Capital Budgeting Process: Analyzing Valley University Bus Project

VerifiedAdded on 2023/01/09

|11

|2578

|49

Case Study

AI Summary

This case study examines Valley University's consideration of a dedicated bus service for staff and students, prompting an inquiry to the municipal bus service (MARTS). The analysis employs capital budgeting techniques, including discounted cash flow (DCF) and net present value (NPV), to evaluate the financial viability of the project. Key factors such as capital fund accessibility, rate of return, future earnings, profit estimation, and cash inflows are considered. The critical review and evaluation of the bus service investment include a cost analysis, revenue projections, and recommendations for improving profitability, such as adjusting fare charges and managing driver compensation. The study concludes with an internal rate of return of 25%, a net present value of $2,456, and a payback period of 4 years.

CAPITAL BUDGTING

PROCESS AND

TECHNIQUES

PROCESS AND

TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

CAPITAL BUDGTING PROCESS AND TECHNIQUES.................................................................................... 1

INTRODUCTION....................................................................................................................................... 3

The Bus Decision: A Case Study Employing Capital Budgeting and Creative Thinking................................................3

1. Capital budgeting and creative thinking....................................................................................................... 3

2. Background of the case study of Valley University.......................................................................................... 4

3. Capital Budgeting Process used in the case study........................................................................................... 5

4. Other factors were considered besides Capital financing and allocation functions during Capital Budgeting Process..........6

1. Accessibility of Capital funds................................................................................................................ 6

2. Rate of Return................................................................................................................................... 6

Every investment needs the minimum rate of return for maintaining the minimum cash inflow from the executing

investments. Rate of return of an investments depicts the cash inflow from the investment.........................................6

3. Future Earnings.................................................................................................................................. 6

4. Estimation of Profit............................................................................................................................. 6

5. Cash Inflows..................................................................................................................................... 7

5. Providing critical review and evaluation as well as clarifying the recommendations in relation to the capital invested in this

case study............................................................................................................................................... 7

Factors which are essential to consider as recommendations.................................................................................. 8

CONCLUSION......................................................................................................................................... 10

REFERENCES......................................................................................................................................... 11

CAPITAL BUDGTING PROCESS AND TECHNIQUES.................................................................................... 1

INTRODUCTION....................................................................................................................................... 3

The Bus Decision: A Case Study Employing Capital Budgeting and Creative Thinking................................................3

1. Capital budgeting and creative thinking....................................................................................................... 3

2. Background of the case study of Valley University.......................................................................................... 4

3. Capital Budgeting Process used in the case study........................................................................................... 5

4. Other factors were considered besides Capital financing and allocation functions during Capital Budgeting Process..........6

1. Accessibility of Capital funds................................................................................................................ 6

2. Rate of Return................................................................................................................................... 6

Every investment needs the minimum rate of return for maintaining the minimum cash inflow from the executing

investments. Rate of return of an investments depicts the cash inflow from the investment.........................................6

3. Future Earnings.................................................................................................................................. 6

4. Estimation of Profit............................................................................................................................. 6

5. Cash Inflows..................................................................................................................................... 7

5. Providing critical review and evaluation as well as clarifying the recommendations in relation to the capital invested in this

case study............................................................................................................................................... 7

Factors which are essential to consider as recommendations.................................................................................. 8

CONCLUSION......................................................................................................................................... 10

REFERENCES......................................................................................................................................... 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Capital budgeting or investment appraisal refer to the process of planning applies for

the determination of criteria and outcomes entity's long term investments for example fresh

machinery installation, changing of old machinery, developing new plants and products.

Moreover, investments over research development projects require funding of budget with the

help of firm's capitalization structure which pertains debt, equity or retained earnings of

stakeholders (Gitman and Forrester, 2017).

Furthermore, capital budgeting is the methodology of allocation of resources for

huge capital investments or expenditures. The main objective of capital budgeting investments is

make increment in the value of business entity as well as its shareholders

The Bus Decision: A Case Study Employing Capital Budgeting and Creative Thinking

1. Capital budgeting and creative thinking

Capital budgeting termed as a methodology used for analysis and comparison subsequent

future investments and expenditures for enjoying future opportunities for business entity.

Furthermore, it refers to the process that organizational management adopts for the identification

of capital projects for decision making regarding the future capital investment for estimation

better opportunity for attaining good outcomes. Every investment analyzed on the basis of its

potential future return, so the entity’s managers becomes able to choose the better investment

opportunity. Capital budgeting techniques upon determining cash flow of municipal bus service.

The information is mentioned is on the base of actual bus service. The location is a regional

university based 25 miles away from locality with many staff and student living in the area. Staff

and student have already asked for commute to and from community to Valley university.

As accordance with the case study, Valley University makes an inquiry to the municipal bus

service to open a dedicated bus service to staff and student and what would be the fare charges to

costumers(Haka, Gordon and Pinches, 2015). Hence, it is essential to determine the cash flow

and capital budgeting with effective cost and identifying fare charges through budgeting tools

and analyze the cash flows in account to proposal and analysis for university and community

transit authority

Capital budgeting or investment appraisal refer to the process of planning applies for

the determination of criteria and outcomes entity's long term investments for example fresh

machinery installation, changing of old machinery, developing new plants and products.

Moreover, investments over research development projects require funding of budget with the

help of firm's capitalization structure which pertains debt, equity or retained earnings of

stakeholders (Gitman and Forrester, 2017).

Furthermore, capital budgeting is the methodology of allocation of resources for

huge capital investments or expenditures. The main objective of capital budgeting investments is

make increment in the value of business entity as well as its shareholders

The Bus Decision: A Case Study Employing Capital Budgeting and Creative Thinking

1. Capital budgeting and creative thinking

Capital budgeting termed as a methodology used for analysis and comparison subsequent

future investments and expenditures for enjoying future opportunities for business entity.

Furthermore, it refers to the process that organizational management adopts for the identification

of capital projects for decision making regarding the future capital investment for estimation

better opportunity for attaining good outcomes. Every investment analyzed on the basis of its

potential future return, so the entity’s managers becomes able to choose the better investment

opportunity. Capital budgeting techniques upon determining cash flow of municipal bus service.

The information is mentioned is on the base of actual bus service. The location is a regional

university based 25 miles away from locality with many staff and student living in the area. Staff

and student have already asked for commute to and from community to Valley university.

As accordance with the case study, Valley University makes an inquiry to the municipal bus

service to open a dedicated bus service to staff and student and what would be the fare charges to

costumers(Haka, Gordon and Pinches, 2015). Hence, it is essential to determine the cash flow

and capital budgeting with effective cost and identifying fare charges through budgeting tools

and analyze the cash flows in account to proposal and analysis for university and community

transit authority

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The case study of Valley University is critical and useful as the process of capital budgeting

pertain 3 stages which are as follows:

Brainstorming for identifying several factors such as customer’s need for bus services, bus costs,

other facts which are required to consider while making decision(Block, 2017).

Identify prominent evaluating tools for proper analysis of capital budgeting and its

techniques.

Use of such capital budgeting techniques is to attain the proper estimated results, As in

presented case, the price that must be charged passengers of that devoted commuter bus

line.

2. Background of the case study of Valley University

Anita thought about the travel to work; gas was over $4 a gallon and the car approaches

around 100,000 mile marked. With the discussions of some friends who use the same commute,

they were wondering if a commuter bus can be an option that makes a benefit to which those

drive and the same time is profitable to the Valley University. Anita met with Vice President

Geoff of Business Affairs, to check if Valley University would think to purchase a bus. She

suggests paying whole commuting cost by those who travel to university. Vice President Geoff

met with all staff and the president of the university to approve this service. Post the meeting he

met with Anita to clarify the university’s position. Everyone was ready on the consideration of

bus service, they explained, as the university is not support to the bus service and not having

such equipment, staff and maintenance team so it might lead a loss of money hence this is to

consider to meet with MARTS (Midtown Authority Regional Transit Services) to operating a

dedicated bus line. MARTS known as Public Transportation System in the urbanized midtown

region. Which marks a travels about 1.5 million miles per year. And approx 2,700 people travels

by MARTS buses each day to work, doctor visits, shopping or school. the minimum fare ($1.25

per fixed route), with MARTS. A week later Geoff met with Penny; controller for MARTS.

Penny said that this route is out of their operating line hence they cannot run this service; also it

cannot be subsidized through any public funding. Therefore, the service only be run on entirely

pertain 3 stages which are as follows:

Brainstorming for identifying several factors such as customer’s need for bus services, bus costs,

other facts which are required to consider while making decision(Block, 2017).

Identify prominent evaluating tools for proper analysis of capital budgeting and its

techniques.

Use of such capital budgeting techniques is to attain the proper estimated results, As in

presented case, the price that must be charged passengers of that devoted commuter bus

line.

2. Background of the case study of Valley University

Anita thought about the travel to work; gas was over $4 a gallon and the car approaches

around 100,000 mile marked. With the discussions of some friends who use the same commute,

they were wondering if a commuter bus can be an option that makes a benefit to which those

drive and the same time is profitable to the Valley University. Anita met with Vice President

Geoff of Business Affairs, to check if Valley University would think to purchase a bus. She

suggests paying whole commuting cost by those who travel to university. Vice President Geoff

met with all staff and the president of the university to approve this service. Post the meeting he

met with Anita to clarify the university’s position. Everyone was ready on the consideration of

bus service, they explained, as the university is not support to the bus service and not having

such equipment, staff and maintenance team so it might lead a loss of money hence this is to

consider to meet with MARTS (Midtown Authority Regional Transit Services) to operating a

dedicated bus line. MARTS known as Public Transportation System in the urbanized midtown

region. Which marks a travels about 1.5 million miles per year. And approx 2,700 people travels

by MARTS buses each day to work, doctor visits, shopping or school. the minimum fare ($1.25

per fixed route), with MARTS. A week later Geoff met with Penny; controller for MARTS.

Penny said that this route is out of their operating line hence they cannot run this service; also it

cannot be subsidized through any public funding. Therefore, the service only be run on entirely

by user fares, and would operate on a “for profit” basis. Geoff agrees the term and still wants to

run the service, and asked Penny if a proposal stays on agreement of charging fare from bus

users adding that because the service would be a separate service operated for a profit, they

would arrange or purchase a bus (or busses) for this service besides the existing fleet.

3. Capital Budgeting Process used in the case study

Capital budgeting processes are mainly used for evaluation for making the capital

investment decision. It implies executives of managerial level to estimate the value of the

investment. This all can be attain by using the techniques under the capital budgeting process.

The techniques implied under the presented case study are discounted cash flow (DCF)

technique and net present value (NPV) approach.

Moreover, Capital investment decision generally depends on these estimated of values, several

survey depicts that managerial executives doesn’t always apply DCF techniques, besides this the

techniques such as Payback Period (PP) are also implied by managers for clear and deep

evaluation(Haka, 2017). The result oriented form such techniques depicts existing deficiencies

among estimated results and actual results. After that, the managers of the organization like

MARTS analyze the ways and actions for overcoming the deficiencies arising between the

estimated criteria of capital investments and actual criteria. This all helps in faster and effective

decision making of capital investments or capital budgeting.

Furthermore, under the presented case study the following techniques are used for proper

analysis.

Cash payback – the anticipated period time in the date of a venture and the upturn in

cash of the invested amount

Net present value – In comparison of the amount which is to be invested in present value

of the net cash inflows

Internal rate of return – the rate of return from a capital is determined by using present

value concepts for investment proposal. Interest rate is short by the present value of

future cash flows. The factors shows the rate include the risk of the investment, cost of

obtaining funds, etc. A positive indication of net present value that the present value of

run the service, and asked Penny if a proposal stays on agreement of charging fare from bus

users adding that because the service would be a separate service operated for a profit, they

would arrange or purchase a bus (or busses) for this service besides the existing fleet.

3. Capital Budgeting Process used in the case study

Capital budgeting processes are mainly used for evaluation for making the capital

investment decision. It implies executives of managerial level to estimate the value of the

investment. This all can be attain by using the techniques under the capital budgeting process.

The techniques implied under the presented case study are discounted cash flow (DCF)

technique and net present value (NPV) approach.

Moreover, Capital investment decision generally depends on these estimated of values, several

survey depicts that managerial executives doesn’t always apply DCF techniques, besides this the

techniques such as Payback Period (PP) are also implied by managers for clear and deep

evaluation(Haka, 2017). The result oriented form such techniques depicts existing deficiencies

among estimated results and actual results. After that, the managers of the organization like

MARTS analyze the ways and actions for overcoming the deficiencies arising between the

estimated criteria of capital investments and actual criteria. This all helps in faster and effective

decision making of capital investments or capital budgeting.

Furthermore, under the presented case study the following techniques are used for proper

analysis.

Cash payback – the anticipated period time in the date of a venture and the upturn in

cash of the invested amount

Net present value – In comparison of the amount which is to be invested in present value

of the net cash inflows

Internal rate of return – the rate of return from a capital is determined by using present

value concepts for investment proposal. Interest rate is short by the present value of

future cash flows. The factors shows the rate include the risk of the investment, cost of

obtaining funds, etc. A positive indication of net present value that the present value of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the cash inflows exceeds the sum to be invested, making the investment a desirable

investment and profitable investment.

4. Other factors were considered besides Capital financing and allocation functions during

Capital Budgeting Process

1. Accessibility of Capital funds

There are several kinds of investment proposals in company’s investment portfolio and all

investment requires different amount of funds. Some investments needs heavy funds and

generate heavy profitability. As in case study of MARTS, the fund allocation for the capital

investment is necessary for the firm.

2. Rate of Return

Every investment needs the minimum rate of return for maintaining the minimum cash inflow

from the executing investments. Rate of return of an investments depicts the cash inflow from

the investment.

3. Future Earnings

The future earnings can be stable or unstable in nature. Capital budgeting mainly used for capital

or long term investments which generates long term future earnings for the organization like

MARTS. As in the presented case study the bus generates the long term revenues for the

MARTS.

4. Estimation of Profit

It is essential to appraise the amount of profit estimated over the execution of selected

investment as in above case the bus is termed as the capital investment made by the entity and

before making this investment it is crucial to analyze the profit which may be generated in

future. Here, the word profit depicts realization of amount investment made along with some

more return (Chen, 2008).

investment and profitable investment.

4. Other factors were considered besides Capital financing and allocation functions during

Capital Budgeting Process

1. Accessibility of Capital funds

There are several kinds of investment proposals in company’s investment portfolio and all

investment requires different amount of funds. Some investments needs heavy funds and

generate heavy profitability. As in case study of MARTS, the fund allocation for the capital

investment is necessary for the firm.

2. Rate of Return

Every investment needs the minimum rate of return for maintaining the minimum cash inflow

from the executing investments. Rate of return of an investments depicts the cash inflow from

the investment.

3. Future Earnings

The future earnings can be stable or unstable in nature. Capital budgeting mainly used for capital

or long term investments which generates long term future earnings for the organization like

MARTS. As in the presented case study the bus generates the long term revenues for the

MARTS.

4. Estimation of Profit

It is essential to appraise the amount of profit estimated over the execution of selected

investment as in above case the bus is termed as the capital investment made by the entity and

before making this investment it is crucial to analyze the profit which may be generated in

future. Here, the word profit depicts realization of amount investment made along with some

more return (Chen, 2008).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Cash Inflows

The term cash inflows refer to profit after tax but before depreciation. The reason is that

recording of depreciation is a book entry and there is no actual cash outflow. Hence, depreciation

amount is included in the cash inflow.

After considering the above factors the main complications arises in front of managers to meets

the estimation and actual results as well as to deal with the internal or external factors affecting

the investment decision and its completion (Brijlal, 2008). Some complications as according to

the case study are as follows.

Number of minimum number of passengers required for matching the estimated daily

inflows with the actual inflows.

Analysis of minimum fare which must be charged from each bus passenger.

Deciding the per day running distance of bus and number of laps.

Estimating the running life of bus and its scrap value for the purpose of depreciation.

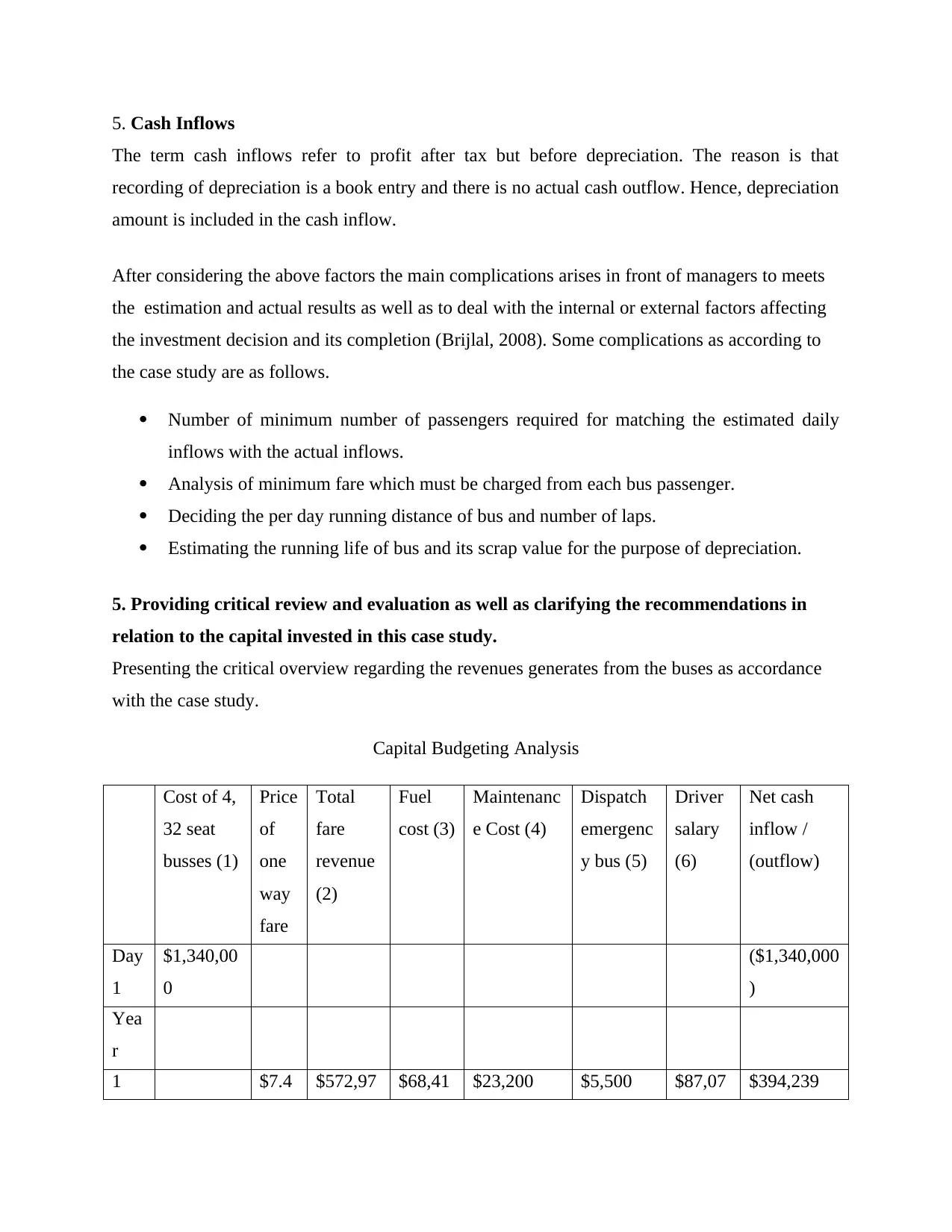

5. Providing critical review and evaluation as well as clarifying the recommendations in

relation to the capital invested in this case study.

Presenting the critical overview regarding the revenues generates from the buses as accordance

with the case study.

Capital Budgeting Analysis

Cost of 4,

32 seat

busses (1)

Price

of

one

way

fare

Total

fare

revenue

(2)

Fuel

cost (3)

Maintenanc

e Cost (4)

Dispatch

emergenc

y bus (5)

Driver

salary

(6)

Net cash

inflow /

(outflow)

Day

1

$1,340,00

0

($1,340,000

)

Yea

r

1 $7.4 $572,97 $68,41 $23,200 $5,500 $87,07 $394,239

The term cash inflows refer to profit after tax but before depreciation. The reason is that

recording of depreciation is a book entry and there is no actual cash outflow. Hence, depreciation

amount is included in the cash inflow.

After considering the above factors the main complications arises in front of managers to meets

the estimation and actual results as well as to deal with the internal or external factors affecting

the investment decision and its completion (Brijlal, 2008). Some complications as according to

the case study are as follows.

Number of minimum number of passengers required for matching the estimated daily

inflows with the actual inflows.

Analysis of minimum fare which must be charged from each bus passenger.

Deciding the per day running distance of bus and number of laps.

Estimating the running life of bus and its scrap value for the purpose of depreciation.

5. Providing critical review and evaluation as well as clarifying the recommendations in

relation to the capital invested in this case study.

Presenting the critical overview regarding the revenues generates from the buses as accordance

with the case study.

Capital Budgeting Analysis

Cost of 4,

32 seat

busses (1)

Price

of

one

way

fare

Total

fare

revenue

(2)

Fuel

cost (3)

Maintenanc

e Cost (4)

Dispatch

emergenc

y bus (5)

Driver

salary

(6)

Net cash

inflow /

(outflow)

Day

1

$1,340,00

0

($1,340,000

)

Yea

r

1 $7.4 $572,97 $68,41 $23,200 $5,500 $87,07 $394,239

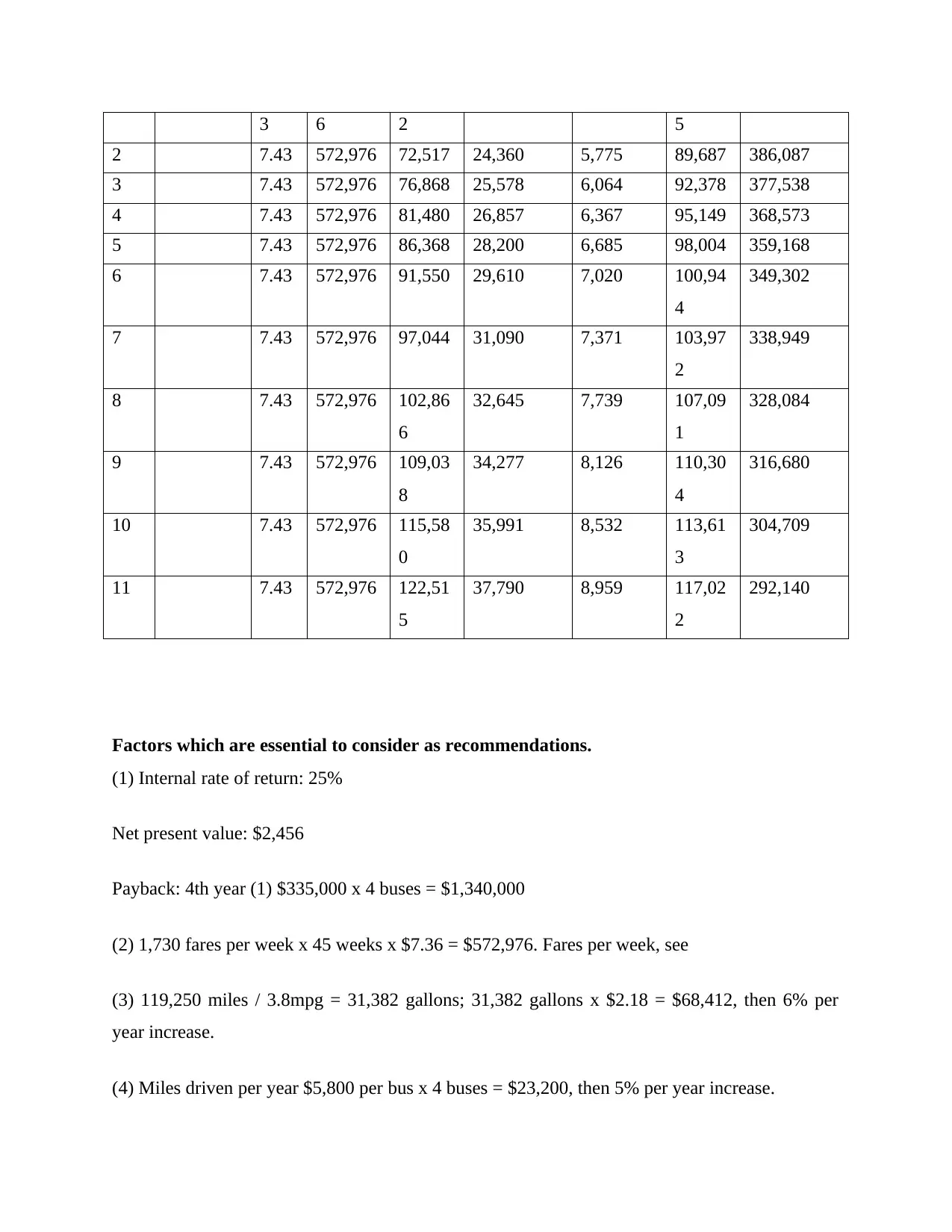

3 6 2 5

2 7.43 572,976 72,517 24,360 5,775 89,687 386,087

3 7.43 572,976 76,868 25,578 6,064 92,378 377,538

4 7.43 572,976 81,480 26,857 6,367 95,149 368,573

5 7.43 572,976 86,368 28,200 6,685 98,004 359,168

6 7.43 572,976 91,550 29,610 7,020 100,94

4

349,302

7 7.43 572,976 97,044 31,090 7,371 103,97

2

338,949

8 7.43 572,976 102,86

6

32,645 7,739 107,09

1

328,084

9 7.43 572,976 109,03

8

34,277 8,126 110,30

4

316,680

10 7.43 572,976 115,58

0

35,991 8,532 113,61

3

304,709

11 7.43 572,976 122,51

5

37,790 8,959 117,02

2

292,140

Factors which are essential to consider as recommendations.

(1) Internal rate of return: 25%

Net present value: $2,456

Payback: 4th year (1) $335,000 x 4 buses = $1,340,000

(2) 1,730 fares per week x 45 weeks x $7.36 = $572,976. Fares per week, see

(3) 119,250 miles / 3.8mpg = 31,382 gallons; 31,382 gallons x $2.18 = $68,412, then 6% per

year increase.

(4) Miles driven per year $5,800 per bus x 4 buses = $23,200, then 5% per year increase.

2 7.43 572,976 72,517 24,360 5,775 89,687 386,087

3 7.43 572,976 76,868 25,578 6,064 92,378 377,538

4 7.43 572,976 81,480 26,857 6,367 95,149 368,573

5 7.43 572,976 86,368 28,200 6,685 98,004 359,168

6 7.43 572,976 91,550 29,610 7,020 100,94

4

349,302

7 7.43 572,976 97,044 31,090 7,371 103,97

2

338,949

8 7.43 572,976 102,86

6

32,645 7,739 107,09

1

328,084

9 7.43 572,976 109,03

8

34,277 8,126 110,30

4

316,680

10 7.43 572,976 115,58

0

35,991 8,532 113,61

3

304,709

11 7.43 572,976 122,51

5

37,790 8,959 117,02

2

292,140

Factors which are essential to consider as recommendations.

(1) Internal rate of return: 25%

Net present value: $2,456

Payback: 4th year (1) $335,000 x 4 buses = $1,340,000

(2) 1,730 fares per week x 45 weeks x $7.36 = $572,976. Fares per week, see

(3) 119,250 miles / 3.8mpg = 31,382 gallons; 31,382 gallons x $2.18 = $68,412, then 6% per

year increase.

(4) Miles driven per year $5,800 per bus x 4 buses = $23,200, then 5% per year increase.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(5) Breakdowns $500 per dispatch x 4 dispatches = $2,000; over capacity $350 per dispatch x 10

dispatches = $3,500;

total $2,000 + $3,500 = $5,500, then 5% per year increase.

(6) $36,500 salary + $21,550 benefits x 1 ½ drivers, then 3% per year increase.

Recommendations for the better implementation of desired investment plan accordance

with the case study.

The MART must increase the fair charges per passenger so, that the revenues and rate of

return increases.

The organization must render the appropriate compensation to driver as the driver’s

salary and maintenance affects the profitability.

Moreover, the entity must appoint a cleaner for the bus cleaning, this will helps in

attaining more satisfaction and helps attaining sustainability standards of investments.

CONCLUSION

On the basis of above case study, it is concluded that capital budgeting is crucial part

managerial activities. The capital budgeting process and its techniques plays a vital role deciding

the business entity's investment decisions. There are several factors like return on investment,

future earnings, allocation of funds for investments etc. which effects the investments decision

and are required to analyze critically with help of capital budgeting techniques.

dispatches = $3,500;

total $2,000 + $3,500 = $5,500, then 5% per year increase.

(6) $36,500 salary + $21,550 benefits x 1 ½ drivers, then 3% per year increase.

Recommendations for the better implementation of desired investment plan accordance

with the case study.

The MART must increase the fair charges per passenger so, that the revenues and rate of

return increases.

The organization must render the appropriate compensation to driver as the driver’s

salary and maintenance affects the profitability.

Moreover, the entity must appoint a cleaner for the bus cleaning, this will helps in

attaining more satisfaction and helps attaining sustainability standards of investments.

CONCLUSION

On the basis of above case study, it is concluded that capital budgeting is crucial part

managerial activities. The capital budgeting process and its techniques plays a vital role deciding

the business entity's investment decisions. There are several factors like return on investment,

future earnings, allocation of funds for investments etc. which effects the investments decision

and are required to analyze critically with help of capital budgeting techniques.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Gitman, L.J. and Forrester Jr, J.R., 2017. A survey of capital budgeting techniques used by major

US firms. Financial management, pp.66-71

Haka, S.F., Gordon, L.A. and Pinches, G.E., 2015. Sophisticated capital budgeting selection

techniques and firm performance. In Readings in Accounting for Management Control (pp. 521-

545). Springer, Boston, MA.

Block, S., 2017. Capital budgeting techniques used by small business firms in the 1990s. The

engineering economist, 42(4), pp.289-302.

Haka, S.F., 2017. Capital budgeting techniques and firm specific contingencies: a correlational

analysis. Accounting, Organizations and Society, 12(1), pp.31-48.

Chen, S., 2008. DCF techniques and nonfinancial measures in capital budgeting: a contingency

approach analysis. Behavioral research in accounting, 20(1), pp.13-29.

Brijlal, P., 2008, August. The use of capital budgeting techniques in businesses: A perspective

from the Western Cape. In 21st Australasian Finance and Banking Conference.

Books and Journals

Gitman, L.J. and Forrester Jr, J.R., 2017. A survey of capital budgeting techniques used by major

US firms. Financial management, pp.66-71

Haka, S.F., Gordon, L.A. and Pinches, G.E., 2015. Sophisticated capital budgeting selection

techniques and firm performance. In Readings in Accounting for Management Control (pp. 521-

545). Springer, Boston, MA.

Block, S., 2017. Capital budgeting techniques used by small business firms in the 1990s. The

engineering economist, 42(4), pp.289-302.

Haka, S.F., 2017. Capital budgeting techniques and firm specific contingencies: a correlational

analysis. Accounting, Organizations and Society, 12(1), pp.31-48.

Chen, S., 2008. DCF techniques and nonfinancial measures in capital budgeting: a contingency

approach analysis. Behavioral research in accounting, 20(1), pp.13-29.

Brijlal, P., 2008, August. The use of capital budgeting techniques in businesses: A perspective

from the Western Cape. In 21st Australasian Finance and Banking Conference.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.