Taxation Assignment: Rental Property, Tax Credits, and Income

VerifiedAdded on 2023/04/20

|14

|1508

|160

Homework Assignment

AI Summary

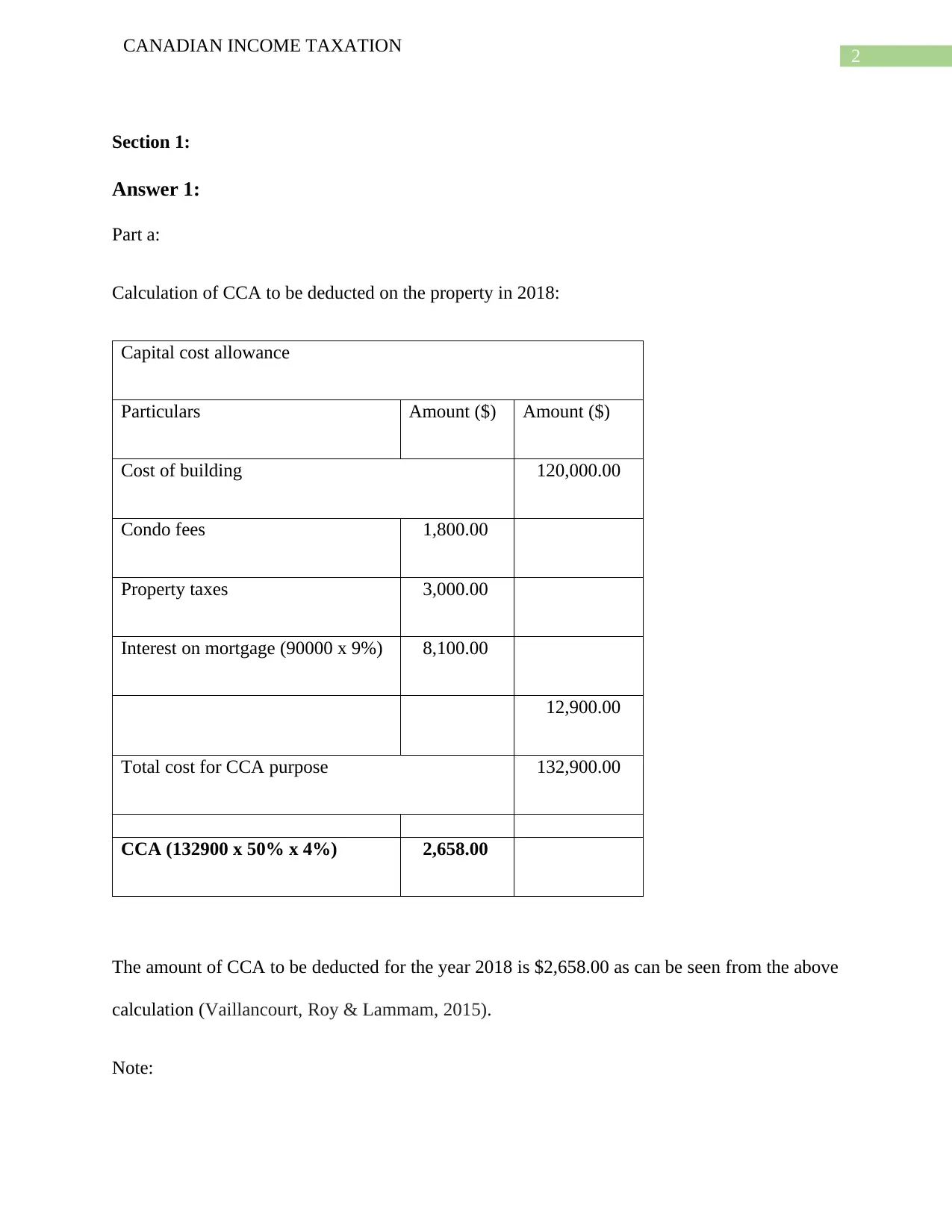

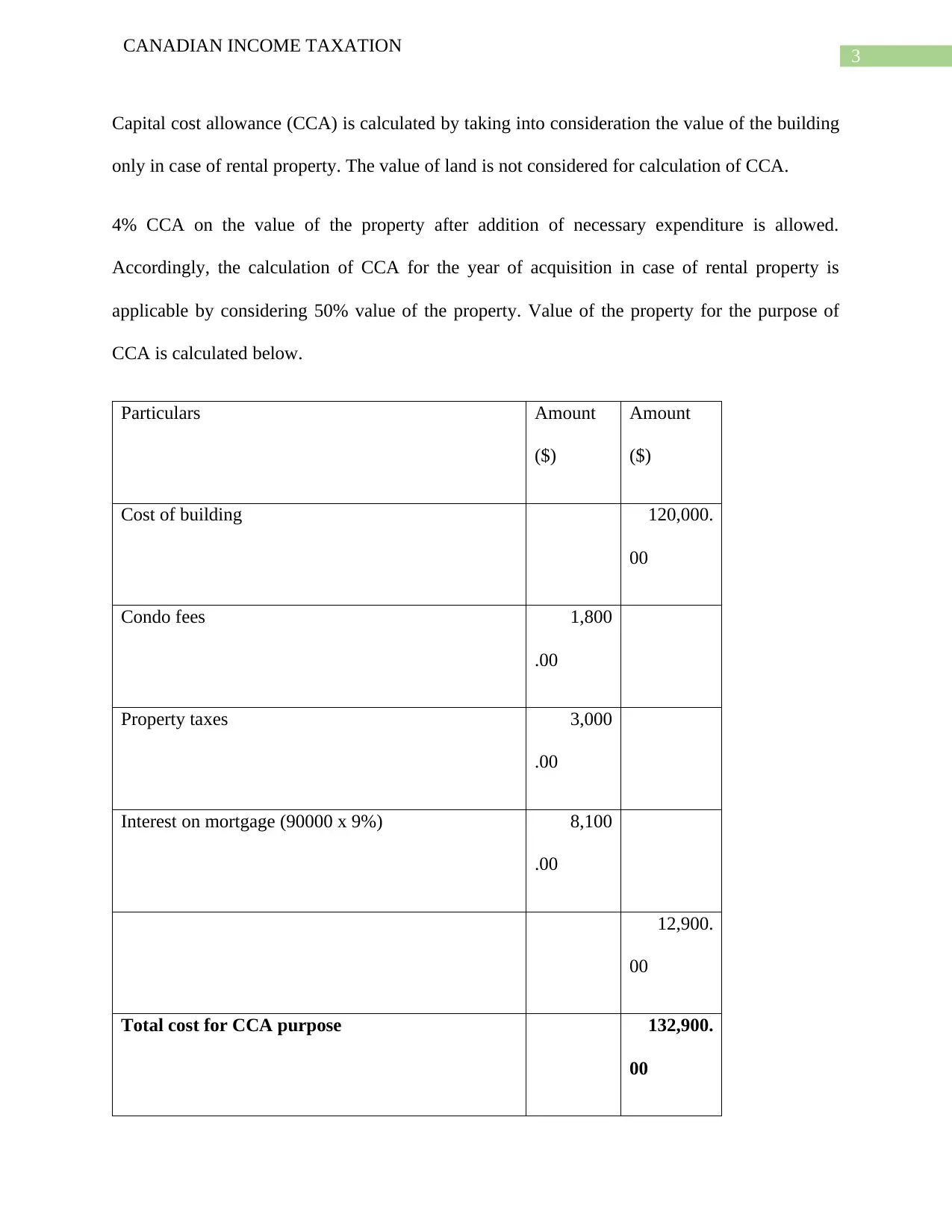

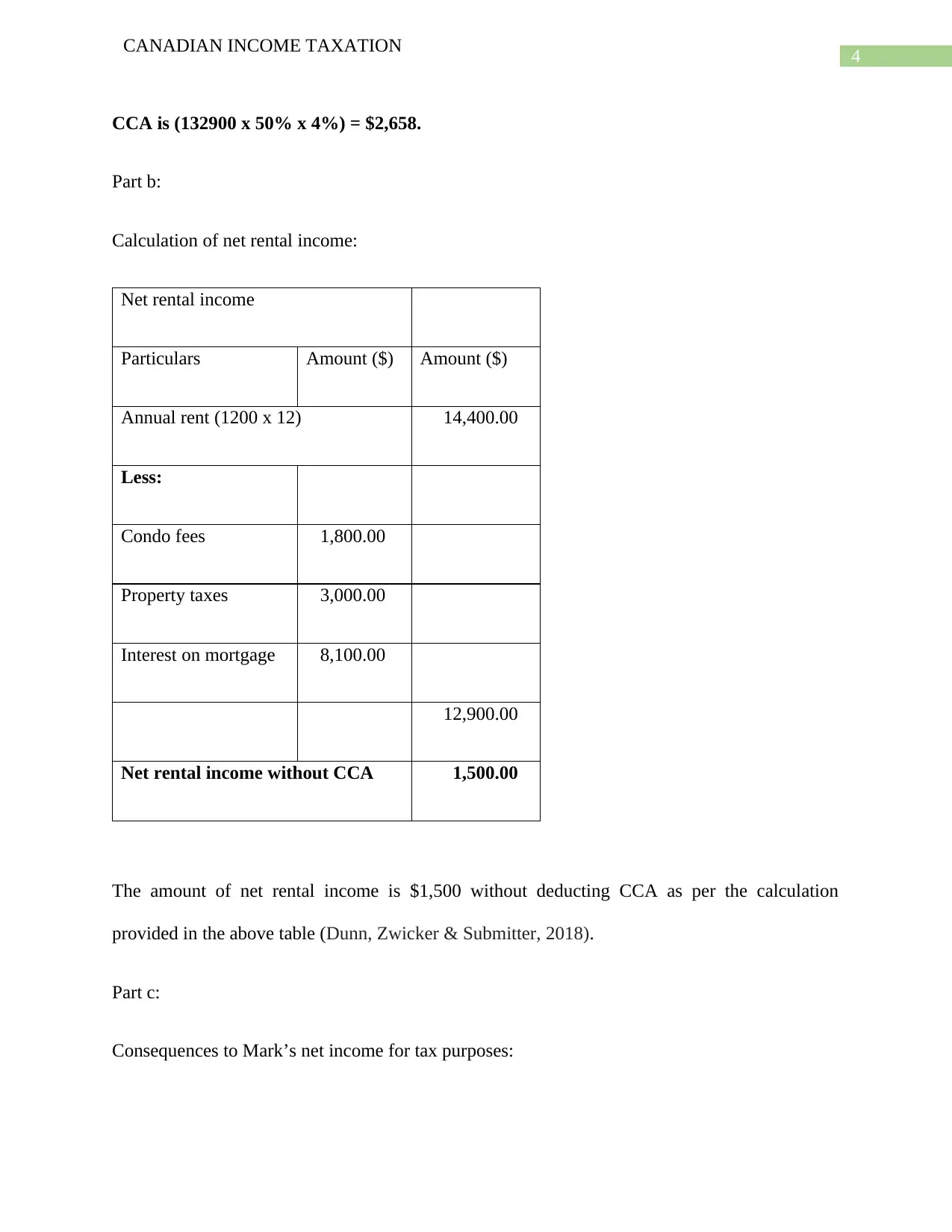

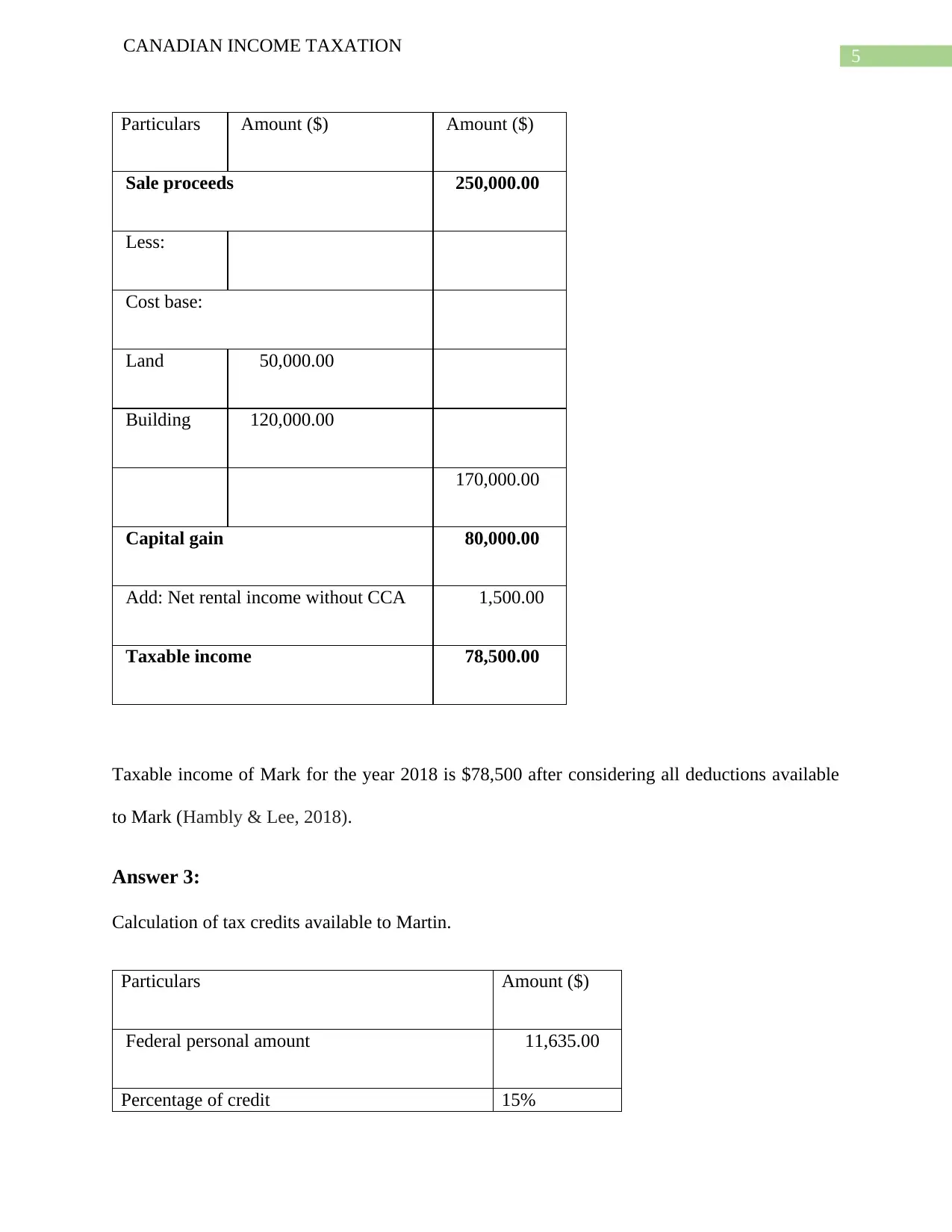

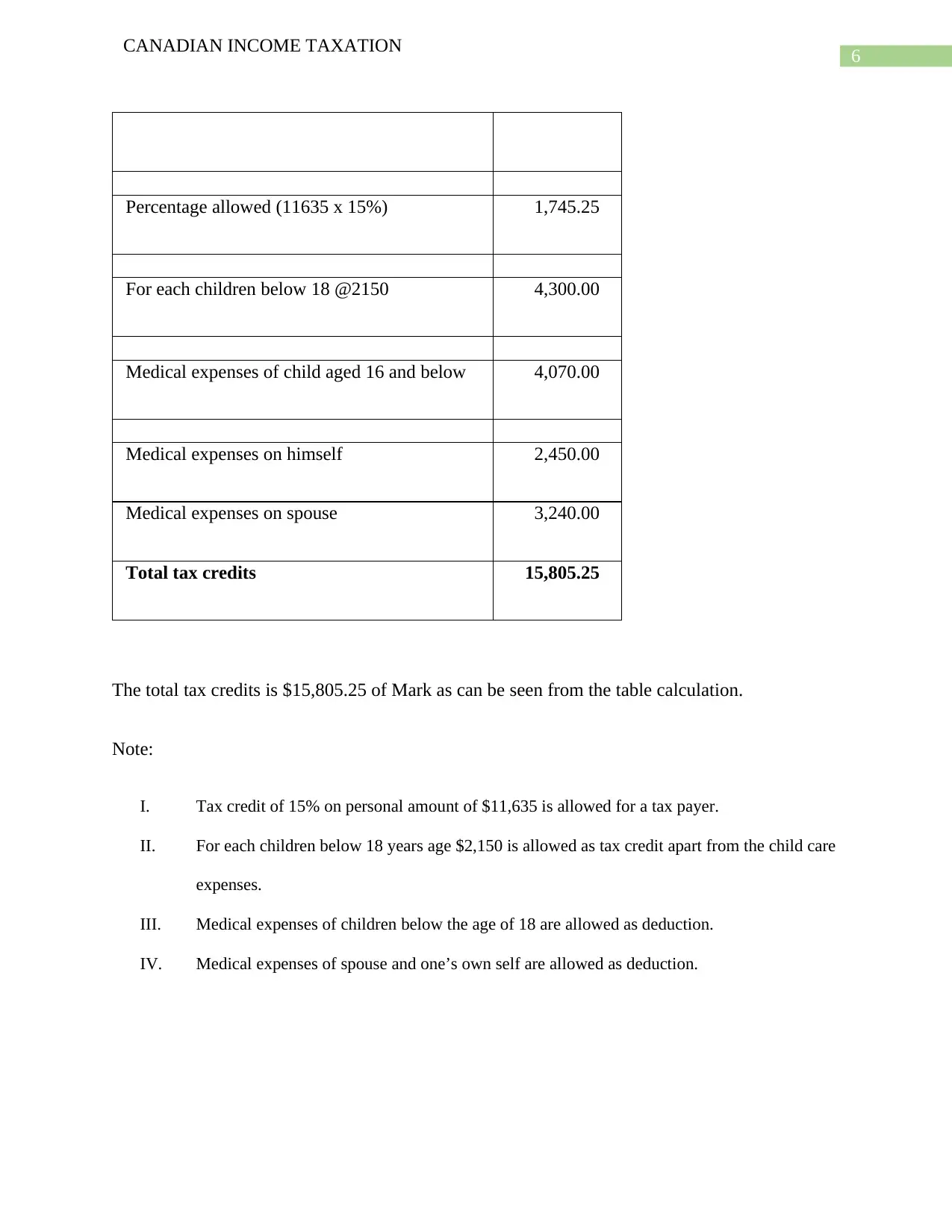

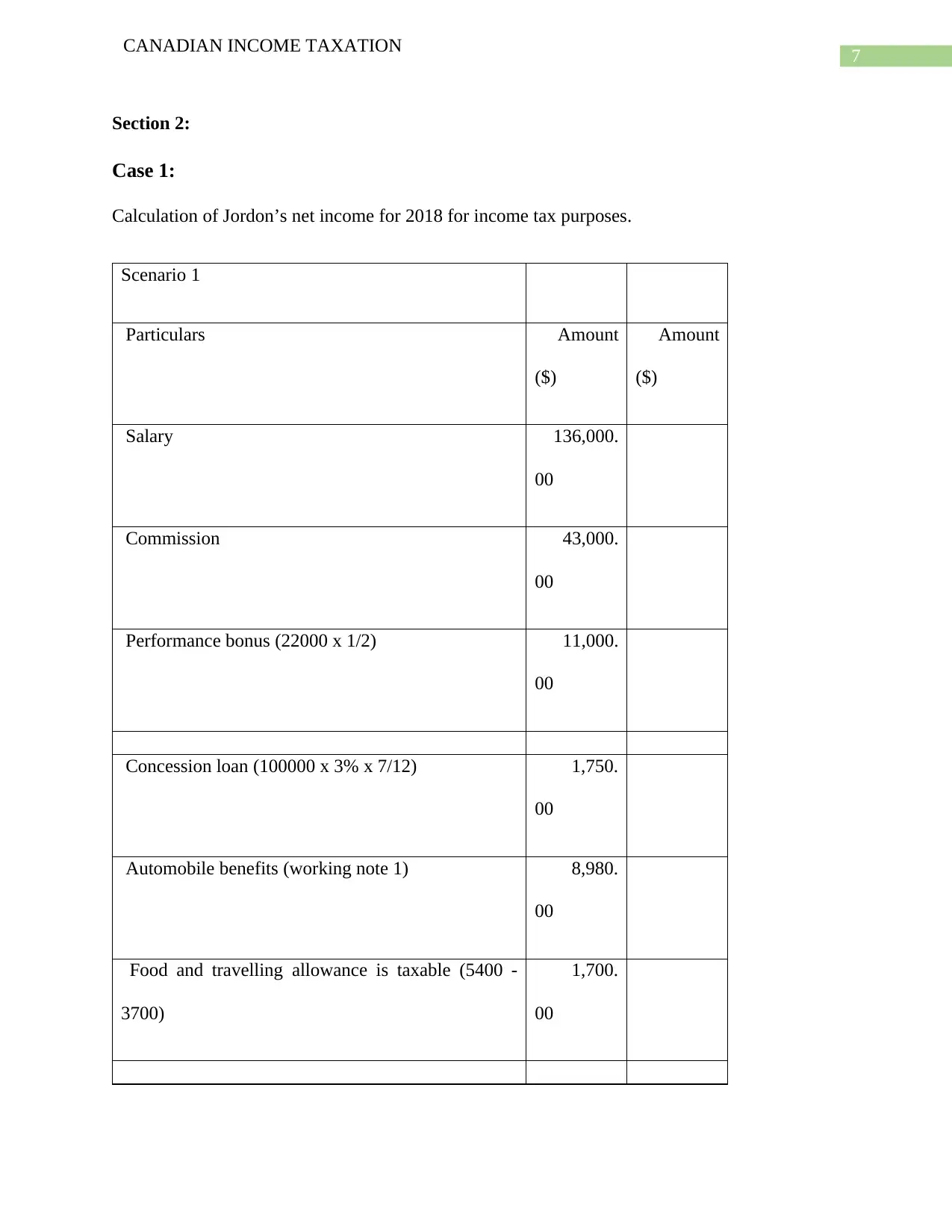

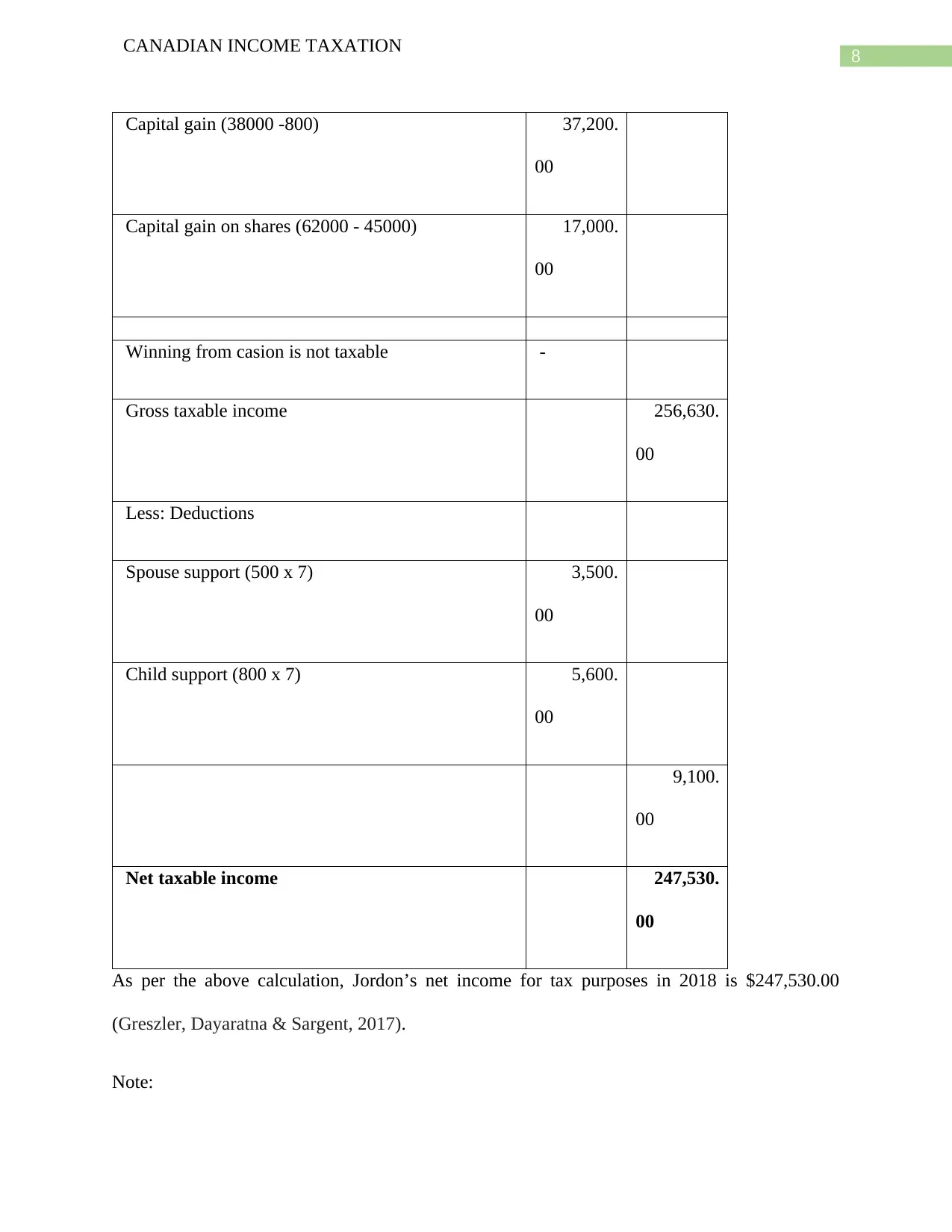

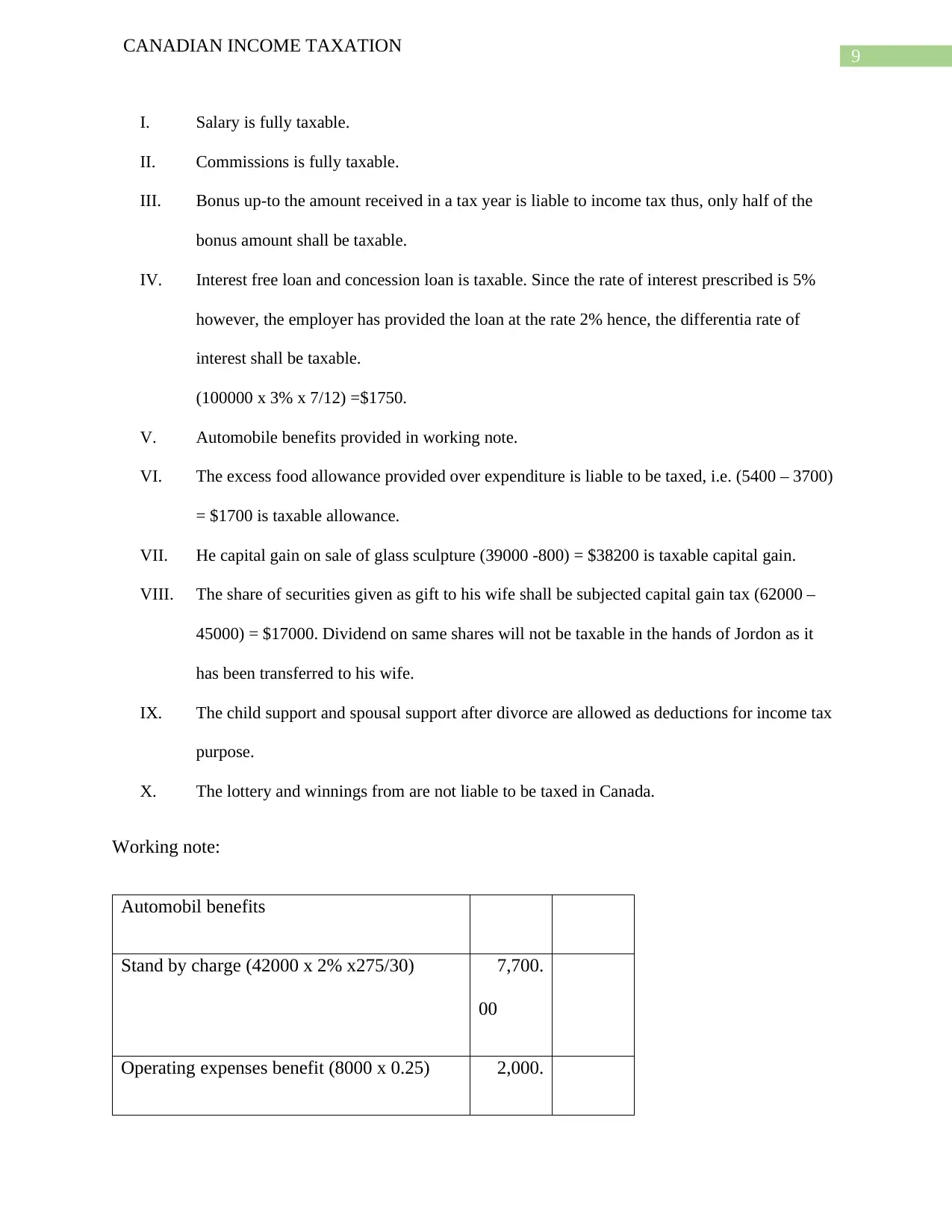

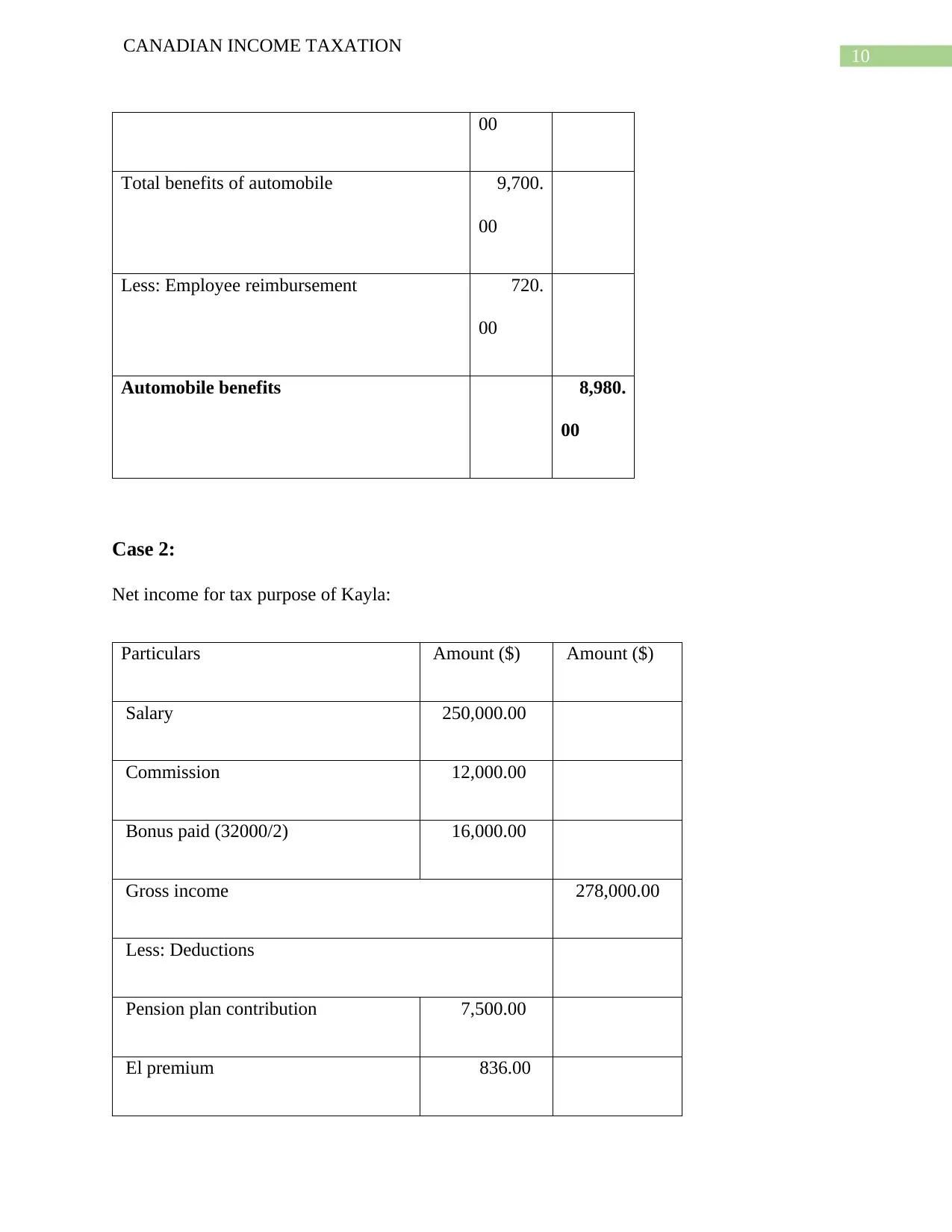

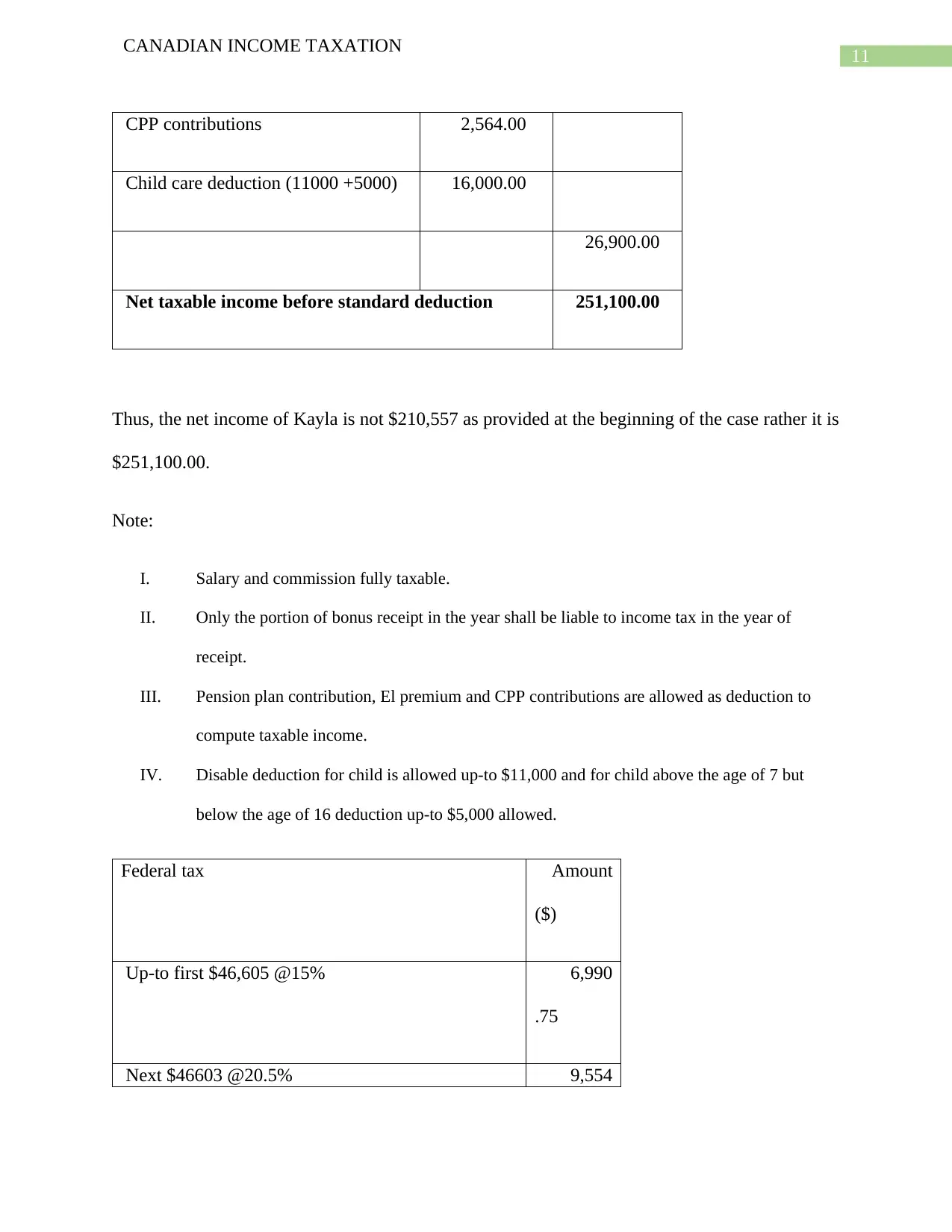

This assignment solution delves into the complexities of Canadian income taxation, presenting detailed calculations for various scenarios. It begins by calculating the Capital Cost Allowance (CCA) and net rental income for a rental property, considering expenses such as condo fees, property taxes, and mortgage interest. The solution then determines the consequences of the property's sale on the owner's net income, including capital gains. Furthermore, the assignment calculates tax credits available to an individual, factoring in personal amounts, child-related credits, and medical expenses. The document also includes calculations of net income for tax purposes in case studies involving employment income, commissions, bonuses, and various deductions like spousal and child support. The assignment explores the taxability of different benefits, such as automobile benefits, and gift allowances, providing a comprehensive overview of Canadian income tax principles.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.