Recording Business Transactions: Accounting and Financial Reporting

VerifiedAdded on 2023/01/03

|12

|2134

|66

Report

AI Summary

This report provides a detailed analysis of recording business transactions, encompassing key aspects of financial accounting. It begins with an introduction to business transactions and the role of accounting information for decision-makers, differentiating between internal and external users and outlining their specific needs. The report then delves into the advantages and disadvantages of recording accounting information. The core of the report involves practical application, including the creation of journal entries, followed by the computation of a general ledger and a trial balance. Furthermore, the report calculates an income statement and discusses the potential impacts of COVID-19 on various income statement items, providing a real-world perspective on financial analysis. The report concludes with a summary of the findings and a list of references.

Recording Business

Transactions

(Portfolio 1)

Transactions

(Portfolio 1)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

PART 1............................................................................................................................................1

a. Identification of decision makers in reference to definition of accounting along with their

requirement for accounting information: ....................................................................................1

b. Explanation of advantages and disadvantages of recording information related to

accounting:...................................................................................................................................2

PART 2............................................................................................................................................3

Recording business transactions through Journal Entries:...........................................................3

PART 3............................................................................................................................................4

a. Computation of General Ledger:.............................................................................................4

b. Computation of Trial Balance:.................................................................................................6

PART 4............................................................................................................................................6

a. Calculation of Income statement:.............................................................................................6

b. Possible impact of COVID 19 on income statement items of business:..................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

PART 1............................................................................................................................................1

a. Identification of decision makers in reference to definition of accounting along with their

requirement for accounting information: ....................................................................................1

b. Explanation of advantages and disadvantages of recording information related to

accounting:...................................................................................................................................2

PART 2............................................................................................................................................3

Recording business transactions through Journal Entries:...........................................................3

PART 3............................................................................................................................................4

a. Computation of General Ledger:.............................................................................................4

b. Computation of Trial Balance:.................................................................................................6

PART 4............................................................................................................................................6

a. Calculation of Income statement:.............................................................................................6

b. Possible impact of COVID 19 on income statement items of business:..................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Business transaction is a term that defines activities which influence financial position of

an organization. Such transactions are firstly recorded in books of accounts and later summarized

in reports of finance, which can be referred as financial report (Berg, Davidson and Potts, 2018).

This report consists description of accounting. Further, decision makers that require accounting

information is identified and explained. In addition to it, pros and cons of recording business

information in relevance to accounting is discussed. Journal entry, general ledger, and trial

balance of company is computed. Lastly, income statement of an organization is calculated and

possible impact of COVID 19 on income statement of business is explained.

ASSESSMENT 1

PART 1

a. Identification of decision makers in reference to definition of accounting along with their

requirement for accounting information:

Accounting information refers to data about business transactions. It indicates

identification and communication of financial information of an organization to the decision-

makers. Decision-makers refers to a person or team that decides policies and strategies on the

basis of accounting information (Allen, 2018). Such decision makers can be divided into two

categories, that is, internal and external, which are discussed below.

Internal decision-makers: It refers to those users of accounting or financial information

that have influence on day to day decision making in an organization.

Management: Managers or management team of company requires accoun6ting

information to monitor financial performance of business and formulate effective

strategies for its future growth operations.

Employees: Accounting information updates employees or staff members of an

organization about its financial health. It helps employees in determining job security it

pertains, future remuneration possibilities, so that working staff can make decisions about

their employment opportunities (Black, 2019).

External decision-makers: It indicates individuals outside an entity that uses financial in

information for making decisions.

Business transaction is a term that defines activities which influence financial position of

an organization. Such transactions are firstly recorded in books of accounts and later summarized

in reports of finance, which can be referred as financial report (Berg, Davidson and Potts, 2018).

This report consists description of accounting. Further, decision makers that require accounting

information is identified and explained. In addition to it, pros and cons of recording business

information in relevance to accounting is discussed. Journal entry, general ledger, and trial

balance of company is computed. Lastly, income statement of an organization is calculated and

possible impact of COVID 19 on income statement of business is explained.

ASSESSMENT 1

PART 1

a. Identification of decision makers in reference to definition of accounting along with their

requirement for accounting information:

Accounting information refers to data about business transactions. It indicates

identification and communication of financial information of an organization to the decision-

makers. Decision-makers refers to a person or team that decides policies and strategies on the

basis of accounting information (Allen, 2018). Such decision makers can be divided into two

categories, that is, internal and external, which are discussed below.

Internal decision-makers: It refers to those users of accounting or financial information

that have influence on day to day decision making in an organization.

Management: Managers or management team of company requires accoun6ting

information to monitor financial performance of business and formulate effective

strategies for its future growth operations.

Employees: Accounting information updates employees or staff members of an

organization about its financial health. It helps employees in determining job security it

pertains, future remuneration possibilities, so that working staff can make decisions about

their employment opportunities (Black, 2019).

External decision-makers: It indicates individuals outside an entity that uses financial in

information for making decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investors: It refers to persons who are planning to invest in company. Accounting

information is utilised by investors to determine value of company as well as its credit

analysis. It is vital for estimating the risk involved while investing in company which

furthers guides their investment decisions.

Creditors: Accounting information provides outline for credit worthiness of an

enterprise. If credit worthiness of company is good than creditors can lend money and

vice versa (Hoerl and Snee, 2020).

Customers: Financial performance of company can be assessed through its accounting

information which enables customers to judge the value and sustainability of entity.

Government: Information related to accounting guides government about authenticity of

tax paid by an enterprise (Wiatt, 2019). So that government can make decisions regarding

trade practices of company.

b. Explanation of advantages and disadvantages of recording information related to accounting:

Accounting: It is a process of documentation, assembling and acknowledging the

financial information so that the proper results can be generated which help in taking the better

future decisions (Jeter and Chaney, 2019). It helps in keeping the records of all the assets,

liabilities, expenses, revenue and the equity of the firm.

Advantages:

Cost control: All the income and expenditure of the accounts are maintained in a proper

way. If there is excess of expenditure then it can be controlled and there is no misuse of

the income generated.

Prevention of errors: It becomes easy to detect the fraud of an organisation by keeping

the record in a proper way (Weygandt, Kimmel and Kieso, 2019). By preparing the trial

balance the accurate data can be obtained and to correct it steps are taken on time.

Knowing cash position: All the cash receipts and payments are to be recorded in a

proper way so that the amount related to the cash in hand and cash in bank can be

determined easily which is essential for the running of the business.

Taking Loans: Advantage of taking the loans become easier if the accounts are

maintained in a proper and accurate basis there are no chances of fraud (Roberts, 2018).

Disadvantages:

information is utilised by investors to determine value of company as well as its credit

analysis. It is vital for estimating the risk involved while investing in company which

furthers guides their investment decisions.

Creditors: Accounting information provides outline for credit worthiness of an

enterprise. If credit worthiness of company is good than creditors can lend money and

vice versa (Hoerl and Snee, 2020).

Customers: Financial performance of company can be assessed through its accounting

information which enables customers to judge the value and sustainability of entity.

Government: Information related to accounting guides government about authenticity of

tax paid by an enterprise (Wiatt, 2019). So that government can make decisions regarding

trade practices of company.

b. Explanation of advantages and disadvantages of recording information related to accounting:

Accounting: It is a process of documentation, assembling and acknowledging the

financial information so that the proper results can be generated which help in taking the better

future decisions (Jeter and Chaney, 2019). It helps in keeping the records of all the assets,

liabilities, expenses, revenue and the equity of the firm.

Advantages:

Cost control: All the income and expenditure of the accounts are maintained in a proper

way. If there is excess of expenditure then it can be controlled and there is no misuse of

the income generated.

Prevention of errors: It becomes easy to detect the fraud of an organisation by keeping

the record in a proper way (Weygandt, Kimmel and Kieso, 2019). By preparing the trial

balance the accurate data can be obtained and to correct it steps are taken on time.

Knowing cash position: All the cash receipts and payments are to be recorded in a

proper way so that the amount related to the cash in hand and cash in bank can be

determined easily which is essential for the running of the business.

Taking Loans: Advantage of taking the loans become easier if the accounts are

maintained in a proper and accurate basis there are no chances of fraud (Roberts, 2018).

Disadvantages:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

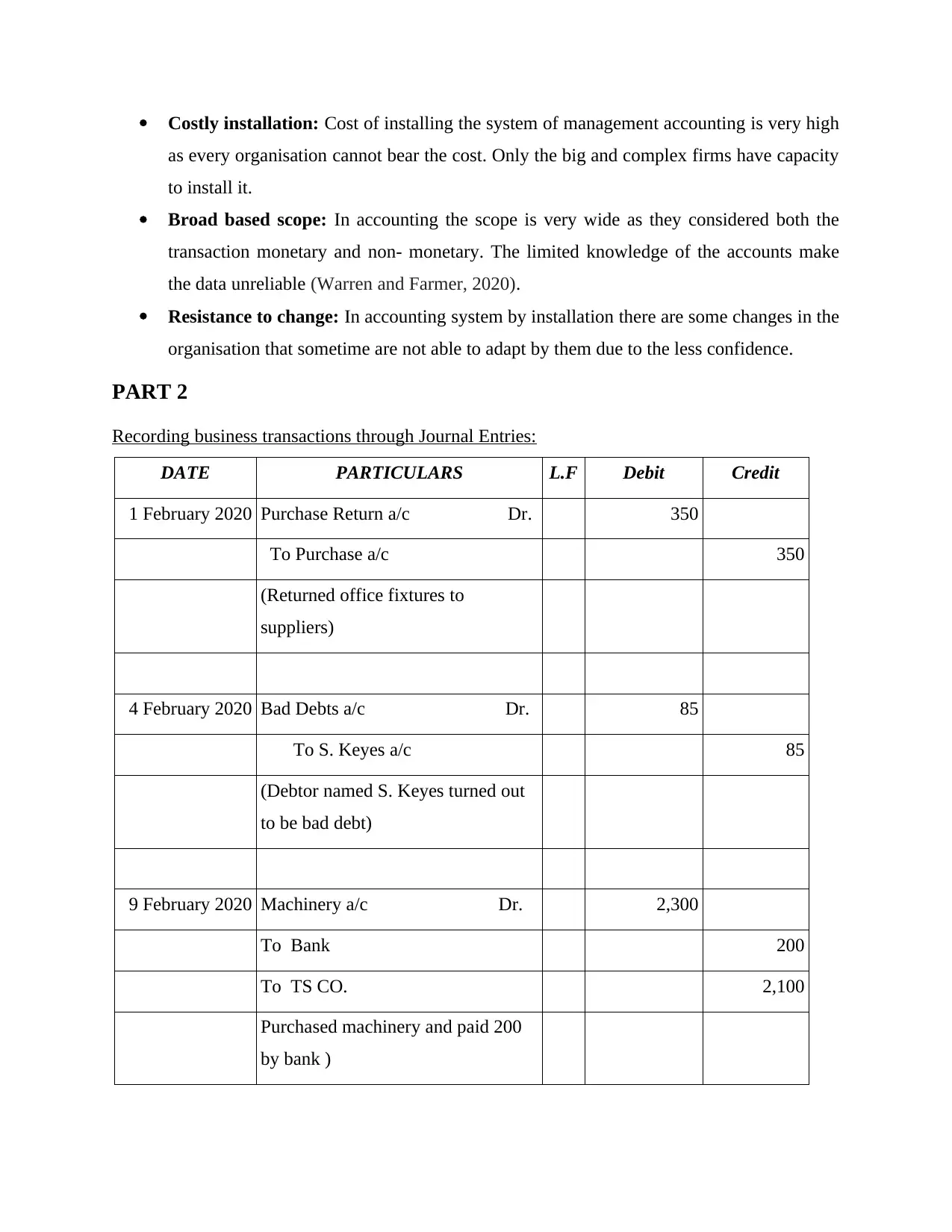

Costly installation: Cost of installing the system of management accounting is very high

as every organisation cannot bear the cost. Only the big and complex firms have capacity

to install it.

Broad based scope: In accounting the scope is very wide as they considered both the

transaction monetary and non- monetary. The limited knowledge of the accounts make

the data unreliable (Warren and Farmer, 2020).

Resistance to change: In accounting system by installation there are some changes in the

organisation that sometime are not able to adapt by them due to the less confidence.

PART 2

Recording business transactions through Journal Entries:

DATE PARTICULARS L.F Debit Credit

1 February 2020 Purchase Return a/c Dr. 350

To Purchase a/c 350

(Returned office fixtures to

suppliers)

4 February 2020 Bad Debts a/c Dr. 85

To S. Keyes a/c 85

(Debtor named S. Keyes turned out

to be bad debt)

9 February 2020 Machinery a/c Dr. 2,300

To Bank 200

To TS CO. 2,100

Purchased machinery and paid 200

by bank )

as every organisation cannot bear the cost. Only the big and complex firms have capacity

to install it.

Broad based scope: In accounting the scope is very wide as they considered both the

transaction monetary and non- monetary. The limited knowledge of the accounts make

the data unreliable (Warren and Farmer, 2020).

Resistance to change: In accounting system by installation there are some changes in the

organisation that sometime are not able to adapt by them due to the less confidence.

PART 2

Recording business transactions through Journal Entries:

DATE PARTICULARS L.F Debit Credit

1 February 2020 Purchase Return a/c Dr. 350

To Purchase a/c 350

(Returned office fixtures to

suppliers)

4 February 2020 Bad Debts a/c Dr. 85

To S. Keyes a/c 85

(Debtor named S. Keyes turned out

to be bad debt)

9 February 2020 Machinery a/c Dr. 2,300

To Bank 200

To TS CO. 2,100

Purchased machinery and paid 200

by bank )

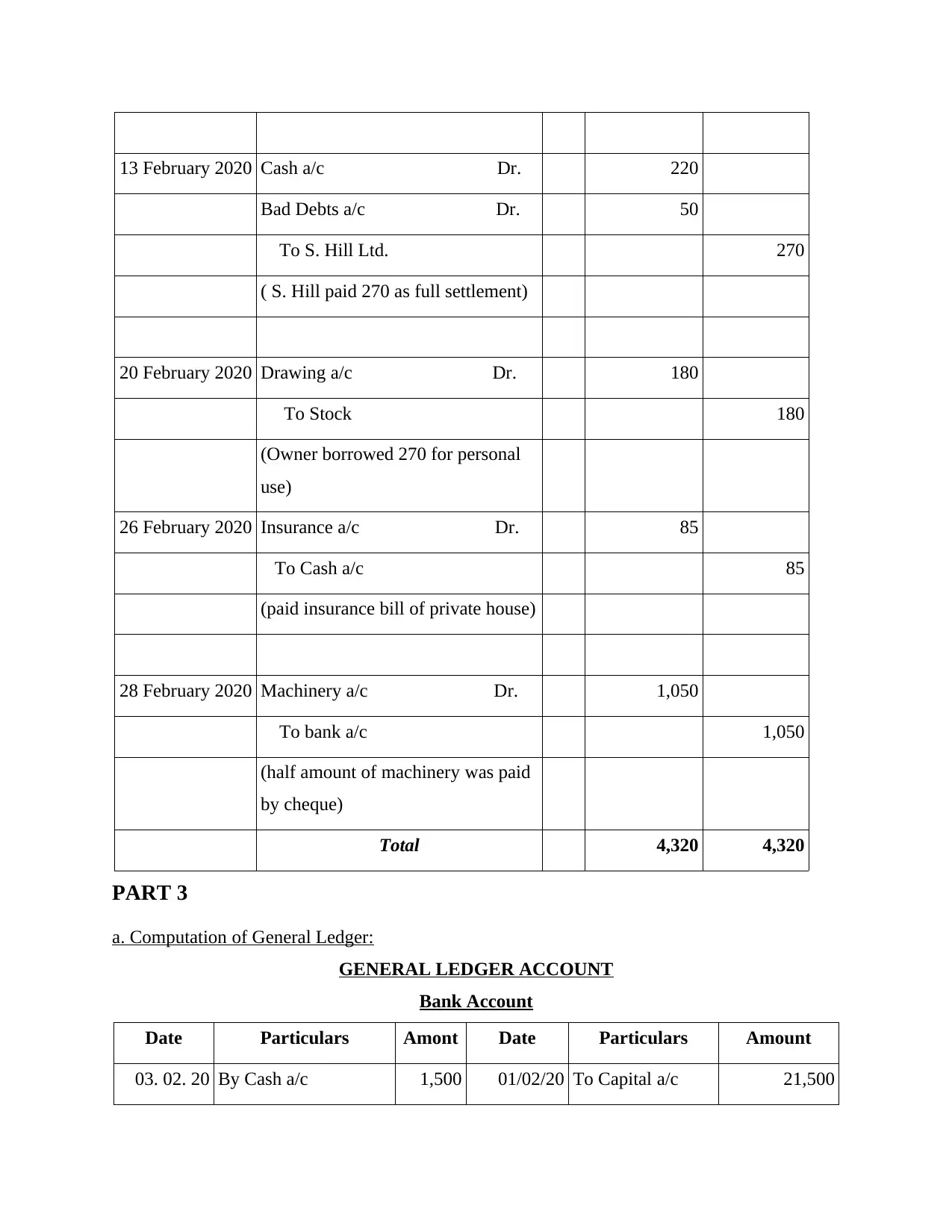

13 February 2020 Cash a/c Dr. 220

Bad Debts a/c Dr. 50

To S. Hill Ltd. 270

( S. Hill paid 270 as full settlement)

20 February 2020 Drawing a/c Dr. 180

To Stock 180

(Owner borrowed 270 for personal

use)

26 February 2020 Insurance a/c Dr. 85

To Cash a/c 85

(paid insurance bill of private house)

28 February 2020 Machinery a/c Dr. 1,050

To bank a/c 1,050

(half amount of machinery was paid

by cheque)

Total 4,320 4,320

PART 3

a. Computation of General Ledger:

GENERAL LEDGER ACCOUNT

Bank Account

Date Particulars Amont Date Particulars Amount

03. 02. 20 By Cash a/c 1,500 01/02/20 To Capital a/c 21,500

Bad Debts a/c Dr. 50

To S. Hill Ltd. 270

( S. Hill paid 270 as full settlement)

20 February 2020 Drawing a/c Dr. 180

To Stock 180

(Owner borrowed 270 for personal

use)

26 February 2020 Insurance a/c Dr. 85

To Cash a/c 85

(paid insurance bill of private house)

28 February 2020 Machinery a/c Dr. 1,050

To bank a/c 1,050

(half amount of machinery was paid

by cheque)

Total 4,320 4,320

PART 3

a. Computation of General Ledger:

GENERAL LEDGER ACCOUNT

Bank Account

Date Particulars Amont Date Particulars Amount

03. 02. 20 By Cash a/c 1,500 01/02/20 To Capital a/c 21,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

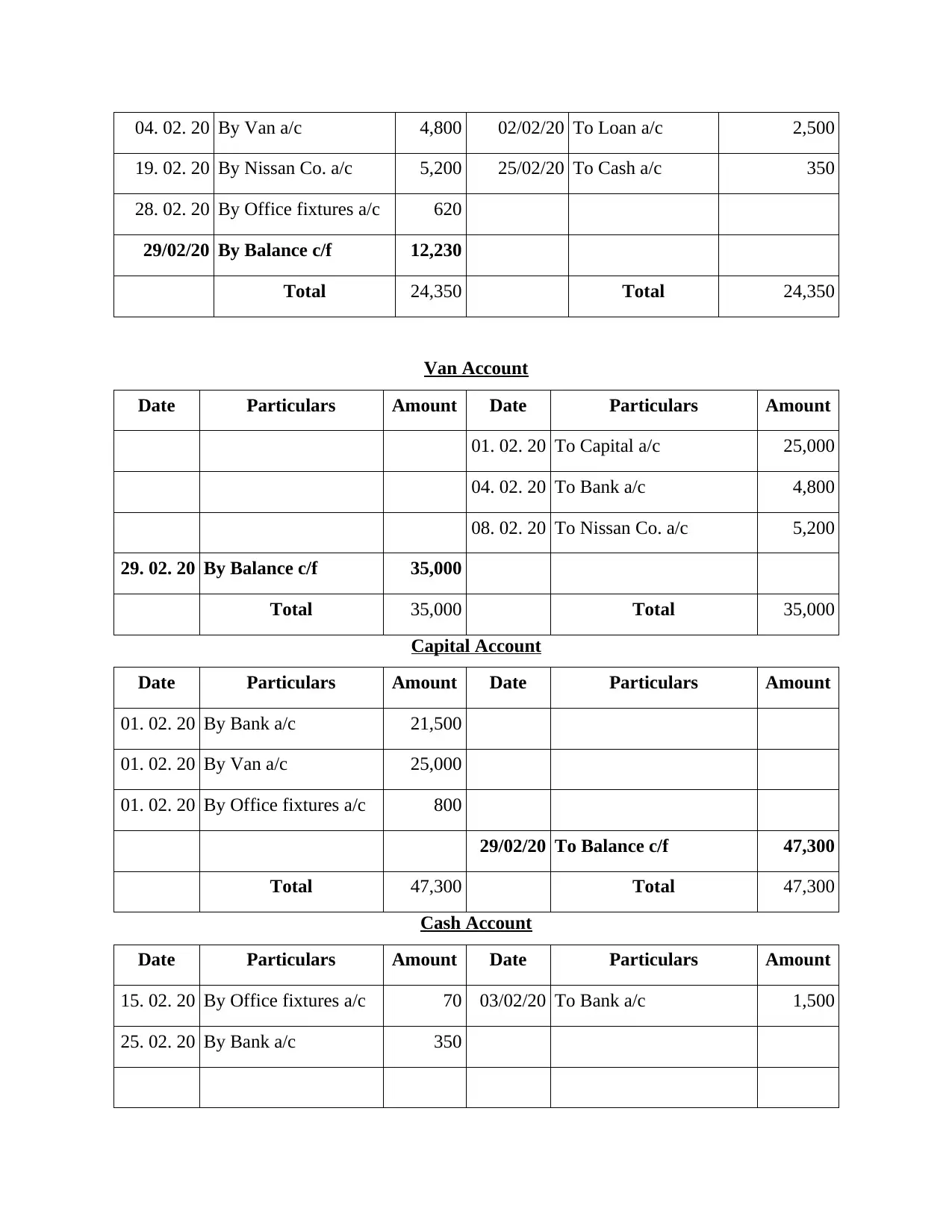

04. 02. 20 By Van a/c 4,800 02/02/20 To Loan a/c 2,500

19. 02. 20 By Nissan Co. a/c 5,200 25/02/20 To Cash a/c 350

28. 02. 20 By Office fixtures a/c 620

29/02/20 By Balance c/f 12,230

Total 24,350 Total 24,350

Van Account

Date Particulars Amount Date Particulars Amount

01. 02. 20 To Capital a/c 25,000

04. 02. 20 To Bank a/c 4,800

08. 02. 20 To Nissan Co. a/c 5,200

29. 02. 20 By Balance c/f 35,000

Total 35,000 Total 35,000

Capital Account

Date Particulars Amount Date Particulars Amount

01. 02. 20 By Bank a/c 21,500

01. 02. 20 By Van a/c 25,000

01. 02. 20 By Office fixtures a/c 800

29/02/20 To Balance c/f 47,300

Total 47,300 Total 47,300

Cash Account

Date Particulars Amount Date Particulars Amount

15. 02. 20 By Office fixtures a/c 70 03/02/20 To Bank a/c 1,500

25. 02. 20 By Bank a/c 350

19. 02. 20 By Nissan Co. a/c 5,200 25/02/20 To Cash a/c 350

28. 02. 20 By Office fixtures a/c 620

29/02/20 By Balance c/f 12,230

Total 24,350 Total 24,350

Van Account

Date Particulars Amount Date Particulars Amount

01. 02. 20 To Capital a/c 25,000

04. 02. 20 To Bank a/c 4,800

08. 02. 20 To Nissan Co. a/c 5,200

29. 02. 20 By Balance c/f 35,000

Total 35,000 Total 35,000

Capital Account

Date Particulars Amount Date Particulars Amount

01. 02. 20 By Bank a/c 21,500

01. 02. 20 By Van a/c 25,000

01. 02. 20 By Office fixtures a/c 800

29/02/20 To Balance c/f 47,300

Total 47,300 Total 47,300

Cash Account

Date Particulars Amount Date Particulars Amount

15. 02. 20 By Office fixtures a/c 70 03/02/20 To Bank a/c 1,500

25. 02. 20 By Bank a/c 350

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

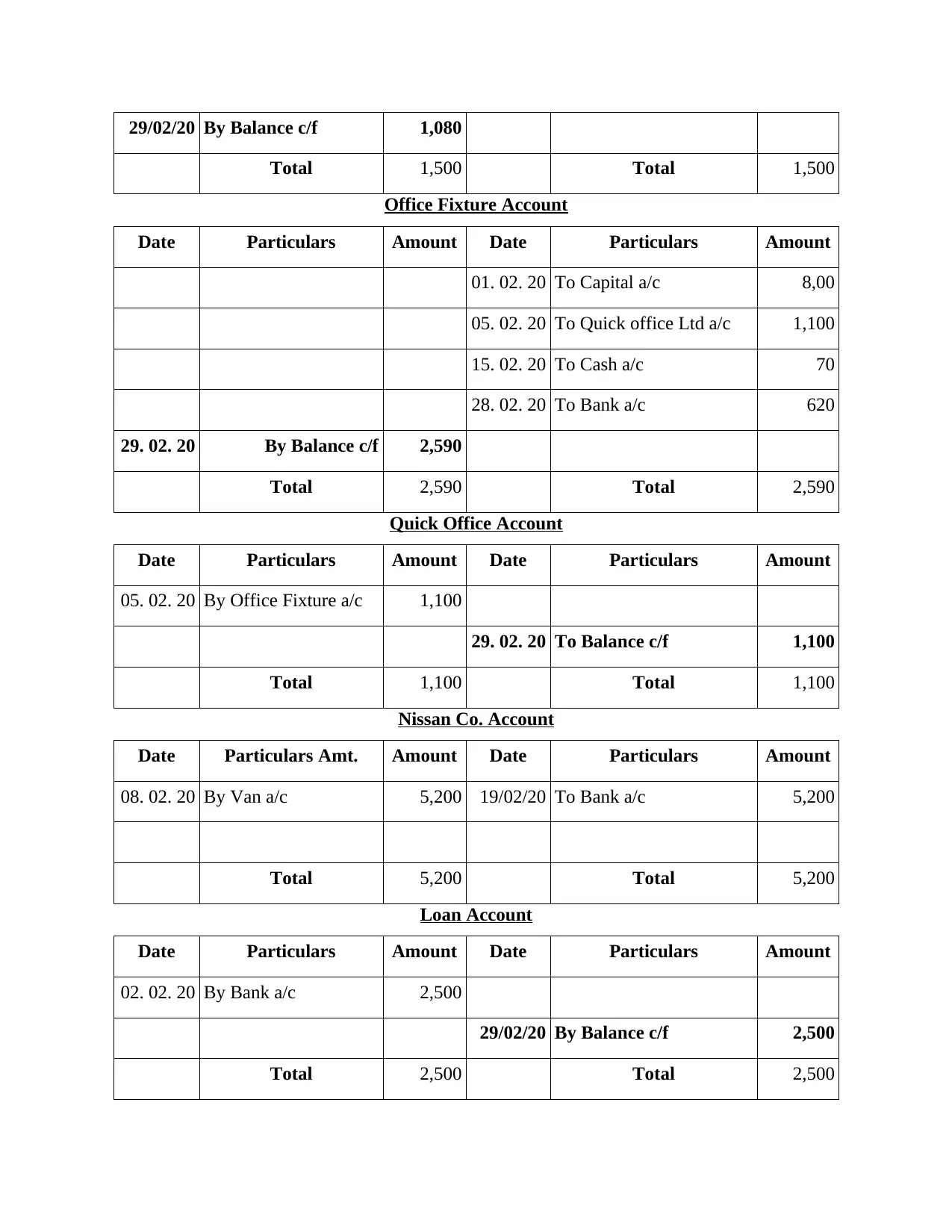

29/02/20 By Balance c/f 1,080

Total 1,500 Total 1,500

Office Fixture Account

Date Particulars Amount Date Particulars Amount

01. 02. 20 To Capital a/c 8,00

05. 02. 20 To Quick office Ltd a/c 1,100

15. 02. 20 To Cash a/c 70

28. 02. 20 To Bank a/c 620

29. 02. 20 By Balance c/f 2,590

Total 2,590 Total 2,590

Quick Office Account

Date Particulars Amount Date Particulars Amount

05. 02. 20 By Office Fixture a/c 1,100

29. 02. 20 To Balance c/f 1,100

Total 1,100 Total 1,100

Nissan Co. Account

Date Particulars Amt. Amount Date Particulars Amount

08. 02. 20 By Van a/c 5,200 19/02/20 To Bank a/c 5,200

Total 5,200 Total 5,200

Loan Account

Date Particulars Amount Date Particulars Amount

02. 02. 20 By Bank a/c 2,500

29/02/20 By Balance c/f 2,500

Total 2,500 Total 2,500

Total 1,500 Total 1,500

Office Fixture Account

Date Particulars Amount Date Particulars Amount

01. 02. 20 To Capital a/c 8,00

05. 02. 20 To Quick office Ltd a/c 1,100

15. 02. 20 To Cash a/c 70

28. 02. 20 To Bank a/c 620

29. 02. 20 By Balance c/f 2,590

Total 2,590 Total 2,590

Quick Office Account

Date Particulars Amount Date Particulars Amount

05. 02. 20 By Office Fixture a/c 1,100

29. 02. 20 To Balance c/f 1,100

Total 1,100 Total 1,100

Nissan Co. Account

Date Particulars Amt. Amount Date Particulars Amount

08. 02. 20 By Van a/c 5,200 19/02/20 To Bank a/c 5,200

Total 5,200 Total 5,200

Loan Account

Date Particulars Amount Date Particulars Amount

02. 02. 20 By Bank a/c 2,500

29/02/20 By Balance c/f 2,500

Total 2,500 Total 2,500

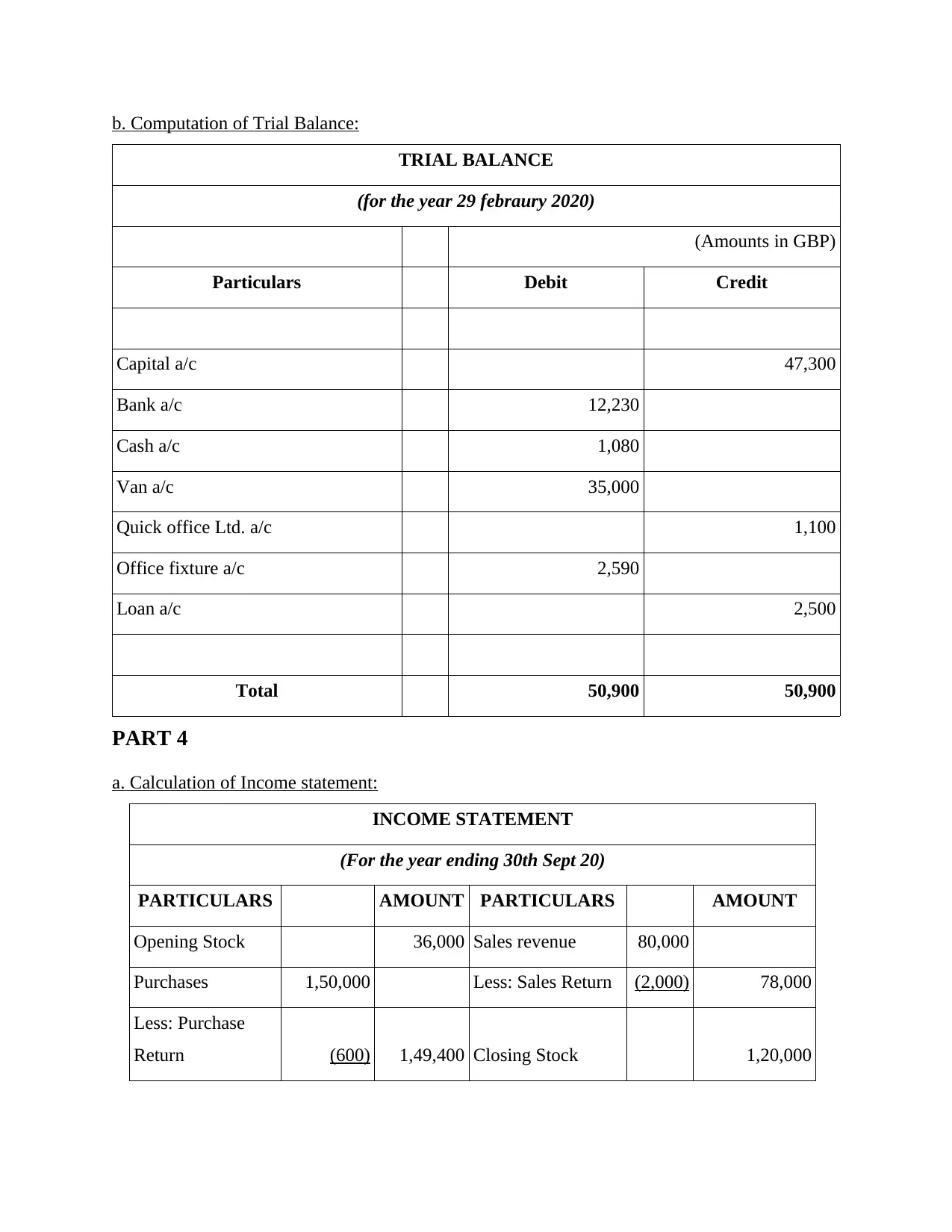

b. Computation of Trial Balance:

TRIAL BALANCE

(for the year 29 febraury 2020)

(Amounts in GBP)

Particulars Debit Credit

Capital a/c 47,300

Bank a/c 12,230

Cash a/c 1,080

Van a/c 35,000

Quick office Ltd. a/c 1,100

Office fixture a/c 2,590

Loan a/c 2,500

Total 50,900 50,900

PART 4

a. Calculation of Income statement:

INCOME STATEMENT

(For the year ending 30th Sept 20)

PARTICULARS AMOUNT PARTICULARS AMOUNT

Opening Stock 36,000 Sales revenue 80,000

Purchases 1,50,000 Less: Sales Return (2,000) 78,000

Less: Purchase

Return (600) 1,49,400 Closing Stock 1,20,000

TRIAL BALANCE

(for the year 29 febraury 2020)

(Amounts in GBP)

Particulars Debit Credit

Capital a/c 47,300

Bank a/c 12,230

Cash a/c 1,080

Van a/c 35,000

Quick office Ltd. a/c 1,100

Office fixture a/c 2,590

Loan a/c 2,500

Total 50,900 50,900

PART 4

a. Calculation of Income statement:

INCOME STATEMENT

(For the year ending 30th Sept 20)

PARTICULARS AMOUNT PARTICULARS AMOUNT

Opening Stock 36,000 Sales revenue 80,000

Purchases 1,50,000 Less: Sales Return (2,000) 78,000

Less: Purchase

Return (600) 1,49,400 Closing Stock 1,20,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

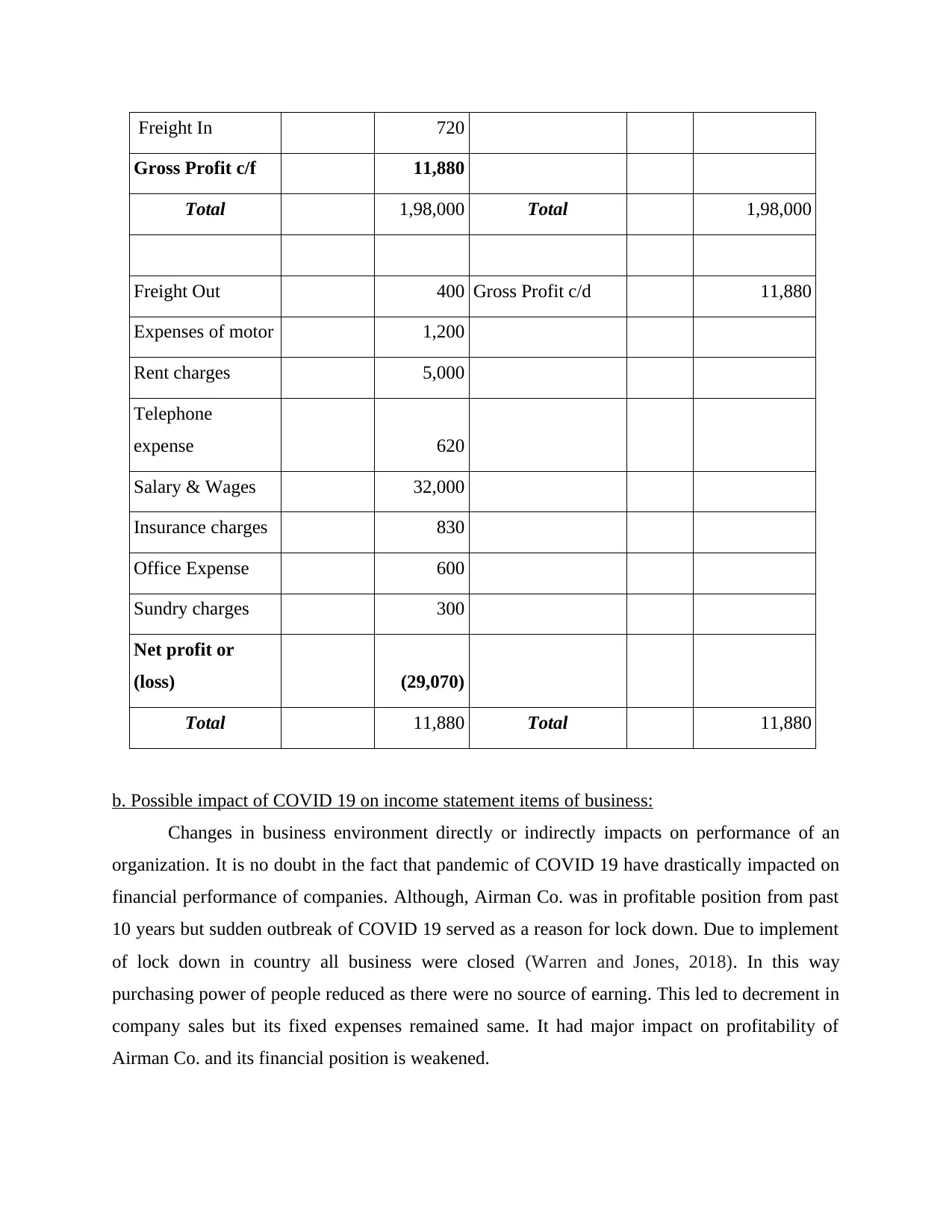

Freight In 720

Gross Profit c/f 11,880

Total 1,98,000 Total 1,98,000

Freight Out 400 Gross Profit c/d 11,880

Expenses of motor 1,200

Rent charges 5,000

Telephone

expense 620

Salary & Wages 32,000

Insurance charges 830

Office Expense 600

Sundry charges 300

Net profit or

(loss) (29,070)

Total 11,880 Total 11,880

b. Possible impact of COVID 19 on income statement items of business:

Changes in business environment directly or indirectly impacts on performance of an

organization. It is no doubt in the fact that pandemic of COVID 19 have drastically impacted on

financial performance of companies. Although, Airman Co. was in profitable position from past

10 years but sudden outbreak of COVID 19 served as a reason for lock down. Due to implement

of lock down in country all business were closed (Warren and Jones, 2018). In this way

purchasing power of people reduced as there were no source of earning. This led to decrement in

company sales but its fixed expenses remained same. It had major impact on profitability of

Airman Co. and its financial position is weakened.

Gross Profit c/f 11,880

Total 1,98,000 Total 1,98,000

Freight Out 400 Gross Profit c/d 11,880

Expenses of motor 1,200

Rent charges 5,000

Telephone

expense 620

Salary & Wages 32,000

Insurance charges 830

Office Expense 600

Sundry charges 300

Net profit or

(loss) (29,070)

Total 11,880 Total 11,880

b. Possible impact of COVID 19 on income statement items of business:

Changes in business environment directly or indirectly impacts on performance of an

organization. It is no doubt in the fact that pandemic of COVID 19 have drastically impacted on

financial performance of companies. Although, Airman Co. was in profitable position from past

10 years but sudden outbreak of COVID 19 served as a reason for lock down. Due to implement

of lock down in country all business were closed (Warren and Jones, 2018). In this way

purchasing power of people reduced as there were no source of earning. This led to decrement in

company sales but its fixed expenses remained same. It had major impact on profitability of

Airman Co. and its financial position is weakened.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

Above report concludes that business transaction is business events that pertains

monetary value or that can be measured in terms of cash or money. Accounting information

plays a key role in decision making process. It is useful for internal as well as external decision-

makers, former consists of managers and employees, while later consists of creditors, customers,

government, and investors. Business transactions are recorded through journal entries and is later

categorised and summarised through ledger and trial balance. Income statement showcase

financial position of company. Additionally, it is noted that COVID 19 have huge impact on

business.

Above report concludes that business transaction is business events that pertains

monetary value or that can be measured in terms of cash or money. Accounting information

plays a key role in decision making process. It is useful for internal as well as external decision-

makers, former consists of managers and employees, while later consists of creditors, customers,

government, and investors. Business transactions are recorded through journal entries and is later

categorised and summarised through ledger and trial balance. Income statement showcase

financial position of company. Additionally, it is noted that COVID 19 have huge impact on

business.

REFERENCES

Books and Journals:

Allen, P., 2018. Artist management for the music business. Routledge.

Berg, C., Davidson, S. and Potts, J., 2018. Ledgers. Available at SSRN 3157421.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Hoerl, R. W. and Snee, R. D., 2020. Statistical thinking: Improving business performance. John

Wiley & Sons.

Jeter, D. C. and Chaney, P. K., 2019. Advanced accounting. John Wiley & Sons.

Roberts, J., 2018. Multinational business service firms: development of multinational

organization structures in the UK business service sector. Routledge.

Warren, C. S. and Farmer, A., 2020. Survey of accounting. Cengage Learning.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2019. Financial accounting. John Wiley &

Sons.

Wiatt, R. G., 2019. From the mainframe to the blockchain. Strategic Finance. 100(7). pp. 26-35.

Books and Journals:

Allen, P., 2018. Artist management for the music business. Routledge.

Berg, C., Davidson, S. and Potts, J., 2018. Ledgers. Available at SSRN 3157421.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Hoerl, R. W. and Snee, R. D., 2020. Statistical thinking: Improving business performance. John

Wiley & Sons.

Jeter, D. C. and Chaney, P. K., 2019. Advanced accounting. John Wiley & Sons.

Roberts, J., 2018. Multinational business service firms: development of multinational

organization structures in the UK business service sector. Routledge.

Warren, C. S. and Farmer, A., 2020. Survey of accounting. Cengage Learning.

Warren, C. S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E., 2019. Financial accounting. John Wiley &

Sons.

Wiatt, R. G., 2019. From the mainframe to the blockchain. Strategic Finance. 100(7). pp. 26-35.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.