Taxation Assignment: Canadian Income Tax and Instalments

VerifiedAdded on 2022/09/02

|18

|2225

|20

Homework Assignment

AI Summary

This assignment solution addresses various aspects of Canadian income tax, including multiple-choice questions on taxable benefits, residency status, and filing requirements. It delves into long-answer questions, such as calculating tax instalments based on prior year liabilities and determining car benefits for employees. The solution provides detailed explanations and calculations for each scenario, covering topics like the impact of employer-provided loans, prescribed interest rates, and the tax implications of different types of employee benefits. It also covers the tax consequences of car benefits, including standby charges and operating costs, providing a comprehensive understanding of Canadian tax principles. The document aims to provide a comprehensive understanding of key Canadian tax concepts.

Section 1 - Multiple Choice Questions

1. Which of the following is a taxable benefit?

a. A cash Christmas gift to an employee from the employer valued at $450.

b. Payment of the tuition for an employee completing a degree that will benefit the employer.

c. A 20% discount on the employer’s merchandise, available to all employees.

d. Subsidized meals offered to all employees of the company assuming the price is

approximately equal to the cost.

2. Carla lives in Detroit, Michigan, USA. She commutes daily to Windsor, Ontario, Canada, where

she is employed by Ford Motor Company of Canada Limited. She works 9 am to 5 pm, Monday

through Friday. Which one of the following best indicates Carla’s residency status for Canadian

income tax purposes for 2019?

a. A full-time resident

b. A part-year resident

c. A non-resident

d. A deemed resident (sojourner)

3. All of the following statements are true, except:

a. Canadian residents must report their worldwide income for tax purposes.

b. If an individual is a resident of Canada for part of the calendar year, that individual only has

to report his worldwide income during the period of residency for Canadian tax purposes.

c. An individual who immigrates to Canada during the year is a resident of Canada for tax

purposes for the full calendar year.

d. An individual can be a resident of Canada for tax purposes, even if she is not a Canadian

citizen.

4. Of the following individuals, who would be considered a part-year resident of Canada for the

current taxation year?

a. Ravi is a citizen of India, where he was born and lived until moving to Canada on March 1

of the current year with his wife and child. He was transferred by his employer to its

Canadian head office.

b. Helga had lived and worked in Canada for 10 years. She was transferred by her employer

to its flagship hotel in Switzerland on March 1 of the current year for a 1 year training

assignment. Her husband remained in Canada to complete his MBA.

c. Marc is a French citizen who lives in Paris. On March 1 of the current year he begins work

as a translator in Ottawa. It is a 1 year assignment.

1 | Page

1. Which of the following is a taxable benefit?

a. A cash Christmas gift to an employee from the employer valued at $450.

b. Payment of the tuition for an employee completing a degree that will benefit the employer.

c. A 20% discount on the employer’s merchandise, available to all employees.

d. Subsidized meals offered to all employees of the company assuming the price is

approximately equal to the cost.

2. Carla lives in Detroit, Michigan, USA. She commutes daily to Windsor, Ontario, Canada, where

she is employed by Ford Motor Company of Canada Limited. She works 9 am to 5 pm, Monday

through Friday. Which one of the following best indicates Carla’s residency status for Canadian

income tax purposes for 2019?

a. A full-time resident

b. A part-year resident

c. A non-resident

d. A deemed resident (sojourner)

3. All of the following statements are true, except:

a. Canadian residents must report their worldwide income for tax purposes.

b. If an individual is a resident of Canada for part of the calendar year, that individual only has

to report his worldwide income during the period of residency for Canadian tax purposes.

c. An individual who immigrates to Canada during the year is a resident of Canada for tax

purposes for the full calendar year.

d. An individual can be a resident of Canada for tax purposes, even if she is not a Canadian

citizen.

4. Of the following individuals, who would be considered a part-year resident of Canada for the

current taxation year?

a. Ravi is a citizen of India, where he was born and lived until moving to Canada on March 1

of the current year with his wife and child. He was transferred by his employer to its

Canadian head office.

b. Helga had lived and worked in Canada for 10 years. She was transferred by her employer

to its flagship hotel in Switzerland on March 1 of the current year for a 1 year training

assignment. Her husband remained in Canada to complete his MBA.

c. Marc is a French citizen who lives in Paris. On March 1 of the current year he begins work

as a translator in Ottawa. It is a 1 year assignment.

1 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d. Billy Bob is a U.S. Marshall on loan to the RCMP detachment in Nunavut. It is a 9 month

assignment.

5. Dominique, a Canadian citizen, lives in Buffalo, NY, USA. Throughout the current year she

commutes to Fort Erie, Ontario, Canada, where she is the bartender at the Cross Border Bar.

She normally works 7 pm to 3 am Tuesday through Saturday. Dominique is:

a. A deemed resident (sojourner)

b. A non-resident

c. A full-time resident

d. A part-year resident

6. With respect to the filing of an individual income tax return, which of the following statements is

correct?

a. An individual is required to file an income tax return if their only source of income is

business income, even if no tax is payable.

b. An individual is required to file an income tax return if they have reached the age of 18 by

the end of the year.

c. If an individual has disposed of a capital property during the year, they are required to file

an income tax return, even if no tax is payable.

d. An individual is not required to file an income tax return if no tax is payable for the year.

7. For the 2019 taxation year, John Bookman had a taxable capital gain of $45,000 and a net

business loss of $45,000, resulting in a Taxable Income of nil. Which of the following statements

is correct?

a. John is not required to file a tax return for 2019.

b. John must file a tax return on or before June 15, 2020.

c. John must file a tax return on or before December 31, 2020.

d. John must file a tax return on or before April 30, 2020.

8. John Barron is self-employed and plans to file his 2019 tax return on June 15, 2020. His balance-

due day is:

a. April 30, 2019.

b. April 30, 2020.

c. June 15, 2020.

2 | Page

assignment.

5. Dominique, a Canadian citizen, lives in Buffalo, NY, USA. Throughout the current year she

commutes to Fort Erie, Ontario, Canada, where she is the bartender at the Cross Border Bar.

She normally works 7 pm to 3 am Tuesday through Saturday. Dominique is:

a. A deemed resident (sojourner)

b. A non-resident

c. A full-time resident

d. A part-year resident

6. With respect to the filing of an individual income tax return, which of the following statements is

correct?

a. An individual is required to file an income tax return if their only source of income is

business income, even if no tax is payable.

b. An individual is required to file an income tax return if they have reached the age of 18 by

the end of the year.

c. If an individual has disposed of a capital property during the year, they are required to file

an income tax return, even if no tax is payable.

d. An individual is not required to file an income tax return if no tax is payable for the year.

7. For the 2019 taxation year, John Bookman had a taxable capital gain of $45,000 and a net

business loss of $45,000, resulting in a Taxable Income of nil. Which of the following statements

is correct?

a. John is not required to file a tax return for 2019.

b. John must file a tax return on or before June 15, 2020.

c. John must file a tax return on or before December 31, 2020.

d. John must file a tax return on or before April 30, 2020.

8. John Barron is self-employed and plans to file his 2019 tax return on June 15, 2020. His balance-

due day is:

a. April 30, 2019.

b. April 30, 2020.

c. June 15, 2020.

2 | Page

d. June 15, 2019.

9. Mr. Khan, a self-employed construction contractor, dies on April 1, 2019. What is the latest filing

date for his final tax return?

a. April 30, 2020.

b. June 15, 2020.

c. October 1, 2020.

d. December 31, 2020.

10. Individuals are required to pay instalments:

a. When net tax owing is over $3,000 for any one of the past two years.

b. When net tax owing is over $3,000 for the current year and both of the two prior years.

c. When net tax owing is over $3,000 for the current year and one of the two prior years.

d. When net tax owing is over $3,000 for the current year only.

Section 2 – Long Answer Questions

Question 1 (8 Marks)

3 | Page

9. Mr. Khan, a self-employed construction contractor, dies on April 1, 2019. What is the latest filing

date for his final tax return?

a. April 30, 2020.

b. June 15, 2020.

c. October 1, 2020.

d. December 31, 2020.

10. Individuals are required to pay instalments:

a. When net tax owing is over $3,000 for any one of the past two years.

b. When net tax owing is over $3,000 for the current year and both of the two prior years.

c. When net tax owing is over $3,000 for the current year and one of the two prior years.

d. When net tax owing is over $3,000 for the current year only.

Section 2 – Long Answer Questions

Question 1 (8 Marks)

3 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

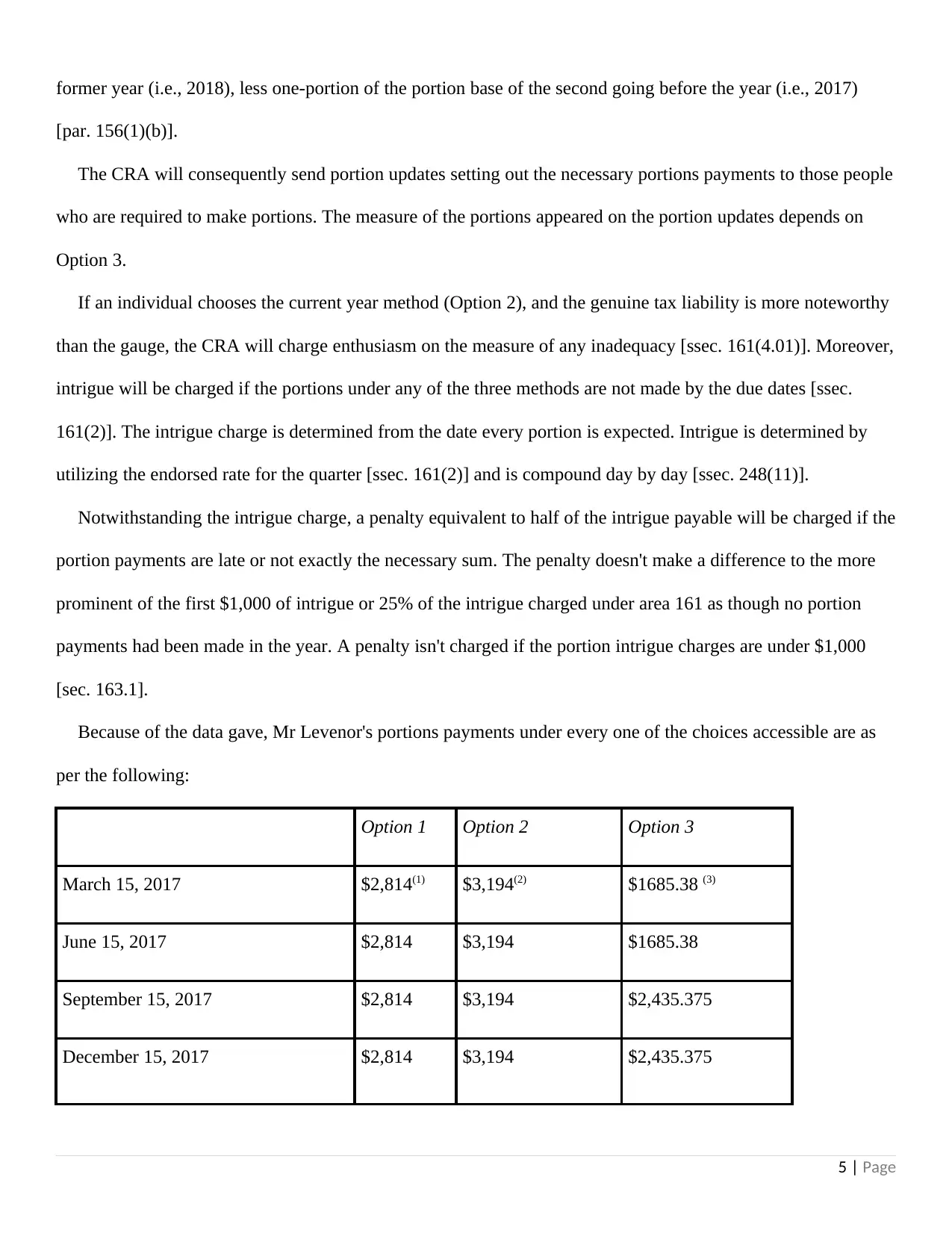

Assume that Barry Levenor’s combined federal and provincial Tax Payable is as follows:

2017 $14,256

2018 15,776

2019 (Estimated) 16,483

The amount Barry’s employer withholds for the three independent cases is as follows:

$14,920 in 2017, $11,400 in 2018, and $13,226 (estimated) in 2019

Required:

1. Indicate whether instalments are required for the 2019 taxation year;

1. In those Cases where instalments are required, calculate the amount of the instalments that

would be required under each of the three acceptable methods; and

2. For those Cases where instalments are required, indicate the dates on which the payments will

be due.

Solution-1:

Portion payments are required since the tax liability in the two earlier years was in abundance of $3,000 and

apparently, there were no withholding taxes on the pay [sec. 156.1]. The CRA approach permits certain

findings, for example, withholding taxes, from the portion base. (See Form 1033-WS for the suitable

derivations.)

Portion payments are required to be made on March 15, June 15, September 15, and December 15 paying

little heed to the choice picked [ssec. 156(1)].

An individual has three methods to look over to decide the measure of portions to be paid on the above dates.

Choice 1 The prior year method: one-quarter of the portion base, which is taxes payable for the quickly

going before year [spar. 156(1)(a)(ii)].

Choice 2 The current year method: one-quarter of the assessed tax payable for the current year [spar.

156(1)(a)(i)].

Choice 3 One quarter of the portion base for the second going before the year (i.e., 2010) for the March and

June portions, and for the September and December portions, 1/2 of the abundance of the portion base for the

4 | Page

2017 $14,256

2018 15,776

2019 (Estimated) 16,483

The amount Barry’s employer withholds for the three independent cases is as follows:

$14,920 in 2017, $11,400 in 2018, and $13,226 (estimated) in 2019

Required:

1. Indicate whether instalments are required for the 2019 taxation year;

1. In those Cases where instalments are required, calculate the amount of the instalments that

would be required under each of the three acceptable methods; and

2. For those Cases where instalments are required, indicate the dates on which the payments will

be due.

Solution-1:

Portion payments are required since the tax liability in the two earlier years was in abundance of $3,000 and

apparently, there were no withholding taxes on the pay [sec. 156.1]. The CRA approach permits certain

findings, for example, withholding taxes, from the portion base. (See Form 1033-WS for the suitable

derivations.)

Portion payments are required to be made on March 15, June 15, September 15, and December 15 paying

little heed to the choice picked [ssec. 156(1)].

An individual has three methods to look over to decide the measure of portions to be paid on the above dates.

Choice 1 The prior year method: one-quarter of the portion base, which is taxes payable for the quickly

going before year [spar. 156(1)(a)(ii)].

Choice 2 The current year method: one-quarter of the assessed tax payable for the current year [spar.

156(1)(a)(i)].

Choice 3 One quarter of the portion base for the second going before the year (i.e., 2010) for the March and

June portions, and for the September and December portions, 1/2 of the abundance of the portion base for the

4 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

former year (i.e., 2018), less one-portion of the portion base of the second going before the year (i.e., 2017)

[par. 156(1)(b)].

The CRA will consequently send portion updates setting out the necessary portions payments to those people

who are required to make portions. The measure of the portions appeared on the portion updates depends on

Option 3.

If an individual chooses the current year method (Option 2), and the genuine tax liability is more noteworthy

than the gauge, the CRA will charge enthusiasm on the measure of any inadequacy [ssec. 161(4.01)]. Moreover,

intrigue will be charged if the portions under any of the three methods are not made by the due dates [ssec.

161(2)]. The intrigue charge is determined from the date every portion is expected. Intrigue is determined by

utilizing the endorsed rate for the quarter [ssec. 161(2)] and is compound day by day [ssec. 248(11)].

Notwithstanding the intrigue charge, a penalty equivalent to half of the intrigue payable will be charged if the

portion payments are late or not exactly the necessary sum. The penalty doesn't make a difference to the more

prominent of the first $1,000 of intrigue or 25% of the intrigue charged under area 161 as though no portion

payments had been made in the year. A penalty isn't charged if the portion intrigue charges are under $1,000

[sec. 163.1].

Because of the data gave, Mr Levenor's portions payments under every one of the choices accessible are as

per the following:

Option 1 Option 2 Option 3

March 15, 2017 $2,814(1) $3,194(2) $1685.38 (3)

June 15, 2017 $2,814 $3,194 $1685.38

September 15, 2017 $2,814 $3,194 $2,435.375

December 15, 2017 $2,814 $3,194 $2,435.375

5 | Page

[par. 156(1)(b)].

The CRA will consequently send portion updates setting out the necessary portions payments to those people

who are required to make portions. The measure of the portions appeared on the portion updates depends on

Option 3.

If an individual chooses the current year method (Option 2), and the genuine tax liability is more noteworthy

than the gauge, the CRA will charge enthusiasm on the measure of any inadequacy [ssec. 161(4.01)]. Moreover,

intrigue will be charged if the portions under any of the three methods are not made by the due dates [ssec.

161(2)]. The intrigue charge is determined from the date every portion is expected. Intrigue is determined by

utilizing the endorsed rate for the quarter [ssec. 161(2)] and is compound day by day [ssec. 248(11)].

Notwithstanding the intrigue charge, a penalty equivalent to half of the intrigue payable will be charged if the

portion payments are late or not exactly the necessary sum. The penalty doesn't make a difference to the more

prominent of the first $1,000 of intrigue or 25% of the intrigue charged under area 161 as though no portion

payments had been made in the year. A penalty isn't charged if the portion intrigue charges are under $1,000

[sec. 163.1].

Because of the data gave, Mr Levenor's portions payments under every one of the choices accessible are as

per the following:

Option 1 Option 2 Option 3

March 15, 2017 $2,814(1) $3,194(2) $1685.38 (3)

June 15, 2017 $2,814 $3,194 $1685.38

September 15, 2017 $2,814 $3,194 $2,435.375

December 15, 2017 $2,814 $3,194 $2,435.375

5 | Page

Based on the above calculations, Option 1 results in a lower instalment requirement than the other methods.

However, as indicated above, if the 2019 actual tax liability is higher, interest will be charged on the deficiency.

—NOTES TO SOLUTION

(1) 1/4 of $11,256 (instalment base for 2017) = $2,814

(2) 1/4 of $12,776 (estimated 2018 tax payable) = $3,194

(3) First two instalments: 1/4 of $6741.5 (instalment base for 2019) = $1685.38

Last two instalments: 1/2 ◊ [$8,241.5 – (1/2 ◊ $6741.5)] = $2,435.375 ("Home page", 2020)

Question 2 (16 Marks)

Roman Round was born and raised in Canada, where he had lived continuously until March of 2019.

Roman was VP at International Products Manufacturing Ltd. (IPML), which had its head office in

Canada. The corporation transferred him to its Hungarian subsidiary. IPML planned to have him

return to Canada as its president in about two years. Review the following facts:

● The family home in Canada was listed for sale in February 2019 with hopes of selling it by

June.

● Roman left Canada on March 1, 2019 to begin his position in Hungary.

● He left his wife and children in Canada for the children to complete the school year.

● Roman took all of his personal possessions with him when he left.

● He sold his car, but the family kept a second car registered to his wife for their use in Canada.

● The Company obtained a furnished three-bedroom apartment for Roman and his family.

● Roman planned to look for a house to purchase when his family arrived.

● As a result of the slow real estate market in Canada, the family home could not be sold. The

family decided to rent the house for the period that they were living in Hungary.

● In July 2019, tenants were found to rent the house and the furniture on a one-year lease.

● Roman's wife and kids left Canada to join him on August 1, 2019, after selling the second car.

● Roman and his wife own a cottage in Canada which they plan to live in during a one-month

vacation in each of the summers that they will be away, starting with the summer of 2019.

● Roman retained his golf club membership in Canada, because he did not want to lose the high

initiation fee that he had paid fairly recently to become a member.

● Roman resigned from two Canadian business clubs that required annual membership fees. He

joined similar clubs on his arrival in Hungary.

6 | Page

However, as indicated above, if the 2019 actual tax liability is higher, interest will be charged on the deficiency.

—NOTES TO SOLUTION

(1) 1/4 of $11,256 (instalment base for 2017) = $2,814

(2) 1/4 of $12,776 (estimated 2018 tax payable) = $3,194

(3) First two instalments: 1/4 of $6741.5 (instalment base for 2019) = $1685.38

Last two instalments: 1/2 ◊ [$8,241.5 – (1/2 ◊ $6741.5)] = $2,435.375 ("Home page", 2020)

Question 2 (16 Marks)

Roman Round was born and raised in Canada, where he had lived continuously until March of 2019.

Roman was VP at International Products Manufacturing Ltd. (IPML), which had its head office in

Canada. The corporation transferred him to its Hungarian subsidiary. IPML planned to have him

return to Canada as its president in about two years. Review the following facts:

● The family home in Canada was listed for sale in February 2019 with hopes of selling it by

June.

● Roman left Canada on March 1, 2019 to begin his position in Hungary.

● He left his wife and children in Canada for the children to complete the school year.

● Roman took all of his personal possessions with him when he left.

● He sold his car, but the family kept a second car registered to his wife for their use in Canada.

● The Company obtained a furnished three-bedroom apartment for Roman and his family.

● Roman planned to look for a house to purchase when his family arrived.

● As a result of the slow real estate market in Canada, the family home could not be sold. The

family decided to rent the house for the period that they were living in Hungary.

● In July 2019, tenants were found to rent the house and the furniture on a one-year lease.

● Roman's wife and kids left Canada to join him on August 1, 2019, after selling the second car.

● Roman and his wife own a cottage in Canada which they plan to live in during a one-month

vacation in each of the summers that they will be away, starting with the summer of 2019.

● Roman retained his golf club membership in Canada, because he did not want to lose the high

initiation fee that he had paid fairly recently to become a member.

● Roman resigned from two Canadian business clubs that required annual membership fees. He

joined similar clubs on his arrival in Hungary.

6 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

● Roman was paid in Hungarian currency by the subsidiary, which deposited his pay directly into

his account with Bank of Hungary.

● He kept his RRSP and his investment portfolio in Canada.

● He maintained a bank account in Canada – his rental income was deposited into this account.

● The tenants were instructed to withhold and remit to the Canada Revenue Agency 25% of the

agreed monthly rental, as required on payments to non-residents.

Required:

1. Evaluate the alternatives in the residence issue as they relate to this fact situation.

2. Present your answer by discussing each degree of residence and its tax consequences as it

applies to this fact situation.

3. Provide your advice, in conclusion, after weighing the relevance of the facts you have

considered.

SOLUTION -2:

Full-time resident: taxed on overall salary for the entire year 2019

Standard: proceeding with the condition of relationship with Canada; i.e., ties not cut.

Evidence:

Primary

● didn't sell a house in Canada

● cost may have been set excessively high deliberately with the goal that it would not be sold

● house in Canada leased with furniture, perhaps showing a plan to come back to it

● the one-year lease makes it progressively hard to sell with empty belonging

● house claimed in Canada

● demonstrated aim to come back to it during summer get-away of one month

● the close family didn't leave with him

Secondary

● conceived, raised, taught, and worked in Canada

7 | Page

his account with Bank of Hungary.

● He kept his RRSP and his investment portfolio in Canada.

● He maintained a bank account in Canada – his rental income was deposited into this account.

● The tenants were instructed to withhold and remit to the Canada Revenue Agency 25% of the

agreed monthly rental, as required on payments to non-residents.

Required:

1. Evaluate the alternatives in the residence issue as they relate to this fact situation.

2. Present your answer by discussing each degree of residence and its tax consequences as it

applies to this fact situation.

3. Provide your advice, in conclusion, after weighing the relevance of the facts you have

considered.

SOLUTION -2:

Full-time resident: taxed on overall salary for the entire year 2019

Standard: proceeding with the condition of relationship with Canada; i.e., ties not cut.

Evidence:

Primary

● didn't sell a house in Canada

● cost may have been set excessively high deliberately with the goal that it would not be sold

● house in Canada leased with furniture, perhaps showing a plan to come back to it

● the one-year lease makes it progressively hard to sell with empty belonging

● house claimed in Canada

● demonstrated aim to come back to it during summer get-away of one month

● the close family didn't leave with him

Secondary

● conceived, raised, taught, and worked in Canada

7 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

● plan to have him return in a few years

● rental of outfitted loft in Hungary may show transitory remain there

● family members and companions stayed in Canada

● held golf club participation

● held RRSP and speculation portfolio in Canada

● kept up the ledger in Canada ("Home page", 2020)

Deemed full-time resident:taxed in Canada on overall salary for the entire year.

Paradigm: section 250(1)(a) necessitates that he stay in Canada for a total of 183 days or more while a non-

resident.

Evidence:

● at the point when he was in Canada during 2019, he was not staying, because he was not living in

Canada briefly or visiting

● besides, he left Canada on March 1, 2019, in this way, being in Canada for under 183 days

● accordingly, regarded full-time living arrangement is anything but a practical end right now

Part-year resident: a tax on overall pay for the piece of 2019 when fully resident.

Foundation: "clean break" from Canada in 2019.

Evidence:

● arranged remain abroad was for an uncertain term of "a few years"

● recorded family home available to be purchased

no deal because of poor economic situations

● work license got in Hungary

8 | Page

● rental of outfitted loft in Hungary may show transitory remain there

● family members and companions stayed in Canada

● held golf club participation

● held RRSP and speculation portfolio in Canada

● kept up the ledger in Canada ("Home page", 2020)

Deemed full-time resident:taxed in Canada on overall salary for the entire year.

Paradigm: section 250(1)(a) necessitates that he stay in Canada for a total of 183 days or more while a non-

resident.

Evidence:

● at the point when he was in Canada during 2019, he was not staying, because he was not living in

Canada briefly or visiting

● besides, he left Canada on March 1, 2019, in this way, being in Canada for under 183 days

● accordingly, regarded full-time living arrangement is anything but a practical end right now

Part-year resident: a tax on overall pay for the piece of 2019 when fully resident.

Foundation: "clean break" from Canada in 2019.

Evidence:

● arranged remain abroad was for an uncertain term of "a few years"

● recorded family home available to be purchased

no deal because of poor economic situations

● work license got in Hungary

8 | Page

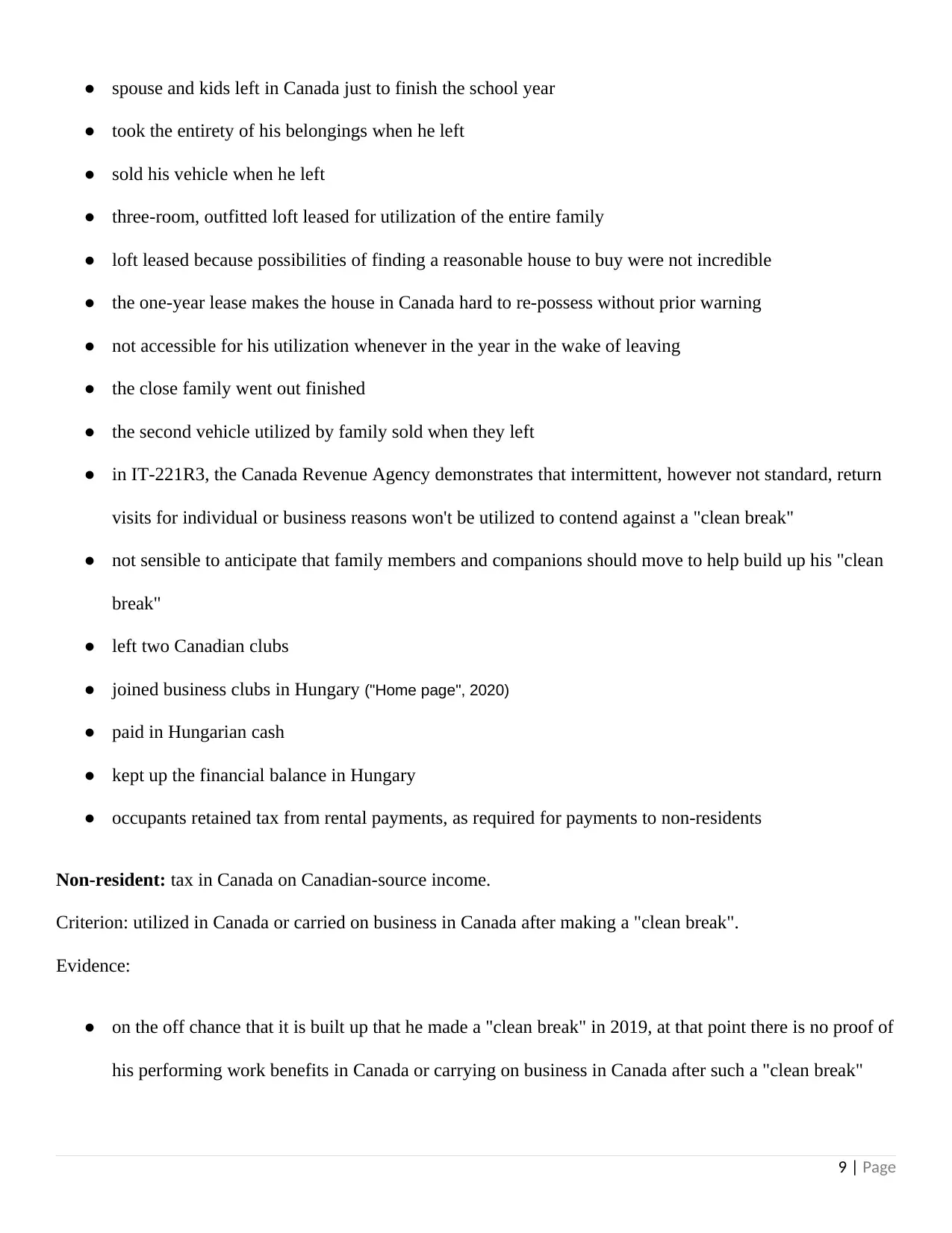

● spouse and kids left in Canada just to finish the school year

● took the entirety of his belongings when he left

● sold his vehicle when he left

● three-room, outfitted loft leased for utilization of the entire family

● loft leased because possibilities of finding a reasonable house to buy were not incredible

● the one-year lease makes the house in Canada hard to re-possess without prior warning

● not accessible for his utilization whenever in the year in the wake of leaving

● the close family went out finished

● the second vehicle utilized by family sold when they left

● in IT-221R3, the Canada Revenue Agency demonstrates that intermittent, however not standard, return

visits for individual or business reasons won't be utilized to contend against a "clean break"

● not sensible to anticipate that family members and companions should move to help build up his "clean

break"

● left two Canadian clubs

● joined business clubs in Hungary ("Home page", 2020)

● paid in Hungarian cash

● kept up the financial balance in Hungary

● occupants retained tax from rental payments, as required for payments to non-residents

Non-resident: tax in Canada on Canadian-source income.

Criterion: utilized in Canada or carried on business in Canada after making a "clean break".

Evidence:

● on the off chance that it is built up that he made a "clean break" in 2019, at that point there is no proof of

his performing work benefits in Canada or carrying on business in Canada after such a "clean break"

9 | Page

● took the entirety of his belongings when he left

● sold his vehicle when he left

● three-room, outfitted loft leased for utilization of the entire family

● loft leased because possibilities of finding a reasonable house to buy were not incredible

● the one-year lease makes the house in Canada hard to re-possess without prior warning

● not accessible for his utilization whenever in the year in the wake of leaving

● the close family went out finished

● the second vehicle utilized by family sold when they left

● in IT-221R3, the Canada Revenue Agency demonstrates that intermittent, however not standard, return

visits for individual or business reasons won't be utilized to contend against a "clean break"

● not sensible to anticipate that family members and companions should move to help build up his "clean

break"

● left two Canadian clubs

● joined business clubs in Hungary ("Home page", 2020)

● paid in Hungarian cash

● kept up the financial balance in Hungary

● occupants retained tax from rental payments, as required for payments to non-residents

Non-resident: tax in Canada on Canadian-source income.

Criterion: utilized in Canada or carried on business in Canada after making a "clean break".

Evidence:

● on the off chance that it is built up that he made a "clean break" in 2019, at that point there is no proof of

his performing work benefits in Canada or carrying on business in Canada after such a "clean break"

9 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

● as a non-resident, the rental payments are liable to withholding tax as orchestrated with the

occupants

Conclusion:

● Roman ought to be encouraged to report his pay for 2019 as a section year resident

● the realities seem to gauge all the more intensely right now, not very many huge connections to

Canada remain

● his previous history in Canada isn't deciding

● resources went out and cabin are either not accessible for his utilization or won't

be utilized routinely

● the golf participation isn't deciding; it very well may be utilized when in the midst

of a get-away to recuperate a portion of the advantage of the high inception

expense

● interests in Canada are not deciding; anybody can put resources into Canada as a

non-resident

● there might be an inquiry concerning when in 2011 he turned into a non-resident by

making the "clean break"

● the Schujahn case would propose that the "clean break" happened when he left on

March 1, not when his family left on August 1

● in any case, the CRA's position is that the "clean break" may not happen until the person's

family leaves Canada [IT-221R3, standard. 15]

Question 3 (12 Marks)

Bonnie is a qualified caregiver. Bonnie is registered with Nannies R Us, a personnel agency which

specializes in placing caregivers for temporary work when parents are ill or when regular caregivers

are unavailable. When a client calls Nannies R Us, they indicate their needs and the requirements of

the position. Nannies R Us then goes through their list of available caregivers. They will call those

10 | Page

occupants

Conclusion:

● Roman ought to be encouraged to report his pay for 2019 as a section year resident

● the realities seem to gauge all the more intensely right now, not very many huge connections to

Canada remain

● his previous history in Canada isn't deciding

● resources went out and cabin are either not accessible for his utilization or won't

be utilized routinely

● the golf participation isn't deciding; it very well may be utilized when in the midst

of a get-away to recuperate a portion of the advantage of the high inception

expense

● interests in Canada are not deciding; anybody can put resources into Canada as a

non-resident

● there might be an inquiry concerning when in 2011 he turned into a non-resident by

making the "clean break"

● the Schujahn case would propose that the "clean break" happened when he left on

March 1, not when his family left on August 1

● in any case, the CRA's position is that the "clean break" may not happen until the person's

family leaves Canada [IT-221R3, standard. 15]

Question 3 (12 Marks)

Bonnie is a qualified caregiver. Bonnie is registered with Nannies R Us, a personnel agency which

specializes in placing caregivers for temporary work when parents are ill or when regular caregivers

are unavailable. When a client calls Nannies R Us, they indicate their needs and the requirements of

the position. Nannies R Us then goes through their list of available caregivers. They will call those

10 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

who they believe are most suitable and offer them the work. The caregivers have the choice as to

whether they wish to take the position.

If a caregiver takes the position, they are paid by Nannies R Us at an hourly rate for the work they

perform. Nannies R Us does not take any source deductions (income tax, Canada Pension Plan

premiums, or Employment Insurance premiums) against this income. It is the responsibility of the

caregiver to provide his or her own transportation to and from the position. The hours for the position

are dictated by the client and the client generally provides detailed instructions as to what is to take

place during the duration of the placement. The caregivers are responsible for ensuring that they

keep up to date with emergency health procedures and general childcare issues. To this end, each

caregiver registered with Nannies R Us is required to pay for and attend an annual childcare seminar

as well as one workshop a year which relates to general childcare issues.

Bonnie is currently supplementing her income from Nannies R Us with income from some of her own

clients. She is working two days a week providing childcare to a family of three children. This is

expected to last until the end of the year. She is also working three mornings a week for another

client who is physically impaired and requires general care and attendance. This position is indefinite.

In the past, Bonnie has done housekeeping to supplement her income as required.

Required:

Using the appropriate tests, determine whether Bonnie is an employee or self-employed (an

independent contractor). Be sure to consider both sides of the issue in detail.

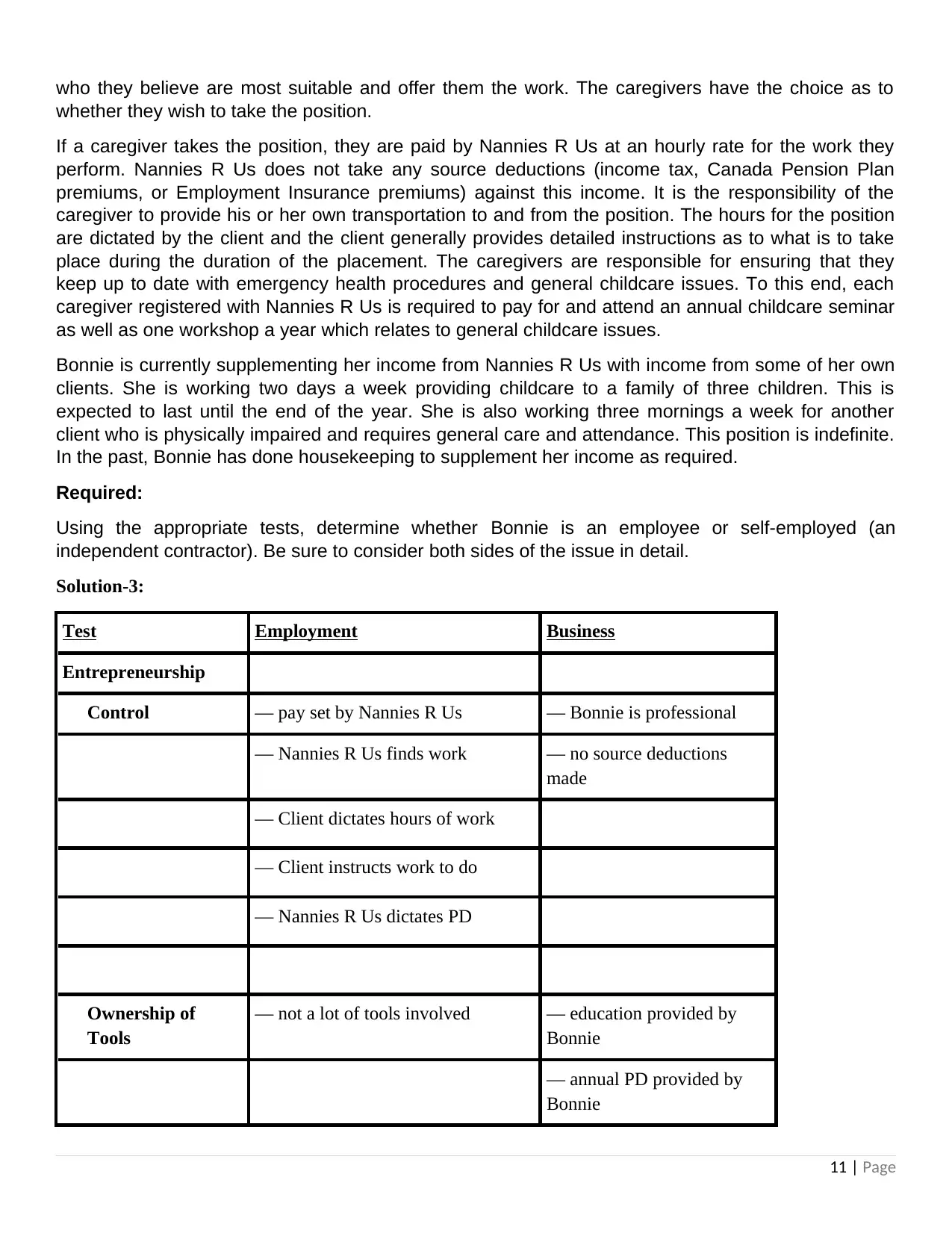

Solution-3:

Test Employment Business

Entrepreneurship

Control — pay set by Nannies R Us — Bonnie is professional

— Nannies R Us finds work — no source deductions

made

— Client dictates hours of work

— Client instructs work to do

— Nannies R Us dictates PD

Ownership of

Tools

— not a lot of tools involved — education provided by

Bonnie

— annual PD provided by

Bonnie

11 | Page

whether they wish to take the position.

If a caregiver takes the position, they are paid by Nannies R Us at an hourly rate for the work they

perform. Nannies R Us does not take any source deductions (income tax, Canada Pension Plan

premiums, or Employment Insurance premiums) against this income. It is the responsibility of the

caregiver to provide his or her own transportation to and from the position. The hours for the position

are dictated by the client and the client generally provides detailed instructions as to what is to take

place during the duration of the placement. The caregivers are responsible for ensuring that they

keep up to date with emergency health procedures and general childcare issues. To this end, each

caregiver registered with Nannies R Us is required to pay for and attend an annual childcare seminar

as well as one workshop a year which relates to general childcare issues.

Bonnie is currently supplementing her income from Nannies R Us with income from some of her own

clients. She is working two days a week providing childcare to a family of three children. This is

expected to last until the end of the year. She is also working three mornings a week for another

client who is physically impaired and requires general care and attendance. This position is indefinite.

In the past, Bonnie has done housekeeping to supplement her income as required.

Required:

Using the appropriate tests, determine whether Bonnie is an employee or self-employed (an

independent contractor). Be sure to consider both sides of the issue in detail.

Solution-3:

Test Employment Business

Entrepreneurship

Control — pay set by Nannies R Us — Bonnie is professional

— Nannies R Us finds work — no source deductions

made

— Client dictates hours of work

— Client instructs work to do

— Nannies R Us dictates PD

Ownership of

Tools

— not a lot of tools involved — education provided by

Bonnie

— annual PD provided by

Bonnie

11 | Page

Chance of Profit/

Risk of Loss

— few expenses involved Nannies R

US

— Nannies R US assumes liabilities

— Bonnie provided

transportation

— Bonnie paid annual PD

costs

Integration — Bonnie can refuse work

Organization Test — Bonnie is not

dependent; she has

other income

Specific Results Test — work is always temporary

Question 4 (10 Marks)

Lennox Lowes was granted, in year one, an option to purchase 50,000 common shares at $1 per

share from her employer, Michael Ltd., a Canadian-controlled private corporation. The shares had an

estimated fair market value at this date of $1.50. However, according to the agreement, Lennox could

not exercise her option until her fourth employment year. Lennox did exercise her entire option in year

five; the fair market value of the shares at that time was $3. Lennox sold all the shares in year six, at

$6 per share.

Required:

Discuss the tax implications of the above transactions.

Solution-4:

At the time of exercise – as a perquisite. When the employee has exercised the option, the difference

between the FMV (on exercise date) and exercise price is taxed as perquisite. The employer deducts TDS

on this perquisite

12 | Page

Risk of Loss

— few expenses involved Nannies R

US

— Nannies R US assumes liabilities

— Bonnie provided

transportation

— Bonnie paid annual PD

costs

Integration — Bonnie can refuse work

Organization Test — Bonnie is not

dependent; she has

other income

Specific Results Test — work is always temporary

Question 4 (10 Marks)

Lennox Lowes was granted, in year one, an option to purchase 50,000 common shares at $1 per

share from her employer, Michael Ltd., a Canadian-controlled private corporation. The shares had an

estimated fair market value at this date of $1.50. However, according to the agreement, Lennox could

not exercise her option until her fourth employment year. Lennox did exercise her entire option in year

five; the fair market value of the shares at that time was $3. Lennox sold all the shares in year six, at

$6 per share.

Required:

Discuss the tax implications of the above transactions.

Solution-4:

At the time of exercise – as a perquisite. When the employee has exercised the option, the difference

between the FMV (on exercise date) and exercise price is taxed as perquisite. The employer deducts TDS

on this perquisite

12 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.