Management Accounting Report for Cambridge Manufacturing Ltd.

VerifiedAdded on 2021/02/19

|18

|5293

|25

Report

AI Summary

This report delves into the realm of management accounting, focusing on its application within a medium-sized financial consultancy, Marling. The report examines the role of management accounting in supporting business activities like planning, organizing, and controlling, using Cambridge Manufacturing Ltd. as a case study. It explores various management accounting systems, including price optimization, inventory management, cost accounting, and job costing. The report also analyzes different types of management accounting reports such as performance reports, budget reports, and cost managerial accounting reports. Furthermore, it contrasts marginal and absorption costing methods, providing income statements for Cambridge Manufacturing Ltd. The report highlights the benefits of these systems and their interrelation, offering insights into effective financial decision-making and cost management. This analysis aims to provide a comprehensive understanding of how management accounting contributes to organizational success.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION

Management accounting is the presentation of accounting information in order to

formulate the policies to be adopted by the management and assist its day to day activities. Good

management accounting consist of responsibilities to manage a broad variety of critical

management accounting information through management accounting system and techniques

like cash budget, absorption and marginal costing. It helps to management to conduct all

business activities in efficient manner such as planning, organising, staffing, directing and

controlling. To understand this, selected medium sized organisation Marling financial

consultancy company. It was established in 1988 and developed due to the trust instil in clients.

It serves clients operating in various sectors like retail, manufacturing and construction to

provide important information to making business decision. There are company provide

suggestions to manufacturing and retail company like Airdri limited, Cambridge manufacturing

and Argos, Waitrose. In this report selected client company Cambridge manufacturing Ltd. Here

in the project report apply several types of accounting system and prepare management

accounting reports. Apart from it, calculate net profit through absorption and marginal costing.

Along with, apply different planning tools and accounting tools to overcome from financial

issues.

TASK 1

P1

The management accounting system is an accounting system which is connected to the

collecting, analysing and presenting the monetary and non monetary information to the users as

per the requirement. It is considering as important part of the companies which is implement in

internal system to control business activities and execute in proper way. These systems can help

to keep proper records of accounts and make effective accounts (Arnaboldi, Lapsley and

Steccolini, 2015). There are discussed various types of management accounting system in order

to improve growth and market image. The Cambridge manufacturing Ltd use different types of

accounting system in their organisation -

Price optimization system – Every company wants to generate more profitability so they

can focus on their price structure of different products. The Cambridge manufacturing Ltd

applied particular system in order to set price of their products. There is company conduct

1

Management accounting is the presentation of accounting information in order to

formulate the policies to be adopted by the management and assist its day to day activities. Good

management accounting consist of responsibilities to manage a broad variety of critical

management accounting information through management accounting system and techniques

like cash budget, absorption and marginal costing. It helps to management to conduct all

business activities in efficient manner such as planning, organising, staffing, directing and

controlling. To understand this, selected medium sized organisation Marling financial

consultancy company. It was established in 1988 and developed due to the trust instil in clients.

It serves clients operating in various sectors like retail, manufacturing and construction to

provide important information to making business decision. There are company provide

suggestions to manufacturing and retail company like Airdri limited, Cambridge manufacturing

and Argos, Waitrose. In this report selected client company Cambridge manufacturing Ltd. Here

in the project report apply several types of accounting system and prepare management

accounting reports. Apart from it, calculate net profit through absorption and marginal costing.

Along with, apply different planning tools and accounting tools to overcome from financial

issues.

TASK 1

P1

The management accounting system is an accounting system which is connected to the

collecting, analysing and presenting the monetary and non monetary information to the users as

per the requirement. It is considering as important part of the companies which is implement in

internal system to control business activities and execute in proper way. These systems can help

to keep proper records of accounts and make effective accounts (Arnaboldi, Lapsley and

Steccolini, 2015). There are discussed various types of management accounting system in order

to improve growth and market image. The Cambridge manufacturing Ltd use different types of

accounting system in their organisation -

Price optimization system – Every company wants to generate more profitability so they

can focus on their price structure of different products. The Cambridge manufacturing Ltd

applied particular system in order to set price of their products. There is company conduct

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

market research and know perception of customers about the products as well as services. The

manager of the company apply the system in effective manner and help to maintain profits.

Inventory management system – The particular system major part of manufacturing

company to track record and manage stocks within organisation. Every manufacturing company

can be used this accounting system to keep proper records analysis of stock at each production

level. In Cambridge manufacturing Ltd apply particular system. It can assist every activities and

help to know requirement of material at different level. As a result it can reduce wastages and

help to place next order of goods and services. The company use different techniques of

inventory which is -

LIFO – According to this method stock which come last that goes out first so last in first

out.

FIFO – There are stock coming first and sale out first so it depends on first in first out.

AVOC – It is calculating cost of inventory on average basis.

Cost accounting system – This system provide direction to business to concentrate on

cost and increase the profitability. There are considering systematic set of activities like

understanding, entering, analysing, categorising and summarizing the cost of products and

services. In Cambridge manufacturing Ltd implement particular system to analysis variance

through compare between actual and budgeted cost. It is mainly used by business to improve

their production level and profitability (Cost accounting system, 2013).

Job costing system – The particular system is a kind of accounting system where

analysis the cost of expenditure of revenues which happen for particular job. Through this

system get detailed information about the cost which is connected to accounting period of time.

In Cambridge manufacturing Ltd apply particular system to know about several assign job. It can

provide different types of variable information in details -

Direct material – It is a part of variable cost which is related to production unit and track

the cost of materials during to specific job.

Direct labour– There are tracking the cost of labour regarding to specific job where

consist of time card and time sheet.

Overhead – At the end of every accounting period the total amount of each cost to apply

methodology regarding to allocation.

2

manager of the company apply the system in effective manner and help to maintain profits.

Inventory management system – The particular system major part of manufacturing

company to track record and manage stocks within organisation. Every manufacturing company

can be used this accounting system to keep proper records analysis of stock at each production

level. In Cambridge manufacturing Ltd apply particular system. It can assist every activities and

help to know requirement of material at different level. As a result it can reduce wastages and

help to place next order of goods and services. The company use different techniques of

inventory which is -

LIFO – According to this method stock which come last that goes out first so last in first

out.

FIFO – There are stock coming first and sale out first so it depends on first in first out.

AVOC – It is calculating cost of inventory on average basis.

Cost accounting system – This system provide direction to business to concentrate on

cost and increase the profitability. There are considering systematic set of activities like

understanding, entering, analysing, categorising and summarizing the cost of products and

services. In Cambridge manufacturing Ltd implement particular system to analysis variance

through compare between actual and budgeted cost. It is mainly used by business to improve

their production level and profitability (Cost accounting system, 2013).

Job costing system – The particular system is a kind of accounting system where

analysis the cost of expenditure of revenues which happen for particular job. Through this

system get detailed information about the cost which is connected to accounting period of time.

In Cambridge manufacturing Ltd apply particular system to know about several assign job. It can

provide different types of variable information in details -

Direct material – It is a part of variable cost which is related to production unit and track

the cost of materials during to specific job.

Direct labour– There are tracking the cost of labour regarding to specific job where

consist of time card and time sheet.

Overhead – At the end of every accounting period the total amount of each cost to apply

methodology regarding to allocation.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2.

Management accounting reporting consists of different types which should be considered

by KEF Ltd. In order to maintain records of every business transactions. It assist management to

make relevant decisions on the basis of information provided through such report that will bring

profitable outcome to company near future. These reporting systems are briefly discussed as

under:

Types of reports :

Performance report : These are the reports on the performance of something . Its is

prepared to measure, evaluate, analyse the performance of the organisations as well as

employees. Performance reports are created on the routine basis produced by the government

bodies and is financed by public money in regards to show that the money is spent effectively

and usefully (Chapman, 2011). It is also a part of communication management plans. Company

like Cambridge manufacturing Ltd. should make performance report on a routine basis to

identify the current performance, differences between actual and baselines, forecasting about

future, to know about the interest of stakeholder and to determine the work of employees.

Budget report : These reports are prepared to compare the actual with the estimated

budgets. All the financial data of the company is recorded in the budget reports. Budget reports

serves as a blueprint to the companies objectives . This also helps in determining the level of

expenditure in the organisation. Cambridge manufacturing Ltd. will make budget report to

ensure that the resource allocation is properly done , it will also help them in reducing the cost of

operations and helps in determining the availability of sufficient amount of funds .

Account receivable ageing reports : It is a critical tool for managing the business . This

reports shows the amount that a customer needs to pay a company and the length of time the

amount has been obscure. It also assist the Cambridge manufacturing Ltd. to know whether the

finance department is collecting receivables slowly , their credit policies etc.

Cost managerial accounting report : This report is prepared to know the cost of amount

spent on manufacturing the article . It provides full detail about the money invested in carrying

out business operations. Cambridge manufacturing Ltd. needs to prepared this to control the cost

which unnecessarily affects the profitability of the business and to understand the exact

expenditure of the organisations so that the optimization of resources can be done properly

(Fowzia, 2011).

3

Management accounting reporting consists of different types which should be considered

by KEF Ltd. In order to maintain records of every business transactions. It assist management to

make relevant decisions on the basis of information provided through such report that will bring

profitable outcome to company near future. These reporting systems are briefly discussed as

under:

Types of reports :

Performance report : These are the reports on the performance of something . Its is

prepared to measure, evaluate, analyse the performance of the organisations as well as

employees. Performance reports are created on the routine basis produced by the government

bodies and is financed by public money in regards to show that the money is spent effectively

and usefully (Chapman, 2011). It is also a part of communication management plans. Company

like Cambridge manufacturing Ltd. should make performance report on a routine basis to

identify the current performance, differences between actual and baselines, forecasting about

future, to know about the interest of stakeholder and to determine the work of employees.

Budget report : These reports are prepared to compare the actual with the estimated

budgets. All the financial data of the company is recorded in the budget reports. Budget reports

serves as a blueprint to the companies objectives . This also helps in determining the level of

expenditure in the organisation. Cambridge manufacturing Ltd. will make budget report to

ensure that the resource allocation is properly done , it will also help them in reducing the cost of

operations and helps in determining the availability of sufficient amount of funds .

Account receivable ageing reports : It is a critical tool for managing the business . This

reports shows the amount that a customer needs to pay a company and the length of time the

amount has been obscure. It also assist the Cambridge manufacturing Ltd. to know whether the

finance department is collecting receivables slowly , their credit policies etc.

Cost managerial accounting report : This report is prepared to know the cost of amount

spent on manufacturing the article . It provides full detail about the money invested in carrying

out business operations. Cambridge manufacturing Ltd. needs to prepared this to control the cost

which unnecessarily affects the profitability of the business and to understand the exact

expenditure of the organisations so that the optimization of resources can be done properly

(Fowzia, 2011).

3

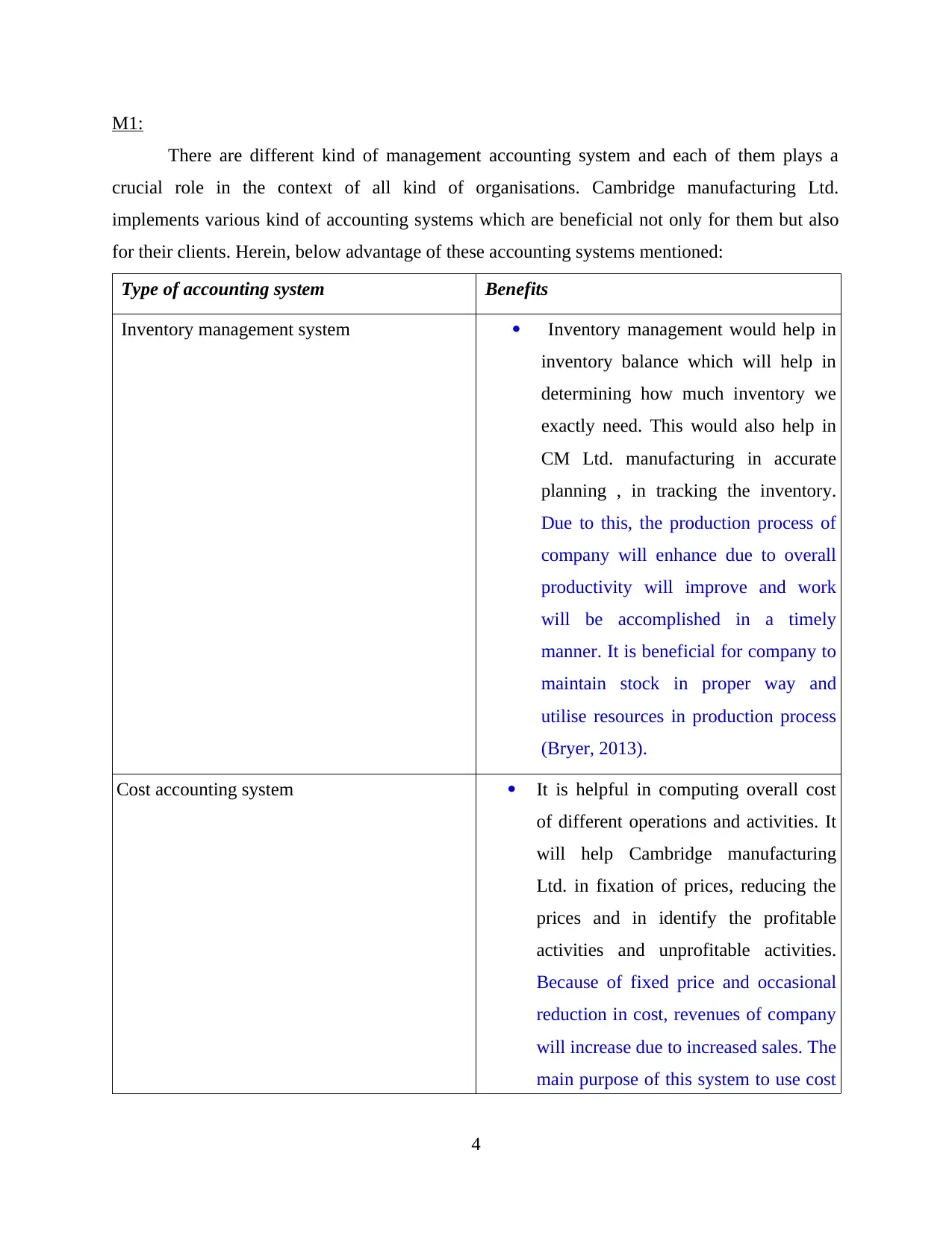

M1:

There are different kind of management accounting system and each of them plays a

crucial role in the context of all kind of organisations. Cambridge manufacturing Ltd.

implements various kind of accounting systems which are beneficial not only for them but also

for their clients. Herein, below advantage of these accounting systems mentioned:

Type of accounting system Benefits

Inventory management system Inventory management would help in

inventory balance which will help in

determining how much inventory we

exactly need. This would also help in

CM Ltd. manufacturing in accurate

planning , in tracking the inventory.

Due to this, the production process of

company will enhance due to overall

productivity will improve and work

will be accomplished in a timely

manner. It is beneficial for company to

maintain stock in proper way and

utilise resources in production process

(Bryer, 2013).

Cost accounting system It is helpful in computing overall cost

of different operations and activities. It

will help Cambridge manufacturing

Ltd. in fixation of prices, reducing the

prices and in identify the profitable

activities and unprofitable activities.

Because of fixed price and occasional

reduction in cost, revenues of company

will increase due to increased sales. The

main purpose of this system to use cost

4

There are different kind of management accounting system and each of them plays a

crucial role in the context of all kind of organisations. Cambridge manufacturing Ltd.

implements various kind of accounting systems which are beneficial not only for them but also

for their clients. Herein, below advantage of these accounting systems mentioned:

Type of accounting system Benefits

Inventory management system Inventory management would help in

inventory balance which will help in

determining how much inventory we

exactly need. This would also help in

CM Ltd. manufacturing in accurate

planning , in tracking the inventory.

Due to this, the production process of

company will enhance due to overall

productivity will improve and work

will be accomplished in a timely

manner. It is beneficial for company to

maintain stock in proper way and

utilise resources in production process

(Bryer, 2013).

Cost accounting system It is helpful in computing overall cost

of different operations and activities. It

will help Cambridge manufacturing

Ltd. in fixation of prices, reducing the

prices and in identify the profitable

activities and unprofitable activities.

Because of fixed price and occasional

reduction in cost, revenues of company

will increase due to increased sales. The

main purpose of this system to use cost

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in suitable manner and intensify the

cost efficiency to increase the

production.

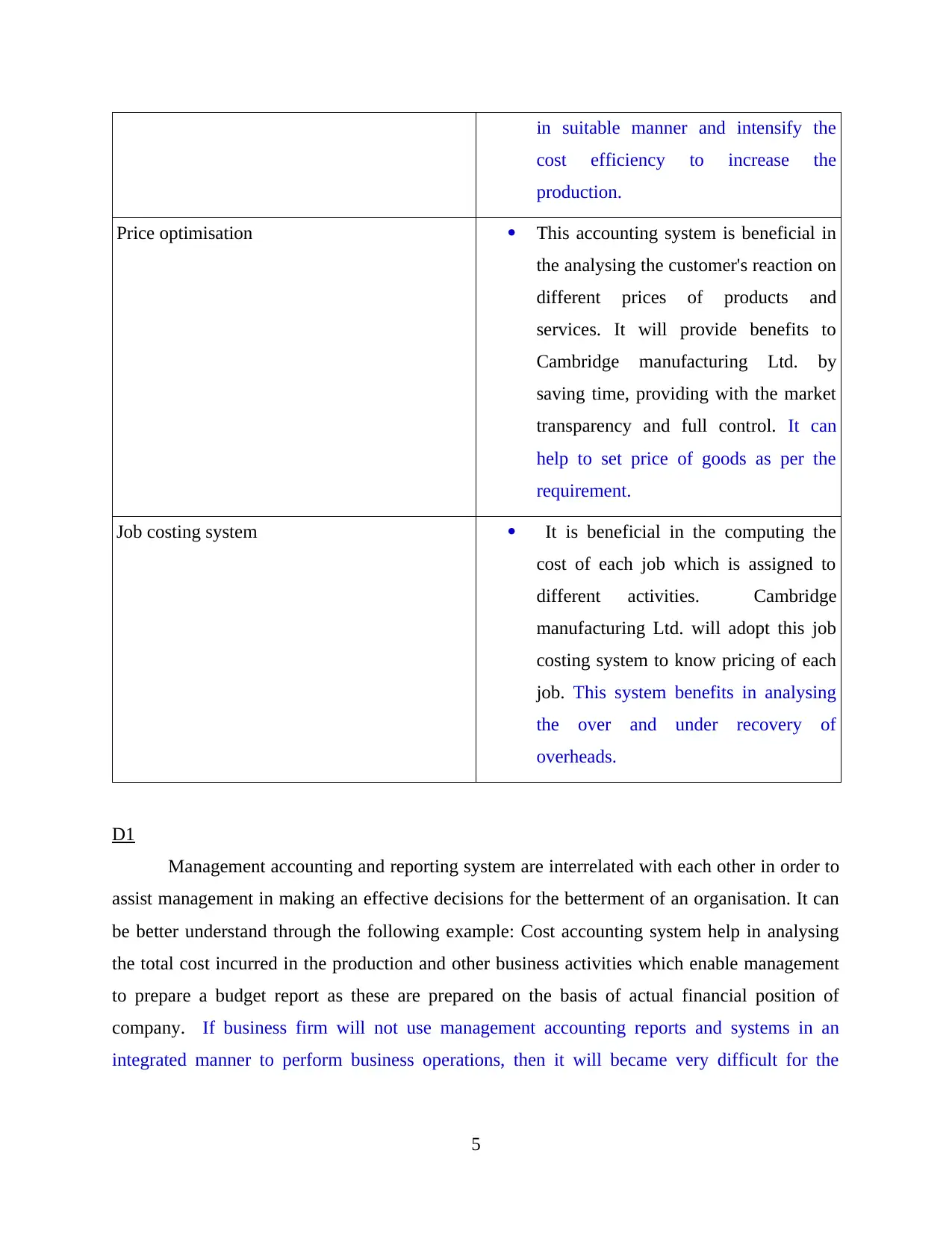

Price optimisation This accounting system is beneficial in

the analysing the customer's reaction on

different prices of products and

services. It will provide benefits to

Cambridge manufacturing Ltd. by

saving time, providing with the market

transparency and full control. It can

help to set price of goods as per the

requirement.

Job costing system It is beneficial in the computing the

cost of each job which is assigned to

different activities. Cambridge

manufacturing Ltd. will adopt this job

costing system to know pricing of each

job. This system benefits in analysing

the over and under recovery of

overheads.

D1

Management accounting and reporting system are interrelated with each other in order to

assist management in making an effective decisions for the betterment of an organisation. It can

be better understand through the following example: Cost accounting system help in analysing

the total cost incurred in the production and other business activities which enable management

to prepare a budget report as these are prepared on the basis of actual financial position of

company. If business firm will not use management accounting reports and systems in an

integrated manner to perform business operations, then it will became very difficult for the

5

cost efficiency to increase the

production.

Price optimisation This accounting system is beneficial in

the analysing the customer's reaction on

different prices of products and

services. It will provide benefits to

Cambridge manufacturing Ltd. by

saving time, providing with the market

transparency and full control. It can

help to set price of goods as per the

requirement.

Job costing system It is beneficial in the computing the

cost of each job which is assigned to

different activities. Cambridge

manufacturing Ltd. will adopt this job

costing system to know pricing of each

job. This system benefits in analysing

the over and under recovery of

overheads.

D1

Management accounting and reporting system are interrelated with each other in order to

assist management in making an effective decisions for the betterment of an organisation. It can

be better understand through the following example: Cost accounting system help in analysing

the total cost incurred in the production and other business activities which enable management

to prepare a budget report as these are prepared on the basis of actual financial position of

company. If business firm will not use management accounting reports and systems in an

integrated manner to perform business operations, then it will became very difficult for the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

concerned company to manage their income and financial statements in a proper manner. This

will reduce the overall effectiveness of company.

TASK 2.

P3.

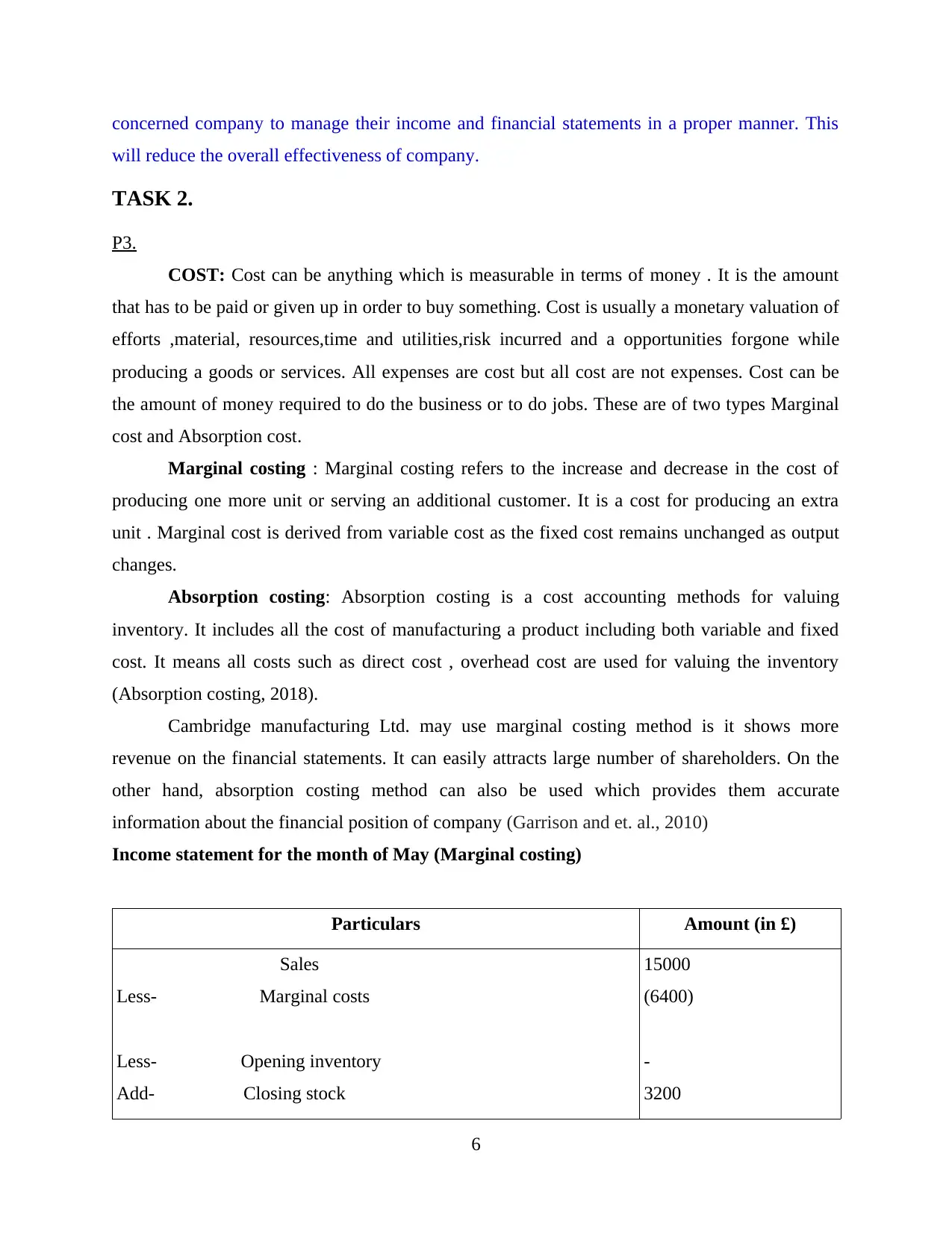

COST: Cost can be anything which is measurable in terms of money . It is the amount

that has to be paid or given up in order to buy something. Cost is usually a monetary valuation of

efforts ,material, resources,time and utilities,risk incurred and a opportunities forgone while

producing a goods or services. All expenses are cost but all cost are not expenses. Cost can be

the amount of money required to do the business or to do jobs. These are of two types Marginal

cost and Absorption cost.

Marginal costing : Marginal costing refers to the increase and decrease in the cost of

producing one more unit or serving an additional customer. It is a cost for producing an extra

unit . Marginal cost is derived from variable cost as the fixed cost remains unchanged as output

changes.

Absorption costing: Absorption costing is a cost accounting methods for valuing

inventory. It includes all the cost of manufacturing a product including both variable and fixed

cost. It means all costs such as direct cost , overhead cost are used for valuing the inventory

(Absorption costing, 2018).

Cambridge manufacturing Ltd. may use marginal costing method is it shows more

revenue on the financial statements. It can easily attracts large number of shareholders. On the

other hand, absorption costing method can also be used which provides them accurate

information about the financial position of company (Garrison and et. al., 2010)

Income statement for the month of May (Marginal costing)

Particulars Amount (in £)

Sales

Less- Marginal costs

Less- Opening inventory

Add- Closing stock

15000

(6400)

-

3200

6

will reduce the overall effectiveness of company.

TASK 2.

P3.

COST: Cost can be anything which is measurable in terms of money . It is the amount

that has to be paid or given up in order to buy something. Cost is usually a monetary valuation of

efforts ,material, resources,time and utilities,risk incurred and a opportunities forgone while

producing a goods or services. All expenses are cost but all cost are not expenses. Cost can be

the amount of money required to do the business or to do jobs. These are of two types Marginal

cost and Absorption cost.

Marginal costing : Marginal costing refers to the increase and decrease in the cost of

producing one more unit or serving an additional customer. It is a cost for producing an extra

unit . Marginal cost is derived from variable cost as the fixed cost remains unchanged as output

changes.

Absorption costing: Absorption costing is a cost accounting methods for valuing

inventory. It includes all the cost of manufacturing a product including both variable and fixed

cost. It means all costs such as direct cost , overhead cost are used for valuing the inventory

(Absorption costing, 2018).

Cambridge manufacturing Ltd. may use marginal costing method is it shows more

revenue on the financial statements. It can easily attracts large number of shareholders. On the

other hand, absorption costing method can also be used which provides them accurate

information about the financial position of company (Garrison and et. al., 2010)

Income statement for the month of May (Marginal costing)

Particulars Amount (in £)

Sales

Less- Marginal costs

Less- Opening inventory

Add- Closing stock

15000

(6400)

-

3200

6

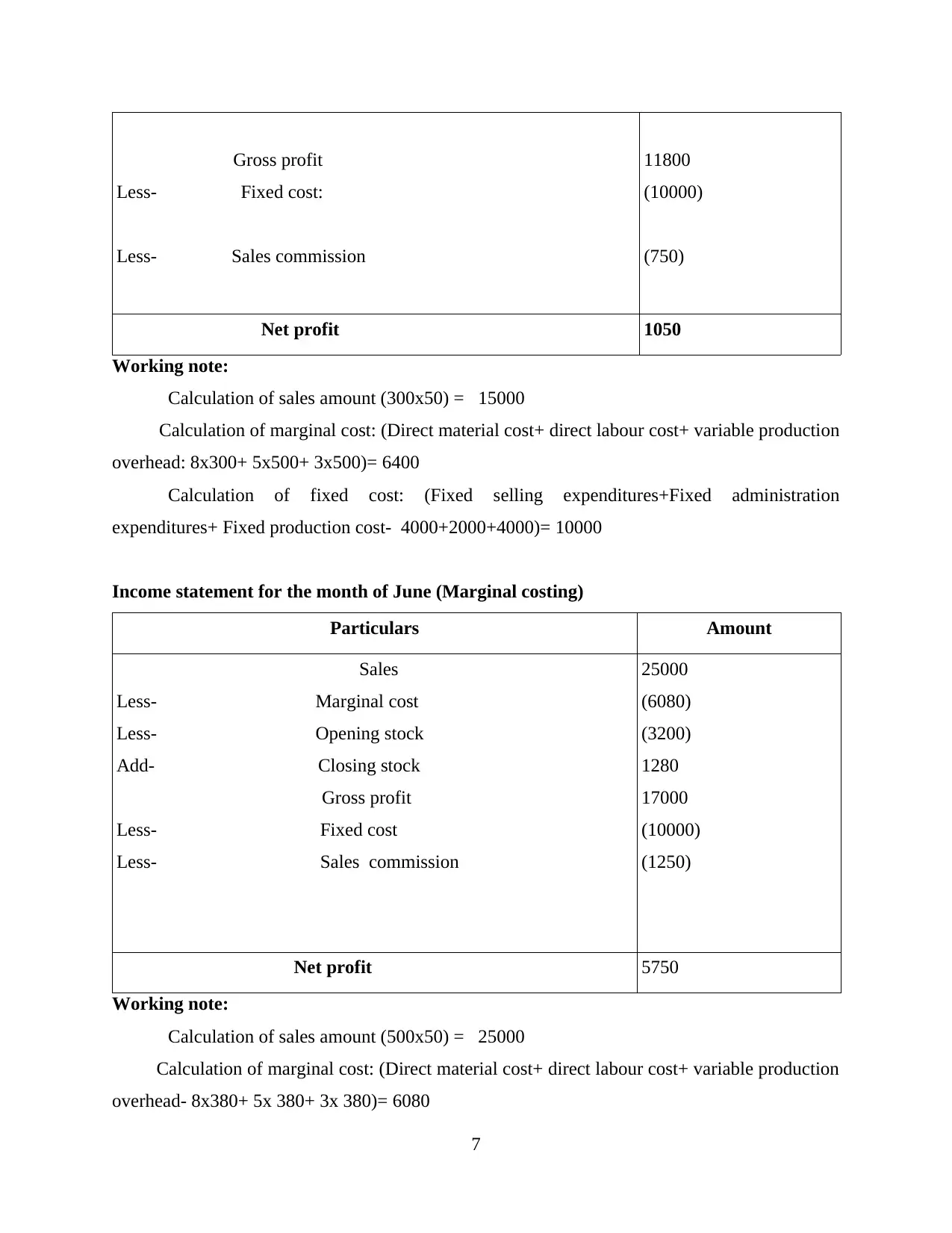

Gross profit

Less- Fixed cost:

Less- Sales commission

11800

(10000)

(750)

Net profit 1050

Working note:

Calculation of sales amount (300x50) = 15000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead: 8x300+ 5x500+ 3x500)= 6400

Calculation of fixed cost: (Fixed selling expenditures+Fixed administration

expenditures+ Fixed production cost- 4000+2000+4000)= 10000

Income statement for the month of June (Marginal costing)

Particulars Amount

Sales

Less- Marginal cost

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost

Less- Sales commission

25000

(6080)

(3200)

1280

17000

(10000)

(1250)

Net profit 5750

Working note:

Calculation of sales amount (500x50) = 25000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead- 8x380+ 5x 380+ 3x 380)= 6080

7

Less- Fixed cost:

Less- Sales commission

11800

(10000)

(750)

Net profit 1050

Working note:

Calculation of sales amount (300x50) = 15000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead: 8x300+ 5x500+ 3x500)= 6400

Calculation of fixed cost: (Fixed selling expenditures+Fixed administration

expenditures+ Fixed production cost- 4000+2000+4000)= 10000

Income statement for the month of June (Marginal costing)

Particulars Amount

Sales

Less- Marginal cost

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost

Less- Sales commission

25000

(6080)

(3200)

1280

17000

(10000)

(1250)

Net profit 5750

Working note:

Calculation of sales amount (500x50) = 25000

Calculation of marginal cost: (Direct material cost+ direct labour cost+ variable production

overhead- 8x380+ 5x 380+ 3x 380)= 6080

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

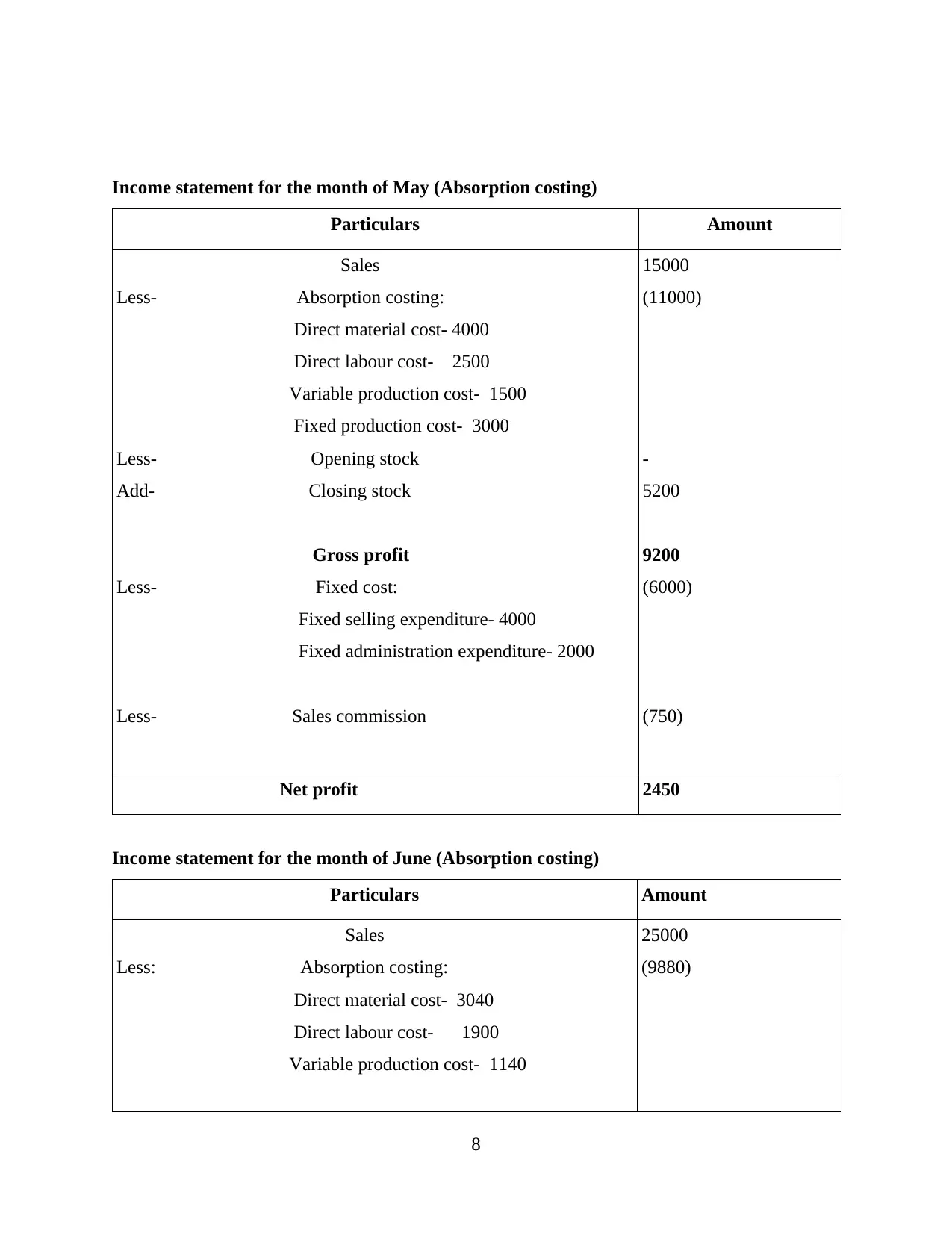

Income statement for the month of May (Absorption costing)

Particulars Amount

Sales

Less- Absorption costing:

Direct material cost- 4000

Direct labour cost- 2500

Variable production cost- 1500

Fixed production cost- 3000

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

Fixed administration expenditure- 2000

Less- Sales commission

15000

(11000)

-

5200

9200

(6000)

(750)

Net profit 2450

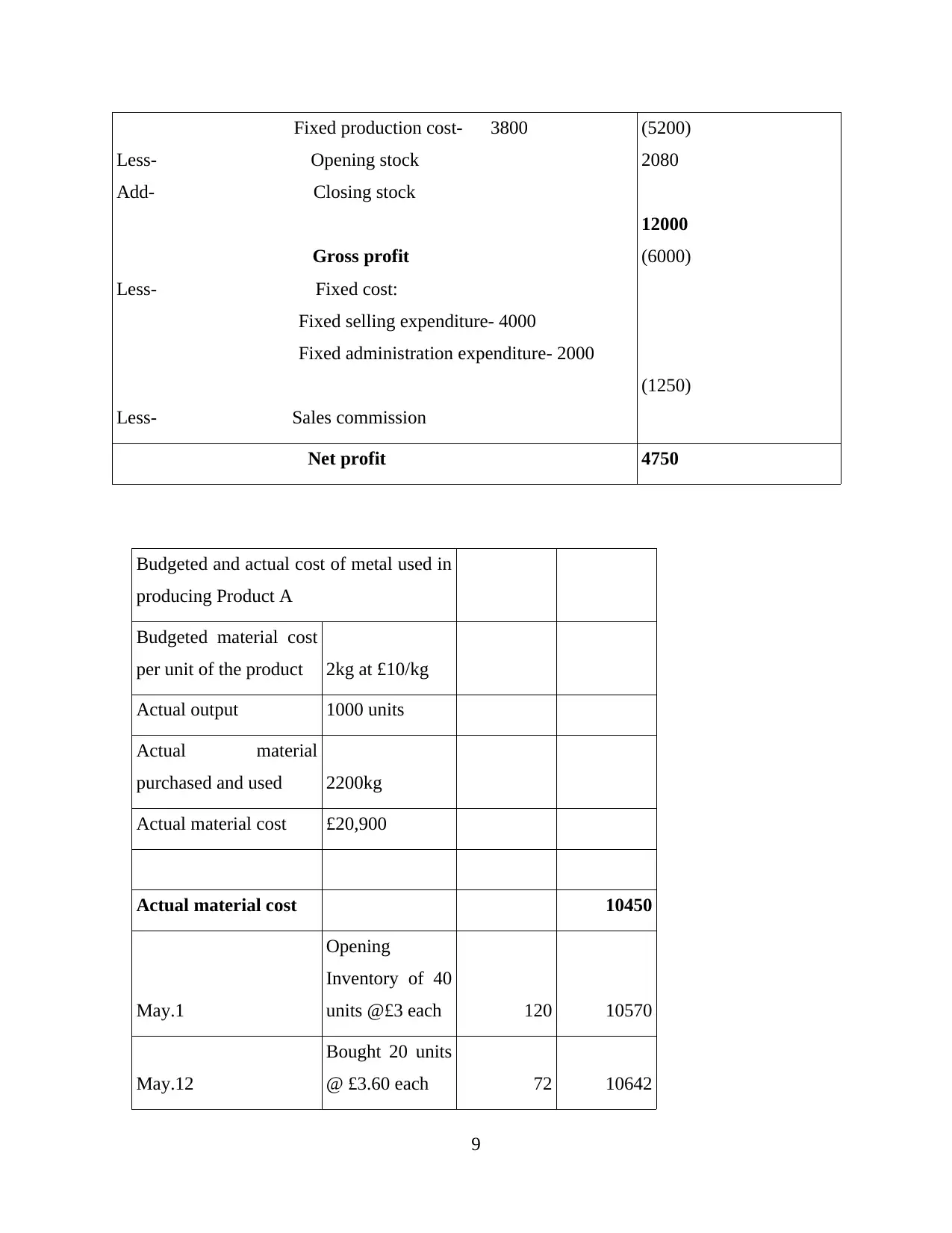

Income statement for the month of June (Absorption costing)

Particulars Amount

Sales

Less: Absorption costing:

Direct material cost- 3040

Direct labour cost- 1900

Variable production cost- 1140

25000

(9880)

8

Particulars Amount

Sales

Less- Absorption costing:

Direct material cost- 4000

Direct labour cost- 2500

Variable production cost- 1500

Fixed production cost- 3000

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

Fixed administration expenditure- 2000

Less- Sales commission

15000

(11000)

-

5200

9200

(6000)

(750)

Net profit 2450

Income statement for the month of June (Absorption costing)

Particulars Amount

Sales

Less: Absorption costing:

Direct material cost- 3040

Direct labour cost- 1900

Variable production cost- 1140

25000

(9880)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed production cost- 3800

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

Fixed administration expenditure- 2000

Less- Sales commission

(5200)

2080

12000

(6000)

(1250)

Net profit 4750

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost

per unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

Actual material cost 10450

May.1

Opening

Inventory of 40

units @£3 each 120 10570

May.12

Bought 20 units

@ £3.60 each 72 10642

9

Less- Opening stock

Add- Closing stock

Gross profit

Less- Fixed cost:

Fixed selling expenditure- 4000

Fixed administration expenditure- 2000

Less- Sales commission

(5200)

2080

12000

(6000)

(1250)

Net profit 4750

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost

per unit of the product 2kg at £10/kg

Actual output 1000 units

Actual material

purchased and used 2200kg

Actual material cost £20,900

Actual material cost 10450

May.1

Opening

Inventory of 40

units @£3 each 120 10570

May.12

Bought 20 units

@ £3.60 each 72 10642

9

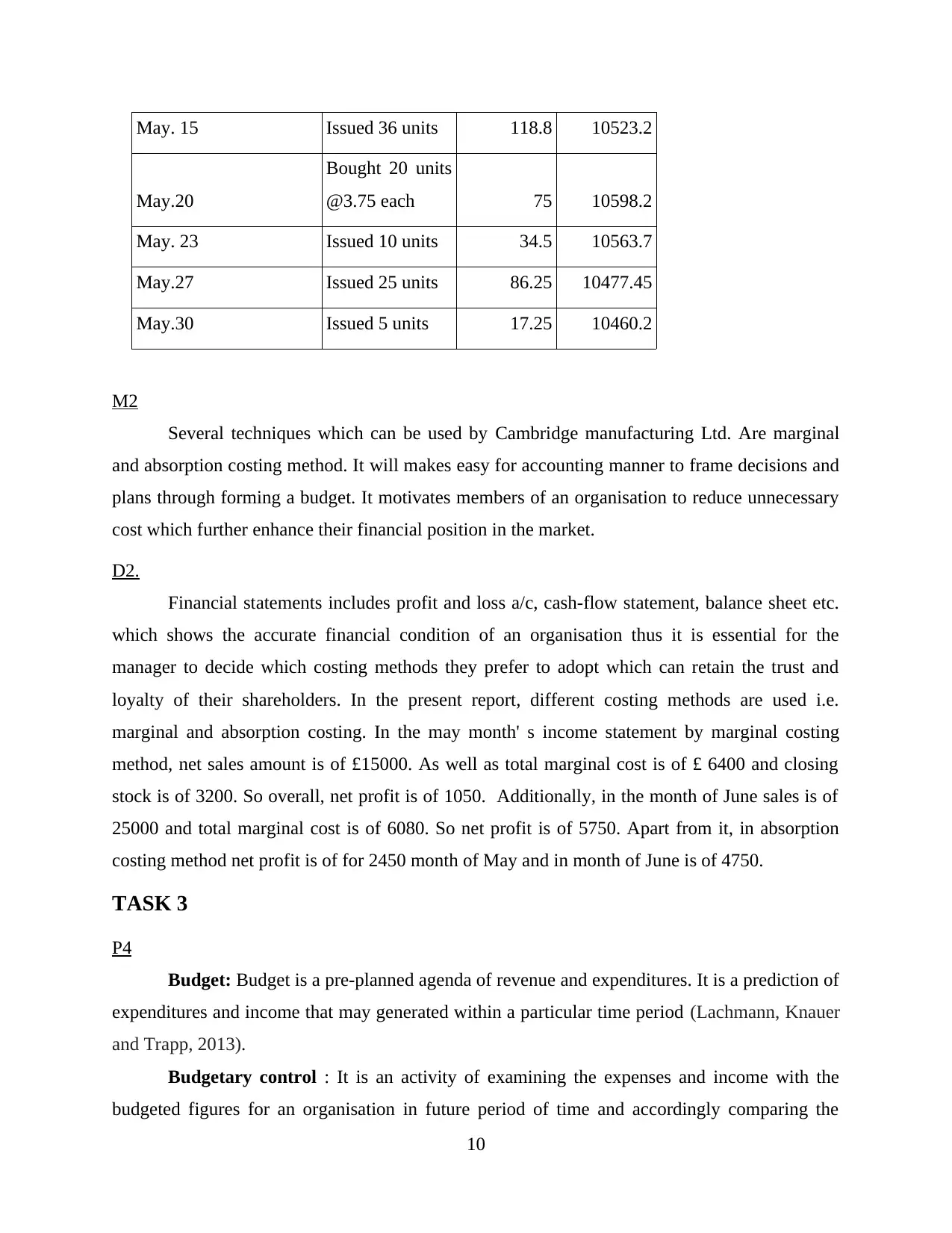

May. 15 Issued 36 units 118.8 10523.2

May.20

Bought 20 units

@3.75 each 75 10598.2

May. 23 Issued 10 units 34.5 10563.7

May.27 Issued 25 units 86.25 10477.45

May.30 Issued 5 units 17.25 10460.2

M2

Several techniques which can be used by Cambridge manufacturing Ltd. Are marginal

and absorption costing method. It will makes easy for accounting manner to frame decisions and

plans through forming a budget. It motivates members of an organisation to reduce unnecessary

cost which further enhance their financial position in the market.

D2.

Financial statements includes profit and loss a/c, cash-flow statement, balance sheet etc.

which shows the accurate financial condition of an organisation thus it is essential for the

manager to decide which costing methods they prefer to adopt which can retain the trust and

loyalty of their shareholders. In the present report, different costing methods are used i.e.

marginal and absorption costing. In the may month' s income statement by marginal costing

method, net sales amount is of £15000. As well as total marginal cost is of £ 6400 and closing

stock is of 3200. So overall, net profit is of 1050. Additionally, in the month of June sales is of

25000 and total marginal cost is of 6080. So net profit is of 5750. Apart from it, in absorption

costing method net profit is of for 2450 month of May and in month of June is of 4750.

TASK 3

P4

Budget: Budget is a pre-planned agenda of revenue and expenditures. It is a prediction of

expenditures and income that may generated within a particular time period (Lachmann, Knauer

and Trapp, 2013).

Budgetary control : It is an activity of examining the expenses and income with the

budgeted figures for an organisation in future period of time and accordingly comparing the

10

May.20

Bought 20 units

@3.75 each 75 10598.2

May. 23 Issued 10 units 34.5 10563.7

May.27 Issued 25 units 86.25 10477.45

May.30 Issued 5 units 17.25 10460.2

M2

Several techniques which can be used by Cambridge manufacturing Ltd. Are marginal

and absorption costing method. It will makes easy for accounting manner to frame decisions and

plans through forming a budget. It motivates members of an organisation to reduce unnecessary

cost which further enhance their financial position in the market.

D2.

Financial statements includes profit and loss a/c, cash-flow statement, balance sheet etc.

which shows the accurate financial condition of an organisation thus it is essential for the

manager to decide which costing methods they prefer to adopt which can retain the trust and

loyalty of their shareholders. In the present report, different costing methods are used i.e.

marginal and absorption costing. In the may month' s income statement by marginal costing

method, net sales amount is of £15000. As well as total marginal cost is of £ 6400 and closing

stock is of 3200. So overall, net profit is of 1050. Additionally, in the month of June sales is of

25000 and total marginal cost is of 6080. So net profit is of 5750. Apart from it, in absorption

costing method net profit is of for 2450 month of May and in month of June is of 4750.

TASK 3

P4

Budget: Budget is a pre-planned agenda of revenue and expenditures. It is a prediction of

expenditures and income that may generated within a particular time period (Lachmann, Knauer

and Trapp, 2013).

Budgetary control : It is an activity of examining the expenses and income with the

budgeted figures for an organisation in future period of time and accordingly comparing the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.