Comprehensive Bond Valuation: Time Value of Money & Excel Report

VerifiedAdded on 2022/08/12

|4

|762

|34

Report

AI Summary

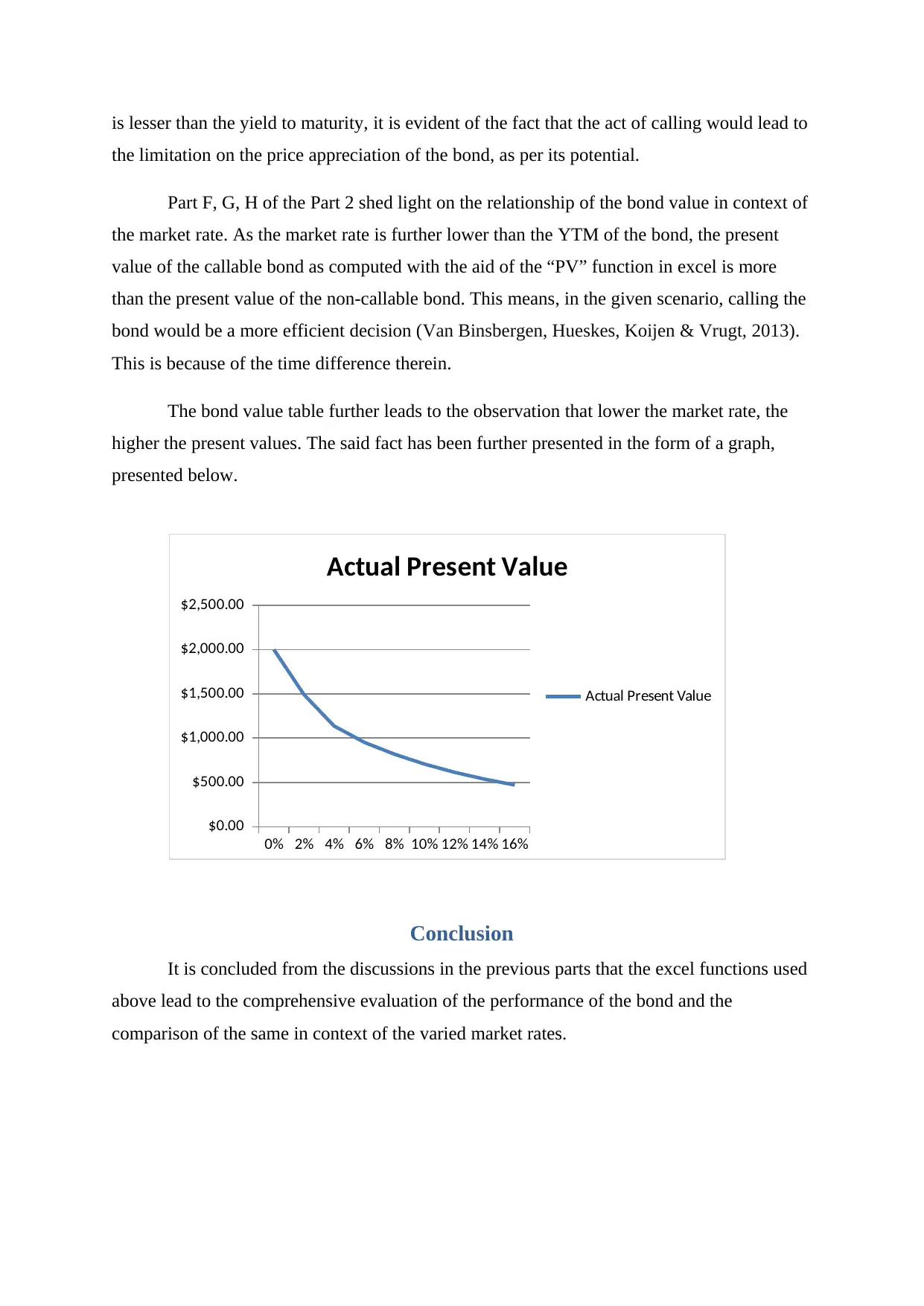

This report provides a comprehensive analysis of bond valuation using time value of money techniques, including present value, future value, and rate calculations. It focuses on both callable and non-callable bonds, demonstrating practical applications using Excel functions such as "Rate," "PV," and "FV." The analysis includes calculating periodic and annualized Yield to Maturity (YTM), current yield, and capital loss percentage. The report also examines the impact of market rates on bond values, concluding that lower market rates lead to higher present values. The findings suggest that calling a bond can be a more efficient decision under certain market conditions. The report uses excel functions to evaluate bond performance and compares bonds in the context of various market rates.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.