Analysis of Capacity, Bottlenecks, and Contribution Margin for Finance

VerifiedAdded on 2021/06/14

|4

|1460

|78

Report

AI Summary

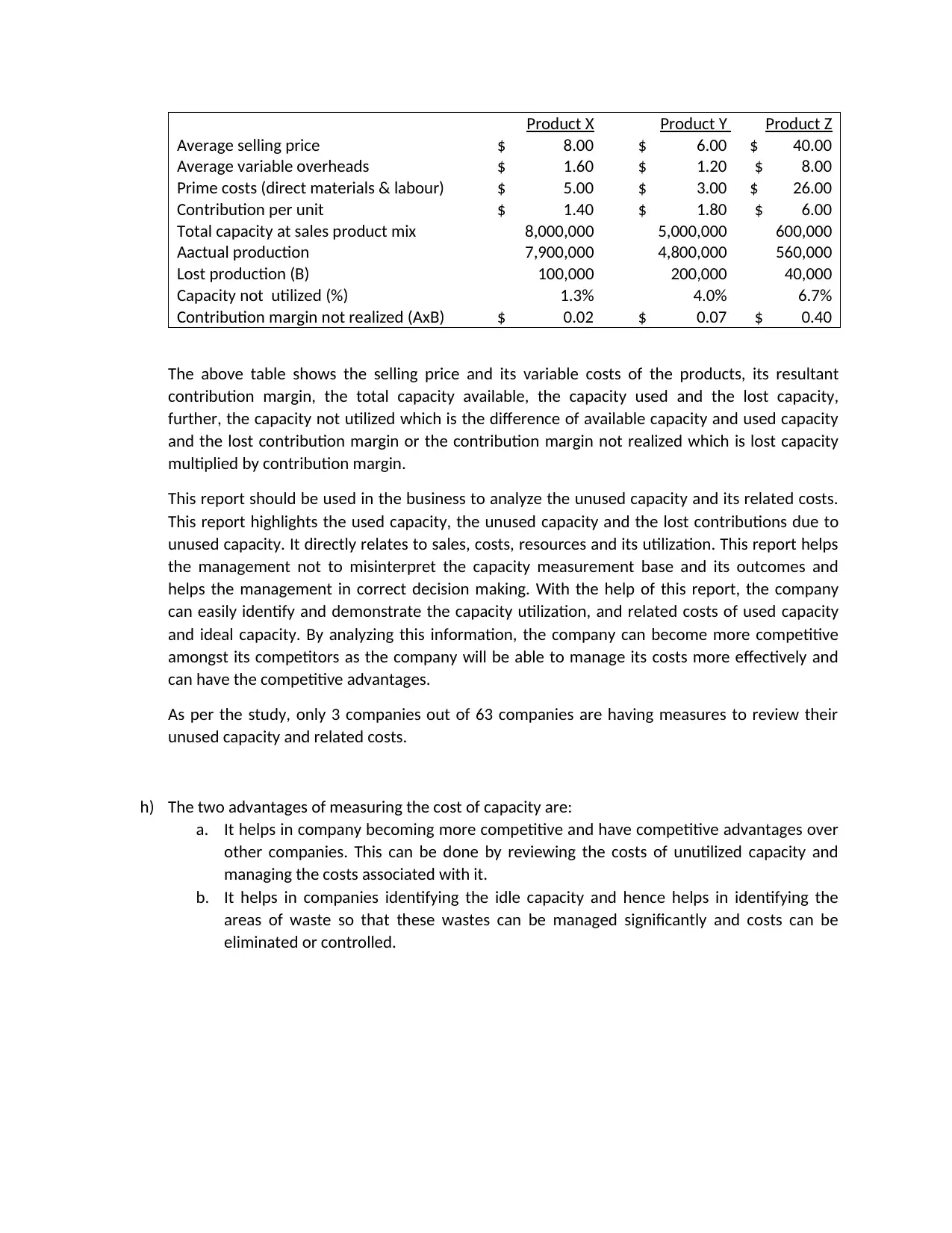

This report provides a comprehensive analysis of capacity management, cost of capacity, and bottlenecks. It defines the cost of capacity as the expenses incurred to increase production capacity, including fixed costs like land, machinery, and labor, and the cost of unused capacity. The report highlights the negative consequences of flawed data in capacity investment decisions, such as increased fixed costs and decreased profits. It differentiates between theoretical and practical capacity, emphasizing the importance of effective capacity management to make informed decisions regarding capacity expansion and resource utilization. The report also explains the concept of bottlenecks and offers solutions that do not require a permanent increase in capacity, like overtime and outsourcing. It includes a schedule of contribution margin not realized, analyzing products X, Y, and Z, highlighting the lost production and unused capacity. The report emphasizes the importance of measuring the cost of capacity to enhance competitiveness and identify areas of waste. The analysis concludes that only a few companies actively measure unused capacity and its associated costs.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.