ACCT20075: Audit & Ethics Report on Caltex Australia Ltd (2017)

VerifiedAdded on 2023/06/10

|14

|3387

|155

Report

AI Summary

This report provides a detailed analysis of the audit and ethics related to Caltex Australia Ltd, focusing on the 2017 annual report. It covers key aspects such as materiality assessment, the scope of the audit, and a review of draft notes and disclosures. The report includes an analytical review of the financial statements, examining liquidity, profitability, asset management, and leverage ratios to assess the company's financial health. Furthermore, it analyzes the cash flow statement and reviews the auditor's report, offering a comprehensive evaluation of the company's financial reporting and ethical considerations within the auditing process. This document is available on Desklib, a platform offering a wide array of study resources, including past papers and solved assignments, to support students' academic endeavors.

Running head: AUDIT AND ETHICS

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality and Scope of Audit....................................................................................................2

Review of Draft notes and Disclosures.......................................................................................4

Section 2..........................................................................................................................................5

Analytical Review of the Financial statements...........................................................................5

Section 3..........................................................................................................................................9

Analysis of Cash Flow Statement................................................................................................9

Review of the Auditor Report....................................................................................................10

Reference.......................................................................................................................................12

AUDIT AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality and Scope of Audit....................................................................................................2

Review of Draft notes and Disclosures.......................................................................................4

Section 2..........................................................................................................................................5

Analytical Review of the Financial statements...........................................................................5

Section 3..........................................................................................................................................9

Analysis of Cash Flow Statement................................................................................................9

Review of the Auditor Report....................................................................................................10

Reference.......................................................................................................................................12

2

AUDIT AND ETHICS

Section 1

Materiality and Scope of Audit

The main purpose of this assessment is to undertake audit procedures for the purpose of

reviewing the materiality which is to be considered by the auditor for detecting material

misstatements in the financial statements (Louwers et al., 2015). The concept of materiality is

considered to be important in the scope of audit as the same determines which misstatements are

to be considered minor misstatements and which are to be considered significant misstatements.

Significant misstatements are judged on the level of materiality of the item and how it will affect

the decisions taken by potential investors and also other estimates which are shown in the

financial statements (Reid, 2015). The company which is selected for this assessment is Caltex

Australia ltd which is engaged in operations in Australia (Caltex Australia., 2018).

The concept of materiality is fundamental in the scope of audit as the auditor needs to

consider material items and if the same are reported accurately by the management or not. The

auditor needs to apply his judgements for the purpose of setting the materiality of the business.

The auditor considers materiality on the basis of qualitative characteristics and quantitative

characteristics. In qualitative aspect of materiality, the auditor considers significant items of the

business such as net profit, inventory of the business, changes in accounting method and

significant legislations. In the quantitative aspect of judging materiality, the auditor considers

estimated percentages which are charged on appropriate bases in order to determine the

materiality level for different items which are shown in the annual report of the business. The

percentage which is to be charged for determining materiality are up to the judgements of the

auditor depending on the size of the business and nature of its operations. The auditor compute

the planning materiality at the initial planning stage of the audit and on the basis of such

AUDIT AND ETHICS

Section 1

Materiality and Scope of Audit

The main purpose of this assessment is to undertake audit procedures for the purpose of

reviewing the materiality which is to be considered by the auditor for detecting material

misstatements in the financial statements (Louwers et al., 2015). The concept of materiality is

considered to be important in the scope of audit as the same determines which misstatements are

to be considered minor misstatements and which are to be considered significant misstatements.

Significant misstatements are judged on the level of materiality of the item and how it will affect

the decisions taken by potential investors and also other estimates which are shown in the

financial statements (Reid, 2015). The company which is selected for this assessment is Caltex

Australia ltd which is engaged in operations in Australia (Caltex Australia., 2018).

The concept of materiality is fundamental in the scope of audit as the auditor needs to

consider material items and if the same are reported accurately by the management or not. The

auditor needs to apply his judgements for the purpose of setting the materiality of the business.

The auditor considers materiality on the basis of qualitative characteristics and quantitative

characteristics. In qualitative aspect of materiality, the auditor considers significant items of the

business such as net profit, inventory of the business, changes in accounting method and

significant legislations. In the quantitative aspect of judging materiality, the auditor considers

estimated percentages which are charged on appropriate bases in order to determine the

materiality level for different items which are shown in the annual report of the business. The

percentage which is to be charged for determining materiality are up to the judgements of the

auditor depending on the size of the business and nature of its operations. The auditor compute

the planning materiality at the initial planning stage of the audit and on the basis of such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT AND ETHICS

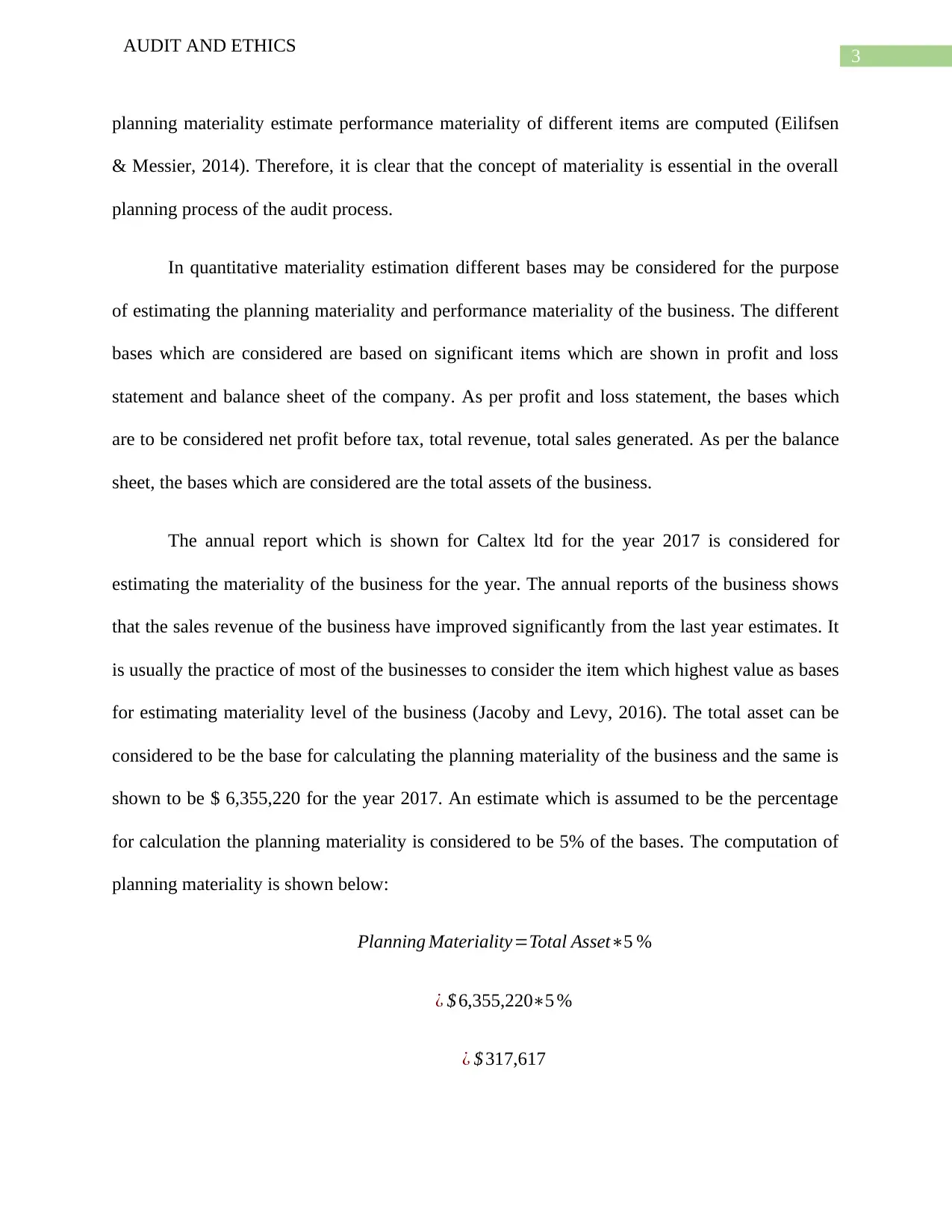

planning materiality estimate performance materiality of different items are computed (Eilifsen

& Messier, 2014). Therefore, it is clear that the concept of materiality is essential in the overall

planning process of the audit process.

In quantitative materiality estimation different bases may be considered for the purpose

of estimating the planning materiality and performance materiality of the business. The different

bases which are considered are based on significant items which are shown in profit and loss

statement and balance sheet of the company. As per profit and loss statement, the bases which

are to be considered net profit before tax, total revenue, total sales generated. As per the balance

sheet, the bases which are considered are the total assets of the business.

The annual report which is shown for Caltex ltd for the year 2017 is considered for

estimating the materiality of the business for the year. The annual reports of the business shows

that the sales revenue of the business have improved significantly from the last year estimates. It

is usually the practice of most of the businesses to consider the item which highest value as bases

for estimating materiality level of the business (Jacoby and Levy, 2016). The total asset can be

considered to be the base for calculating the planning materiality of the business and the same is

shown to be $ 6,355,220 for the year 2017. An estimate which is assumed to be the percentage

for calculation the planning materiality is considered to be 5% of the bases. The computation of

planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 6,355,220∗5 %

¿ $ 317,617

AUDIT AND ETHICS

planning materiality estimate performance materiality of different items are computed (Eilifsen

& Messier, 2014). Therefore, it is clear that the concept of materiality is essential in the overall

planning process of the audit process.

In quantitative materiality estimation different bases may be considered for the purpose

of estimating the planning materiality and performance materiality of the business. The different

bases which are considered are based on significant items which are shown in profit and loss

statement and balance sheet of the company. As per profit and loss statement, the bases which

are to be considered net profit before tax, total revenue, total sales generated. As per the balance

sheet, the bases which are considered are the total assets of the business.

The annual report which is shown for Caltex ltd for the year 2017 is considered for

estimating the materiality of the business for the year. The annual reports of the business shows

that the sales revenue of the business have improved significantly from the last year estimates. It

is usually the practice of most of the businesses to consider the item which highest value as bases

for estimating materiality level of the business (Jacoby and Levy, 2016). The total asset can be

considered to be the base for calculating the planning materiality of the business and the same is

shown to be $ 6,355,220 for the year 2017. An estimate which is assumed to be the percentage

for calculation the planning materiality is considered to be 5% of the bases. The computation of

planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 6,355,220∗5 %

¿ $ 317,617

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT AND ETHICS

Therefore, the planning materiality for the company considering the total asset as base

and 5% as the percentage based on the judgement of the auditor (Coppage & Shastri, 2014). On

the basis of planning materiality, performance materiality of different items is shown.

Review of Draft notes and Disclosures

The draft notes and disclosures which appear in the annual report of Caltex ltd also have

a level of significance on the audit process as the notes section contains certain treatments and

explanations of items which are shown in the financial statements of the business. The

significant items which are shown in the notes to account section of the annual reports are listed

below:

Dividend: The breakup for the dividend is shown in the notes to account section of the

annual report which is important from the perspective of audit as misstatement or

manipulations can take place in the same. The auditor can check the accuracy of the

information by applying audit procedures and also with the help of external confirmation.

Business Combinations: The annual reports also show business combination

commitments of the company which can be affect the audit process and therefore, the

auditor needs to check the same by verifying the deeds and analyzing management

representations (Müller-Burmeister & Velte, 2016).

Financial leases: The financial leases of the business are also disclosed in the notes to

account section and the auditor needs to check the viability and treatment of such lease

item and ensure that the management has treated the same consider relevant Australian

accounting standard.

AUDIT AND ETHICS

Therefore, the planning materiality for the company considering the total asset as base

and 5% as the percentage based on the judgement of the auditor (Coppage & Shastri, 2014). On

the basis of planning materiality, performance materiality of different items is shown.

Review of Draft notes and Disclosures

The draft notes and disclosures which appear in the annual report of Caltex ltd also have

a level of significance on the audit process as the notes section contains certain treatments and

explanations of items which are shown in the financial statements of the business. The

significant items which are shown in the notes to account section of the annual reports are listed

below:

Dividend: The breakup for the dividend is shown in the notes to account section of the

annual report which is important from the perspective of audit as misstatement or

manipulations can take place in the same. The auditor can check the accuracy of the

information by applying audit procedures and also with the help of external confirmation.

Business Combinations: The annual reports also show business combination

commitments of the company which can be affect the audit process and therefore, the

auditor needs to check the same by verifying the deeds and analyzing management

representations (Müller-Burmeister & Velte, 2016).

Financial leases: The financial leases of the business are also disclosed in the notes to

account section and the auditor needs to check the viability and treatment of such lease

item and ensure that the management has treated the same consider relevant Australian

accounting standard.

5

AUDIT AND ETHICS

Section 2

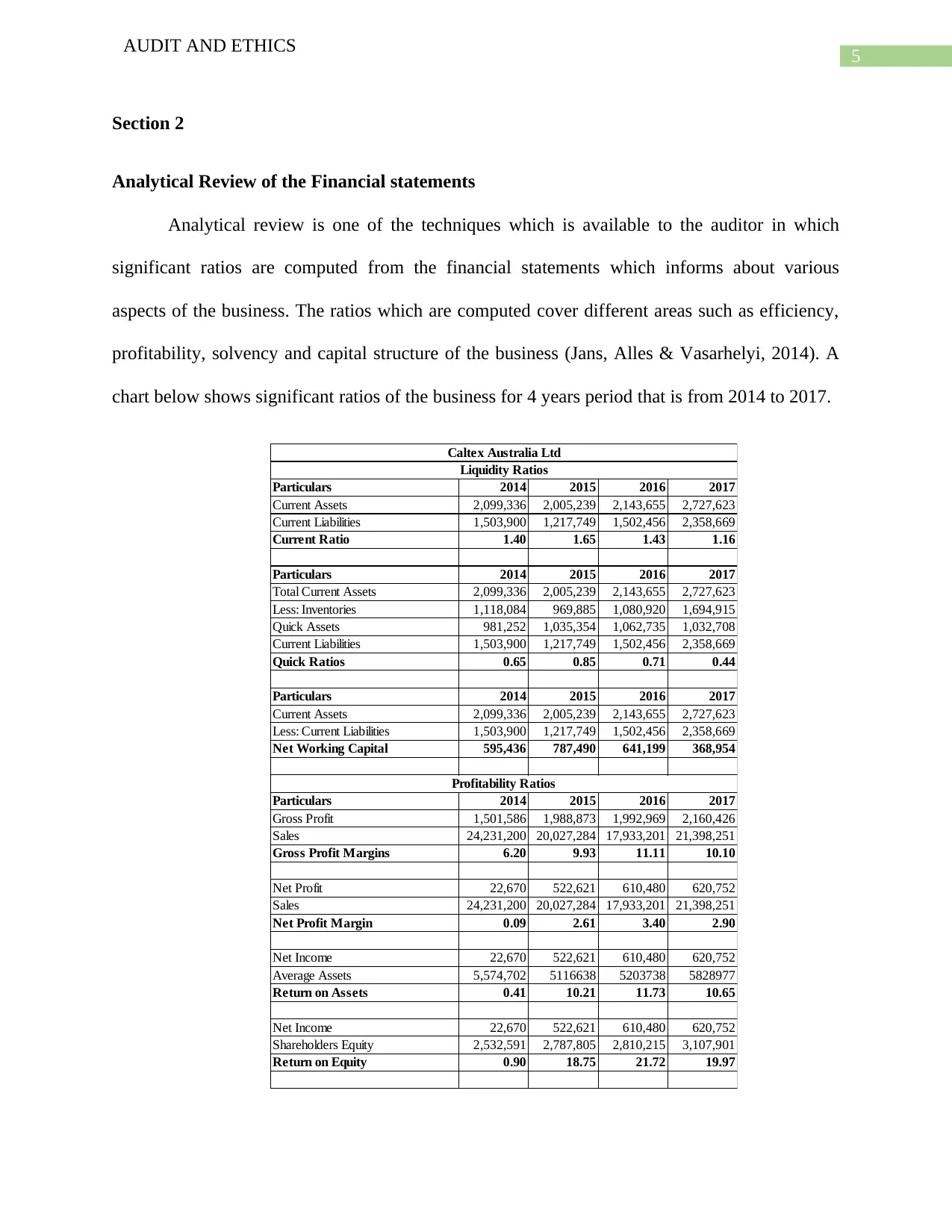

Analytical Review of the Financial statements

Analytical review is one of the techniques which is available to the auditor in which

significant ratios are computed from the financial statements which informs about various

aspects of the business. The ratios which are computed cover different areas such as efficiency,

profitability, solvency and capital structure of the business (Jans, Alles & Vasarhelyi, 2014). A

chart below shows significant ratios of the business for 4 years period that is from 2014 to 2017.

Particulars 2014 2015 2016 2017

Current Assets 2,099,336 2,005,239 2,143,655 2,727,623

Current Liabilities 1,503,900 1,217,749 1,502,456 2,358,669

Current Ratio 1.40 1.65 1.43 1.16

Particulars 2014 2015 2016 2017

Total Current Assets 2,099,336 2,005,239 2,143,655 2,727,623

Less: Inventories 1,118,084 969,885 1,080,920 1,694,915

Quick Assets 981,252 1,035,354 1,062,735 1,032,708

Current Liabilities 1,503,900 1,217,749 1,502,456 2,358,669

Quick Ratios 0.65 0.85 0.71 0.44

Particulars 2014 2015 2016 2017

Current Assets 2,099,336 2,005,239 2,143,655 2,727,623

Less: Current Liabilities 1,503,900 1,217,749 1,502,456 2,358,669

Net Working Capital 595,436 787,490 641,199 368,954

Particulars 2014 2015 2016 2017

Gross Profit 1,501,586 1,988,873 1,992,969 2,160,426

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Gross Profit Margins 6.20 9.93 11.11 10.10

Net Profit 22,670 522,621 610,480 620,752

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Net Profit Margin 0.09 2.61 3.40 2.90

Net Income 22,670 522,621 610,480 620,752

Average Assets 5,574,702 5116638 5203738 5828977

Return on Assets 0.41 10.21 11.73 10.65

Net Income 22,670 522,621 610,480 620,752

Shareholders Equity 2,532,591 2,787,805 2,810,215 3,107,901

Return on Equity 0.90 18.75 21.72 19.97

Caltex Australia Ltd

Liquidity Ratios

Profitability Ratios

AUDIT AND ETHICS

Section 2

Analytical Review of the Financial statements

Analytical review is one of the techniques which is available to the auditor in which

significant ratios are computed from the financial statements which informs about various

aspects of the business. The ratios which are computed cover different areas such as efficiency,

profitability, solvency and capital structure of the business (Jans, Alles & Vasarhelyi, 2014). A

chart below shows significant ratios of the business for 4 years period that is from 2014 to 2017.

Particulars 2014 2015 2016 2017

Current Assets 2,099,336 2,005,239 2,143,655 2,727,623

Current Liabilities 1,503,900 1,217,749 1,502,456 2,358,669

Current Ratio 1.40 1.65 1.43 1.16

Particulars 2014 2015 2016 2017

Total Current Assets 2,099,336 2,005,239 2,143,655 2,727,623

Less: Inventories 1,118,084 969,885 1,080,920 1,694,915

Quick Assets 981,252 1,035,354 1,062,735 1,032,708

Current Liabilities 1,503,900 1,217,749 1,502,456 2,358,669

Quick Ratios 0.65 0.85 0.71 0.44

Particulars 2014 2015 2016 2017

Current Assets 2,099,336 2,005,239 2,143,655 2,727,623

Less: Current Liabilities 1,503,900 1,217,749 1,502,456 2,358,669

Net Working Capital 595,436 787,490 641,199 368,954

Particulars 2014 2015 2016 2017

Gross Profit 1,501,586 1,988,873 1,992,969 2,160,426

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Gross Profit Margins 6.20 9.93 11.11 10.10

Net Profit 22,670 522,621 610,480 620,752

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Net Profit Margin 0.09 2.61 3.40 2.90

Net Income 22,670 522,621 610,480 620,752

Average Assets 5,574,702 5116638 5203738 5828977

Return on Assets 0.41 10.21 11.73 10.65

Net Income 22,670 522,621 610,480 620,752

Shareholders Equity 2,532,591 2,787,805 2,810,215 3,107,901

Return on Equity 0.90 18.75 21.72 19.97

Caltex Australia Ltd

Liquidity Ratios

Profitability Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT AND ETHICS

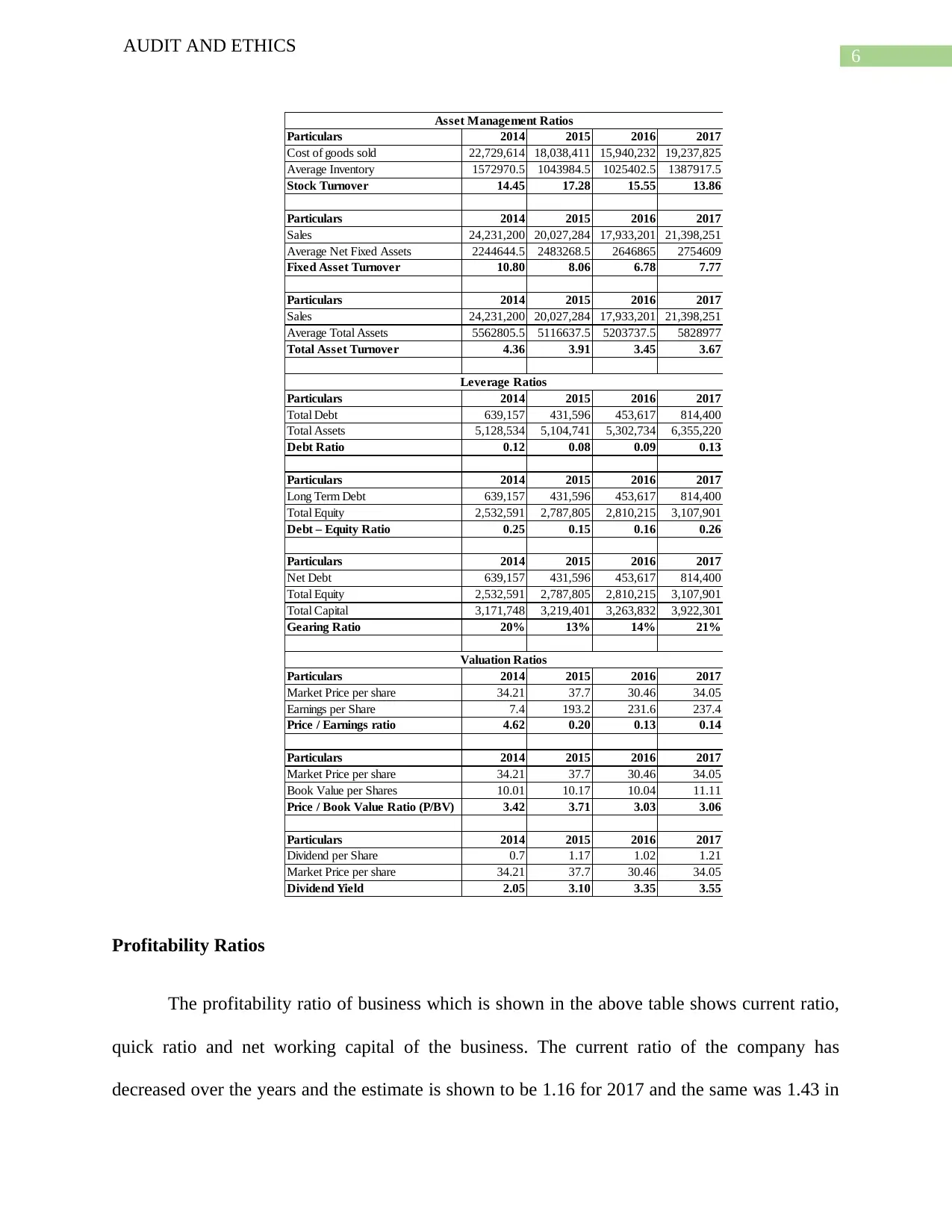

Particulars 2014 2015 2016 2017

Cost of goods sold 22,729,614 18,038,411 15,940,232 19,237,825

Average Inventory 1572970.5 1043984.5 1025402.5 1387917.5

Stock Turnover 14.45 17.28 15.55 13.86

Particulars 2014 2015 2016 2017

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Average Net Fixed Assets 2244644.5 2483268.5 2646865 2754609

Fixed Asset Turnover 10.80 8.06 6.78 7.77

Particulars 2014 2015 2016 2017

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Average Total Assets 5562805.5 5116637.5 5203737.5 5828977

Total Asset Turnover 4.36 3.91 3.45 3.67

Particulars 2014 2015 2016 2017

Total Debt 639,157 431,596 453,617 814,400

Total Assets 5,128,534 5,104,741 5,302,734 6,355,220

Debt Ratio 0.12 0.08 0.09 0.13

Particulars 2014 2015 2016 2017

Long Term Debt 639,157 431,596 453,617 814,400

Total Equity 2,532,591 2,787,805 2,810,215 3,107,901

Debt – Equity Ratio 0.25 0.15 0.16 0.26

Particulars 2014 2015 2016 2017

Net Debt 639,157 431,596 453,617 814,400

Total Equity 2,532,591 2,787,805 2,810,215 3,107,901

Total Capital 3,171,748 3,219,401 3,263,832 3,922,301

Gearing Ratio 20% 13% 14% 21%

Particulars 2014 2015 2016 2017

Market Price per share 34.21 37.7 30.46 34.05

Earnings per Share 7.4 193.2 231.6 237.4

Price / Earnings ratio 4.62 0.20 0.13 0.14

Particulars 2014 2015 2016 2017

Market Price per share 34.21 37.7 30.46 34.05

Book Value per Shares 10.01 10.17 10.04 11.11

Price / Book Value Ratio (P/BV) 3.42 3.71 3.03 3.06

Particulars 2014 2015 2016 2017

Dividend per Share 0.7 1.17 1.02 1.21

Market Price per share 34.21 37.7 30.46 34.05

Dividend Yield 2.05 3.10 3.35 3.55

Valuation Ratios

Asset Management Ratios

Leverage Ratios

Profitability Ratios

The profitability ratio of business which is shown in the above table shows current ratio,

quick ratio and net working capital of the business. The current ratio of the company has

decreased over the years and the estimate is shown to be 1.16 for 2017 and the same was 1.43 in

AUDIT AND ETHICS

Particulars 2014 2015 2016 2017

Cost of goods sold 22,729,614 18,038,411 15,940,232 19,237,825

Average Inventory 1572970.5 1043984.5 1025402.5 1387917.5

Stock Turnover 14.45 17.28 15.55 13.86

Particulars 2014 2015 2016 2017

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Average Net Fixed Assets 2244644.5 2483268.5 2646865 2754609

Fixed Asset Turnover 10.80 8.06 6.78 7.77

Particulars 2014 2015 2016 2017

Sales 24,231,200 20,027,284 17,933,201 21,398,251

Average Total Assets 5562805.5 5116637.5 5203737.5 5828977

Total Asset Turnover 4.36 3.91 3.45 3.67

Particulars 2014 2015 2016 2017

Total Debt 639,157 431,596 453,617 814,400

Total Assets 5,128,534 5,104,741 5,302,734 6,355,220

Debt Ratio 0.12 0.08 0.09 0.13

Particulars 2014 2015 2016 2017

Long Term Debt 639,157 431,596 453,617 814,400

Total Equity 2,532,591 2,787,805 2,810,215 3,107,901

Debt – Equity Ratio 0.25 0.15 0.16 0.26

Particulars 2014 2015 2016 2017

Net Debt 639,157 431,596 453,617 814,400

Total Equity 2,532,591 2,787,805 2,810,215 3,107,901

Total Capital 3,171,748 3,219,401 3,263,832 3,922,301

Gearing Ratio 20% 13% 14% 21%

Particulars 2014 2015 2016 2017

Market Price per share 34.21 37.7 30.46 34.05

Earnings per Share 7.4 193.2 231.6 237.4

Price / Earnings ratio 4.62 0.20 0.13 0.14

Particulars 2014 2015 2016 2017

Market Price per share 34.21 37.7 30.46 34.05

Book Value per Shares 10.01 10.17 10.04 11.11

Price / Book Value Ratio (P/BV) 3.42 3.71 3.03 3.06

Particulars 2014 2015 2016 2017

Dividend per Share 0.7 1.17 1.02 1.21

Market Price per share 34.21 37.7 30.46 34.05

Dividend Yield 2.05 3.10 3.35 3.55

Valuation Ratios

Asset Management Ratios

Leverage Ratios

Profitability Ratios

The profitability ratio of business which is shown in the above table shows current ratio,

quick ratio and net working capital of the business. The current ratio of the company has

decreased over the years and the estimate is shown to be 1.16 for 2017 and the same was 1.43 in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT AND ETHICS

2016 which suggest that the liquidity situation of the business has fallen. The auditor needs to

apply verification procedures to verify the values of current assets of the business. Similarly, the

quick ratio of the business has fallen which is also related to liquidity position of the business.

The net working capital of the business has also fallen which is a serious matter and the business

might be facing liquidity risks. The auditor can look in the assets and verify the values to ensure

that everything is showing true and fair view.

Profitability Ratios

The profitability ratios are directly linked with the profit generating capability of the

business. The gross profit margin and net profit margin of the company has slightly decreased

from 2016 estimates. The overall sale has increased for the business but the management has not

be able to control the expenses of the company and therefore the profits have fallen (Pike, Curtis

& Chui, 2013). The return on assets of the business and return on equity are considered to

financial indicators of business performance and the same have decreased from previous year’s

estimates. This can be due to the high costs and low profits which are earned by the business.

The auditor needs to ensure that the profits are not understated or overstated in the

financial reports for which the auditor needs to check the sales figure including both cash and

credit sales of the business. The auditor then must apply vouching procedures to check the

viability of the expenses incurred by the business as all the ratios under profitability is affected

by sales and total expenses figures (Elder et al., 2013). The auditor can use external confirmation

for determining the extent and amount of expenses which the business actually owed.

Asset Management Ratios

AUDIT AND ETHICS

2016 which suggest that the liquidity situation of the business has fallen. The auditor needs to

apply verification procedures to verify the values of current assets of the business. Similarly, the

quick ratio of the business has fallen which is also related to liquidity position of the business.

The net working capital of the business has also fallen which is a serious matter and the business

might be facing liquidity risks. The auditor can look in the assets and verify the values to ensure

that everything is showing true and fair view.

Profitability Ratios

The profitability ratios are directly linked with the profit generating capability of the

business. The gross profit margin and net profit margin of the company has slightly decreased

from 2016 estimates. The overall sale has increased for the business but the management has not

be able to control the expenses of the company and therefore the profits have fallen (Pike, Curtis

& Chui, 2013). The return on assets of the business and return on equity are considered to

financial indicators of business performance and the same have decreased from previous year’s

estimates. This can be due to the high costs and low profits which are earned by the business.

The auditor needs to ensure that the profits are not understated or overstated in the

financial reports for which the auditor needs to check the sales figure including both cash and

credit sales of the business. The auditor then must apply vouching procedures to check the

viability of the expenses incurred by the business as all the ratios under profitability is affected

by sales and total expenses figures (Elder et al., 2013). The auditor can use external confirmation

for determining the extent and amount of expenses which the business actually owed.

Asset Management Ratios

8

AUDIT AND ETHICS

The asset management ratio comprises of stock turnover ratio, asset turnover ratio of the

business. Th inventories are considered to be important items of the business and are most

vulnerable to material misstatement. The assets of the business also need to be appropriate

regarding misstatements.

The auditor of the business needs to verify the inventory accounts and records and if need

be arise conduct physical stock take to appropriate value the stocks of the business. The auditor

needs to apply verification process for assets of the business and in order to undertake effective

valuation of the assets, the auditor can also take the help of experts for the same reasons.

Leverage Ratios

These are significant ratios of a business and the same inform whether the business is

using more of a debt capital and equity capital. The ratios show debt ratio, debt to equity ratio.

The debt ratio of the business has increased which suggest that the borrowing of the business has

also increased as per the annual report of the business. The business has not made much changes

in the equity capital of the business and therefore it is clear that the business is putting more

reliance on the application of debt capital.

The auditor needs to assess the risks which are associated with debt capital of the

business and ensure that the same are not affecting the business in any way (Appelbaum, Kogan

& Vasarhelyi, 2017). Moreover, the auditor needs to check whether the debt capital are

appropriately stated in the financial statement.

Valuation Ratios

AUDIT AND ETHICS

The asset management ratio comprises of stock turnover ratio, asset turnover ratio of the

business. Th inventories are considered to be important items of the business and are most

vulnerable to material misstatement. The assets of the business also need to be appropriate

regarding misstatements.

The auditor of the business needs to verify the inventory accounts and records and if need

be arise conduct physical stock take to appropriate value the stocks of the business. The auditor

needs to apply verification process for assets of the business and in order to undertake effective

valuation of the assets, the auditor can also take the help of experts for the same reasons.

Leverage Ratios

These are significant ratios of a business and the same inform whether the business is

using more of a debt capital and equity capital. The ratios show debt ratio, debt to equity ratio.

The debt ratio of the business has increased which suggest that the borrowing of the business has

also increased as per the annual report of the business. The business has not made much changes

in the equity capital of the business and therefore it is clear that the business is putting more

reliance on the application of debt capital.

The auditor needs to assess the risks which are associated with debt capital of the

business and ensure that the same are not affecting the business in any way (Appelbaum, Kogan

& Vasarhelyi, 2017). Moreover, the auditor needs to check whether the debt capital are

appropriately stated in the financial statement.

Valuation Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT AND ETHICS

The valuation ratio of the business comprises of price-earning ratio, price to book value

ratio which are considered to be significant indicators for overall success of a business. The

price-earning ratio and price to book value ratio are shown to have increased from previous

year’s estimates which indicates that the business is developing.

The auditor needs to check the earning per shares of the business and the dividends which

is offered by the business to the shareholders for the period. The auditor also needs to verify the

share capital which is accumulated by the business.

Section 3

Analysis of Cash Flow Statement

The cash flow statement of the business shows the cash inflows and outflows of the

business during a particular year and the same is also a display of the liquidity position of the

business. The cash flow statement for Caltex ltd for the year 2017 shows cash from operating

activities, investing activities and financing activities.

The cash flow from operating activities of the business show the maximum cash inflows

of the business due to the receipts from the customers which is shown to be $ 23,693,457 for the

year. The cash from operating activities of the business is shown to be $ 735,032 which as

slightly fallen from previous year. The cash flow from investing activities show the maximum

cash outflow of the business (Bhandari & Iyer, 2013). This is because the business has acquired a

new business plant, property equipment and also made investments during the year. The primary

cash receipts which is shown in the operating section which is receipts from the customers which

is from the sales and the primary cash payments which is shown in the cash from operating

activities of the business is from cash payments made to the creditors of the business.

AUDIT AND ETHICS

The valuation ratio of the business comprises of price-earning ratio, price to book value

ratio which are considered to be significant indicators for overall success of a business. The

price-earning ratio and price to book value ratio are shown to have increased from previous

year’s estimates which indicates that the business is developing.

The auditor needs to check the earning per shares of the business and the dividends which

is offered by the business to the shareholders for the period. The auditor also needs to verify the

share capital which is accumulated by the business.

Section 3

Analysis of Cash Flow Statement

The cash flow statement of the business shows the cash inflows and outflows of the

business during a particular year and the same is also a display of the liquidity position of the

business. The cash flow statement for Caltex ltd for the year 2017 shows cash from operating

activities, investing activities and financing activities.

The cash flow from operating activities of the business show the maximum cash inflows

of the business due to the receipts from the customers which is shown to be $ 23,693,457 for the

year. The cash from operating activities of the business is shown to be $ 735,032 which as

slightly fallen from previous year. The cash flow from investing activities show the maximum

cash outflow of the business (Bhandari & Iyer, 2013). This is because the business has acquired a

new business plant, property equipment and also made investments during the year. The primary

cash receipts which is shown in the operating section which is receipts from the customers which

is from the sales and the primary cash payments which is shown in the cash from operating

activities of the business is from cash payments made to the creditors of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT AND ETHICS

The main cash flow from investing and financing activities are mainly from purchase of

business net of cash in case of investing activities and the main cash which is acquired by the

business in case of financing activities is shown as borrowings of the business which is shown to

be $ 5,001,095.

The going concern principle is the fundamental principle in accounting process and the

auditor needs to report any factor which can affect the going concern principle of the business.

The liquidity ratio of the business shows that liquidity position of the business has deteriorate

from the previous year’s estimate which is not a favorable sign. The profits of the business has

fallen from previous year estimates and the overall cost of operations has increased. In addition

to this, the debt capital of the business has increased as well which increased the risks of debts. It

can be said that the indicators suggest that the going concern principle of the business might be

affected (Goh, Krishnan & Li, 2013). The auditor can advise the business to improve the

liquidity position and putting more reliance on equity capital rather than debt capital of the

business.

Review of the Auditor Report

The auditor of the company is one of the big four auditing firm KPMG who has prepared

the audit report of the business. As per the opinion of the auditor the financial statements are

prepared following relevant accounting standards and followed provisions of Corporation Act

2001 and therefore are also showing true and fair view. This means that the financial statements

are free from any material misstatements.

The key audit matter section of the audit report emphasizes on taxation issue which is

related to entities in Singapore for which certain uncertainties are there for the timing of the

AUDIT AND ETHICS

The main cash flow from investing and financing activities are mainly from purchase of

business net of cash in case of investing activities and the main cash which is acquired by the

business in case of financing activities is shown as borrowings of the business which is shown to

be $ 5,001,095.

The going concern principle is the fundamental principle in accounting process and the

auditor needs to report any factor which can affect the going concern principle of the business.

The liquidity ratio of the business shows that liquidity position of the business has deteriorate

from the previous year’s estimate which is not a favorable sign. The profits of the business has

fallen from previous year estimates and the overall cost of operations has increased. In addition

to this, the debt capital of the business has increased as well which increased the risks of debts. It

can be said that the indicators suggest that the going concern principle of the business might be

affected (Goh, Krishnan & Li, 2013). The auditor can advise the business to improve the

liquidity position and putting more reliance on equity capital rather than debt capital of the

business.

Review of the Auditor Report

The auditor of the company is one of the big four auditing firm KPMG who has prepared

the audit report of the business. As per the opinion of the auditor the financial statements are

prepared following relevant accounting standards and followed provisions of Corporation Act

2001 and therefore are also showing true and fair view. This means that the financial statements

are free from any material misstatements.

The key audit matter section of the audit report emphasizes on taxation issue which is

related to entities in Singapore for which certain uncertainties are there for the timing of the

11

AUDIT AND ETHICS

transactions as per the provisions of Australian Tax office (ATO). Another recognized key audit

matter relates to site remediation matters for oil and exploration projects which are of complex

nature and thus included in the key audit matters of the business.

AUDIT AND ETHICS

transactions as per the provisions of Australian Tax office (ATO). Another recognized key audit

matter relates to site remediation matters for oil and exploration projects which are of complex

nature and thus included in the key audit matters of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.