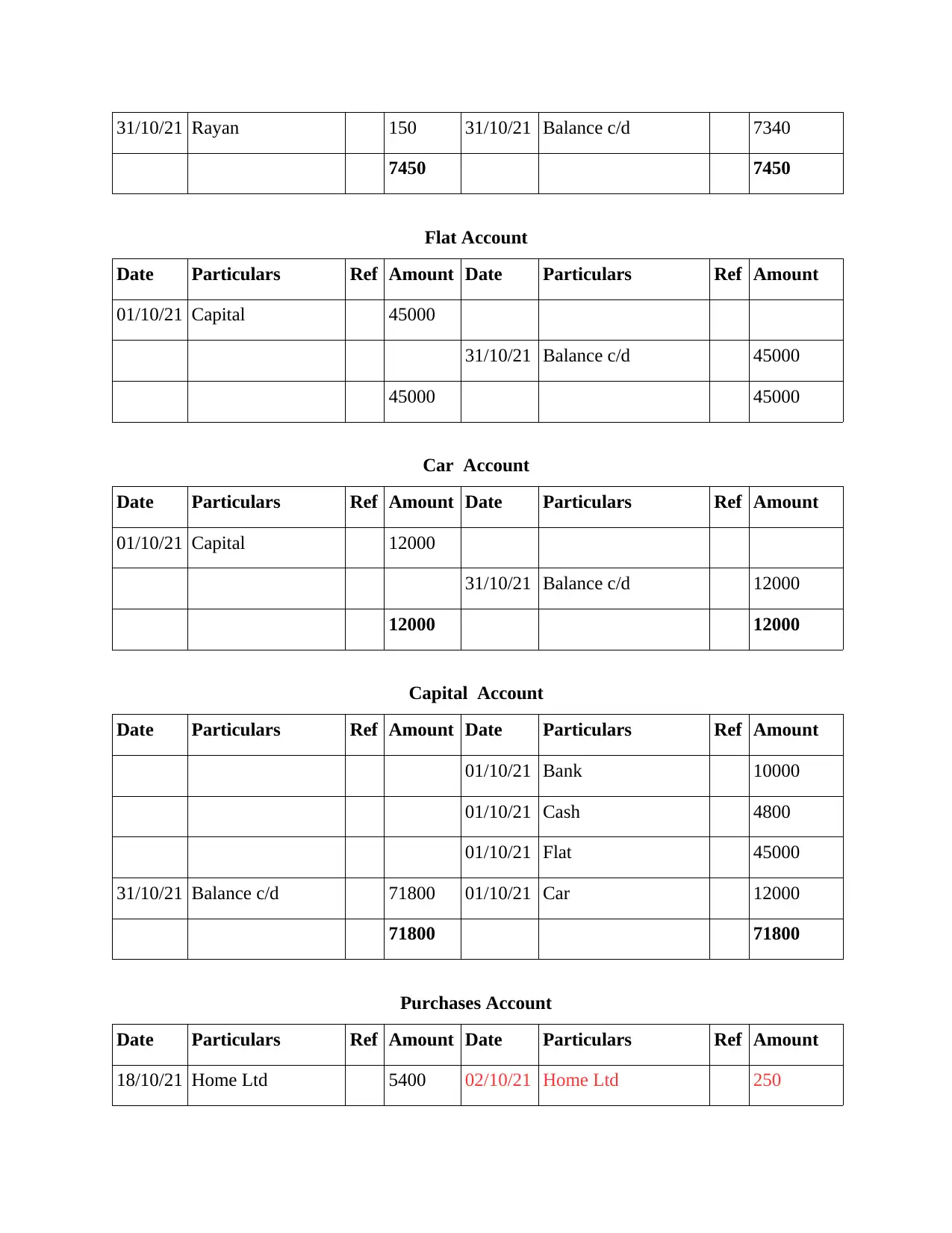

This report provides a detailed analysis of business transactions, starting with the recording of journal entries in T-accounts and progressing to the creation of accounting ledgers, a trial balance, an income statement, and a balance sheet. It includes an explanation of drawings in the context of Anne's business. Furthermore, the report calculates and analyzes various accounting ratios, comparing Anne's business performance to competitors and considering the impact of the Covid-19 pandemic. The analysis reveals that Anne's enterprise is underperforming compared to its rivals, and the report recommends strategies to regain lost profits and improve the business's financial standing. The report concludes by emphasizing the importance of accurate financial recording and strategic revision for better retention in the marketplace.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.