Detailed Financial Analysis of Caltex Australia for HI5002 Finance

VerifiedAdded on 2022/11/14

|23

|3898

|463

Report

AI Summary

This report presents a detailed financial analysis of Caltex Australia, an ASX-listed company, examining its performance using ratio analysis, cash management assessment, sensitivity analysis, and risk identification (systematic and unsystematic). The analysis includes profitability ratios (operating profit, net profit, and return on equity) and operating efficiency ratios (inventory turnover, account receivable turnover, and asset turnover). The report further assesses cash management, applies capital budgeting and sensitivity analysis, and identifies systematic and unsystematic risks impacting Caltex's performance. A dividend payout ratio is calculated to identify the company's dividend policy. The findings suggest that Caltex Australia is not in a high state of growth, exhibiting weak profitability and efficiency. The report concludes with a recommendation letter for institutional investors, offering insights to aid their investment decisions.

Finance for business - Masters

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

This report has been undertaken to examine the financial performance of selected ASX

listed entity, that is, Caltex Australia. The financial performance as examined through the use of

analysis of ratios, cash management, sensitivity, dividend payout, systematic and unsystematic

risks ahs reflected that the company is presently not in a high state of growth and development, It

has weak profitability, cash management and efficiency position and therefore an investor need

to examine the future financial performance before taking any significant investment decision.

2

This report has been undertaken to examine the financial performance of selected ASX

listed entity, that is, Caltex Australia. The financial performance as examined through the use of

analysis of ratios, cash management, sensitivity, dividend payout, systematic and unsystematic

risks ahs reflected that the company is presently not in a high state of growth and development, It

has weak profitability, cash management and efficiency position and therefore an investor need

to examine the future financial performance before taking any significant investment decision.

2

Contents

Abstract............................................................................................................................................2

1. Introduction..................................................................................................................................4

2. Financial Analysis of Caltex Australia........................................................................................4

2.1: Description of the Company.................................................................................................4

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia...............5

2.3: Cash Management Analysis...............................................................................................10

Part 2.4: Application of capital budgeting and sensitivity analysis...........................................11

2.5 Identification and Discussion of Systematic and Un-systematic Risk Impacting the

Performance of Caltex Australia...............................................................................................16

Unsystematic Risk.....................................................................................................................16

Systematic Risks........................................................................................................................17

Part 2.6: Calculation of dividend payout ratio and identification of dividend policy of Caltex

Australia Limited.......................................................................................................................19

3. Recommendation Letter.............................................................................................................21

4. Conclusion.................................................................................................................................22

References......................................................................................................................................23

3

Abstract............................................................................................................................................2

1. Introduction..................................................................................................................................4

2. Financial Analysis of Caltex Australia........................................................................................4

2.1: Description of the Company.................................................................................................4

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia...............5

2.3: Cash Management Analysis...............................................................................................10

Part 2.4: Application of capital budgeting and sensitivity analysis...........................................11

2.5 Identification and Discussion of Systematic and Un-systematic Risk Impacting the

Performance of Caltex Australia...............................................................................................16

Unsystematic Risk.....................................................................................................................16

Systematic Risks........................................................................................................................17

Part 2.6: Calculation of dividend payout ratio and identification of dividend policy of Caltex

Australia Limited.......................................................................................................................19

3. Recommendation Letter.............................................................................................................21

4. Conclusion.................................................................................................................................22

References......................................................................................................................................23

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Introduction

The purpose of the present report is to develop an understanding of the methods used in

conducting financial analysis of a selected listed company within ASX. The financial analysis

has been performed through evaluation of the financial statements of the selected company. The

overall financial evaluation of the selected company is done for proving suggestions to

institutional investors for investing within the Australian market. The recommendations provided

through report will assist the investors to take correct investment decision based on the financial

outcomes of the company.

The ASX listed entity selected for financial evaluation purpose is Caltex Australia, a

transport based fuel supplier and convenience retailer of Australia. The report, in this context,

has performed financial analysis of the selected company through the use of ratio analysis,

evaluation of its cash management, performing sensitivity analysis, identifications of the

systematic and unsystematic risks and examination of its dividend policy. The recommendation

letter is provided to the institutional investors on the basis of overall evaluation conducted and

lastly the findings obtained are summarized in the conclusion section of the report.

2. Financial Analysis of Caltex Australia

2.1: Description of the Company

Caltex Australia Limited is a recognized Australian based Transport Company involved

in providing fuel and operates convenience stores across Australia. The core activities of the

company consist of purchasing, distributing and marketing of petroleum based products and also

operating its convenience stories. It is an ASX listed entity that has attained a leading position in

meeting the fuel needs within Australia. It has developed a flexible supply chain that has enabled

it to develop high quality fuel products to its diverse number of customer segments such as retail,

mining, agriculture, aviation, marine and automotive sector. In addition to this, it is also

recognized to be prominent convenience retailers within the country. It is only fuel and

convenience retailing company of Australia that is listed on the ASX. It has attained a unique

position among the refiner and marketers in Australia on the basis of carrying out its operations

4

The purpose of the present report is to develop an understanding of the methods used in

conducting financial analysis of a selected listed company within ASX. The financial analysis

has been performed through evaluation of the financial statements of the selected company. The

overall financial evaluation of the selected company is done for proving suggestions to

institutional investors for investing within the Australian market. The recommendations provided

through report will assist the investors to take correct investment decision based on the financial

outcomes of the company.

The ASX listed entity selected for financial evaluation purpose is Caltex Australia, a

transport based fuel supplier and convenience retailer of Australia. The report, in this context,

has performed financial analysis of the selected company through the use of ratio analysis,

evaluation of its cash management, performing sensitivity analysis, identifications of the

systematic and unsystematic risks and examination of its dividend policy. The recommendation

letter is provided to the institutional investors on the basis of overall evaluation conducted and

lastly the findings obtained are summarized in the conclusion section of the report.

2. Financial Analysis of Caltex Australia

2.1: Description of the Company

Caltex Australia Limited is a recognized Australian based Transport Company involved

in providing fuel and operates convenience stores across Australia. The core activities of the

company consist of purchasing, distributing and marketing of petroleum based products and also

operating its convenience stories. It is an ASX listed entity that has attained a leading position in

meeting the fuel needs within Australia. It has developed a flexible supply chain that has enabled

it to develop high quality fuel products to its diverse number of customer segments such as retail,

mining, agriculture, aviation, marine and automotive sector. In addition to this, it is also

recognized to be prominent convenience retailers within the country. It is only fuel and

convenience retailing company of Australia that is listed on the ASX. It has attained a unique

position among the refiner and marketers in Australia on the basis of carrying out its operations

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in an independent manner and all the decision-taking is with management and the Board (Caltex

Australia: Our Company, 2019).

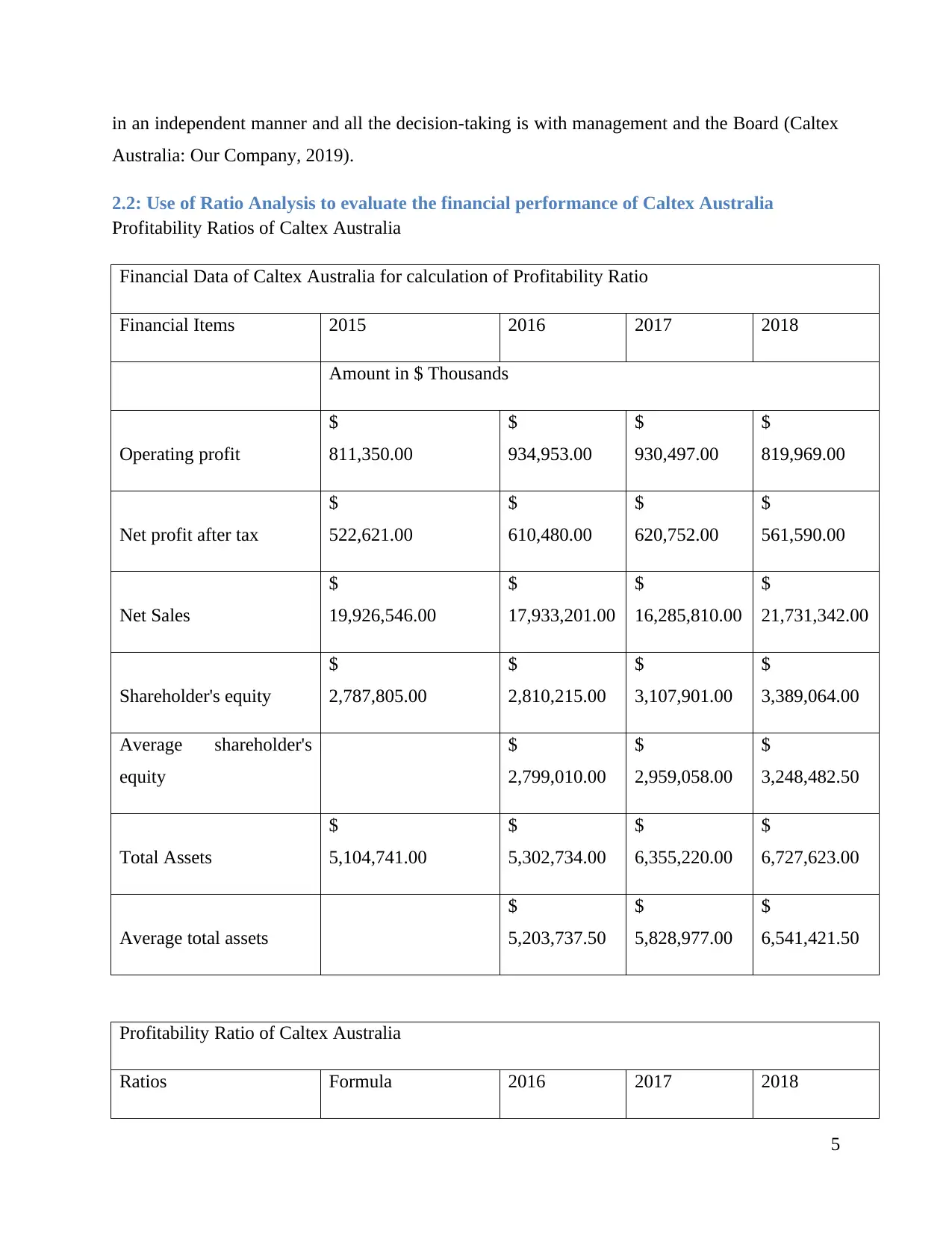

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia

Profitability Ratios of Caltex Australia

Financial Data of Caltex Australia for calculation of Profitability Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Operating profit

$

811,350.00

$

934,953.00

$

930,497.00

$

819,969.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Shareholder's equity

$

2,787,805.00

$

2,810,215.00

$

3,107,901.00

$

3,389,064.00

Average shareholder's

equity

$

2,799,010.00

$

2,959,058.00

$

3,248,482.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

5

Australia: Our Company, 2019).

2.2: Use of Ratio Analysis to evaluate the financial performance of Caltex Australia

Profitability Ratios of Caltex Australia

Financial Data of Caltex Australia for calculation of Profitability Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Operating profit

$

811,350.00

$

934,953.00

$

930,497.00

$

819,969.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Shareholder's equity

$

2,787,805.00

$

2,810,215.00

$

3,107,901.00

$

3,389,064.00

Average shareholder's

equity

$

2,799,010.00

$

2,959,058.00

$

3,248,482.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

5

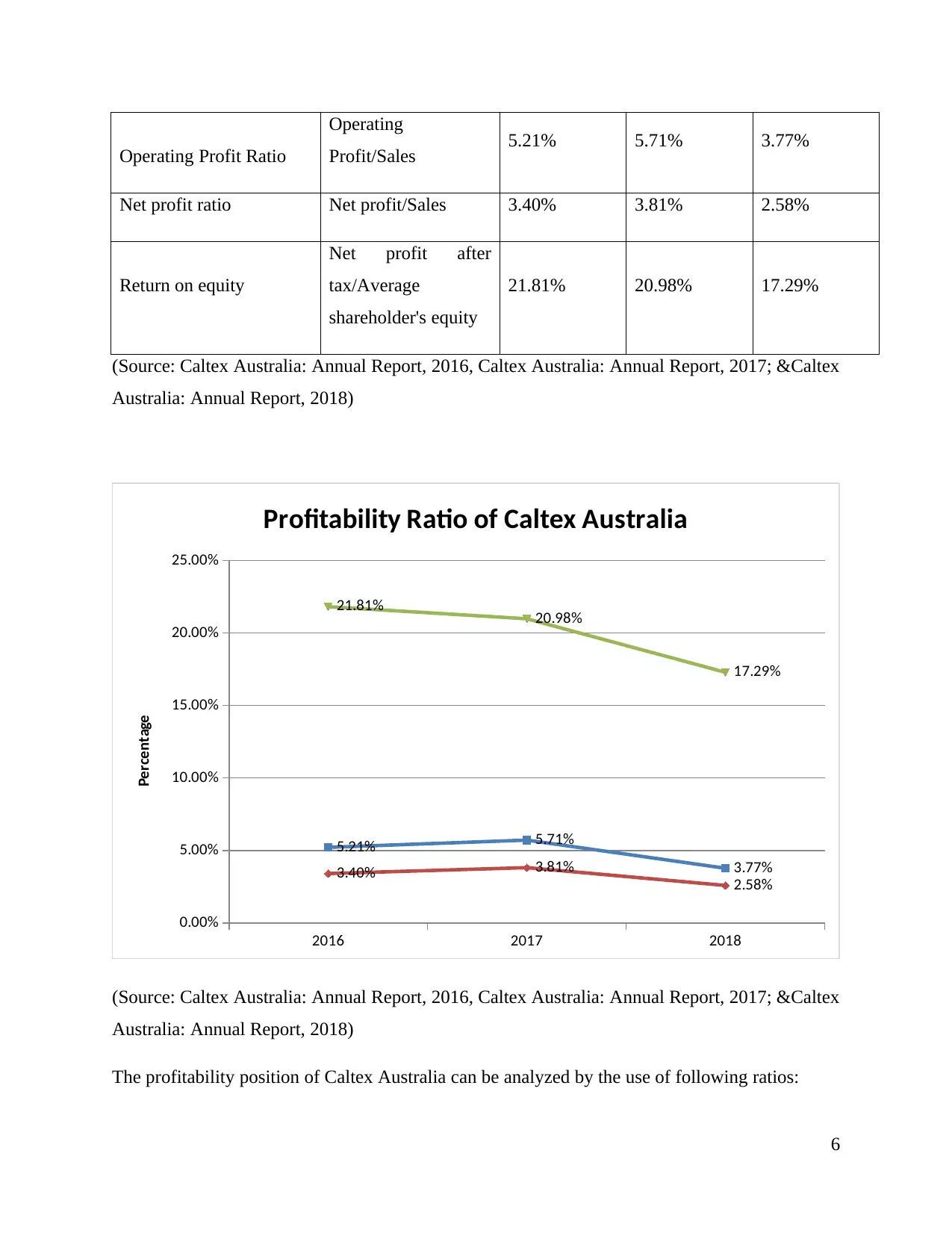

Operating Profit Ratio

Operating

Profit/Sales 5.21% 5.71% 3.77%

Net profit ratio Net profit/Sales 3.40% 3.81% 2.58%

Return on equity

Net profit after

tax/Average

shareholder's equity

21.81% 20.98% 17.29%

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

5.21% 5.71%

3.77%3.40% 3.81%

2.58%

21.81% 20.98%

17.29%

Profitability Ratio of Caltex Australia

Percentage

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

The profitability position of Caltex Australia can be analyzed by the use of following ratios:

6

Operating

Profit/Sales 5.21% 5.71% 3.77%

Net profit ratio Net profit/Sales 3.40% 3.81% 2.58%

Return on equity

Net profit after

tax/Average

shareholder's equity

21.81% 20.98% 17.29%

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

5.21% 5.71%

3.77%3.40% 3.81%

2.58%

21.81% 20.98%

17.29%

Profitability Ratio of Caltex Australia

Percentage

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017; &Caltex

Australia: Annual Report, 2018)

The profitability position of Caltex Australia can be analyzed by the use of following ratios:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating Profit Ratio: The Operating Profit ratio indicates the profit from operating

Activities attributable towards per $ of net Sales. Caltex Australia’s operating Profit has

an upward trend from 2016 to 2017 but in 2018 it has a downward trend as operating

profit ratio comes to 3.77% from 5.71%. If we analyses the data the reason behind a low

operating profit as compared to 2017’s operating profit is increase in selling and

distribution expenses. Net sales in 2018 is increased as compared to previous years so as

other expenses, but Caltex Australia had to spent a higher amount on selling and

distribution expenses. It may be due to new competitors in market, or availability of

substitutes in market resulting in a low operating profit (Krantz, 2016).

Net Profit Ratio: Net Profit Ratio Measures the net profit attributable towards per $ of

Net Sales. However Net profit ratio is also increased from 3.40% (2016) to 3.81 %( 2017)

but then it went down to 2.58% in 2018. The reason behind the downward trend in year

2017 to year 2018 is the same as of the operating profit ratio. Because Caltex Australia

has a low finance cost and a high share of profit/loss from other entities as compared to

2017. Company had to spend money on Selling and distribution of its products due to

competitors and substitutes available in market (Reilly and Brown, 2011).

Return on Equity: ROE states the rate of return realized by company on its equity

investment. Here also an upward trend is noticed in year 2016 to year 2017 but then there

is a downward trend in year 2017 to 2018. However the downward trend is not because

of increase in equity (Moles and Kidwekk, 2011). But it can be said that Caltex Australia

has lower finance cost as compared to 2017 that shows that it has repaid its debt resulting

in a lower profit as well as company has created reserves in 2018 which was not there in

2017 or can say has a negative balance in 2017. Thus Caltex Australia has a low return on

equity 17.29% as compared to 2017 of 20.98%.

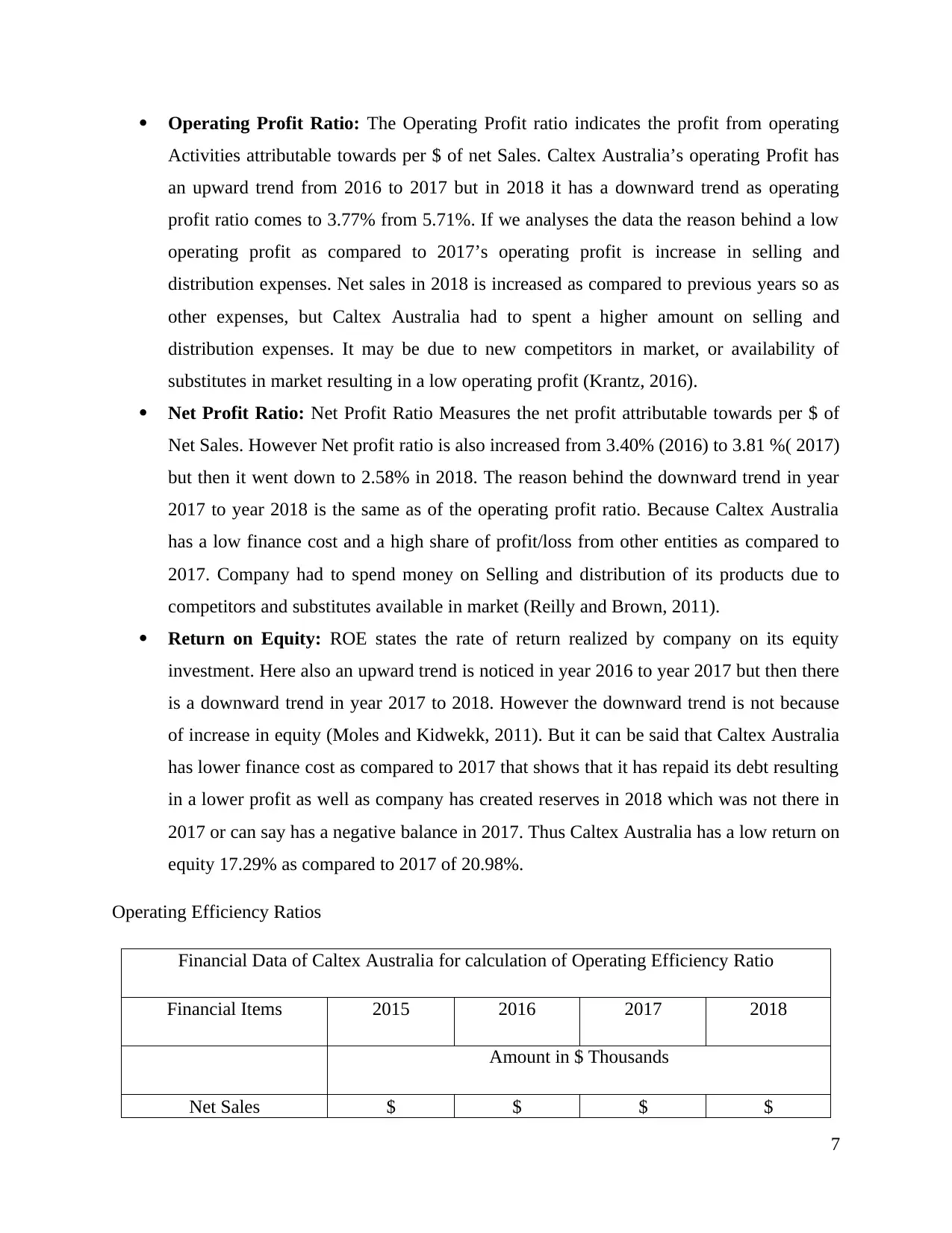

Operating Efficiency Ratios

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ $ $ $

7

Activities attributable towards per $ of net Sales. Caltex Australia’s operating Profit has

an upward trend from 2016 to 2017 but in 2018 it has a downward trend as operating

profit ratio comes to 3.77% from 5.71%. If we analyses the data the reason behind a low

operating profit as compared to 2017’s operating profit is increase in selling and

distribution expenses. Net sales in 2018 is increased as compared to previous years so as

other expenses, but Caltex Australia had to spent a higher amount on selling and

distribution expenses. It may be due to new competitors in market, or availability of

substitutes in market resulting in a low operating profit (Krantz, 2016).

Net Profit Ratio: Net Profit Ratio Measures the net profit attributable towards per $ of

Net Sales. However Net profit ratio is also increased from 3.40% (2016) to 3.81 %( 2017)

but then it went down to 2.58% in 2018. The reason behind the downward trend in year

2017 to year 2018 is the same as of the operating profit ratio. Because Caltex Australia

has a low finance cost and a high share of profit/loss from other entities as compared to

2017. Company had to spend money on Selling and distribution of its products due to

competitors and substitutes available in market (Reilly and Brown, 2011).

Return on Equity: ROE states the rate of return realized by company on its equity

investment. Here also an upward trend is noticed in year 2016 to year 2017 but then there

is a downward trend in year 2017 to 2018. However the downward trend is not because

of increase in equity (Moles and Kidwekk, 2011). But it can be said that Caltex Australia

has lower finance cost as compared to 2017 that shows that it has repaid its debt resulting

in a lower profit as well as company has created reserves in 2018 which was not there in

2017 or can say has a negative balance in 2017. Thus Caltex Australia has a low return on

equity 17.29% as compared to 2017 of 20.98%.

Operating Efficiency Ratios

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ $ $ $

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19,926,546.00 17,933,201.00 16,285,810.00 21,731,342.00

Account Receivables

$

681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average account

receivable

$

714,563.50

$

835,002.50

$

1,053,222.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Cost of Goods Sold

$

12,903,682.00

$

11,154,208.00

$

14,125,384.00

$

19,606,994.00

Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Inventory Turnover ratio

Cost of goods

sold/Average

inventory

10.88 10.18 11.84

Account Receivable

turnover ratio

Net

sales/Average

account

receivables

25.10 19.50 20.63

8

Account Receivables

$

681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average account

receivable

$

714,563.50

$

835,002.50

$

1,053,222.50

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Cost of Goods Sold

$

12,903,682.00

$

11,154,208.00

$

14,125,384.00

$

19,606,994.00

Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Inventory Turnover ratio

Cost of goods

sold/Average

inventory

10.88 10.18 11.84

Account Receivable

turnover ratio

Net

sales/Average

account

receivables

25.10 19.50 20.63

8

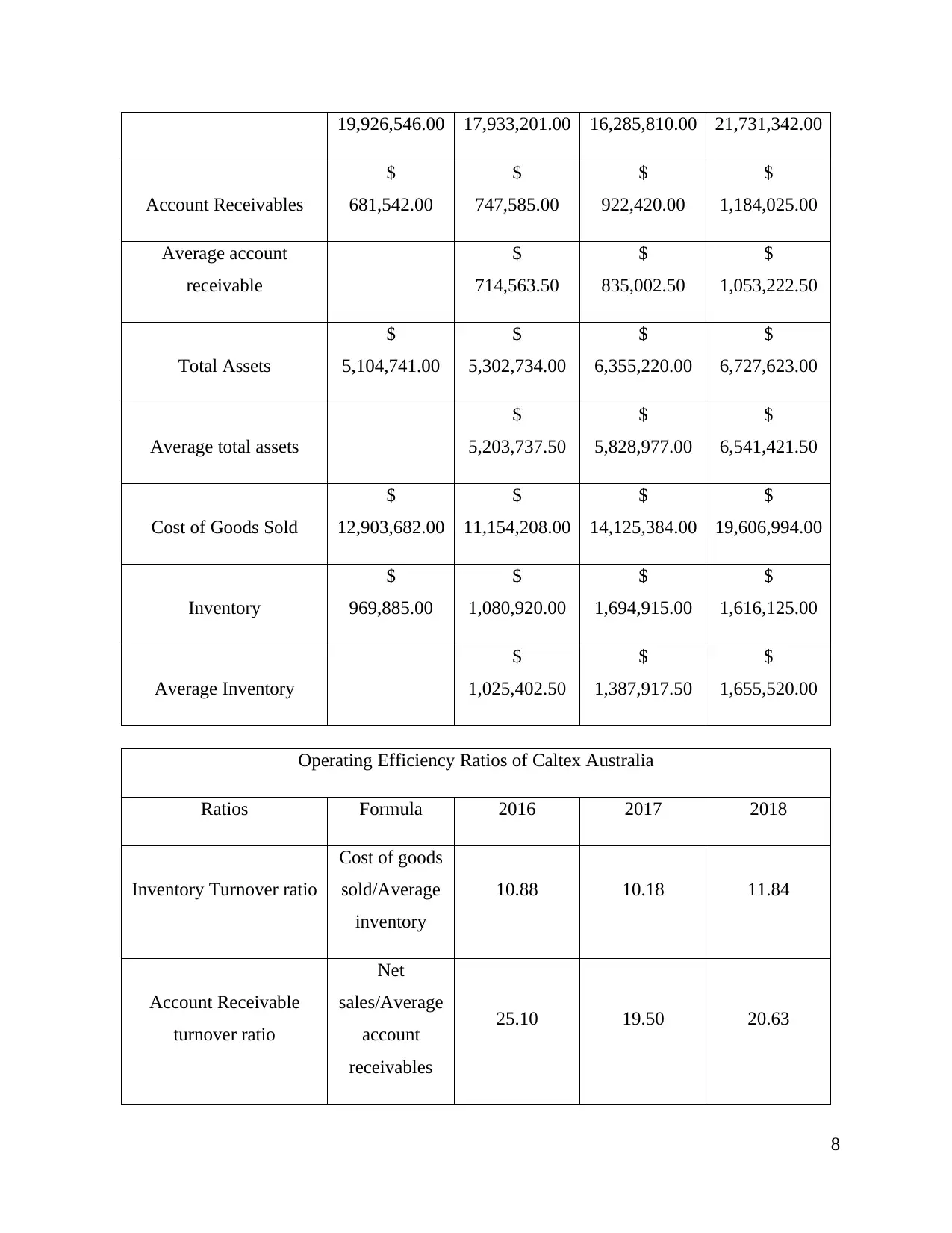

Asset Turnover ratio

Net

Sales/Average

total assets

3.45 2.79 3.32

2016

2017

2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

10.88

10.18 11.84

25.10

19.50 20.63

3.45

2.79 3.32

Operating Effeciency Ratio

Axis Title

Times

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017 &Caltex

Australia: Annual Report, 2018)

The operational efficiency of Caltex Australia has been analyzed with calculation of following

ratios:

Inventory Turnover Ratio: This ratio depicts how many times a company has sold or

replaced its inventory during a period. Caltex Australia has an overall upward trend in

inventory turnover ratio from 2016 to 2018 which is 10.88 to 11.84. It implies that

9

Net

Sales/Average

total assets

3.45 2.79 3.32

2016

2017

2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

10.88

10.18 11.84

25.10

19.50 20.63

3.45

2.79 3.32

Operating Effeciency Ratio

Axis Title

Times

(Source: Caltex Australia: Annual Report, 2016, Caltex Australia: Annual Report, 2017 &Caltex

Australia: Annual Report, 2018)

The operational efficiency of Caltex Australia has been analyzed with calculation of following

ratios:

Inventory Turnover Ratio: This ratio depicts how many times a company has sold or

replaced its inventory during a period. Caltex Australia has an overall upward trend in

inventory turnover ratio from 2016 to 2018 which is 10.88 to 11.84. It implies that

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company is very good at replacing its inventory regularly which will result in low cost of

holding and storage and improve its profitability in long run (Bragg, 2010).

Account Receivable Ratio: Account Receivable ratio depicts number of times a

company can realize payment from its average debtors in a year. If we look into the chart

we notice a downward trend but actually company is improving its efficiency. In 2016

this ratio was 25.10 times which comes to 19.50 times in 2017 but in 2018 company has

efficiently collected its debtors and it comes to 20.63. In 2017 the downward trend is

noticed because of loss of $14 million and in 2018 its $12 million.

Asset Turnover Ratio: This ratio shows company’s ability to best use of its assets to

generate revenue. A downward trend is noticed in past three years (2016-2018) which

may be due to the abnormal loss company has faced in 2017 and 2018. But overall

company is improving its efficiency and using its resources at its best to generate revenue

(Feldman and Libman, 2011).

2.3: Cash Management Analysis

Marketable securities are regarded as the liquid instruments of the company that can be

quickly transferred into cash for meeting the current financial obligations. The liquidity of

marketable securities is due to the fact that they possess the maturity of less than a year and

therefore can be quickly transferred into cash for meeting the financial obligations (Gibson,

2011). As analyzed form the balance sheet of Caltex Australia, the current assets of the company

includes cash and cash equivalents and receivables as marketable securities that presents the

assets that can be quickly transferred into cash. The cash and cash equivalents of the company

has depicted a decline over the past three financial years from 2016-2018 as analyzed from the

financial reports of the company over the selected time period. The cash and cash equivalents

have decreased from 116,606 to 6,142 over the selected financial period. On the other hand, its

account receivables have depicted a large increase over the selected time period as reflected in

the current assets of the company within its balance sheet. It has largely increased from 554,769

to 1,184,025 over the selected financial period (Caltex Australia: Annual Reports, 2019). These

means that the company need to quickly realize its accounts receivable for improving the future

cash flow position as it is holding less cash equivalents. The decrease in the cash equivalents can

results in causing a liquidity risk within the company due to its inability to meet the current

10

holding and storage and improve its profitability in long run (Bragg, 2010).

Account Receivable Ratio: Account Receivable ratio depicts number of times a

company can realize payment from its average debtors in a year. If we look into the chart

we notice a downward trend but actually company is improving its efficiency. In 2016

this ratio was 25.10 times which comes to 19.50 times in 2017 but in 2018 company has

efficiently collected its debtors and it comes to 20.63. In 2017 the downward trend is

noticed because of loss of $14 million and in 2018 its $12 million.

Asset Turnover Ratio: This ratio shows company’s ability to best use of its assets to

generate revenue. A downward trend is noticed in past three years (2016-2018) which

may be due to the abnormal loss company has faced in 2017 and 2018. But overall

company is improving its efficiency and using its resources at its best to generate revenue

(Feldman and Libman, 2011).

2.3: Cash Management Analysis

Marketable securities are regarded as the liquid instruments of the company that can be

quickly transferred into cash for meeting the current financial obligations. The liquidity of

marketable securities is due to the fact that they possess the maturity of less than a year and

therefore can be quickly transferred into cash for meeting the financial obligations (Gibson,

2011). As analyzed form the balance sheet of Caltex Australia, the current assets of the company

includes cash and cash equivalents and receivables as marketable securities that presents the

assets that can be quickly transferred into cash. The cash and cash equivalents of the company

has depicted a decline over the past three financial years from 2016-2018 as analyzed from the

financial reports of the company over the selected time period. The cash and cash equivalents

have decreased from 116,606 to 6,142 over the selected financial period. On the other hand, its

account receivables have depicted a large increase over the selected time period as reflected in

the current assets of the company within its balance sheet. It has largely increased from 554,769

to 1,184,025 over the selected financial period (Caltex Australia: Annual Reports, 2019). These

means that the company need to quickly realize its accounts receivable for improving the future

cash flow position as it is holding less cash equivalents. The decrease in the cash equivalents can

results in causing a liquidity risk within the company due to its inability to meet the current

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

obligations. The cash realized from its accounts receivables can provide large assistance to the

company in meeting its future financial obligations (Brigham and Michael, 2013).

Part 2.4: Application of capital budgeting and sensitivity analysis

Project Life 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per

year 450,000.00$

Initial Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Data Given

11

company in meeting its future financial obligations (Brigham and Michael, 2013).

Part 2.4: Application of capital budgeting and sensitivity analysis

Project Life 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per

year 450,000.00$

Initial Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Data Given

11

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

Statement of Cash flows

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,605,000.00$ 0.909 1,459,090.909$

2 1,605,000.00$ 0.826 1,326,446.281$

3 1,605,000.00$ 0.751 1,205,860.255$

4 2,405,000.00$ 0.683 1,642,647.360$

NPV 3,034,044.806$

Project NPV when there is no change in value drivers

12

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

Statement of Cash flows

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,605,000.00$ 0.909 1,459,090.909$

2 1,605,000.00$ 0.826 1,326,446.281$

3 1,605,000.00$ 0.751 1,205,860.255$

4 2,405,000.00$ 0.683 1,642,647.360$

NPV 3,034,044.806$

Project NPV when there is no change in value drivers

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.