Financial Reporting Analysis of Caltex Australia Limited

VerifiedAdded on 2023/06/08

|8

|1832

|355

Report

AI Summary

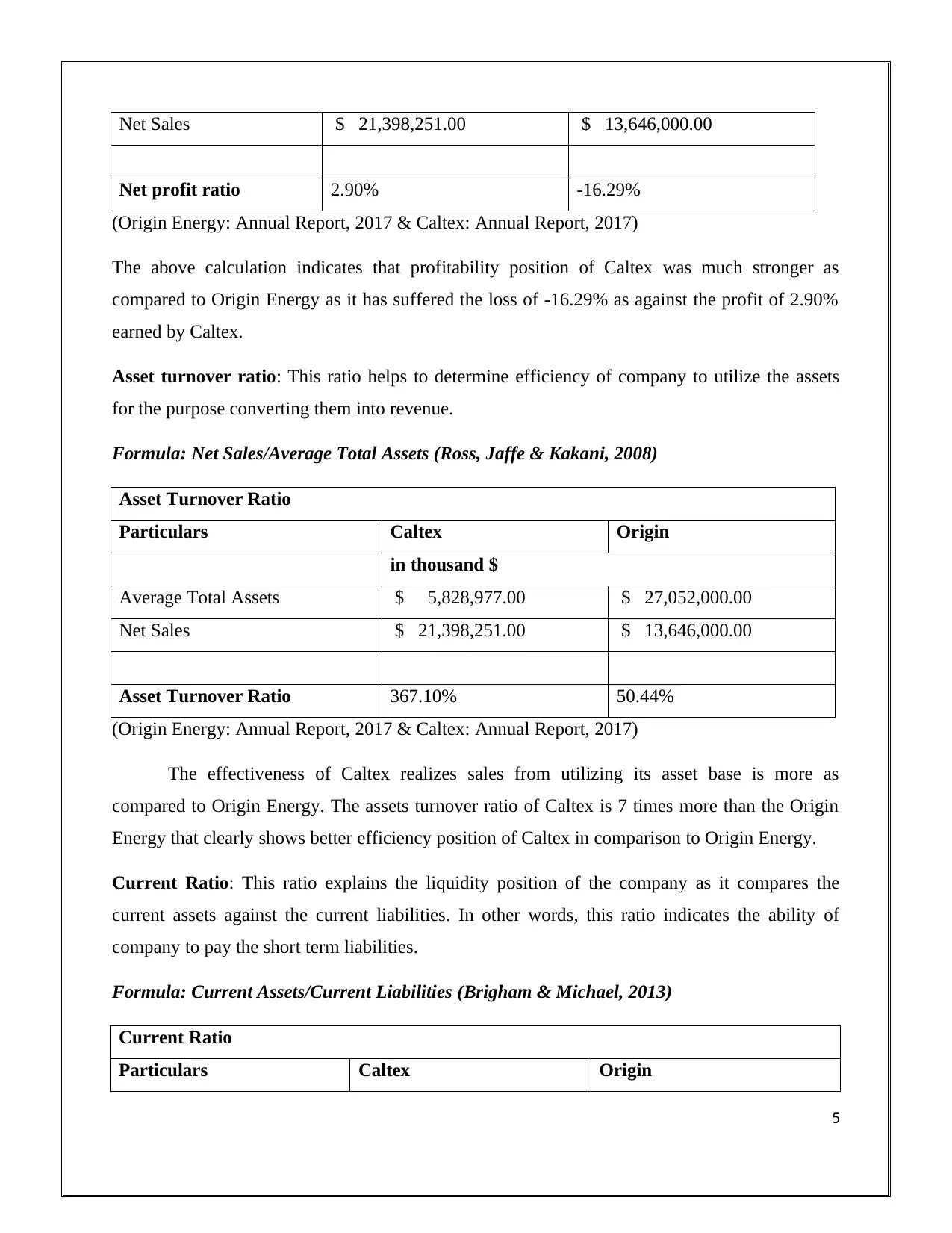

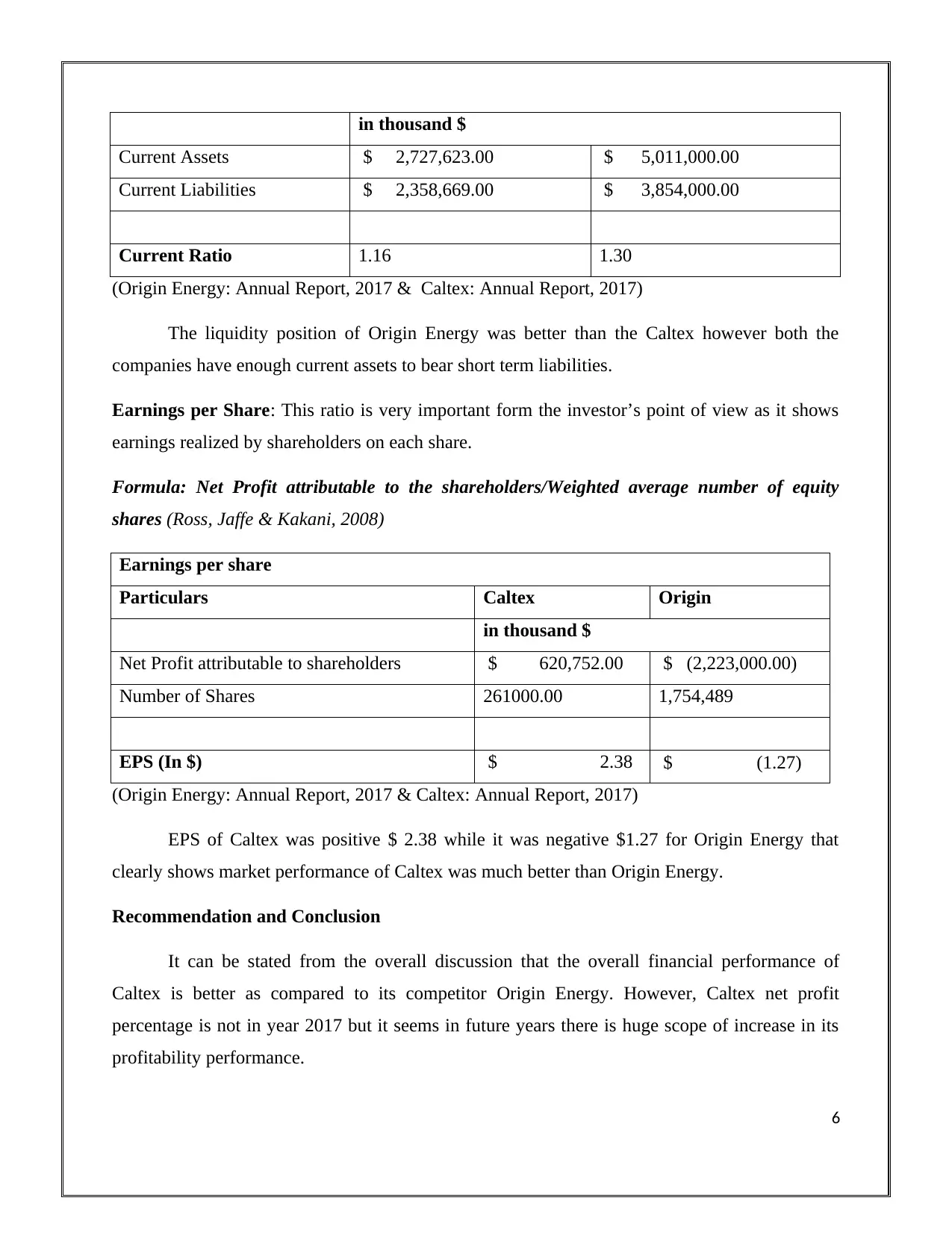

This report critically analyzes Caltex Australia Limited's application of General Purpose Financial Reporting, examining its effectiveness in meeting the obligations of the conceptual accounting framework as directed by the Australian Accounting Standards Board (AASB). It compares Caltex's annual report with that of Origin Energy, focusing on adherence to AASB, conceptual framework, and corporation law, using ratio analysis to compare the company's net profit ratio, asset turnover ratio, current ratio, and earnings per share. The analysis reveals that Caltex has a stronger profitability position, better efficiency in utilizing assets, and a positive EPS, making it a potentially favorable investment compared to Origin Energy. The report concludes that Caltex's financial reporting aligns with stakeholder theory, presenting a true and fair view to stakeholders, and recommends investment in Caltex based on its financial performance and compliance with accounting standards; access more solved assignments and reports on Desklib.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.