Financial Management Report: Capital Budgeting and Financial Analysis

VerifiedAdded on 2020/03/16

|20

|4184

|205

Report

AI Summary

This financial management report begins with an analysis of two investment projects, evaluating them based on net present values, payback periods, and average annual rates of return, concluding that Project B is the more suitable investment. The report then calculates various elements of financial statements, followed by a critical analysis of Jaguar Land Rover's financial performance using ratio analysis, revealing areas for improvement. Finally, it discusses the importance of budgeting in financial planning, emphasizing the need for participation from all management levels. The report provides a comprehensive overview of capital budgeting techniques, financial statement analysis, and the application of financial ratios to assess a company's performance.

Running Head: Financial Management

Capital Budgeting & Financial Analysis

Capital Budgeting & Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 1

Executive summary:

In the first part of report the two projects investments are analysed on the basis of their net

present values, payback periods and the average annual rate of return. From the results of

those capital budgeting techniques project B is considered as the appropriate investment

proposal due to the fact that it is providing higher returns and keeps the ability to recover its

invested amounts in the shorter time than the project A. In the second part various elements

of financial statements have been calculated using certain financial formulas. Using those

calculated amounts the extract for the next year is drawn. In the third part, critical analysis of

financial performance of Jaguar Land Rover is made using ratio analysis approach which

proved that in company needs to improve its performance in certain areas and in some

financial areas it is currently performing well. In the last part of the report, the budgeting

process and its importance is discussed as budgets are necessary for financial planning and

therefore participation from all the levels of management is necessary to make the best use of

budgeting practices.

Executive summary:

In the first part of report the two projects investments are analysed on the basis of their net

present values, payback periods and the average annual rate of return. From the results of

those capital budgeting techniques project B is considered as the appropriate investment

proposal due to the fact that it is providing higher returns and keeps the ability to recover its

invested amounts in the shorter time than the project A. In the second part various elements

of financial statements have been calculated using certain financial formulas. Using those

calculated amounts the extract for the next year is drawn. In the third part, critical analysis of

financial performance of Jaguar Land Rover is made using ratio analysis approach which

proved that in company needs to improve its performance in certain areas and in some

financial areas it is currently performing well. In the last part of the report, the budgeting

process and its importance is discussed as budgets are necessary for financial planning and

therefore participation from all the levels of management is necessary to make the best use of

budgeting practices.

Financial Management 2

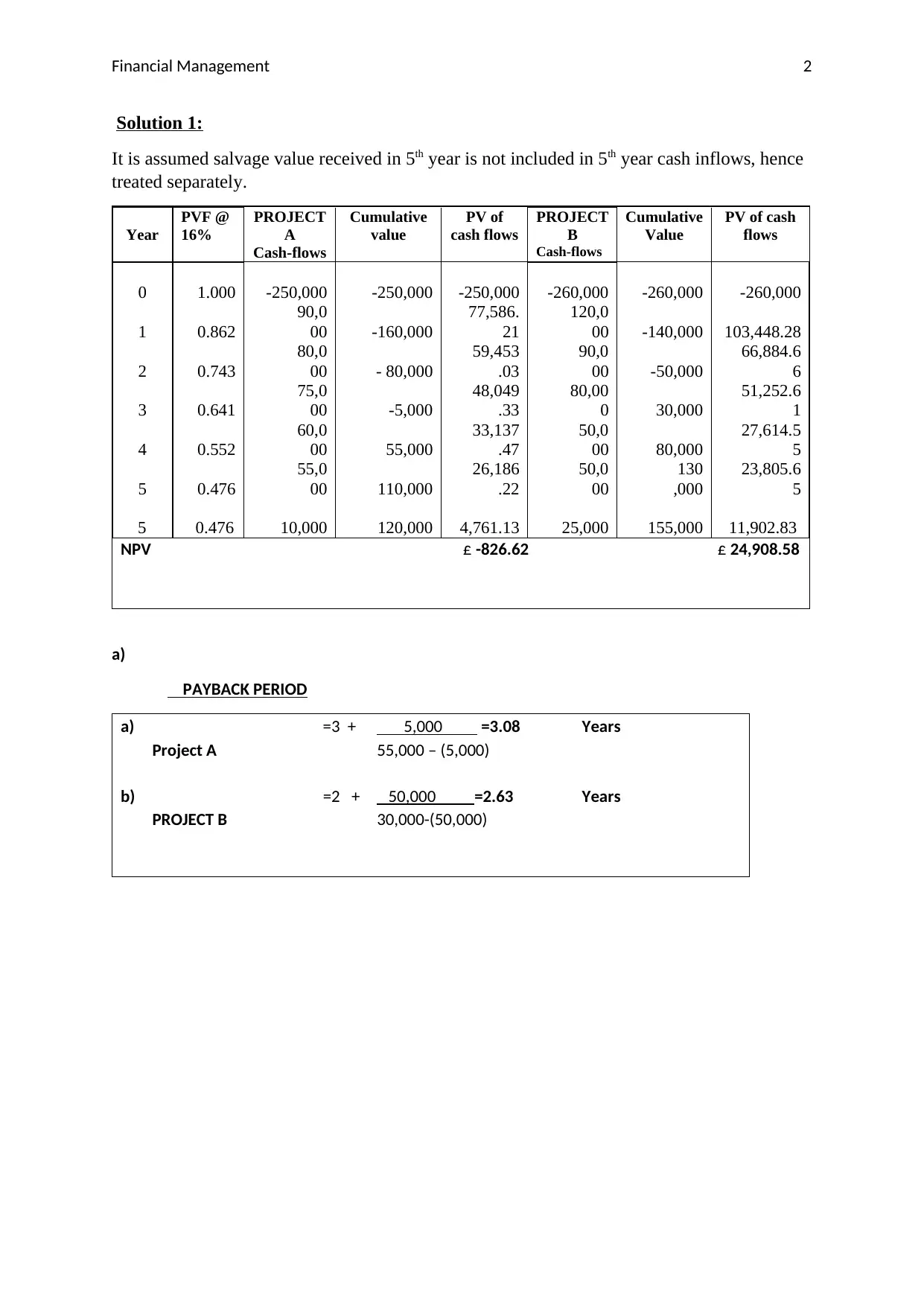

Solution 1:

It is assumed salvage value received in 5th year is not included in 5th year cash inflows, hence

treated separately.

Year

PVF @

16%

PROJECT

A

Cash-flows

Cumulative

value

PV of

cash flows

PROJECT

B

Cash-flows

Cumulative

Value

PV of cash

flows

0 1.000 -250,000 -250,000 -250,000 -260,000 -260,000 -260,000

1 0.862

90,0

00 -160,000

77,586.

21

120,0

00 -140,000 103,448.28

2 0.743

80,0

00 - 80,000

59,453

.03

90,0

00 -50,000

66,884.6

6

3 0.641

75,0

00 -5,000

48,049

.33

80,00

0 30,000

51,252.6

1

4 0.552

60,0

00 55,000

33,137

.47

50,0

00 80,000

27,614.5

5

5 0.476

55,0

00 110,000

26,186

.22

50,0

00

130

,000

23,805.6

5

5 0.476 10,000 120,000 4,761.13 25,000 155,000 11,902.83

NPV £ -826.62 £ 24,908.58

a)

PAYBACK PERIOD

a) =3 + 5,000 =3.08 Years

Project A 55,000 – (5,000)

b) =2 + 50,000 =2.63 Years

PROJECT B 30,000-(50,000)

Solution 1:

It is assumed salvage value received in 5th year is not included in 5th year cash inflows, hence

treated separately.

Year

PVF @

16%

PROJECT

A

Cash-flows

Cumulative

value

PV of

cash flows

PROJECT

B

Cash-flows

Cumulative

Value

PV of cash

flows

0 1.000 -250,000 -250,000 -250,000 -260,000 -260,000 -260,000

1 0.862

90,0

00 -160,000

77,586.

21

120,0

00 -140,000 103,448.28

2 0.743

80,0

00 - 80,000

59,453

.03

90,0

00 -50,000

66,884.6

6

3 0.641

75,0

00 -5,000

48,049

.33

80,00

0 30,000

51,252.6

1

4 0.552

60,0

00 55,000

33,137

.47

50,0

00 80,000

27,614.5

5

5 0.476

55,0

00 110,000

26,186

.22

50,0

00

130

,000

23,805.6

5

5 0.476 10,000 120,000 4,761.13 25,000 155,000 11,902.83

NPV £ -826.62 £ 24,908.58

a)

PAYBACK PERIOD

a) =3 + 5,000 =3.08 Years

Project A 55,000 – (5,000)

b) =2 + 50,000 =2.63 Years

PROJECT B 30,000-(50,000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 3

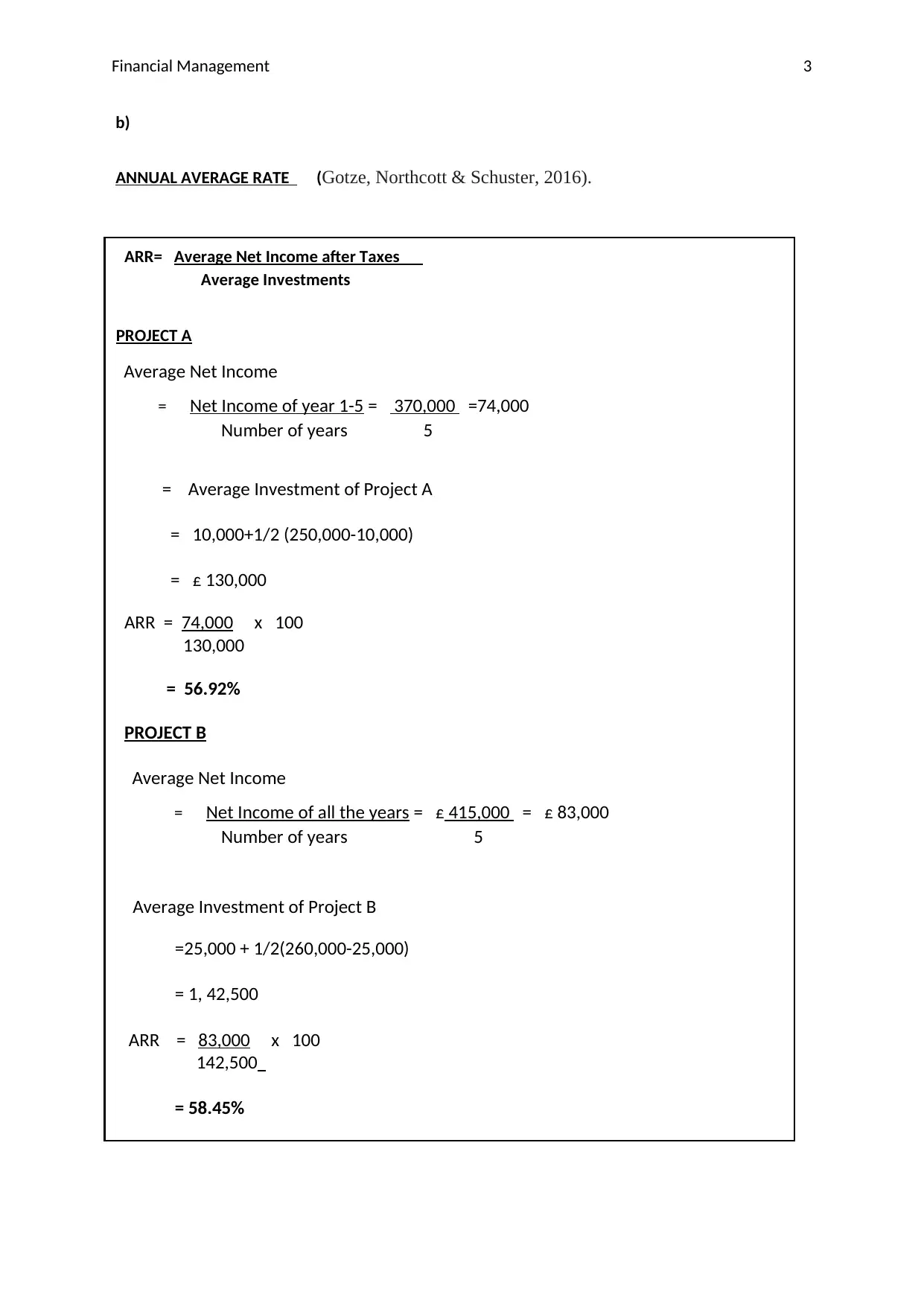

b)

ANNUAL AVERAGE RATE (Gotze, Northcott & Schuster, 2016).

ARR= Average Net Income after Taxes

Average Investments

PROJECT A

Average Net Income

= Net Income of year 1-5 = 370,000 =74,000

Number of years 5

= Average Investment of Project A

= 10,000+1/2 (250,000-10,000)

= £ 130,000

ARR = 74,000 x 100

130,000

= 56.92%

PROJECT B

Average Net Income

= Net Income of all the years = £ 415,000 = £ 83,000

Number of years 5

Average Investment of Project B

=25,000 + 1/2(260,000-25,000)

= 1, 42,500

ARR = 83,000 x 100

£ 142,500

= 58.45%

b)

ANNUAL AVERAGE RATE (Gotze, Northcott & Schuster, 2016).

ARR= Average Net Income after Taxes

Average Investments

PROJECT A

Average Net Income

= Net Income of year 1-5 = 370,000 =74,000

Number of years 5

= Average Investment of Project A

= 10,000+1/2 (250,000-10,000)

= £ 130,000

ARR = 74,000 x 100

130,000

= 56.92%

PROJECT B

Average Net Income

= Net Income of all the years = £ 415,000 = £ 83,000

Number of years 5

Average Investment of Project B

=25,000 + 1/2(260,000-25,000)

= 1, 42,500

ARR = 83,000 x 100

£ 142,500

= 58.45%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 4

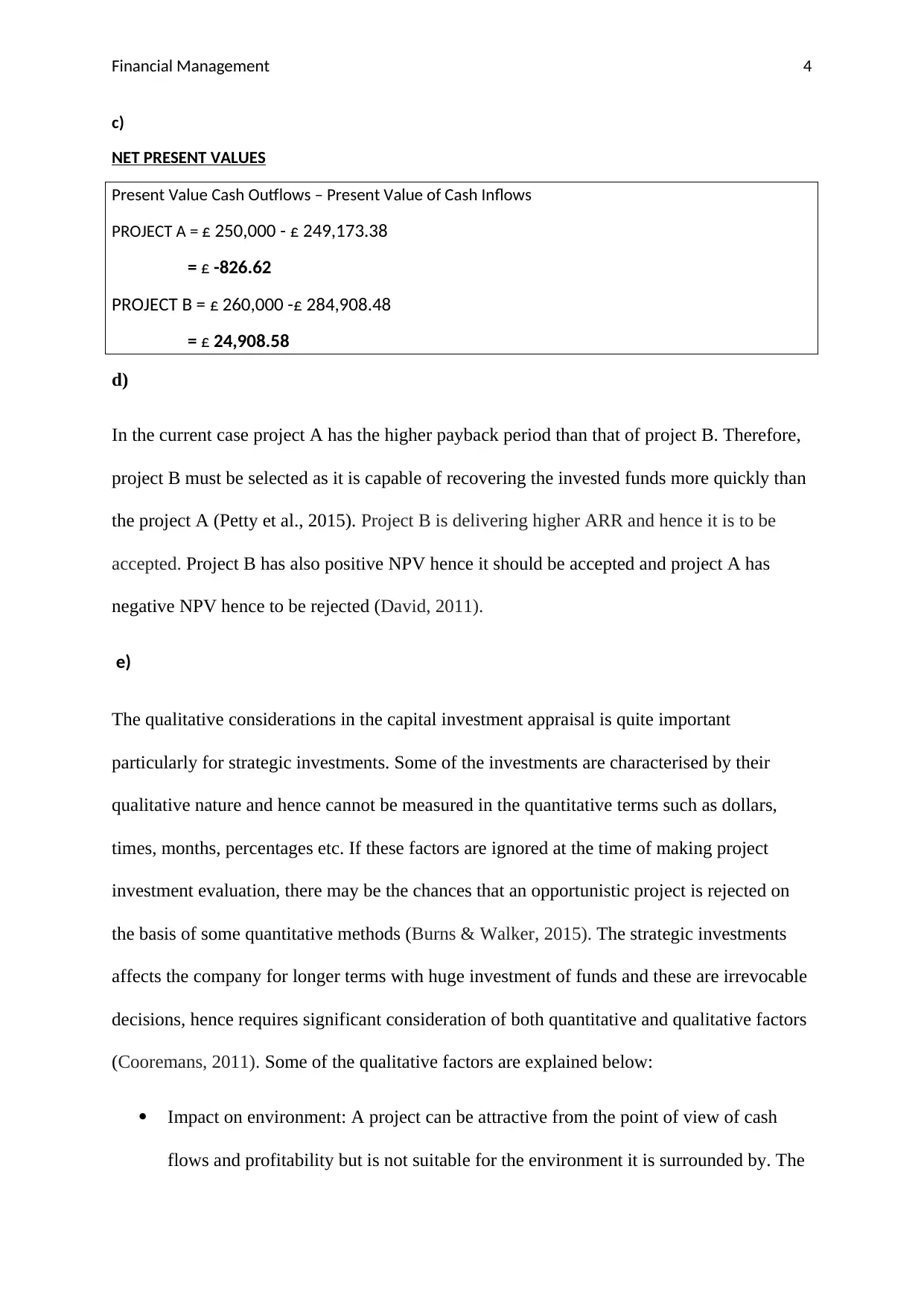

c)

NET PRESENT VALUES

Present Value Cash Outflows – Present Value of Cash Inflows

PROJECT A = £ 250,000 - £ 249,173.38

= £ -826.62

PROJECT B = £ 260,000 -£ 284,908.48

= £ 24,908.58

d)

In the current case project A has the higher payback period than that of project B. Therefore,

project B must be selected as it is capable of recovering the invested funds more quickly than

the project A (Petty et al., 2015). Project B is delivering higher ARR and hence it is to be

accepted. Project B has also positive NPV hence it should be accepted and project A has

negative NPV hence to be rejected (David, 2011).

e)

The qualitative considerations in the capital investment appraisal is quite important

particularly for strategic investments. Some of the investments are characterised by their

qualitative nature and hence cannot be measured in the quantitative terms such as dollars,

times, months, percentages etc. If these factors are ignored at the time of making project

investment evaluation, there may be the chances that an opportunistic project is rejected on

the basis of some quantitative methods (Burns & Walker, 2015). The strategic investments

affects the company for longer terms with huge investment of funds and these are irrevocable

decisions, hence requires significant consideration of both quantitative and qualitative factors

(Cooremans, 2011). Some of the qualitative factors are explained below:

Impact on environment: A project can be attractive from the point of view of cash

flows and profitability but is not suitable for the environment it is surrounded by. The

c)

NET PRESENT VALUES

Present Value Cash Outflows – Present Value of Cash Inflows

PROJECT A = £ 250,000 - £ 249,173.38

= £ -826.62

PROJECT B = £ 260,000 -£ 284,908.48

= £ 24,908.58

d)

In the current case project A has the higher payback period than that of project B. Therefore,

project B must be selected as it is capable of recovering the invested funds more quickly than

the project A (Petty et al., 2015). Project B is delivering higher ARR and hence it is to be

accepted. Project B has also positive NPV hence it should be accepted and project A has

negative NPV hence to be rejected (David, 2011).

e)

The qualitative considerations in the capital investment appraisal is quite important

particularly for strategic investments. Some of the investments are characterised by their

qualitative nature and hence cannot be measured in the quantitative terms such as dollars,

times, months, percentages etc. If these factors are ignored at the time of making project

investment evaluation, there may be the chances that an opportunistic project is rejected on

the basis of some quantitative methods (Burns & Walker, 2015). The strategic investments

affects the company for longer terms with huge investment of funds and these are irrevocable

decisions, hence requires significant consideration of both quantitative and qualitative factors

(Cooremans, 2011). Some of the qualitative factors are explained below:

Impact on environment: A project can be attractive from the point of view of cash

flows and profitability but is not suitable for the environment it is surrounded by. The

Financial Management 5

project may involve use of excessive natural resources affecting their sustainability or

its operations may impose harmful impact on the nature such as plants, animals,

human beings, water bodies etc. Such a project has the huge chances of public

opposition which would definitely hinders the investment’s ability to produce

desirable outputs (McNeil, Frey & Embrechts, 2015).

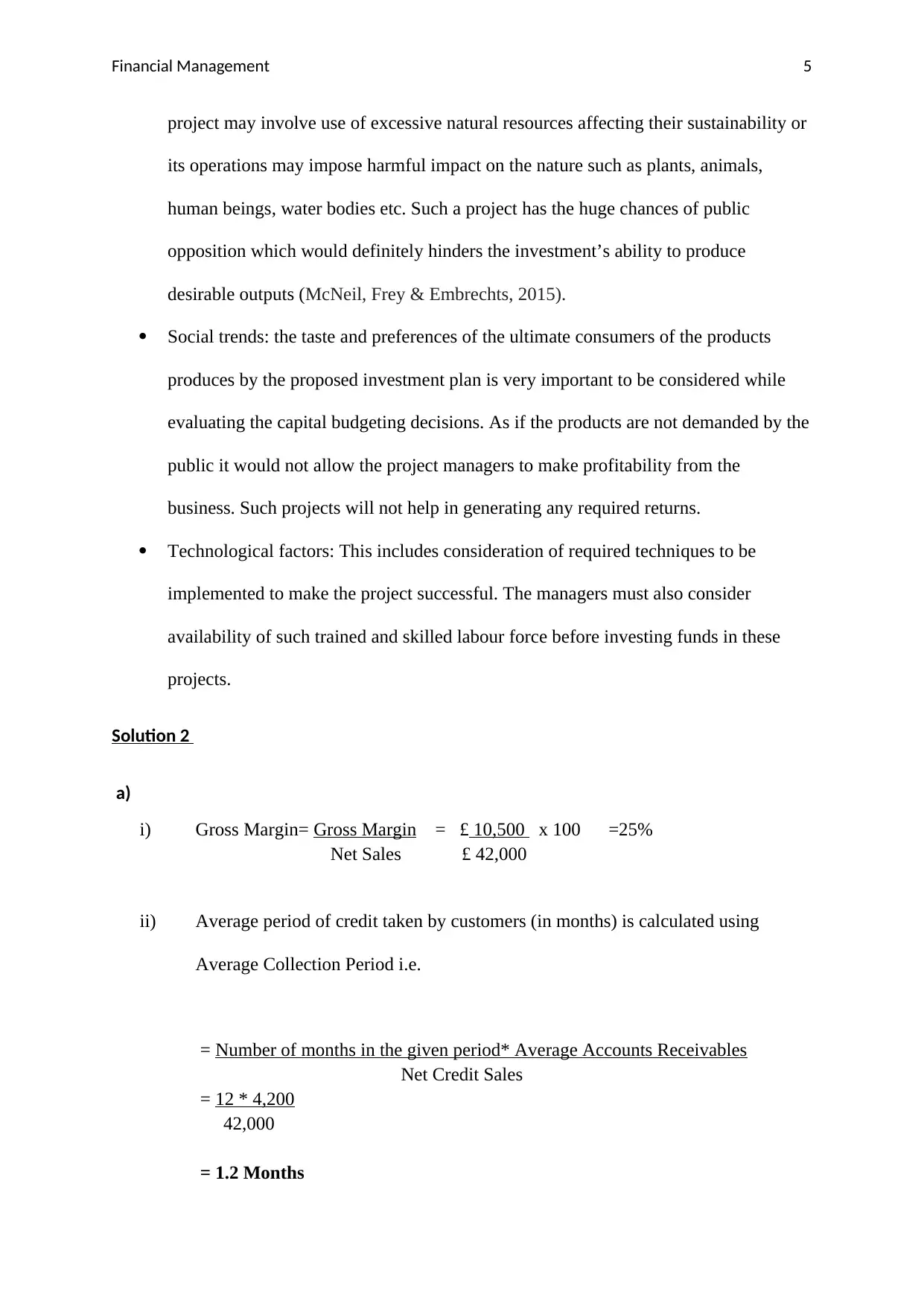

Social trends: the taste and preferences of the ultimate consumers of the products

produces by the proposed investment plan is very important to be considered while

evaluating the capital budgeting decisions. As if the products are not demanded by the

public it would not allow the project managers to make profitability from the

business. Such projects will not help in generating any required returns.

Technological factors: This includes consideration of required techniques to be

implemented to make the project successful. The managers must also consider

availability of such trained and skilled labour force before investing funds in these

projects.

Solution 2

a)

i) Gross Margin= Gross Margin = £ 10,500 x 100 =25%

Net Sales £ 42,000

ii) Average period of credit taken by customers (in months) is calculated using

Average Collection Period i.e.

= Number of months in the given period* Average Accounts Receivables

Net Credit Sales

= 12 * 4,200

42,000

= 1.2 Months

project may involve use of excessive natural resources affecting their sustainability or

its operations may impose harmful impact on the nature such as plants, animals,

human beings, water bodies etc. Such a project has the huge chances of public

opposition which would definitely hinders the investment’s ability to produce

desirable outputs (McNeil, Frey & Embrechts, 2015).

Social trends: the taste and preferences of the ultimate consumers of the products

produces by the proposed investment plan is very important to be considered while

evaluating the capital budgeting decisions. As if the products are not demanded by the

public it would not allow the project managers to make profitability from the

business. Such projects will not help in generating any required returns.

Technological factors: This includes consideration of required techniques to be

implemented to make the project successful. The managers must also consider

availability of such trained and skilled labour force before investing funds in these

projects.

Solution 2

a)

i) Gross Margin= Gross Margin = £ 10,500 x 100 =25%

Net Sales £ 42,000

ii) Average period of credit taken by customers (in months) is calculated using

Average Collection Period i.e.

= Number of months in the given period* Average Accounts Receivables

Net Credit Sales

= 12 * 4,200

42,000

= 1.2 Months

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management 6

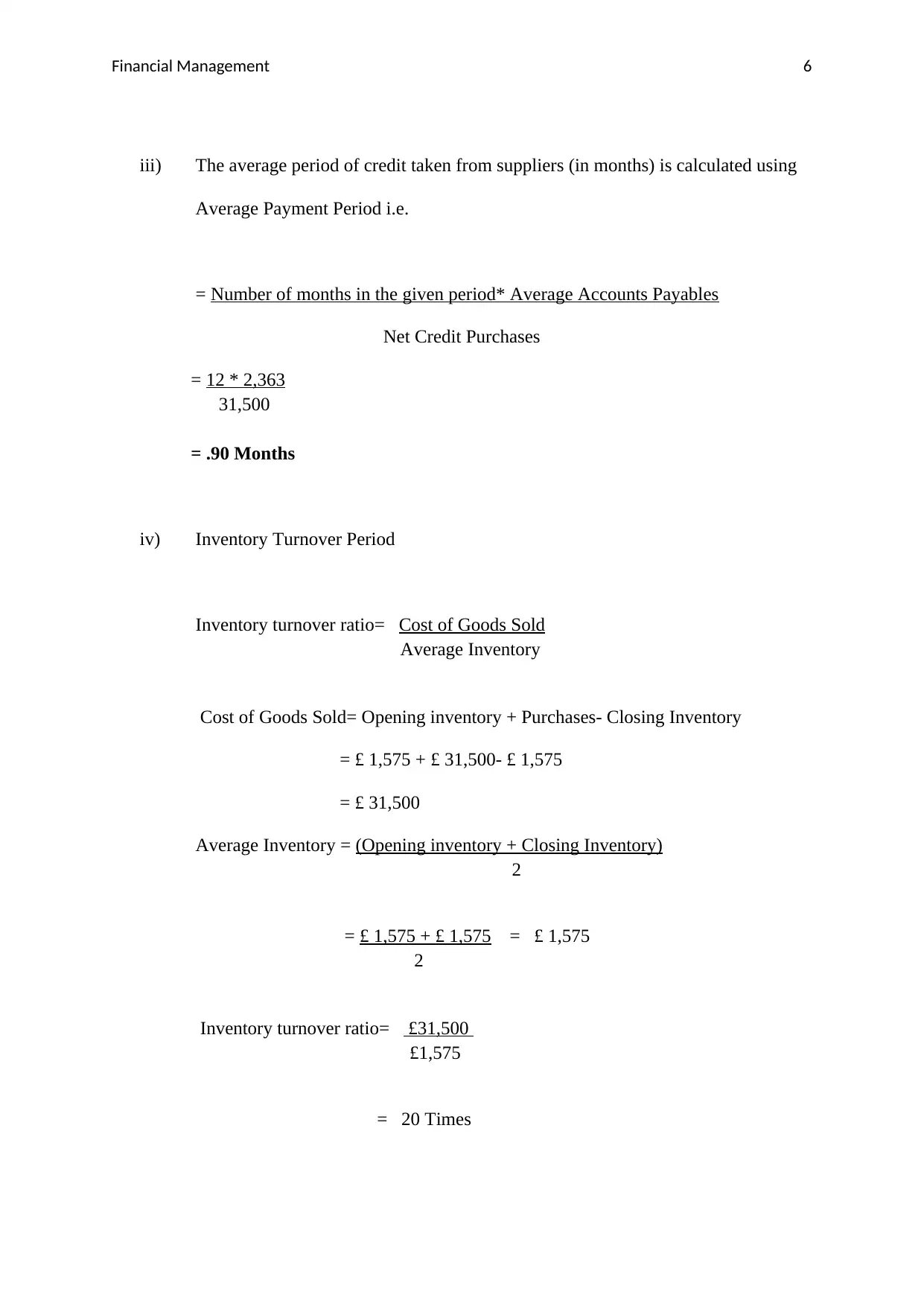

iii) The average period of credit taken from suppliers (in months) is calculated using

Average Payment Period i.e.

= Number of months in the given period* Average Accounts Payables

Net Credit Purchases

= 12 * 2,363

31,500

= .90 Months

iv) Inventory Turnover Period

Inventory turnover ratio= Cost of Goods Sold

Average Inventory

Cost of Goods Sold= Opening inventory + Purchases- Closing Inventory

= £ 1,575 + £ 31,500- £ 1,575

= £ 31,500

Average Inventory = (Opening inventory + Closing Inventory)

2

= £ 1,575 + £ 1,575 = £ 1,575

2

Inventory turnover ratio= £31,500

£1,575

= 20 Times

iii) The average period of credit taken from suppliers (in months) is calculated using

Average Payment Period i.e.

= Number of months in the given period* Average Accounts Payables

Net Credit Purchases

= 12 * 2,363

31,500

= .90 Months

iv) Inventory Turnover Period

Inventory turnover ratio= Cost of Goods Sold

Average Inventory

Cost of Goods Sold= Opening inventory + Purchases- Closing Inventory

= £ 1,575 + £ 31,500- £ 1,575

= £ 31,500

Average Inventory = (Opening inventory + Closing Inventory)

2

= £ 1,575 + £ 1,575 = £ 1,575

2

Inventory turnover ratio= £31,500

£1,575

= 20 Times

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 7

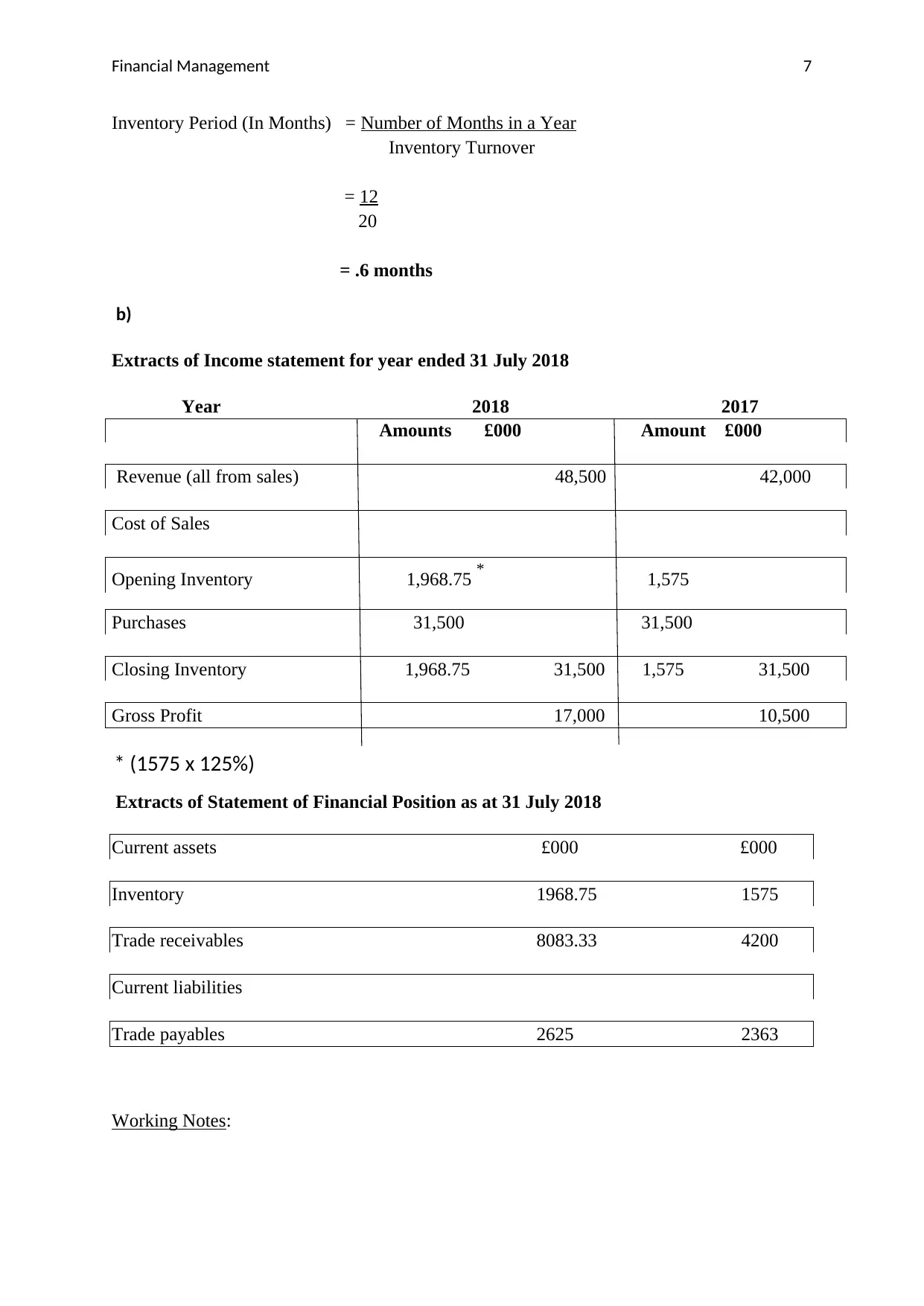

Inventory Period (In Months) = Number of Months in a Year

Inventory Turnover

= 12

20

= .6 months

b)

Extracts of Income statement for year ended 31 July 2018

Year 2018 2017

Amounts £000 Amount £000

Revenue (all from sales) 48,500 42,000

Cost of Sales

Opening Inventory 1,968.75 * 1,575

Purchases 31,500 31,500

Closing Inventory 1,968.75 31,500 1,575 31,500

Gross Profit 17,000 10,500

* (1575 x 125%)

Extracts of Statement of Financial Position as at 31 July 2018

Current assets £000 £000

Inventory 1968.75 1575

Trade receivables 8083.33 4200

Current liabilities

Trade payables 2625 2363

Working Notes:

Inventory Period (In Months) = Number of Months in a Year

Inventory Turnover

= 12

20

= .6 months

b)

Extracts of Income statement for year ended 31 July 2018

Year 2018 2017

Amounts £000 Amount £000

Revenue (all from sales) 48,500 42,000

Cost of Sales

Opening Inventory 1,968.75 * 1,575

Purchases 31,500 31,500

Closing Inventory 1,968.75 31,500 1,575 31,500

Gross Profit 17,000 10,500

* (1575 x 125%)

Extracts of Statement of Financial Position as at 31 July 2018

Current assets £000 £000

Inventory 1968.75 1575

Trade receivables 8083.33 4200

Current liabilities

Trade payables 2625 2363

Working Notes:

Financial Management 8

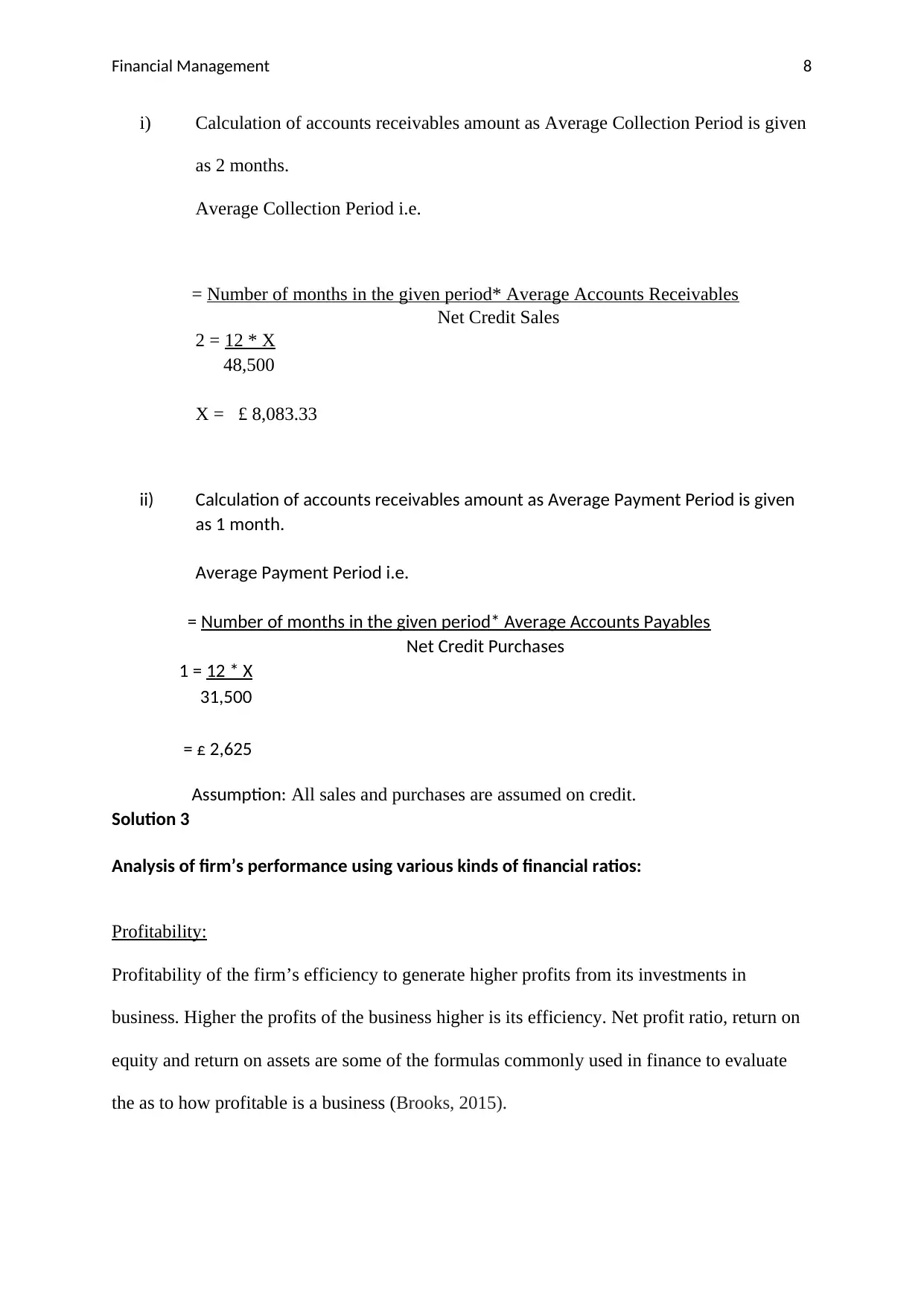

i) Calculation of accounts receivables amount as Average Collection Period is given

as 2 months.

Average Collection Period i.e.

= Number of months in the given period* Average Accounts Receivables

Net Credit Sales

2 = 12 * X

48,500

X = £ 8,083.33

ii) Calculation of accounts receivables amount as Average Payment Period is given

as 1 month.

Average Payment Period i.e.

= Number of months in the given period* Average Accounts Payables

Net Credit Purchases

1 = 12 * X

31,500

= £ 2,625

Assumption: All sales and purchases are assumed on credit.

Solution 3

Analysis of firm’s performance using various kinds of financial ratios:

Profitability:

Profitability of the firm’s efficiency to generate higher profits from its investments in

business. Higher the profits of the business higher is its efficiency. Net profit ratio, return on

equity and return on assets are some of the formulas commonly used in finance to evaluate

the as to how profitable is a business (Brooks, 2015).

i) Calculation of accounts receivables amount as Average Collection Period is given

as 2 months.

Average Collection Period i.e.

= Number of months in the given period* Average Accounts Receivables

Net Credit Sales

2 = 12 * X

48,500

X = £ 8,083.33

ii) Calculation of accounts receivables amount as Average Payment Period is given

as 1 month.

Average Payment Period i.e.

= Number of months in the given period* Average Accounts Payables

Net Credit Purchases

1 = 12 * X

31,500

= £ 2,625

Assumption: All sales and purchases are assumed on credit.

Solution 3

Analysis of firm’s performance using various kinds of financial ratios:

Profitability:

Profitability of the firm’s efficiency to generate higher profits from its investments in

business. Higher the profits of the business higher is its efficiency. Net profit ratio, return on

equity and return on assets are some of the formulas commonly used in finance to evaluate

the as to how profitable is a business (Brooks, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

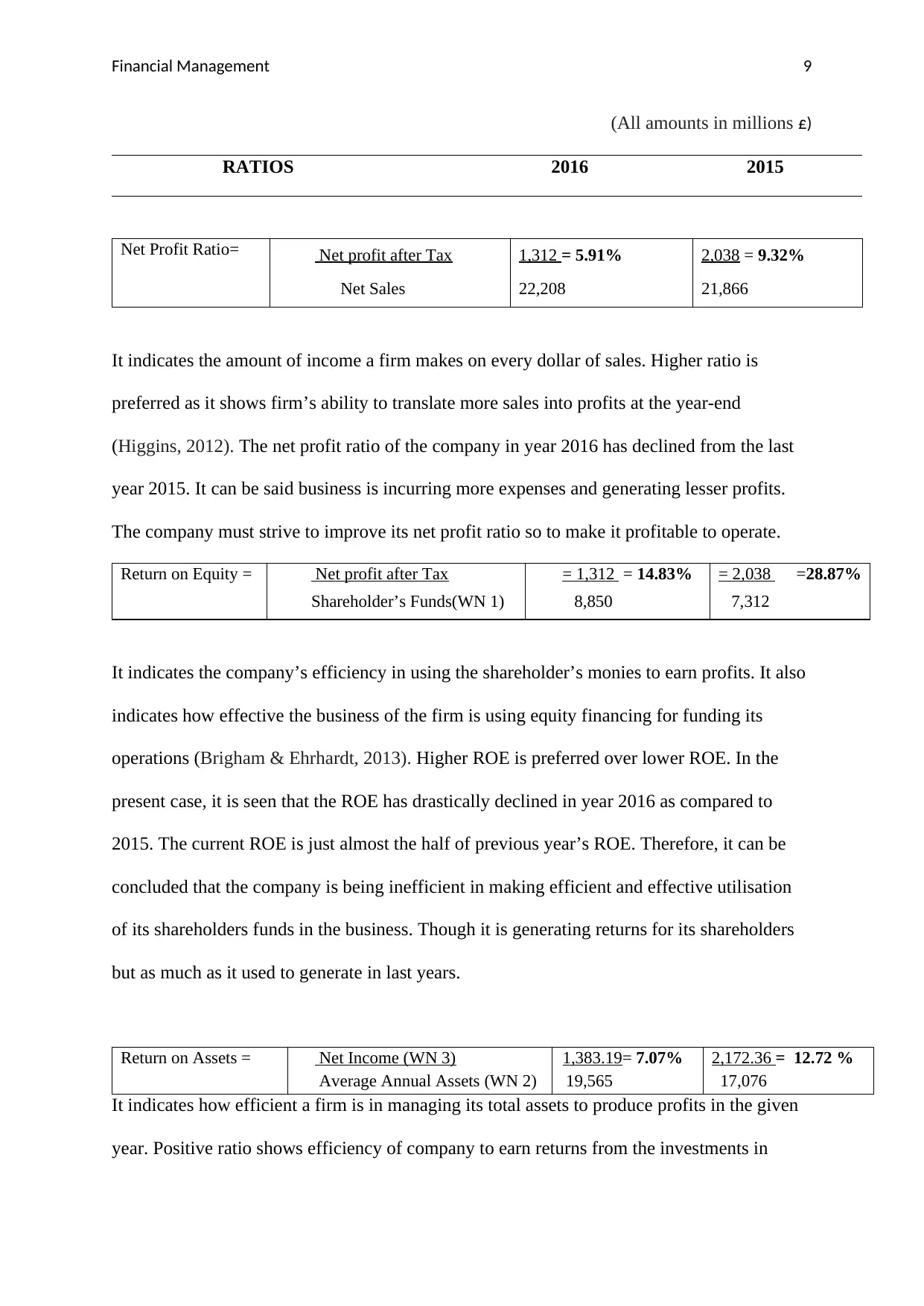

Financial Management 9

(All amounts in millions £)

RATIOS 2016 2015

Net Profit Ratio= Net profit after Tax 1,312 = 5.91% 2,038 = 9.32%

Net Sales 22,208 21,866

It indicates the amount of income a firm makes on every dollar of sales. Higher ratio is

preferred as it shows firm’s ability to translate more sales into profits at the year-end

(Higgins, 2012). The net profit ratio of the company in year 2016 has declined from the last

year 2015. It can be said business is incurring more expenses and generating lesser profits.

The company must strive to improve its net profit ratio so to make it profitable to operate.

Return on Equity = Net profit after Tax = 1,312 = 14.83% = 2,038 =28.87%

Shareholder’s Funds(WN 1) 8,850 7,312

It indicates the company’s efficiency in using the shareholder’s monies to earn profits. It also

indicates how effective the business of the firm is using equity financing for funding its

operations (Brigham & Ehrhardt, 2013). Higher ROE is preferred over lower ROE. In the

present case, it is seen that the ROE has drastically declined in year 2016 as compared to

2015. The current ROE is just almost the half of previous year’s ROE. Therefore, it can be

concluded that the company is being inefficient in making efficient and effective utilisation

of its shareholders funds in the business. Though it is generating returns for its shareholders

but as much as it used to generate in last years.

Return on Assets = Net Income (WN 3) 1,383.19= 7.07% 2,172.36 = 12.72 %

Average Annual Assets (WN 2) 19,565 17,076

It indicates how efficient a firm is in managing its total assets to produce profits in the given

year. Positive ratio shows efficiency of company to earn returns from the investments in

(All amounts in millions £)

RATIOS 2016 2015

Net Profit Ratio= Net profit after Tax 1,312 = 5.91% 2,038 = 9.32%

Net Sales 22,208 21,866

It indicates the amount of income a firm makes on every dollar of sales. Higher ratio is

preferred as it shows firm’s ability to translate more sales into profits at the year-end

(Higgins, 2012). The net profit ratio of the company in year 2016 has declined from the last

year 2015. It can be said business is incurring more expenses and generating lesser profits.

The company must strive to improve its net profit ratio so to make it profitable to operate.

Return on Equity = Net profit after Tax = 1,312 = 14.83% = 2,038 =28.87%

Shareholder’s Funds(WN 1) 8,850 7,312

It indicates the company’s efficiency in using the shareholder’s monies to earn profits. It also

indicates how effective the business of the firm is using equity financing for funding its

operations (Brigham & Ehrhardt, 2013). Higher ROE is preferred over lower ROE. In the

present case, it is seen that the ROE has drastically declined in year 2016 as compared to

2015. The current ROE is just almost the half of previous year’s ROE. Therefore, it can be

concluded that the company is being inefficient in making efficient and effective utilisation

of its shareholders funds in the business. Though it is generating returns for its shareholders

but as much as it used to generate in last years.

Return on Assets = Net Income (WN 3) 1,383.19= 7.07% 2,172.36 = 12.72 %

Average Annual Assets (WN 2) 19,565 17,076

It indicates how efficient a firm is in managing its total assets to produce profits in the given

year. Positive ratio shows efficiency of company to earn returns from the investments in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management 10

assets. The above calculation is showing that the company’s performance has been degraded

in the year 2016 as compared to 2015 as the return to asset ratio is declining.

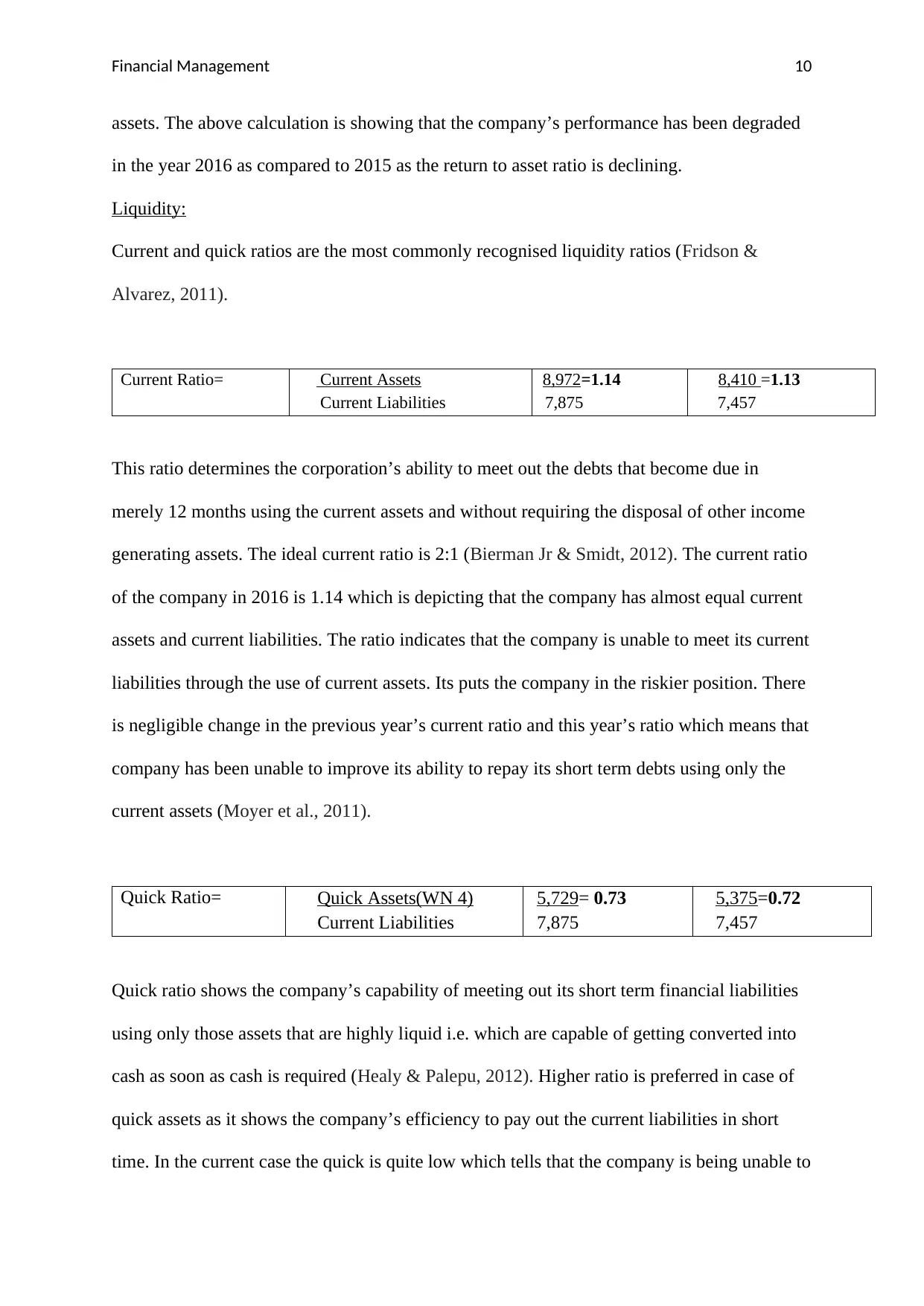

Liquidity:

Current and quick ratios are the most commonly recognised liquidity ratios (Fridson &

Alvarez, 2011).

Current Ratio= Current Assets 8,972=1.14 8,410 =1.13

Current Liabilities 7,875 7,457

This ratio determines the corporation’s ability to meet out the debts that become due in

merely 12 months using the current assets and without requiring the disposal of other income

generating assets. The ideal current ratio is 2:1 (Bierman Jr & Smidt, 2012). The current ratio

of the company in 2016 is 1.14 which is depicting that the company has almost equal current

assets and current liabilities. The ratio indicates that the company is unable to meet its current

liabilities through the use of current assets. Its puts the company in the riskier position. There

is negligible change in the previous year’s current ratio and this year’s ratio which means that

company has been unable to improve its ability to repay its short term debts using only the

current assets (Moyer et al., 2011).

Quick Ratio= Quick Assets(WN 4) 5,729= 0.73 5,375=0.72

Current Liabilities 7,875 7,457

Quick ratio shows the company’s capability of meeting out its short term financial liabilities

using only those assets that are highly liquid i.e. which are capable of getting converted into

cash as soon as cash is required (Healy & Palepu, 2012). Higher ratio is preferred in case of

quick assets as it shows the company’s efficiency to pay out the current liabilities in short

time. In the current case the quick is quite low which tells that the company is being unable to

assets. The above calculation is showing that the company’s performance has been degraded

in the year 2016 as compared to 2015 as the return to asset ratio is declining.

Liquidity:

Current and quick ratios are the most commonly recognised liquidity ratios (Fridson &

Alvarez, 2011).

Current Ratio= Current Assets 8,972=1.14 8,410 =1.13

Current Liabilities 7,875 7,457

This ratio determines the corporation’s ability to meet out the debts that become due in

merely 12 months using the current assets and without requiring the disposal of other income

generating assets. The ideal current ratio is 2:1 (Bierman Jr & Smidt, 2012). The current ratio

of the company in 2016 is 1.14 which is depicting that the company has almost equal current

assets and current liabilities. The ratio indicates that the company is unable to meet its current

liabilities through the use of current assets. Its puts the company in the riskier position. There

is negligible change in the previous year’s current ratio and this year’s ratio which means that

company has been unable to improve its ability to repay its short term debts using only the

current assets (Moyer et al., 2011).

Quick Ratio= Quick Assets(WN 4) 5,729= 0.73 5,375=0.72

Current Liabilities 7,875 7,457

Quick ratio shows the company’s capability of meeting out its short term financial liabilities

using only those assets that are highly liquid i.e. which are capable of getting converted into

cash as soon as cash is required (Healy & Palepu, 2012). Higher ratio is preferred in case of

quick assets as it shows the company’s efficiency to pay out the current liabilities in short

time. In the current case the quick is quite low which tells that the company is being unable to

Financial Management 11

manage its short term liabilities with the only use of quick assets. The ratio was almost

similar in the last year that means that the company was unable to arrange and manage

required quick assets for its business (Brigham & Houston, 2012).

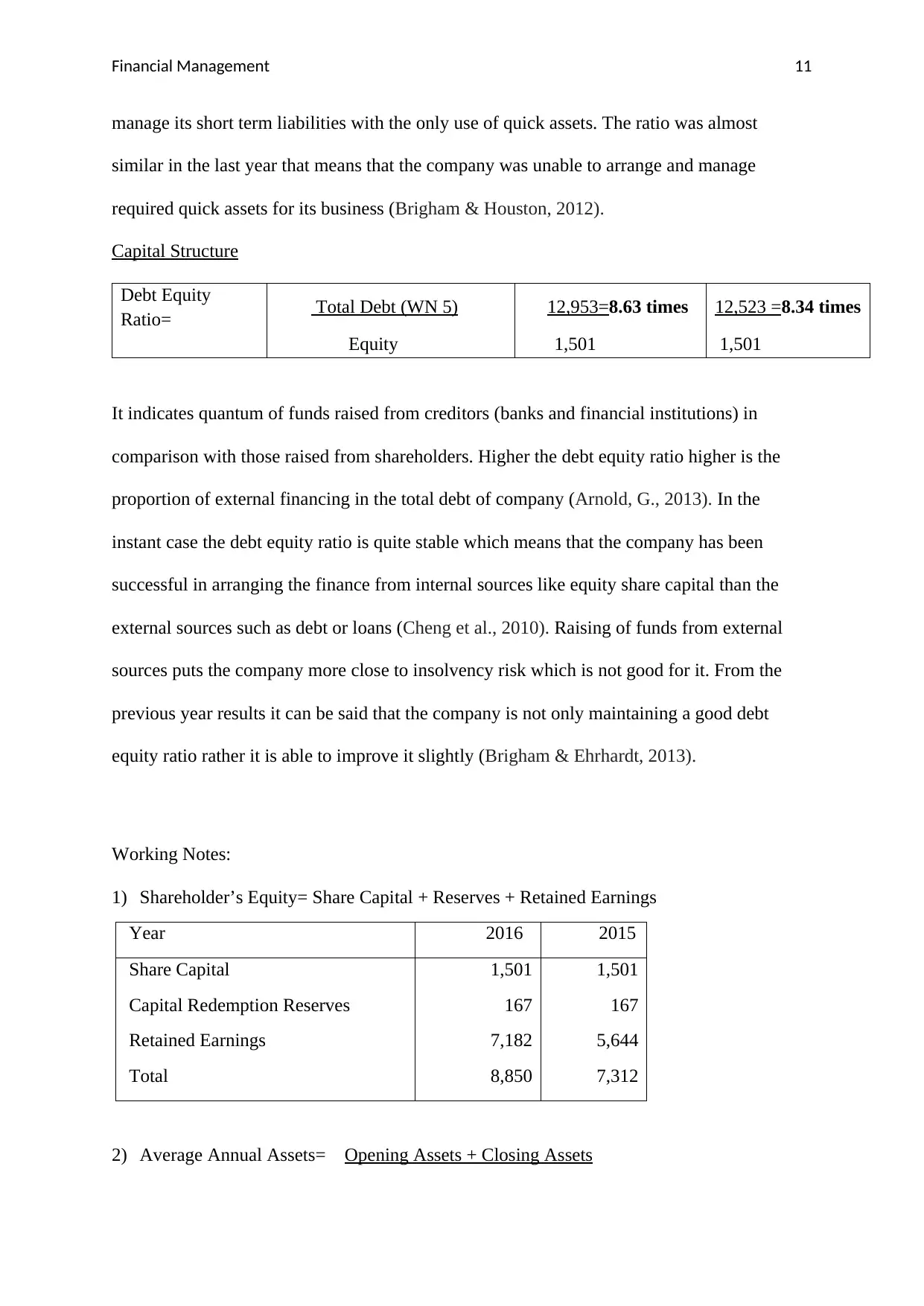

Capital Structure

Debt Equity

Ratio= Total Debt (WN 5) 12,953=8.63 times 12,523 =8.34 times

Equity 1,501 1,501

It indicates quantum of funds raised from creditors (banks and financial institutions) in

comparison with those raised from shareholders. Higher the debt equity ratio higher is the

proportion of external financing in the total debt of company (Arnold, G., 2013). In the

instant case the debt equity ratio is quite stable which means that the company has been

successful in arranging the finance from internal sources like equity share capital than the

external sources such as debt or loans (Cheng et al., 2010). Raising of funds from external

sources puts the company more close to insolvency risk which is not good for it. From the

previous year results it can be said that the company is not only maintaining a good debt

equity ratio rather it is able to improve it slightly (Brigham & Ehrhardt, 2013).

Working Notes:

1) Shareholder’s Equity= Share Capital + Reserves + Retained Earnings

Year 2016 2015

Share Capital

Capital Redemption Reserves

Retained Earnings

Total

1,501

167

7,182

8,850

1,501

167

5,644

7,312

2) Average Annual Assets= Opening Assets + Closing Assets

manage its short term liabilities with the only use of quick assets. The ratio was almost

similar in the last year that means that the company was unable to arrange and manage

required quick assets for its business (Brigham & Houston, 2012).

Capital Structure

Debt Equity

Ratio= Total Debt (WN 5) 12,953=8.63 times 12,523 =8.34 times

Equity 1,501 1,501

It indicates quantum of funds raised from creditors (banks and financial institutions) in

comparison with those raised from shareholders. Higher the debt equity ratio higher is the

proportion of external financing in the total debt of company (Arnold, G., 2013). In the

instant case the debt equity ratio is quite stable which means that the company has been

successful in arranging the finance from internal sources like equity share capital than the

external sources such as debt or loans (Cheng et al., 2010). Raising of funds from external

sources puts the company more close to insolvency risk which is not good for it. From the

previous year results it can be said that the company is not only maintaining a good debt

equity ratio rather it is able to improve it slightly (Brigham & Ehrhardt, 2013).

Working Notes:

1) Shareholder’s Equity= Share Capital + Reserves + Retained Earnings

Year 2016 2015

Share Capital

Capital Redemption Reserves

Retained Earnings

Total

1,501

167

7,182

8,850

1,501

167

5,644

7,312

2) Average Annual Assets= Opening Assets + Closing Assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.