Business Transactions Recording and Financial Statement Analysis

VerifiedAdded on 2022/12/28

|16

|2833

|74

Report

AI Summary

This report provides a comprehensive analysis of recording business transactions and their impact on financial performance. It begins with an introduction to business transactions and their importance, followed by a detailed examination of journal entries, ledger accounts, and the trial balance for Linda's business. The report then delves into the preparation of the profitability statement and balance sheet, interpreting the financial position of the business. A letter to Linda explains the concept of drawings in small businesses. Part B of the report focuses on ratio analysis, calculating and interpreting profitability, liquidity, and solvency ratios to assess Linda's financial performance and compare it to a competitor. The analysis highlights areas for improvement, such as reducing operating expenses, improving liquidity, and managing debtors and creditors effectively to enhance the financial health and long-term sustainability of the business.

Recording Business

Transactions

Transactions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..........................................................................................................................3

PART A..........................................................................................................................................3

(a) Journal entries in the books of Linda....................................................................................3

(b) Ledger accounts in the books of Linda.................................................................................5

(c) Trial balance as at 31st October in the books of Linda.........................................................5

(d) Prepare profitability statement for the period ended 31 October 2020.................................6

(e) Financial Position of Linda's Business as at 31st October 2020...........................................7

(f) Letter to Linda explaining about what drawings are concerning small businesses...............9

PART B..........................................................................................................................................9

(i) Calculation of ratios in the books of Linda............................................................................9

(ii) Analysis of Linda's Financial performance with ratios......................................................11

REFERENCES.............................................................................................................................14

APPENDIX...................................................................................................................................15

INTRODUCTION..........................................................................................................................3

PART A..........................................................................................................................................3

(a) Journal entries in the books of Linda....................................................................................3

(b) Ledger accounts in the books of Linda.................................................................................5

(c) Trial balance as at 31st October in the books of Linda.........................................................5

(d) Prepare profitability statement for the period ended 31 October 2020.................................6

(e) Financial Position of Linda's Business as at 31st October 2020...........................................7

(f) Letter to Linda explaining about what drawings are concerning small businesses...............9

PART B..........................................................................................................................................9

(i) Calculation of ratios in the books of Linda............................................................................9

(ii) Analysis of Linda's Financial performance with ratios......................................................11

REFERENCES.............................................................................................................................14

APPENDIX...................................................................................................................................15

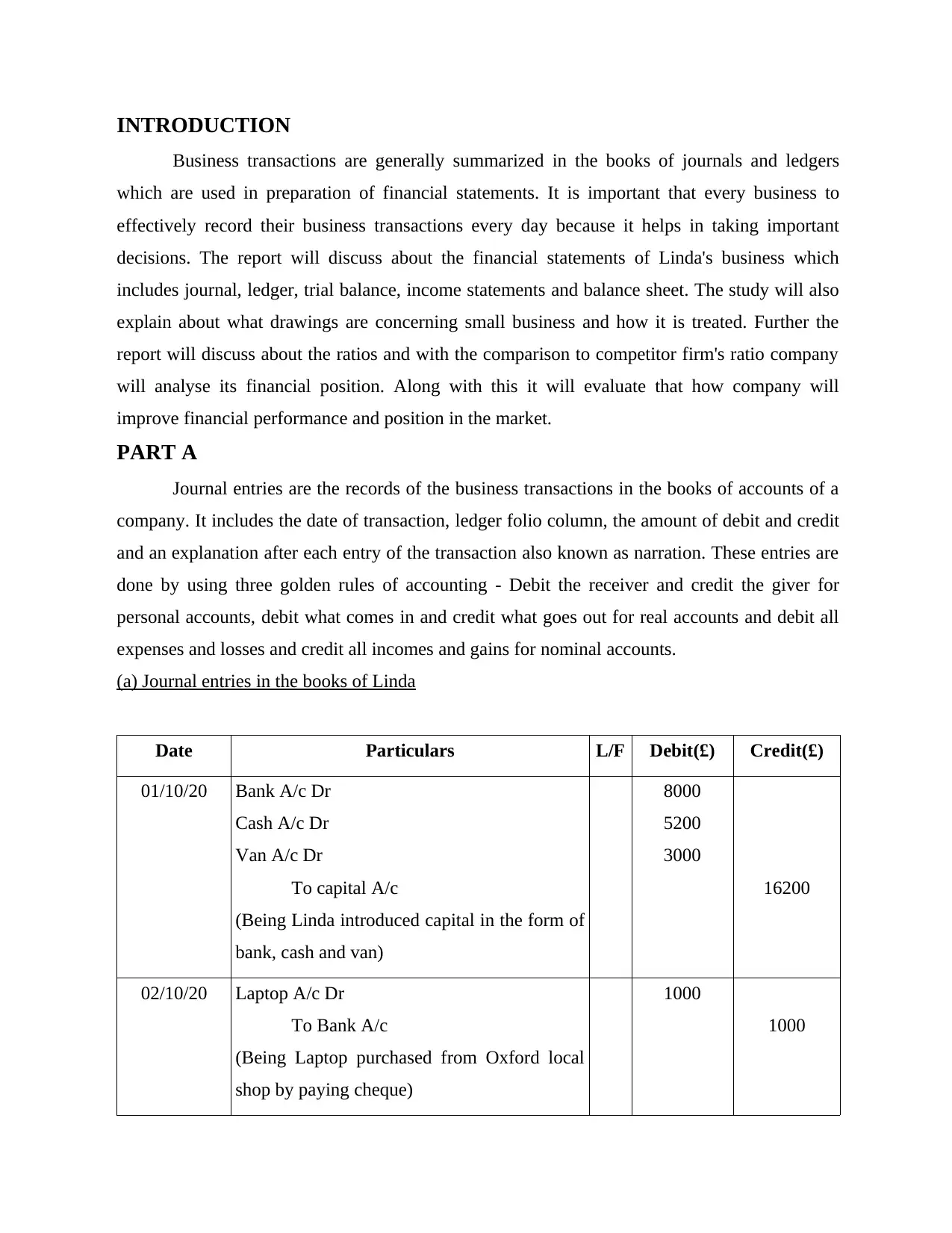

INTRODUCTION

Business transactions are generally summarized in the books of journals and ledgers

which are used in preparation of financial statements. It is important that every business to

effectively record their business transactions every day because it helps in taking important

decisions. The report will discuss about the financial statements of Linda's business which

includes journal, ledger, trial balance, income statements and balance sheet. The study will also

explain about what drawings are concerning small business and how it is treated. Further the

report will discuss about the ratios and with the comparison to competitor firm's ratio company

will analyse its financial position. Along with this it will evaluate that how company will

improve financial performance and position in the market.

PART A

Journal entries are the records of the business transactions in the books of accounts of a

company. It includes the date of transaction, ledger folio column, the amount of debit and credit

and an explanation after each entry of the transaction also known as narration. These entries are

done by using three golden rules of accounting - Debit the receiver and credit the giver for

personal accounts, debit what comes in and credit what goes out for real accounts and debit all

expenses and losses and credit all incomes and gains for nominal accounts.

(a) Journal entries in the books of Linda

Date Particulars L/F Debit(£) Credit(£)

01/10/20 Bank A/c Dr

Cash A/c Dr

Van A/c Dr

To capital A/c

(Being Linda introduced capital in the form of

bank, cash and van)

8000

5200

3000

16200

02/10/20 Laptop A/c Dr

To Bank A/c

(Being Laptop purchased from Oxford local

shop by paying cheque)

1000

1000

Business transactions are generally summarized in the books of journals and ledgers

which are used in preparation of financial statements. It is important that every business to

effectively record their business transactions every day because it helps in taking important

decisions. The report will discuss about the financial statements of Linda's business which

includes journal, ledger, trial balance, income statements and balance sheet. The study will also

explain about what drawings are concerning small business and how it is treated. Further the

report will discuss about the ratios and with the comparison to competitor firm's ratio company

will analyse its financial position. Along with this it will evaluate that how company will

improve financial performance and position in the market.

PART A

Journal entries are the records of the business transactions in the books of accounts of a

company. It includes the date of transaction, ledger folio column, the amount of debit and credit

and an explanation after each entry of the transaction also known as narration. These entries are

done by using three golden rules of accounting - Debit the receiver and credit the giver for

personal accounts, debit what comes in and credit what goes out for real accounts and debit all

expenses and losses and credit all incomes and gains for nominal accounts.

(a) Journal entries in the books of Linda

Date Particulars L/F Debit(£) Credit(£)

01/10/20 Bank A/c Dr

Cash A/c Dr

Van A/c Dr

To capital A/c

(Being Linda introduced capital in the form of

bank, cash and van)

8000

5200

3000

16200

02/10/20 Laptop A/c Dr

To Bank A/c

(Being Laptop purchased from Oxford local

shop by paying cheque)

1000

1000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

04/10/20 Purchased A/c Dr

To Toys Ltd

(Being goods purchased on credit from toys

limited)

2450

2450

05/10/20 Bank A/c Dr

To Sales A/c

(Being goods sold and received amount in

bank)

1500

1500

12/10/20 Repairing A/c Dr

To Cash a/c

(Being cash paid for repairing laptop )

80

80

18/10/20 Toys Ltd A/c Dr

To Purchase Return A/c

(Being goods return to Toys Ltd )

100

100

21/10/20 Bank A/c Dr

To Rent A/c

(Being Rent received from the premises)

500

500

23/10/20 Cash A/c Dr

Fred A/c Dr

To Sales A/c

(Being good sold on credit to Fred and 80 %

cash revived )

1500

400

1900

23/10/20 Cash A/c Dr

To sales A/c

(Being goods sold to David in cash)

500

500

24/10/20 Car A/c Dr

To Bank A/c

(Being second hand car purchased From

Oxford motor vehicle auction sale)

2500

2500

To Toys Ltd

(Being goods purchased on credit from toys

limited)

2450

2450

05/10/20 Bank A/c Dr

To Sales A/c

(Being goods sold and received amount in

bank)

1500

1500

12/10/20 Repairing A/c Dr

To Cash a/c

(Being cash paid for repairing laptop )

80

80

18/10/20 Toys Ltd A/c Dr

To Purchase Return A/c

(Being goods return to Toys Ltd )

100

100

21/10/20 Bank A/c Dr

To Rent A/c

(Being Rent received from the premises)

500

500

23/10/20 Cash A/c Dr

Fred A/c Dr

To Sales A/c

(Being good sold on credit to Fred and 80 %

cash revived )

1500

400

1900

23/10/20 Cash A/c Dr

To sales A/c

(Being goods sold to David in cash)

500

500

24/10/20 Car A/c Dr

To Bank A/c

(Being second hand car purchased From

Oxford motor vehicle auction sale)

2500

2500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

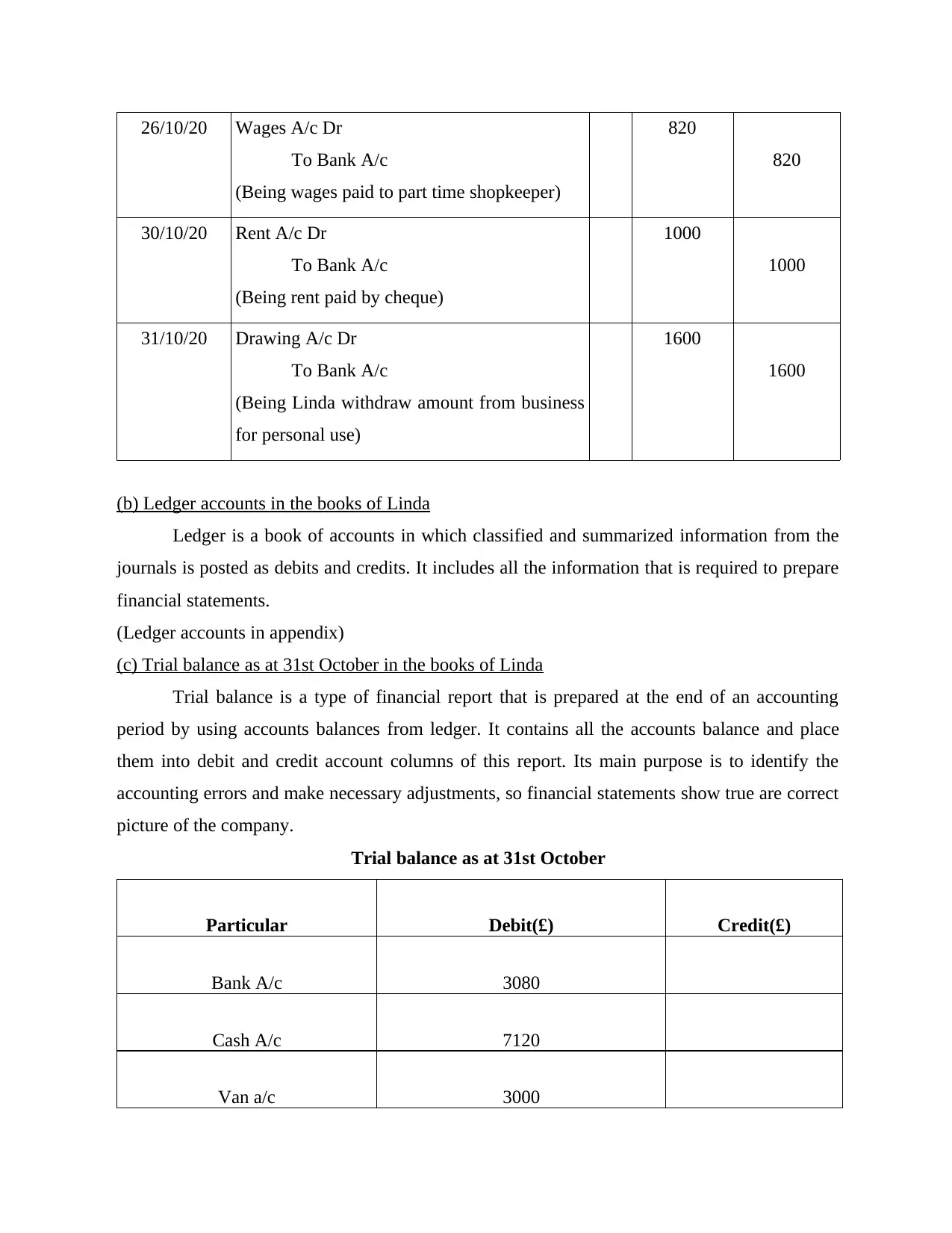

26/10/20 Wages A/c Dr

To Bank A/c

(Being wages paid to part time shopkeeper)

820

820

30/10/20 Rent A/c Dr

To Bank A/c

(Being rent paid by cheque)

1000

1000

31/10/20 Drawing A/c Dr

To Bank A/c

(Being Linda withdraw amount from business

for personal use)

1600

1600

(b) Ledger accounts in the books of Linda

Ledger is a book of accounts in which classified and summarized information from the

journals is posted as debits and credits. It includes all the information that is required to prepare

financial statements.

(Ledger accounts in appendix)

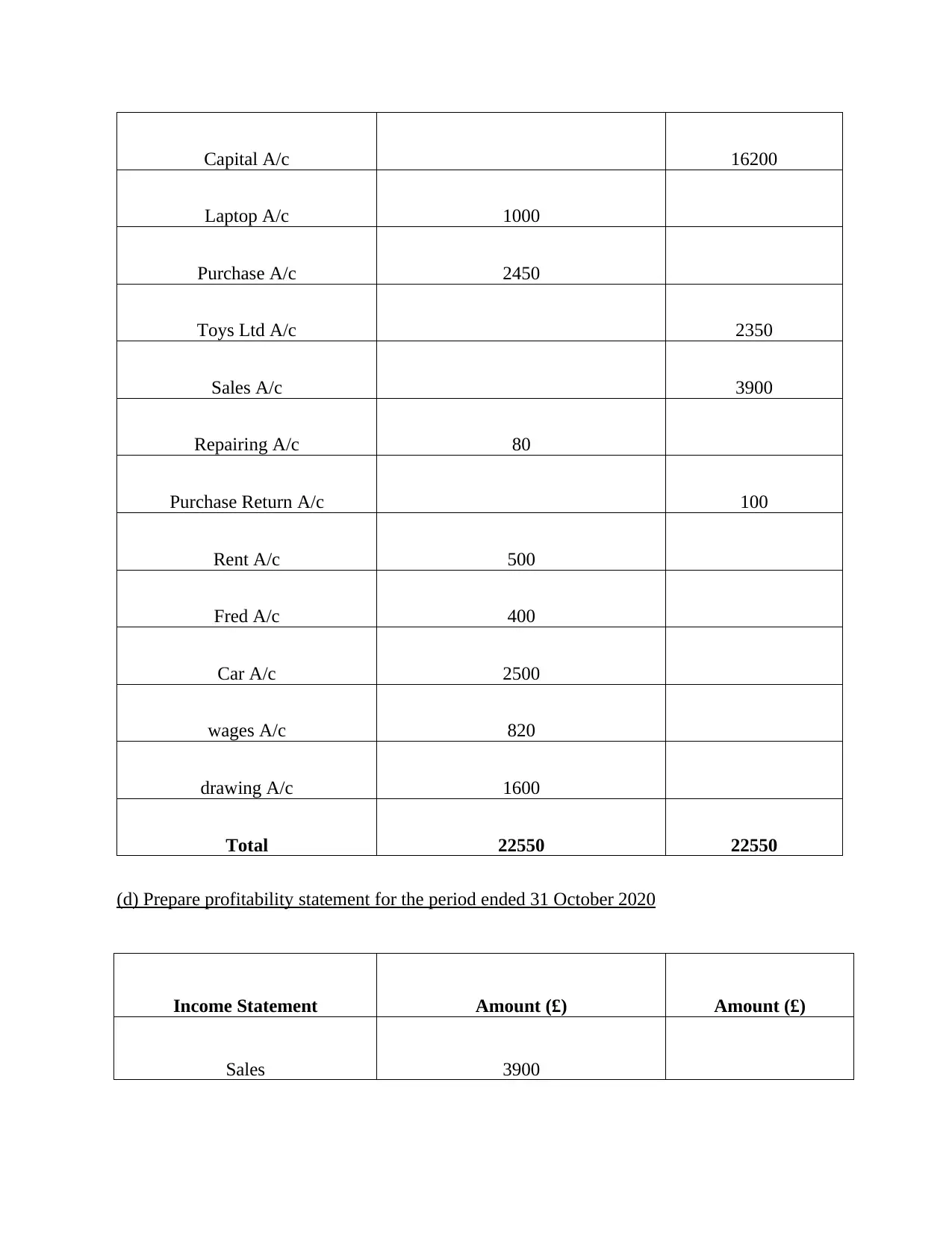

(c) Trial balance as at 31st October in the books of Linda

Trial balance is a type of financial report that is prepared at the end of an accounting

period by using accounts balances from ledger. It contains all the accounts balance and place

them into debit and credit account columns of this report. Its main purpose is to identify the

accounting errors and make necessary adjustments, so financial statements show true are correct

picture of the company.

Trial balance as at 31st October

Particular Debit(£) Credit(£)

Bank A/c 3080

Cash A/c 7120

Van a/c 3000

To Bank A/c

(Being wages paid to part time shopkeeper)

820

820

30/10/20 Rent A/c Dr

To Bank A/c

(Being rent paid by cheque)

1000

1000

31/10/20 Drawing A/c Dr

To Bank A/c

(Being Linda withdraw amount from business

for personal use)

1600

1600

(b) Ledger accounts in the books of Linda

Ledger is a book of accounts in which classified and summarized information from the

journals is posted as debits and credits. It includes all the information that is required to prepare

financial statements.

(Ledger accounts in appendix)

(c) Trial balance as at 31st October in the books of Linda

Trial balance is a type of financial report that is prepared at the end of an accounting

period by using accounts balances from ledger. It contains all the accounts balance and place

them into debit and credit account columns of this report. Its main purpose is to identify the

accounting errors and make necessary adjustments, so financial statements show true are correct

picture of the company.

Trial balance as at 31st October

Particular Debit(£) Credit(£)

Bank A/c 3080

Cash A/c 7120

Van a/c 3000

Capital A/c 16200

Laptop A/c 1000

Purchase A/c 2450

Toys Ltd A/c 2350

Sales A/c 3900

Repairing A/c 80

Purchase Return A/c 100

Rent A/c 500

Fred A/c 400

Car A/c 2500

wages A/c 820

drawing A/c 1600

Total 22550 22550

(d) Prepare profitability statement for the period ended 31 October 2020

Income Statement Amount (£) Amount (£)

Sales 3900

Laptop A/c 1000

Purchase A/c 2450

Toys Ltd A/c 2350

Sales A/c 3900

Repairing A/c 80

Purchase Return A/c 100

Rent A/c 500

Fred A/c 400

Car A/c 2500

wages A/c 820

drawing A/c 1600

Total 22550 22550

(d) Prepare profitability statement for the period ended 31 October 2020

Income Statement Amount (£) Amount (£)

Sales 3900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

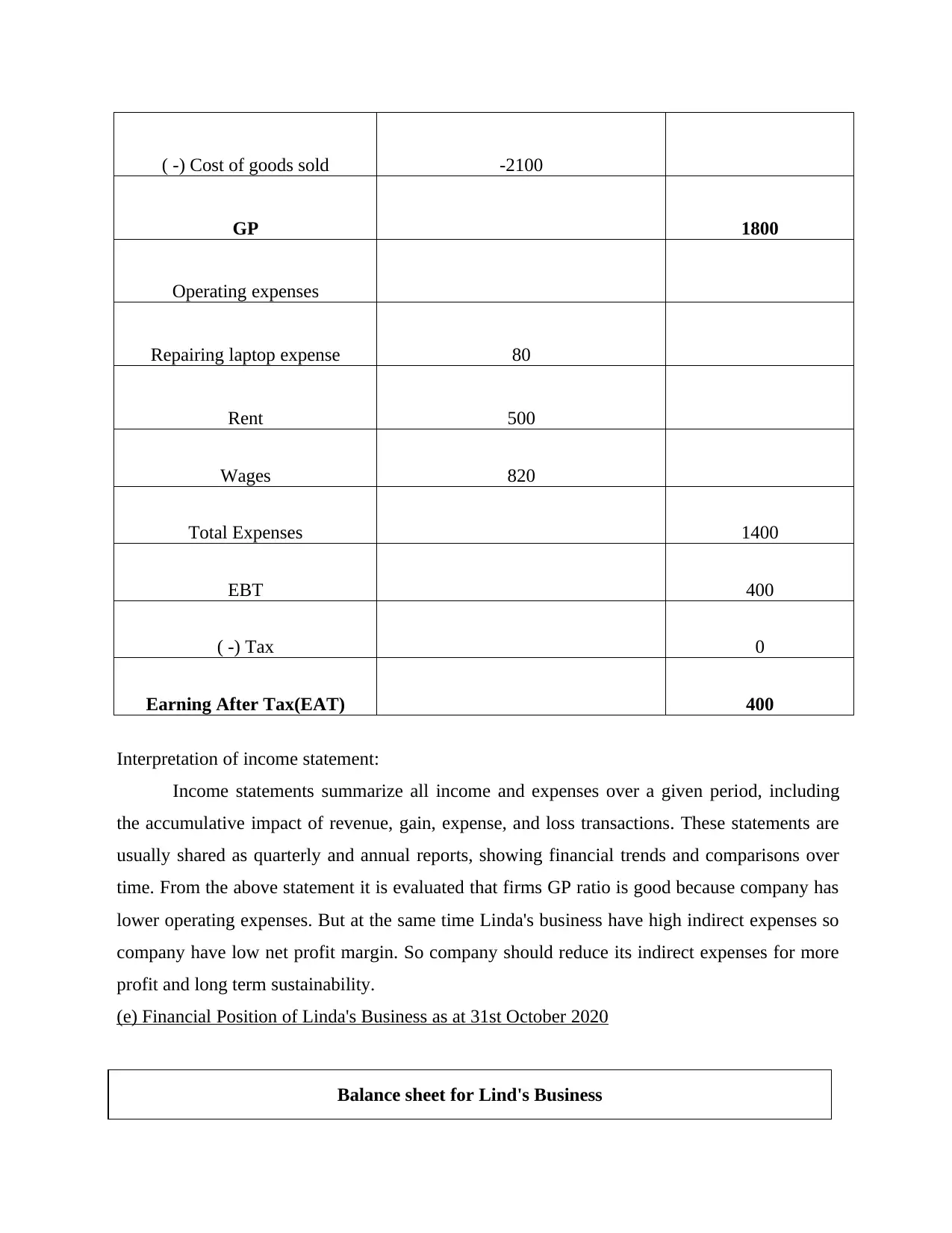

( -) Cost of goods sold -2100

GP 1800

Operating expenses

Repairing laptop expense 80

Rent 500

Wages 820

Total Expenses 1400

EBT 400

( -) Tax 0

Earning After Tax(EAT) 400

Interpretation of income statement:

Income statements summarize all income and expenses over a given period, including

the accumulative impact of revenue, gain, expense, and loss transactions. These statements are

usually shared as quarterly and annual reports, showing financial trends and comparisons over

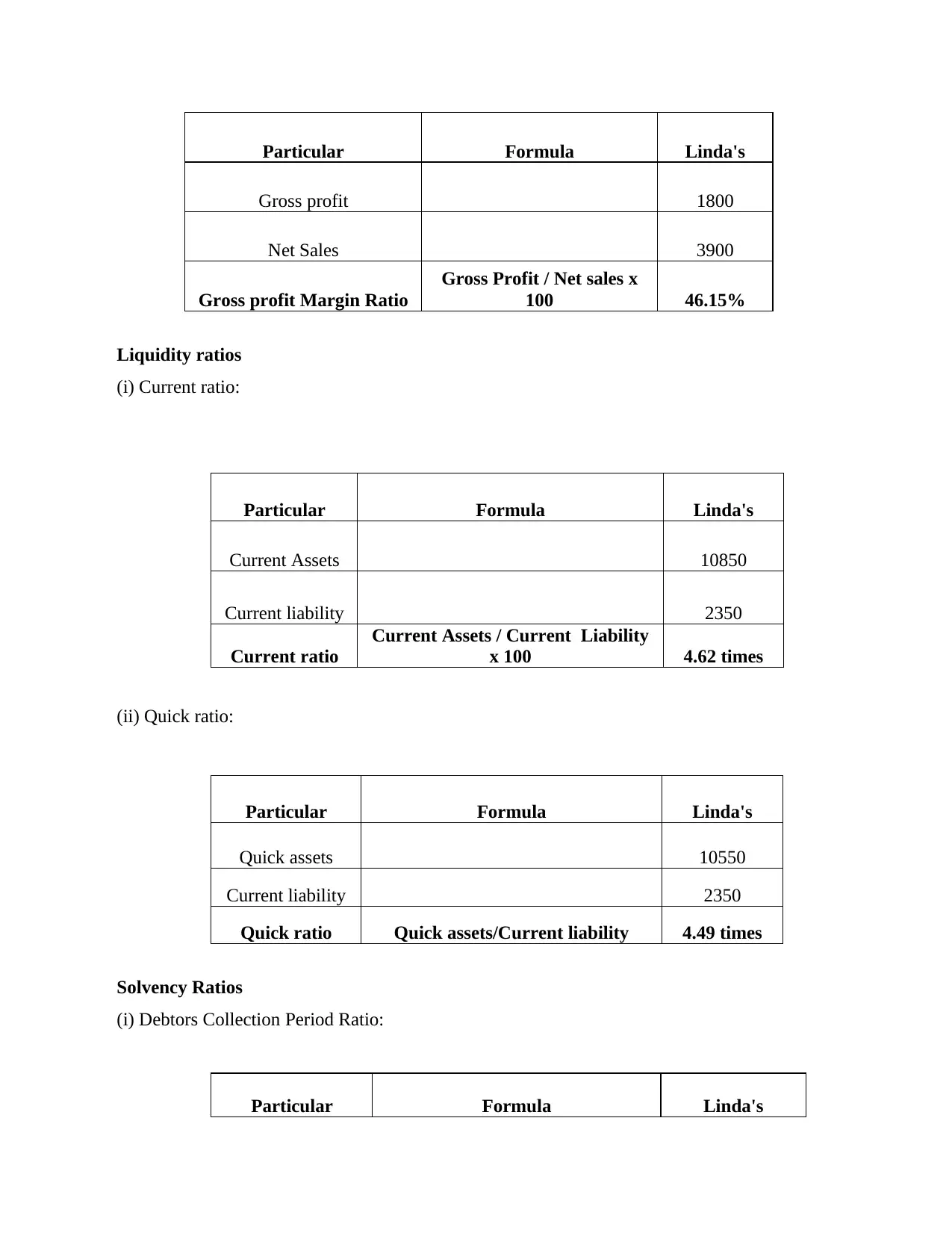

time. From the above statement it is evaluated that firms GP ratio is good because company has

lower operating expenses. But at the same time Linda's business have high indirect expenses so

company have low net profit margin. So company should reduce its indirect expenses for more

profit and long term sustainability.

(e) Financial Position of Linda's Business as at 31st October 2020

Balance sheet for Lind's Business

GP 1800

Operating expenses

Repairing laptop expense 80

Rent 500

Wages 820

Total Expenses 1400

EBT 400

( -) Tax 0

Earning After Tax(EAT) 400

Interpretation of income statement:

Income statements summarize all income and expenses over a given period, including

the accumulative impact of revenue, gain, expense, and loss transactions. These statements are

usually shared as quarterly and annual reports, showing financial trends and comparisons over

time. From the above statement it is evaluated that firms GP ratio is good because company has

lower operating expenses. But at the same time Linda's business have high indirect expenses so

company have low net profit margin. So company should reduce its indirect expenses for more

profit and long term sustainability.

(e) Financial Position of Linda's Business as at 31st October 2020

Balance sheet for Lind's Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As On 31st October 2020

ASSETS Amount(£)

Non-current assets

Van 3000

laptop 1000

Car 2500

Total Non-Current assets 6500

Current Assets

Bank 3080

Cash 7120

Debtors 400

Closing Stock 250 10850

Total assets 17350

LIABILITY

Non-Current Liability

Capital 16200

(-) Drawings 1600

(+) Net profit 400

Net Capital 15000

Total Non-Current liability

Current Liability

Creditors 2350

Total Current Liability 2350

Total Liability 17350

Interpretation of balance sheet:

Balance sheet is a financial document that display company's assets, liabilities and

overall shareholder equity. Balance sheets are useful tools for potential investors in a company,

as they show the general financial status of a company. It allows to calculate several financial

ratios that measures performance of a company. It includes total assets and liabilities of the firm

as on date.

(f) Letter to Linda explaining about what drawings are concerning small businesses

Linda's Business

Dear Sir,

Subject: Explaining about what drawings are pertaining for small businesses

ASSETS Amount(£)

Non-current assets

Van 3000

laptop 1000

Car 2500

Total Non-Current assets 6500

Current Assets

Bank 3080

Cash 7120

Debtors 400

Closing Stock 250 10850

Total assets 17350

LIABILITY

Non-Current Liability

Capital 16200

(-) Drawings 1600

(+) Net profit 400

Net Capital 15000

Total Non-Current liability

Current Liability

Creditors 2350

Total Current Liability 2350

Total Liability 17350

Interpretation of balance sheet:

Balance sheet is a financial document that display company's assets, liabilities and

overall shareholder equity. Balance sheets are useful tools for potential investors in a company,

as they show the general financial status of a company. It allows to calculate several financial

ratios that measures performance of a company. It includes total assets and liabilities of the firm

as on date.

(f) Letter to Linda explaining about what drawings are concerning small businesses

Linda's Business

Dear Sir,

Subject: Explaining about what drawings are pertaining for small businesses

I am writing this letter to draw your attention on your financial position. Currently your

company's financial position is not good and if you do not pay attention on this then it may starts

declining the position in the market. If any amount of money or assets which are taken by owner

for their personal use will considered as a drawings and it will reduce owners’ equity and assets

of the firm. Drawings are not considered as a business expenses it only reduces capital of the

owner. So if you withdraw any amount either for holidays or anything it will treated as a

personal expense. In small businesses capital is invested by only single person and if

continuously owner withdraw that amount then it will reduce capital and firm have to take loan

for performing regular business activities. On loan Amount high interest rate is charged by the

banks or other financial institutions so it is better to reduce the drawings for smooth functioning

of the businesses

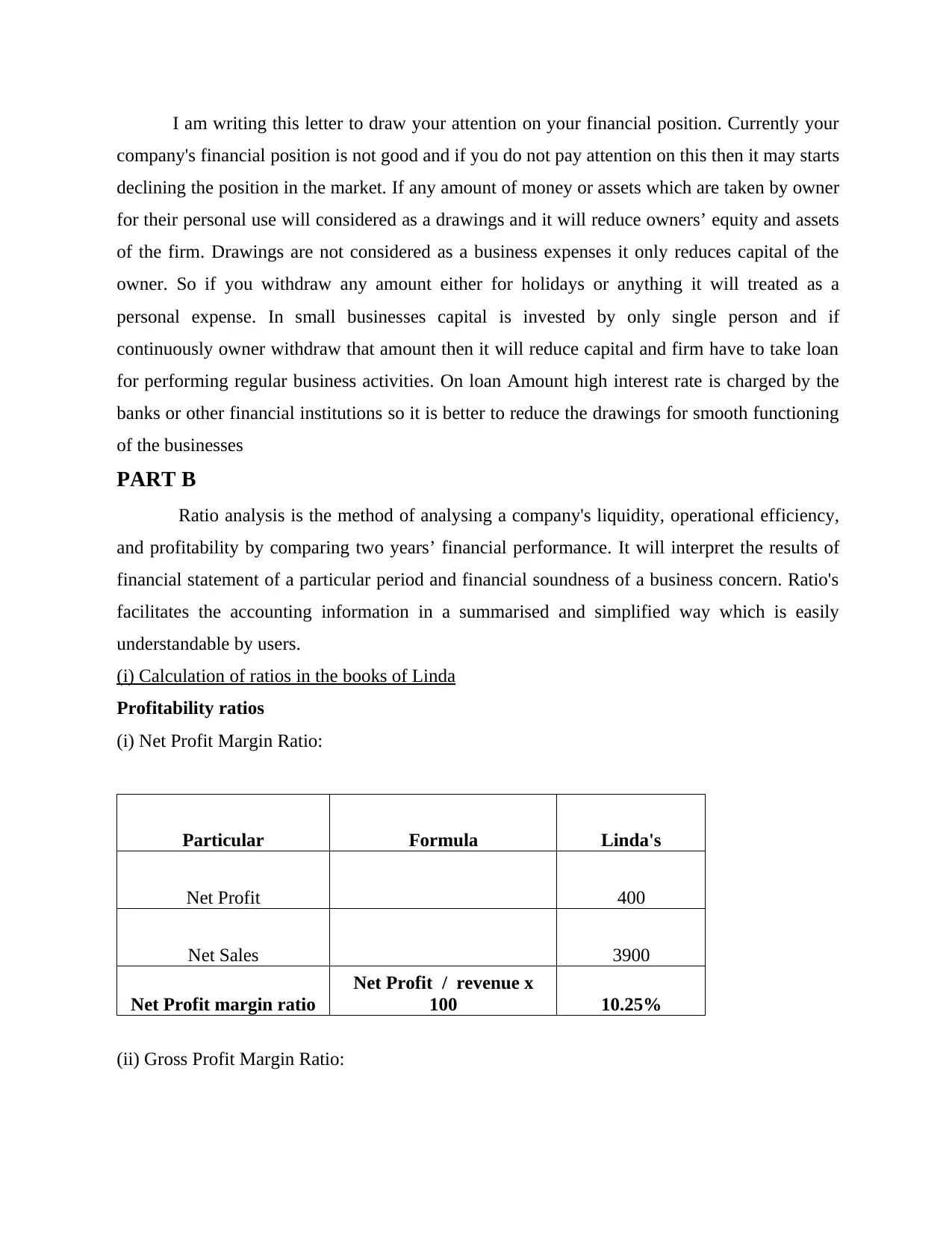

PART B

Ratio analysis is the method of analysing a company's liquidity, operational efficiency,

and profitability by comparing two years’ financial performance. It will interpret the results of

financial statement of a particular period and financial soundness of a business concern. Ratio's

facilitates the accounting information in a summarised and simplified way which is easily

understandable by users.

(i) Calculation of ratios in the books of Linda

Profitability ratios

(i) Net Profit Margin Ratio:

Particular Formula Linda's

Net Profit 400

Net Sales 3900

Net Profit margin ratio

Net Profit / revenue x

100 10.25%

(ii) Gross Profit Margin Ratio:

company's financial position is not good and if you do not pay attention on this then it may starts

declining the position in the market. If any amount of money or assets which are taken by owner

for their personal use will considered as a drawings and it will reduce owners’ equity and assets

of the firm. Drawings are not considered as a business expenses it only reduces capital of the

owner. So if you withdraw any amount either for holidays or anything it will treated as a

personal expense. In small businesses capital is invested by only single person and if

continuously owner withdraw that amount then it will reduce capital and firm have to take loan

for performing regular business activities. On loan Amount high interest rate is charged by the

banks or other financial institutions so it is better to reduce the drawings for smooth functioning

of the businesses

PART B

Ratio analysis is the method of analysing a company's liquidity, operational efficiency,

and profitability by comparing two years’ financial performance. It will interpret the results of

financial statement of a particular period and financial soundness of a business concern. Ratio's

facilitates the accounting information in a summarised and simplified way which is easily

understandable by users.

(i) Calculation of ratios in the books of Linda

Profitability ratios

(i) Net Profit Margin Ratio:

Particular Formula Linda's

Net Profit 400

Net Sales 3900

Net Profit margin ratio

Net Profit / revenue x

100 10.25%

(ii) Gross Profit Margin Ratio:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particular Formula Linda's

Gross profit 1800

Net Sales 3900

Gross profit Margin Ratio

Gross Profit / Net sales x

100 46.15%

Liquidity ratios

(i) Current ratio:

Particular Formula Linda's

Current Assets 10850

Current liability 2350

Current ratio

Current Assets / Current Liability

x 100 4.62 times

(ii) Quick ratio:

Particular Formula Linda's

Quick assets 10550

Current liability 2350

Quick ratio Quick assets/Current liability 4.49 times

Solvency Ratios

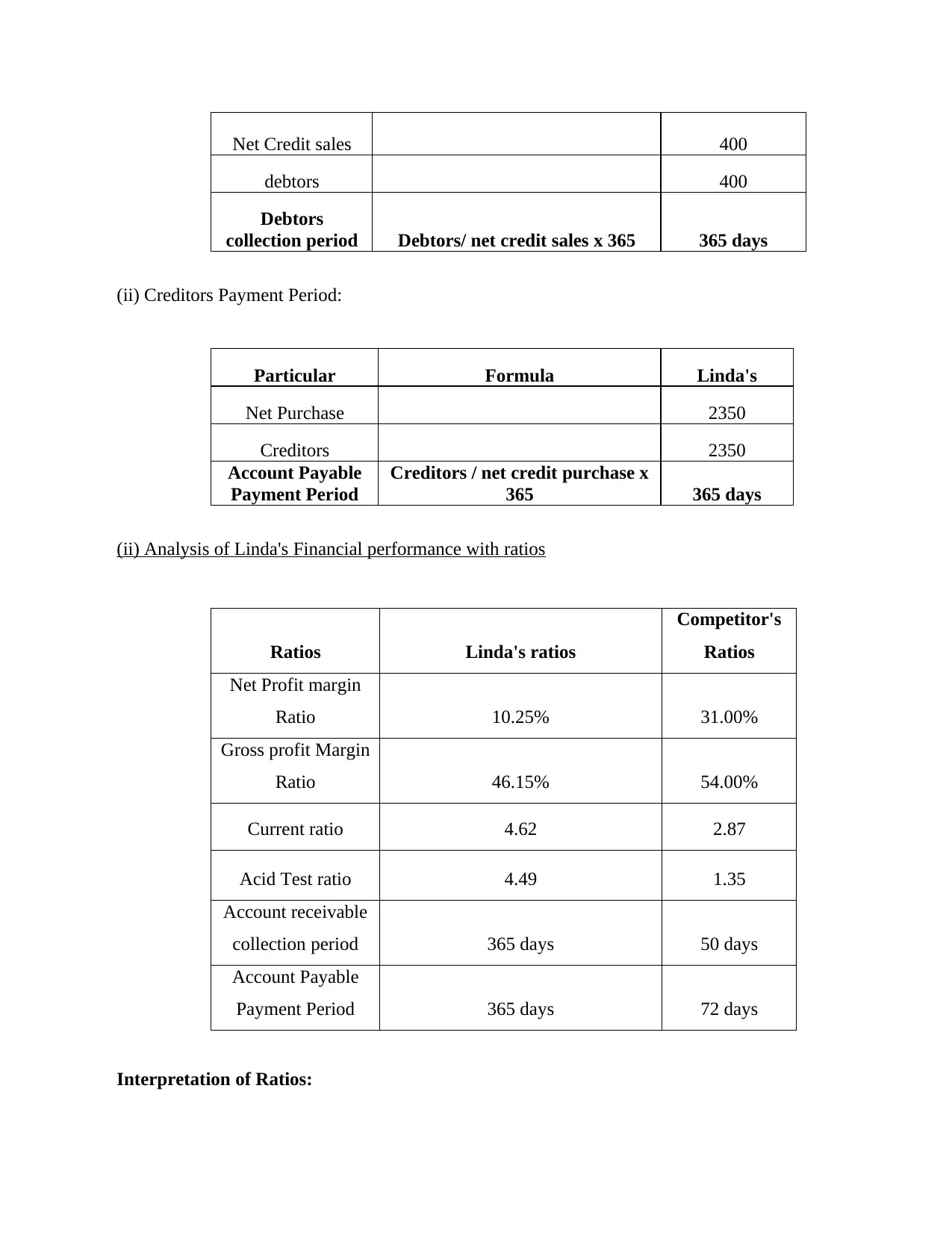

(i) Debtors Collection Period Ratio:

Particular Formula Linda's

Gross profit 1800

Net Sales 3900

Gross profit Margin Ratio

Gross Profit / Net sales x

100 46.15%

Liquidity ratios

(i) Current ratio:

Particular Formula Linda's

Current Assets 10850

Current liability 2350

Current ratio

Current Assets / Current Liability

x 100 4.62 times

(ii) Quick ratio:

Particular Formula Linda's

Quick assets 10550

Current liability 2350

Quick ratio Quick assets/Current liability 4.49 times

Solvency Ratios

(i) Debtors Collection Period Ratio:

Particular Formula Linda's

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Credit sales 400

debtors 400

Debtors

collection period Debtors/ net credit sales x 365 365 days

(ii) Creditors Payment Period:

Particular Formula Linda's

Net Purchase 2350

Creditors 2350

Account Payable

Payment Period

Creditors / net credit purchase x

365 365 days

(ii) Analysis of Linda's Financial performance with ratios

Ratios Linda's ratios

Competitor's

Ratios

Net Profit margin

Ratio 10.25% 31.00%

Gross profit Margin

Ratio 46.15% 54.00%

Current ratio 4.62 2.87

Acid Test ratio 4.49 1.35

Account receivable

collection period 365 days 50 days

Account Payable

Payment Period 365 days 72 days

Interpretation of Ratios:

debtors 400

Debtors

collection period Debtors/ net credit sales x 365 365 days

(ii) Creditors Payment Period:

Particular Formula Linda's

Net Purchase 2350

Creditors 2350

Account Payable

Payment Period

Creditors / net credit purchase x

365 365 days

(ii) Analysis of Linda's Financial performance with ratios

Ratios Linda's ratios

Competitor's

Ratios

Net Profit margin

Ratio 10.25% 31.00%

Gross profit Margin

Ratio 46.15% 54.00%

Current ratio 4.62 2.87

Acid Test ratio 4.49 1.35

Account receivable

collection period 365 days 50 days

Account Payable

Payment Period 365 days 72 days

Interpretation of Ratios:

Ratio analysis shows that Linda's profitability ratio is adequate and they highlight that

company is earning high profit and maximise its revenue. while on the other side competitor’s

profitability ratio is 20% higher than the Quoted firm. So company need to have more focus on

increasing its profit by reducing operating expenses and making effective strategies for

expanding firm's revenue. As shown in above table GP ratio of Lind's business is low from its

competitors. For Improving its GP ratio firm needs to identify those expenses which declines

firm Gross profit margin. After that making strategies for controlling those direct expenses only

then firm's enlarged its sales.

It will further inter prate that liquidity ratios of firm declines the overall financial

position of Linda's business. The reason behind that is current and quick ratio of the company is

very high and will more invested the money in current assets which leads to shortages of funds.

For improving this firm have to pay its current obligations on time and can withdraw funds from

current assets and invest that fund in a profitable portfolio. while the competitor’s firms have

high liquidity for paying off its short term obligations. So chosen firm have to more focus on

improving its liquidity position.

The account receivable collection period of the company is too high which shows Linda

debtors does not pay their debts on time. So company should reduce its credit sales for better

solvency ratios Because if payments from debtors does not collect on time, then it may increase

the chances of bad debts. So it is necessary for the company to offer early payment discounts to

the clients and diversify firm’s client for cover firm’s bad debts. Competitor firm's Collection

period is only 50 days which is more adequate as compared to Linda's business.

It shall also be reflected that account payable payment period of the company is too high

which depicts that the quoted firm does not pay off its current liabilities on time. If company

continuously follow this policy, then it may negative impact on credit purchases. It will decline

the goodwill and creditworthiness to its creditors. For Improving creditors payment period

company may negotiate with its suppliers or avail more discount from early paying. while

Linda's competitor firm will pay off its obligations in 72 days which is best time to pay. Linda

will also more focused on payment period for reflection of better solvency ratios in the financial

statements.

From the above analysis it is clear that the firm’s financial performance is not good from

its competitors. For long run sustainability of Linda's business firstly firm have to reduce its cost

company is earning high profit and maximise its revenue. while on the other side competitor’s

profitability ratio is 20% higher than the Quoted firm. So company need to have more focus on

increasing its profit by reducing operating expenses and making effective strategies for

expanding firm's revenue. As shown in above table GP ratio of Lind's business is low from its

competitors. For Improving its GP ratio firm needs to identify those expenses which declines

firm Gross profit margin. After that making strategies for controlling those direct expenses only

then firm's enlarged its sales.

It will further inter prate that liquidity ratios of firm declines the overall financial

position of Linda's business. The reason behind that is current and quick ratio of the company is

very high and will more invested the money in current assets which leads to shortages of funds.

For improving this firm have to pay its current obligations on time and can withdraw funds from

current assets and invest that fund in a profitable portfolio. while the competitor’s firms have

high liquidity for paying off its short term obligations. So chosen firm have to more focus on

improving its liquidity position.

The account receivable collection period of the company is too high which shows Linda

debtors does not pay their debts on time. So company should reduce its credit sales for better

solvency ratios Because if payments from debtors does not collect on time, then it may increase

the chances of bad debts. So it is necessary for the company to offer early payment discounts to

the clients and diversify firm’s client for cover firm’s bad debts. Competitor firm's Collection

period is only 50 days which is more adequate as compared to Linda's business.

It shall also be reflected that account payable payment period of the company is too high

which depicts that the quoted firm does not pay off its current liabilities on time. If company

continuously follow this policy, then it may negative impact on credit purchases. It will decline

the goodwill and creditworthiness to its creditors. For Improving creditors payment period

company may negotiate with its suppliers or avail more discount from early paying. while

Linda's competitor firm will pay off its obligations in 72 days which is best time to pay. Linda

will also more focused on payment period for reflection of better solvency ratios in the financial

statements.

From the above analysis it is clear that the firm’s financial performance is not good from

its competitors. For long run sustainability of Linda's business firstly firm have to reduce its cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.