Case Study: BV 4th Edition - Detailed Income Approach Analysis

VerifiedAdded on 2022/11/18

|3

|886

|220

Case Study

AI Summary

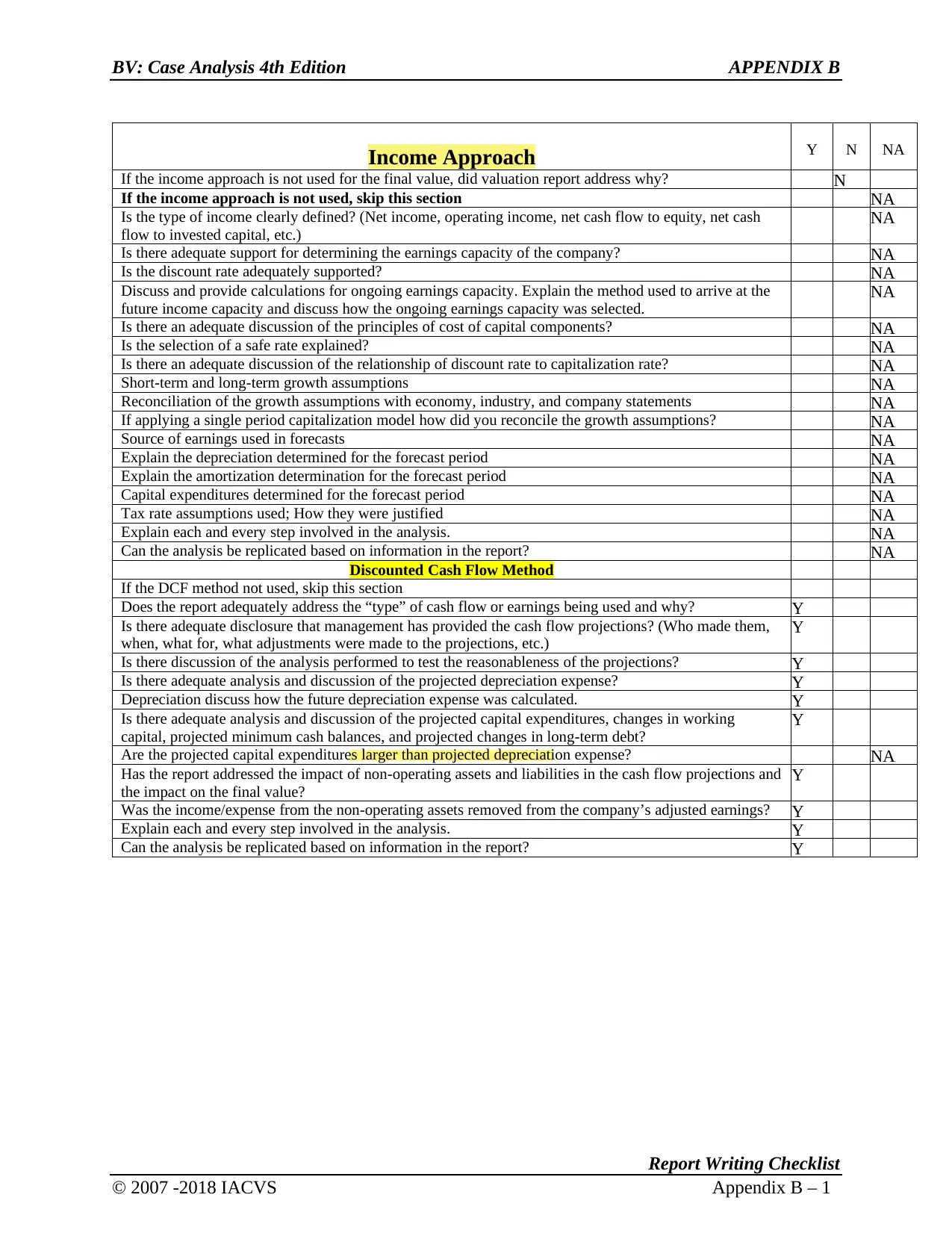

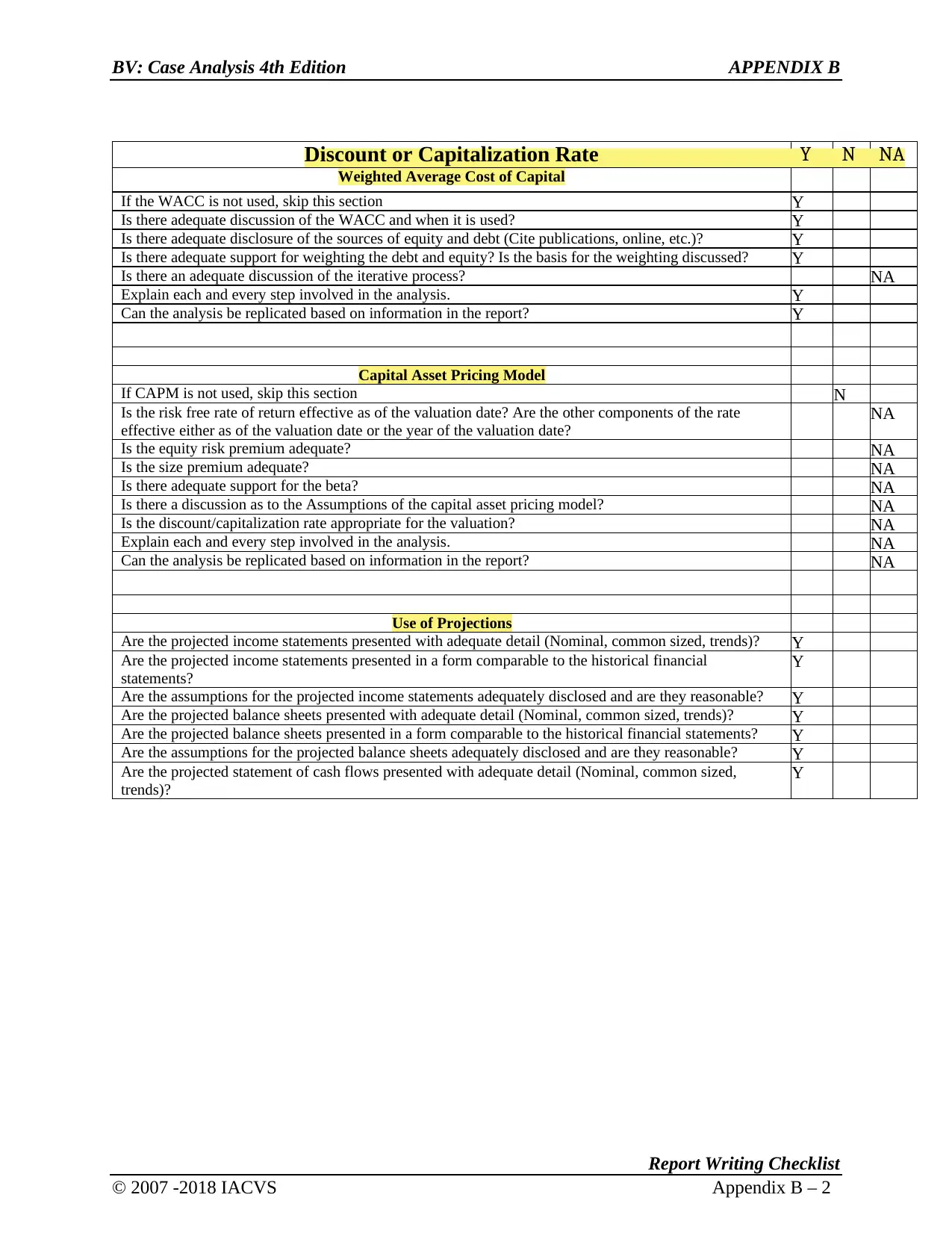

This case study analyzes the income approach for business valuation (BV), specifically referencing the 4th Edition. The analysis meticulously examines various aspects of the income approach, including whether it was used, and if not, the justification provided. It assesses the clarity of income types (net income, operating income, etc.) and the support for determining the company's earnings capacity. The study delves into the discount rate's support, ongoing earnings capacity calculations, and the discussion of cost of capital components. It scrutinizes the selection of a safe rate, the relationship between discount and capitalization rates, growth assumptions (short-term and long-term), and the reconciliation of these assumptions with economic, industry, and company statements. Furthermore, the case study explores the discounted cash flow (DCF) method, including the type of cash flow used, disclosure of management's projections, reasonableness testing of projections, depreciation and capital expenditures, and the impact of non-operating assets and liabilities. It also examines the discount or capitalization rate, including the weighted average cost of capital (WACC) and the capital asset pricing model (CAPM). The analysis evaluates the use of projections, including the detail and comparability of projected income statements, balance sheets, and statements of cash flows. The document concludes with a detailed report writing checklist from Appendix B of the BV 4th Edition.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.