Camberwell Services Ltd: Tax Effect Accounting Assignment Solution

VerifiedAdded on 2022/11/07

|36

|2520

|412

Homework Assignment

AI Summary

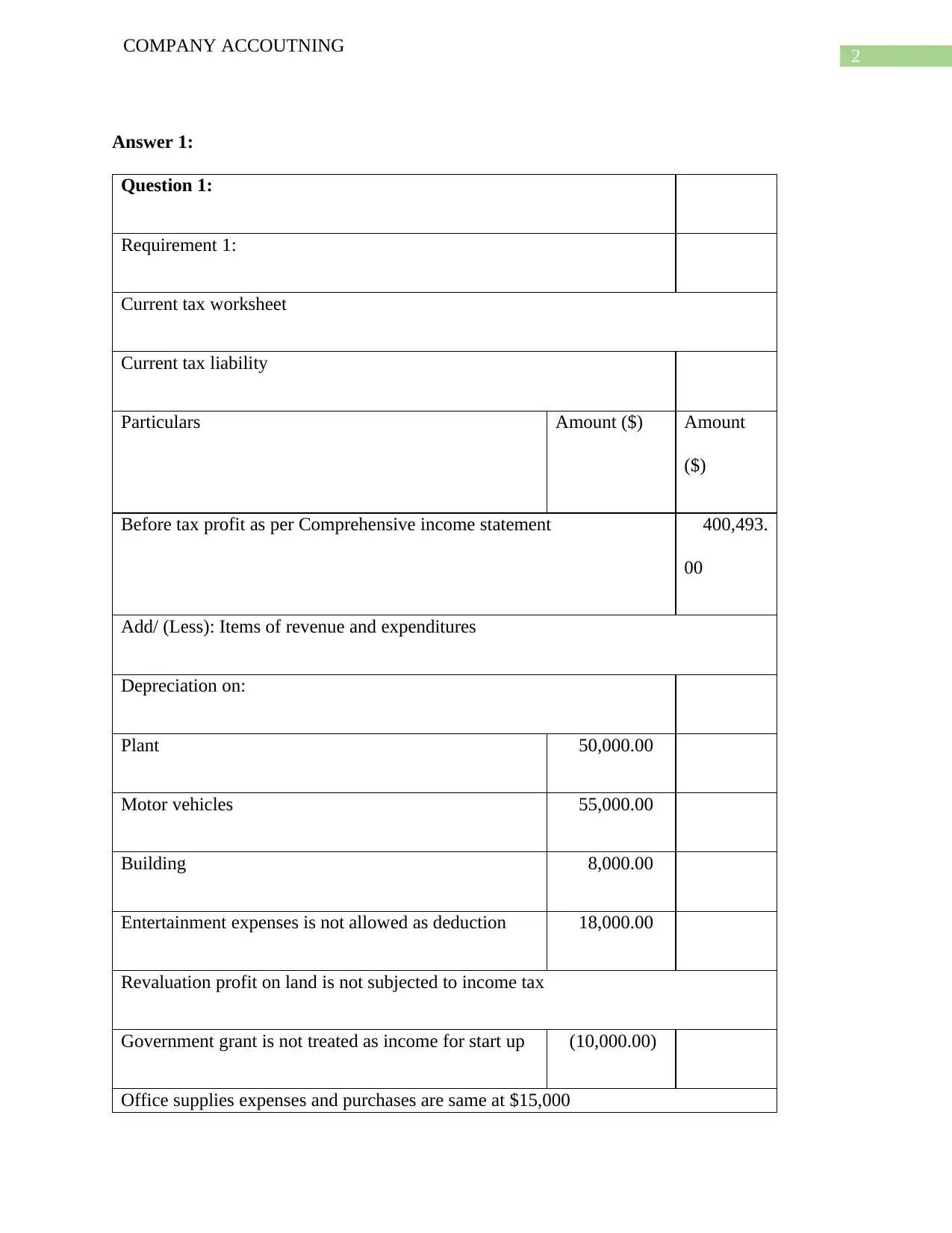

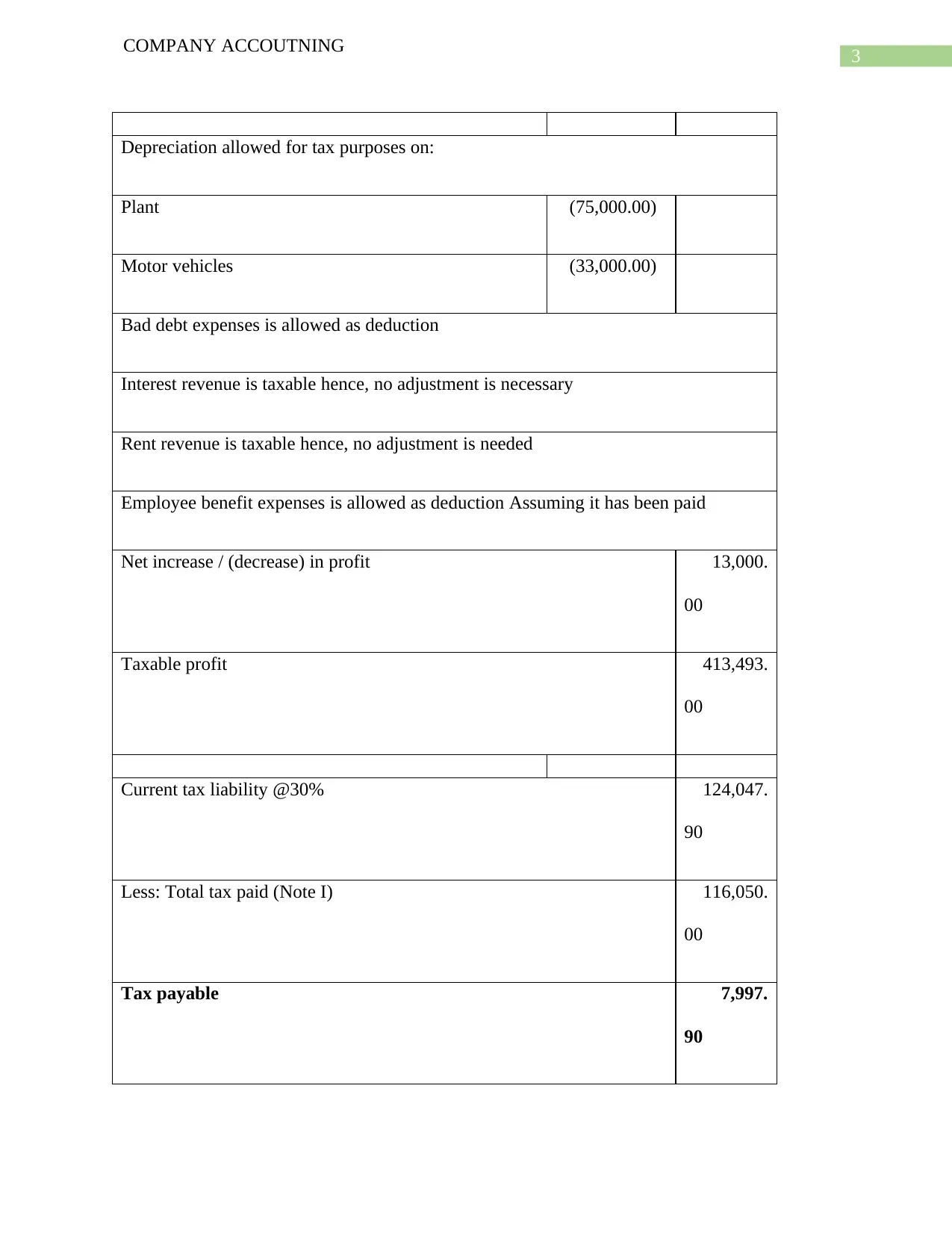

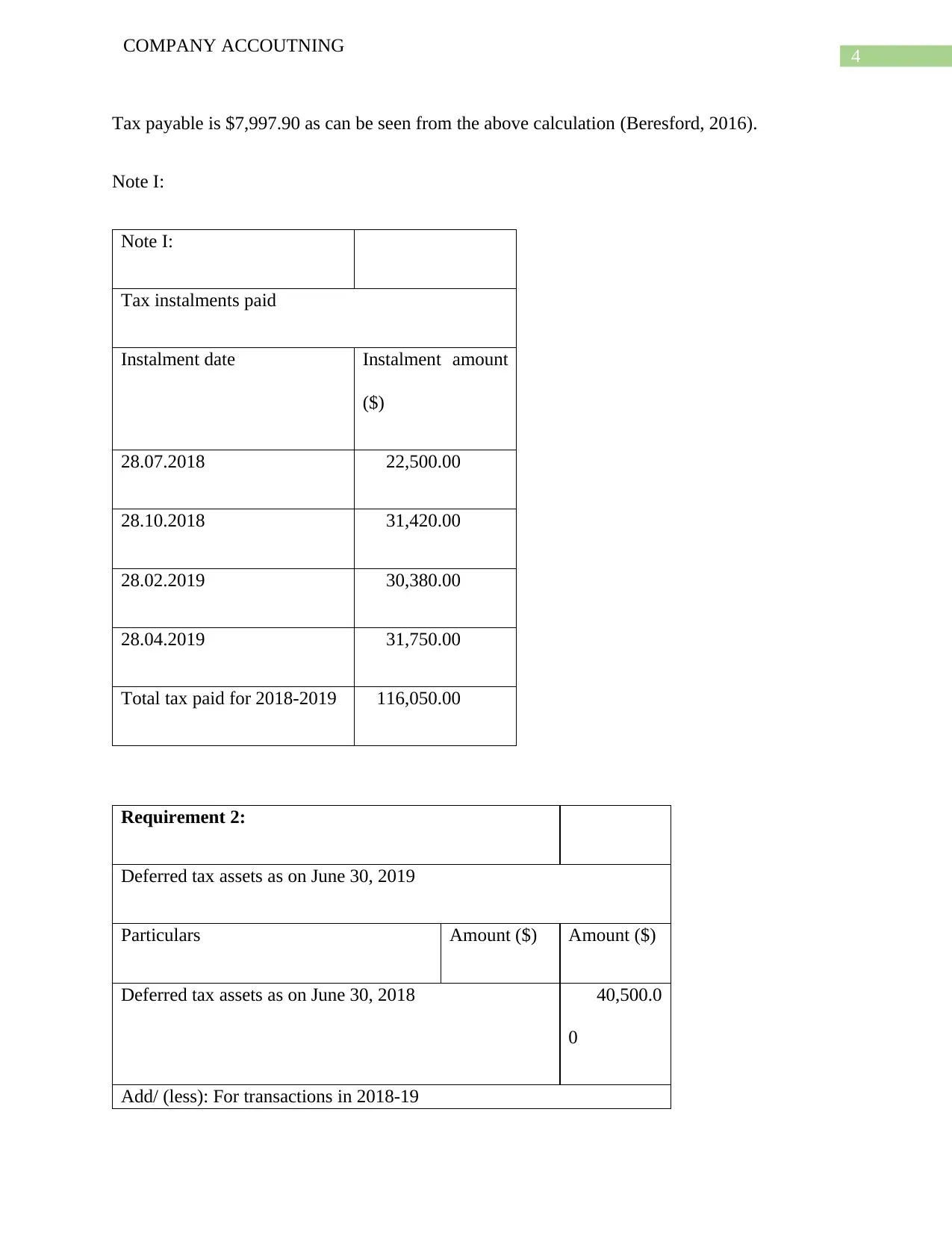

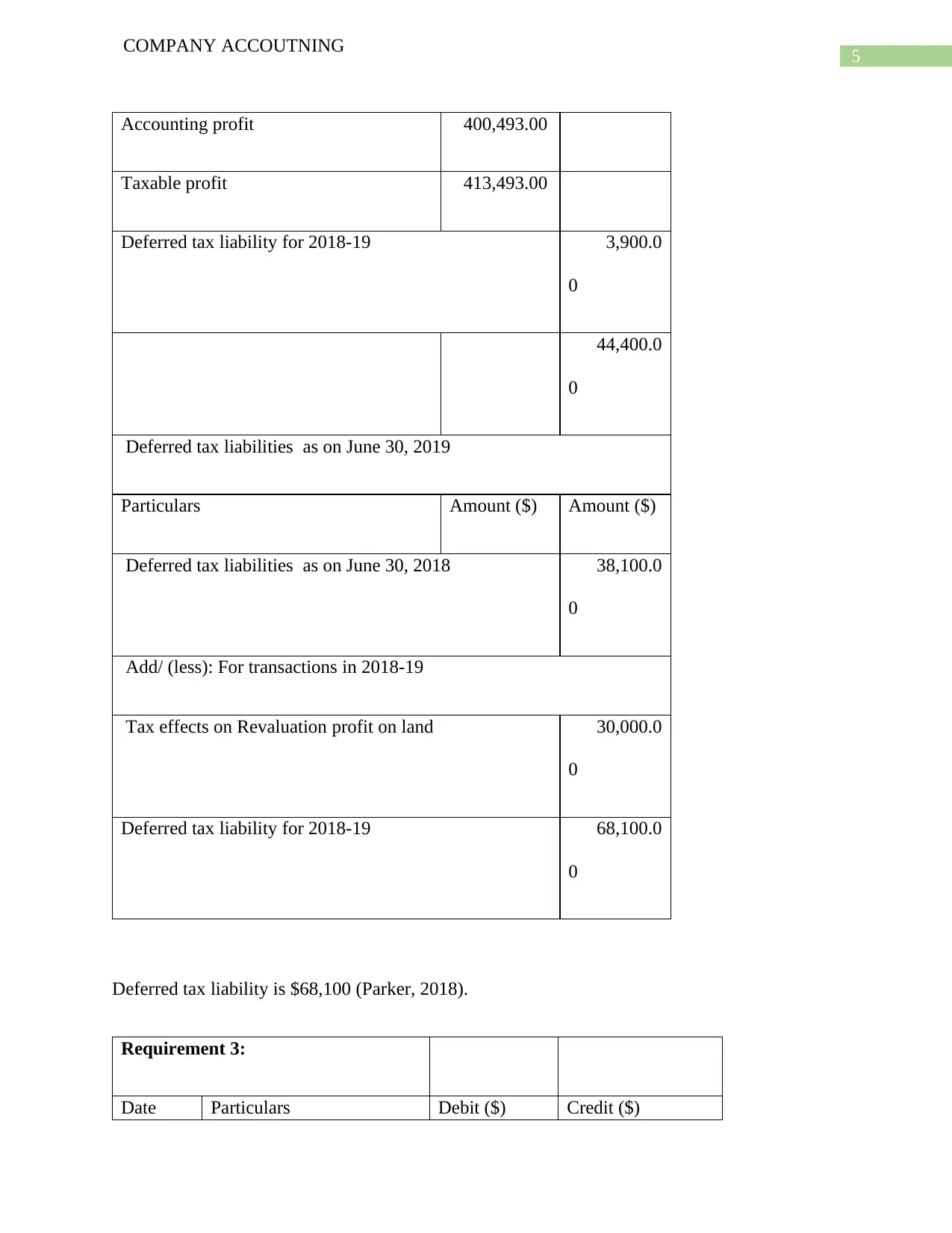

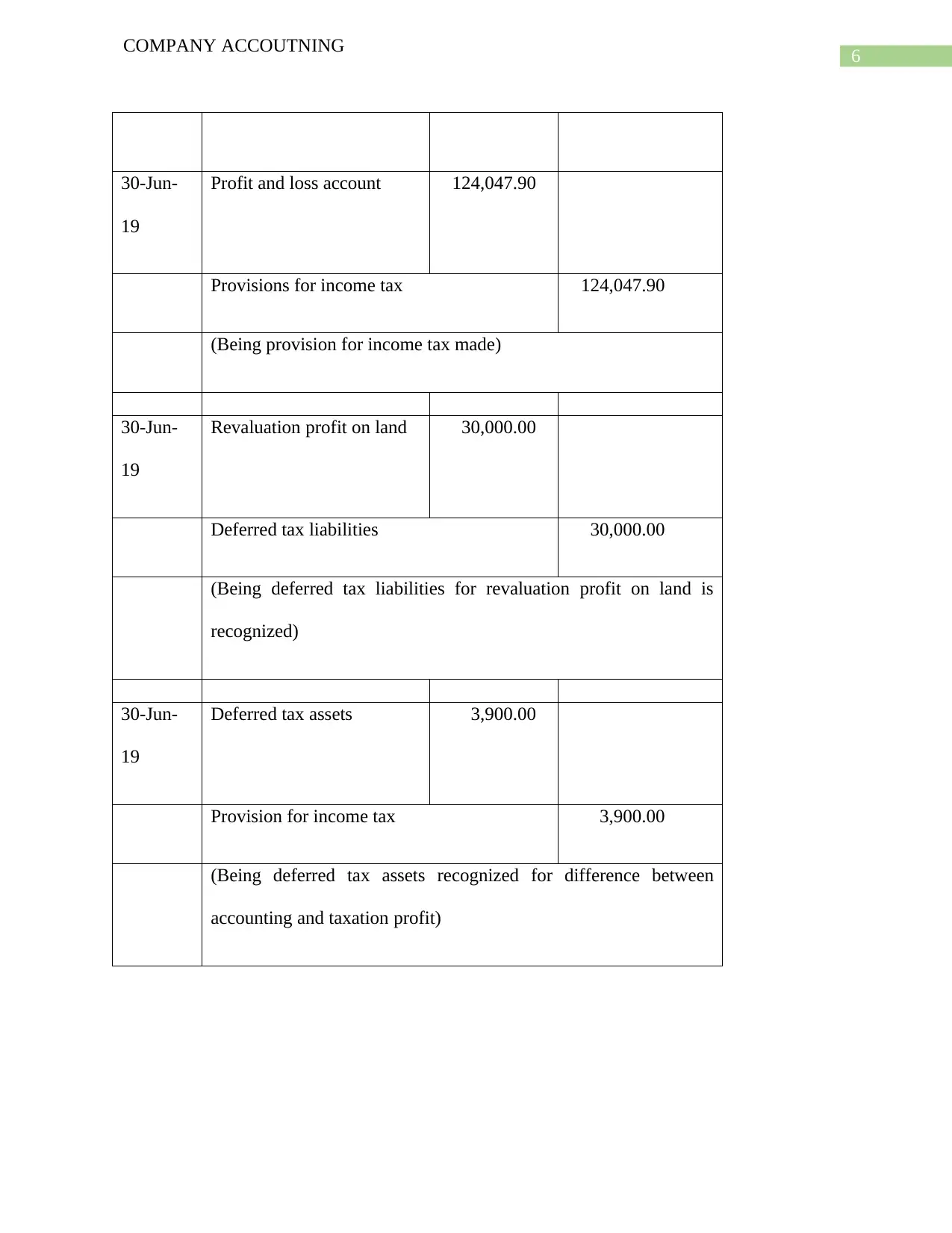

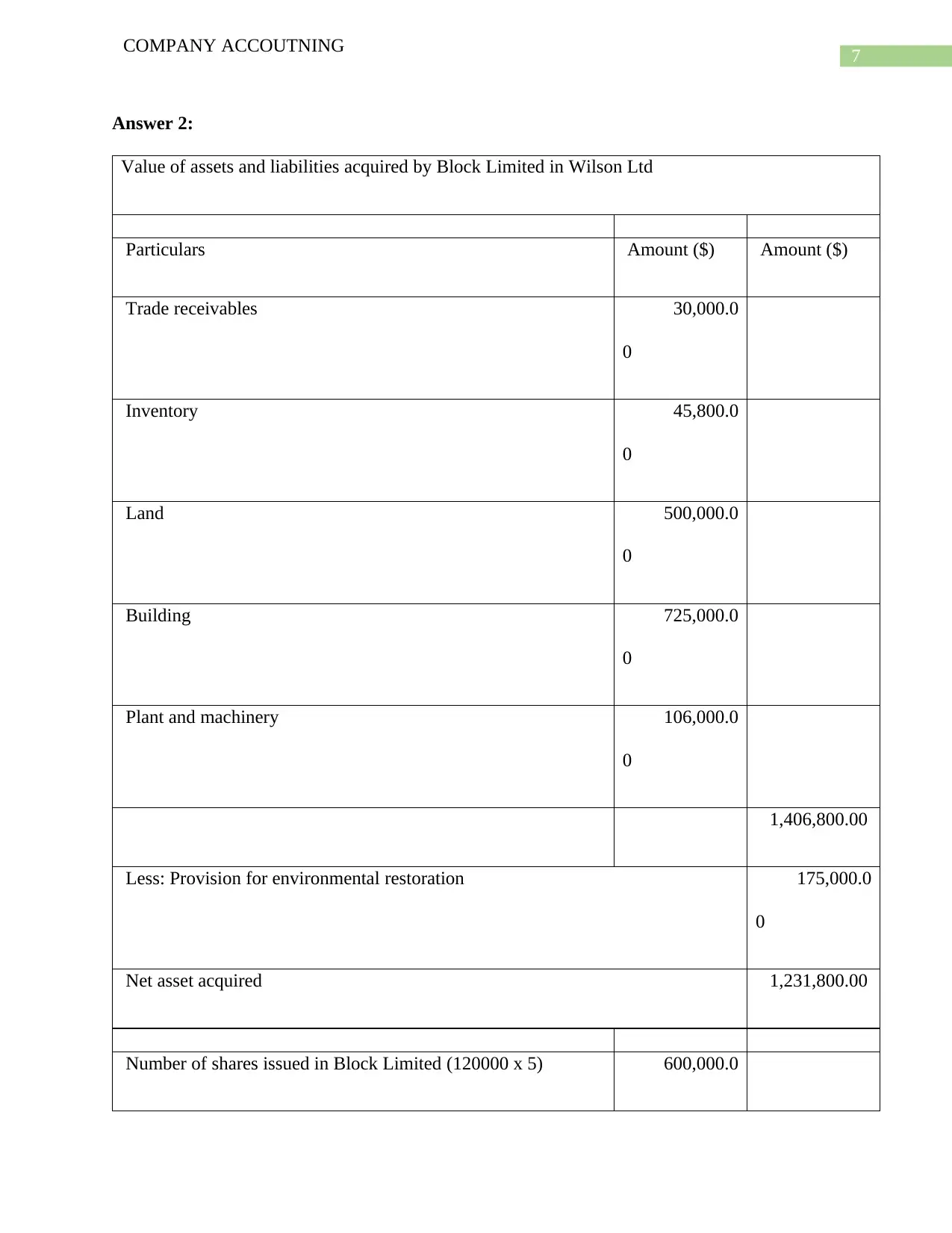

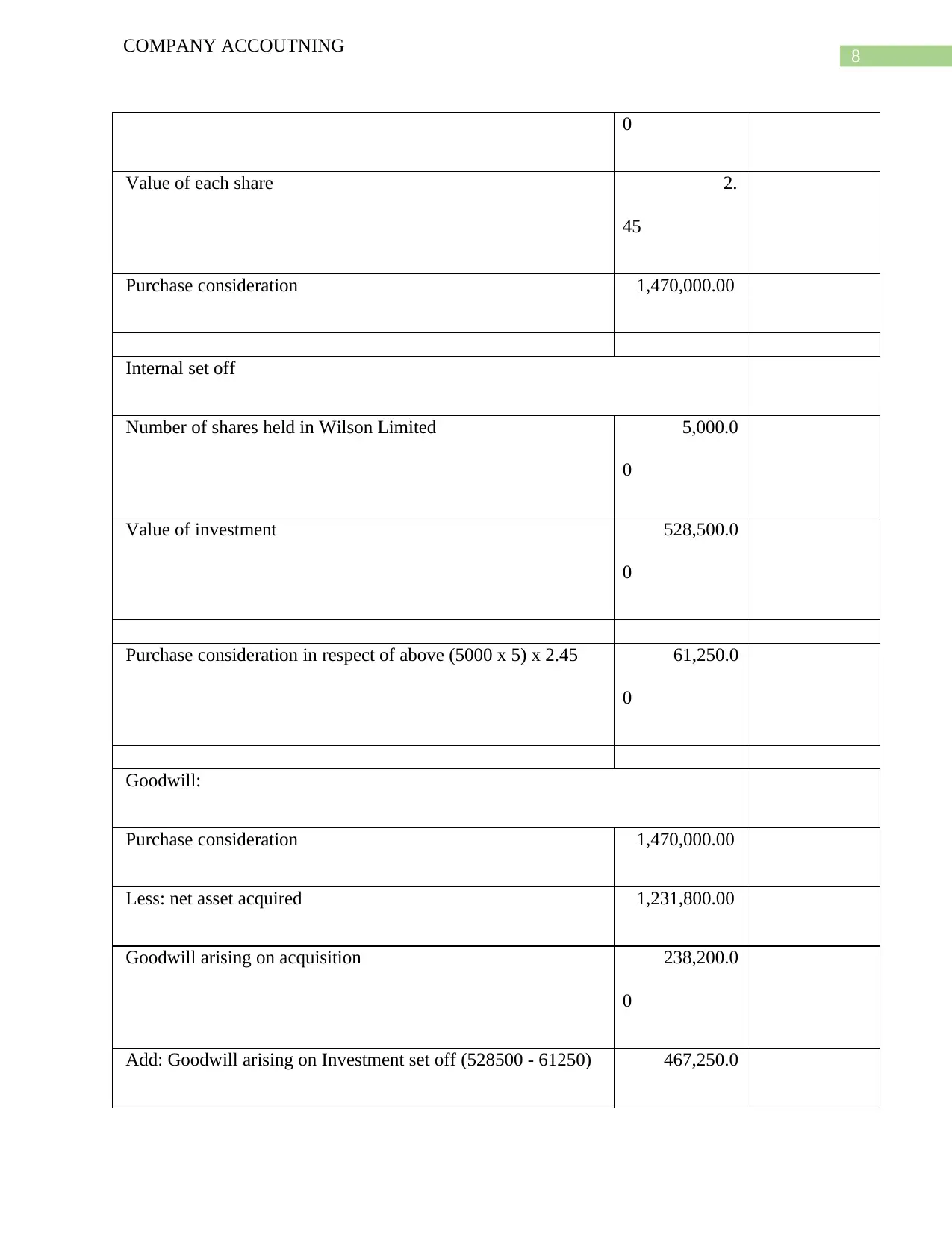

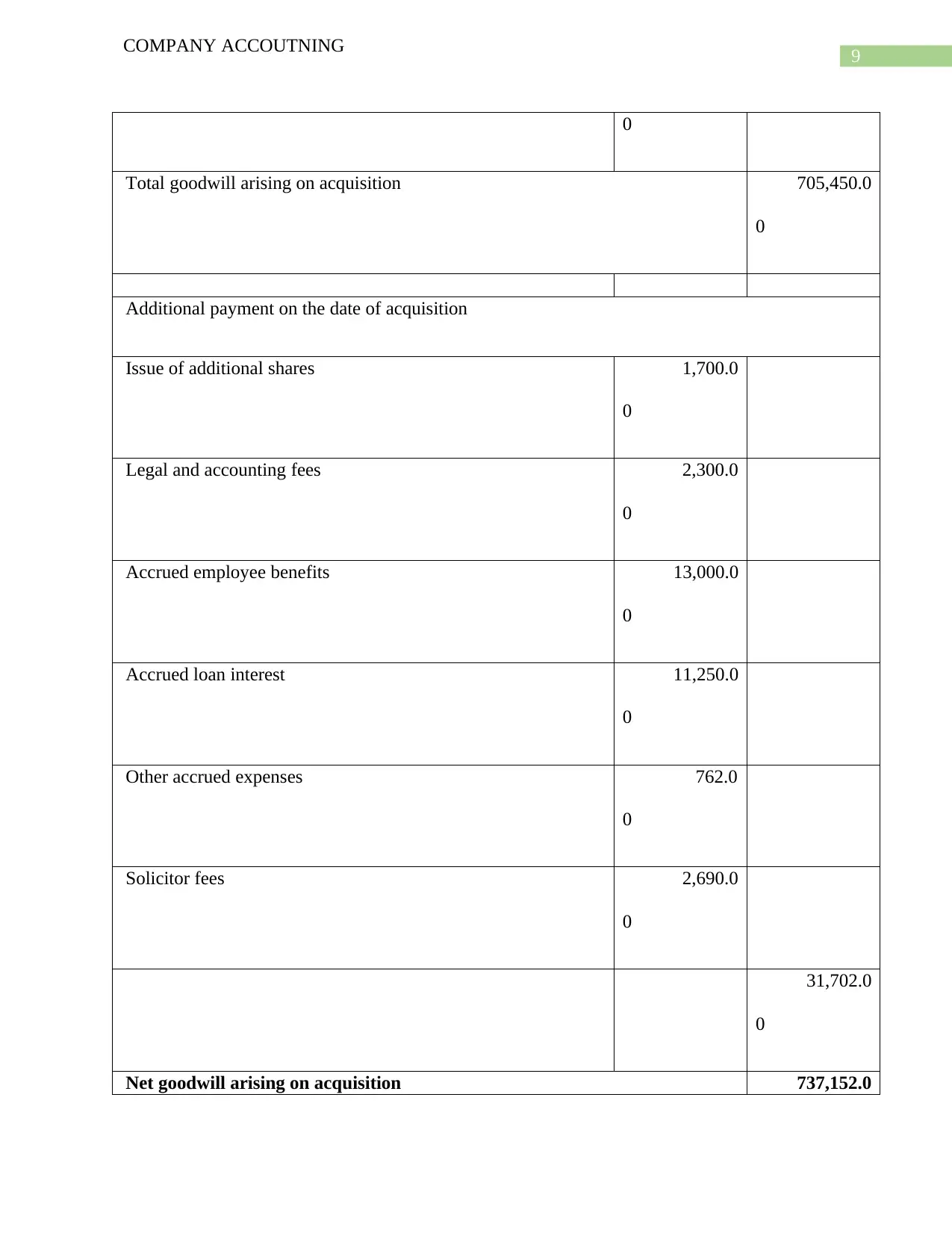

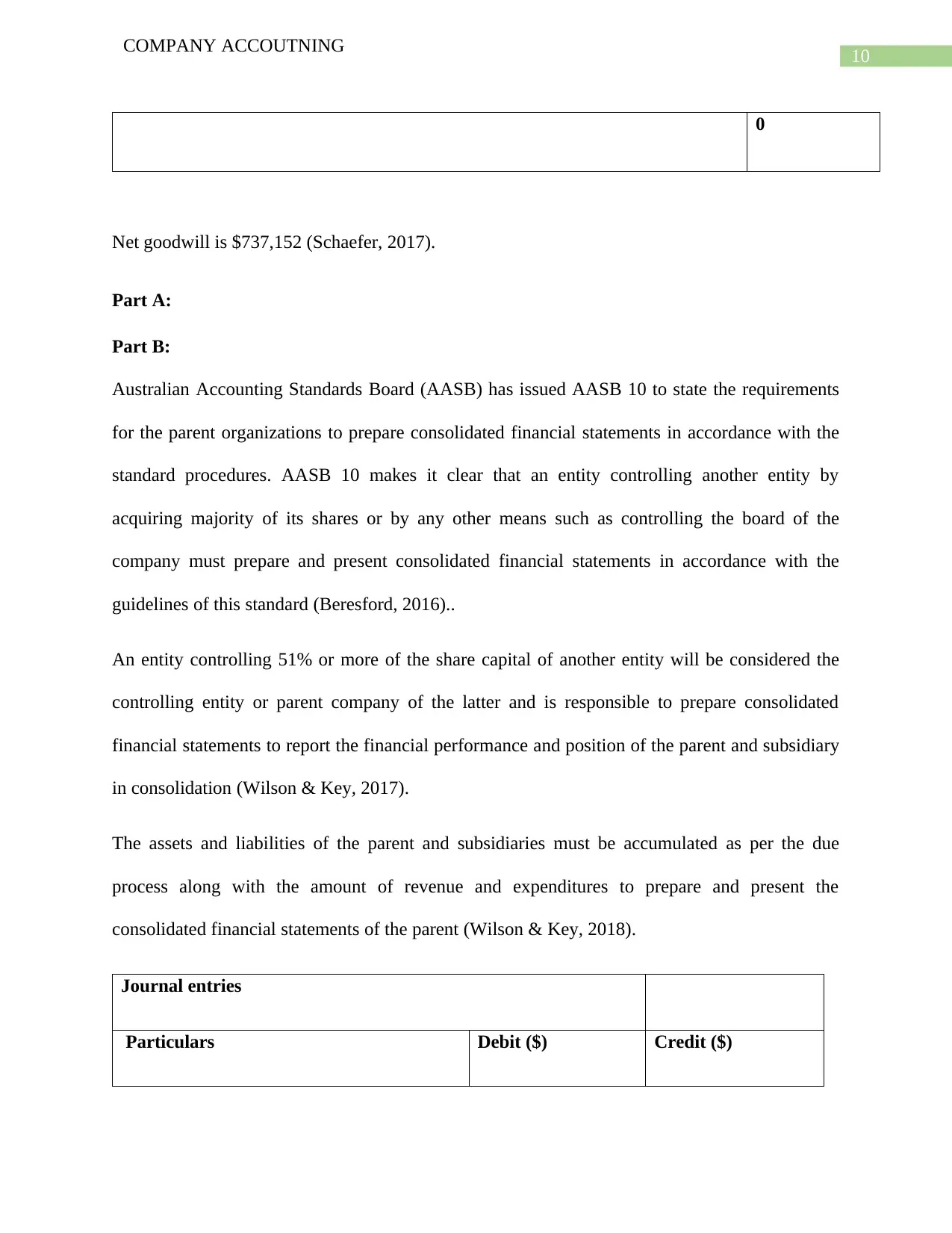

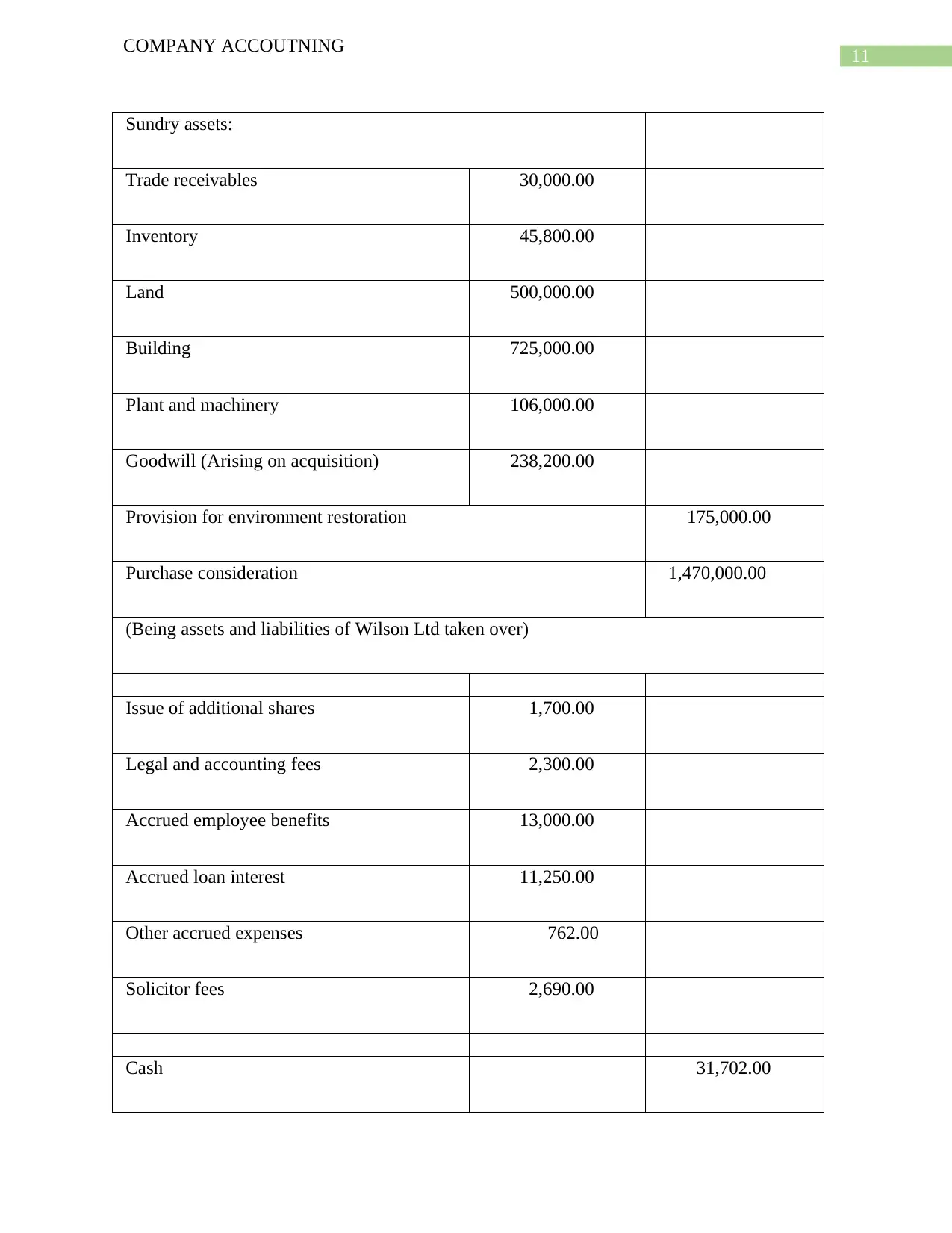

This document presents a comprehensive solution to a company accounting assignment centered on tax effect accounting. The assignment covers various aspects, including calculating the current tax liability, deferred tax assets and liabilities, and preparing relevant journal entries. The solution begins with a detailed current tax worksheet, adjusting the before-tax profit for items like depreciation, entertainment expenses, and government grants to arrive at the taxable profit and current tax liability. It then calculates deferred tax assets and liabilities, considering the differences between accounting and taxable profits, and the tax effects of revaluation gains. The document also provides the necessary journal entries to record the provisions for income tax, deferred tax liabilities, and deferred tax assets. The solution also includes the value of assets and liabilities acquired by Block Limited in Wilson Ltd, along with the purchase consideration and the calculation of goodwill. The document also explains the requirements for parent organizations to prepare consolidated financial statements in accordance with AASB 10, and provides journal entries for the acquisition of assets and liabilities of Wilson Ltd. Further, the document provides solutions for business combinations including calculation of gain on purchase, and consolidation entries. The solution includes detailed workings and calculations, ensuring a clear understanding of the concepts and their application in accounting practice. This assignment demonstrates a solid understanding of tax effect accounting, business combinations, and consolidation principles.

1 out of 36

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.