University Business Valuation and Analysis Homework Solution 2017

VerifiedAdded on 2020/05/16

|8

|1068

|256

Homework Assignment

AI Summary

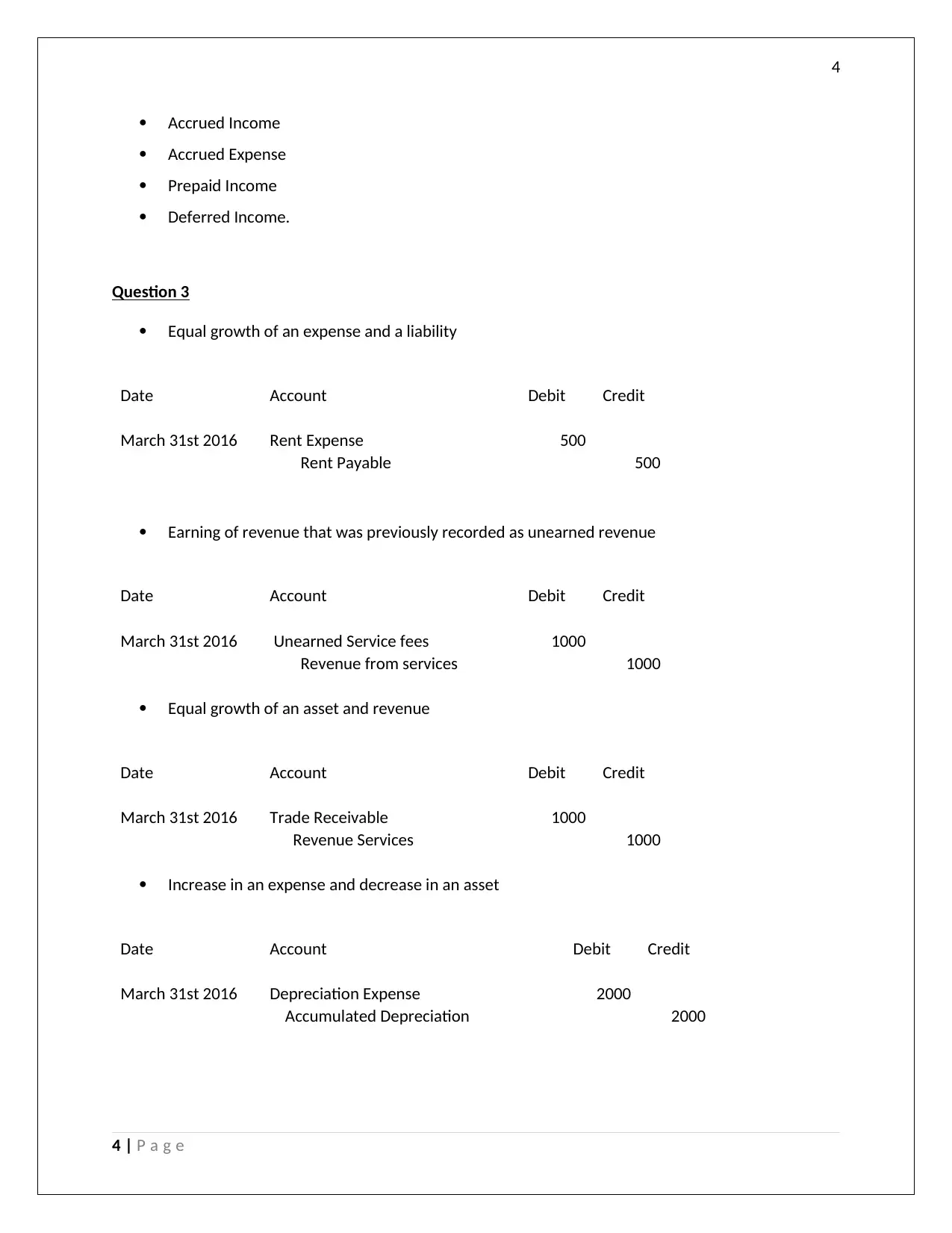

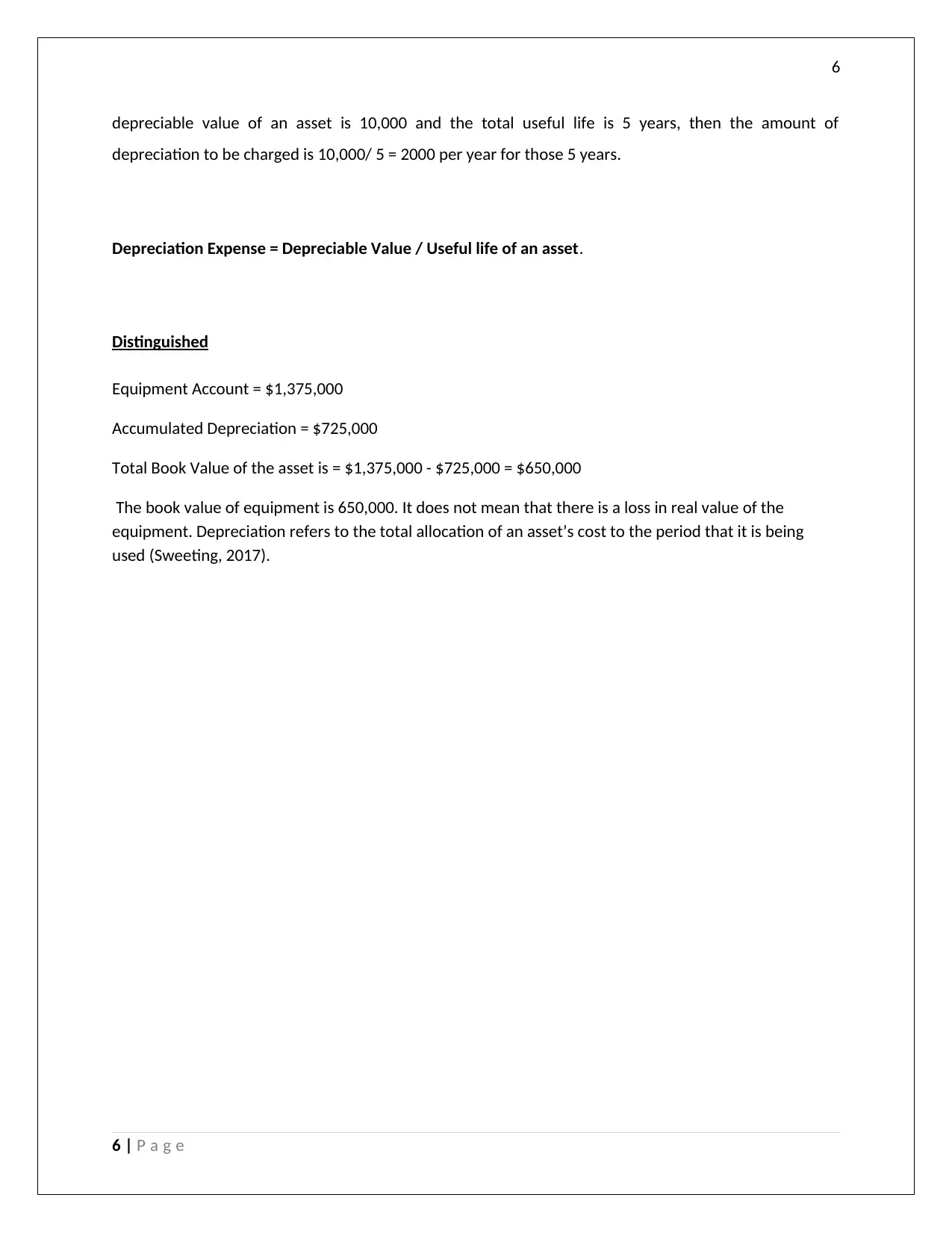

This homework assignment covers key concepts in business valuation and accounting. It begins by differentiating between cash and accrual basis accounting, explaining how transactions are recorded in each method and highlighting the advantages and disadvantages of each. The assignment then focuses on adjusting entries, detailing their importance in ensuring the accuracy of financial statements and providing examples of common types such as accrued income and prepaid expenses. The solution includes examples of journal entries. The assignment also addresses the distinction between depreciation and accumulated depreciation, explaining how depreciation is calculated using the straight-line method and its impact on the balance sheet. Finally, it discusses the book value of an asset and its relationship to depreciation.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.