MBS 665 Business Valuation Report: Towngas China Case Study

VerifiedAdded on 2022/08/11

|7

|1470

|19

Report

AI Summary

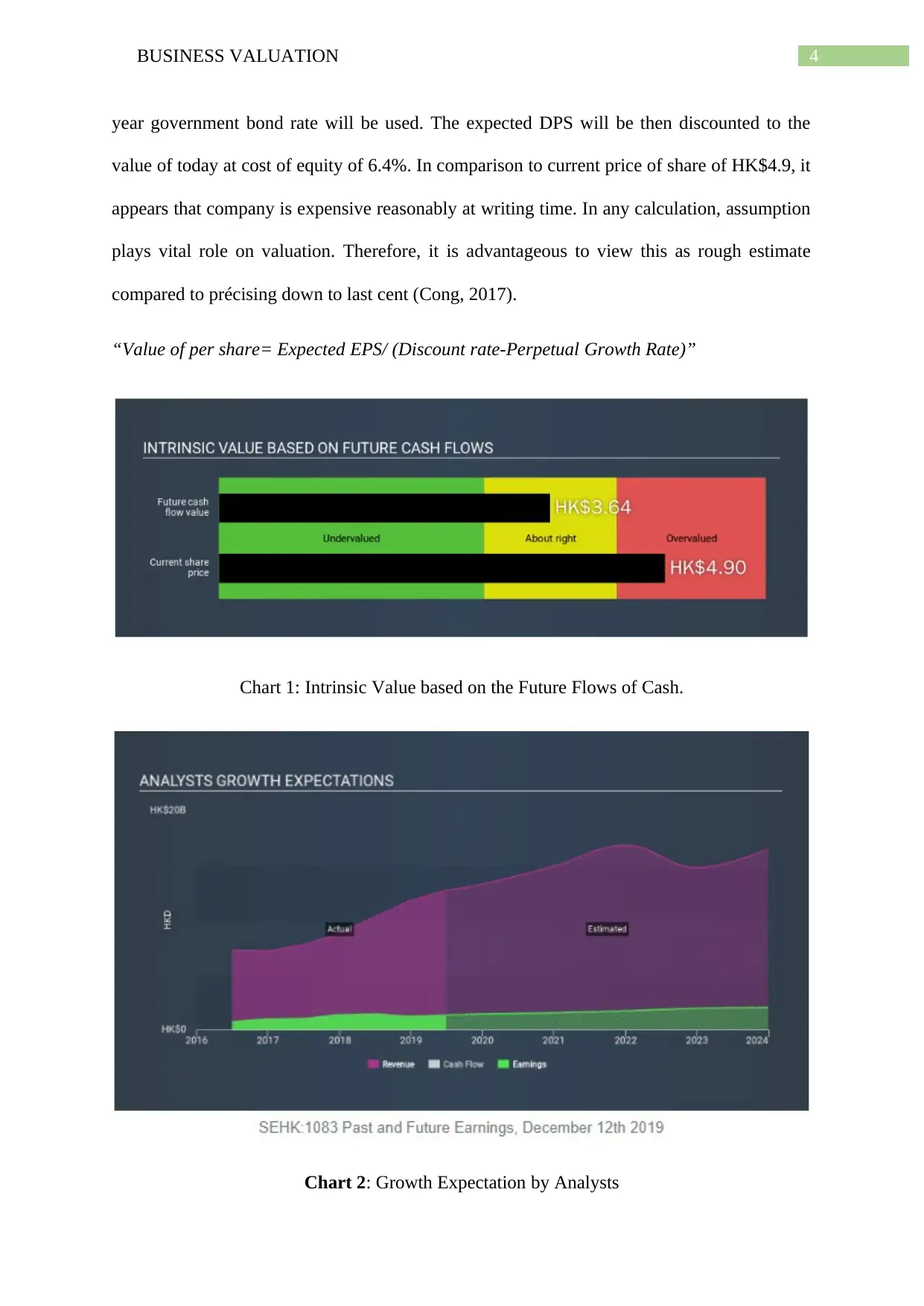

This report presents a critique of an article concerning the business valuation of Towngas China Company Limited. It begins by identifying the key issue: whether the share price of HK$4.9 accurately reflects the company's intrinsic value. The report connects this issue to the broader topic of business valuation, specifically the use of discounted cash flow (DCF) analysis to determine intrinsic value. It evaluates the main issues, including the application of the Gordon Growth Model and the challenges in estimating free cash flows within the gas utilities sector. The report also explores the importance of assumptions in valuation and considers the role of beta in assessing stock volatility. Ultimately, the report concludes that while company valuation is important, it is not the only metric to consider, and the DCF model should be viewed as a guide rather than a definitive tool for stock valuation. The analysis emphasizes the need to consider financial health, future earnings, and other factors in evaluating Towngas China's performance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.