Derivatives Analysis: CAC 40 Futures, Options, and Structured Products

VerifiedAdded on 2022/07/27

|9

|987

|18

Homework Assignment

AI Summary

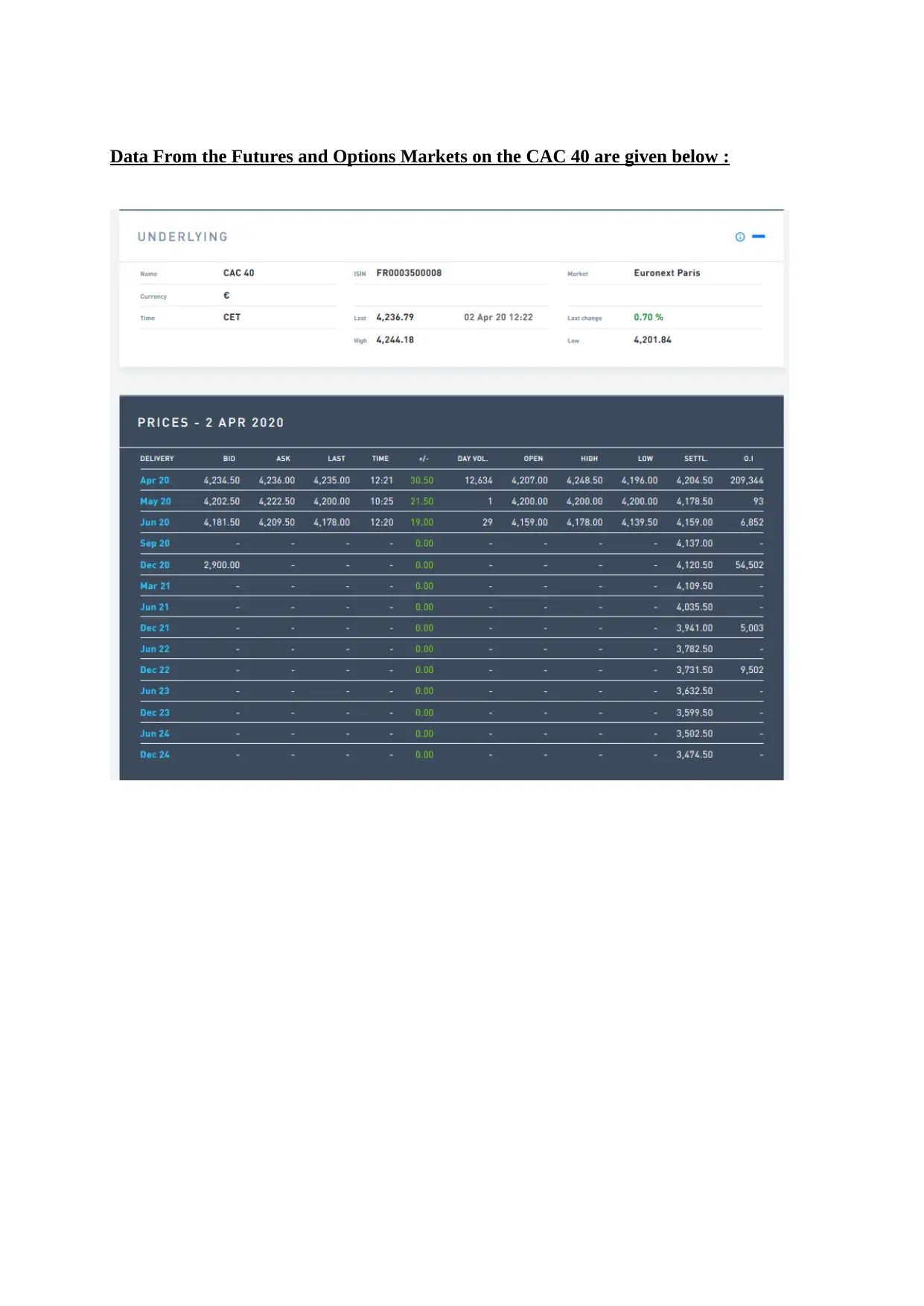

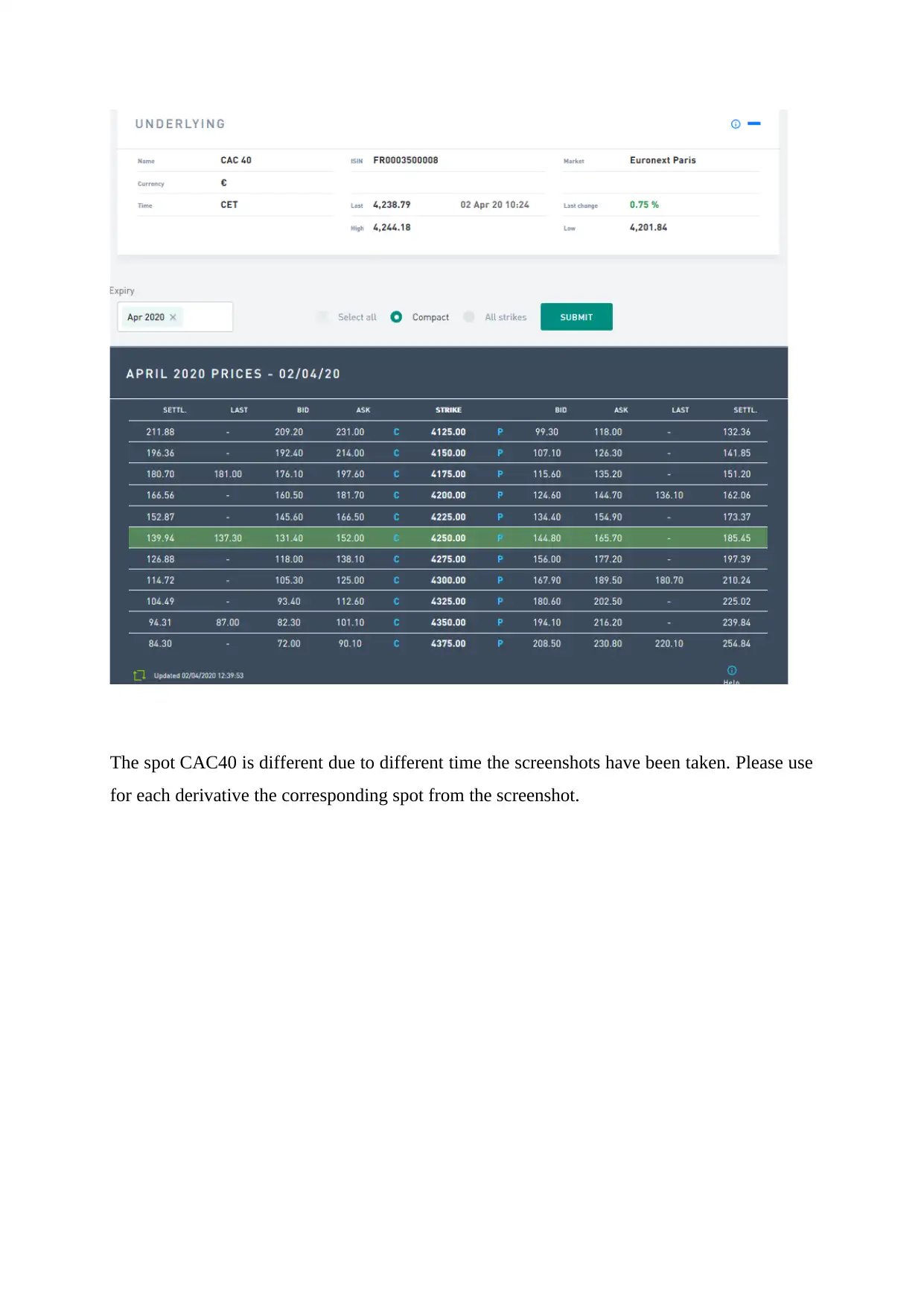

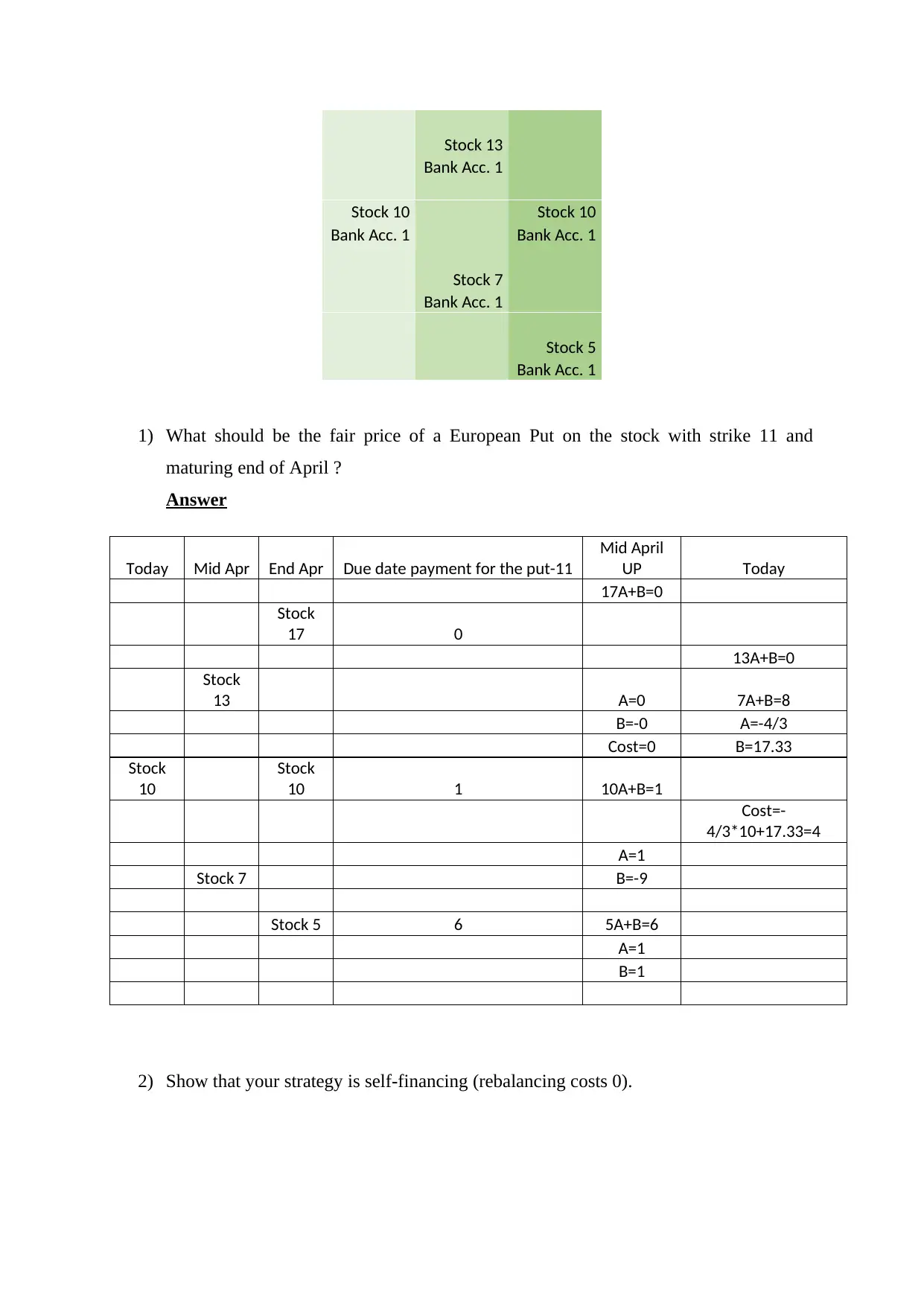

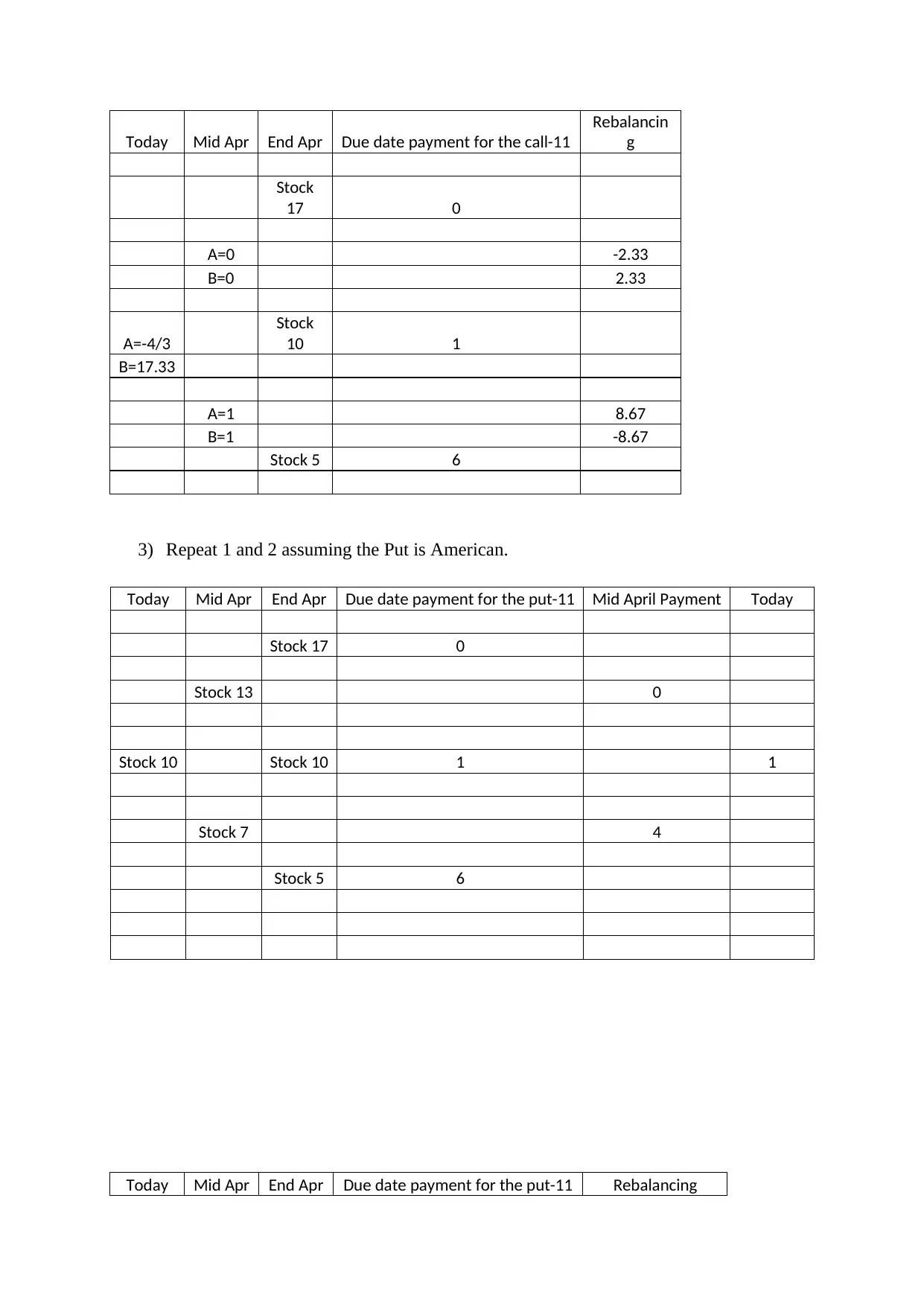

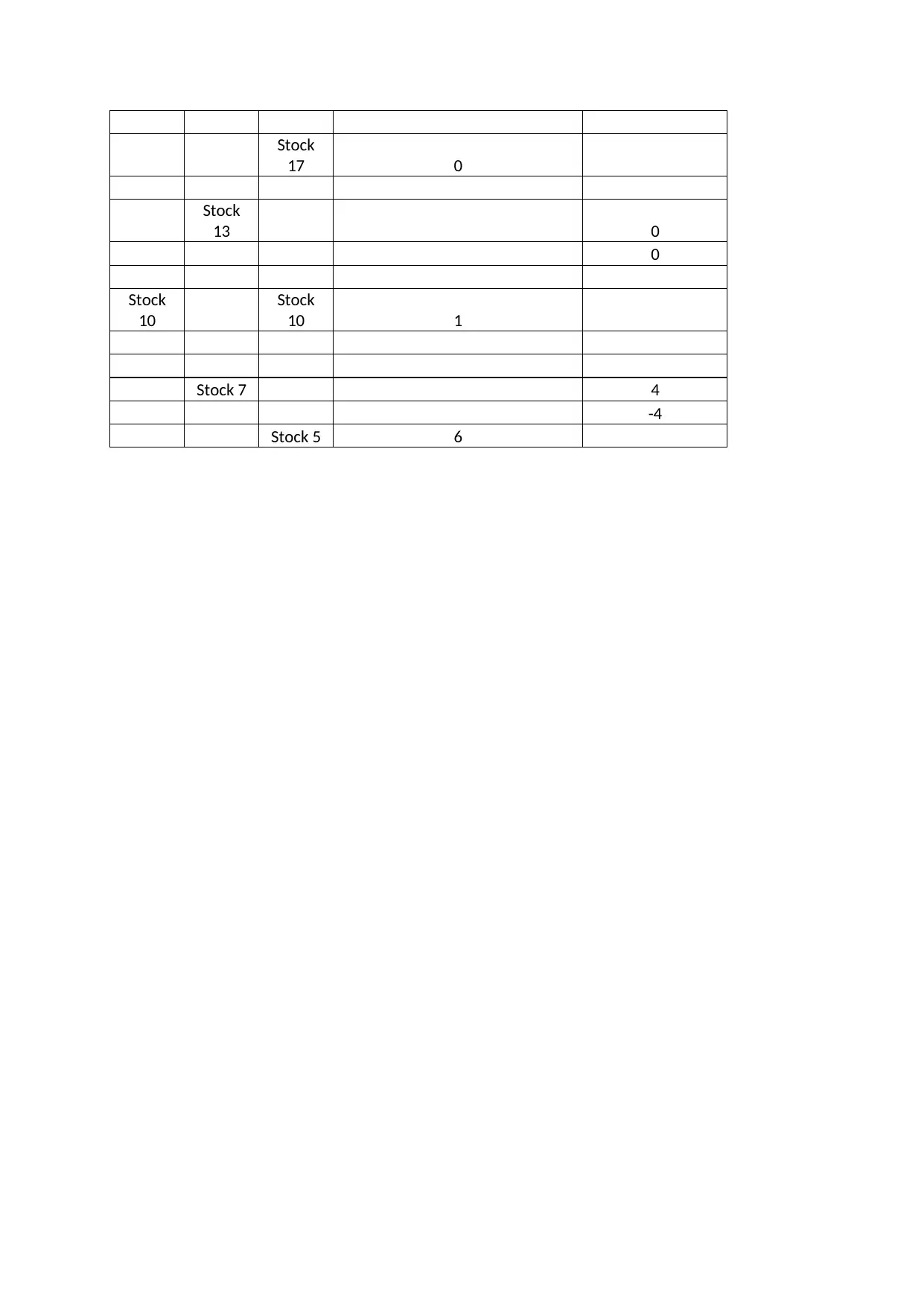

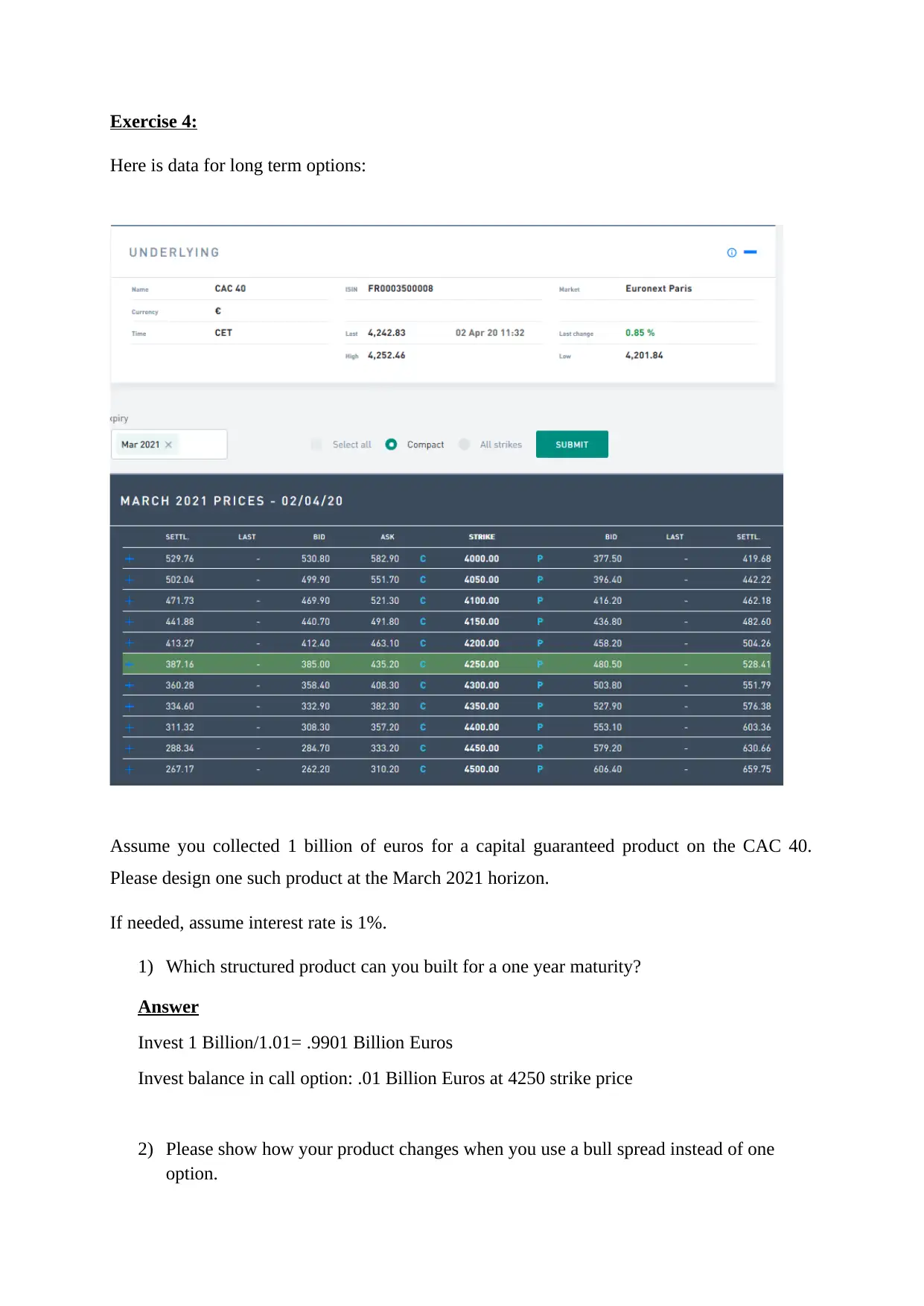

This assignment delves into the analysis of CAC 40 futures and options, covering various aspects of derivatives trading and financial product design. The student is tasked with interpreting market expectations by analyzing April and May futures contracts, calculating and comparing implied dividend yields from settlement prices, and constructing and evaluating options strategies such as strangles and spreads. Furthermore, the assignment explores the pricing of European puts in a simplified financial market and examines the construction of a capital-guaranteed structured product, including the use of a bull spread. The solutions involve quantitative analysis, strategic decision-making, and an understanding of financial market dynamics, providing a comprehensive overview of derivatives and structured products.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.