Comprehensive Audit Report: BWP Trust Company Financial Analysis 2018

VerifiedAdded on 2022/09/17

|12

|2806

|25

Report

AI Summary

This report provides a comprehensive analysis of the audit of BWP Trust Company, focusing on the year 2018. The report begins by determining the level of materiality used in the audit, emphasizing its significance in ensuring the accuracy and fairness of financial statements. It delves into the application of materiality principles, considering qualitative aspects like investment property valuation and the judgments made by management. The report then moves on to a preliminary analytical review, assessing the company's financial health through liquidity, activity, efficiency, and profitability ratios. It highlights key trends and potential risks, such as decreasing liquidity and falling profitability ratios. The analysis continues with a review of the cash flow statement, examining operational, investing, and financing activities. Finally, the report concludes with a review of the audit report, summarizing the auditor's opinion on the financial statements and highlighting key findings. The report also includes draft notes and disclosures, providing insights into accounting estimates and judgments made by BWP Trust Company.

Running head: AUDIT AND ETHICS

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note:

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT

Table of Contents

Part 1................................................................................................................................................2

Materiality Principles Application in the context of Auditing....................................................2

Draft Notes and Disclosures........................................................................................................4

Part 2................................................................................................................................................5

Preliminary Analytical Review....................................................................................................5

Part 3................................................................................................................................................7

Cash Flows Statement Analysis...................................................................................................7

Audit Report Review...................................................................................................................9

References......................................................................................................................................10

Table of Contents

Part 1................................................................................................................................................2

Materiality Principles Application in the context of Auditing....................................................2

Draft Notes and Disclosures........................................................................................................4

Part 2................................................................................................................................................5

Preliminary Analytical Review....................................................................................................5

Part 3................................................................................................................................................7

Cash Flows Statement Analysis...................................................................................................7

Audit Report Review...................................................................................................................9

References......................................................................................................................................10

2AUDIT

Part 1

Materiality Principles Application in the context of Auditing

Materiality in the context of Audit shows or represents the Opinion of Auditors in the

context of Annual statements preparation whether they are free from all accounting and auditing

errors. Materiality shows that the Annual report of BWP Trust Company are well prepared and

applicable in compliance and adherence with the presented Annual Reporting Framework such

as IFRS. BWP Trust Company taken into consideration for the reviewing and analysing is the

BWP Trust Company that is operating in the Australian Region as a Real Estate Investment

Trust Company (Lai, Melloni & Stacchezzini, 2017).

In terms of materiality the concept states that the auditor of BWP Trust Company should

take appropriate steps in order to determine whether the Annual statement presented by BWP

Trust Company matches with the Corporation Act upon which the Annual statement of BWP

Trust Company were prepared. There are various items in the presented Annual statement of the

BWP Trust Company and the same has been classified in accordance with the accounting

policies and judgements used by the management for the purpose of classifying and reporting the

expenses or income (Boiral et al., 2019). Materiality in the context of Auditing plays an

important role when there are various judgements and assumptions made by a company for the

purpose of preparing and presenting the Annual statement of BWP Trust Company for the

Annual year. In this context it is important the Auditors review the Annual statement of BWP

Trust Company whereby it should reflect a true and fair view of the Annual Position of the BWP

Trust Company for the time period taken into consideration (Chen & Tsay, 2017). It is the key

responsibility of the Auditor to obtain reasonable assurance and materiality about whether the

Part 1

Materiality Principles Application in the context of Auditing

Materiality in the context of Audit shows or represents the Opinion of Auditors in the

context of Annual statements preparation whether they are free from all accounting and auditing

errors. Materiality shows that the Annual report of BWP Trust Company are well prepared and

applicable in compliance and adherence with the presented Annual Reporting Framework such

as IFRS. BWP Trust Company taken into consideration for the reviewing and analysing is the

BWP Trust Company that is operating in the Australian Region as a Real Estate Investment

Trust Company (Lai, Melloni & Stacchezzini, 2017).

In terms of materiality the concept states that the auditor of BWP Trust Company should

take appropriate steps in order to determine whether the Annual statement presented by BWP

Trust Company matches with the Corporation Act upon which the Annual statement of BWP

Trust Company were prepared. There are various items in the presented Annual statement of the

BWP Trust Company and the same has been classified in accordance with the accounting

policies and judgements used by the management for the purpose of classifying and reporting the

expenses or income (Boiral et al., 2019). Materiality in the context of Auditing plays an

important role when there are various judgements and assumptions made by a company for the

purpose of preparing and presenting the Annual statement of BWP Trust Company for the

Annual year. In this context it is important the Auditors review the Annual statement of BWP

Trust Company whereby it should reflect a true and fair view of the Annual Position of the BWP

Trust Company for the time period taken into consideration (Chen & Tsay, 2017). It is the key

responsibility of the Auditor to obtain reasonable assurance and materiality about whether the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT

Annual Report as a whole is considerable free from material misstatement that could affect the

quality of Annual information presented. The ability of usage and application of Annual

information for the purpose of analysing the stakeholders of BWP Trust Company should be

present. Misstatements can generally arise from fraud or errors whereby the same is considered

material if the same on an individual or an aggregate basis could affect the Annual performance.

The presented qualitative materiality items that are considered in the Annual statement of BWP

Trust Company is the estimates and judgements made for the purpose of valuation of the

Investment Property that was valued at $2.358 million for BWP Trust Company (Ribera, 2017).

The judgement required for the purpose of assessing the choosing and selecting the capitalisation

of income valuation process and method as the only primary source of valuation methodology

for the RWP Trust’s investment properties under the various presented accounting standards

(Wee et al., 2016).

For arriving at the estimate of auditing planning materiality RWP auditor’s would be

considering various estimates and the highest value that is shown in the Annual statement of

BWP Trust Company that the auditor would be making for the purpose of calculation of

planning overall materiality of the business. The auditor has applied various judgements that can

be better used for the calculating an overall estimated figure of the planning materiality in the

business that is being considered for the purpose of business evaluation (González-Díaz &

García-Fernández, 2016). A total of 2% would be taken into consideration of the purpose of

planning the overall accurate estimates of planning materiality in the business. Planning

materiality can be well computed as presented below:

Planning Materiality = Total Assets of Company * Estimated Percentage

=$ 2,369,529*2%

Annual Report as a whole is considerable free from material misstatement that could affect the

quality of Annual information presented. The ability of usage and application of Annual

information for the purpose of analysing the stakeholders of BWP Trust Company should be

present. Misstatements can generally arise from fraud or errors whereby the same is considered

material if the same on an individual or an aggregate basis could affect the Annual performance.

The presented qualitative materiality items that are considered in the Annual statement of BWP

Trust Company is the estimates and judgements made for the purpose of valuation of the

Investment Property that was valued at $2.358 million for BWP Trust Company (Ribera, 2017).

The judgement required for the purpose of assessing the choosing and selecting the capitalisation

of income valuation process and method as the only primary source of valuation methodology

for the RWP Trust’s investment properties under the various presented accounting standards

(Wee et al., 2016).

For arriving at the estimate of auditing planning materiality RWP auditor’s would be

considering various estimates and the highest value that is shown in the Annual statement of

BWP Trust Company that the auditor would be making for the purpose of calculation of

planning overall materiality of the business. The auditor has applied various judgements that can

be better used for the calculating an overall estimated figure of the planning materiality in the

business that is being considered for the purpose of business evaluation (González-Díaz &

García-Fernández, 2016). A total of 2% would be taken into consideration of the purpose of

planning the overall accurate estimates of planning materiality in the business. Planning

materiality can be well computed as presented below:

Planning Materiality = Total Assets of Company * Estimated Percentage

=$ 2,369,529*2%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT

=$ 47,390

The amount derived in the above equation will be considered in evaluating he

performance materiality. The computed figure would be helping the auditor BWP Trust

Company in assessing the various items presented in the Annual statements of BWP Trust

Company (Swart, 2018).

Draft Notes and Disclosures

The draft notes that are presented by BWP Trust Company are prepared and presented by

BWP Trust Company in accordance with the various accounting estimates that are used by BWP

Trust Company for the purpose of the computation of the overall materiality and the value of the

assets (Baldacchino, Tabone & Demanuele, 2017).

Investment Properties: The investment property is measured at cost value and is then

subsequently measured at the cost and subsequent fair value recognising any changes in the

profit and loss account. The key judgement that has been made by the management of BWP

Trust Company is that the valuation of BWP Trust Company would be done at the end of the

each balance date thereby assessing the fair value with the help of generally accepted valuation

criteria, methodology and assumptions taken into considerations.

Financial Instruments: The key judgements that has been applied for the purpose of the

valuation of the Financial instruments is with the help of the current interest rate thereby using

the applicable or the current interest rate for the purpose of discounting the cash flows associated

or flowing to BWP Trust Company.

=$ 47,390

The amount derived in the above equation will be considered in evaluating he

performance materiality. The computed figure would be helping the auditor BWP Trust

Company in assessing the various items presented in the Annual statements of BWP Trust

Company (Swart, 2018).

Draft Notes and Disclosures

The draft notes that are presented by BWP Trust Company are prepared and presented by

BWP Trust Company in accordance with the various accounting estimates that are used by BWP

Trust Company for the purpose of the computation of the overall materiality and the value of the

assets (Baldacchino, Tabone & Demanuele, 2017).

Investment Properties: The investment property is measured at cost value and is then

subsequently measured at the cost and subsequent fair value recognising any changes in the

profit and loss account. The key judgement that has been made by the management of BWP

Trust Company is that the valuation of BWP Trust Company would be done at the end of the

each balance date thereby assessing the fair value with the help of generally accepted valuation

criteria, methodology and assumptions taken into considerations.

Financial Instruments: The key judgements that has been applied for the purpose of the

valuation of the Financial instruments is with the help of the current interest rate thereby using

the applicable or the current interest rate for the purpose of discounting the cash flows associated

or flowing to BWP Trust Company.

5AUDIT

Part 2

Preliminary Analytical Review

The key Preliminary Analytical Review that BWP Trust Company can deploy is the

application of Annual ratio that can be well utilized for the purpose of identifying any risks in the

business. The compliance procedures where various aspects of BWP Trust Company including

the profitability, liquidity and leverage position of BWP Trust Company would be assessed.

Liquidity Ratio: The liquidity ratio for BWP Trust Company explains the coverage of the

current assets of BWP Trust Company in contrast to the current liabilities of BWP Trust

Company. The current ratio for BWP Trust Company has been decreasing at a very poor rate

improving the chances of liquidity crisis that BWP Trust Company might have during the

Annual year. During the year 2018, it was found that the current ratio for BWP Trust Company

has decreased consistently from 0.71 times in year 2017 to around 0.32 times in the year 2018

due to classification of interest bearing loans and borrowings in the current liabilities. The

auditor of BWP Trust Company should take preemptive and necessary actions for the purpose of

evaluation of the liquidity of BWP Trust Company (Reports, 2019).

Activity Ratio: The activity ratio for BWP Trust Company shows the various activities

undertaken by BWP Trust Company and the same was evaluated with the help of the receivables

turnover ratio. The receivables turnover ratio for BWP Trust Company has consistently increased

for BWP Trust Company in the trend period taken into consideration stating that BWP Trust

Company’s ability in collecting the accounts receivables from the debtors of BWP Trust

Company has increased consistently over the due course period which is good for BWP Trust

Company.

Part 2

Preliminary Analytical Review

The key Preliminary Analytical Review that BWP Trust Company can deploy is the

application of Annual ratio that can be well utilized for the purpose of identifying any risks in the

business. The compliance procedures where various aspects of BWP Trust Company including

the profitability, liquidity and leverage position of BWP Trust Company would be assessed.

Liquidity Ratio: The liquidity ratio for BWP Trust Company explains the coverage of the

current assets of BWP Trust Company in contrast to the current liabilities of BWP Trust

Company. The current ratio for BWP Trust Company has been decreasing at a very poor rate

improving the chances of liquidity crisis that BWP Trust Company might have during the

Annual year. During the year 2018, it was found that the current ratio for BWP Trust Company

has decreased consistently from 0.71 times in year 2017 to around 0.32 times in the year 2018

due to classification of interest bearing loans and borrowings in the current liabilities. The

auditor of BWP Trust Company should take preemptive and necessary actions for the purpose of

evaluation of the liquidity of BWP Trust Company (Reports, 2019).

Activity Ratio: The activity ratio for BWP Trust Company shows the various activities

undertaken by BWP Trust Company and the same was evaluated with the help of the receivables

turnover ratio. The receivables turnover ratio for BWP Trust Company has consistently increased

for BWP Trust Company in the trend period taken into consideration stating that BWP Trust

Company’s ability in collecting the accounts receivables from the debtors of BWP Trust

Company has increased consistently over the due course period which is good for BWP Trust

Company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT

Efficiency Ratio: The Efficiency Ratio for BWP Trust Company states the efficiency shown by

the management of BWP Trust Company in utilizing and operating the assets of BWP Trust

Company. The fixed asset turnover ratio for BWP Trust Company has fallen in the trend period

due to higher increase in the base value that is asset value in consideration to the total sales of

BWP Trust Company (Williams & Dobelman, 2017). The same applies for the total asset

turnover ratio for BWP Trust Company. It is recommended that the auditors of BWP Trust

Company takes preemptive actions and measures in order to better assess and evaluate the

Annual position of BWP Trust Company for the defined period of time period.

Profitability Ratio: The profitability ratio can be well evaluated in order to define the return

generated by BWP Trust Company in the form of net income generated by BWP Trust Company

for the trend period taken into consideration (Robinson et al., 2015). The return on assets for

BWP Trust Company has fallen in the trend period of 2015-2018 due to the fall in the

profitability of BWP Trust Company and the consistent increase in the total assets of BWP Trust

Company. On the other hand, the return on equity for BWP Trust Company has also fallen

significantly under the trend period due to the consistent rise in the equity value as contrasted to

the decrease of the net profitability of BWP Trust Company. The net profit ratio for BWP Trust

Company also saw a marginal decrease in the trend period. It is equally important for the

auditors of BWP Trust Company to analyze the various aspects and reason behind the

subsequent fall in the revenue baser and the overall profitability of BWP Trust Company for the

trend-period taken into consideration for BWP Trust Company (Lakshmi, Martin & Venkatesan,

2015).

Leverage and Coverage Ratio: The leverage and coverage ratio taken into consideration for

BWP Trust Company shows the overall Annual position of the debt when contrasted to the

Efficiency Ratio: The Efficiency Ratio for BWP Trust Company states the efficiency shown by

the management of BWP Trust Company in utilizing and operating the assets of BWP Trust

Company. The fixed asset turnover ratio for BWP Trust Company has fallen in the trend period

due to higher increase in the base value that is asset value in consideration to the total sales of

BWP Trust Company (Williams & Dobelman, 2017). The same applies for the total asset

turnover ratio for BWP Trust Company. It is recommended that the auditors of BWP Trust

Company takes preemptive actions and measures in order to better assess and evaluate the

Annual position of BWP Trust Company for the defined period of time period.

Profitability Ratio: The profitability ratio can be well evaluated in order to define the return

generated by BWP Trust Company in the form of net income generated by BWP Trust Company

for the trend period taken into consideration (Robinson et al., 2015). The return on assets for

BWP Trust Company has fallen in the trend period of 2015-2018 due to the fall in the

profitability of BWP Trust Company and the consistent increase in the total assets of BWP Trust

Company. On the other hand, the return on equity for BWP Trust Company has also fallen

significantly under the trend period due to the consistent rise in the equity value as contrasted to

the decrease of the net profitability of BWP Trust Company. The net profit ratio for BWP Trust

Company also saw a marginal decrease in the trend period. It is equally important for the

auditors of BWP Trust Company to analyze the various aspects and reason behind the

subsequent fall in the revenue baser and the overall profitability of BWP Trust Company for the

trend-period taken into consideration for BWP Trust Company (Lakshmi, Martin & Venkatesan,

2015).

Leverage and Coverage Ratio: The leverage and coverage ratio taken into consideration for

BWP Trust Company shows the overall Annual position of the debt when contrasted to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT

equity and assets value in BWP Trust Company. The debt to equity ratio for BWP Trust

Company ratio has consistently fallen for BWP Trust Company showing that BWP Trust

Company is decreasing the usage and application of debt financing in the business in order to

reduce the associated Annual risk and the high amount of interest cost that is paid by BWP Trust

Company. However, well in terms of coverage ratio for BWP Trust Company it can be well

stated that the total debt to total assets ratio for BWP Trust Company has fallen on the other hand

for BWP Trust Company in the trend period stating that BWP Trust Company is increasing the

value of assets of BWP Trust Company in contrast to the debt position of BWP Trust Company

for better coverage and managed Annual exposures that BWP Trust Company has in the Annual

statement of BWP Trust Company.

Part 3

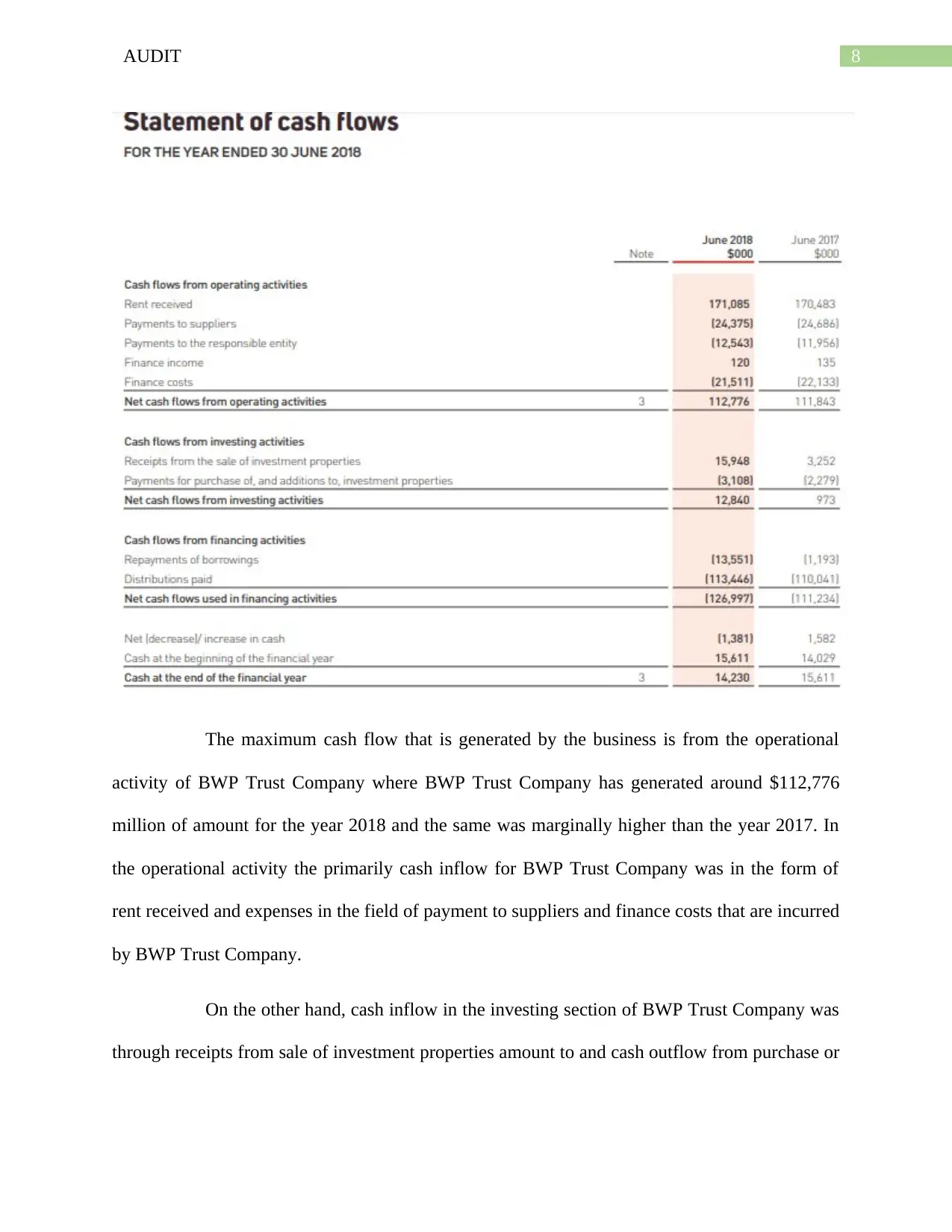

Cash Flows Statement Analysis

The cash flow statement of BWP Trust Company shows the various aspects of BWP

Trust Company including the operational activities carried out by BWP Trust Company

suggesting the cash inflows sources and expenses that BWP Trust Company has incurred. N the

other hand, the investing portions relates to the various purchase and sales of non-current assets

of BWP Trust Company. Finally the financing activities carried out in the form of procurement

and repayment of finance is well done with the help of financing activities (Annual Report,

2018). The cash flow statement of BWP Trust Company is provided below:

equity and assets value in BWP Trust Company. The debt to equity ratio for BWP Trust

Company ratio has consistently fallen for BWP Trust Company showing that BWP Trust

Company is decreasing the usage and application of debt financing in the business in order to

reduce the associated Annual risk and the high amount of interest cost that is paid by BWP Trust

Company. However, well in terms of coverage ratio for BWP Trust Company it can be well

stated that the total debt to total assets ratio for BWP Trust Company has fallen on the other hand

for BWP Trust Company in the trend period stating that BWP Trust Company is increasing the

value of assets of BWP Trust Company in contrast to the debt position of BWP Trust Company

for better coverage and managed Annual exposures that BWP Trust Company has in the Annual

statement of BWP Trust Company.

Part 3

Cash Flows Statement Analysis

The cash flow statement of BWP Trust Company shows the various aspects of BWP

Trust Company including the operational activities carried out by BWP Trust Company

suggesting the cash inflows sources and expenses that BWP Trust Company has incurred. N the

other hand, the investing portions relates to the various purchase and sales of non-current assets

of BWP Trust Company. Finally the financing activities carried out in the form of procurement

and repayment of finance is well done with the help of financing activities (Annual Report,

2018). The cash flow statement of BWP Trust Company is provided below:

8AUDIT

The maximum cash flow that is generated by the business is from the operational

activity of BWP Trust Company where BWP Trust Company has generated around $112,776

million of amount for the year 2018 and the same was marginally higher than the year 2017. In

the operational activity the primarily cash inflow for BWP Trust Company was in the form of

rent received and expenses in the field of payment to suppliers and finance costs that are incurred

by BWP Trust Company.

On the other hand, cash inflow in the investing section of BWP Trust Company was

through receipts from sale of investment properties amount to and cash outflow from purchase or

The maximum cash flow that is generated by the business is from the operational

activity of BWP Trust Company where BWP Trust Company has generated around $112,776

million of amount for the year 2018 and the same was marginally higher than the year 2017. In

the operational activity the primarily cash inflow for BWP Trust Company was in the form of

rent received and expenses in the field of payment to suppliers and finance costs that are incurred

by BWP Trust Company.

On the other hand, cash inflow in the investing section of BWP Trust Company was

through receipts from sale of investment properties amount to and cash outflow from purchase or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT

payment of investment properties. The cash inflows from the investment activities amounted to

around $12,840 which saw a massive increase from the last year figure which was $973.

The financing activities saw a repayment of borrowings and distributions that were

paid out by BWP Trust Company which BWP Trust Company has paid out in the trend period.

Repayment of borrowings was done in order to strategize the operations of BWP Trust Company

by giving more focus on equity financing and removing the Annual risk of BWP Trust Company

for the trend period.

Audit Report Review

The Audit Report Presented by BWP Trust Company states that the Annual report of

BWP Trust Company gives a true and a fair view about the Annual position of BWP Trust

Company and for the Annual performance for BWP Trust Company in the trend period analyzed.

Base for Opinion: The Audit of the Annual statement of BWP Trust Company was done with

the help of Australian Accounting Standards for providing the basis of opinion (Annual report,

2016).

Important Audit Matters: Valuation of the presented Investment Properties and Valuation of

Annual Instruments and Assets along with the various assumption and accounting estimates that

were used by BWP Trust Company for the purpose of assessing the fair value in reaction to

BWP Trust Company. The presented annual reports also complied with all the relevant

applicable accounting standards and the Corporation Act 2001. Compliance with the various

accounting standards shows that that the auditor has issued an unqualified audit report to BWP

Trust Company signifying that the information contained in the annual report is material enough

for the purpose of assessment.

payment of investment properties. The cash inflows from the investment activities amounted to

around $12,840 which saw a massive increase from the last year figure which was $973.

The financing activities saw a repayment of borrowings and distributions that were

paid out by BWP Trust Company which BWP Trust Company has paid out in the trend period.

Repayment of borrowings was done in order to strategize the operations of BWP Trust Company

by giving more focus on equity financing and removing the Annual risk of BWP Trust Company

for the trend period.

Audit Report Review

The Audit Report Presented by BWP Trust Company states that the Annual report of

BWP Trust Company gives a true and a fair view about the Annual position of BWP Trust

Company and for the Annual performance for BWP Trust Company in the trend period analyzed.

Base for Opinion: The Audit of the Annual statement of BWP Trust Company was done with

the help of Australian Accounting Standards for providing the basis of opinion (Annual report,

2016).

Important Audit Matters: Valuation of the presented Investment Properties and Valuation of

Annual Instruments and Assets along with the various assumption and accounting estimates that

were used by BWP Trust Company for the purpose of assessing the fair value in reaction to

BWP Trust Company. The presented annual reports also complied with all the relevant

applicable accounting standards and the Corporation Act 2001. Compliance with the various

accounting standards shows that that the auditor has issued an unqualified audit report to BWP

Trust Company signifying that the information contained in the annual report is material enough

for the purpose of assessment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT

References

Annual report (2016). Bwptrust.com.au. Retrieved 25 August 2019, from

https://www.bwptrust.com.au/site/content/annualreport/2016/files/assets/common/

downloads/2016%20Online%20Annual%20Report.pdf

Annual Report (2018). Bwptrust.com.au. Retrieved 25 August 2019, from

https://www.bwptrust.com.au/site/PDF/1690_0/2018AnnualReport

Baldacchino, P. J., Tabone, N., & Demanuele, R. (2017). Materiality disclosures in statutory

auditing: a Maltese perspective.

Boiral, O., Heras-Saizarbitoria, I., & Brotherton, M. C. (2019). Assessing and improving the

quality of sustainability reports: The auditors’ perspective. Journal of Business

Ethics, 155(3), 703-721.

Chen, S., & Tsay, B. Y. (2017). Refer to materiality as a legal concept. Journal of Corporate

Accounting & Finance, 28(2), 55-61.

González-Díaz, B., & García-Fernández, R. (2016). Auditing. Global Encyclopedia of Public

Administration, Public Policy, and Governance, 1-18.

Ko, Y. C., Fujita, H., & Li, T. (2017). An evidential analysis of Altman Z-score for Annual

predictions: Case study on solar energy companies. Applied Soft Computing, 52, 748-759.

Lai, A., Melloni, G., & Stacchezzini, R. (2017). What does materiality mean to integrated

reporting preparers? An empirical exploration. Meditari Accountancy Research, 25(4),

533-552.

References

Annual report (2016). Bwptrust.com.au. Retrieved 25 August 2019, from

https://www.bwptrust.com.au/site/content/annualreport/2016/files/assets/common/

downloads/2016%20Online%20Annual%20Report.pdf

Annual Report (2018). Bwptrust.com.au. Retrieved 25 August 2019, from

https://www.bwptrust.com.au/site/PDF/1690_0/2018AnnualReport

Baldacchino, P. J., Tabone, N., & Demanuele, R. (2017). Materiality disclosures in statutory

auditing: a Maltese perspective.

Boiral, O., Heras-Saizarbitoria, I., & Brotherton, M. C. (2019). Assessing and improving the

quality of sustainability reports: The auditors’ perspective. Journal of Business

Ethics, 155(3), 703-721.

Chen, S., & Tsay, B. Y. (2017). Refer to materiality as a legal concept. Journal of Corporate

Accounting & Finance, 28(2), 55-61.

González-Díaz, B., & García-Fernández, R. (2016). Auditing. Global Encyclopedia of Public

Administration, Public Policy, and Governance, 1-18.

Ko, Y. C., Fujita, H., & Li, T. (2017). An evidential analysis of Altman Z-score for Annual

predictions: Case study on solar energy companies. Applied Soft Computing, 52, 748-759.

Lai, A., Melloni, G., & Stacchezzini, R. (2017). What does materiality mean to integrated

reporting preparers? An empirical exploration. Meditari Accountancy Research, 25(4),

533-552.

11AUDIT

Lakshmi, T. M., Martin, A., & Venkatesan, V. P. (2015). A genetic bankrupt ratio analysis tool

using a genetic algorithm to identify influencing Annual ratios. IEEE Transactions on

Evolutionary Computation, 20(1), 38-51.

Reports. (2019). Investors BWP Trust | . Bwptrust.com.au. Retrieved 25 August 2019, from

https://www.bwptrust.com.au/site/investors/reports/reports1

Ribera, J. M. (2017). MATERIALITY IN SUSTAINABILITY REPORTING: MULTIPLE

STANDARDS AND LOOKING FOR COMMON PRINCIPLES AND

MEASUREMENT. THE CASE OF THE SEVEN BIGGEST GROUPS IN

SPAIN. European Accounting and Management Review (EAMR), 4(1), 108-147.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International Annual

statement analysis. John Wiley & Sons.

Swart, J. J. (2018). Audit methodologies: developing an integrated planning model

incorporating audit materiality, risk and sampling (Doctoral dissertation, North-West

University).

Wee, M., Tarca, A., Krug, L., Aerts, W., Pink, P., & Tilling, M. (2016). Factors affecting

preparers’ and auditors’ judgements about materiality and conciseness in integrated

reporting. ACCA, London.[Google Scholar].

Williams, E. E., & Dobelman, J. A. (2017). Annual statement analysis. World Scientific Book

Chapters, 109-169.

Lakshmi, T. M., Martin, A., & Venkatesan, V. P. (2015). A genetic bankrupt ratio analysis tool

using a genetic algorithm to identify influencing Annual ratios. IEEE Transactions on

Evolutionary Computation, 20(1), 38-51.

Reports. (2019). Investors BWP Trust | . Bwptrust.com.au. Retrieved 25 August 2019, from

https://www.bwptrust.com.au/site/investors/reports/reports1

Ribera, J. M. (2017). MATERIALITY IN SUSTAINABILITY REPORTING: MULTIPLE

STANDARDS AND LOOKING FOR COMMON PRINCIPLES AND

MEASUREMENT. THE CASE OF THE SEVEN BIGGEST GROUPS IN

SPAIN. European Accounting and Management Review (EAMR), 4(1), 108-147.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International Annual

statement analysis. John Wiley & Sons.

Swart, J. J. (2018). Audit methodologies: developing an integrated planning model

incorporating audit materiality, risk and sampling (Doctoral dissertation, North-West

University).

Wee, M., Tarca, A., Krug, L., Aerts, W., Pink, P., & Tilling, M. (2016). Factors affecting

preparers’ and auditors’ judgements about materiality and conciseness in integrated

reporting. ACCA, London.[Google Scholar].

Williams, E. E., & Dobelman, J. A. (2017). Annual statement analysis. World Scientific Book

Chapters, 109-169.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.