Financial Decision Making Assignment - Part 3, Investment Analysis

VerifiedAdded on 2022/08/23

|8

|1140

|11

Homework Assignment

AI Summary

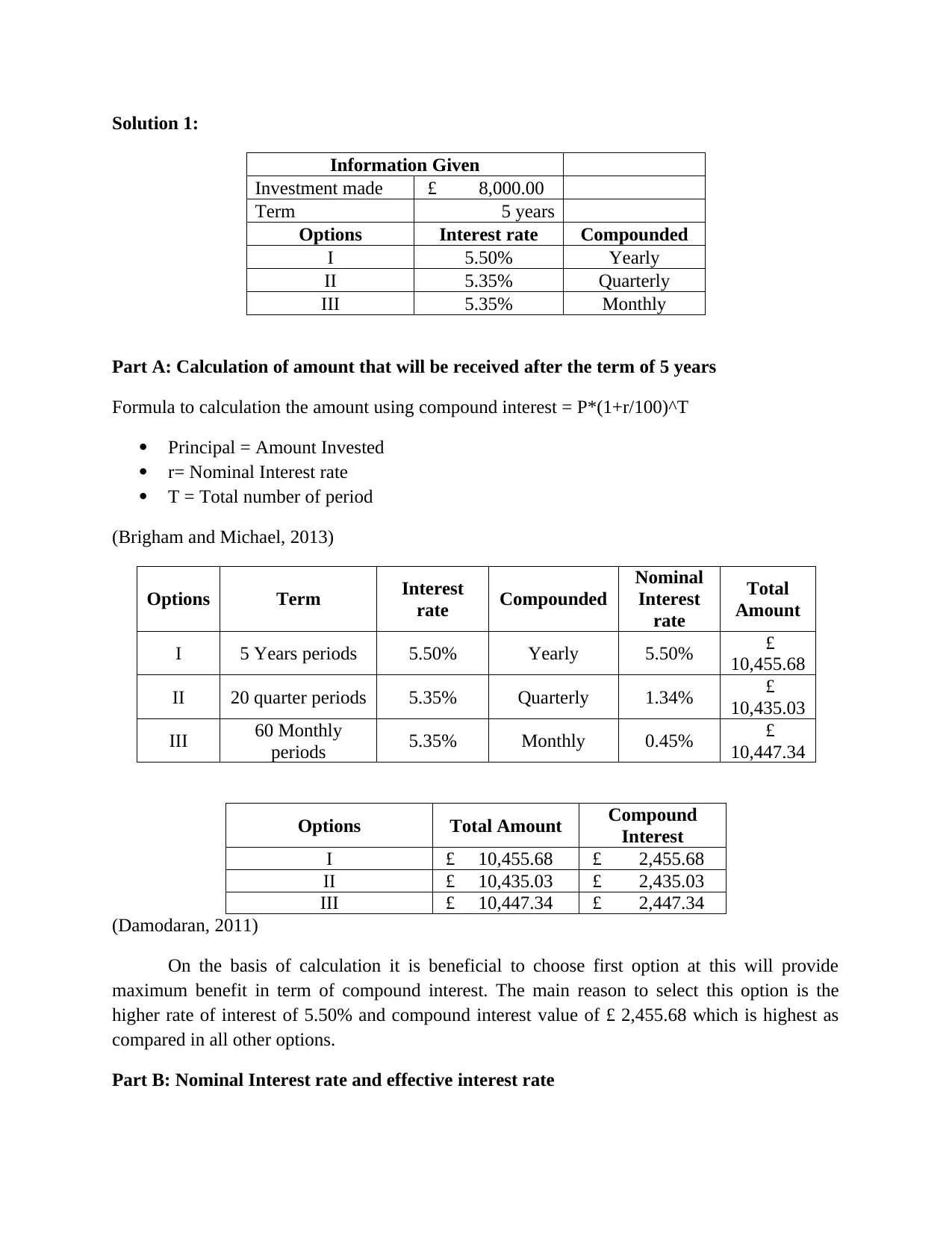

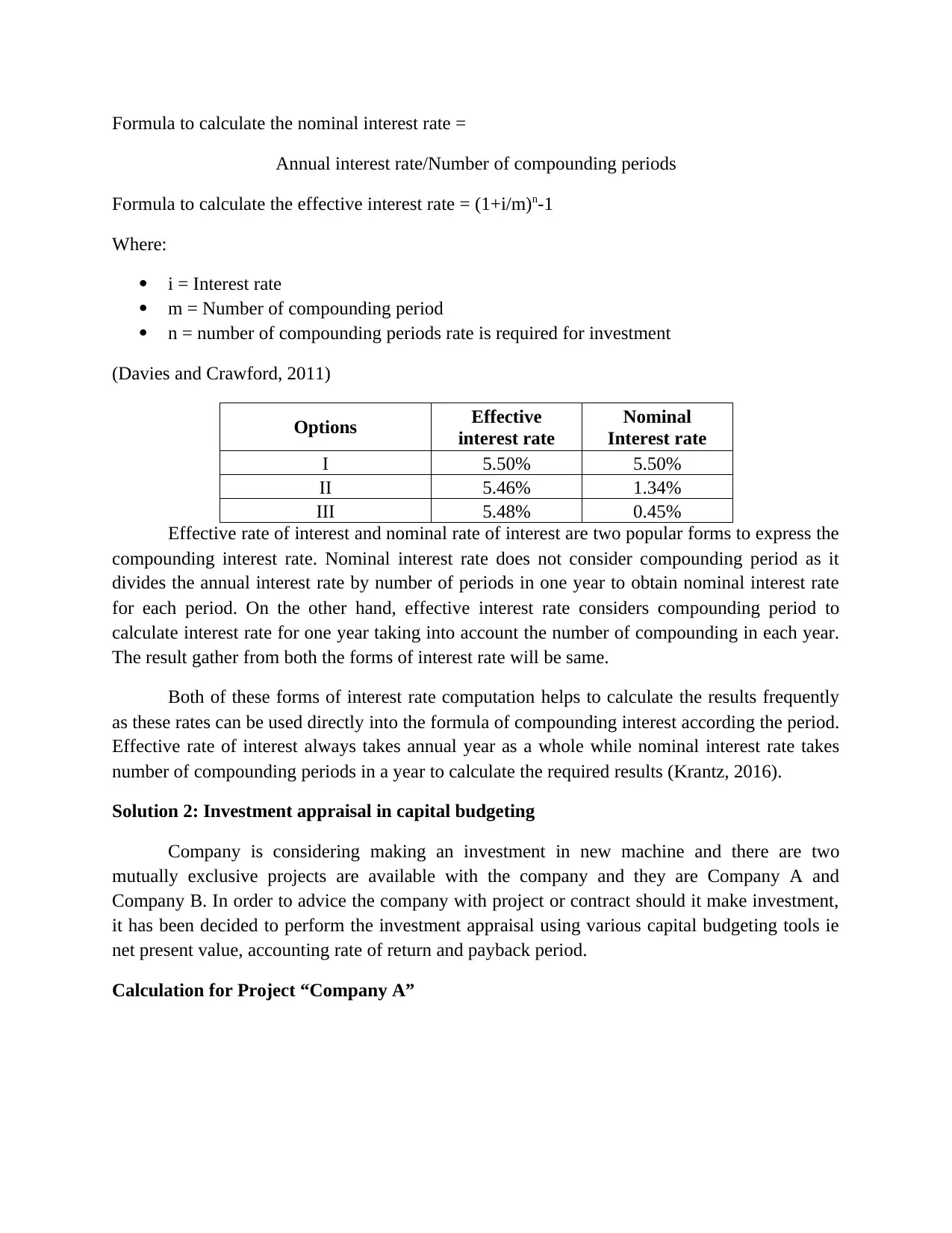

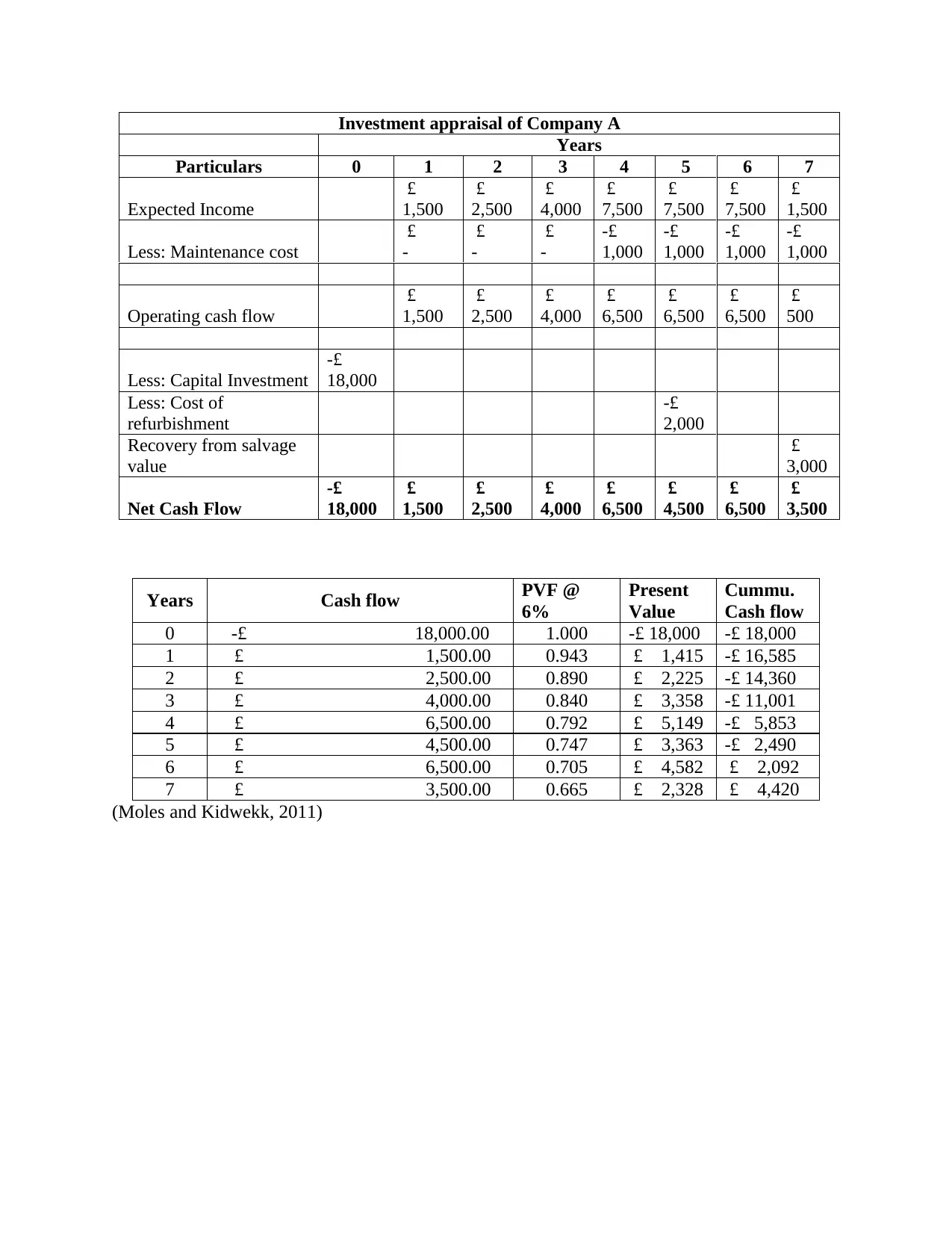

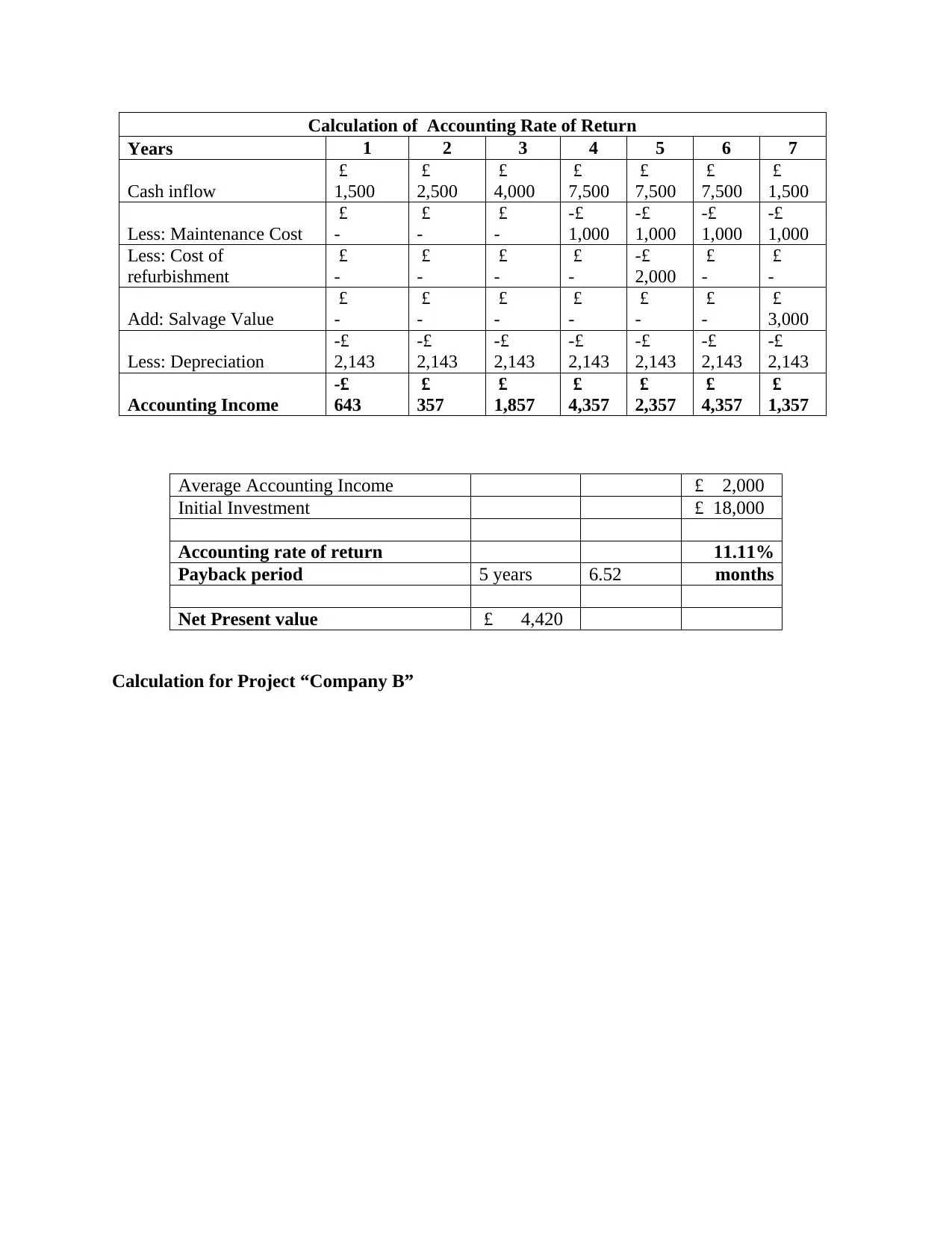

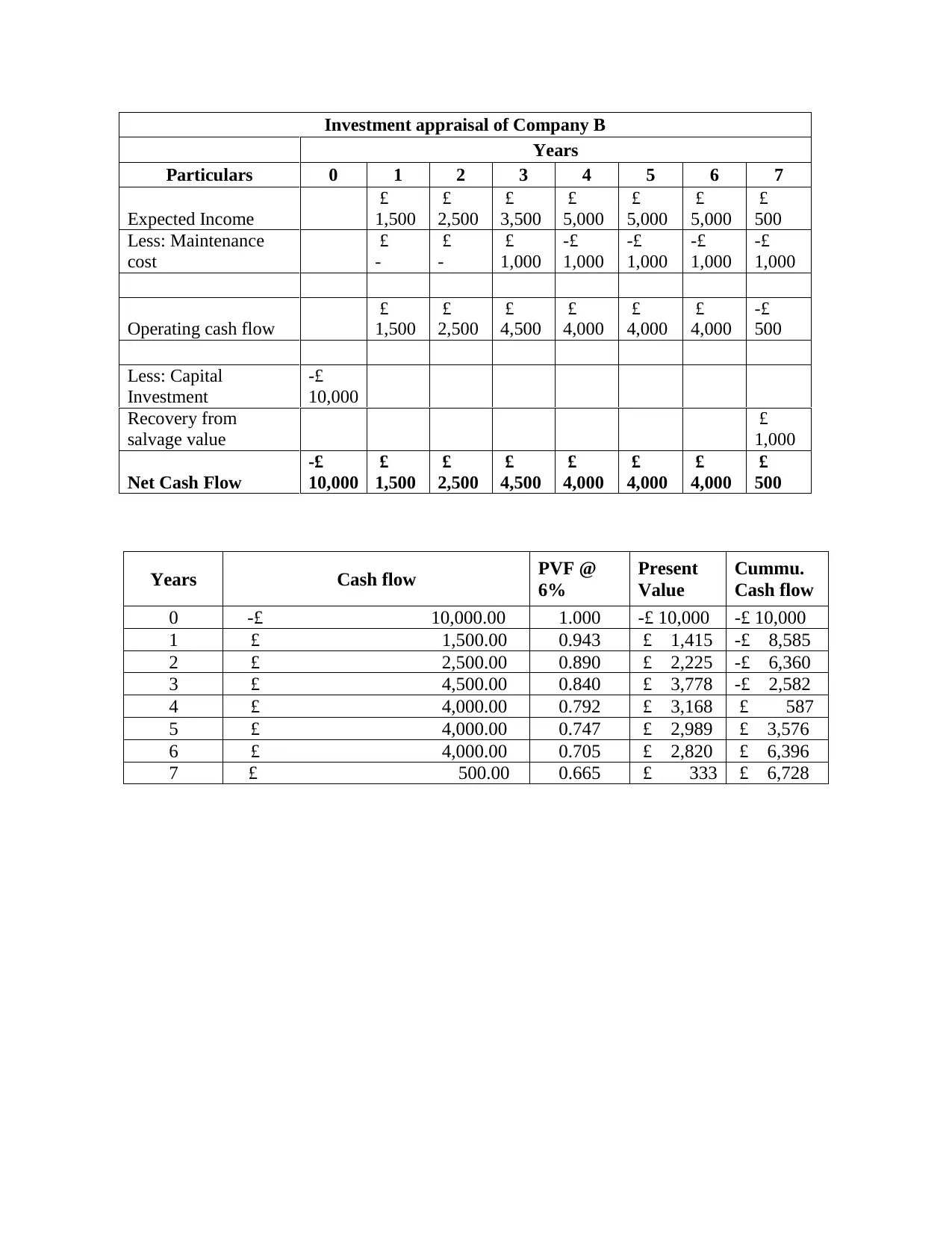

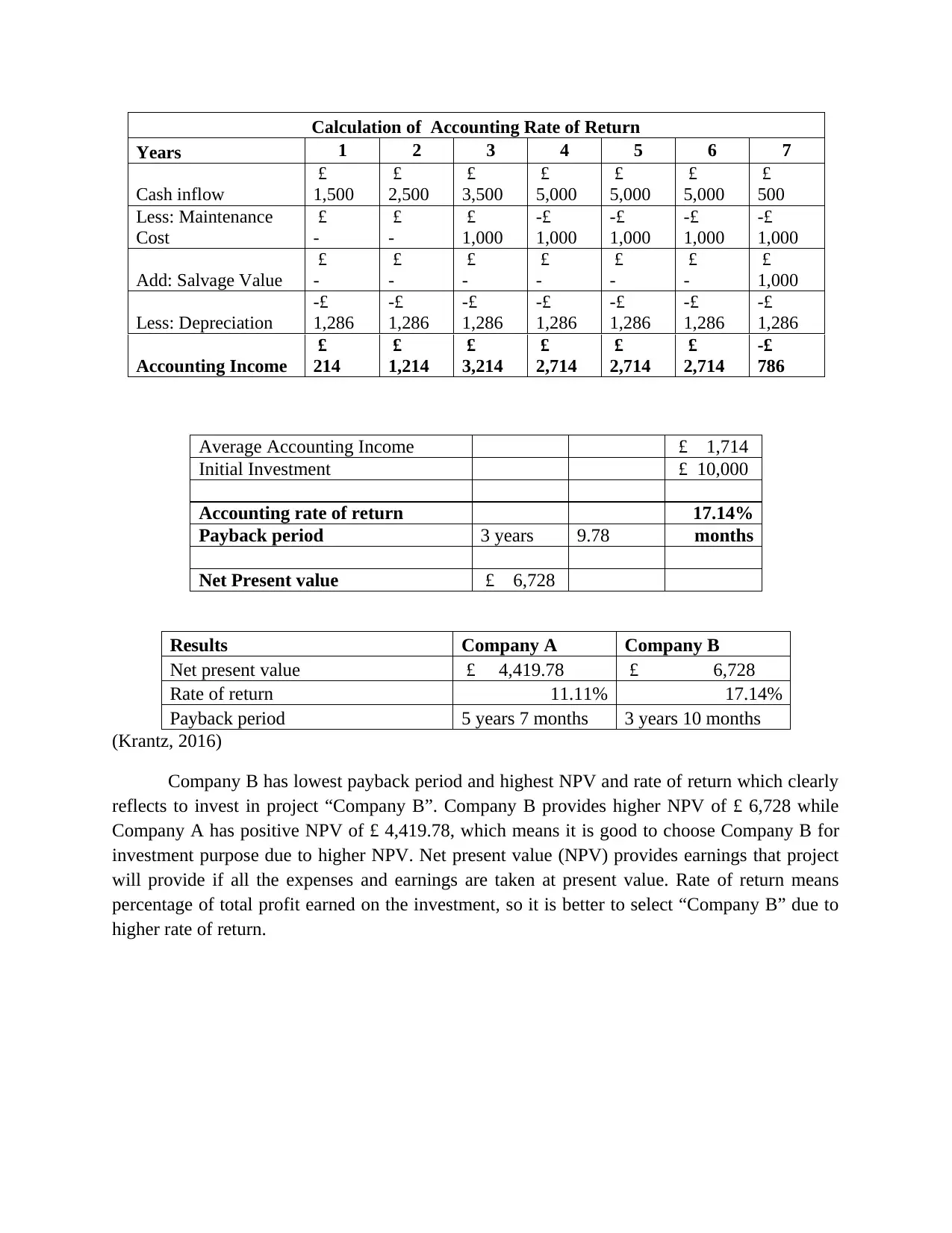

This assignment presents a comprehensive analysis of financial decision-making, focusing on investment appraisal and capital budgeting. The solution begins by evaluating three investment options, calculating the future value of an £8,000 investment over five years with varying compound interest rates (yearly, quarterly, and monthly) to determine the most beneficial option. The second part delves into capital budgeting, comparing two mutually exclusive projects (Company A and Company B) using net present value (NPV), accounting rate of return, and payback period to recommend the optimal investment. The analysis includes detailed calculations for each project, demonstrating how these financial tools guide investment choices. Finally, the assignment concludes with a recommendation, supporting the selection of Project B, and discusses scenarios that could alter this recommendation, such as changes in initial investment, payback period, or rate of return.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.