Accounting for Management Decisions: Caltex Financial Analysis Report

VerifiedAdded on 2022/08/21

|14

|2514

|13

Report

AI Summary

This report provides a comprehensive financial analysis of Caltex Australia, assessing its performance based on key financial results, liquidity, solvency, utilization, profitability, and market-based ratios. The analysis includes an overview of Caltex's background, directors, and remuneration practices. It also examines the competitive landscape using Porter's Five Forces, evaluating supplier power, buyer power, the threat of new entrants, substitutes, and rivalry within the industry. The report delves into key financial results, including earnings per share and sales volumes, and evaluates various financial ratios to assess Caltex's financial health and efficiency. The analysis covers liquidity, solvency, utilization, profitability, and market-based metrics, providing insights into the company's financial performance over the analyzed period. Based on the evaluation, the report concludes with an investment recommendation, guiding potential investors on whether to buy, hold, or sell Caltex shares.

Running head: ACCOUNTING FOR MANAGEMENT DECISION

Accounting for management decision

Name of the Student

Name of the University

Author Note

Accounting for management decision

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGEMENT DECISION

Table of Contents

a) Background:........................................................................................................................2

b) Analysis of competitors of industry:...................................................................................3

c) Key financial results...........................................................................................................4

d) Key ratios:...........................................................................................................................4

e) Recommendation:...............................................................................................................9

References list:.........................................................................................................................10

Appendix:.................................................................................................................................12

Table of Contents

a) Background:........................................................................................................................2

b) Analysis of competitors of industry:...................................................................................3

c) Key financial results...........................................................................................................4

d) Key ratios:...........................................................................................................................4

e) Recommendation:...............................................................................................................9

References list:.........................................................................................................................10

Appendix:.................................................................................................................................12

ACCOUNTING FOR MANAGEMENT DECISION

a) Background:

a. Caltex is an iconic, proud and leading company of Australia which is engaged in

transporting fuel with a network of 1900 affiliated states. The company serve more than three

customers every week by its evolving range of convenience products and complicated supply

chain. It imports, refines and market the lubricants and fuels and meeting one third of the fuel

requirement of Australia (Caltex, 2020). Convenience is being taken to the whole new level

by way of embracing technologies.

b. Julian Segal is the chief financial officer and managing director of Caltex Australia

limited. For the workplace gender equality agency, managing director became a pay equity

ambassador. The board of directors of Caltex Australia comprises of Julian Segal, Steven

Gregg, Trevor Bourne, Melinda Conrad, Mark Chellew, Barbara Ward AM and Bruce

Morgan (Caltex, 2020).

c. Remuneration report is prepared by the directors of the company by adhering with the

section 300 A of the Corporation Act. As required by this section, information presented in

the remuneration report has been done. Fees of non-executive directors are fixed and for

chairing the board, the chairman of the company receives fee and no other fees are paid to

him. A base fee and an additional fees is received by the non-executive directors. In order to

retain and attract quality candidates in the market, remuneration elements are set at the

competitive elements. For removing the distinction in pay due to difference in gender,

reviewing of remuneration is done on a like for like job level.

d. Significant progress has been made by Caltex by the execution of infrastructure, fuels and

convenience retail strategies. The company have nearly doubled its earning per share over the

past five years and this has helped the organization in maintaining the position and

establishing the international footprints. Caltex has been set up for the sustainable growth

a) Background:

a. Caltex is an iconic, proud and leading company of Australia which is engaged in

transporting fuel with a network of 1900 affiliated states. The company serve more than three

customers every week by its evolving range of convenience products and complicated supply

chain. It imports, refines and market the lubricants and fuels and meeting one third of the fuel

requirement of Australia (Caltex, 2020). Convenience is being taken to the whole new level

by way of embracing technologies.

b. Julian Segal is the chief financial officer and managing director of Caltex Australia

limited. For the workplace gender equality agency, managing director became a pay equity

ambassador. The board of directors of Caltex Australia comprises of Julian Segal, Steven

Gregg, Trevor Bourne, Melinda Conrad, Mark Chellew, Barbara Ward AM and Bruce

Morgan (Caltex, 2020).

c. Remuneration report is prepared by the directors of the company by adhering with the

section 300 A of the Corporation Act. As required by this section, information presented in

the remuneration report has been done. Fees of non-executive directors are fixed and for

chairing the board, the chairman of the company receives fee and no other fees are paid to

him. A base fee and an additional fees is received by the non-executive directors. In order to

retain and attract quality candidates in the market, remuneration elements are set at the

competitive elements. For removing the distinction in pay due to difference in gender,

reviewing of remuneration is done on a like for like job level.

d. Significant progress has been made by Caltex by the execution of infrastructure, fuels and

convenience retail strategies. The company have nearly doubled its earning per share over the

past five years and this has helped the organization in maintaining the position and

establishing the international footprints. Caltex has been set up for the sustainable growth

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR MANAGEMENT DECISION

over the year 2019-2024 as it made significant progress in the execution of convenience retail

and fuel and infrastructure strategies. So far, the strategic partnership of Caltex with

Woolworths has been the most considerable step taken by the company in the retail strategy.

b) Analysis of competitors of industry:

a. Supplier power- The supply chain of Caltex Australia is complex and the company works

actively with the suppliers on private label packaging and packaging designs. Supplier’s

bargaining force is weaker for Caltex as they can easily switch to other suppliers as the

products are less differentiated and switching cost is low (Vetrov et al., 2017). Reasonable

pricing is provided by suppliers as the profits is closely associated with the suppliers pricing.

b. Buyer power- Bargaining power of buyers is weaker because of difficulties in switching

and they are less sensitive to price as they base their decisions on quality of products sold.

c. Threat of new entrants- The threat faced by new entrants is low as achieving economies

of scale is difficult and cost advantage cannot be easily reaped. Higher requirements of

capital also makes it difficult for the new entrants to enter the industry (Zainudin & Hashim,

2016).

d. Substitutes- Threat of substitutes is low as there is fewer availability of substitutes in the

industry of operation of Caltex. It is also less likely of buyers switching to the substitute

products as the products are sold by the firm at comparatively lower price.

e. Rivalries- The market space in which Caltex operates is highly competitive and the

increased competition from the existing competitors could adversely impact the operations.

Therefore, it can be said that rivalries from the existing competitors is high as the increased

competition is likely to adversely impact Caltex.

over the year 2019-2024 as it made significant progress in the execution of convenience retail

and fuel and infrastructure strategies. So far, the strategic partnership of Caltex with

Woolworths has been the most considerable step taken by the company in the retail strategy.

b) Analysis of competitors of industry:

a. Supplier power- The supply chain of Caltex Australia is complex and the company works

actively with the suppliers on private label packaging and packaging designs. Supplier’s

bargaining force is weaker for Caltex as they can easily switch to other suppliers as the

products are less differentiated and switching cost is low (Vetrov et al., 2017). Reasonable

pricing is provided by suppliers as the profits is closely associated with the suppliers pricing.

b. Buyer power- Bargaining power of buyers is weaker because of difficulties in switching

and they are less sensitive to price as they base their decisions on quality of products sold.

c. Threat of new entrants- The threat faced by new entrants is low as achieving economies

of scale is difficult and cost advantage cannot be easily reaped. Higher requirements of

capital also makes it difficult for the new entrants to enter the industry (Zainudin & Hashim,

2016).

d. Substitutes- Threat of substitutes is low as there is fewer availability of substitutes in the

industry of operation of Caltex. It is also less likely of buyers switching to the substitute

products as the products are sold by the firm at comparatively lower price.

e. Rivalries- The market space in which Caltex operates is highly competitive and the

increased competition from the existing competitors could adversely impact the operations.

Therefore, it can be said that rivalries from the existing competitors is high as the increased

competition is likely to adversely impact Caltex.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGEMENT DECISION

c) Key financial results

a) Earnings per share has nearly doubled for the past five years and has gained the

confidence of investors in the business. Outcome of earnings before interest and tax

aligned with the guidance of $ 570 million. Total volume of fuels sold was higher in

year 2019 by 2% by what was achieved in year 2017. The profit margin and volume

sold by Caltex was impacted by rising product and crude oil prices. Financial year

2018 delivered a lower earnings before and tax from the convenience retail business.

Fuel sales of total convenience retail was lower than 4% than what was reported in

year 2017. However, the supply volumes at the international level increased by 39%

in year 2018 compared to 2017 marking the total volume sold at 3.5 billion liters.

Great progress has been made by the team of convenience retail. Earnings per share

declined from $ 237.4 in year 2017 to $ 214.9 in year 2018 (Caltex, 2020).

d) Key ratios:

In this section, the financial performance of Caltex Australia limited is assessed by

examining various ratios such as efficiency, profitability, market based, solvency and

liquidity.

a. Liquidity

Liquidity position of Caltex limited is assessed by analyzing ratios such as current

ratio and quick ratio.

c) Key financial results

a) Earnings per share has nearly doubled for the past five years and has gained the

confidence of investors in the business. Outcome of earnings before interest and tax

aligned with the guidance of $ 570 million. Total volume of fuels sold was higher in

year 2019 by 2% by what was achieved in year 2017. The profit margin and volume

sold by Caltex was impacted by rising product and crude oil prices. Financial year

2018 delivered a lower earnings before and tax from the convenience retail business.

Fuel sales of total convenience retail was lower than 4% than what was reported in

year 2017. However, the supply volumes at the international level increased by 39%

in year 2018 compared to 2017 marking the total volume sold at 3.5 billion liters.

Great progress has been made by the team of convenience retail. Earnings per share

declined from $ 237.4 in year 2017 to $ 214.9 in year 2018 (Caltex, 2020).

d) Key ratios:

In this section, the financial performance of Caltex Australia limited is assessed by

examining various ratios such as efficiency, profitability, market based, solvency and

liquidity.

a. Liquidity

Liquidity position of Caltex limited is assessed by analyzing ratios such as current

ratio and quick ratio.

ACCOUNTING FOR MANAGEMENT DECISION

2018 2017 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.31

1.16

1.43

0.6 0.4

0.7 Current Ratio

Quick Ratio

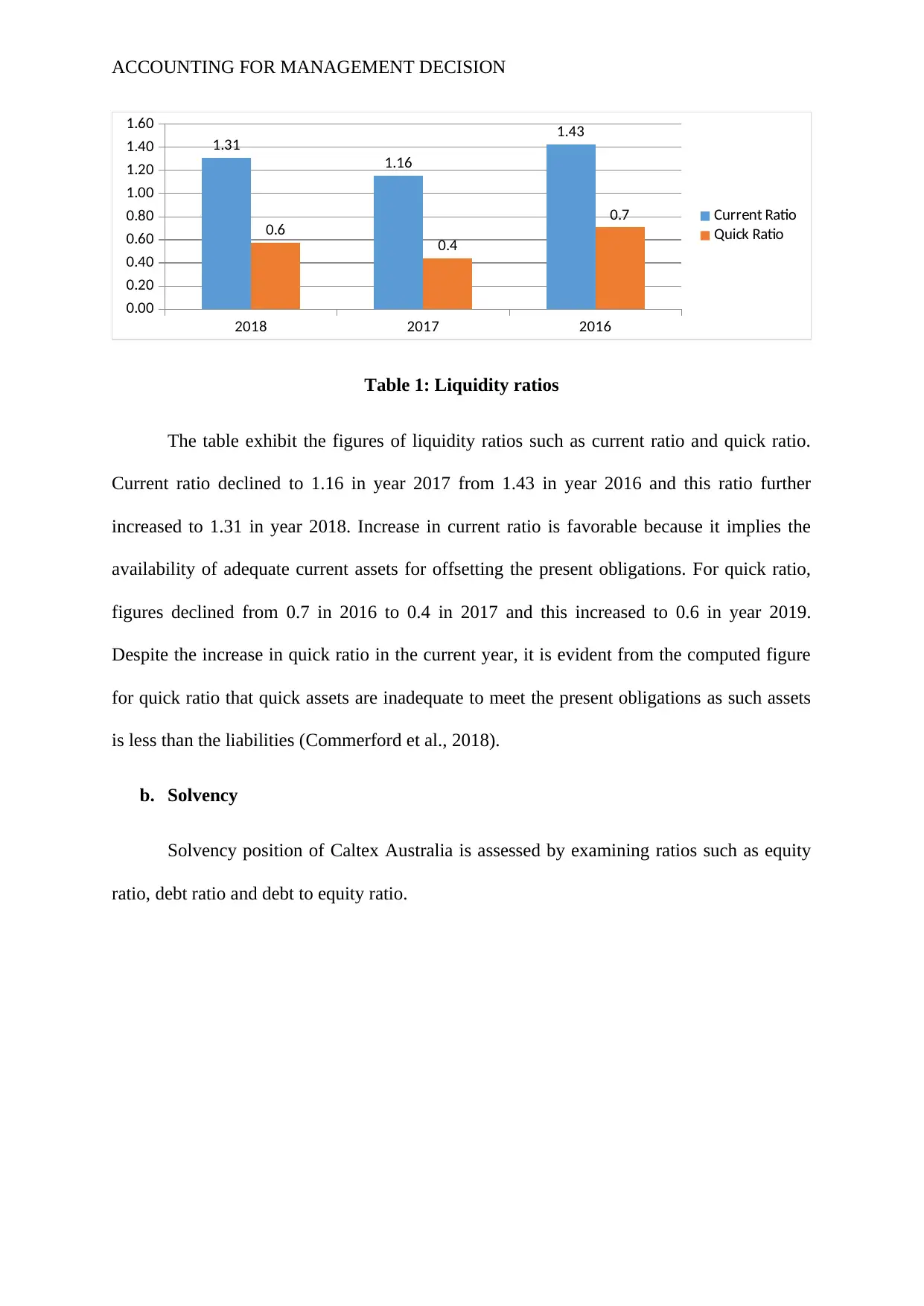

Table 1: Liquidity ratios

The table exhibit the figures of liquidity ratios such as current ratio and quick ratio.

Current ratio declined to 1.16 in year 2017 from 1.43 in year 2016 and this ratio further

increased to 1.31 in year 2018. Increase in current ratio is favorable because it implies the

availability of adequate current assets for offsetting the present obligations. For quick ratio,

figures declined from 0.7 in 2016 to 0.4 in 2017 and this increased to 0.6 in year 2019.

Despite the increase in quick ratio in the current year, it is evident from the computed figure

for quick ratio that quick assets are inadequate to meet the present obligations as such assets

is less than the liabilities (Commerford et al., 2018).

b. Solvency

Solvency position of Caltex Australia is assessed by examining ratios such as equity

ratio, debt ratio and debt to equity ratio.

2018 2017 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.31

1.16

1.43

0.6 0.4

0.7 Current Ratio

Quick Ratio

Table 1: Liquidity ratios

The table exhibit the figures of liquidity ratios such as current ratio and quick ratio.

Current ratio declined to 1.16 in year 2017 from 1.43 in year 2016 and this ratio further

increased to 1.31 in year 2018. Increase in current ratio is favorable because it implies the

availability of adequate current assets for offsetting the present obligations. For quick ratio,

figures declined from 0.7 in 2016 to 0.4 in 2017 and this increased to 0.6 in year 2019.

Despite the increase in quick ratio in the current year, it is evident from the computed figure

for quick ratio that quick assets are inadequate to meet the present obligations as such assets

is less than the liabilities (Commerford et al., 2018).

b. Solvency

Solvency position of Caltex Australia is assessed by examining ratios such as equity

ratio, debt ratio and debt to equity ratio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR MANAGEMENT DECISION

2018 2017 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0.99 1.04

0.89

0.50 0.51 0.47

0.50 0.49 0.53 Debt to Equity Ratio

Debt Ratio

Equity Ratio

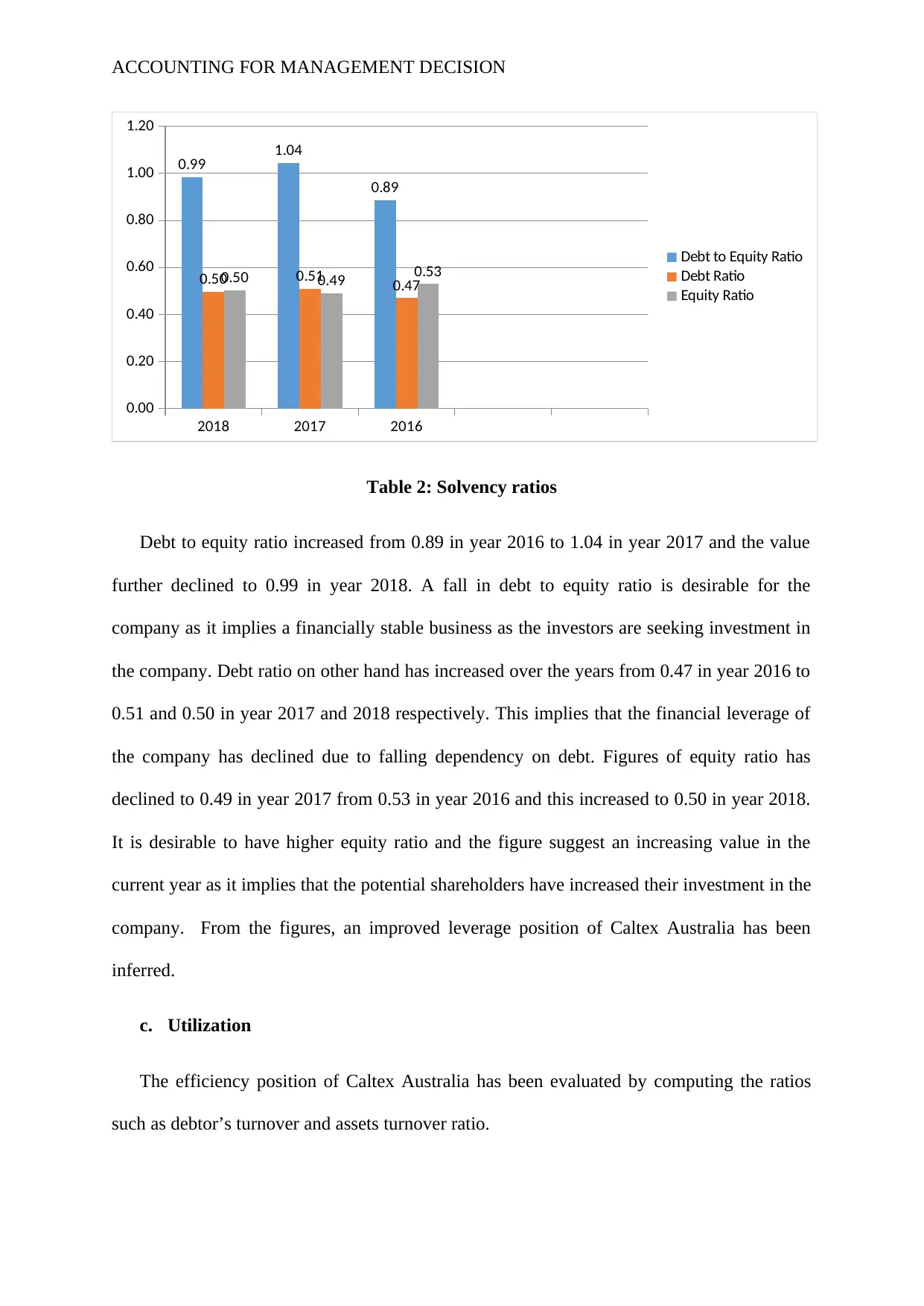

Table 2: Solvency ratios

Debt to equity ratio increased from 0.89 in year 2016 to 1.04 in year 2017 and the value

further declined to 0.99 in year 2018. A fall in debt to equity ratio is desirable for the

company as it implies a financially stable business as the investors are seeking investment in

the company. Debt ratio on other hand has increased over the years from 0.47 in year 2016 to

0.51 and 0.50 in year 2017 and 2018 respectively. This implies that the financial leverage of

the company has declined due to falling dependency on debt. Figures of equity ratio has

declined to 0.49 in year 2017 from 0.53 in year 2016 and this increased to 0.50 in year 2018.

It is desirable to have higher equity ratio and the figure suggest an increasing value in the

current year as it implies that the potential shareholders have increased their investment in the

company. From the figures, an improved leverage position of Caltex Australia has been

inferred.

c. Utilization

The efficiency position of Caltex Australia has been evaluated by computing the ratios

such as debtor’s turnover and assets turnover ratio.

2018 2017 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

0.99 1.04

0.89

0.50 0.51 0.47

0.50 0.49 0.53 Debt to Equity Ratio

Debt Ratio

Equity Ratio

Table 2: Solvency ratios

Debt to equity ratio increased from 0.89 in year 2016 to 1.04 in year 2017 and the value

further declined to 0.99 in year 2018. A fall in debt to equity ratio is desirable for the

company as it implies a financially stable business as the investors are seeking investment in

the company. Debt ratio on other hand has increased over the years from 0.47 in year 2016 to

0.51 and 0.50 in year 2017 and 2018 respectively. This implies that the financial leverage of

the company has declined due to falling dependency on debt. Figures of equity ratio has

declined to 0.49 in year 2017 from 0.53 in year 2016 and this increased to 0.50 in year 2018.

It is desirable to have higher equity ratio and the figure suggest an increasing value in the

current year as it implies that the potential shareholders have increased their investment in the

company. From the figures, an improved leverage position of Caltex Australia has been

inferred.

c. Utilization

The efficiency position of Caltex Australia has been evaluated by computing the ratios

such as debtor’s turnover and assets turnover ratio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGEMENT DECISION

2018 2017 2016

0.00

5.00

10.00

15.00

20.00

25.00

30.00

18.35 17.66

23.99

3.23 2.56 3.38

Debtors Turnover

Total Asset turnover

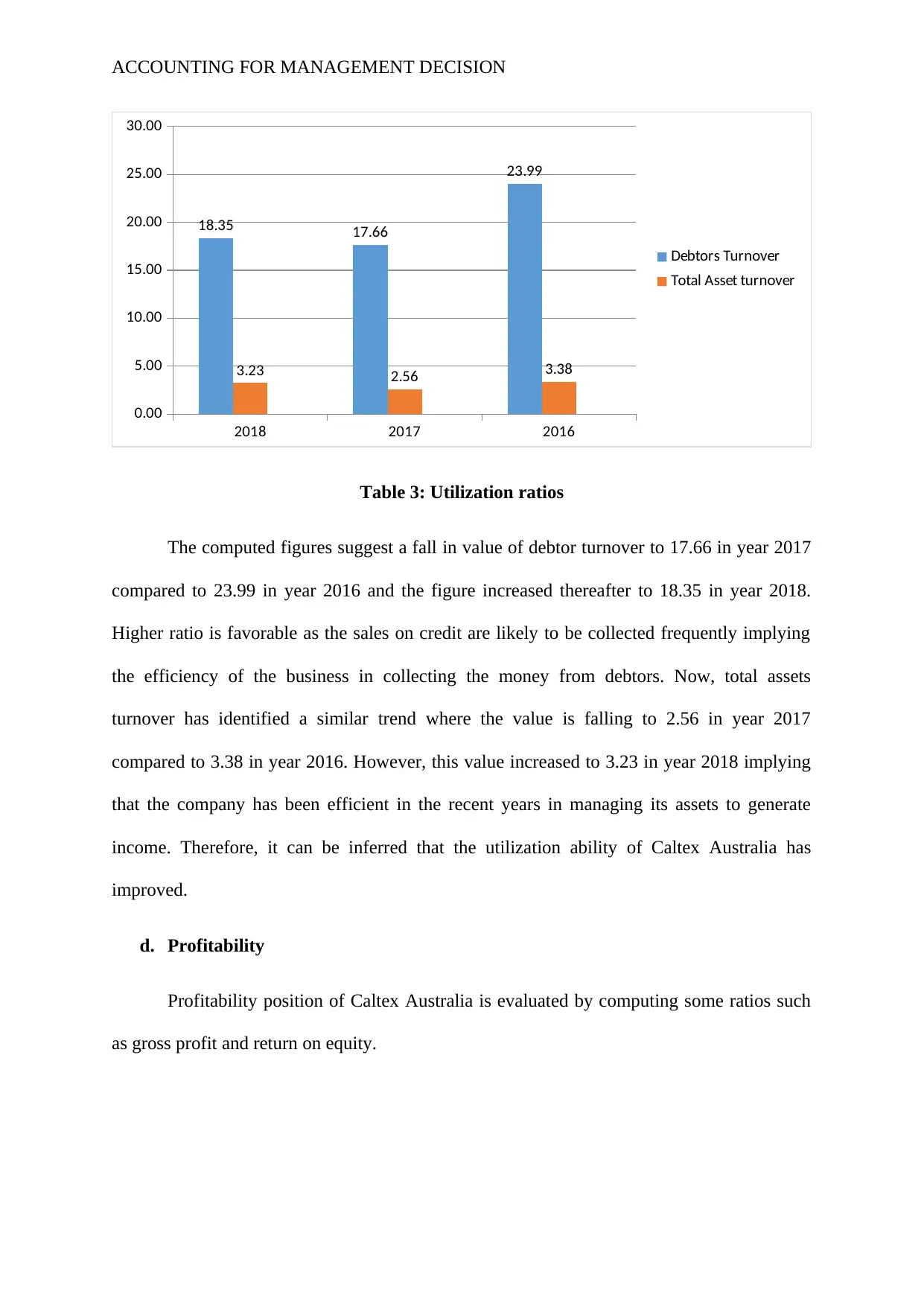

Table 3: Utilization ratios

The computed figures suggest a fall in value of debtor turnover to 17.66 in year 2017

compared to 23.99 in year 2016 and the figure increased thereafter to 18.35 in year 2018.

Higher ratio is favorable as the sales on credit are likely to be collected frequently implying

the efficiency of the business in collecting the money from debtors. Now, total assets

turnover has identified a similar trend where the value is falling to 2.56 in year 2017

compared to 3.38 in year 2016. However, this value increased to 3.23 in year 2018 implying

that the company has been efficient in the recent years in managing its assets to generate

income. Therefore, it can be inferred that the utilization ability of Caltex Australia has

improved.

d. Profitability

Profitability position of Caltex Australia is evaluated by computing some ratios such

as gross profit and return on equity.

2018 2017 2016

0.00

5.00

10.00

15.00

20.00

25.00

30.00

18.35 17.66

23.99

3.23 2.56 3.38

Debtors Turnover

Total Asset turnover

Table 3: Utilization ratios

The computed figures suggest a fall in value of debtor turnover to 17.66 in year 2017

compared to 23.99 in year 2016 and the figure increased thereafter to 18.35 in year 2018.

Higher ratio is favorable as the sales on credit are likely to be collected frequently implying

the efficiency of the business in collecting the money from debtors. Now, total assets

turnover has identified a similar trend where the value is falling to 2.56 in year 2017

compared to 3.38 in year 2016. However, this value increased to 3.23 in year 2018 implying

that the company has been efficient in the recent years in managing its assets to generate

income. Therefore, it can be inferred that the utilization ability of Caltex Australia has

improved.

d. Profitability

Profitability position of Caltex Australia is evaluated by computing some ratios such

as gross profit and return on equity.

ACCOUNTING FOR MANAGEMENT DECISION

2018 2017 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

9.78%

13.27%

11.11%

16.57%

19.97%

21.72%

Gross Profit Margin Return on Equity

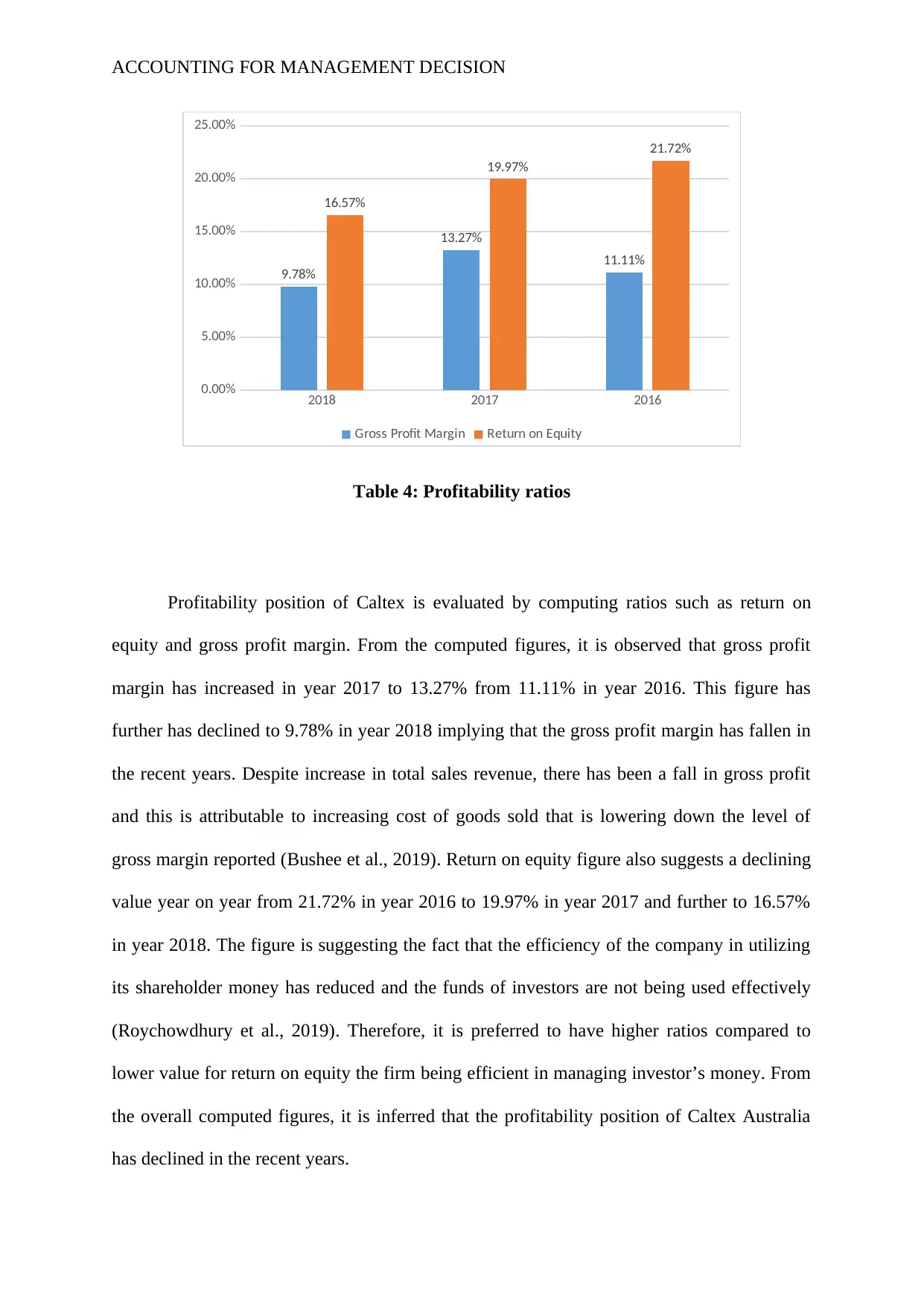

Table 4: Profitability ratios

Profitability position of Caltex is evaluated by computing ratios such as return on

equity and gross profit margin. From the computed figures, it is observed that gross profit

margin has increased in year 2017 to 13.27% from 11.11% in year 2016. This figure has

further has declined to 9.78% in year 2018 implying that the gross profit margin has fallen in

the recent years. Despite increase in total sales revenue, there has been a fall in gross profit

and this is attributable to increasing cost of goods sold that is lowering down the level of

gross margin reported (Bushee et al., 2019). Return on equity figure also suggests a declining

value year on year from 21.72% in year 2016 to 19.97% in year 2017 and further to 16.57%

in year 2018. The figure is suggesting the fact that the efficiency of the company in utilizing

its shareholder money has reduced and the funds of investors are not being used effectively

(Roychowdhury et al., 2019). Therefore, it is preferred to have higher ratios compared to

lower value for return on equity the firm being efficient in managing investor’s money. From

the overall computed figures, it is inferred that the profitability position of Caltex Australia

has declined in the recent years.

2018 2017 2016

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

9.78%

13.27%

11.11%

16.57%

19.97%

21.72%

Gross Profit Margin Return on Equity

Table 4: Profitability ratios

Profitability position of Caltex is evaluated by computing ratios such as return on

equity and gross profit margin. From the computed figures, it is observed that gross profit

margin has increased in year 2017 to 13.27% from 11.11% in year 2016. This figure has

further has declined to 9.78% in year 2018 implying that the gross profit margin has fallen in

the recent years. Despite increase in total sales revenue, there has been a fall in gross profit

and this is attributable to increasing cost of goods sold that is lowering down the level of

gross margin reported (Bushee et al., 2019). Return on equity figure also suggests a declining

value year on year from 21.72% in year 2016 to 19.97% in year 2017 and further to 16.57%

in year 2018. The figure is suggesting the fact that the efficiency of the company in utilizing

its shareholder money has reduced and the funds of investors are not being used effectively

(Roychowdhury et al., 2019). Therefore, it is preferred to have higher ratios compared to

lower value for return on equity the firm being efficient in managing investor’s money. From

the overall computed figures, it is inferred that the profitability position of Caltex Australia

has declined in the recent years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR MANAGEMENT DECISION

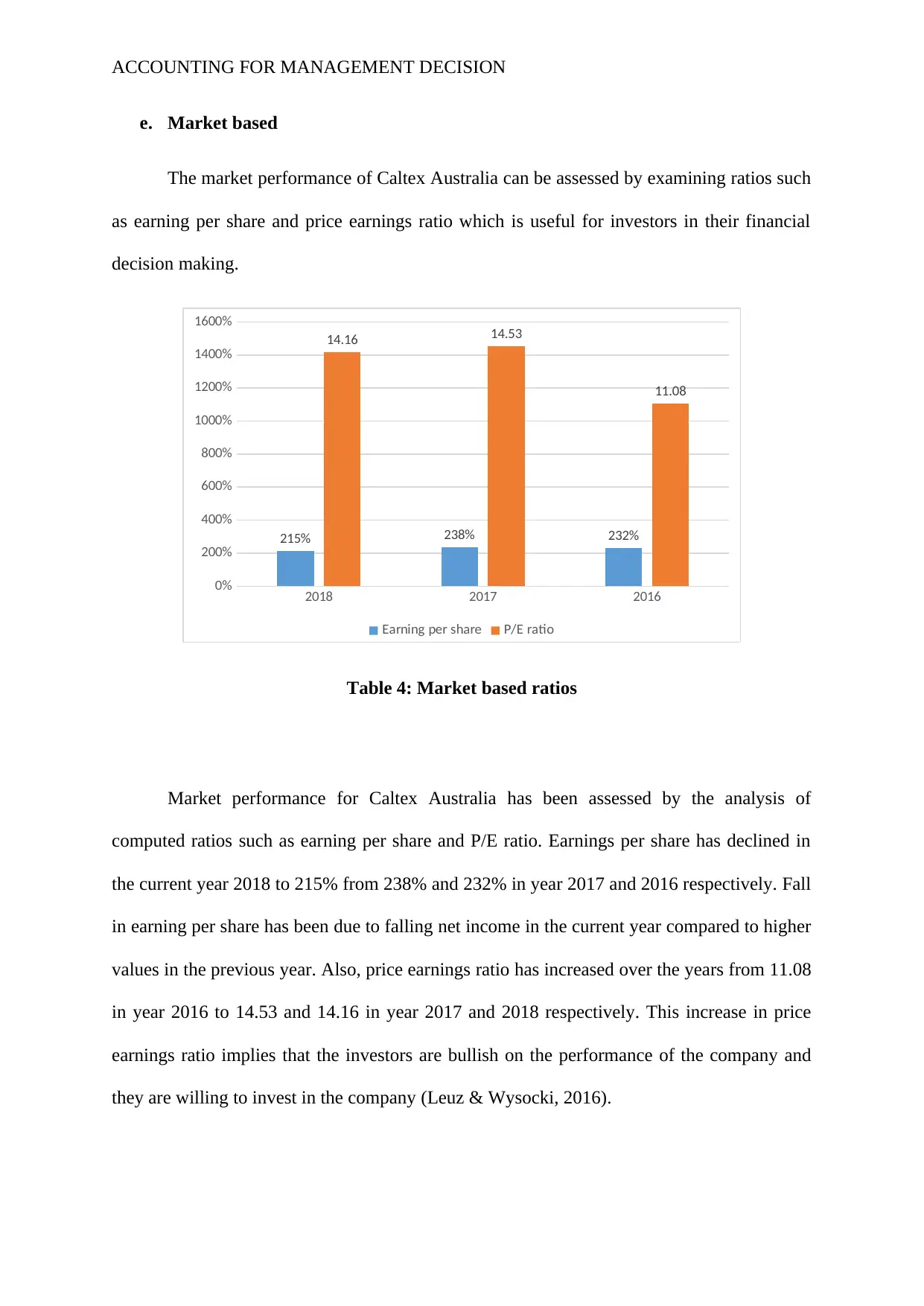

e. Market based

The market performance of Caltex Australia can be assessed by examining ratios such

as earning per share and price earnings ratio which is useful for investors in their financial

decision making.

2018 2017 2016

0%

200%

400%

600%

800%

1000%

1200%

1400%

1600%

215% 238% 232%

14.16 14.53

11.08

Earning per share P/E ratio

Table 4: Market based ratios

Market performance for Caltex Australia has been assessed by the analysis of

computed ratios such as earning per share and P/E ratio. Earnings per share has declined in

the current year 2018 to 215% from 238% and 232% in year 2017 and 2016 respectively. Fall

in earning per share has been due to falling net income in the current year compared to higher

values in the previous year. Also, price earnings ratio has increased over the years from 11.08

in year 2016 to 14.53 and 14.16 in year 2017 and 2018 respectively. This increase in price

earnings ratio implies that the investors are bullish on the performance of the company and

they are willing to invest in the company (Leuz & Wysocki, 2016).

e. Market based

The market performance of Caltex Australia can be assessed by examining ratios such

as earning per share and price earnings ratio which is useful for investors in their financial

decision making.

2018 2017 2016

0%

200%

400%

600%

800%

1000%

1200%

1400%

1600%

215% 238% 232%

14.16 14.53

11.08

Earning per share P/E ratio

Table 4: Market based ratios

Market performance for Caltex Australia has been assessed by the analysis of

computed ratios such as earning per share and P/E ratio. Earnings per share has declined in

the current year 2018 to 215% from 238% and 232% in year 2017 and 2016 respectively. Fall

in earning per share has been due to falling net income in the current year compared to higher

values in the previous year. Also, price earnings ratio has increased over the years from 11.08

in year 2016 to 14.53 and 14.16 in year 2017 and 2018 respectively. This increase in price

earnings ratio implies that the investors are bullish on the performance of the company and

they are willing to invest in the company (Leuz & Wysocki, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGEMENT DECISION

e) Recommendation:

a. From the overall analysis of the figures relating to various ratios identifying the

performance of company, it has been ascertained that Caltex has become more

efficient in generating income and have improved their financial leverage. However,

there has been fall in the profitability level and earnings per share paid to the

shareholders. Nonetheless, price earnings ratios have improved year on year and the

figures being recorded at 14.53 in year 2017 compared to 14.16 in year 2018.

Although, the profitability of Caltex has declined recently, investors are bullish on

their investment in the shares of the company. Therefore, it is recommended to the

exiting investors to hold the shares and the new investors should hold on to buy the

shares.

References list:

Bushee, B. J., Goodman, T. H., & Sunder, S. V. (2019). Financial reporting quality,

investment horizon, and institutional investor trading strategies. The Accounting

Review, 94(3), 87-112.

Caltex. (2020). Annual Reports & Reviews | Caltex Australia. [online] Available at:

https://www.caltex.com.au/our-company/investor-centre/annual-reports-and-reviews

[Accessed 31 Jan. 2020].

e) Recommendation:

a. From the overall analysis of the figures relating to various ratios identifying the

performance of company, it has been ascertained that Caltex has become more

efficient in generating income and have improved their financial leverage. However,

there has been fall in the profitability level and earnings per share paid to the

shareholders. Nonetheless, price earnings ratios have improved year on year and the

figures being recorded at 14.53 in year 2017 compared to 14.16 in year 2018.

Although, the profitability of Caltex has declined recently, investors are bullish on

their investment in the shares of the company. Therefore, it is recommended to the

exiting investors to hold the shares and the new investors should hold on to buy the

shares.

References list:

Bushee, B. J., Goodman, T. H., & Sunder, S. V. (2019). Financial reporting quality,

investment horizon, and institutional investor trading strategies. The Accounting

Review, 94(3), 87-112.

Caltex. (2020). Annual Reports & Reviews | Caltex Australia. [online] Available at:

https://www.caltex.com.au/our-company/investor-centre/annual-reports-and-reviews

[Accessed 31 Jan. 2020].

ACCOUNTING FOR MANAGEMENT DECISION

Chychyla, R., Leone, A. J., & Minutti-Meza, M. (2019). Complexity of financial reporting

standards and accounting expertise. Journal of Accounting and Economics, 67(1), 226-253.

Commerford, B. P., Hatfield, R. C., & Houston, R. W. (2018). The effect of real earnings

management on auditor scrutiny of management's other financial reporting decisions. The

accounting review, 93(5), 145-163.

Hassan, O. A., & Marston, C. (2019). Corporate Financial Disclosure Measurement in the

Empirical Accounting Literature: A Review Article. The International Journal of

Accounting, 54(02), 1950006.

Ioan, È. A., Ioana, G. A., & Andreea, M. P. (2018). Influence of Managerial Accounting in

the Decision Making Process. Ovidius University Annals, Economic Sciences Series, 18(2),

707-711.

Koo, D. S., Ramalingegowda, S., & Yu, Y. (2017). The effect of financial reporting quality

on corporate dividend policy. Review of Accounting Studies, 22(2), 753-790.

Leuz, C., & Wysocki, P. D. (2016). The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of accounting

research, 54(2), 525-622.

Richardson, A. J. (2017). The relationship between management and financial accounting as

professions and technologies of practice. In The Role of the Management Accountant (pp.

246-261). Routledge.

Roychowdhury, S., Shroff, N., & Verdi, R. S. (2019). The effects of financial reporting and

disclosure on corporate investment: A review. Journal of Accounting and Economics, 68(2-

3), 101246.

Chychyla, R., Leone, A. J., & Minutti-Meza, M. (2019). Complexity of financial reporting

standards and accounting expertise. Journal of Accounting and Economics, 67(1), 226-253.

Commerford, B. P., Hatfield, R. C., & Houston, R. W. (2018). The effect of real earnings

management on auditor scrutiny of management's other financial reporting decisions. The

accounting review, 93(5), 145-163.

Hassan, O. A., & Marston, C. (2019). Corporate Financial Disclosure Measurement in the

Empirical Accounting Literature: A Review Article. The International Journal of

Accounting, 54(02), 1950006.

Ioan, È. A., Ioana, G. A., & Andreea, M. P. (2018). Influence of Managerial Accounting in

the Decision Making Process. Ovidius University Annals, Economic Sciences Series, 18(2),

707-711.

Koo, D. S., Ramalingegowda, S., & Yu, Y. (2017). The effect of financial reporting quality

on corporate dividend policy. Review of Accounting Studies, 22(2), 753-790.

Leuz, C., & Wysocki, P. D. (2016). The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of accounting

research, 54(2), 525-622.

Richardson, A. J. (2017). The relationship between management and financial accounting as

professions and technologies of practice. In The Role of the Management Accountant (pp.

246-261). Routledge.

Roychowdhury, S., Shroff, N., & Verdi, R. S. (2019). The effects of financial reporting and

disclosure on corporate investment: A review. Journal of Accounting and Economics, 68(2-

3), 101246.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.