Caltex Australia Pvt Ltd: Executive Summary on ABC Model and Tools

VerifiedAdded on 2020/10/04

|11

|2642

|176

Report

AI Summary

This report provides an executive summary analyzing the application of the Activity Based Costing (ABC) model for Caltex Australia Pvt Ltd, a transport fuel supplier. It begins by explaining the ABC model, detailing its features and advantages over traditional costing methods, emphasizing its usefulness in allocating costs to activities and improving cost control. The report then aligns the ABC model with Caltex Australia's current goals and strategies, focusing on optimizing infrastructure, expanding trading and shipping, growing the supply base, and enhancing customer offerings. Recommendations are provided for implementing the ABC model within the company, highlighting the importance of activity-based cost allocation and identifying areas for cost reduction. Furthermore, the report discusses the suitability of budgetary control as another management accounting tool beneficial for Caltex Australia, emphasizing its role in comparing planned and actual performance to identify and address variances, ultimately assisting the company in meeting its objectives.

Caltex Australia pvt Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The management accounting tools are important in organisation. ABC model is discussed

in the report in relation to Caltex Australia Pvt Ltd so that it may extract benefits out of the same.

Features and importance are discussed of this model in accordance to the goals and strategies of

firm.

The management accounting tools are important in organisation. ABC model is discussed

in the report in relation to Caltex Australia Pvt Ltd so that it may extract benefits out of the same.

Features and importance are discussed of this model in accordance to the goals and strategies of

firm.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A) Explaining ABC model and its features............................................................................1

B) Explaining how ABC model aligns with current goals and strategies of Caltex Australia

Pvt Ltd....................................................................................................................................3

C) Providing recommendations about implementation of ABC model.................................5

D) Management accounting tool suitable for company apart from ABC model...................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

A) Explaining ABC model and its features............................................................................1

B) Explaining how ABC model aligns with current goals and strategies of Caltex Australia

Pvt Ltd....................................................................................................................................3

C) Providing recommendations about implementation of ABC model.................................5

D) Management accounting tool suitable for company apart from ABC model...................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting tools are beneficial in assisting management to take well-

structured decisions and strengthening internal operations of business. Present report deals with

importance of ABC model in Caltex Australia Pvt Ltd which is engaged in business of transport

fuel supplier. The features of ABC model is outlined in the report. Moreover, company's

corporate strategies and current goals are highlighted. Recommendations are imparted to

implement ABC system in firm for attaining benefits. Furthermore, another management

accounting tool such as budgetary control is explained which is also beneficial for business to

achieve objectives with much ease.

A) Explaining ABC model and its features

ABC (Activity Based Costing) model is effective technique which is helpful in

controlling costs of production in the best possible manner. ABC is a useful costing system

helping company in achieving desired manufacturing by allocating cost of each activity so that

overall expenses can be reduced up to a high extent. In simpler words, expenses are assigned to

each activity on the basis of actual consumption by them in effectual way. ABC model assigns

costs by identifying the same to various overheads and then allocates those expenditures to the

product. Hence, it is helpful as cost is recognised between overheads and manufactured items

and as such, it allocates indirect expenses to products in effective way (Introduction to Activity

Based Costing. 2018). This model is quite effective and better than traditional method as it do

not allocate costs in the manner which ABC model does. It is useful for Caltex Australia Pvt Ltd

to effectively assign costs and achieve production in the best possible manner.

ABC model is quite helpful in manufacturing sector as costs can be ascertained and

reliable figures are obtained with much ease. It classifies expenditures in a better way during

actual consumption and as a result, company can easily ascertain actual costs incurred during

manufacturing process of items in effective way (Plank, 2018). It helps to develop better

corporate strategies because expenses of production are grasped by this model with much ease.

Under ABC model, activity can be considered as a cost driver. It is termed as driver of activity

which effectively drives cost which is incurred in manufacturing a particular product in a better

way. ABC model enhances cost pools that could be utilised for assembling costs of overheads in

effectual manner. Moreover, ABC accumulates several indirect expenditures and as such, it is

1

Management accounting tools are beneficial in assisting management to take well-

structured decisions and strengthening internal operations of business. Present report deals with

importance of ABC model in Caltex Australia Pvt Ltd which is engaged in business of transport

fuel supplier. The features of ABC model is outlined in the report. Moreover, company's

corporate strategies and current goals are highlighted. Recommendations are imparted to

implement ABC system in firm for attaining benefits. Furthermore, another management

accounting tool such as budgetary control is explained which is also beneficial for business to

achieve objectives with much ease.

A) Explaining ABC model and its features

ABC (Activity Based Costing) model is effective technique which is helpful in

controlling costs of production in the best possible manner. ABC is a useful costing system

helping company in achieving desired manufacturing by allocating cost of each activity so that

overall expenses can be reduced up to a high extent. In simpler words, expenses are assigned to

each activity on the basis of actual consumption by them in effectual way. ABC model assigns

costs by identifying the same to various overheads and then allocates those expenditures to the

product. Hence, it is helpful as cost is recognised between overheads and manufactured items

and as such, it allocates indirect expenses to products in effective way (Introduction to Activity

Based Costing. 2018). This model is quite effective and better than traditional method as it do

not allocate costs in the manner which ABC model does. It is useful for Caltex Australia Pvt Ltd

to effectively assign costs and achieve production in the best possible manner.

ABC model is quite helpful in manufacturing sector as costs can be ascertained and

reliable figures are obtained with much ease. It classifies expenditures in a better way during

actual consumption and as a result, company can easily ascertain actual costs incurred during

manufacturing process of items in effective way (Plank, 2018). It helps to develop better

corporate strategies because expenses of production are grasped by this model with much ease.

Under ABC model, activity can be considered as a cost driver. It is termed as driver of activity

which effectively drives cost which is incurred in manufacturing a particular product in a better

way. ABC model enhances cost pools that could be utilised for assembling costs of overheads in

effectual manner. Moreover, ABC accumulates several indirect expenditures and as such, it is

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

easy to initiate better control over costs. In relation to this, certain features of ABC model can be

discussed below-

1. ABC model is advantageous as it divides overall cost into two types such as fixed and

variable. This help to classify expenditures in respective categories and as such, quality

information is provided to management to effectively formulate suitable cost system in the

company.

2. Another feature of such model is that cost behaviour patterns are effectively

determined. It is possible as total cost is bifurcated into variable and fixed costs in the best

possible way (Zhuang and Chang, 2017). On the other hand, various behaviour patterns such as

volume related pattern, event related and time related patterns. Moreover, diversity related cost

behaviour pattern are attained with much ease.

3. Next feature of ABC model is that relevant cost driver is required to be determined so

that it may be traced to particular product by the overheads. Moreover, cost drivers are

interrelated to cost behaviour pattern in effectual manner.

4. ABC model is helpful as it rectifies information related to costs which may be

inaccurate and as such, it helps to gather and grasp accurate cost information. Moreover, it helps

in allocating overheads on the basis of activity. Senior management can easily take decision

within stipulated time.

2

discussed below-

1. ABC model is advantageous as it divides overall cost into two types such as fixed and

variable. This help to classify expenditures in respective categories and as such, quality

information is provided to management to effectively formulate suitable cost system in the

company.

2. Another feature of such model is that cost behaviour patterns are effectively

determined. It is possible as total cost is bifurcated into variable and fixed costs in the best

possible way (Zhuang and Chang, 2017). On the other hand, various behaviour patterns such as

volume related pattern, event related and time related patterns. Moreover, diversity related cost

behaviour pattern are attained with much ease.

3. Next feature of ABC model is that relevant cost driver is required to be determined so

that it may be traced to particular product by the overheads. Moreover, cost drivers are

interrelated to cost behaviour pattern in effectual manner.

4. ABC model is helpful as it rectifies information related to costs which may be

inaccurate and as such, it helps to gather and grasp accurate cost information. Moreover, it helps

in allocating overheads on the basis of activity. Senior management can easily take decision

within stipulated time.

2

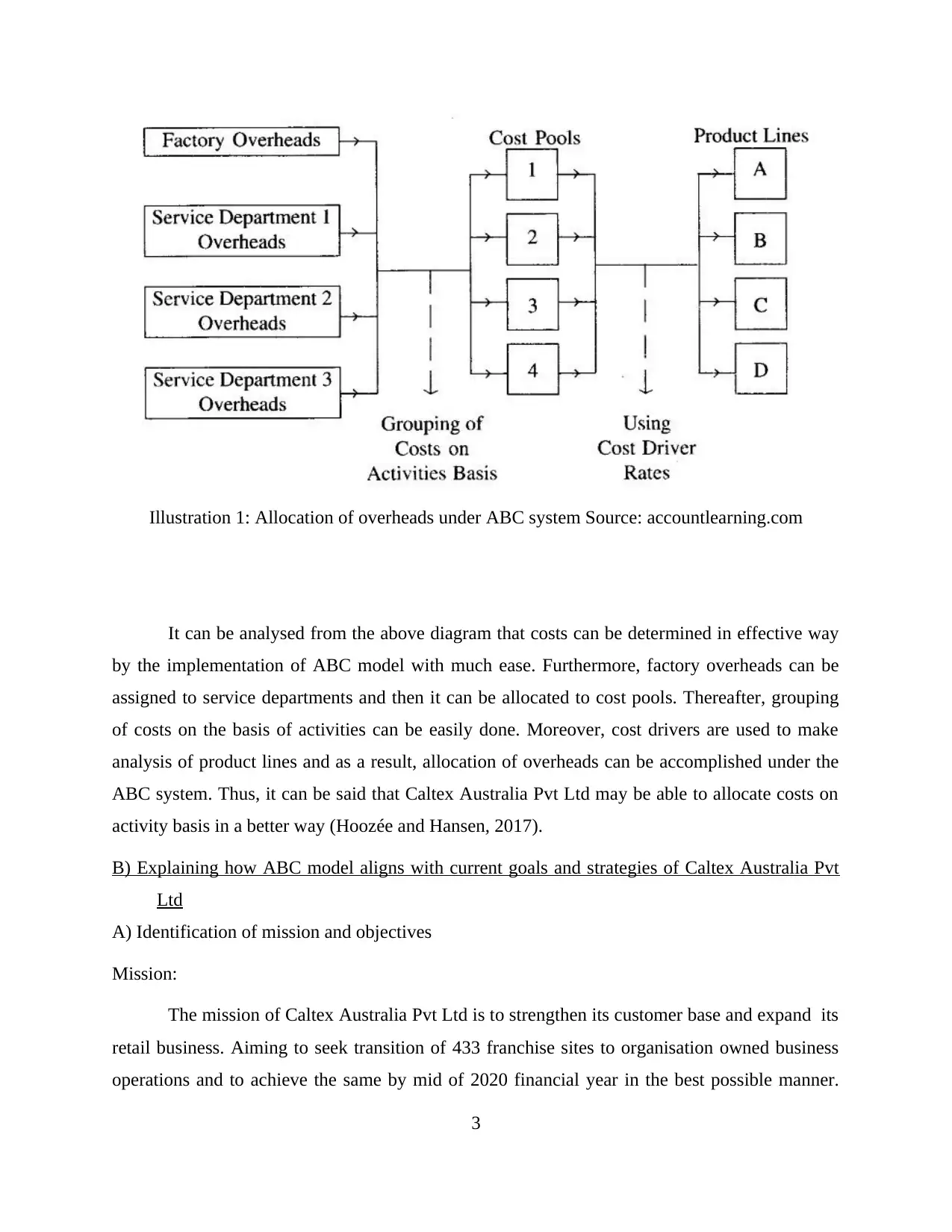

It can be analysed from the above diagram that costs can be determined in effective way

by the implementation of ABC model with much ease. Furthermore, factory overheads can be

assigned to service departments and then it can be allocated to cost pools. Thereafter, grouping

of costs on the basis of activities can be easily done. Moreover, cost drivers are used to make

analysis of product lines and as a result, allocation of overheads can be accomplished under the

ABC system. Thus, it can be said that Caltex Australia Pvt Ltd may be able to allocate costs on

activity basis in a better way (Hoozée and Hansen, 2017).

B) Explaining how ABC model aligns with current goals and strategies of Caltex Australia Pvt

Ltd

A) Identification of mission and objectives

Mission:

The mission of Caltex Australia Pvt Ltd is to strengthen its customer base and expand its

retail business. Aiming to seek transition of 433 franchise sites to organisation owned business

operations and to achieve the same by mid of 2020 financial year in the best possible manner.

3

Illustration 1: Allocation of overheads under ABC system Source: accountlearning.com

by the implementation of ABC model with much ease. Furthermore, factory overheads can be

assigned to service departments and then it can be allocated to cost pools. Thereafter, grouping

of costs on the basis of activities can be easily done. Moreover, cost drivers are used to make

analysis of product lines and as a result, allocation of overheads can be accomplished under the

ABC system. Thus, it can be said that Caltex Australia Pvt Ltd may be able to allocate costs on

activity basis in a better way (Hoozée and Hansen, 2017).

B) Explaining how ABC model aligns with current goals and strategies of Caltex Australia Pvt

Ltd

A) Identification of mission and objectives

Mission:

The mission of Caltex Australia Pvt Ltd is to strengthen its customer base and expand its

retail business. Aiming to seek transition of 433 franchise sites to organisation owned business

operations and to achieve the same by mid of 2020 financial year in the best possible manner.

3

Illustration 1: Allocation of overheads under ABC system Source: accountlearning.com

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Moreover, to launch between 50 and 60 foodary sites and nearly 5 to 10 Nashi high street

convenience sites in 2018 by investing at a cost of 100 million which is ahead of roll-out in

future periods.

Objectives:

To enhance customer experience in more consistent way

To roll-out brand new platforms

To achieve better quality by standardising services

To enhance and simplify the supply chain arrangements

B) Identification of corporate strategies of organisation

The strategies are required to be implemented so that company can attain objectives and

goals in effective manner by implementing well-structured strategies to outreach rivals. It helps

organisation to achieve market share as well. In relation to this, corporate strategies of Caltex

Australia Pvt Ltd are as follows-

1. Optimising infrastructure-

It is one of the focus of organisation to maintain cost-effective operations of supply chain

through optimum infrastructure. This will help to become proactive in responding and adapting

market dynamics and enhancing refinery management. Thus, strategy to expand and pursue new

opportunities in relation to infrastructure (Costabile, Fera, Fruggiero, Lambiase and Pham,

2017).

2. Expanding trading and shipping -

For expanding and developing capabilities and business operations of Ampol. This will

be beneficial for Caltex Australia Pvt Ltd to capture new opportunities and creating value in

delivering items and as such, Asia Pacific region can be explored in a better way. International

expansion will be possible and supply chain could be expand as well.

3. Grow supply base-

For executing strategies to maximise marketing volumes in target market or regions and

to support development of infrastructure in long-term and attaining competitive supply of items.

4

convenience sites in 2018 by investing at a cost of 100 million which is ahead of roll-out in

future periods.

Objectives:

To enhance customer experience in more consistent way

To roll-out brand new platforms

To achieve better quality by standardising services

To enhance and simplify the supply chain arrangements

B) Identification of corporate strategies of organisation

The strategies are required to be implemented so that company can attain objectives and

goals in effective manner by implementing well-structured strategies to outreach rivals. It helps

organisation to achieve market share as well. In relation to this, corporate strategies of Caltex

Australia Pvt Ltd are as follows-

1. Optimising infrastructure-

It is one of the focus of organisation to maintain cost-effective operations of supply chain

through optimum infrastructure. This will help to become proactive in responding and adapting

market dynamics and enhancing refinery management. Thus, strategy to expand and pursue new

opportunities in relation to infrastructure (Costabile, Fera, Fruggiero, Lambiase and Pham,

2017).

2. Expanding trading and shipping -

For expanding and developing capabilities and business operations of Ampol. This will

be beneficial for Caltex Australia Pvt Ltd to capture new opportunities and creating value in

delivering items and as such, Asia Pacific region can be explored in a better way. International

expansion will be possible and supply chain could be expand as well.

3. Grow supply base-

For executing strategies to maximise marketing volumes in target market or regions and

to support development of infrastructure in long-term and attaining competitive supply of items.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Fuel retailing offering to customers-

This strategy will help Caltex Australia Pvt Ltd to effectively analyse the market and then

offering fuel site offer to lure customers and increase in spending of consumers in the best

possible manner.

5. Creating new solutions for customers in the market-

Providing new customer solutions as network of more than 900 retail sites are in the

market and weekly customers over three millions. Thus, building new and attractive offers for

potential consumers across multiple channels and locations and enhancing satisfaction level in

effectual way.

C) How ABC model assists in accomplishing firm's strategies

ABC model is quite effectively for Caltex Australia Pvt Ltd to maintain cost level and

attaining reduction of expenses to carry out various manufacturing activities quite effectually

(Etienne and et.al, 2017). It can be assessed from the company's strategies that supply chain costs

can be controlled and better trading could be possible. The costs of trading may be analysed in a

better manner. ABC model is helpful as organisation may be able to allocate cost of overheads

with much ease. Furthermore, company can accumulate cost of infrastructure so that direct

labour costs can be managed in the best possible way. Thus, ABC model will be helpful to

company in allocating costs on the activity basis.

C) Providing recommendations about implementation of ABC model

ABC model is useful for company as costs can be classified on activity basis. In relation

to this, it is required that Caltex Australia Pvt Ltd should implement such model so that benefits

may be extracted as it is engaged in the business of transport fuel supplier and provides delivery

of fuel through complex supply chains in effective way. It is recommended to implement ABC

model as it will provide way to organisation to initiate control upon expenditures. In order to

meet customer's satisfaction, it is required that company produces items and refines through

adequate management so that system can be easily implemented (Keel, Savage, Rafiq and

Mazzocato, 2017). Moreover, it is required to identify those functional areas which will meet out

demands of production with much ease. Then after identifying these areas, it is now required to

5

This strategy will help Caltex Australia Pvt Ltd to effectively analyse the market and then

offering fuel site offer to lure customers and increase in spending of consumers in the best

possible manner.

5. Creating new solutions for customers in the market-

Providing new customer solutions as network of more than 900 retail sites are in the

market and weekly customers over three millions. Thus, building new and attractive offers for

potential consumers across multiple channels and locations and enhancing satisfaction level in

effectual way.

C) How ABC model assists in accomplishing firm's strategies

ABC model is quite effectively for Caltex Australia Pvt Ltd to maintain cost level and

attaining reduction of expenses to carry out various manufacturing activities quite effectually

(Etienne and et.al, 2017). It can be assessed from the company's strategies that supply chain costs

can be controlled and better trading could be possible. The costs of trading may be analysed in a

better manner. ABC model is helpful as organisation may be able to allocate cost of overheads

with much ease. Furthermore, company can accumulate cost of infrastructure so that direct

labour costs can be managed in the best possible way. Thus, ABC model will be helpful to

company in allocating costs on the activity basis.

C) Providing recommendations about implementation of ABC model

ABC model is useful for company as costs can be classified on activity basis. In relation

to this, it is required that Caltex Australia Pvt Ltd should implement such model so that benefits

may be extracted as it is engaged in the business of transport fuel supplier and provides delivery

of fuel through complex supply chains in effective way. It is recommended to implement ABC

model as it will provide way to organisation to initiate control upon expenditures. In order to

meet customer's satisfaction, it is required that company produces items and refines through

adequate management so that system can be easily implemented (Keel, Savage, Rafiq and

Mazzocato, 2017). Moreover, it is required to identify those functional areas which will meet out

demands of production with much ease. Then after identifying these areas, it is now required to

5

assign main activities that will be able to complete task quite effectually. It will be helpful for

company and as such, activities can be easily aligned in achieving production.

Another recommendation is that Caltex Australia Pvt Ltd should allocate indirect

expenses to functional areas. Then afterwards, suitable cost driver should be aligned under the

functional areas and as such, activities wise statement of costs should be prepared. Now

comparing the statement with value addition on activity wise basis. Lastly, to effectively identify

activities that can be eradicated from the processing and as such, better control can be initiated

on the overall activities of organisation. Thus, these two recommendations are provided to

organisation so that it can be easily implement ABC model of accounting and as a result, senior

management can take benefits out of the same for injecting overall productivity and decreasing

costs in effective way (Angelopoulos and Pollalis, 2017).

D) Management accounting tool suitable for company apart from ABC model

ABC model is effective tool in having clarity about the costs so that it can be controlled

in adequate manner. It can be said that management accounting tools are useful in carrying out

effective financial decision in the best possible way. Hence, ABC system is helpful for company.

However, another management tool such as budgetary control is beneficial for the firm in

carrying out business operations with much ease. Budgets are financial goal which is formulated

and prepared for the coming period in anticipation of expected income to be earned and

expenditures that would be incurred in the future. Thus, budgets are prepared in anticipation of

future activities of business.

Budgetary control is required so that planned performance of firm can be compared with

actual performance of company in the best possible way. When both of them are matched,

management can find out variations if any in actual performance and planned one. Deviations are

analysed and as such, improvement is required to be made so that variations can be removed up

to a high extent. Thus, company's management takes corrective actions in order to eradicate

deviations in effective way. Thus, improvement is initiated by the company and as a result,

variances are removed (MacBeath, 2017).

Moreover, it is called as budgetary control which is a helpful management accounting

tool as variances can be reduced and control can be initiated quite effectually. It will help Caltex

Australia Pvt Ltd to effectively met business operations in desired way. Moreover, it would be

6

company and as such, activities can be easily aligned in achieving production.

Another recommendation is that Caltex Australia Pvt Ltd should allocate indirect

expenses to functional areas. Then afterwards, suitable cost driver should be aligned under the

functional areas and as such, activities wise statement of costs should be prepared. Now

comparing the statement with value addition on activity wise basis. Lastly, to effectively identify

activities that can be eradicated from the processing and as such, better control can be initiated

on the overall activities of organisation. Thus, these two recommendations are provided to

organisation so that it can be easily implement ABC model of accounting and as a result, senior

management can take benefits out of the same for injecting overall productivity and decreasing

costs in effective way (Angelopoulos and Pollalis, 2017).

D) Management accounting tool suitable for company apart from ABC model

ABC model is effective tool in having clarity about the costs so that it can be controlled

in adequate manner. It can be said that management accounting tools are useful in carrying out

effective financial decision in the best possible way. Hence, ABC system is helpful for company.

However, another management tool such as budgetary control is beneficial for the firm in

carrying out business operations with much ease. Budgets are financial goal which is formulated

and prepared for the coming period in anticipation of expected income to be earned and

expenditures that would be incurred in the future. Thus, budgets are prepared in anticipation of

future activities of business.

Budgetary control is required so that planned performance of firm can be compared with

actual performance of company in the best possible way. When both of them are matched,

management can find out variations if any in actual performance and planned one. Deviations are

analysed and as such, improvement is required to be made so that variations can be removed up

to a high extent. Thus, company's management takes corrective actions in order to eradicate

deviations in effective way. Thus, improvement is initiated by the company and as a result,

variances are removed (MacBeath, 2017).

Moreover, it is called as budgetary control which is a helpful management accounting

tool as variances can be reduced and control can be initiated quite effectually. It will help Caltex

Australia Pvt Ltd to effectively met business operations in desired way. Moreover, it would be

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

able to inject its business and as such, trading and shipping will be streamlined in effectual way.

Thus, it can be said senior management and CEO of organisation will be benefited by

implementation budgetary control as a management accounting tool. It would be worthwhile for

the business in meeting out objectives quite effectively.

CONCLUSION

Hereby it can be concluded that there are various management accounting tools which are

beneficial for the management of organisation to implement the same and extract benefits out of

it. In relation to this, ABC model is one such tool helping organisation to assess costs in that way

which do not hamper production and overall productivity can be enhanced with much ease.

Moreover, allocating costs on behalf of activities is another essence of this model. Thus, Caltex

Australia Pvt Ltd may be able to extract benefits out of the same and costs can be controlled

quite effectually.

7

Thus, it can be said senior management and CEO of organisation will be benefited by

implementation budgetary control as a management accounting tool. It would be worthwhile for

the business in meeting out objectives quite effectively.

CONCLUSION

Hereby it can be concluded that there are various management accounting tools which are

beneficial for the management of organisation to implement the same and extract benefits out of

it. In relation to this, ABC model is one such tool helping organisation to assess costs in that way

which do not hamper production and overall productivity can be enhanced with much ease.

Moreover, allocating costs on behalf of activities is another essence of this model. Thus, Caltex

Australia Pvt Ltd may be able to extract benefits out of the same and costs can be controlled

quite effectually.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Angelopoulos, M. and Pollalis, Y., 2017. Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Costabile, G., Fera, M., Fruggiero, F., Lambiase, A. and Pham, D., 2017. Cost models of additive

manufacturing: A literature review. International Journal of Industrial Engineering

Computations. 8(2). pp.263-283.

Etienne, A. and et.al, 2017. Cost engineering for variation management during the product and

process development. International Journal on Interactive Design and Manufacturing

(IJIDeM).11(2). pp.289-300.

Hoozée, S. and Hansen, S., 2017. A comparison of activity-based costing and time-driven

activity-based costing. Journal of Management Accounting Research.

Keel, G., Savage, C., Rafiq, M. and Mazzocato, P., 2017. Time-driven activity-based costing in

health care: A systematic review of the literature. Health Policy. 121(7).pp.755-763.

MacBeath, J., 2017. A role for parents, students and teachers in school self-evaluation and

development planning. InMeasuring Quality: Education Indicators (pp. 100-121).

Routledge.

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost

Systems (pp. 1-5). Springer Gabler, Wiesbaden.

Zhuang, Z. Y. and Chang, S. C., 2017. Deciding product mix based on time-driven activity-based

costing by mixed integer programming. Journal of Intelligent Manufacturing. 28(4).

pp.959-974.

Online

Introduction to Activity Based Costing. 2018 [Online] Available Through:

<https://www.accountingcoach.com/activity-based-costing/explanation>

8

Books and Journals

Angelopoulos, M. and Pollalis, Y., 2017. Activity Based Costing (ABC) as a tool for Lean

Transformation: The Case of the Greek Power Public Corporation (PPC).

Costabile, G., Fera, M., Fruggiero, F., Lambiase, A. and Pham, D., 2017. Cost models of additive

manufacturing: A literature review. International Journal of Industrial Engineering

Computations. 8(2). pp.263-283.

Etienne, A. and et.al, 2017. Cost engineering for variation management during the product and

process development. International Journal on Interactive Design and Manufacturing

(IJIDeM).11(2). pp.289-300.

Hoozée, S. and Hansen, S., 2017. A comparison of activity-based costing and time-driven

activity-based costing. Journal of Management Accounting Research.

Keel, G., Savage, C., Rafiq, M. and Mazzocato, P., 2017. Time-driven activity-based costing in

health care: A systematic review of the literature. Health Policy. 121(7).pp.755-763.

MacBeath, J., 2017. A role for parents, students and teachers in school self-evaluation and

development planning. InMeasuring Quality: Education Indicators (pp. 100-121).

Routledge.

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost

Systems (pp. 1-5). Springer Gabler, Wiesbaden.

Zhuang, Z. Y. and Chang, S. C., 2017. Deciding product mix based on time-driven activity-based

costing by mixed integer programming. Journal of Intelligent Manufacturing. 28(4).

pp.959-974.

Online

Introduction to Activity Based Costing. 2018 [Online] Available Through:

<https://www.accountingcoach.com/activity-based-costing/explanation>

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.