Comprehensive Canadian Tax Assignment for XYZ Company - 2018

VerifiedAdded on 2022/12/26

|10

|674

|40

Homework Assignment

AI Summary

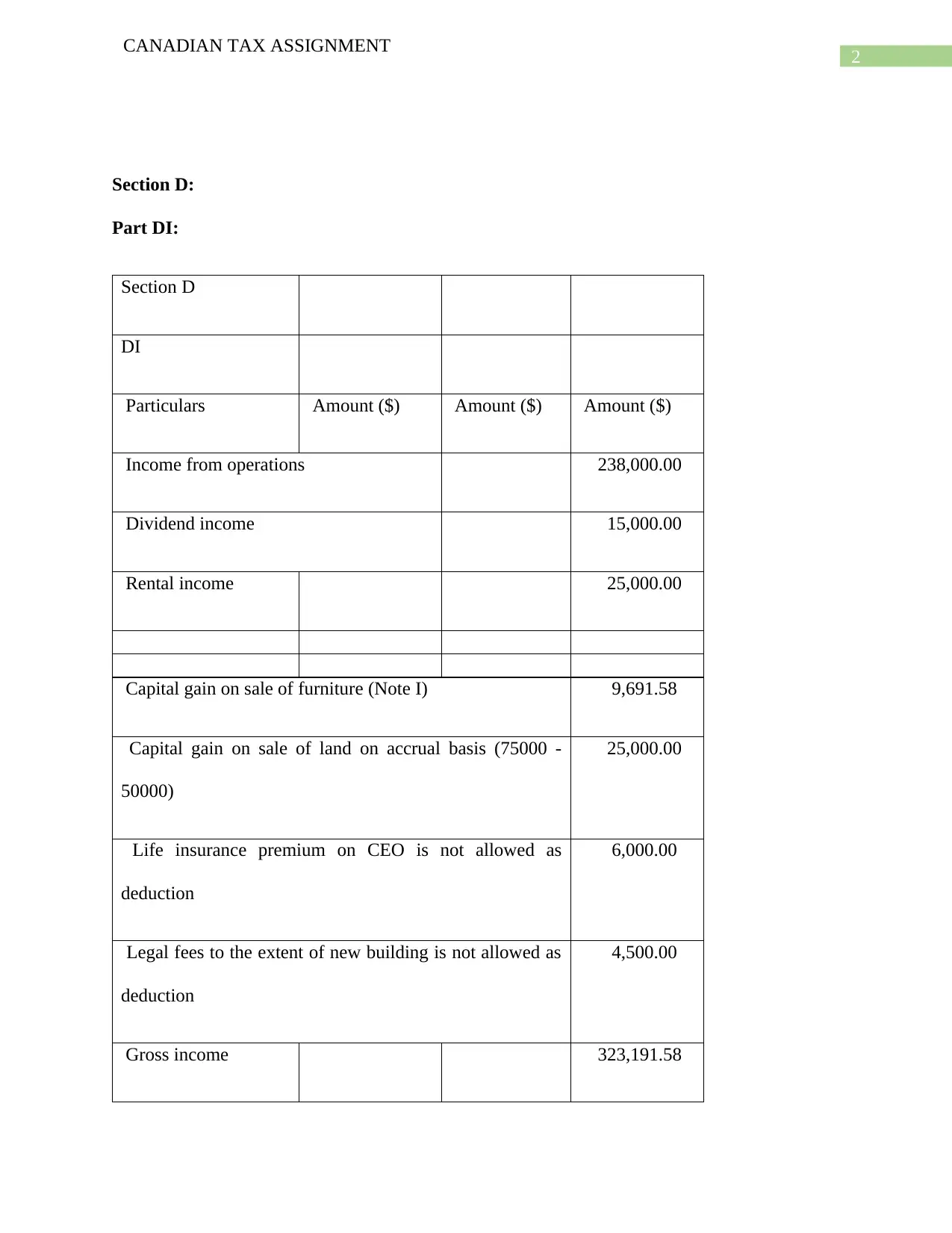

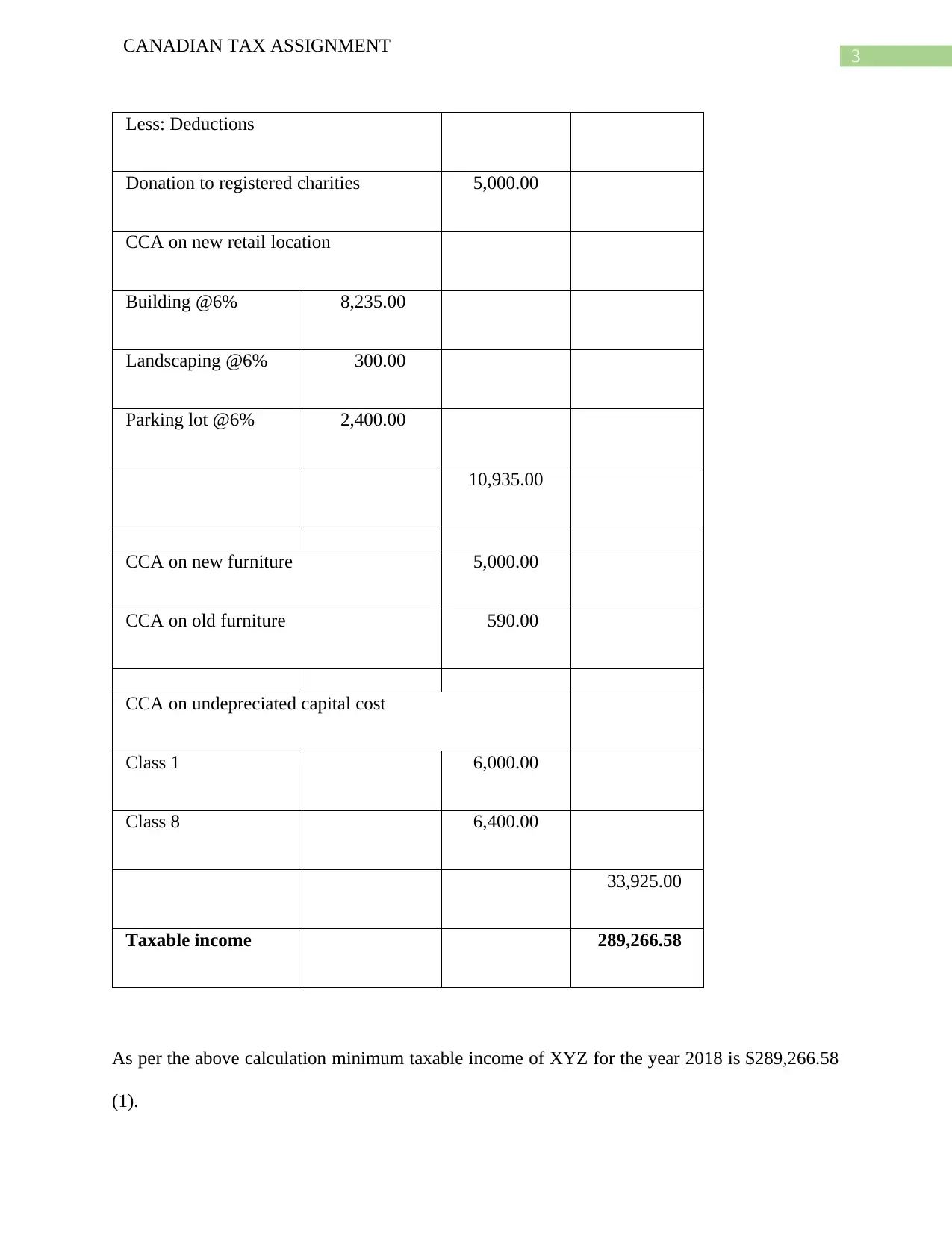

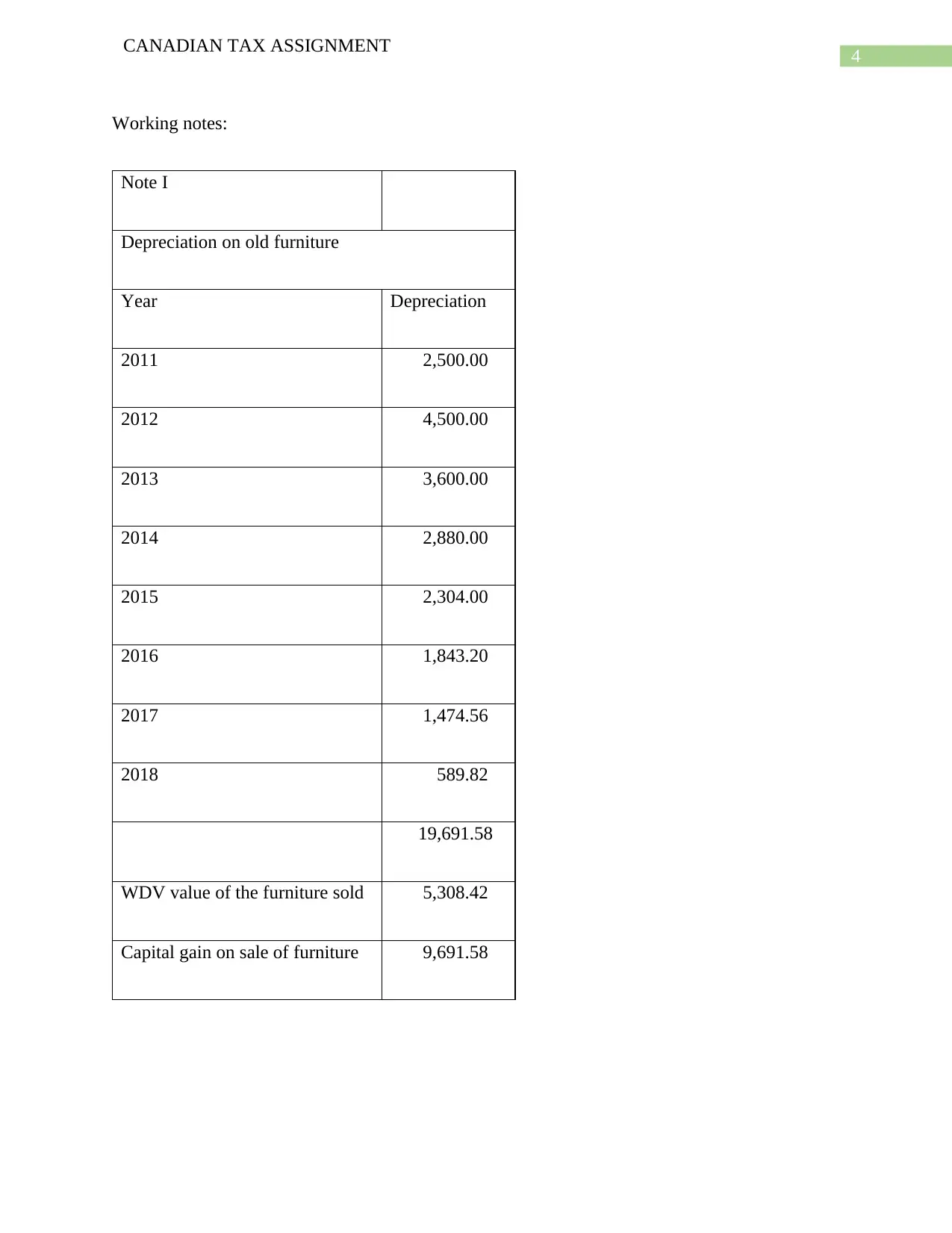

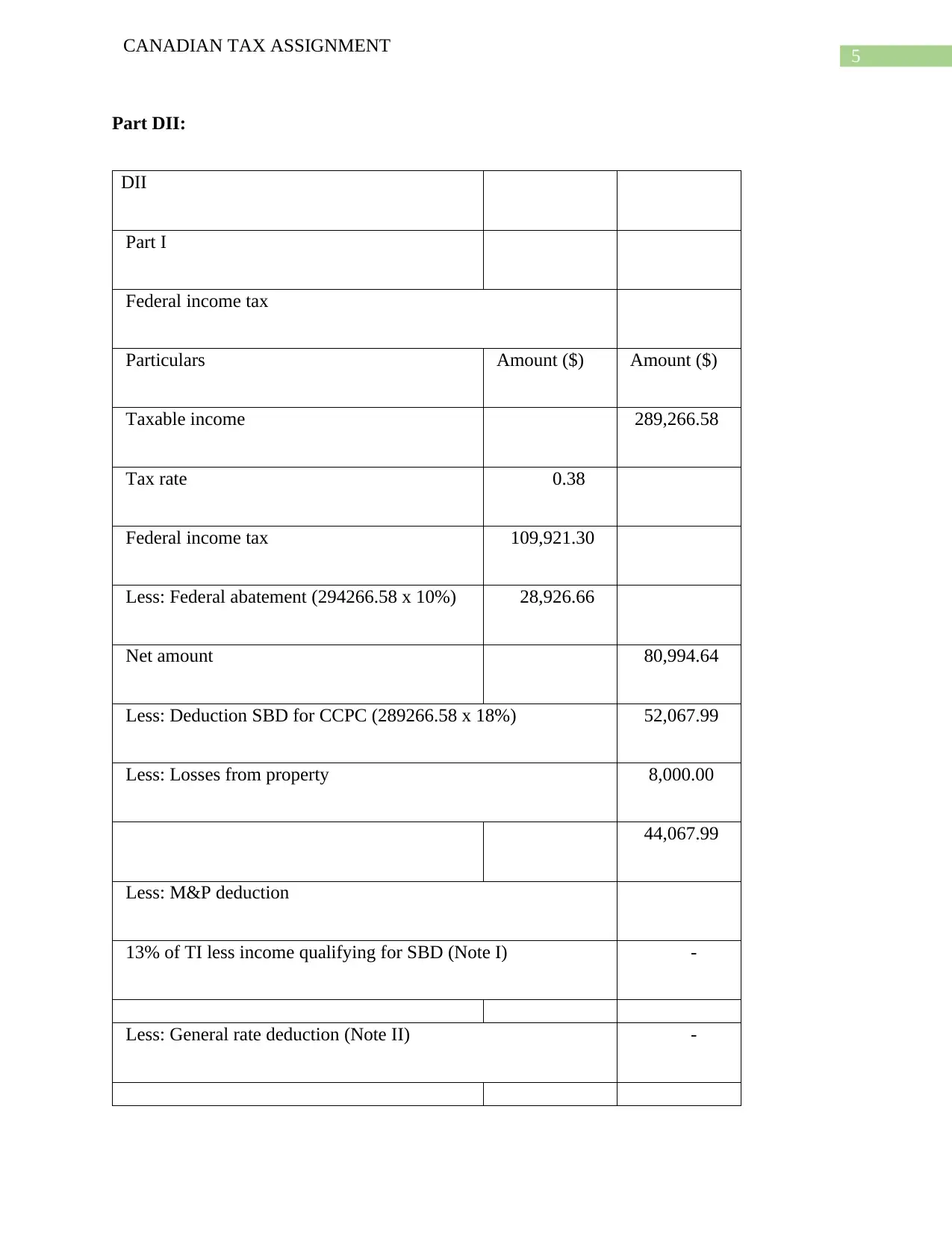

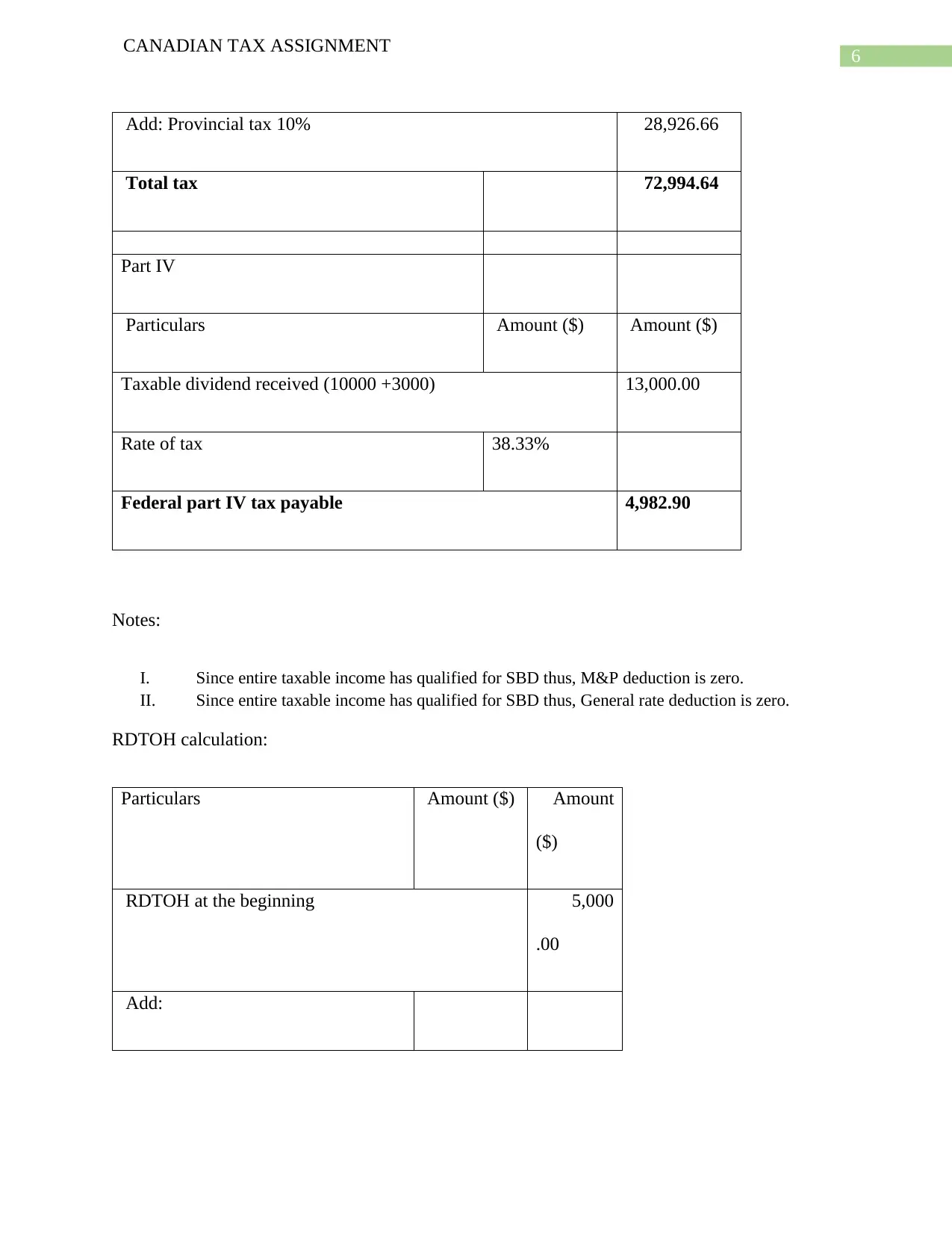

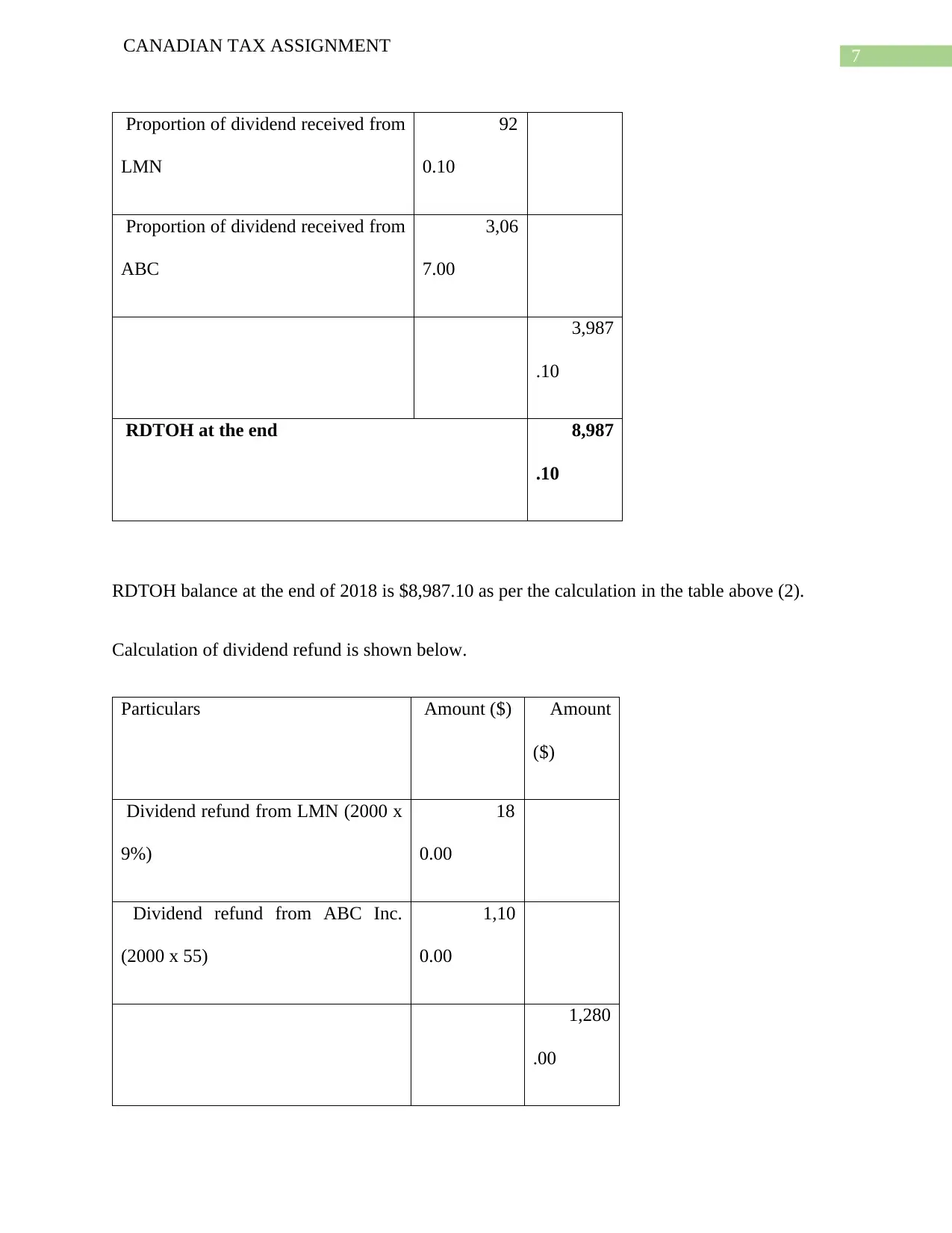

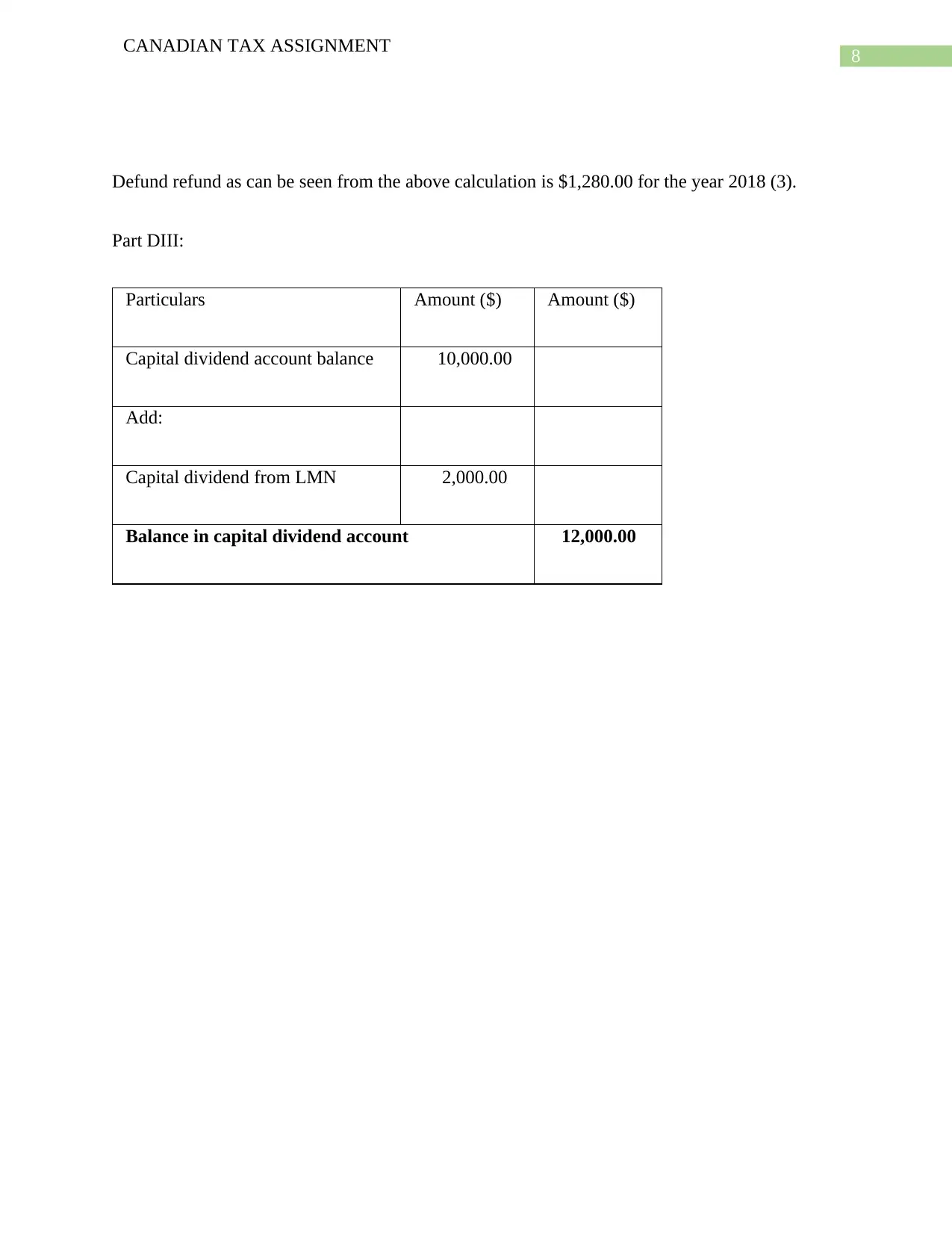

This Canadian tax assignment focuses on calculating the taxable income and tax liability for XYZ Company for the 2018 tax year. The assignment details various income sources, including income from operations, dividend income, and rental income, as well as capital gains. It outlines the deductions, such as donations, CCA on different assets, and losses from property. The solution includes working notes for depreciation calculations and detailed computations for federal income tax, including federal abatement, SBD, and losses. Furthermore, the assignment covers Part IV tax, RDTOH calculation, dividend refund calculation, and the capital dividend account balance. The final calculations determine the minimum taxable income, federal income tax, and other relevant tax components.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.