Management Accounting Report: Capital Bedrooms and Kitchen, Unit 5

VerifiedAdded on 2023/01/13

|13

|984

|26

Report

AI Summary

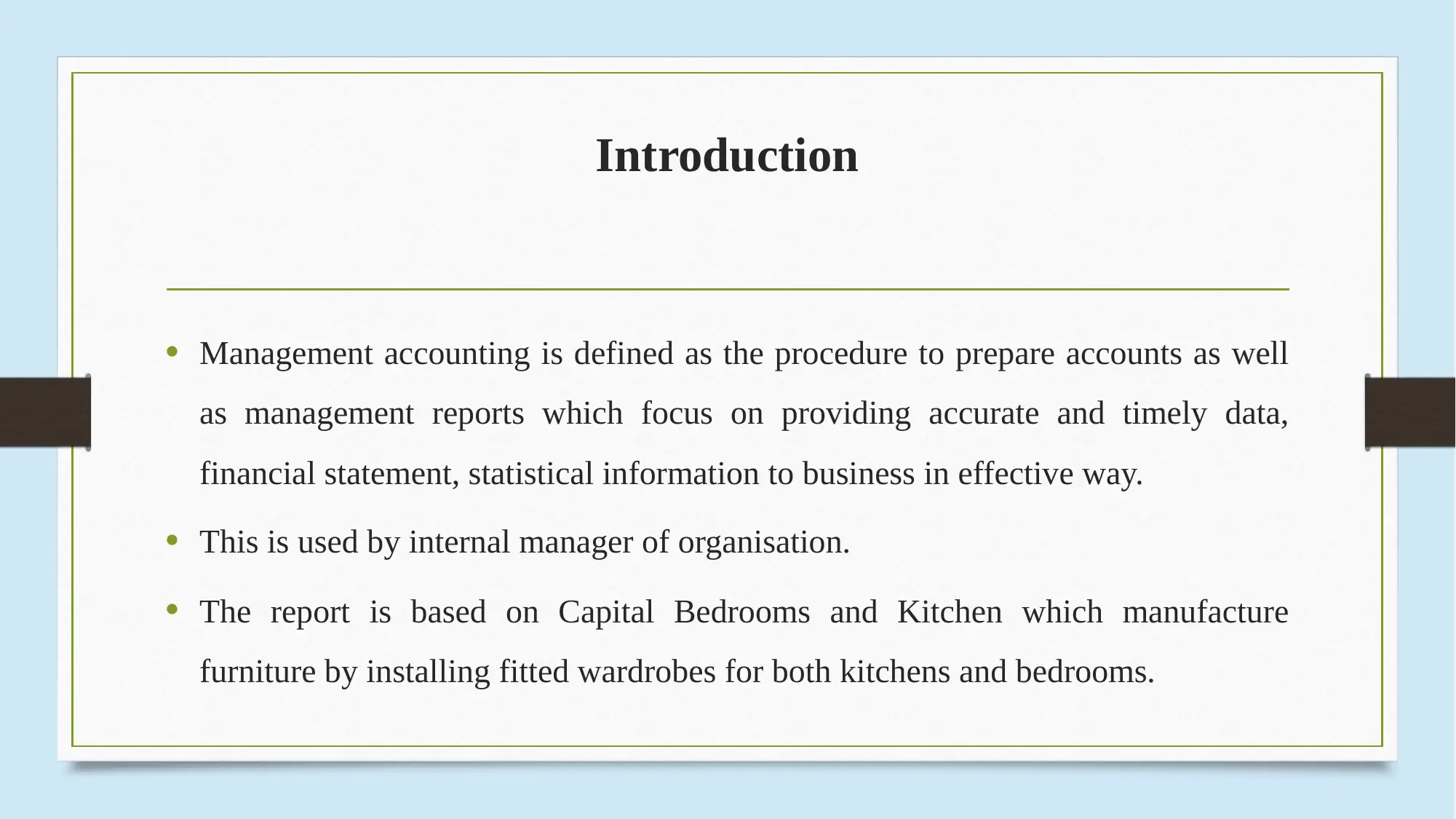

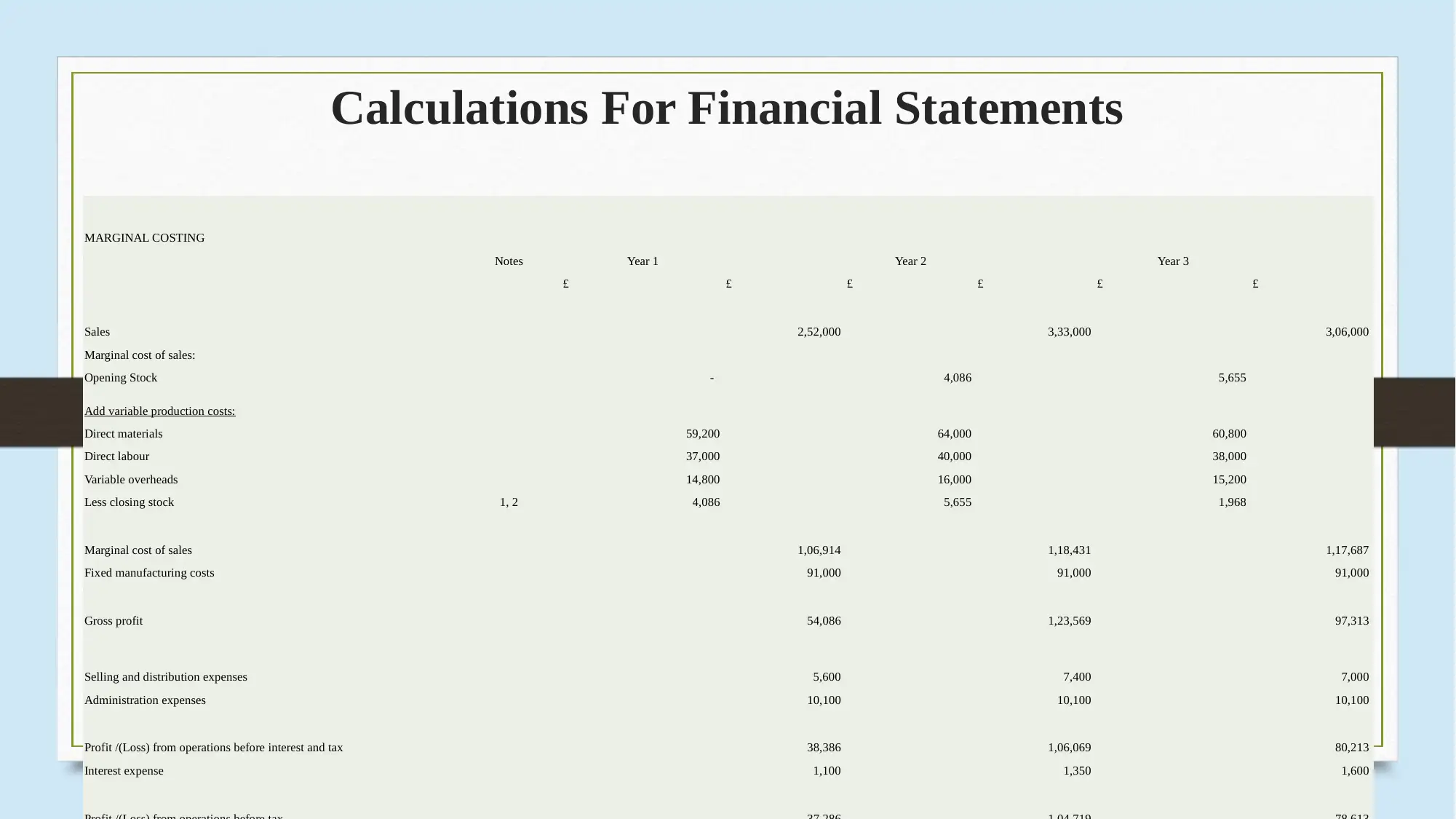

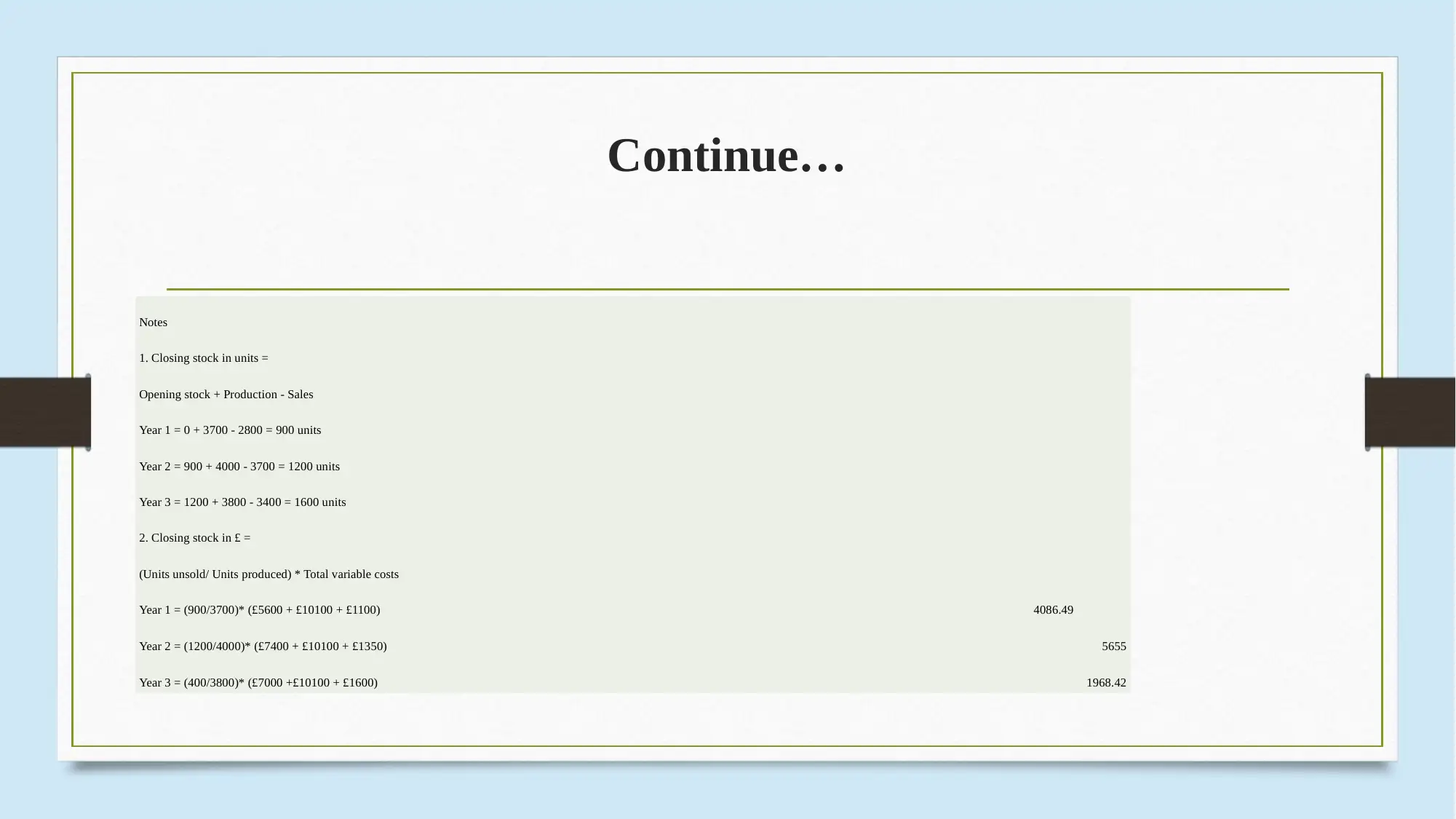

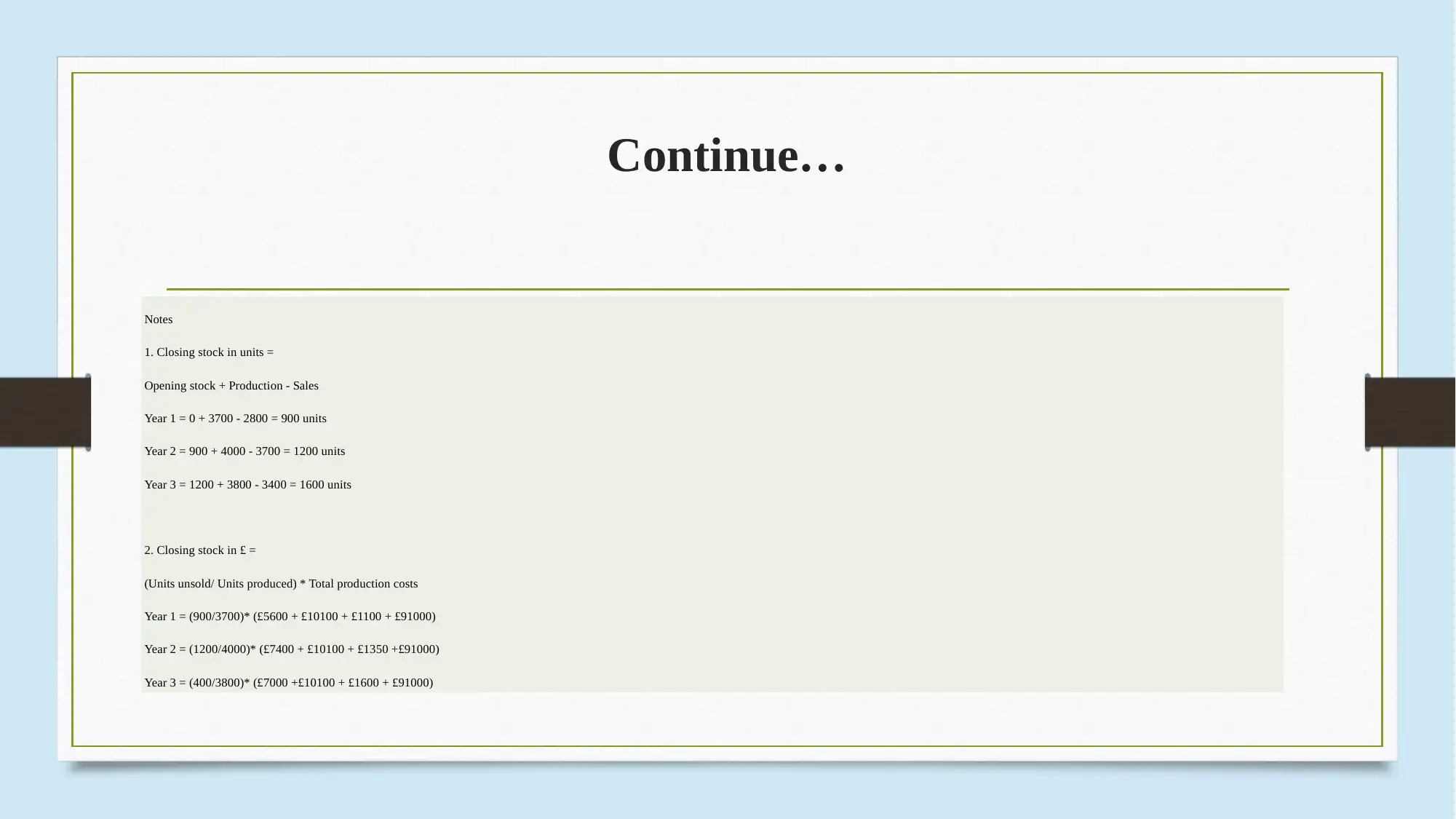

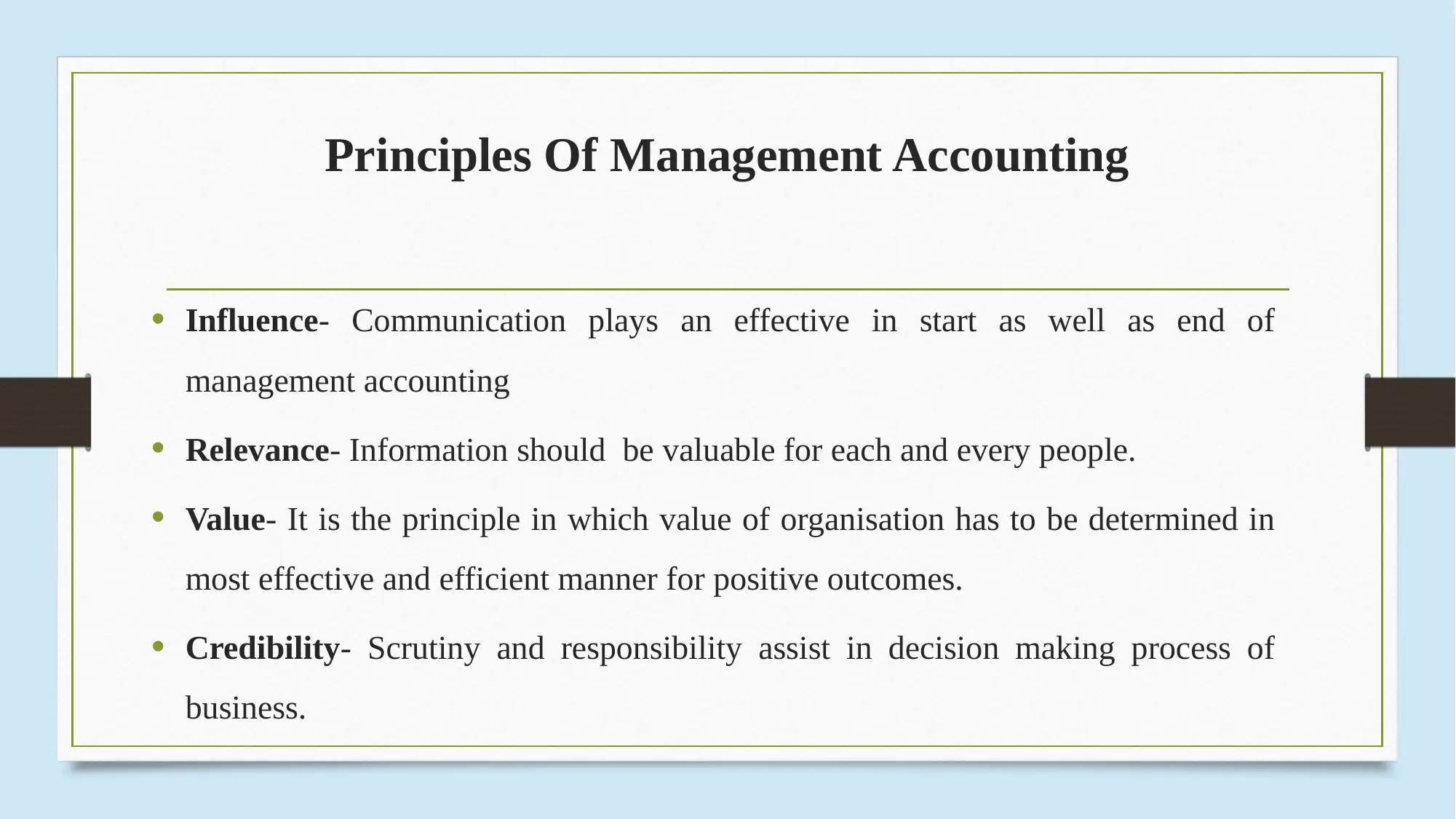

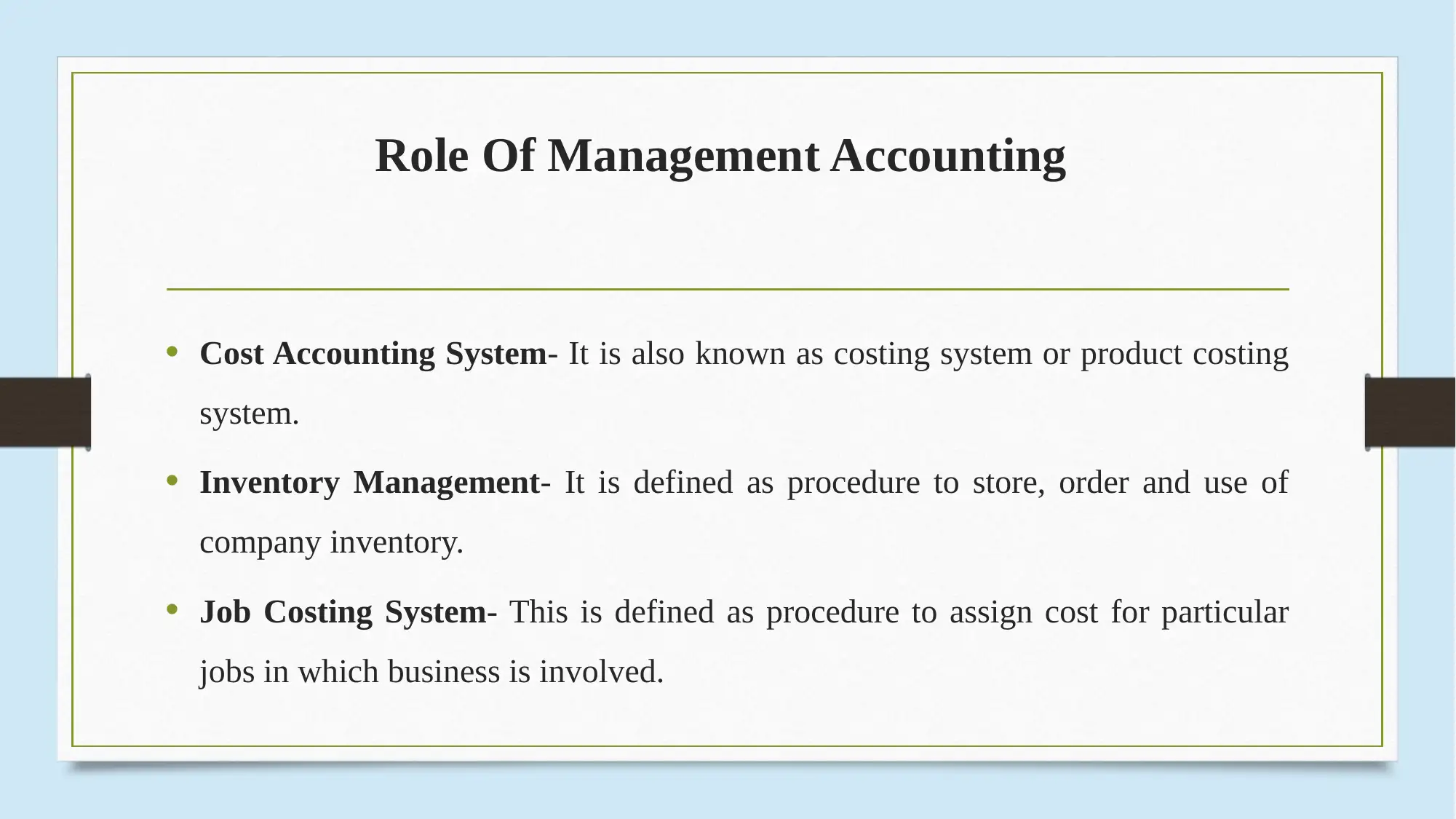

This report provides a comprehensive overview of management accounting principles, focusing on the financial analysis of Capital Bedrooms and Kitchen. It begins with an introduction to management accounting, its purpose, and its application within an organization. The report then delves into detailed calculations for financial statements using both marginal and absorption costing methods over a three-year period. It includes notes explaining the calculations for closing stock in both costing methods. Furthermore, the report explores key principles of management accounting, emphasizing influence, relevance, value, and credibility. It highlights the role of management accounting in cost accounting systems, inventory management, and job costing systems. The report also discusses the methods used, including marginal and absorption costing, and examines how management accounting is integrated within an organization to support decision-making and price setting. Finally, it outlines the benefits of management accounting, such as reducing costs and maximizing profitability, and concludes with a summary of the key takeaways. The report also provides references to support its findings.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.