Strategic Finance Essay: CAPM's Usefulness Despite Assumptions

VerifiedAdded on 2023/06/08

|14

|3395

|171

Essay

AI Summary

This essay provides an overview of the Capital Asset Pricing Model (CAPM), discussing its origins, formula, and underlying assumptions. It examines the model's usefulness in determining asset prices, expected returns, and cost of capital. The essay also addresses criticisms of the CAPM, including its reliance on unrealistic assumptions and its limitations in certain industries. Furthermore, it explores extensions to the CAPM, such as the Fama-French three-factor model, the Intertemporal Capital Asset Pricing Model (ICAPM), and the Consumption Capital Asset Pricing Model (CCAPM). The essay concludes by highlighting the advantages of the CAPM, such as its consideration of systematic risk and its role in empirical research, while also acknowledging its limitations compared to other models.

Running head: CAPITAL ASSET PRICING MODEL 0

Capital Asset Pricing Model

Capital Asset Pricing Model

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPITAL ASSET PRICING MODEL 1

The capital asset pricing model was introduced by the John Litner and the William Sharpe

born in 1965 and 1964 respectively. Thereafter, William Sharpe was the deserving person of

the Nobel Prize in the year 1990. The work is basically developed on the model of the mean

variance model and the model of the portfolio choice. The development of the model is the

ultimate creation of the capital asset pricing model. The investors consider the factor of how

their wealth will vary with future variables and the income, the prices of the consumption of

the goods and the nature of the portfolio opportunities and therefore the CAPM model was

introduced in order to bring the clarification. The base of the CAPM model was that not all

type of risk shall affect the prices of the assets (Barberis, Greenwood, Jin and Shleifer, 2015).

The model that describes the relationship between the expected risk of return and systematic

risk of the assets which are particularly assets is known as the capital asset pricing model.

The major role of the CAPM model is to determine the pricing of the risky securities,

generate the expected returns and also acts a key driver in calculating the cost of capital. The

general ideology behind the CAPM model is that the investors need two forms of

compensation (Sumalatha and Santhi, 2017). This model is termed as the time value of

money and assessment of risk. The CAPM model is determined through the equation which

is determined below.

Ra

Rf + Ba (Rm -

Rf)

Rf = Risk free rate

Ba =

Beta of the

security

Rm = Expected market return

The capital asset pricing model was introduced by the John Litner and the William Sharpe

born in 1965 and 1964 respectively. Thereafter, William Sharpe was the deserving person of

the Nobel Prize in the year 1990. The work is basically developed on the model of the mean

variance model and the model of the portfolio choice. The development of the model is the

ultimate creation of the capital asset pricing model. The investors consider the factor of how

their wealth will vary with future variables and the income, the prices of the consumption of

the goods and the nature of the portfolio opportunities and therefore the CAPM model was

introduced in order to bring the clarification. The base of the CAPM model was that not all

type of risk shall affect the prices of the assets (Barberis, Greenwood, Jin and Shleifer, 2015).

The model that describes the relationship between the expected risk of return and systematic

risk of the assets which are particularly assets is known as the capital asset pricing model.

The major role of the CAPM model is to determine the pricing of the risky securities,

generate the expected returns and also acts a key driver in calculating the cost of capital. The

general ideology behind the CAPM model is that the investors need two forms of

compensation (Sumalatha and Santhi, 2017). This model is termed as the time value of

money and assessment of risk. The CAPM model is determined through the equation which

is determined below.

Ra

Rf + Ba (Rm -

Rf)

Rf = Risk free rate

Ba =

Beta of the

security

Rm = Expected market return

CAPITAL ASSET PRICING MODEL 2

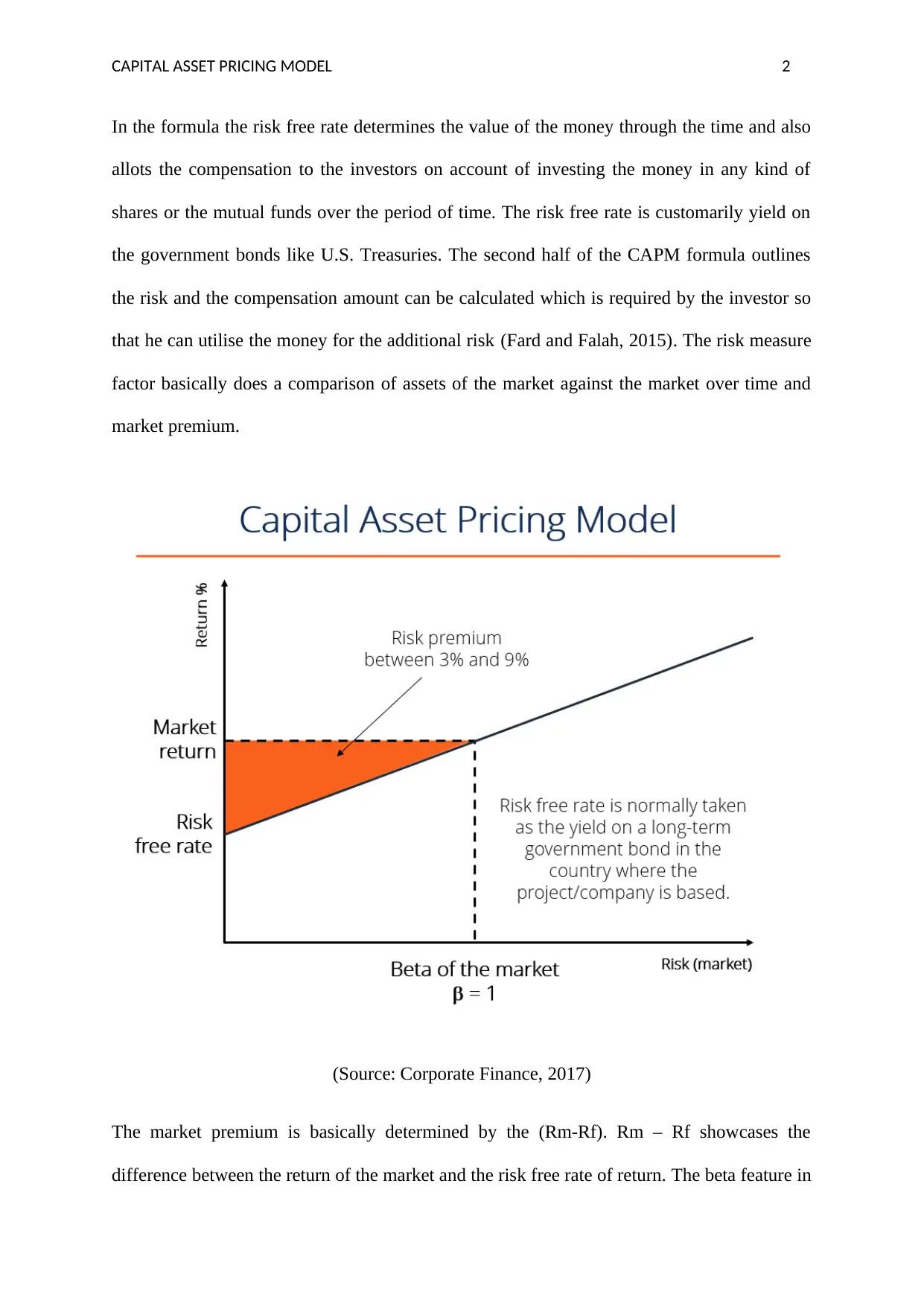

In the formula the risk free rate determines the value of the money through the time and also

allots the compensation to the investors on account of investing the money in any kind of

shares or the mutual funds over the period of time. The risk free rate is customarily yield on

the government bonds like U.S. Treasuries. The second half of the CAPM formula outlines

the risk and the compensation amount can be calculated which is required by the investor so

that he can utilise the money for the additional risk (Fard and Falah, 2015). The risk measure

factor basically does a comparison of assets of the market against the market over time and

market premium.

(Source: Corporate Finance, 2017)

The market premium is basically determined by the (Rm-Rf). Rm – Rf showcases the

difference between the return of the market and the risk free rate of return. The beta feature in

In the formula the risk free rate determines the value of the money through the time and also

allots the compensation to the investors on account of investing the money in any kind of

shares or the mutual funds over the period of time. The risk free rate is customarily yield on

the government bonds like U.S. Treasuries. The second half of the CAPM formula outlines

the risk and the compensation amount can be calculated which is required by the investor so

that he can utilise the money for the additional risk (Fard and Falah, 2015). The risk measure

factor basically does a comparison of assets of the market against the market over time and

market premium.

(Source: Corporate Finance, 2017)

The market premium is basically determined by the (Rm-Rf). Rm – Rf showcases the

difference between the return of the market and the risk free rate of return. The beta feature in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPITAL ASSET PRICING MODEL 3

this formula reflects the risk factor of an asset with the total risk of the market and the volatile

nature of the asset can also be assessed easily (Bao, Diks and Li, 2018). The main purpose of

the formula is to explicitly determine the correlation between the two above factors.

For example the risk free rate of return is 3%, and the beta value of the stock is 3. The

expected market return over the period is 12%, therefore the market risk premium is (12-3)

which is 9% after getting the difference of the risk free rate of return and the expected market

return.

If all the figures are plugged in than the expected return of the stock is 0.29 or 29%

0.03 + [3*(0.12-0.03)]

There are certain assumptions of the CAPM which are as follows. The CAPM model was

extended by Markowitz which was initially introduced. He put forward his argument that the

investors are risk taker investors. The investment made by the investors is basically the

choice between a portfolio by having a trade-off between the risk and the return for the one

investment period (Fernandez, 2015). The investors choose those portfolios that present the

low variance and provide the specific expected return and therefore the model is known as

Markowitz model.

this formula reflects the risk factor of an asset with the total risk of the market and the volatile

nature of the asset can also be assessed easily (Bao, Diks and Li, 2018). The main purpose of

the formula is to explicitly determine the correlation between the two above factors.

For example the risk free rate of return is 3%, and the beta value of the stock is 3. The

expected market return over the period is 12%, therefore the market risk premium is (12-3)

which is 9% after getting the difference of the risk free rate of return and the expected market

return.

If all the figures are plugged in than the expected return of the stock is 0.29 or 29%

0.03 + [3*(0.12-0.03)]

There are certain assumptions of the CAPM which are as follows. The CAPM model was

extended by Markowitz which was initially introduced. He put forward his argument that the

investors are risk taker investors. The investment made by the investors is basically the

choice between a portfolio by having a trade-off between the risk and the return for the one

investment period (Fernandez, 2015). The investors choose those portfolios that present the

low variance and provide the specific expected return and therefore the model is known as

Markowitz model.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPITAL ASSET PRICING MODEL 4

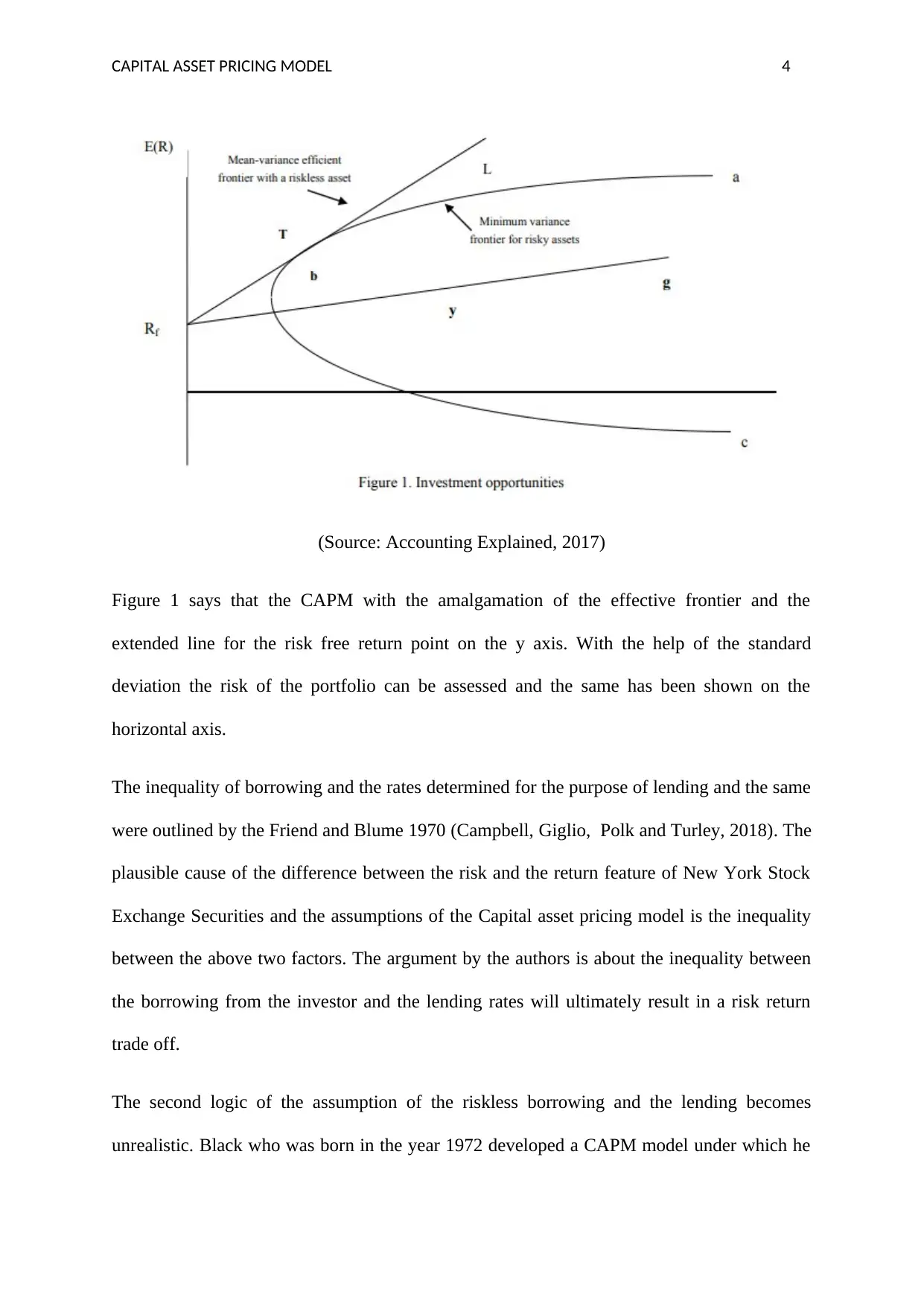

(Source: Accounting Explained, 2017)

Figure 1 says that the CAPM with the amalgamation of the effective frontier and the

extended line for the risk free return point on the y axis. With the help of the standard

deviation the risk of the portfolio can be assessed and the same has been shown on the

horizontal axis.

The inequality of borrowing and the rates determined for the purpose of lending and the same

were outlined by the Friend and Blume 1970 (Campbell, Giglio, Polk and Turley, 2018). The

plausible cause of the difference between the risk and the return feature of New York Stock

Exchange Securities and the assumptions of the Capital asset pricing model is the inequality

between the above two factors. The argument by the authors is about the inequality between

the borrowing from the investor and the lending rates will ultimately result in a risk return

trade off.

The second logic of the assumption of the riskless borrowing and the lending becomes

unrealistic. Black who was born in the year 1972 developed a CAPM model under which he

(Source: Accounting Explained, 2017)

Figure 1 says that the CAPM with the amalgamation of the effective frontier and the

extended line for the risk free return point on the y axis. With the help of the standard

deviation the risk of the portfolio can be assessed and the same has been shown on the

horizontal axis.

The inequality of borrowing and the rates determined for the purpose of lending and the same

were outlined by the Friend and Blume 1970 (Campbell, Giglio, Polk and Turley, 2018). The

plausible cause of the difference between the risk and the return feature of New York Stock

Exchange Securities and the assumptions of the Capital asset pricing model is the inequality

between the above two factors. The argument by the authors is about the inequality between

the borrowing from the investor and the lending rates will ultimately result in a risk return

trade off.

The second logic of the assumption of the riskless borrowing and the lending becomes

unrealistic. Black who was born in the year 1972 developed a CAPM model under which he

CAPITAL ASSET PRICING MODEL 5

did not include the above assumption. His idea of setting up the portfolio is that the mean

variance efficient portfolio can be obtained with the help of the short selling of the risky

assets (Fan, Furger and Xiu, 2016).

Again the next assumption of the CAPM model was the divisibility of all the financial assets

fully where the investors have the choice to buy and sell as much more or less securities they

wanted to. Moreover the time period of the selling of the securities was also not fixed and the

same was sold at the market price. Shahzad, S.J.H., Khalid, S. and Ameer, S., (2016)

The major difference between the model of the Sharpe and the linter against the Black was

that in case of the Sharpe-Linter the return was the return is free from the interest but in case

of the Black the return allows the premium and the beta of the market to be positive. Yet the

assumptions made by the Black were also unrealistic in nature. The efficient portfolio does

not exist because there is no risky asset and no unrestricted shorts selling of the risky asset

and therefore there is lack of relationship between the market beta and CAPM. Therefore the

CAPM model is based on the different assumptions (Mazzola and Gerace, 2015).

1 The expected returns on the underlying assets are linearly related to their

respective betas

2 The premium beta tends to be positive under which the expected return

on the market exceeds the expected return

3 Assets are unrelated with the expected return of the market portfolio

did not include the above assumption. His idea of setting up the portfolio is that the mean

variance efficient portfolio can be obtained with the help of the short selling of the risky

assets (Fan, Furger and Xiu, 2016).

Again the next assumption of the CAPM model was the divisibility of all the financial assets

fully where the investors have the choice to buy and sell as much more or less securities they

wanted to. Moreover the time period of the selling of the securities was also not fixed and the

same was sold at the market price. Shahzad, S.J.H., Khalid, S. and Ameer, S., (2016)

The major difference between the model of the Sharpe and the linter against the Black was

that in case of the Sharpe-Linter the return was the return is free from the interest but in case

of the Black the return allows the premium and the beta of the market to be positive. Yet the

assumptions made by the Black were also unrealistic in nature. The efficient portfolio does

not exist because there is no risky asset and no unrestricted shorts selling of the risky asset

and therefore there is lack of relationship between the market beta and CAPM. Therefore the

CAPM model is based on the different assumptions (Mazzola and Gerace, 2015).

1 The expected returns on the underlying assets are linearly related to their

respective betas

2 The premium beta tends to be positive under which the expected return

on the market exceeds the expected return

3 Assets are unrelated with the expected return of the market portfolio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPITAL ASSET PRICING MODEL 6

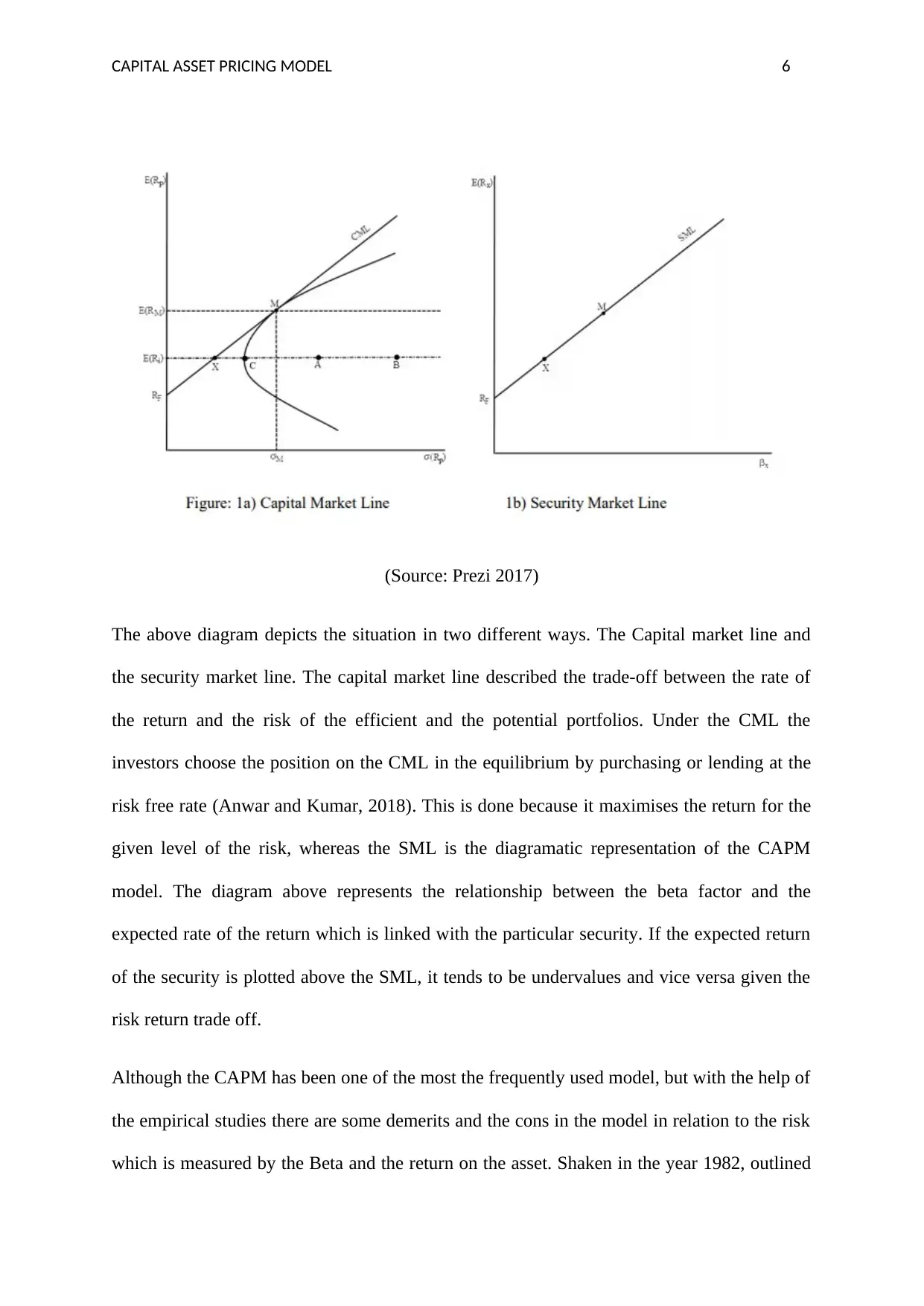

(Source: Prezi 2017)

The above diagram depicts the situation in two different ways. The Capital market line and

the security market line. The capital market line described the trade-off between the rate of

the return and the risk of the efficient and the potential portfolios. Under the CML the

investors choose the position on the CML in the equilibrium by purchasing or lending at the

risk free rate (Anwar and Kumar, 2018). This is done because it maximises the return for the

given level of the risk, whereas the SML is the diagramatic representation of the CAPM

model. The diagram above represents the relationship between the beta factor and the

expected rate of the return which is linked with the particular security. If the expected return

of the security is plotted above the SML, it tends to be undervalues and vice versa given the

risk return trade off.

Although the CAPM has been one of the most the frequently used model, but with the help of

the empirical studies there are some demerits and the cons in the model in relation to the risk

which is measured by the Beta and the return on the asset. Shaken in the year 1982, outlined

(Source: Prezi 2017)

The above diagram depicts the situation in two different ways. The Capital market line and

the security market line. The capital market line described the trade-off between the rate of

the return and the risk of the efficient and the potential portfolios. Under the CML the

investors choose the position on the CML in the equilibrium by purchasing or lending at the

risk free rate (Anwar and Kumar, 2018). This is done because it maximises the return for the

given level of the risk, whereas the SML is the diagramatic representation of the CAPM

model. The diagram above represents the relationship between the beta factor and the

expected rate of the return which is linked with the particular security. If the expected return

of the security is plotted above the SML, it tends to be undervalues and vice versa given the

risk return trade off.

Although the CAPM has been one of the most the frequently used model, but with the help of

the empirical studies there are some demerits and the cons in the model in relation to the risk

which is measured by the Beta and the return on the asset. Shaken in the year 1982, outlined

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPITAL ASSET PRICING MODEL 7

his argument on the fact that CAPM model is not truly testable. According to different

investors in the year after 1982, the CAPM model was found as non-testable unless the

market portfolios of all the assets are used in the empirical test (Bendob, Chikhi and

Bennaceur, 2017).

The CAPM has been criticized in many researches and the observations because of the major

assumptions which rely on the two features which are risk free borrowing and lending.

Furthermore, according to the Fama and French there are specific industries for which the

CAPM model did not work at all. The estimates for the cost of equity capital are covered with

errors of more than 3.5% per year. The estimates are not accurate for individual firms and the

projects. There are certain unrealistic assumptions, because of which the CAPM fails due to

the factors for example one period investment, unrestricted risk free borrowing and lending

(Xiao, Faff, Gharghori and Min, 2017)

There are several extensions to the CAPM model from the one it was introduced. The journey

of the CAPM through different versions is states below. Fama and French propose the third

model named as the three factor model. In their model there was an addition of the two

factors such which enhanced the CAPM model in a better manner. The critical factor that

helps to run the three factor model is the size and the market equity. However, at times the

market risk is also considered. Empirically, they provide evidence on the covariance. The

covariance of the small firms is literally high and in case of the large firms the case is reverse.

Further, the stocks are measured by the book to the market ratio (Ready Ratios, 2016).

Merton introduced the ICAPM model in the year 1973. Merton’s inter temporal capital asset

pricing model is an extension of the CAPM. The ICAPM has a different version of the

assumption about the objectives of the investor. Under this CAPM model, investors are

concerned only about the wealth which is obtained by the portfolio at the end of the current

his argument on the fact that CAPM model is not truly testable. According to different

investors in the year after 1982, the CAPM model was found as non-testable unless the

market portfolios of all the assets are used in the empirical test (Bendob, Chikhi and

Bennaceur, 2017).

The CAPM has been criticized in many researches and the observations because of the major

assumptions which rely on the two features which are risk free borrowing and lending.

Furthermore, according to the Fama and French there are specific industries for which the

CAPM model did not work at all. The estimates for the cost of equity capital are covered with

errors of more than 3.5% per year. The estimates are not accurate for individual firms and the

projects. There are certain unrealistic assumptions, because of which the CAPM fails due to

the factors for example one period investment, unrestricted risk free borrowing and lending

(Xiao, Faff, Gharghori and Min, 2017)

There are several extensions to the CAPM model from the one it was introduced. The journey

of the CAPM through different versions is states below. Fama and French propose the third

model named as the three factor model. In their model there was an addition of the two

factors such which enhanced the CAPM model in a better manner. The critical factor that

helps to run the three factor model is the size and the market equity. However, at times the

market risk is also considered. Empirically, they provide evidence on the covariance. The

covariance of the small firms is literally high and in case of the large firms the case is reverse.

Further, the stocks are measured by the book to the market ratio (Ready Ratios, 2016).

Merton introduced the ICAPM model in the year 1973. Merton’s inter temporal capital asset

pricing model is an extension of the CAPM. The ICAPM has a different version of the

assumption about the objectives of the investor. Under this CAPM model, investors are

concerned only about the wealth which is obtained by the portfolio at the end of the current

CAPITAL ASSET PRICING MODEL 8

year. But under the ICAPM model the renewed version of the CAPM model the investors and

the stakeholders care about not only the end of the period pay off but also the future

possibilities and the opportunities to consume or invest this pay off. The investors consider

the factor of how their wealth will fluctuate with future variables and the income, the prices

of the consumption of the goods and the nature of the portfolio opportunities (Prezi. 2017).

Lucas who introduced the model in the year 1978 extended the traditional CAPM into the

CCAPM commonly known as the Consumption Capital Asset Pricing Model. This model

describes the direct relationship between the consumption and the stock returns and therefore

it relies upon the aggregate consumption in order to have an analysis and the understanding

of the future asset prices unlike the traditional CAPM Model which links the market’s

portfolio return (Finance Formulas, 2016).

The CAPM model has the numerous advantages over the other methods of calculating the

return and the advantages will surely explain why it has been popular for more than 40 years.

The best feature of the CAPM model is that it considers only the systematic risk and reflects

the reality in which major number of the investors has a wide range of the portfolios from

which the unsystematic risk has been totally eliminated and eradicated.

The CAPM model is the theoretical equation between the required rate of return and the

systematic risk which has been forwarded for the purpose of the future empirical research and

the testing procedures (Accounting Explained, 2017).

In terms of the calculation of the cost of the equity the CAPM model is considered better than

the Dividend Growth Model as it explicitly considers the platform of the systematic risk in

association with the entire stock market.

year. But under the ICAPM model the renewed version of the CAPM model the investors and

the stakeholders care about not only the end of the period pay off but also the future

possibilities and the opportunities to consume or invest this pay off. The investors consider

the factor of how their wealth will fluctuate with future variables and the income, the prices

of the consumption of the goods and the nature of the portfolio opportunities (Prezi. 2017).

Lucas who introduced the model in the year 1978 extended the traditional CAPM into the

CCAPM commonly known as the Consumption Capital Asset Pricing Model. This model

describes the direct relationship between the consumption and the stock returns and therefore

it relies upon the aggregate consumption in order to have an analysis and the understanding

of the future asset prices unlike the traditional CAPM Model which links the market’s

portfolio return (Finance Formulas, 2016).

The CAPM model has the numerous advantages over the other methods of calculating the

return and the advantages will surely explain why it has been popular for more than 40 years.

The best feature of the CAPM model is that it considers only the systematic risk and reflects

the reality in which major number of the investors has a wide range of the portfolios from

which the unsystematic risk has been totally eliminated and eradicated.

The CAPM model is the theoretical equation between the required rate of return and the

systematic risk which has been forwarded for the purpose of the future empirical research and

the testing procedures (Accounting Explained, 2017).

In terms of the calculation of the cost of the equity the CAPM model is considered better than

the Dividend Growth Model as it explicitly considers the platform of the systematic risk in

association with the entire stock market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CAPITAL ASSET PRICING MODEL 9

Moreover many investors argue that this model is superior to the Wacc model in providing

the discount rates for the appraisal and the appreciation of the investment in the near future.

There are certain problems in applying the CAPM model which have been outlined below.

The first assumption of the model is to assume that the risk factor has the predictable

relationship with respect to the return. The major issue arise when the volatility of the market

is set at 1 and the higher volatility of the Beta id larger than one. For example if the value of

the Beta is 3 the security price shifts three times as far as the market and if the value of the

beta is 0.75 than the price moves only 3/4th (Wall Street oasis, 2016).

Secondly the model suggests that the variance of the return is the sole measurement of the

risk. But when compared to the other models, in case of the financial statements the variance

is not the only factor, rather it is considered as the probability of the losing and moreover it is

asymmetric in nature.

According to this model the all the investors whether the active or the potential the CAPM

model comes up with the dubious assumption that market of the securities is made up of only

one kind of the investors and every investor requires the same information and analyses the

securities in the same manner. The assumption of the homogeneity is the biggest rival of the

CAPM model itself (Valueadder.com, 2017).

The model also comes up with another kind of the problem that both the active and potential

shareholders will prefer the lower risk but in reality the situation is totally opposite and the

problem occurs in applying the CAPM model (Lai and Stohs, 2015).

The conclusion says that the first angel revealed the ex-ante perspective and suggested the

similar yields of the similar amounts of the risk being priced and on the other hand the second

angle was the so-called ex post which revealed that the ex-ante price of the total risk is a

Moreover many investors argue that this model is superior to the Wacc model in providing

the discount rates for the appraisal and the appreciation of the investment in the near future.

There are certain problems in applying the CAPM model which have been outlined below.

The first assumption of the model is to assume that the risk factor has the predictable

relationship with respect to the return. The major issue arise when the volatility of the market

is set at 1 and the higher volatility of the Beta id larger than one. For example if the value of

the Beta is 3 the security price shifts three times as far as the market and if the value of the

beta is 0.75 than the price moves only 3/4th (Wall Street oasis, 2016).

Secondly the model suggests that the variance of the return is the sole measurement of the

risk. But when compared to the other models, in case of the financial statements the variance

is not the only factor, rather it is considered as the probability of the losing and moreover it is

asymmetric in nature.

According to this model the all the investors whether the active or the potential the CAPM

model comes up with the dubious assumption that market of the securities is made up of only

one kind of the investors and every investor requires the same information and analyses the

securities in the same manner. The assumption of the homogeneity is the biggest rival of the

CAPM model itself (Valueadder.com, 2017).

The model also comes up with another kind of the problem that both the active and potential

shareholders will prefer the lower risk but in reality the situation is totally opposite and the

problem occurs in applying the CAPM model (Lai and Stohs, 2015).

The conclusion says that the first angel revealed the ex-ante perspective and suggested the

similar yields of the similar amounts of the risk being priced and on the other hand the second

angle was the so-called ex post which revealed that the ex-ante price of the total risk is a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CAPITAL ASSET PRICING MODEL 10

function of the revised ex post price. These assumptions are not supportive to the paradigm. It

follows directly from the CAOM;s own assumption that if in the situation of the equilibrium

the investors price only the non-diversifiable risks then the fair ex ante price for the total risk

of the asset shall be eventually higher. Therefore from the above essay in my opinion though

the model started to establish itself around 40 years ago there are certain critiques and the

problems in applying the CAPM model correctly to determine the rate of return. Hence, the

investors may consider other models as well to get a variance of the model and the

comparative analysis so that they can invest accordingly.

function of the revised ex post price. These assumptions are not supportive to the paradigm. It

follows directly from the CAOM;s own assumption that if in the situation of the equilibrium

the investors price only the non-diversifiable risks then the fair ex ante price for the total risk

of the asset shall be eventually higher. Therefore from the above essay in my opinion though

the model started to establish itself around 40 years ago there are certain critiques and the

problems in applying the CAPM model correctly to determine the rate of return. Hence, the

investors may consider other models as well to get a variance of the model and the

comparative analysis so that they can invest accordingly.

CAPITAL ASSET PRICING MODEL 11

References

Accounting Explained, (2017) what is Capital Asset Pricing Model (CAPM)? [Online]

Available from https://accountingexplained.com/capital/equity-valuation/capital-asset-

pricing-model [Accessed on 4th September 2018]

Anwar, M. and Kumar, S., (2018) Sectoral Robustness of Asset Pricing Models: Evidence

from the Indian Capital Market. Indian Journal of Commerce and Management Studies, 9(2),

pp.42-50.

Bao, T., Diks, C. and Li, H., (2018) A generalized CAPM model with asymmetric power

distributed errors with an application to portfolio construction. Economic Modelling, 68,

pp.611-621.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., (2015) X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Bendob, A., Chikhi, M. and Bennaceur, F., (2017) Testing the CAPM-GARCH Models in the

GCC-Wide Equity Sectors. Asian Journal of Economic Modelling, 5(4), pp.413-430.

Campbell, J.Y., Giglio, S., Polk, C. and Turley, R., (2018) An intertemporal CAPM with

stochastic volatility. Journal of Financial Economics, 128(2), pp.207-233.

Fan, J., Furger, A. and Xiu, D., (2016) Incorporating global industrial classification standard

into portfolio allocation: A simple factor-based large covariance matrix estimator with high-

frequency data. Journal of Business & Economic Statistics, 34(4), pp.489-503.

Fard, H.V. and Falah, A.B., (2015) A New Modified CAPM Model: The Two Beta

CAPM. Jurnal UMP Social Sciences and Technology Management Vol, 3(1).

References

Accounting Explained, (2017) what is Capital Asset Pricing Model (CAPM)? [Online]

Available from https://accountingexplained.com/capital/equity-valuation/capital-asset-

pricing-model [Accessed on 4th September 2018]

Anwar, M. and Kumar, S., (2018) Sectoral Robustness of Asset Pricing Models: Evidence

from the Indian Capital Market. Indian Journal of Commerce and Management Studies, 9(2),

pp.42-50.

Bao, T., Diks, C. and Li, H., (2018) A generalized CAPM model with asymmetric power

distributed errors with an application to portfolio construction. Economic Modelling, 68,

pp.611-621.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., (2015) X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Bendob, A., Chikhi, M. and Bennaceur, F., (2017) Testing the CAPM-GARCH Models in the

GCC-Wide Equity Sectors. Asian Journal of Economic Modelling, 5(4), pp.413-430.

Campbell, J.Y., Giglio, S., Polk, C. and Turley, R., (2018) An intertemporal CAPM with

stochastic volatility. Journal of Financial Economics, 128(2), pp.207-233.

Fan, J., Furger, A. and Xiu, D., (2016) Incorporating global industrial classification standard

into portfolio allocation: A simple factor-based large covariance matrix estimator with high-

frequency data. Journal of Business & Economic Statistics, 34(4), pp.489-503.

Fard, H.V. and Falah, A.B., (2015) A New Modified CAPM Model: The Two Beta

CAPM. Jurnal UMP Social Sciences and Technology Management Vol, 3(1).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.