Managerial Finance: Project Evaluation and Capital Budgeting Analysis

VerifiedAdded on 2021/06/17

|8

|1285

|22

Homework Assignment

AI Summary

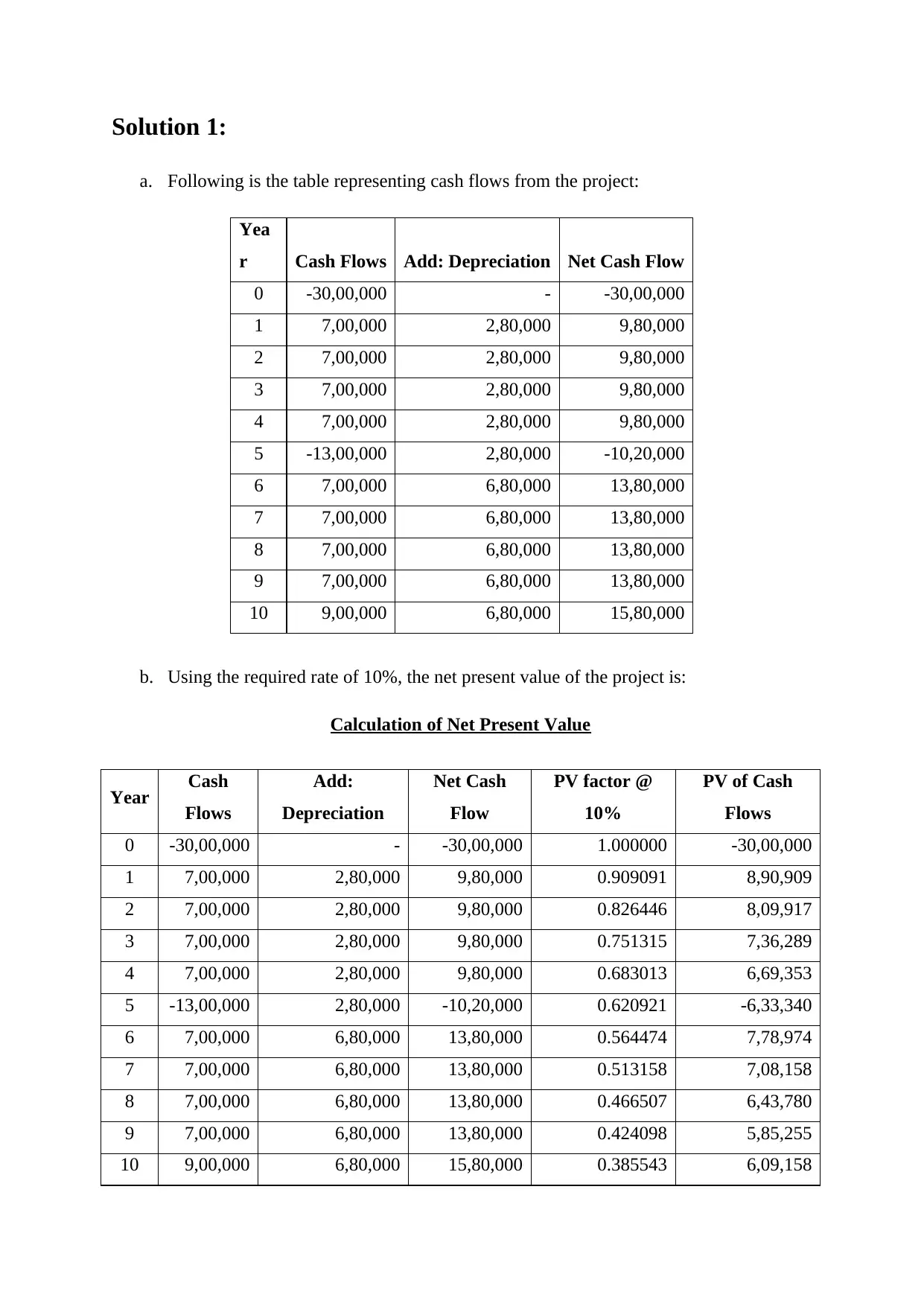

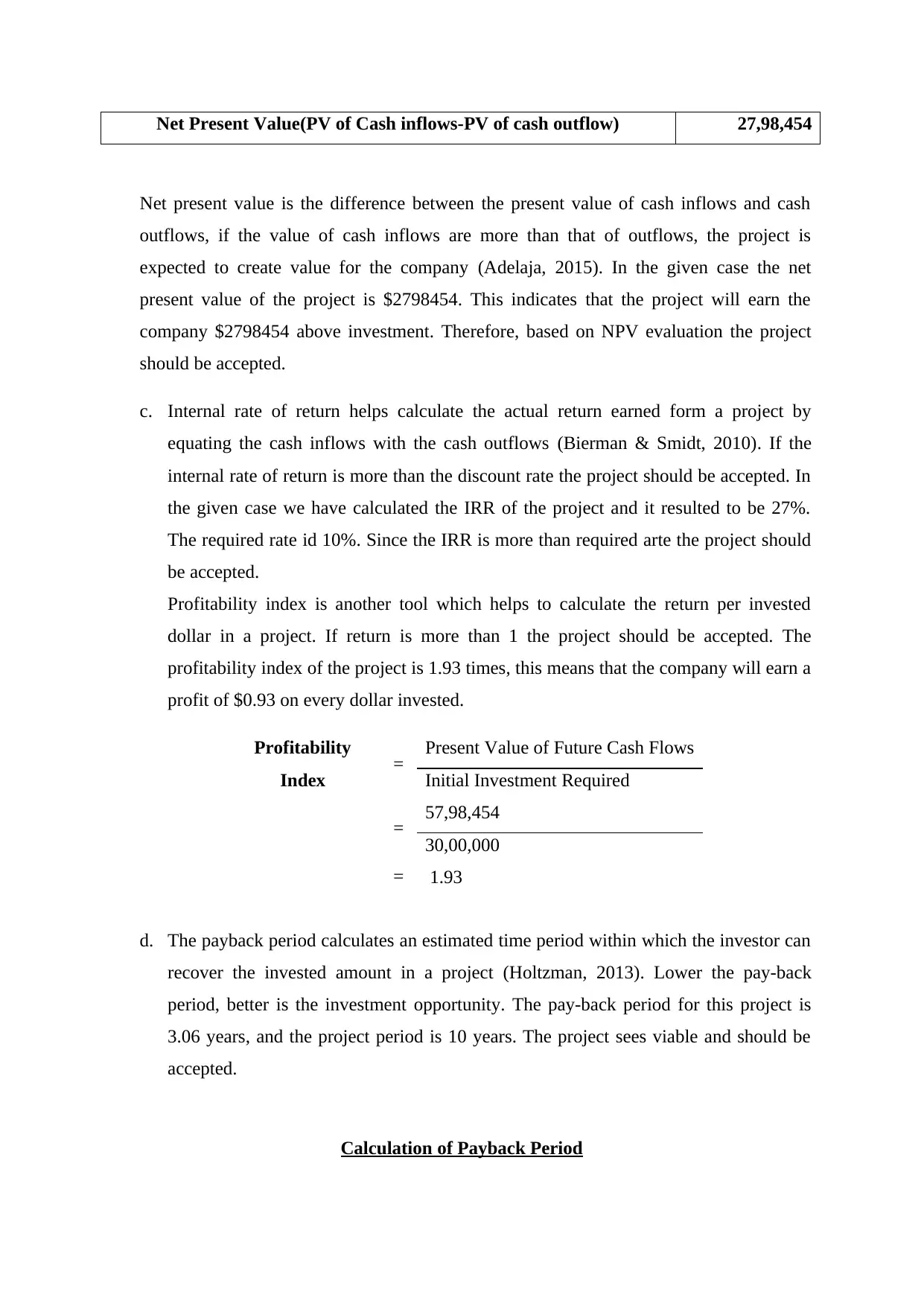

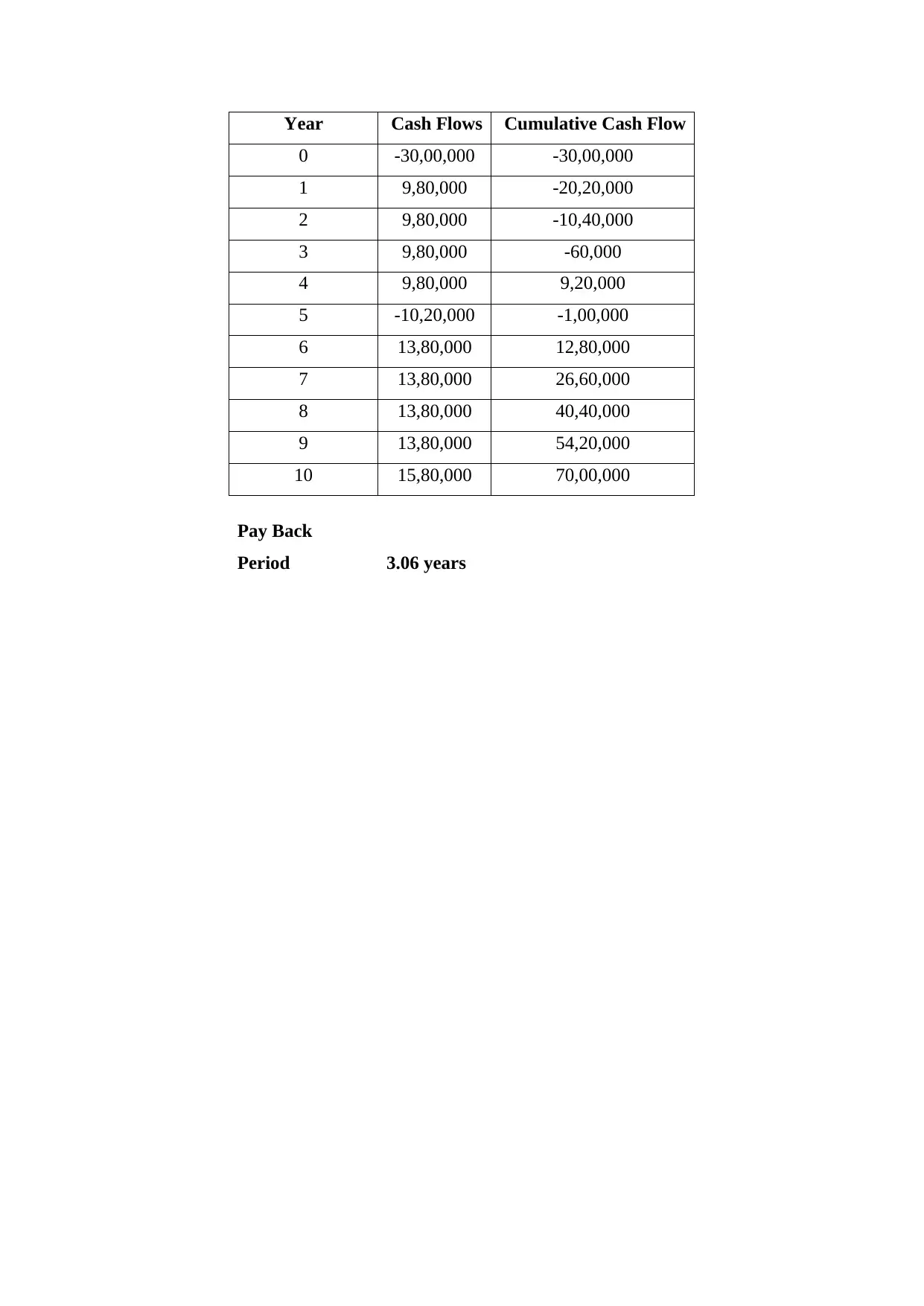

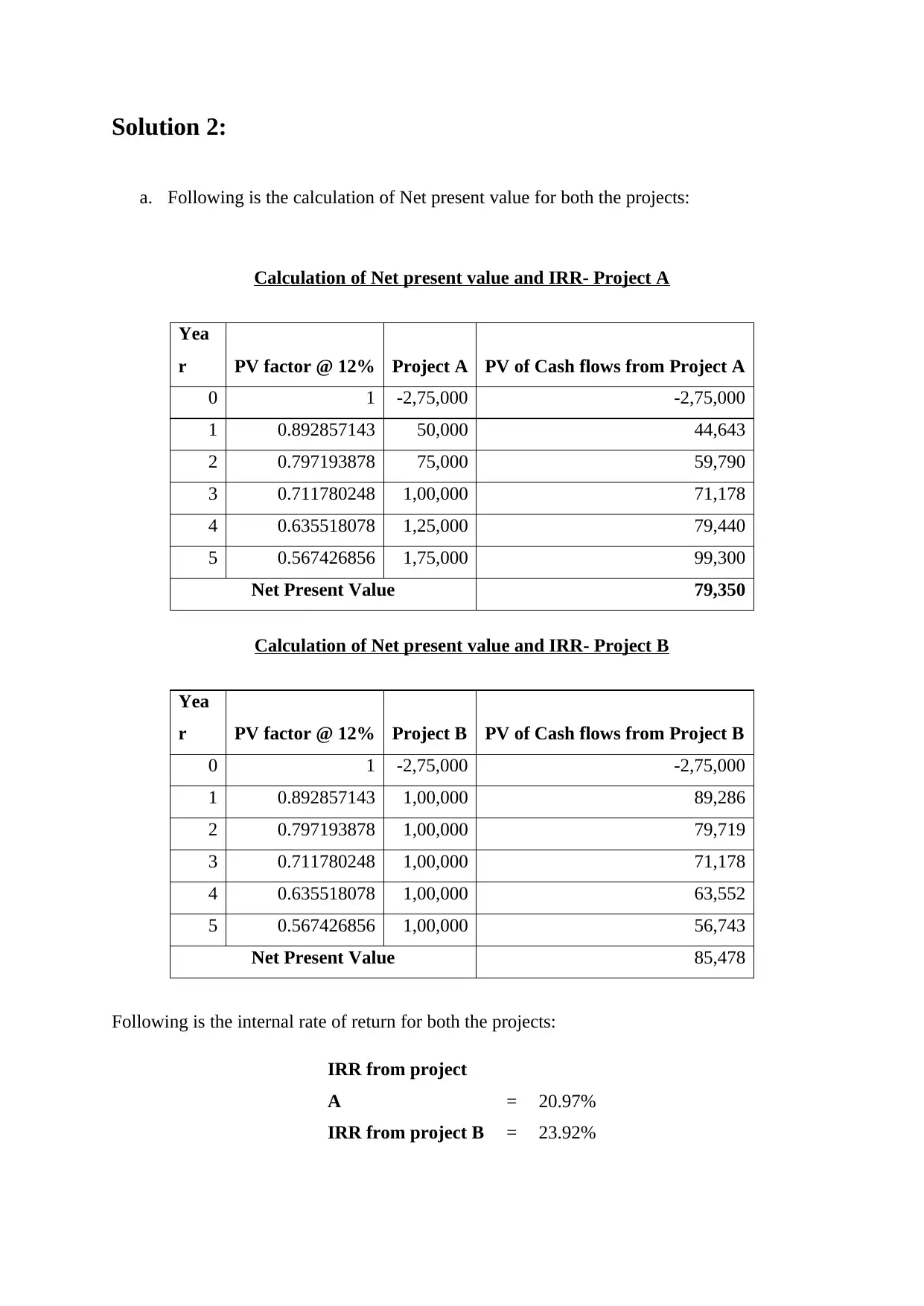

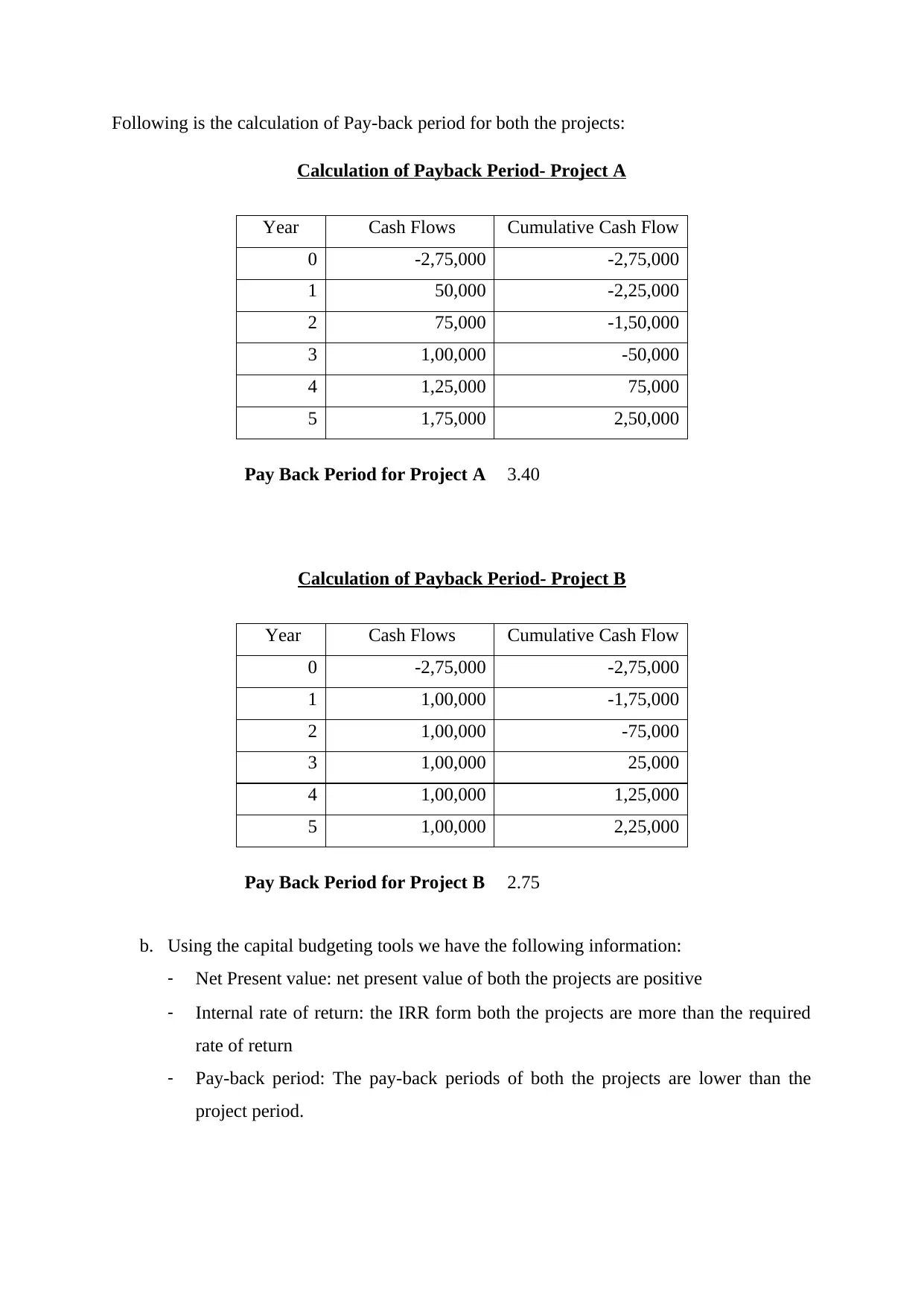

This managerial finance assignment analyzes two projects using capital budgeting techniques. The solution calculates and interprets Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index, and Payback Period for each project. Solution 1 evaluates a single project, determining its financial viability based on the calculated metrics. Solution 2 compares two mutually exclusive projects, providing a ranking based on NPV, IRR, and payback period to determine which project offers the better financial return. The assignment emphasizes the importance of these tools in making sound investment decisions, with detailed calculations and explanations. The analysis includes a discussion of the financial implications of each project, along with a conclusion about which project to accept. The document references several academic sources to support the financial analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.