Capital Budgeting and Cost of Capital Analysis Homework, University

VerifiedAdded on 2022/09/01

|12

|1855

|16

Homework Assignment

AI Summary

This assignment is a comprehensive analysis of capital budgeting techniques, focusing on a project's financial viability. It begins with calculating after-tax cash flows, including initial investment, salvage value, and working capital. Key financial metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and profitability index are calculated and evaluated. The analysis explores the impact of revenue and cost fluctuations on project acceptance, followed by a discussion on capital budgeting decisions for mutually exclusive projects with unequal lifespans. The assignment then delves into the cost of capital, including the value and cost of debt, preference shares, and ordinary shares, culminating in the calculation of the Weighted Average Cost of Capital (WACC). Finally, it examines how a change in the cost of capital affects the company's valuation.

Running head: MASTERS OF PROFESSIONAL ACCOUNTING

Masters of Professional Accounting

Name of the Student:

Name of the University:

Author’s Note:

Masters of Professional Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MASTERS OF PROFESSIONAL ACCOUNTING

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................5

Question 5........................................................................................................................................6

Question 6........................................................................................................................................6

Question 7........................................................................................................................................7

Question 8........................................................................................................................................8

Question 9........................................................................................................................................8

References......................................................................................................................................10

Table of Contents

Question 1........................................................................................................................................2

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................5

Question 5........................................................................................................................................6

Question 6........................................................................................................................................6

Question 7........................................................................................................................................7

Question 8........................................................................................................................................8

Question 9........................................................................................................................................8

References......................................................................................................................................10

2MASTERS OF PROFESSIONAL ACCOUNTING

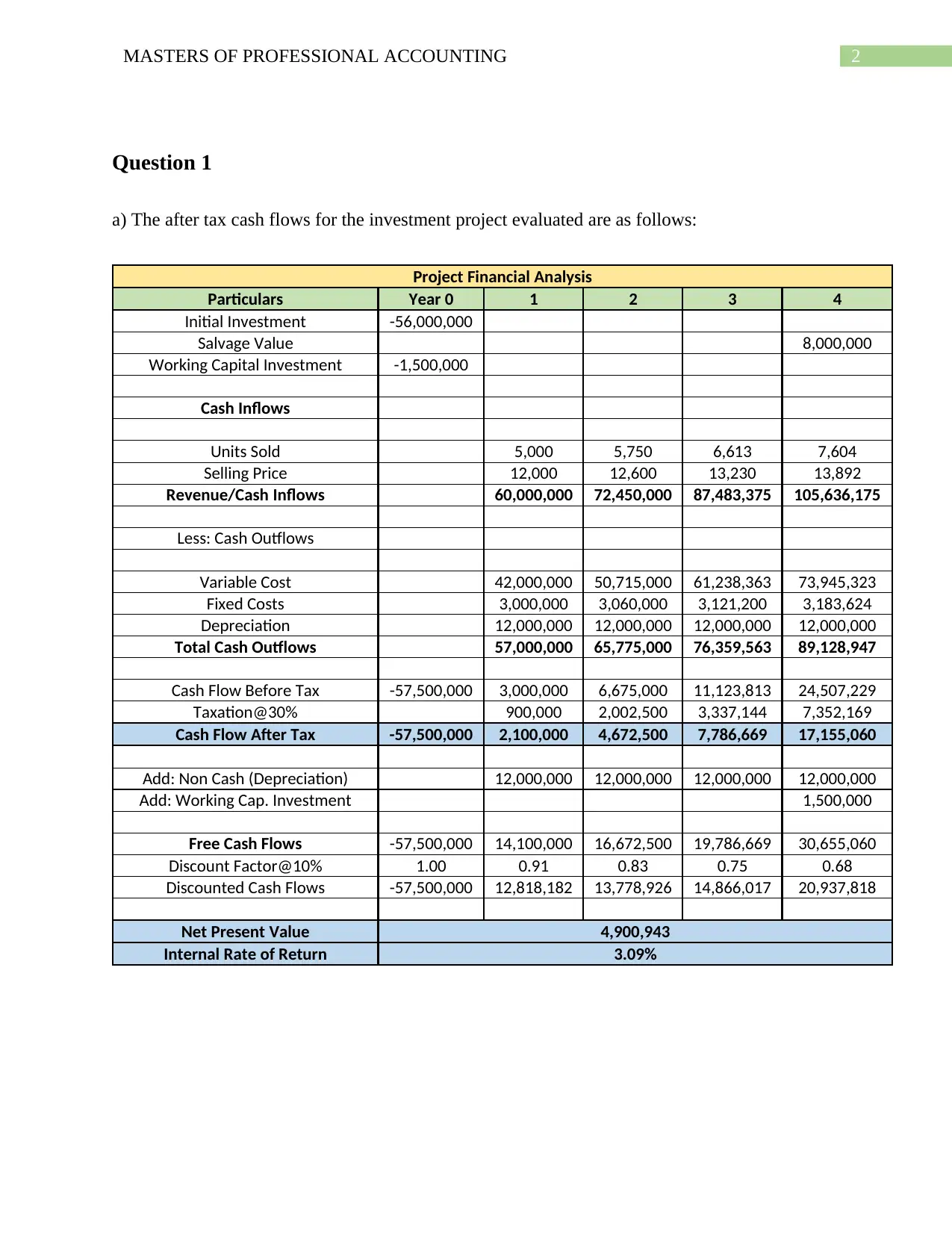

Question 1

a) The after tax cash flows for the investment project evaluated are as follows:

Project Financial Analysis

Particulars Year 0 1 2 3 4

Initial Investment -56,000,000

Salvage Value 8,000,000

Working Capital Investment -1,500,000

Cash Inflows

Units Sold 5,000 5,750 6,613 7,604

Selling Price 12,000 12,600 13,230 13,892

Revenue/Cash Inflows 60,000,000 72,450,000 87,483,375 105,636,175

Less: Cash Outflows

Variable Cost 42,000,000 50,715,000 61,238,363 73,945,323

Fixed Costs 3,000,000 3,060,000 3,121,200 3,183,624

Depreciation 12,000,000 12,000,000 12,000,000 12,000,000

Total Cash Outflows 57,000,000 65,775,000 76,359,563 89,128,947

Cash Flow Before Tax -57,500,000 3,000,000 6,675,000 11,123,813 24,507,229

Taxation@30% 900,000 2,002,500 3,337,144 7,352,169

Cash Flow After Tax -57,500,000 2,100,000 4,672,500 7,786,669 17,155,060

Add: Non Cash (Depreciation) 12,000,000 12,000,000 12,000,000 12,000,000

Add: Working Cap. Investment 1,500,000

Free Cash Flows -57,500,000 14,100,000 16,672,500 19,786,669 30,655,060

Discount Factor@10% 1.00 0.91 0.83 0.75 0.68

Discounted Cash Flows -57,500,000 12,818,182 13,778,926 14,866,017 20,937,818

Net Present Value 4,900,943

Internal Rate of Return 3.09%

Question 1

a) The after tax cash flows for the investment project evaluated are as follows:

Project Financial Analysis

Particulars Year 0 1 2 3 4

Initial Investment -56,000,000

Salvage Value 8,000,000

Working Capital Investment -1,500,000

Cash Inflows

Units Sold 5,000 5,750 6,613 7,604

Selling Price 12,000 12,600 13,230 13,892

Revenue/Cash Inflows 60,000,000 72,450,000 87,483,375 105,636,175

Less: Cash Outflows

Variable Cost 42,000,000 50,715,000 61,238,363 73,945,323

Fixed Costs 3,000,000 3,060,000 3,121,200 3,183,624

Depreciation 12,000,000 12,000,000 12,000,000 12,000,000

Total Cash Outflows 57,000,000 65,775,000 76,359,563 89,128,947

Cash Flow Before Tax -57,500,000 3,000,000 6,675,000 11,123,813 24,507,229

Taxation@30% 900,000 2,002,500 3,337,144 7,352,169

Cash Flow After Tax -57,500,000 2,100,000 4,672,500 7,786,669 17,155,060

Add: Non Cash (Depreciation) 12,000,000 12,000,000 12,000,000 12,000,000

Add: Working Cap. Investment 1,500,000

Free Cash Flows -57,500,000 14,100,000 16,672,500 19,786,669 30,655,060

Discount Factor@10% 1.00 0.91 0.83 0.75 0.68

Discounted Cash Flows -57,500,000 12,818,182 13,778,926 14,866,017 20,937,818

Net Present Value 4,900,943

Internal Rate of Return 3.09%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MASTERS OF PROFESSIONAL ACCOUNTING

b) In the project analyzed the payback period stands out to be around 3.23 years whereby the

payback period exceeds the criteria point of time and it is advisable that the project should not be

accepted based on the given set of criteria (Vartiainen et al., 2019).

c) The net present value that has been derived from the project has been around $4,900,943

stating that the project should be accepted.

d) The profitability index for the project is around $1.09 stating that for every single $1 invested

the project would be generating $1.09 for the shareholders of the company.

Question 2

The project investment analysis has been done by taking all the cash inflows and cash outflows

that the company will be experiencing with respect to the proposed project and the benefits that

would be flowing to the company. The key capital budgeting tools that have been used for the

analysis of the cash flows generated from the project is NPV, IRR, Payback Period and

Profitability Index El (Ghoul et al., 2018). The net present value that has been derived from the

project has been around $4,900,943 stating that the project should be accepted as the project

would be increasing the shareholders wealth by the stated answer. The project would be creating

an additional value in terms of shareholder’s wealth. Profitability Index for the project shows the

extra benefit that has been created by the project with the help or with the undertaken project on

every single dollar that has been invested by the company. The profitability index for the project

is around $1.09 stating that for every single $1 invested the project would be generating $1.09

for the shareholders of the company (Frank & Shen, 2016). Payback Period for the project shows

the amount of time that has been taken by the project for returning back the initial investment

amount. The analyzed project has a criteria of three years which states that the project’s payback

b) In the project analyzed the payback period stands out to be around 3.23 years whereby the

payback period exceeds the criteria point of time and it is advisable that the project should not be

accepted based on the given set of criteria (Vartiainen et al., 2019).

c) The net present value that has been derived from the project has been around $4,900,943

stating that the project should be accepted.

d) The profitability index for the project is around $1.09 stating that for every single $1 invested

the project would be generating $1.09 for the shareholders of the company.

Question 2

The project investment analysis has been done by taking all the cash inflows and cash outflows

that the company will be experiencing with respect to the proposed project and the benefits that

would be flowing to the company. The key capital budgeting tools that have been used for the

analysis of the cash flows generated from the project is NPV, IRR, Payback Period and

Profitability Index El (Ghoul et al., 2018). The net present value that has been derived from the

project has been around $4,900,943 stating that the project should be accepted as the project

would be increasing the shareholders wealth by the stated answer. The project would be creating

an additional value in terms of shareholder’s wealth. Profitability Index for the project shows the

extra benefit that has been created by the project with the help or with the undertaken project on

every single dollar that has been invested by the company. The profitability index for the project

is around $1.09 stating that for every single $1 invested the project would be generating $1.09

for the shareholders of the company (Frank & Shen, 2016). Payback Period for the project shows

the amount of time that has been taken by the project for returning back the initial investment

amount. The analyzed project has a criteria of three years which states that the project’s payback

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MASTERS OF PROFESSIONAL ACCOUNTING

period got to be equal to or less than three years of time frame so that the project is accepted. In

the project analyzed the payback period stands out to be around 3.23 years whereby the payback

period exceeds the criteria point of time and it is advisable that the project should not be

accepted based on the given set of criteria (Liu & Wysocki, 2017).

Question 3

If the revenue grows at 0% and increase in variable cost occurs by 5% then the project

might not be accepted as the same would be a negative NPV, the projects payback at the same

time increases and the profitability index for the project comes to around 0.74 times as shown

below:

period got to be equal to or less than three years of time frame so that the project is accepted. In

the project analyzed the payback period stands out to be around 3.23 years whereby the payback

period exceeds the criteria point of time and it is advisable that the project should not be

accepted based on the given set of criteria (Liu & Wysocki, 2017).

Question 3

If the revenue grows at 0% and increase in variable cost occurs by 5% then the project

might not be accepted as the same would be a negative NPV, the projects payback at the same

time increases and the profitability index for the project comes to around 0.74 times as shown

below:

5MASTERS OF PROFESSIONAL ACCOUNTING

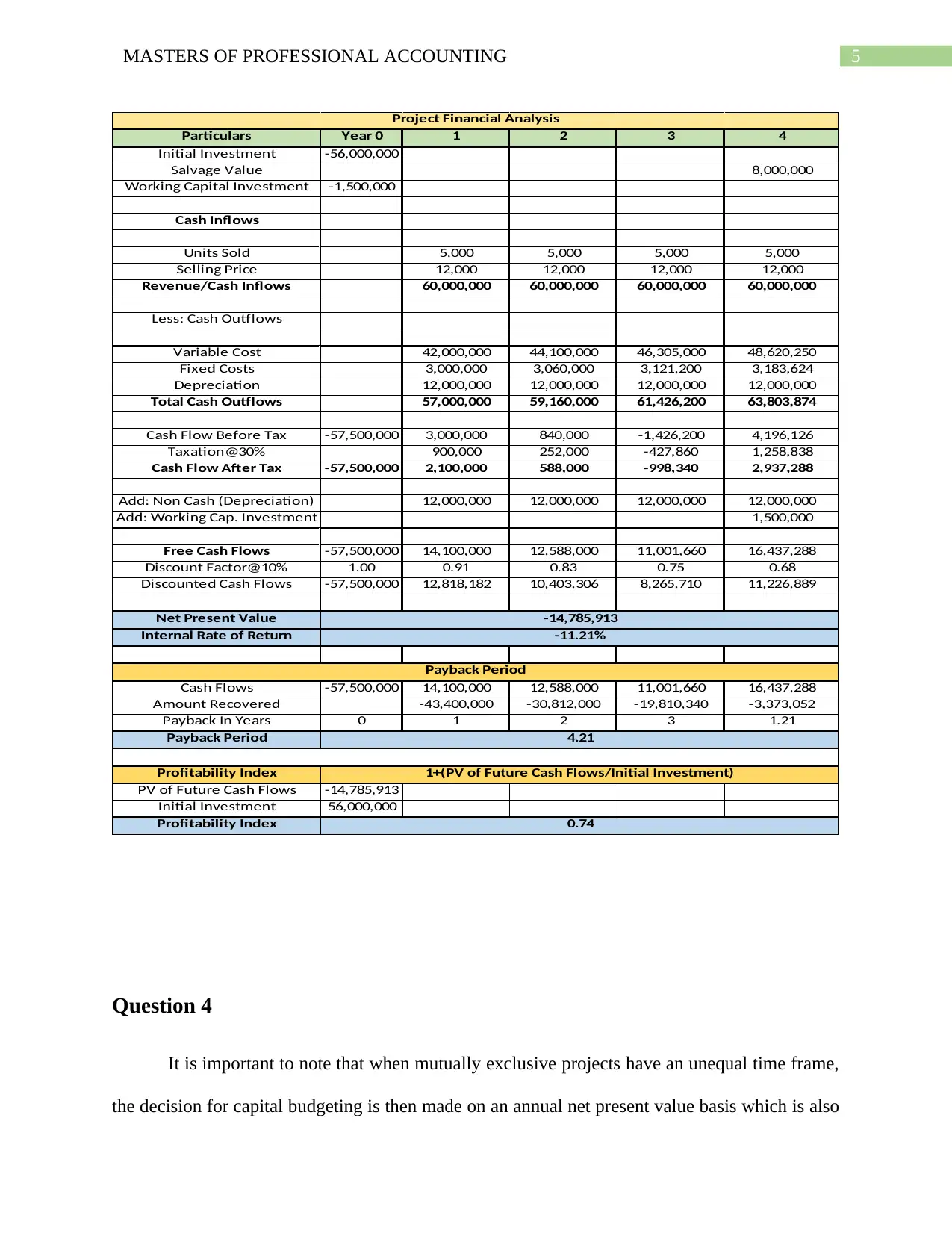

Question 4

It is important to note that when mutually exclusive projects have an unequal time frame,

the decision for capital budgeting is then made on an annual net present value basis which is also

Particulars Year 0 1 2 3 4

Initial Investment -56,000,000

Salvage Value 8,000,000

Working Capital Investment -1,500,000

Cash Inflows

Units Sold 5,000 5,000 5,000 5,000

Selling Price 12,000 12,000 12,000 12,000

Revenue/Cash Inflows 60,000,000 60,000,000 60,000,000 60,000,000

Less: Cash Outflows

Variable Cost 42,000,000 44,100,000 46,305,000 48,620,250

Fixed Costs 3,000,000 3,060,000 3,121,200 3,183,624

Depreciation 12,000,000 12,000,000 12,000,000 12,000,000

Total Cash Outflows 57,000,000 59,160,000 61,426,200 63,803,874

Cash Flow Before Tax -57,500,000 3,000,000 840,000 -1,426,200 4,196,126

Taxation@30% 900,000 252,000 -427,860 1,258,838

Cash Flow After Tax -57,500,000 2,100,000 588,000 -998,340 2,937,288

Add: Non Cash (Depreciation) 12,000,000 12,000,000 12,000,000 12,000,000

Add: Working Cap. Investment 1,500,000

Free Cash Flows -57,500,000 14,100,000 12,588,000 11,001,660 16,437,288

Discount Factor@10% 1.00 0.91 0.83 0.75 0.68

Discounted Cash Flows -57,500,000 12,818,182 10,403,306 8,265,710 11,226,889

Net Present Value

Internal Rate of Return

Cash Flows -57,500,000 14,100,000 12,588,000 11,001,660 16,437,288

Amount Recovered -43,400,000 -30,812,000 -19,810,340 -3,373,052

Payback In Years 0 1 2 3 1.21

Payback Period

Profitability Index

PV of Future Cash Flows -14,785,913

Initial Investment 56,000,000

Profitability Index

1+(PV of Future Cash Flows/Initial Investment)

0.74

Project Financial Analysis

-14,785,913

-11.21%

Payback Period

4.21

Question 4

It is important to note that when mutually exclusive projects have an unequal time frame,

the decision for capital budgeting is then made on an annual net present value basis which is also

Particulars Year 0 1 2 3 4

Initial Investment -56,000,000

Salvage Value 8,000,000

Working Capital Investment -1,500,000

Cash Inflows

Units Sold 5,000 5,000 5,000 5,000

Selling Price 12,000 12,000 12,000 12,000

Revenue/Cash Inflows 60,000,000 60,000,000 60,000,000 60,000,000

Less: Cash Outflows

Variable Cost 42,000,000 44,100,000 46,305,000 48,620,250

Fixed Costs 3,000,000 3,060,000 3,121,200 3,183,624

Depreciation 12,000,000 12,000,000 12,000,000 12,000,000

Total Cash Outflows 57,000,000 59,160,000 61,426,200 63,803,874

Cash Flow Before Tax -57,500,000 3,000,000 840,000 -1,426,200 4,196,126

Taxation@30% 900,000 252,000 -427,860 1,258,838

Cash Flow After Tax -57,500,000 2,100,000 588,000 -998,340 2,937,288

Add: Non Cash (Depreciation) 12,000,000 12,000,000 12,000,000 12,000,000

Add: Working Cap. Investment 1,500,000

Free Cash Flows -57,500,000 14,100,000 12,588,000 11,001,660 16,437,288

Discount Factor@10% 1.00 0.91 0.83 0.75 0.68

Discounted Cash Flows -57,500,000 12,818,182 10,403,306 8,265,710 11,226,889

Net Present Value

Internal Rate of Return

Cash Flows -57,500,000 14,100,000 12,588,000 11,001,660 16,437,288

Amount Recovered -43,400,000 -30,812,000 -19,810,340 -3,373,052

Payback In Years 0 1 2 3 1.21

Payback Period

Profitability Index

PV of Future Cash Flows -14,785,913

Initial Investment 56,000,000

Profitability Index

1+(PV of Future Cash Flows/Initial Investment)

0.74

Project Financial Analysis

-14,785,913

-11.21%

Payback Period

4.21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MASTERS OF PROFESSIONAL ACCOUNTING

referred as Equivalent Annual Annuity method or the replacement chain of method (Shivaani,

Jain & Yadav, 2017). In the case of EAA approach the projects are ranked based on the NPV per

year calculated by dividing the NPV by the present value of annuity factor which is well in

correspondence to the hurdle rate and the life period of the project.

Annual Net Present Value =

Net Present Value

Annuity Discount Factor for the Project

Life

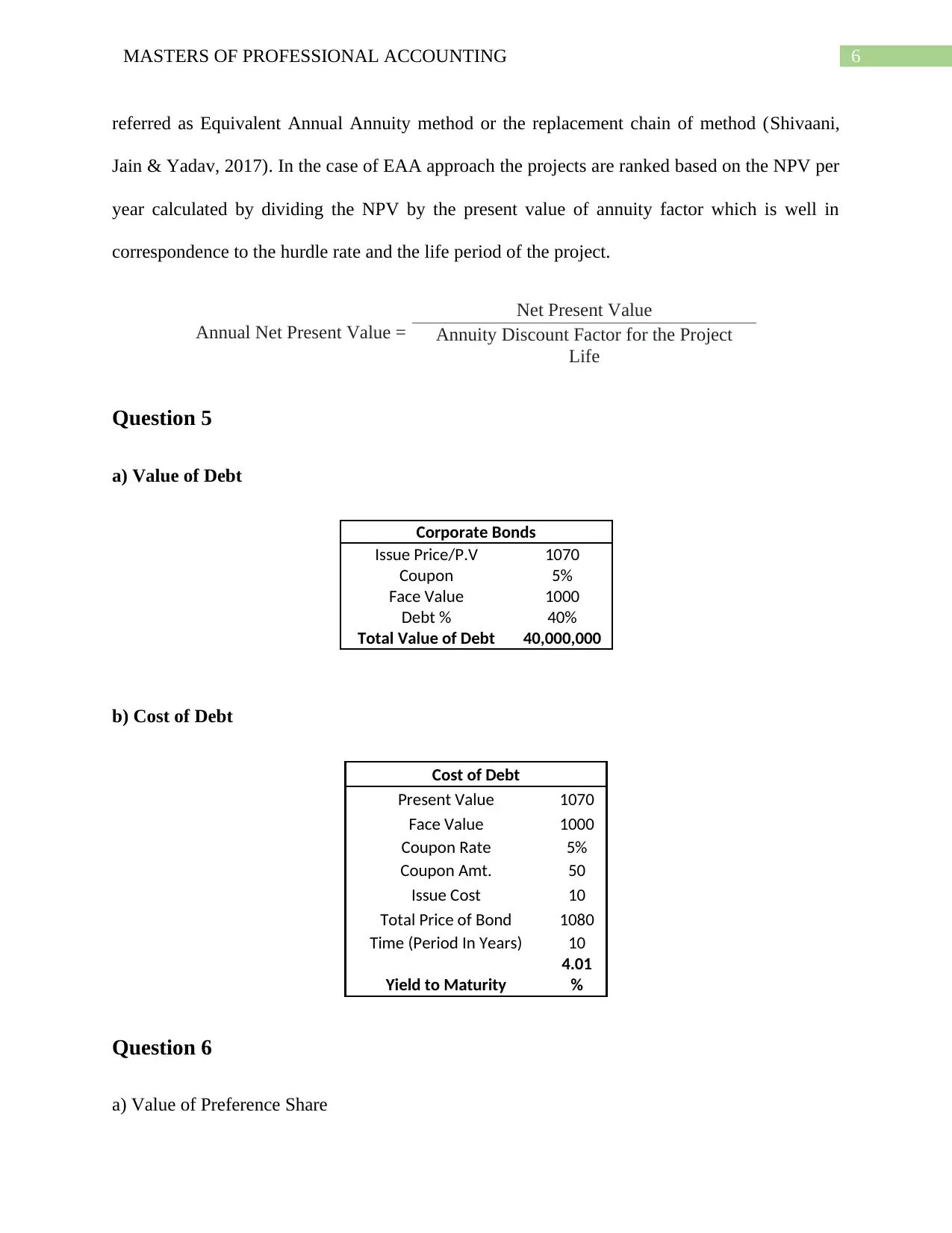

Question 5

a) Value of Debt

Corporate Bonds

Issue Price/P.V 1070

Coupon 5%

Face Value 1000

Debt % 40%

Total Value of Debt 40,000,000

b) Cost of Debt

Cost of Debt

Present Value 1070

Face Value 1000

Coupon Rate 5%

Coupon Amt. 50

Issue Cost 10

Total Price of Bond 1080

Time (Period In Years) 10

Yield to Maturity

4.01

%

Question 6

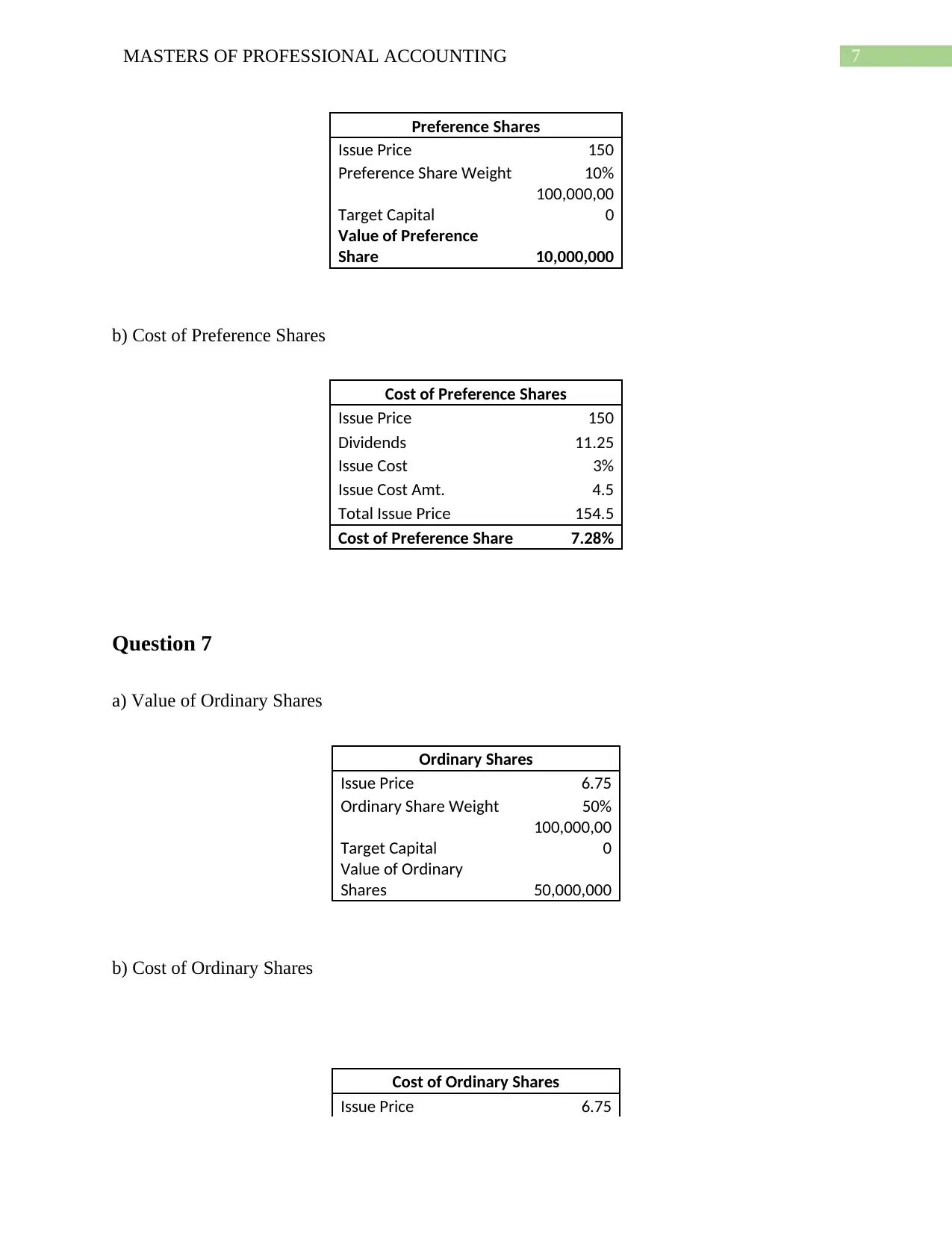

a) Value of Preference Share

referred as Equivalent Annual Annuity method or the replacement chain of method (Shivaani,

Jain & Yadav, 2017). In the case of EAA approach the projects are ranked based on the NPV per

year calculated by dividing the NPV by the present value of annuity factor which is well in

correspondence to the hurdle rate and the life period of the project.

Annual Net Present Value =

Net Present Value

Annuity Discount Factor for the Project

Life

Question 5

a) Value of Debt

Corporate Bonds

Issue Price/P.V 1070

Coupon 5%

Face Value 1000

Debt % 40%

Total Value of Debt 40,000,000

b) Cost of Debt

Cost of Debt

Present Value 1070

Face Value 1000

Coupon Rate 5%

Coupon Amt. 50

Issue Cost 10

Total Price of Bond 1080

Time (Period In Years) 10

Yield to Maturity

4.01

%

Question 6

a) Value of Preference Share

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MASTERS OF PROFESSIONAL ACCOUNTING

Preference Shares

Issue Price 150

Preference Share Weight 10%

Target Capital

100,000,00

0

Value of Preference

Share 10,000,000

b) Cost of Preference Shares

Cost of Preference Shares

Issue Price 150

Dividends 11.25

Issue Cost 3%

Issue Cost Amt. 4.5

Total Issue Price 154.5

Cost of Preference Share 7.28%

Question 7

a) Value of Ordinary Shares

Ordinary Shares

Issue Price 6.75

Ordinary Share Weight 50%

Target Capital

100,000,00

0

Value of Ordinary

Shares 50,000,000

b) Cost of Ordinary Shares

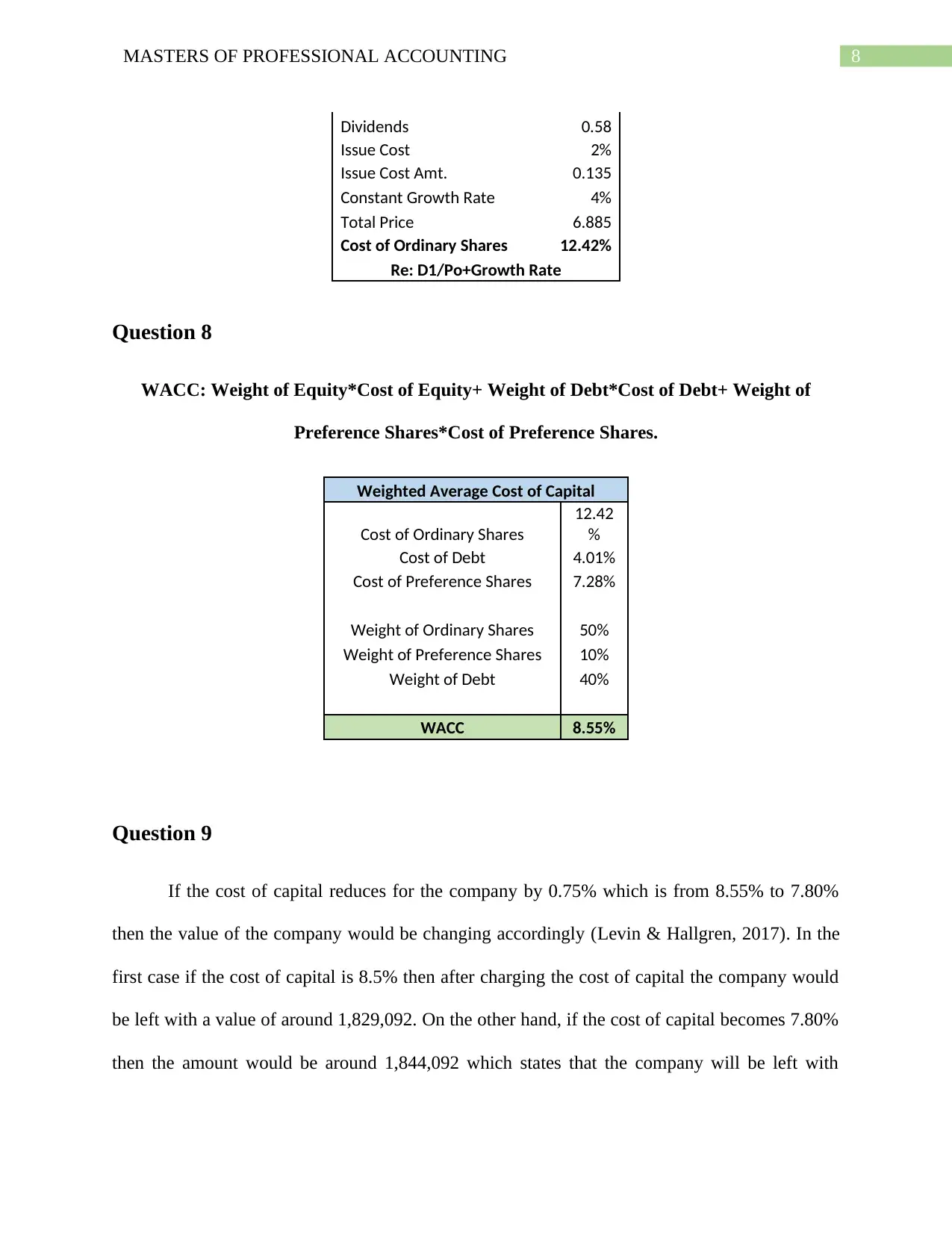

Cost of Ordinary Shares

Issue Price 6.75

Preference Shares

Issue Price 150

Preference Share Weight 10%

Target Capital

100,000,00

0

Value of Preference

Share 10,000,000

b) Cost of Preference Shares

Cost of Preference Shares

Issue Price 150

Dividends 11.25

Issue Cost 3%

Issue Cost Amt. 4.5

Total Issue Price 154.5

Cost of Preference Share 7.28%

Question 7

a) Value of Ordinary Shares

Ordinary Shares

Issue Price 6.75

Ordinary Share Weight 50%

Target Capital

100,000,00

0

Value of Ordinary

Shares 50,000,000

b) Cost of Ordinary Shares

Cost of Ordinary Shares

Issue Price 6.75

8MASTERS OF PROFESSIONAL ACCOUNTING

Dividends 0.58

Issue Cost 2%

Issue Cost Amt. 0.135

Constant Growth Rate 4%

Total Price 6.885

Cost of Ordinary Shares 12.42%

Re: D1/Po+Growth Rate

Question 8

WACC: Weight of Equity*Cost of Equity+ Weight of Debt*Cost of Debt+ Weight of

Preference Shares*Cost of Preference Shares.

Weighted Average Cost of Capital

Cost of Ordinary Shares

12.42

%

Cost of Debt 4.01%

Cost of Preference Shares 7.28%

Weight of Ordinary Shares 50%

Weight of Preference Shares 10%

Weight of Debt 40%

WACC 8.55%

Question 9

If the cost of capital reduces for the company by 0.75% which is from 8.55% to 7.80%

then the value of the company would be changing accordingly (Levin & Hallgren, 2017). In the

first case if the cost of capital is 8.5% then after charging the cost of capital the company would

be left with a value of around 1,829,092. On the other hand, if the cost of capital becomes 7.80%

then the amount would be around 1,844,092 which states that the company will be left with

Dividends 0.58

Issue Cost 2%

Issue Cost Amt. 0.135

Constant Growth Rate 4%

Total Price 6.885

Cost of Ordinary Shares 12.42%

Re: D1/Po+Growth Rate

Question 8

WACC: Weight of Equity*Cost of Equity+ Weight of Debt*Cost of Debt+ Weight of

Preference Shares*Cost of Preference Shares.

Weighted Average Cost of Capital

Cost of Ordinary Shares

12.42

%

Cost of Debt 4.01%

Cost of Preference Shares 7.28%

Weight of Ordinary Shares 50%

Weight of Preference Shares 10%

Weight of Debt 40%

WACC 8.55%

Question 9

If the cost of capital reduces for the company by 0.75% which is from 8.55% to 7.80%

then the value of the company would be changing accordingly (Levin & Hallgren, 2017). In the

first case if the cost of capital is 8.5% then after charging the cost of capital the company would

be left with a value of around 1,829,092. On the other hand, if the cost of capital becomes 7.80%

then the amount would be around 1,844,092 which states that the company will be left with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MASTERS OF PROFESSIONAL ACCOUNTING

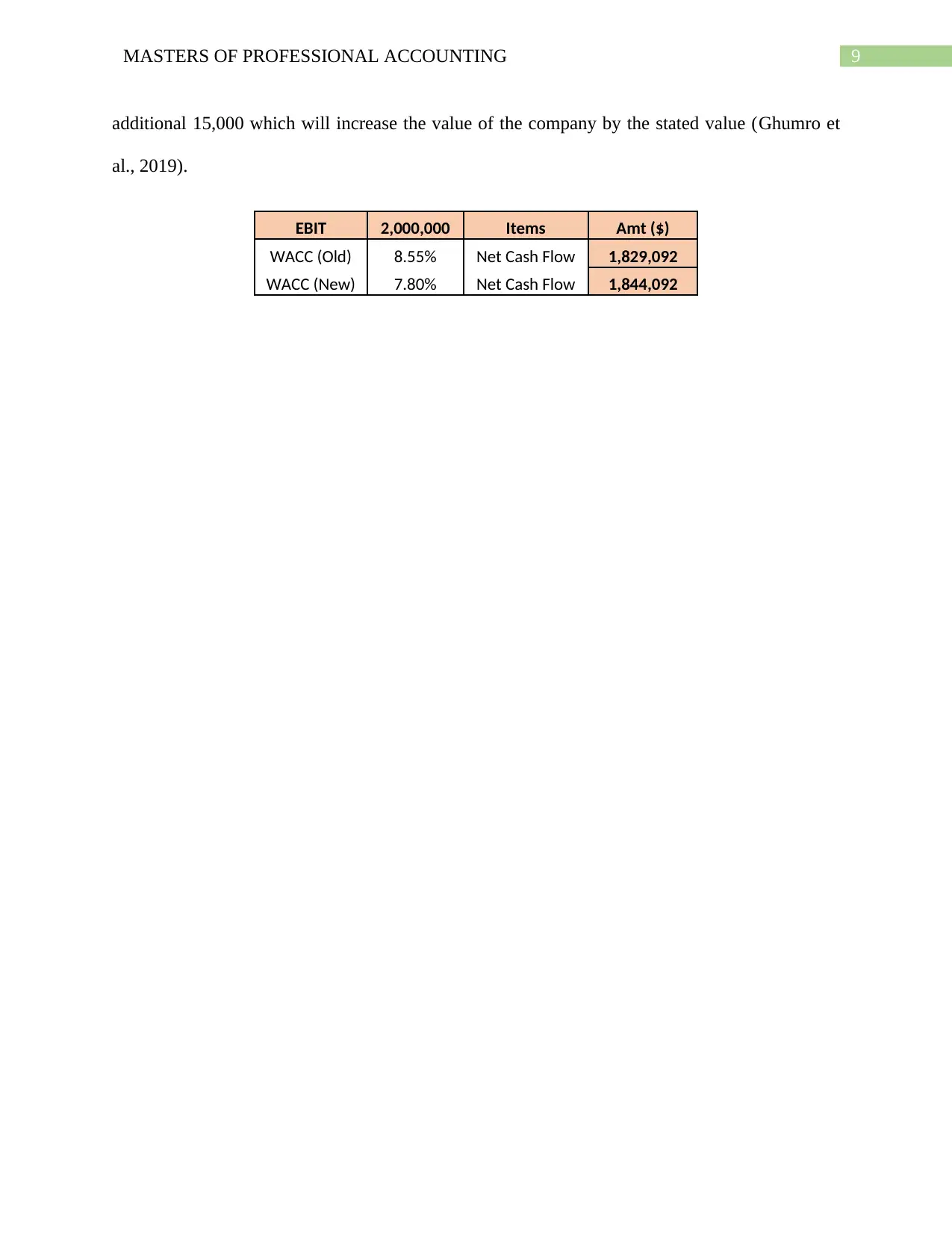

additional 15,000 which will increase the value of the company by the stated value (Ghumro et

al., 2019).

EBIT 2,000,000 Items Amt ($)

WACC (Old) 8.55% Net Cash Flow 1,829,092

WACC (New) 7.80% Net Cash Flow 1,844,092

additional 15,000 which will increase the value of the company by the stated value (Ghumro et

al., 2019).

EBIT 2,000,000 Items Amt ($)

WACC (Old) 8.55% Net Cash Flow 1,829,092

WACC (New) 7.80% Net Cash Flow 1,844,092

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MASTERS OF PROFESSIONAL ACCOUNTING

References

Alkhamis, N., Noreen, U., Ghonaim, L., Alghonaim, S., Ibrahim, S., & Alturki, R. A. A. (2017).

Capital Budgeting and Capital Structure Decisions in Saudi Arabia. Advanced Science

Letters, 23(1), 330-332.

Al-Mutairi, A., Naser, K., & Saeid, M. (2018). Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1),

1468232.

Chadha, S., & Sharma, S. K. (2019). Capital budgeting practices: a survey in the selected Indian

manufacturing firms. International Journal of Indian Culture and Business Management,

18(4), 381-390.

El Ghoul, S., Guedhami, O., Kim, H., & Park, K. (2018). Corporate environmental responsibility

and the cost of capital: International evidence. Journal of Business Ethics, 149(2), 335-

361.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), 300-315.

Ghumro, I. A., Lashari, A. A., Bhatti, I., & Abro, M. U. R. (2019). Investment Decisions: How it

influence Capital Budgeting Practices. Journal of Managerial Sciences, 13(2).

Jha, A., & Arora, S. (2019). Literature Review of Capital Budgeting Practices with Special

Reference to Capital Intensive Industries of India. Prabandhan: Indian Journal of

Management, 12(5), 21-34.

References

Alkhamis, N., Noreen, U., Ghonaim, L., Alghonaim, S., Ibrahim, S., & Alturki, R. A. A. (2017).

Capital Budgeting and Capital Structure Decisions in Saudi Arabia. Advanced Science

Letters, 23(1), 330-332.

Al-Mutairi, A., Naser, K., & Saeid, M. (2018). Capital budgeting practices by non-financial

companies listed on Kuwait Stock Exchange (KSE). Cogent Economics & Finance, 6(1),

1468232.

Chadha, S., & Sharma, S. K. (2019). Capital budgeting practices: a survey in the selected Indian

manufacturing firms. International Journal of Indian Culture and Business Management,

18(4), 381-390.

El Ghoul, S., Guedhami, O., Kim, H., & Park, K. (2018). Corporate environmental responsibility

and the cost of capital: International evidence. Journal of Business Ethics, 149(2), 335-

361.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), 300-315.

Ghumro, I. A., Lashari, A. A., Bhatti, I., & Abro, M. U. R. (2019). Investment Decisions: How it

influence Capital Budgeting Practices. Journal of Managerial Sciences, 13(2).

Jha, A., & Arora, S. (2019). Literature Review of Capital Budgeting Practices with Special

Reference to Capital Intensive Industries of India. Prabandhan: Indian Journal of

Management, 12(5), 21-34.

11MASTERS OF PROFESSIONAL ACCOUNTING

Levin, V., & Hallgren, A. (2017). The choice of capital budgeting techniques: a human capital

approach.

Liu, M., & Wysocki, P. (2017). Cross-sectional determinants of information quality proxies and

cost of capital measures. Quarterly Journal of Finance, 7(02), 1650016.

Robinson, C. J., & Burnett, J. (2016). Financial Management Practices: An Exploratory Study of

Capital Budgeting Techniques in the Caribbean Region. Available at SSRN 2857152.

Shivaani, M. V., Jain, P. K., & Yadav, S. S. (2017). Perceptual Mapping of Capital Budgeting

Techniques: Empirical Evidence from Corporate Enterprises in India. Research Bulletin,

42(4), 106-112.

Su, S. H., Lee, H. L., Chou, J. J., Yeh, J. Y., & Thi, M. H. V. (2018). Application and effects of

capital budgeting among the manufacturing companies in Vietnam. International Journal

of Organizational Innovation (Online), 10(4), 111-120.

Vartiainen, E., Masson, G., Breyer, C., Moser, D., & Román Medina, E. (2019). Impact of

weighted average cost of capital, capital expenditure, and other parameters on future

utility‐scale PV levelised cost of electricity. Progress in Photovoltaics: Research and

Applications.

Zhang, G. (2017). Fundamental (versus Market) Risk and Capital Budgeting Decisions:

Distinguishing between the Investment Hurdle Rate and the Cost of Capital. Available at

SSRN 3019270.

Levin, V., & Hallgren, A. (2017). The choice of capital budgeting techniques: a human capital

approach.

Liu, M., & Wysocki, P. (2017). Cross-sectional determinants of information quality proxies and

cost of capital measures. Quarterly Journal of Finance, 7(02), 1650016.

Robinson, C. J., & Burnett, J. (2016). Financial Management Practices: An Exploratory Study of

Capital Budgeting Techniques in the Caribbean Region. Available at SSRN 2857152.

Shivaani, M. V., Jain, P. K., & Yadav, S. S. (2017). Perceptual Mapping of Capital Budgeting

Techniques: Empirical Evidence from Corporate Enterprises in India. Research Bulletin,

42(4), 106-112.

Su, S. H., Lee, H. L., Chou, J. J., Yeh, J. Y., & Thi, M. H. V. (2018). Application and effects of

capital budgeting among the manufacturing companies in Vietnam. International Journal

of Organizational Innovation (Online), 10(4), 111-120.

Vartiainen, E., Masson, G., Breyer, C., Moser, D., & Román Medina, E. (2019). Impact of

weighted average cost of capital, capital expenditure, and other parameters on future

utility‐scale PV levelised cost of electricity. Progress in Photovoltaics: Research and

Applications.

Zhang, G. (2017). Fundamental (versus Market) Risk and Capital Budgeting Decisions:

Distinguishing between the Investment Hurdle Rate and the Cost of Capital. Available at

SSRN 3019270.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.