Financial Analysis of Proposed Machine Investment Project

VerifiedAdded on 2021/12/20

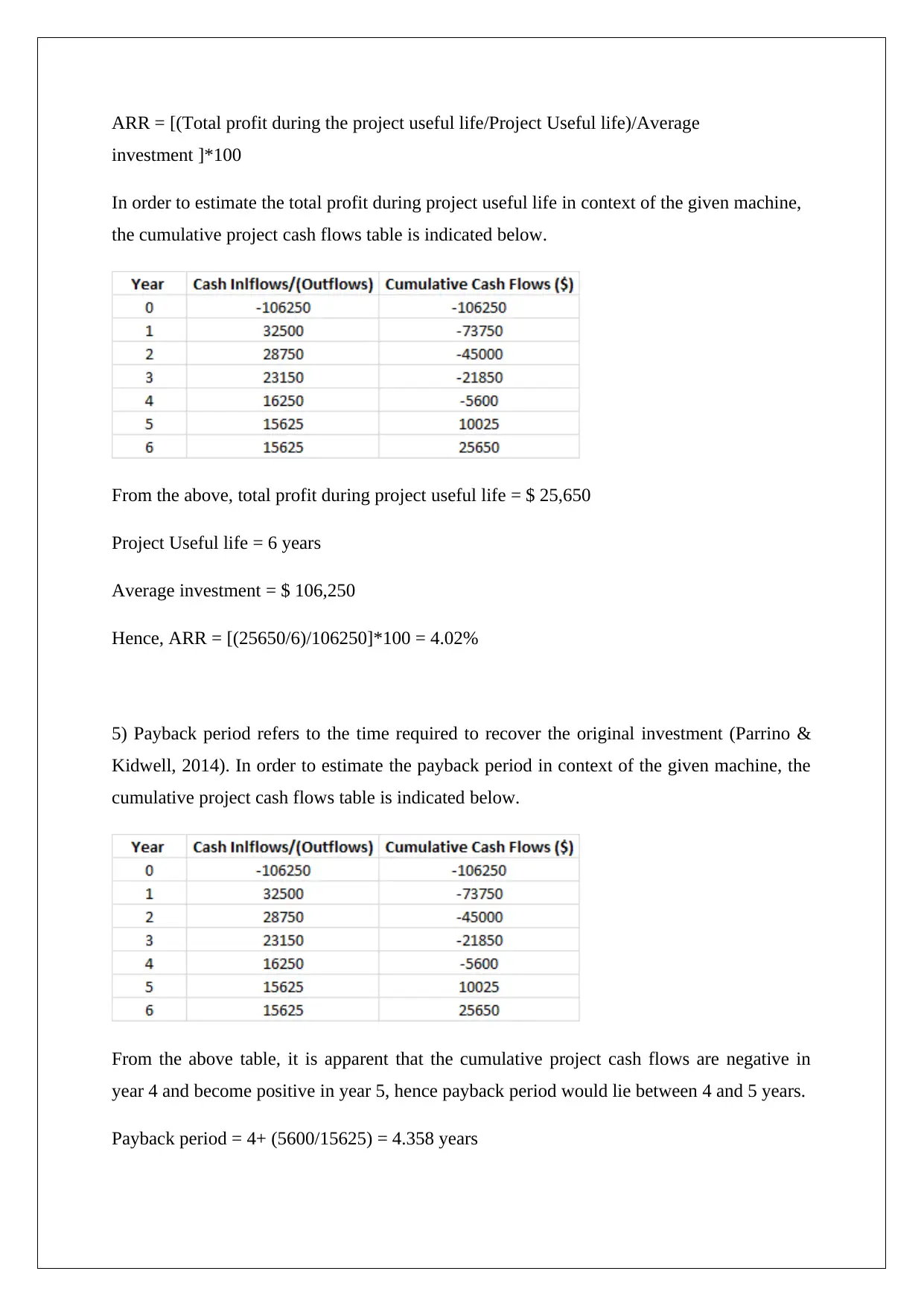

|6

|1253

|36

Homework Assignment

AI Summary

This assignment provides a comprehensive financial analysis of a proposed machine investment. It begins by identifying and mitigating potential risks such as increased cost of capital and uncertain future cash flows using sensitivity and scenario analysis. The analysis includes a detailed cash flow timeline and calculates the annual depreciation expense. The core of the assignment involves calculating key capital budgeting metrics including the Accounting Rate of Return (ARR), payback period, Net Present Value (NPV), and Internal Rate of Return (IRR). Based on these calculations, the assignment concludes with a recommendation on whether or not to invest in the proposed machinery, justifying the decision based on the financial feasibility of the project. The impact of depreciation on cash flows, including its indirect influence via the tax shield, is also discussed. The assignment also highlights the need for additional information, such as the inclusion of tax in project cash flows and the incorporation of depreciation tax shield within cash flows, to make a well-informed investment decision.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.