Tax Law Assignment: Janice Brown's Capital Gains Calculation (2018/19)

VerifiedAdded on 2023/03/17

|9

|1859

|72

Homework Assignment

AI Summary

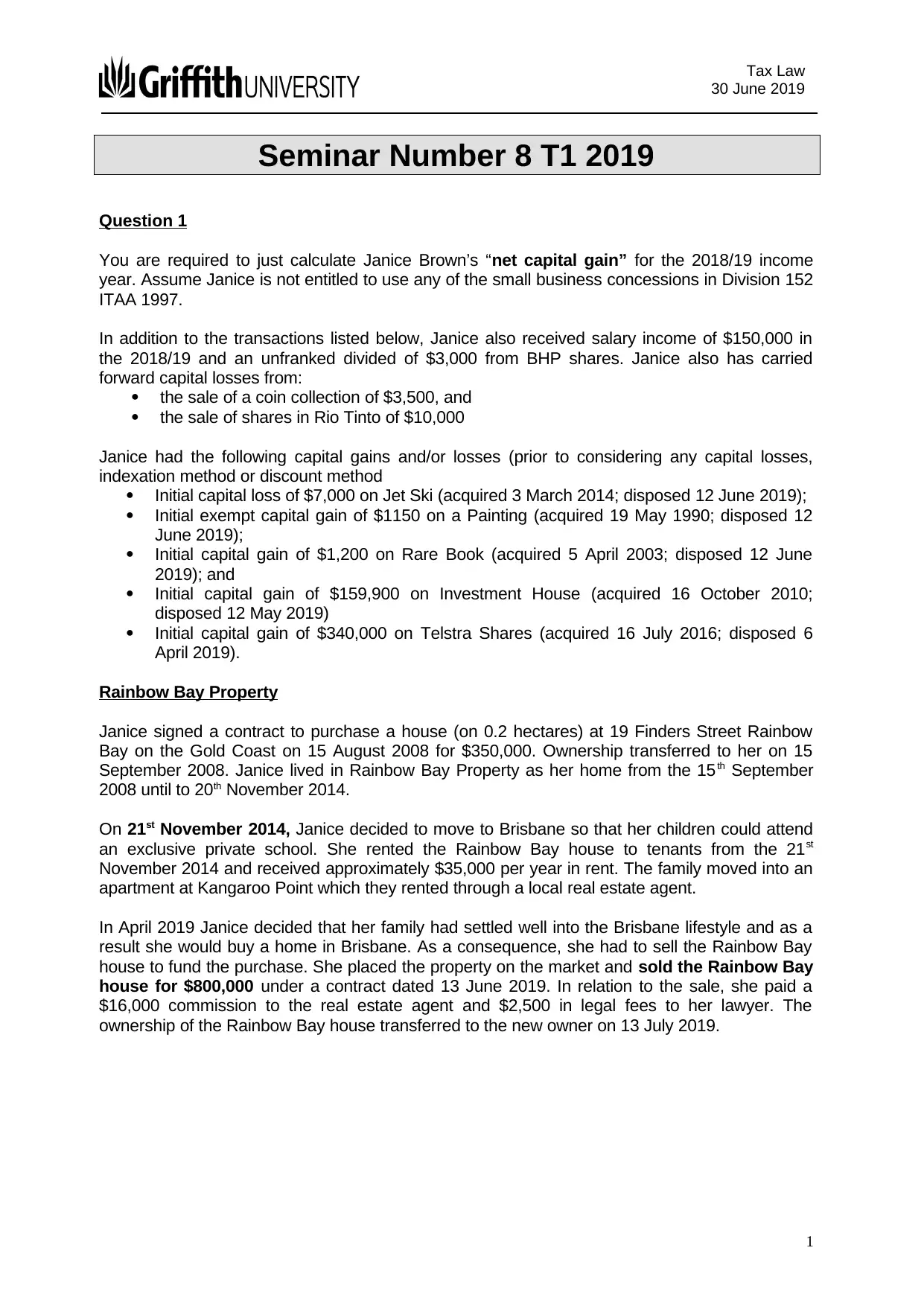

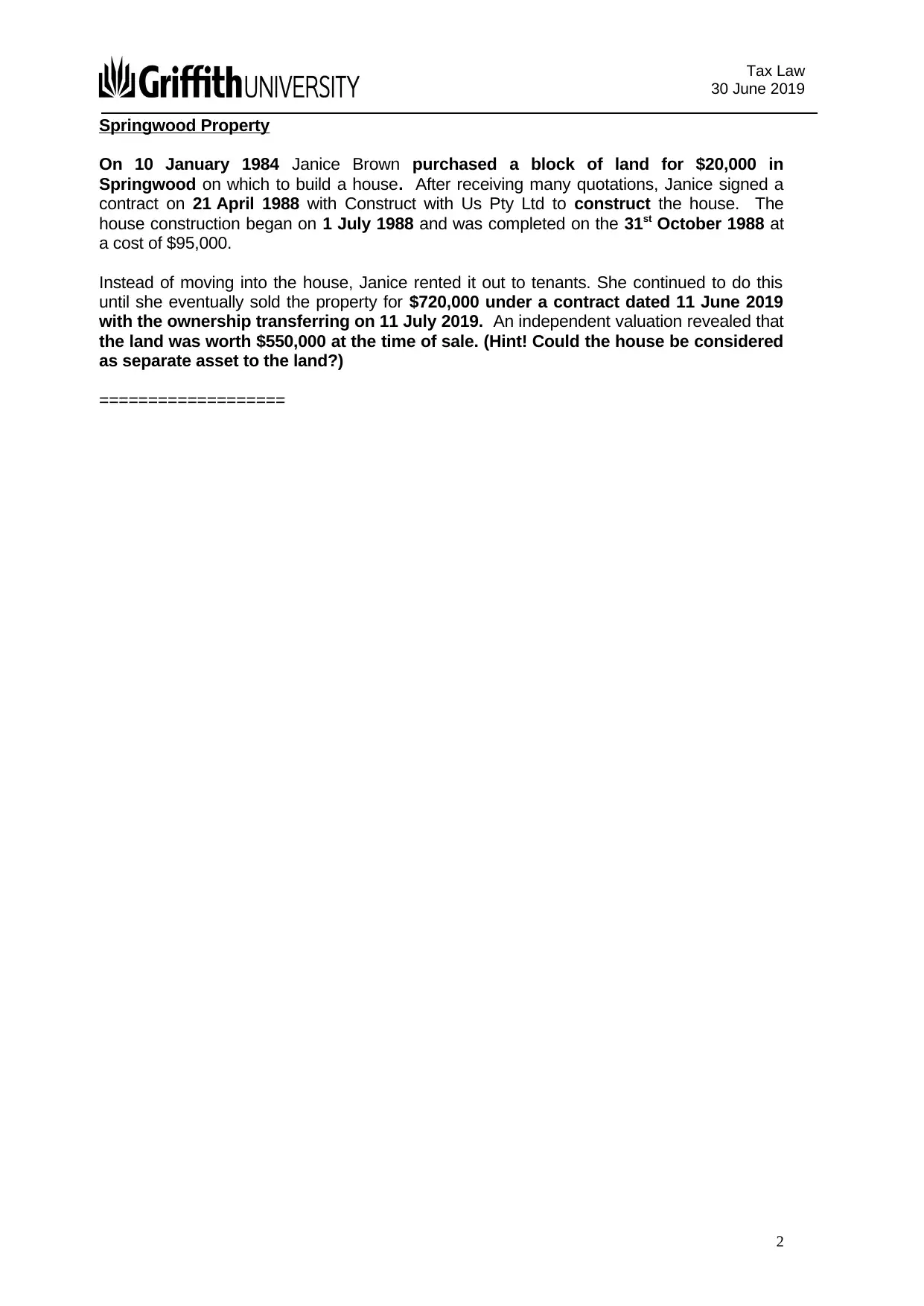

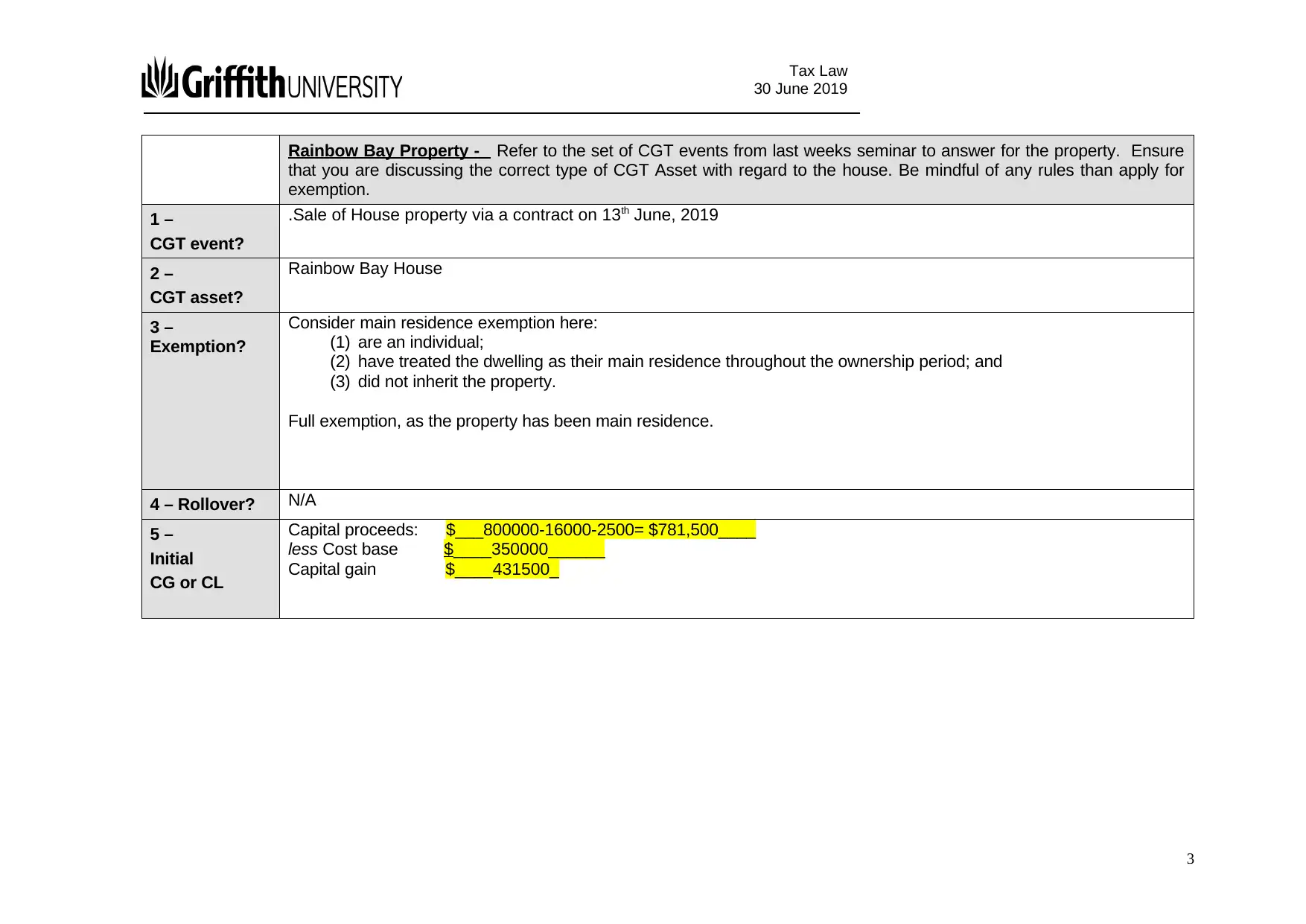

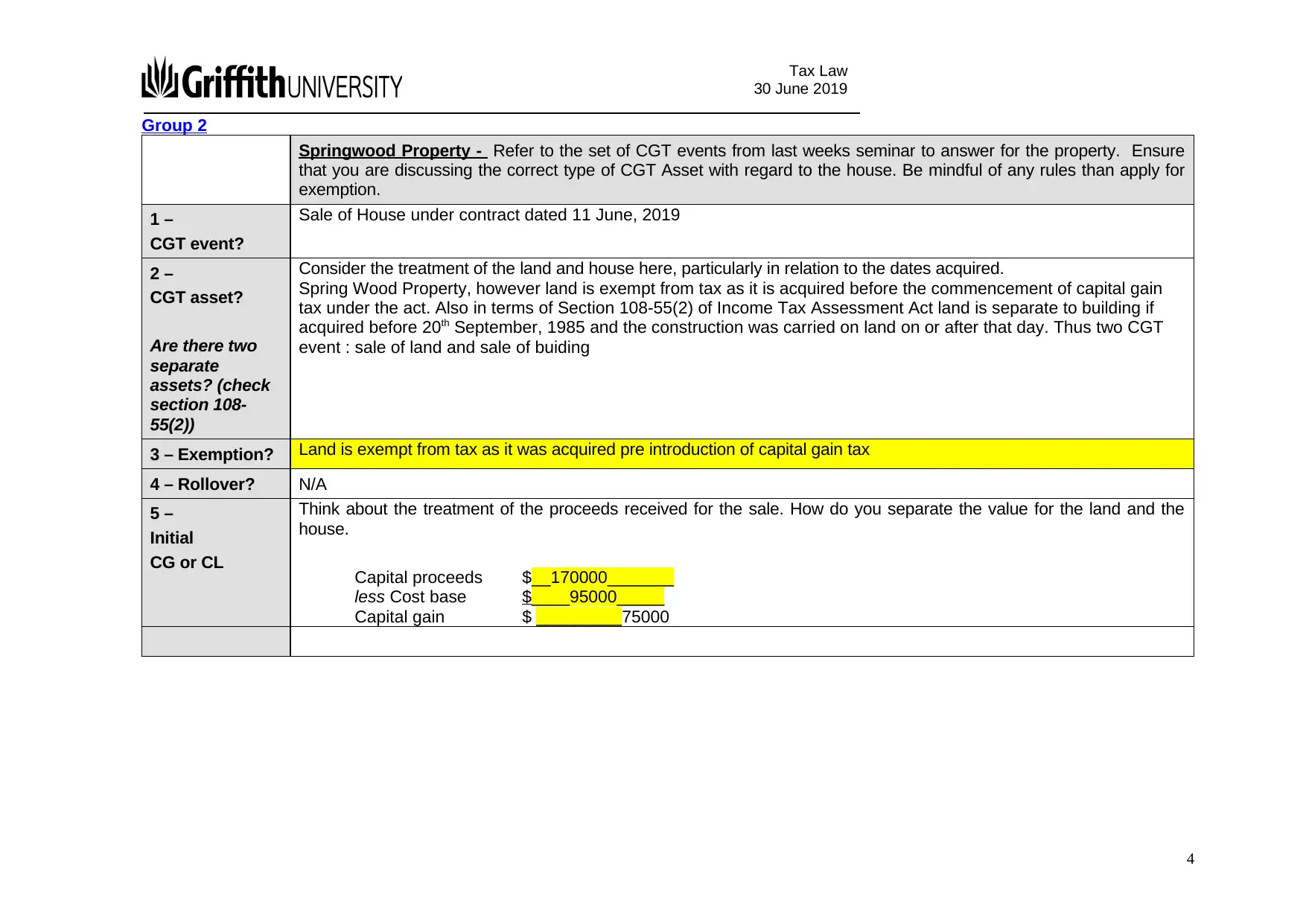

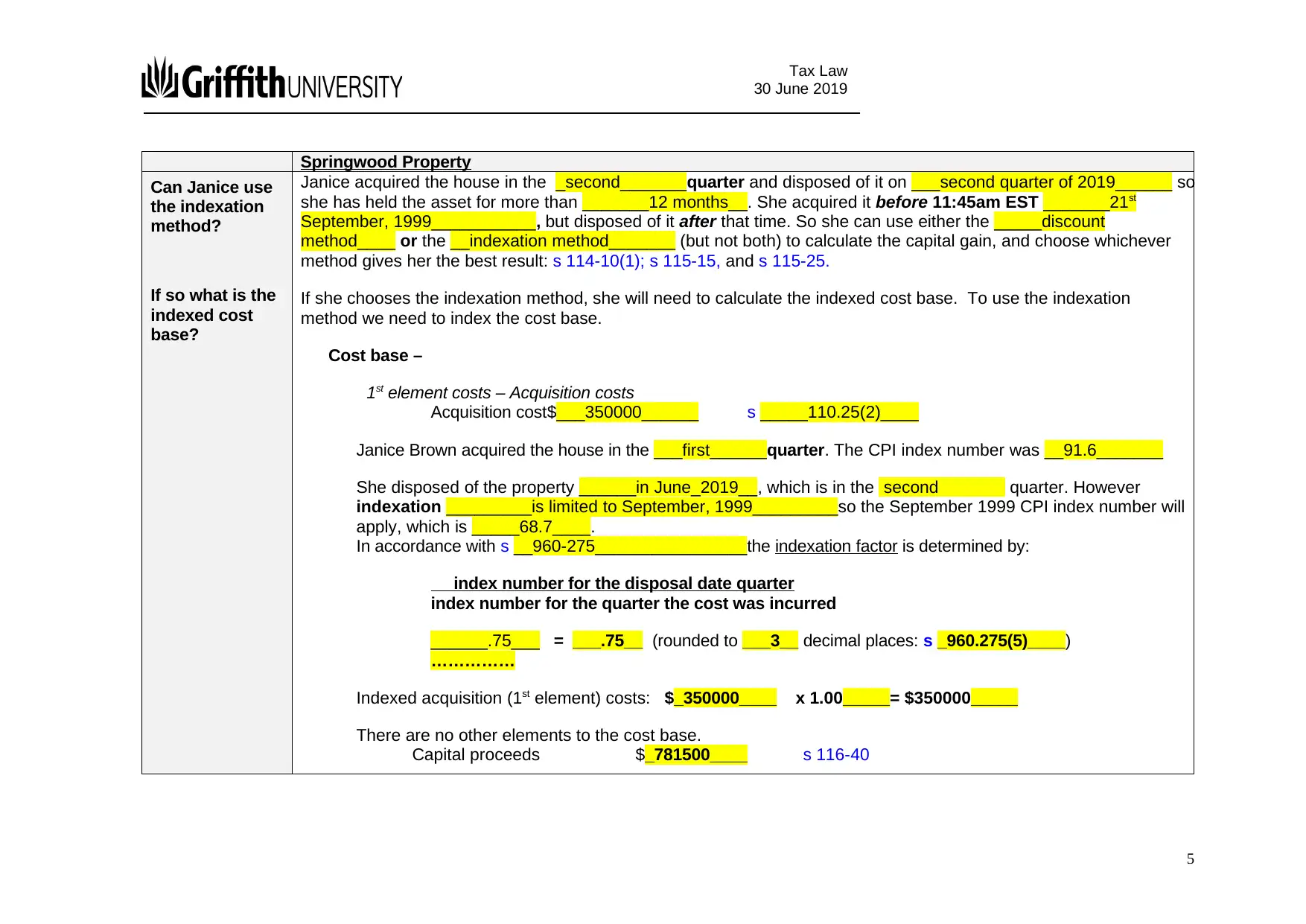

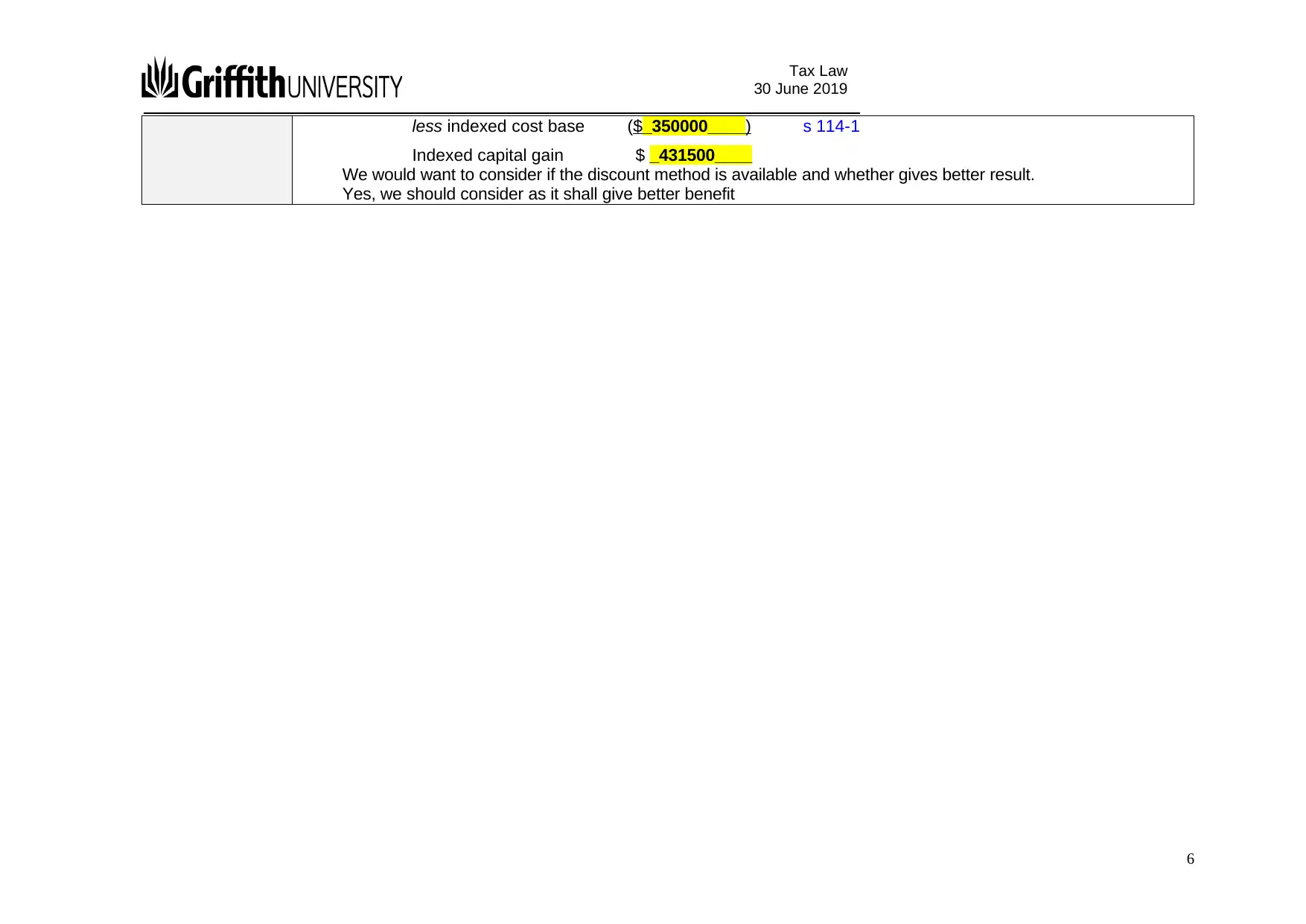

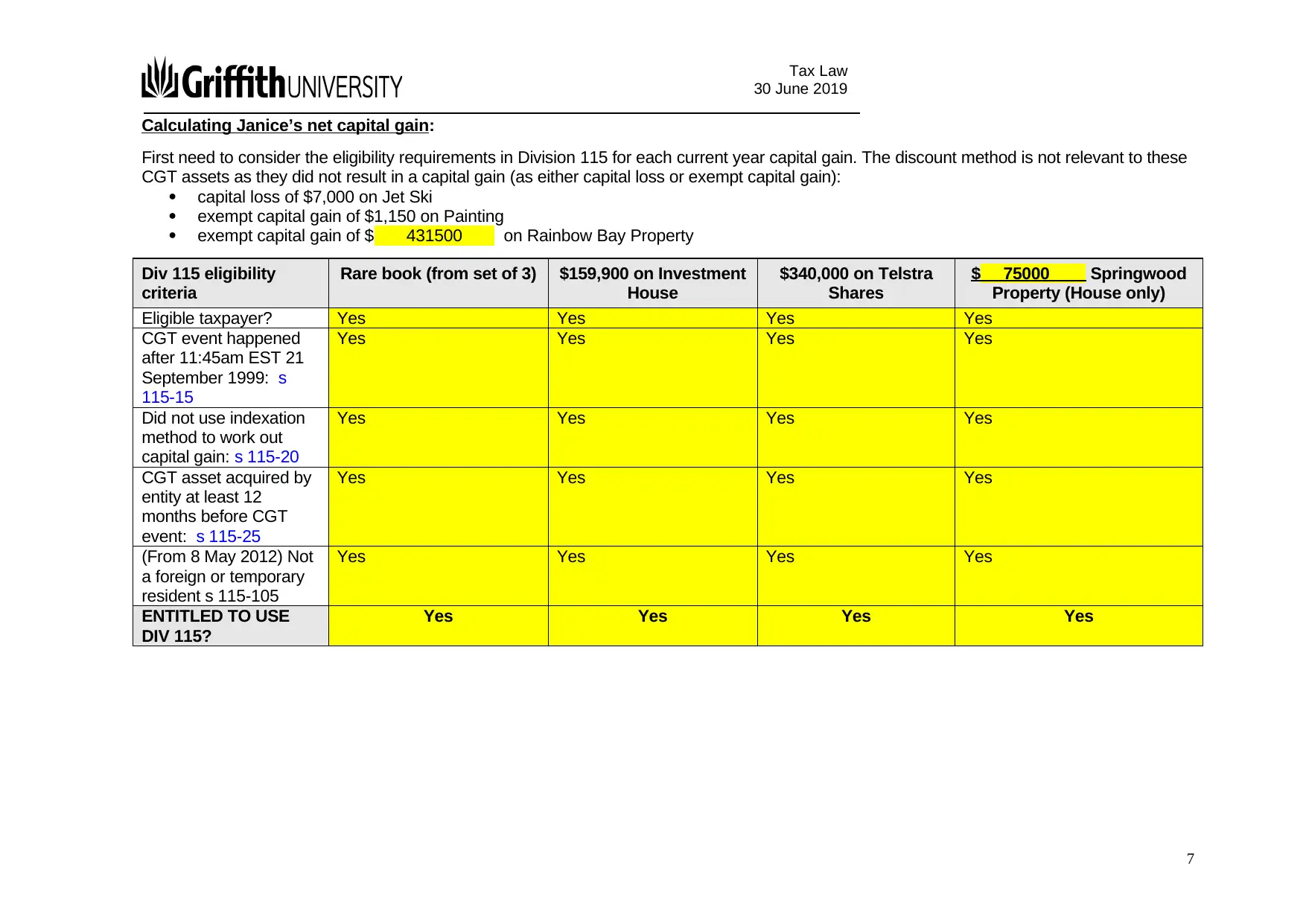

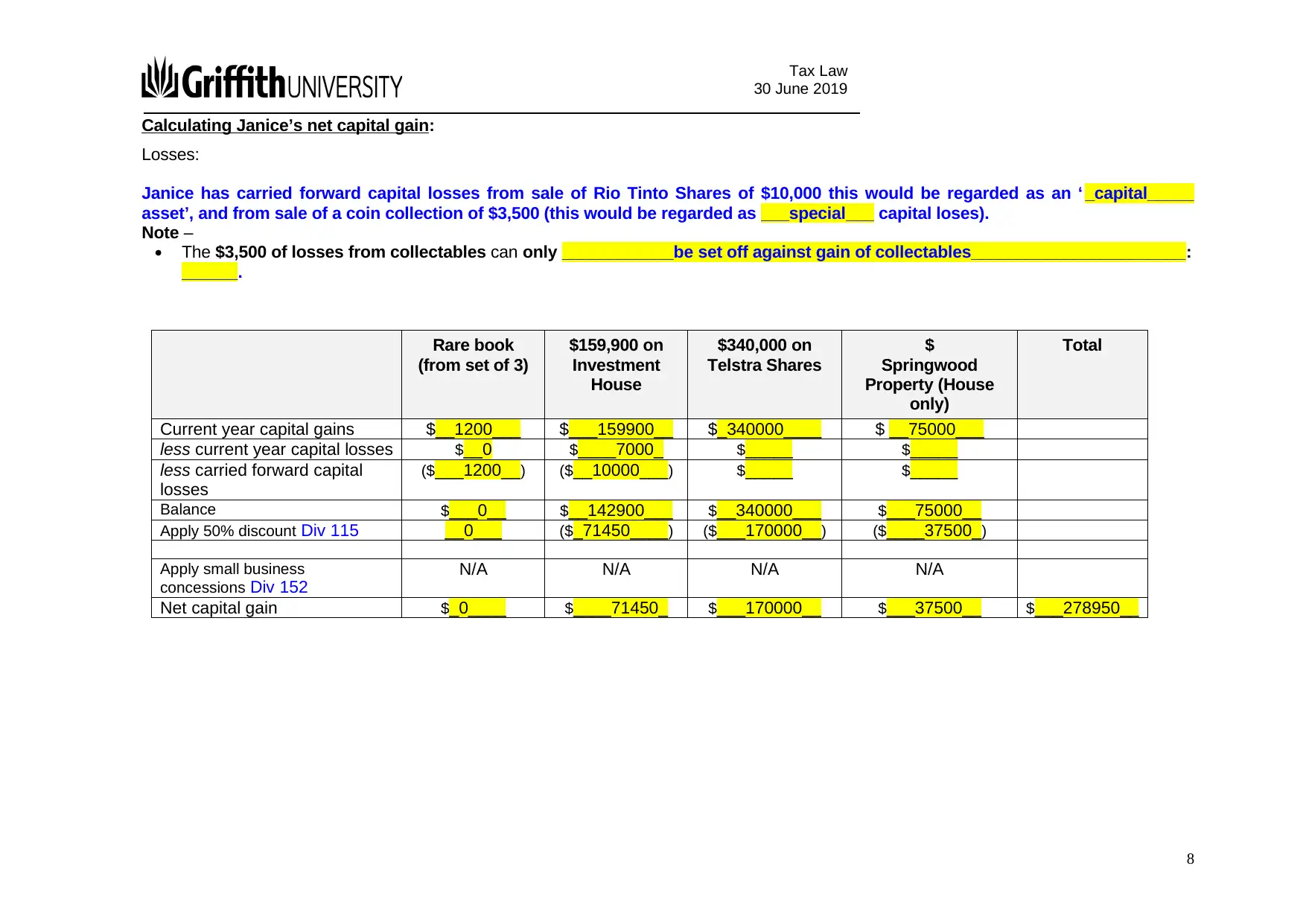

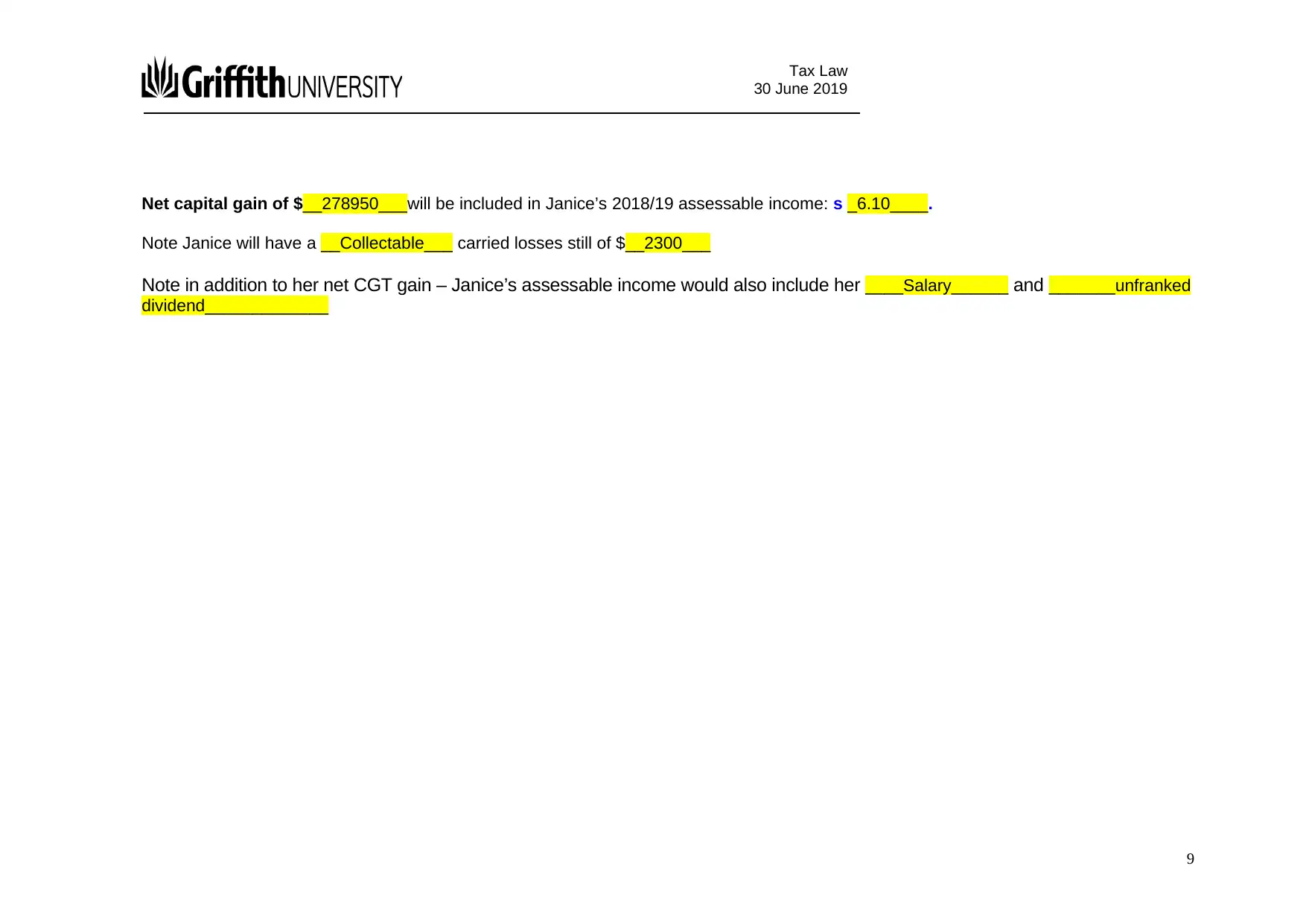

This assignment requires the calculation of Janice Brown's net capital gain for the 2018/19 income year, excluding small business concessions. It involves analyzing various capital gains and losses from the sale of assets like a Jet Ski, painting, rare book, investment house, Telstra shares, and two properties (Rainbow Bay and Springwood). The solution details the application of CGT events, exemptions (including the main residence exemption), and the choice between discount and indexation methods for calculating capital gains. It also accounts for carried-forward capital losses from a coin collection and Rio Tinto shares. The final calculation determines Janice's net capital gain, which is then included in her assessable income, and it also accounts for remaining collectable carried losses.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.