Federal Income Tax Analysis of Estate Freeze for Ann Stanley in Canada

VerifiedAdded on 2023/06/10

|10

|3016

|97

Case Study

AI Summary

This case study provides a detailed analysis of the federal income tax consequences associated with an estate freeze for Ann Stanley, a 65-year-old Canadian resident. The analysis covers various aspects, including capital gains implications, deemed dividends, and income sprinkling rules, while referencing relevant sections of the Income Tax Act. It also explores scenarios involving the transfer of shares to family members and the use of holding companies. The document includes calculations of potential tax liabilities and suggests improvements for minimizing tax burdens. Furthermore, the case study extends to providing tax advice to Ronaldo, considering capital gain investments, and Mr. Batista, regarding electronic tax filing. The document concludes with the importance of understanding and adhering to Canadian taxation laws for effective tax planning. Desklib provides a platform for students to access similar solved assignments and past papers.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To: Ann

From: CPA

Date: 11/08/2018

Subject: Explanation of the federal income tax consequences

Explanation to Ann

The Canadian income tax rules and the regulations are surrounding the Income Tax Act 1985

(c.1) Div A. It is illustrating that the income is depicted to be taxable if the individuals are

acquiring the taxable income with belonging to the resident of Canada. The tax payable by

the non-residents is depicted to be including that employment of the individual in Canada,

carrying out business in Canada and disposed to the taxable Canadian property. It is

illustrating that at the time of the year-end in Canada, the income tax must be paid as per the

taxable income earned (Canada Agency, 2018). The taxable income rules and the regulations

are depicted to be illustrated in the Div D of the norms and the regulations. As per the basic

taxation rules, the total amount of each of which the taxpayer's income is identified from the

source, the generation of the taxation process is depicted to be dependent on the taxpayer's

income for each year. Apart from this, the taxable income is depicted to be dependent on the

depositions which are listed as personal properties, plants, and the equipment. The taxpayer is

depicted to be allowing the capital losses for the years deposition and also it is determined

that the deduction will be made on the taxpayer's income. The total deductions are made on

the basis of determining the total referred values mentioned in the “Paragraph a” of the

Income Tax Act 1985 (Canada Agency, 2018). A taxpayer’s income or loss for the taxation

year is depicted to be computed according to the Act and also the exemptions will be made

on the basis of the losses incurred by the taxpayer in the financial year. As per the subsection

4(3) of the Act, it is indicating the acceptance of the deductions on the taxes implemented on

the taxpayer depending on the losses.

According to the Canadian Taxation laws on the share, the tax treatment is incorporated on

the basis of the purchasing of the shares carried out by the corporation. The adjustment of the

cost base amount is depicted to be paid for the shares and also the commission must be paid

with determining the capital gain losses. The changes in the sales are depicted to be

determining the capital gain taxes, as well as the taxes, are depicted to be incorporated on the

basis of the income made (Canada Agency, 2018). The 50% of the capital gain taxes are

1

From: CPA

Date: 11/08/2018

Subject: Explanation of the federal income tax consequences

Explanation to Ann

The Canadian income tax rules and the regulations are surrounding the Income Tax Act 1985

(c.1) Div A. It is illustrating that the income is depicted to be taxable if the individuals are

acquiring the taxable income with belonging to the resident of Canada. The tax payable by

the non-residents is depicted to be including that employment of the individual in Canada,

carrying out business in Canada and disposed to the taxable Canadian property. It is

illustrating that at the time of the year-end in Canada, the income tax must be paid as per the

taxable income earned (Canada Agency, 2018). The taxable income rules and the regulations

are depicted to be illustrated in the Div D of the norms and the regulations. As per the basic

taxation rules, the total amount of each of which the taxpayer's income is identified from the

source, the generation of the taxation process is depicted to be dependent on the taxpayer's

income for each year. Apart from this, the taxable income is depicted to be dependent on the

depositions which are listed as personal properties, plants, and the equipment. The taxpayer is

depicted to be allowing the capital losses for the years deposition and also it is determined

that the deduction will be made on the taxpayer's income. The total deductions are made on

the basis of determining the total referred values mentioned in the “Paragraph a” of the

Income Tax Act 1985 (Canada Agency, 2018). A taxpayer’s income or loss for the taxation

year is depicted to be computed according to the Act and also the exemptions will be made

on the basis of the losses incurred by the taxpayer in the financial year. As per the subsection

4(3) of the Act, it is indicating the acceptance of the deductions on the taxes implemented on

the taxpayer depending on the losses.

According to the Canadian Taxation laws on the share, the tax treatment is incorporated on

the basis of the purchasing of the shares carried out by the corporation. The adjustment of the

cost base amount is depicted to be paid for the shares and also the commission must be paid

with determining the capital gain losses. The changes in the sales are depicted to be

determining the capital gain taxes, as well as the taxes, are depicted to be incorporated on the

basis of the income made (Canada Agency, 2018). The 50% of the capital gain taxes are

1

depicted to be included under the income tax gathered in the form of the taxes. The reduction

or the elimination of the capital gains except for the death of the individual is being made. If

the shares are depicted to be purchased on different dates of a particular corporation, the tax

will be implemented on the basis of the purchase made in each of the shares (Canada Agency,

2018). The changes in the processes are depicted to be gained by carrying out the adjustment

of the cost base with including each of the share times as the number of the shares is sold.

The superficial losses are depicted to be adjusted on the basis of the costs as per the

repurchasing is being made and also the substitute of the shares are depicted to be claimed on

the basis of the expiry options mentioned in the Canadian taxation laws. If the disposing of

the shares is depicted to be made at the TFSA and also no superficial loss is being depicted

within the 30 days, then it is considered as non-taxable or deductible. Apart from this, it is

depicted to be including the transferring of the shares with including the registering processes

for the accounts.

The income tax is to be charged as per the Canadian income tax rules and regulations. It is

very much important for an individual to follow the taxation rules and regulations. Ann has

to estimate her annual income for paying tax to the government. Ann has purchased all the

shares of the Generations Inc. and the company issued 1000 common shares and it is still

outstanding. The dividends are to be paid by the organization after the income tax on the

basis of the share value. Thus, it is considered to be non-deductible expenses for the

organization (KPMG, 2018). The shareholders receiving dividends in Canada are to be taxed

at the lower tax rate. If the common shares of the investors are held within the taxable income

then the change in the price of the share is considered to the taxable capital loss or gain. Thus,

Ann has to pay the tax after receiving dividends from the company. In Canada, GI is the

small business corporation and Ann has purchased the shares. Ann has never used any capital

gain exemptions but it can be used by selling the shares. Ann can sell the shares at a

minimum gain which will not consider as the taxable income (KPMG, 2018). In the year

1993, GI was being incorporated by an individual who dealt at the length of the arm with

Ann. 1000 common shares was being subscribed by the initial shareholder Ann and paid an

amount of $4000 for purchasing the shares from the company. The fair market value of the

common shares at the time was $240000. The increase or decrease in the value will lead to

capital gain or loss on which the tax is to be paid.

The future growth of the company GI wants to be transferred by Ann to her adult child. The

transfer of the future growth is not to be constituted in the income tax consequences. Ann as

2

or the elimination of the capital gains except for the death of the individual is being made. If

the shares are depicted to be purchased on different dates of a particular corporation, the tax

will be implemented on the basis of the purchase made in each of the shares (Canada Agency,

2018). The changes in the processes are depicted to be gained by carrying out the adjustment

of the cost base with including each of the share times as the number of the shares is sold.

The superficial losses are depicted to be adjusted on the basis of the costs as per the

repurchasing is being made and also the substitute of the shares are depicted to be claimed on

the basis of the expiry options mentioned in the Canadian taxation laws. If the disposing of

the shares is depicted to be made at the TFSA and also no superficial loss is being depicted

within the 30 days, then it is considered as non-taxable or deductible. Apart from this, it is

depicted to be including the transferring of the shares with including the registering processes

for the accounts.

The income tax is to be charged as per the Canadian income tax rules and regulations. It is

very much important for an individual to follow the taxation rules and regulations. Ann has

to estimate her annual income for paying tax to the government. Ann has purchased all the

shares of the Generations Inc. and the company issued 1000 common shares and it is still

outstanding. The dividends are to be paid by the organization after the income tax on the

basis of the share value. Thus, it is considered to be non-deductible expenses for the

organization (KPMG, 2018). The shareholders receiving dividends in Canada are to be taxed

at the lower tax rate. If the common shares of the investors are held within the taxable income

then the change in the price of the share is considered to the taxable capital loss or gain. Thus,

Ann has to pay the tax after receiving dividends from the company. In Canada, GI is the

small business corporation and Ann has purchased the shares. Ann has never used any capital

gain exemptions but it can be used by selling the shares. Ann can sell the shares at a

minimum gain which will not consider as the taxable income (KPMG, 2018). In the year

1993, GI was being incorporated by an individual who dealt at the length of the arm with

Ann. 1000 common shares was being subscribed by the initial shareholder Ann and paid an

amount of $4000 for purchasing the shares from the company. The fair market value of the

common shares at the time was $240000. The increase or decrease in the value will lead to

capital gain or loss on which the tax is to be paid.

The future growth of the company GI wants to be transferred by Ann to her adult child. The

transfer of the future growth is not to be constituted in the income tax consequences. Ann as

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the part of the estate freeze will incorporate the Newco into a new company. She also wants

to subscribe to the common shares of the company Newco to her child. Ann will not be

eligible for the capital gain exemption if she sells the shares to the family members as per the

Canadian Income Tax Act (Tax Tips, 2018). The rule also explains that the family members

should have purchased the shares for twenty months before the sale. Around 50% of the

assets of the company in the period of 24 months should have been used for the purpose of

business. When the shares are sold than 90% of the assets of the company should be engaged

in carrying out the business operation in Canada. The rules and regulations need to be

followed by Ann in an appropriate manner. Ann can purchase the assets for the tax benefits

but the sale of the assets makes an individual ineligible for the exemption from the capital

gains.

Ann wants for receiving the maximum boot amount and the preferred shares for balancing the

considering while selling the GI shares to the company Newco in the year 2018. The

subsection 85 (1) allows the taxpayer to elect for deferring part or all the income that arise on

the transfer of some types of property to the taxable Canadian company. The section provides

the taxpayer to make the transfer at the agreed amounts on which the Act imposing many

limitations. The income tax is to be imposed on the basis of the subsection 85 (1). It is also

found that GI is not being associated with any other organization. The taxable capital amount

has always been less than $10 million. The tax is to be charged on the basis of the corporate

income tax rate. The taxable capital employed is the amount which is being used for the

estimation of the capital tax of the organizations (Capital Gains, 2018). The organization is

considered to be a large organization when the capital employed is more than $10 million.

The current worth of common shares of GI is $1500 per share.

Section 84.1 would be applied to the estate freeze due to the following reasons:

Ann is a Canadian resident who wants to transfer her shares.

Shares of GI are considered to be the capital property

Ronaldo deals with Ann at arm's length

GI and Holding Co. are incorporated

Deemed Dividend

FMV of Boot: $1500000

Less:

3

to subscribe to the common shares of the company Newco to her child. Ann will not be

eligible for the capital gain exemption if she sells the shares to the family members as per the

Canadian Income Tax Act (Tax Tips, 2018). The rule also explains that the family members

should have purchased the shares for twenty months before the sale. Around 50% of the

assets of the company in the period of 24 months should have been used for the purpose of

business. When the shares are sold than 90% of the assets of the company should be engaged

in carrying out the business operation in Canada. The rules and regulations need to be

followed by Ann in an appropriate manner. Ann can purchase the assets for the tax benefits

but the sale of the assets makes an individual ineligible for the exemption from the capital

gains.

Ann wants for receiving the maximum boot amount and the preferred shares for balancing the

considering while selling the GI shares to the company Newco in the year 2018. The

subsection 85 (1) allows the taxpayer to elect for deferring part or all the income that arise on

the transfer of some types of property to the taxable Canadian company. The section provides

the taxpayer to make the transfer at the agreed amounts on which the Act imposing many

limitations. The income tax is to be imposed on the basis of the subsection 85 (1). It is also

found that GI is not being associated with any other organization. The taxable capital amount

has always been less than $10 million. The tax is to be charged on the basis of the corporate

income tax rate. The taxable capital employed is the amount which is being used for the

estimation of the capital tax of the organizations (Capital Gains, 2018). The organization is

considered to be a large organization when the capital employed is more than $10 million.

The current worth of common shares of GI is $1500 per share.

Section 84.1 would be applied to the estate freeze due to the following reasons:

Ann is a Canadian resident who wants to transfer her shares.

Shares of GI are considered to be the capital property

Ronaldo deals with Ann at arm's length

GI and Holding Co. are incorporated

Deemed Dividend

FMV of Boot: $1500000

Less:

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

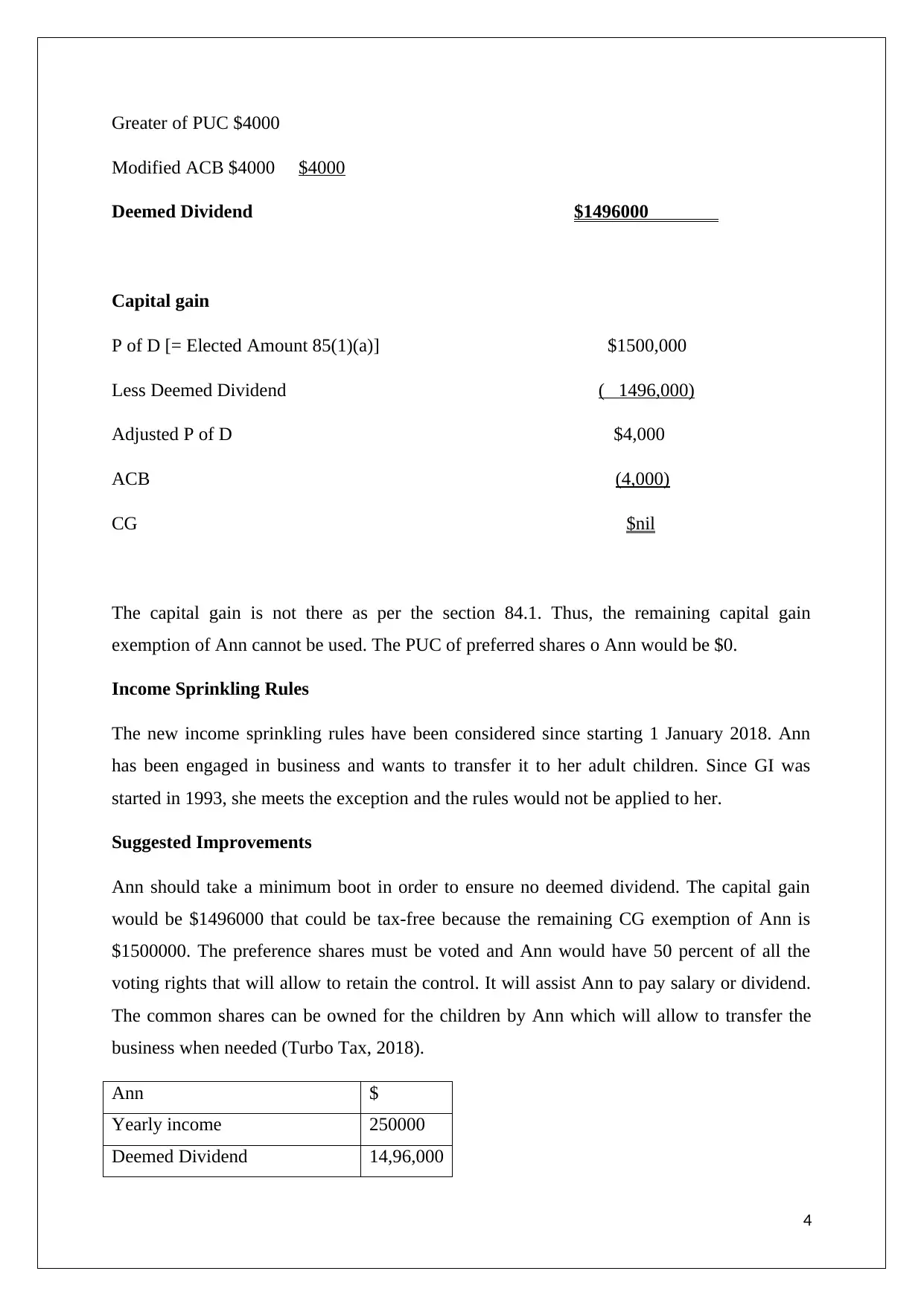

Greater of PUC $4000

Modified ACB $4000 $4000

Deemed Dividend $1496000

Capital gain

P of D [= Elected Amount 85(1)(a)] $1500,000

Less Deemed Dividend ( 1496,000)

Adjusted P of D $4,000

ACB (4,000)

CG $nil

The capital gain is not there as per the section 84.1. Thus, the remaining capital gain

exemption of Ann cannot be used. The PUC of preferred shares o Ann would be $0.

Income Sprinkling Rules

The new income sprinkling rules have been considered since starting 1 January 2018. Ann

has been engaged in business and wants to transfer it to her adult children. Since GI was

started in 1993, she meets the exception and the rules would not be applied to her.

Suggested Improvements

Ann should take a minimum boot in order to ensure no deemed dividend. The capital gain

would be $1496000 that could be tax-free because the remaining CG exemption of Ann is

$1500000. The preference shares must be voted and Ann would have 50 percent of all the

voting rights that will allow to retain the control. It will assist Ann to pay salary or dividend.

The common shares can be owned for the children by Ann which will allow to transfer the

business when needed (Turbo Tax, 2018).

Ann $

Yearly income 250000

Deemed Dividend 14,96,000

4

Modified ACB $4000 $4000

Deemed Dividend $1496000

Capital gain

P of D [= Elected Amount 85(1)(a)] $1500,000

Less Deemed Dividend ( 1496,000)

Adjusted P of D $4,000

ACB (4,000)

CG $nil

The capital gain is not there as per the section 84.1. Thus, the remaining capital gain

exemption of Ann cannot be used. The PUC of preferred shares o Ann would be $0.

Income Sprinkling Rules

The new income sprinkling rules have been considered since starting 1 January 2018. Ann

has been engaged in business and wants to transfer it to her adult children. Since GI was

started in 1993, she meets the exception and the rules would not be applied to her.

Suggested Improvements

Ann should take a minimum boot in order to ensure no deemed dividend. The capital gain

would be $1496000 that could be tax-free because the remaining CG exemption of Ann is

$1500000. The preference shares must be voted and Ann would have 50 percent of all the

voting rights that will allow to retain the control. It will assist Ann to pay salary or dividend.

The common shares can be owned for the children by Ann which will allow to transfer the

business when needed (Turbo Tax, 2018).

Ann $

Yearly income 250000

Deemed Dividend 14,96,000

4

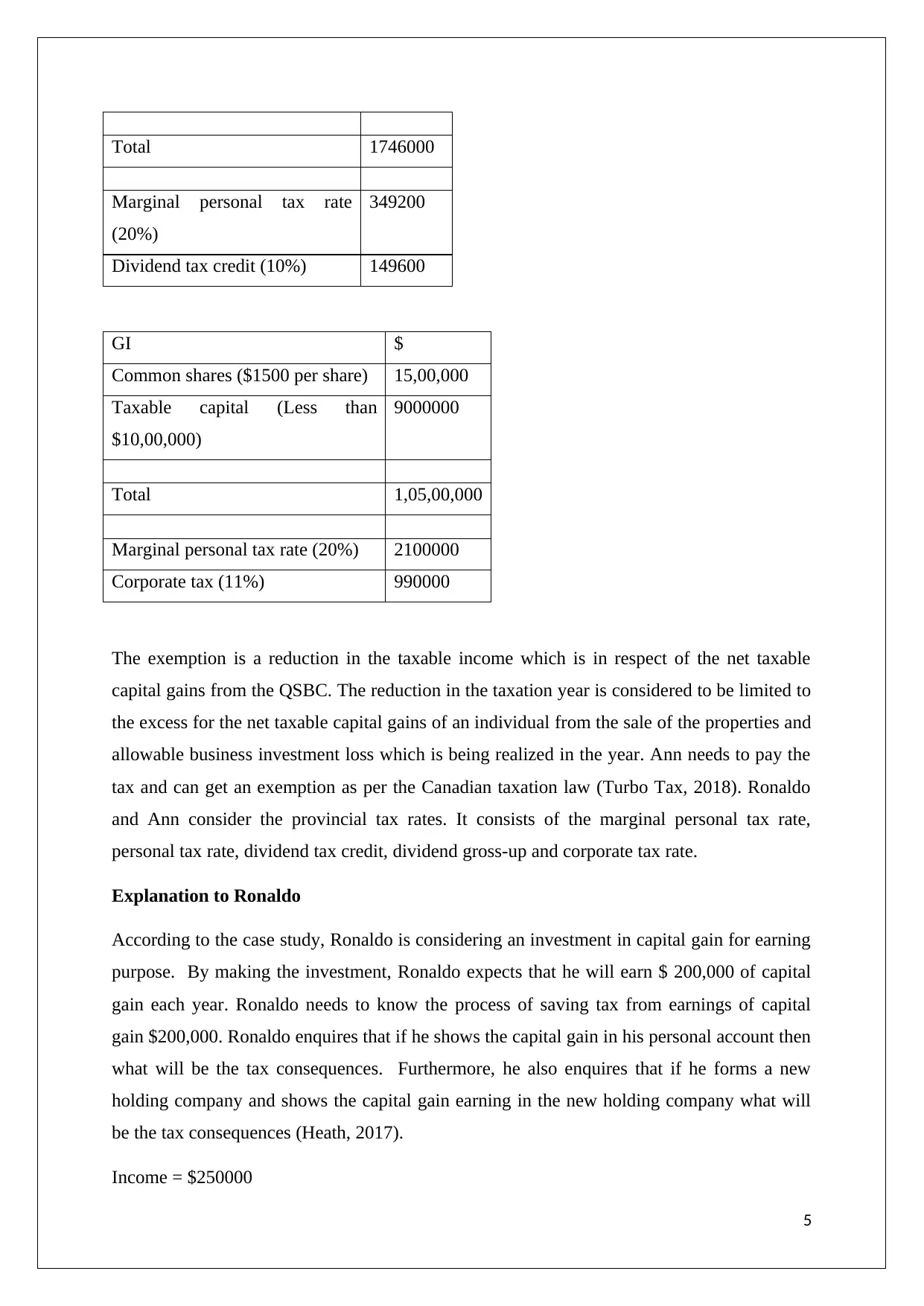

Total 1746000

Marginal personal tax rate

(20%)

349200

Dividend tax credit (10%) 149600

GI $

Common shares ($1500 per share) 15,00,000

Taxable capital (Less than

$10,00,000)

9000000

Total 1,05,00,000

Marginal personal tax rate (20%) 2100000

Corporate tax (11%) 990000

The exemption is a reduction in the taxable income which is in respect of the net taxable

capital gains from the QSBC. The reduction in the taxation year is considered to be limited to

the excess for the net taxable capital gains of an individual from the sale of the properties and

allowable business investment loss which is being realized in the year. Ann needs to pay the

tax and can get an exemption as per the Canadian taxation law (Turbo Tax, 2018). Ronaldo

and Ann consider the provincial tax rates. It consists of the marginal personal tax rate,

personal tax rate, dividend tax credit, dividend gross-up and corporate tax rate.

Explanation to Ronaldo

According to the case study, Ronaldo is considering an investment in capital gain for earning

purpose. By making the investment, Ronaldo expects that he will earn $ 200,000 of capital

gain each year. Ronaldo needs to know the process of saving tax from earnings of capital

gain $200,000. Ronaldo enquires that if he shows the capital gain in his personal account then

what will be the tax consequences. Furthermore, he also enquires that if he forms a new

holding company and shows the capital gain earning in the new holding company what will

be the tax consequences (Heath, 2017).

Income = $250000

5

Marginal personal tax rate

(20%)

349200

Dividend tax credit (10%) 149600

GI $

Common shares ($1500 per share) 15,00,000

Taxable capital (Less than

$10,00,000)

9000000

Total 1,05,00,000

Marginal personal tax rate (20%) 2100000

Corporate tax (11%) 990000

The exemption is a reduction in the taxable income which is in respect of the net taxable

capital gains from the QSBC. The reduction in the taxation year is considered to be limited to

the excess for the net taxable capital gains of an individual from the sale of the properties and

allowable business investment loss which is being realized in the year. Ann needs to pay the

tax and can get an exemption as per the Canadian taxation law (Turbo Tax, 2018). Ronaldo

and Ann consider the provincial tax rates. It consists of the marginal personal tax rate,

personal tax rate, dividend tax credit, dividend gross-up and corporate tax rate.

Explanation to Ronaldo

According to the case study, Ronaldo is considering an investment in capital gain for earning

purpose. By making the investment, Ronaldo expects that he will earn $ 200,000 of capital

gain each year. Ronaldo needs to know the process of saving tax from earnings of capital

gain $200,000. Ronaldo enquires that if he shows the capital gain in his personal account then

what will be the tax consequences. Furthermore, he also enquires that if he forms a new

holding company and shows the capital gain earning in the new holding company what will

be the tax consequences (Heath, 2017).

Income = $250000

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

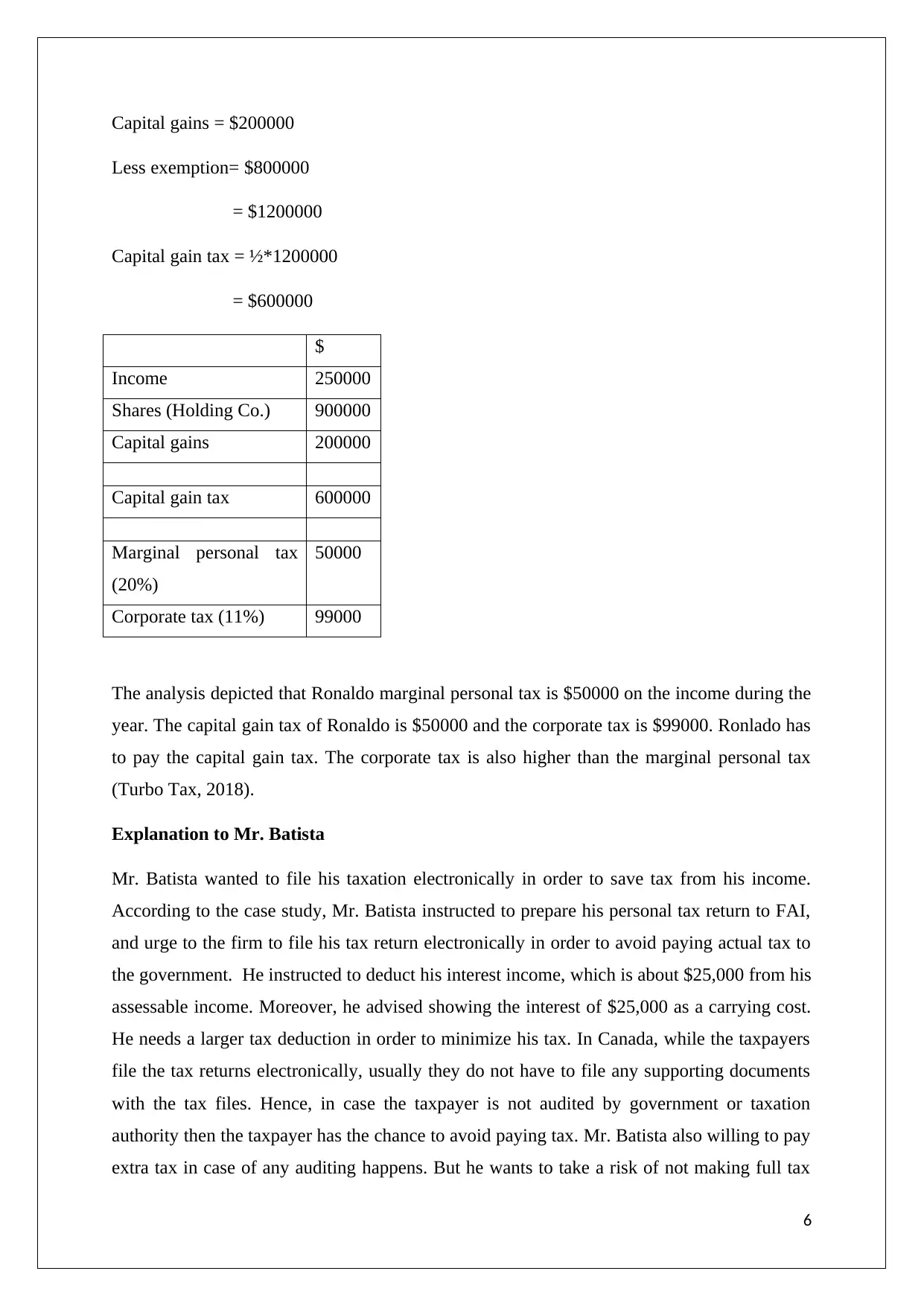

Capital gains = $200000

Less exemption= $800000

= $1200000

Capital gain tax = ½*1200000

= $600000

$

Income 250000

Shares (Holding Co.) 900000

Capital gains 200000

Capital gain tax 600000

Marginal personal tax

(20%)

50000

Corporate tax (11%) 99000

The analysis depicted that Ronaldo marginal personal tax is $50000 on the income during the

year. The capital gain tax of Ronaldo is $50000 and the corporate tax is $99000. Ronlado has

to pay the capital gain tax. The corporate tax is also higher than the marginal personal tax

(Turbo Tax, 2018).

Explanation to Mr. Batista

Mr. Batista wanted to file his taxation electronically in order to save tax from his income.

According to the case study, Mr. Batista instructed to prepare his personal tax return to FAI,

and urge to the firm to file his tax return electronically in order to avoid paying actual tax to

the government. He instructed to deduct his interest income, which is about $25,000 from his

assessable income. Moreover, he advised showing the interest of $25,000 as a carrying cost.

He needs a larger tax deduction in order to minimize his tax. In Canada, while the taxpayers

file the tax returns electronically, usually they do not have to file any supporting documents

with the tax files. Hence, in case the taxpayer is not audited by government or taxation

authority then the taxpayer has the chance to avoid paying tax. Mr. Batista also willing to pay

extra tax in case of any auditing happens. But he wants to take a risk of not making full tax

6

Less exemption= $800000

= $1200000

Capital gain tax = ½*1200000

= $600000

$

Income 250000

Shares (Holding Co.) 900000

Capital gains 200000

Capital gain tax 600000

Marginal personal tax

(20%)

50000

Corporate tax (11%) 99000

The analysis depicted that Ronaldo marginal personal tax is $50000 on the income during the

year. The capital gain tax of Ronaldo is $50000 and the corporate tax is $99000. Ronlado has

to pay the capital gain tax. The corporate tax is also higher than the marginal personal tax

(Turbo Tax, 2018).

Explanation to Mr. Batista

Mr. Batista wanted to file his taxation electronically in order to save tax from his income.

According to the case study, Mr. Batista instructed to prepare his personal tax return to FAI,

and urge to the firm to file his tax return electronically in order to avoid paying actual tax to

the government. He instructed to deduct his interest income, which is about $25,000 from his

assessable income. Moreover, he advised showing the interest of $25,000 as a carrying cost.

He needs a larger tax deduction in order to minimize his tax. In Canada, while the taxpayers

file the tax returns electronically, usually they do not have to file any supporting documents

with the tax files. Hence, in case the taxpayer is not audited by government or taxation

authority then the taxpayer has the chance to avoid paying tax. Mr. Batista also willing to pay

extra tax in case of any auditing happens. But he wants to take a risk of not making full tax

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

payment (Canada Agency, 2018). The customer of FAI also offer the firm that in case Mr.

Batista saves his tax regarding this additional deduction then he would pay one-quarter of the

amount, which he can save from the additional deduction.

The deduction of the interest expense will assist to decrease the taxable income of Batista as

per the Canadian taxation law. The interest expense is amounts to $25000 and the interest

expense is $2500. The amounts can be charged in the income of Batista in order to decrease

the taxable income as per the law. It can be possible to deduct his $25,000 of interest expense

at the time of filing Mr. Batista's tax return electronically (Turbo Tax, 2018). Because when

the tax will be filing electronically by a computer, the document will not be required to be

attached. Moreover, the FAI also will not be liable to deny getting any document from the

clients regarding the $25,000 interest expenses of the client named Mr. Batista.

7

Batista saves his tax regarding this additional deduction then he would pay one-quarter of the

amount, which he can save from the additional deduction.

The deduction of the interest expense will assist to decrease the taxable income of Batista as

per the Canadian taxation law. The interest expense is amounts to $25000 and the interest

expense is $2500. The amounts can be charged in the income of Batista in order to decrease

the taxable income as per the law. It can be possible to deduct his $25,000 of interest expense

at the time of filing Mr. Batista's tax return electronically (Turbo Tax, 2018). Because when

the tax will be filing electronically by a computer, the document will not be required to be

attached. Moreover, the FAI also will not be liable to deny getting any document from the

clients regarding the $25,000 interest expenses of the client named Mr. Batista.

7

References

Canada Agency (2018) Canadian income tax rates for individuals - current and previous

years - Canada.ca, Canada.Ca, [Online]. Available at https://www.canada.ca/en/revenue-

agency/services/tax/individuals/frequently-asked-questions-individuals/canadian-income-tax-

rates-individuals-current-previous-years.html (Accessed 13 August 2018).

Canada Agency (2018) Corporation tax rates - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/

corporation-tax-rates.html (Accessed 13 August 2018).

Canada Agency (2018) Deemed dividends - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/completing-slips-

summaries/financial-slips-summaries/return-investment-income-t5/deemed-dividends.html

(Accessed 13 August 2018).

Canada Agency (2018) Income tax - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/services/taxes/income-tax.html (Accessed 13 August 2018).

Canada Agency (2018) Line 221 - Carrying charges and interest expenses -

Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-

return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-221-carrying-

charges-interest-expenses.html (Accessed 13 August 2018).

Capital Gains (2018) Capital Gains – 2017 - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4037/

capital-gains-2016.html (Accessed 13 August 2018).

Heath, J. (2017) How to get the most out of the capital gains exemption -

MoneySense, Moneysense, [Online]. Available at

https://www.moneysense.ca/save/taxes/how-to-get-the-most-out-of-the-capital-gains-

exemption/ (Accessed 13 August 2018).

KPMG (2018) Canada - Income Tax, KPMG, [Online]. Available at

https://home.kpmg.com/xx/en/home/insights/2011/12/canada-income-tax.html (Accessed 13

August 2018).

8

Canada Agency (2018) Canadian income tax rates for individuals - current and previous

years - Canada.ca, Canada.Ca, [Online]. Available at https://www.canada.ca/en/revenue-

agency/services/tax/individuals/frequently-asked-questions-individuals/canadian-income-tax-

rates-individuals-current-previous-years.html (Accessed 13 August 2018).

Canada Agency (2018) Corporation tax rates - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/

corporation-tax-rates.html (Accessed 13 August 2018).

Canada Agency (2018) Deemed dividends - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/completing-slips-

summaries/financial-slips-summaries/return-investment-income-t5/deemed-dividends.html

(Accessed 13 August 2018).

Canada Agency (2018) Income tax - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/services/taxes/income-tax.html (Accessed 13 August 2018).

Canada Agency (2018) Line 221 - Carrying charges and interest expenses -

Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-

return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-221-carrying-

charges-interest-expenses.html (Accessed 13 August 2018).

Capital Gains (2018) Capital Gains – 2017 - Canada.ca, Canada.Ca, [Online]. Available at

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4037/

capital-gains-2016.html (Accessed 13 August 2018).

Heath, J. (2017) How to get the most out of the capital gains exemption -

MoneySense, Moneysense, [Online]. Available at

https://www.moneysense.ca/save/taxes/how-to-get-the-most-out-of-the-capital-gains-

exemption/ (Accessed 13 August 2018).

KPMG (2018) Canada - Income Tax, KPMG, [Online]. Available at

https://home.kpmg.com/xx/en/home/insights/2011/12/canada-income-tax.html (Accessed 13

August 2018).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

KPMG (2018) Canadian Corporate Tax Tables, KPMG, [Online]. Available at

https://home.kpmg.com/ca/en/home/services/tax/canadian-corporate-tax-tables.html

(Accessed 13 August 2018).

Tax Tips (2018) TaxTips.ca - Canada's Federal Personal Income Tax Rates, Taxtips.Ca,

[Online]. Available at https://www.taxtips.ca/taxrates/canada.htm (Accessed 13 August

2018).

Turbo Tax (2018) An Overview of Federal Tax Rates for 2017 | 2018 TurboTax® Canada

Tips, 2018 Turbotax® Canada Tips, [Online]. Available at https://turbotax.intuit.ca/tips/an-

overview-of-federal-tax-rates-286 (Accessed 13 August 2018).

Turbo Tax (2018) Claiming Carrying Charges and Interest Expenses | 2018 TurboTax®

Canada Tips, 2018 Turbotax® Canada Tips, [Online]. Available at

https://turbotax.intuit.ca/tips/claiming-carrying-charges-and-interest-expenses-162 (Accessed

13 August 2018).

Turbo Tax (2018) How to Reduce Capital Gains Tax in Canada | 2018 TurboTax® Canada

Tips, 2018 Turbotax® Canada Tips, [Online]. Available at https://turbotax.intuit.ca/tips/how-

to-reduce-capital-gains-tax-in-canada-6546 (Accessed 13 August 2018).

Turbo Tax (2018) The Federal Dividend Tax Credit in Canada | 2018 TurboTax® Canada

Tips, 2018 Turbotax® Canada Tips, [Online]. Available at https://turbotax.intuit.ca/tips/the-

federal-dividend-tax-credit-in-canada-332 (Accessed 13 August 2018).

9

https://home.kpmg.com/ca/en/home/services/tax/canadian-corporate-tax-tables.html

(Accessed 13 August 2018).

Tax Tips (2018) TaxTips.ca - Canada's Federal Personal Income Tax Rates, Taxtips.Ca,

[Online]. Available at https://www.taxtips.ca/taxrates/canada.htm (Accessed 13 August

2018).

Turbo Tax (2018) An Overview of Federal Tax Rates for 2017 | 2018 TurboTax® Canada

Tips, 2018 Turbotax® Canada Tips, [Online]. Available at https://turbotax.intuit.ca/tips/an-

overview-of-federal-tax-rates-286 (Accessed 13 August 2018).

Turbo Tax (2018) Claiming Carrying Charges and Interest Expenses | 2018 TurboTax®

Canada Tips, 2018 Turbotax® Canada Tips, [Online]. Available at

https://turbotax.intuit.ca/tips/claiming-carrying-charges-and-interest-expenses-162 (Accessed

13 August 2018).

Turbo Tax (2018) How to Reduce Capital Gains Tax in Canada | 2018 TurboTax® Canada

Tips, 2018 Turbotax® Canada Tips, [Online]. Available at https://turbotax.intuit.ca/tips/how-

to-reduce-capital-gains-tax-in-canada-6546 (Accessed 13 August 2018).

Turbo Tax (2018) The Federal Dividend Tax Credit in Canada | 2018 TurboTax® Canada

Tips, 2018 Turbotax® Canada Tips, [Online]. Available at https://turbotax.intuit.ca/tips/the-

federal-dividend-tax-credit-in-canada-332 (Accessed 13 August 2018).

9

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.