Business Finance Report: Investment Appraisal and Standard Costing

VerifiedAdded on 2023/06/15

|16

|4289

|199

Report

AI Summary

This report provides a detailed analysis of capital budgeting and standard costing for K PLC. It evaluates various investment projects using payback period and net present value methods, ranking them to determine the most profitable options. The report discusses the strengths and weaknesses of these methods and considers qualitative factors influencing capital budgeting decisions. Furthermore, it explores external funding sources for K PLC and examines the link between investing and financing activities. The report also includes a standard costing system analysis, explaining identified variances. Finally, it differentiates between centralized and decentralized purchase management, offering a comprehensive overview of financial strategies and procurement processes within the company. Desklib provides access to similar solved assignments and past papers for students.

Business Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction......................................................................................................................................2

Task A…………………………………………………………………………………………....2

In this, company will determine its payback period for each of its project.................................2

To calculate Net present value of the projects.............................................................................3

Ranking the projects on basis of payback period and net present value....................................5

To choose the projects if they are mutually exclusive.................................................................6

Strengths and Weaknesses of Payback period and Net Present Value.........................................6

Qualitative Factors of Capital Budgeting....................................................................................8

Task B..............................................................................................................................................9

There are various external sources available to K PLC for the purpose of raising the funds.....9

Link between investing and financing activity :........................................................................10

TASK C..........................................................................................................................................10

Standard costing system............................................................................................................10

Explanations of the variances identified :..................................................................................12

TASK D.........................................................................................................................................13

Difference between centralised and decentralised purchase management :..............................13

Conclusion.....................................................................................................................................14

REFERENCES..............................................................................................................................15

Task A…………………………………………………………………………………………....2

In this, company will determine its payback period for each of its project.................................2

To calculate Net present value of the projects.............................................................................3

Ranking the projects on basis of payback period and net present value....................................5

To choose the projects if they are mutually exclusive.................................................................6

Strengths and Weaknesses of Payback period and Net Present Value.........................................6

Qualitative Factors of Capital Budgeting....................................................................................8

Task B..............................................................................................................................................9

There are various external sources available to K PLC for the purpose of raising the funds.....9

Link between investing and financing activity :........................................................................10

TASK C..........................................................................................................................................10

Standard costing system............................................................................................................10

Explanations of the variances identified :..................................................................................12

TASK D.........................................................................................................................................13

Difference between centralised and decentralised purchase management :..............................13

Conclusion.....................................................................................................................................14

REFERENCES..............................................................................................................................15

Introduction

This report include the basic description of the company to complete the working and

manage the sources in the range of financial strategies that are associated to make budget,

effective financial management and accounting process. Furthermore the use of approaches for

procurement and contracting information are analyse within the use of organisation within the

company. In last the commercial context for the organisational operating activities are analyse

and discuss within the report.

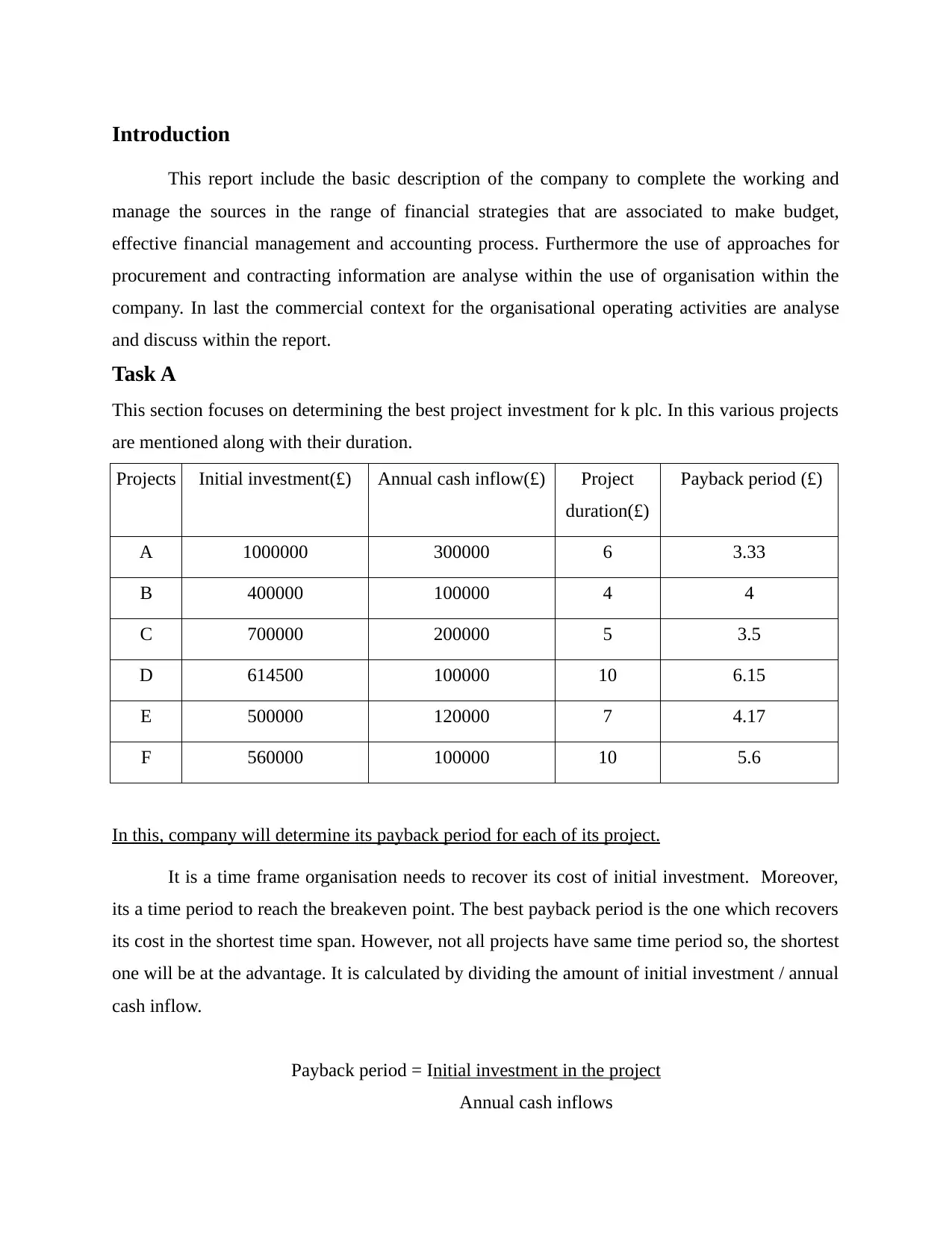

Task A

This section focuses on determining the best project investment for k plc. In this various projects

are mentioned along with their duration.

Projects Initial investment(£) Annual cash inflow(£) Project

duration(£)

Payback period (£)

A 1000000 300000 6 3.33

B 400000 100000 4 4

C 700000 200000 5 3.5

D 614500 100000 10 6.15

E 500000 120000 7 4.17

F 560000 100000 10 5.6

In this, company will determine its payback period for each of its project.

It is a time frame organisation needs to recover its cost of initial investment. Moreover,

its a time period to reach the breakeven point. The best payback period is the one which recovers

its cost in the shortest time span. However, not all projects have same time period so, the shortest

one will be at the advantage. It is calculated by dividing the amount of initial investment / annual

cash inflow.

Payback period = Initial investment in the project

Annual cash inflows

This report include the basic description of the company to complete the working and

manage the sources in the range of financial strategies that are associated to make budget,

effective financial management and accounting process. Furthermore the use of approaches for

procurement and contracting information are analyse within the use of organisation within the

company. In last the commercial context for the organisational operating activities are analyse

and discuss within the report.

Task A

This section focuses on determining the best project investment for k plc. In this various projects

are mentioned along with their duration.

Projects Initial investment(£) Annual cash inflow(£) Project

duration(£)

Payback period (£)

A 1000000 300000 6 3.33

B 400000 100000 4 4

C 700000 200000 5 3.5

D 614500 100000 10 6.15

E 500000 120000 7 4.17

F 560000 100000 10 5.6

In this, company will determine its payback period for each of its project.

It is a time frame organisation needs to recover its cost of initial investment. Moreover,

its a time period to reach the breakeven point. The best payback period is the one which recovers

its cost in the shortest time span. However, not all projects have same time period so, the shortest

one will be at the advantage. It is calculated by dividing the amount of initial investment / annual

cash inflow.

Payback period = Initial investment in the project

Annual cash inflows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation for project G, in this cash flow on annual basis is not equal. So, by applying

formula it will the back period will be calculated.

Year Uncovered amount at start

of the year (£)

Investment done

(£)

Cash inflows

(£)

Uncovered

investment at year

end (£)

0 - -200000 - -200000

1 -200000 - 100000 -100000

2 -100000 - 100000 0

3 - - 20000

4 - - 20000

5 - - 20000

6 - - 20000

By applying, the formula,

Payback period for uneven cash inflows = Years before full recovery + uncovered amount

at the start of the year / cash flow during the year

Time taken to recover the amount of the project is 2 years.

To calculate Net present value of the projects

Company finds the difference between cash inflows and cash outflows. It is used for

capital budgeting purposes to measure which project will give higher returns.

Projects Initial

investment (£)

Cash inflow

(£)

Project

duration

Present annuity

value (£)

Net present value

(£)

A 1000000 300000 6 4.355 306500

B 400000 100000 4 3.170 -83000

formula it will the back period will be calculated.

Year Uncovered amount at start

of the year (£)

Investment done

(£)

Cash inflows

(£)

Uncovered

investment at year

end (£)

0 - -200000 - -200000

1 -200000 - 100000 -100000

2 -100000 - 100000 0

3 - - 20000

4 - - 20000

5 - - 20000

6 - - 20000

By applying, the formula,

Payback period for uneven cash inflows = Years before full recovery + uncovered amount

at the start of the year / cash flow during the year

Time taken to recover the amount of the project is 2 years.

To calculate Net present value of the projects

Company finds the difference between cash inflows and cash outflows. It is used for

capital budgeting purposes to measure which project will give higher returns.

Projects Initial

investment (£)

Cash inflow

(£)

Project

duration

Present annuity

value (£)

Net present value

(£)

A 1000000 300000 6 4.355 306500

B 400000 100000 4 3.170 -83000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

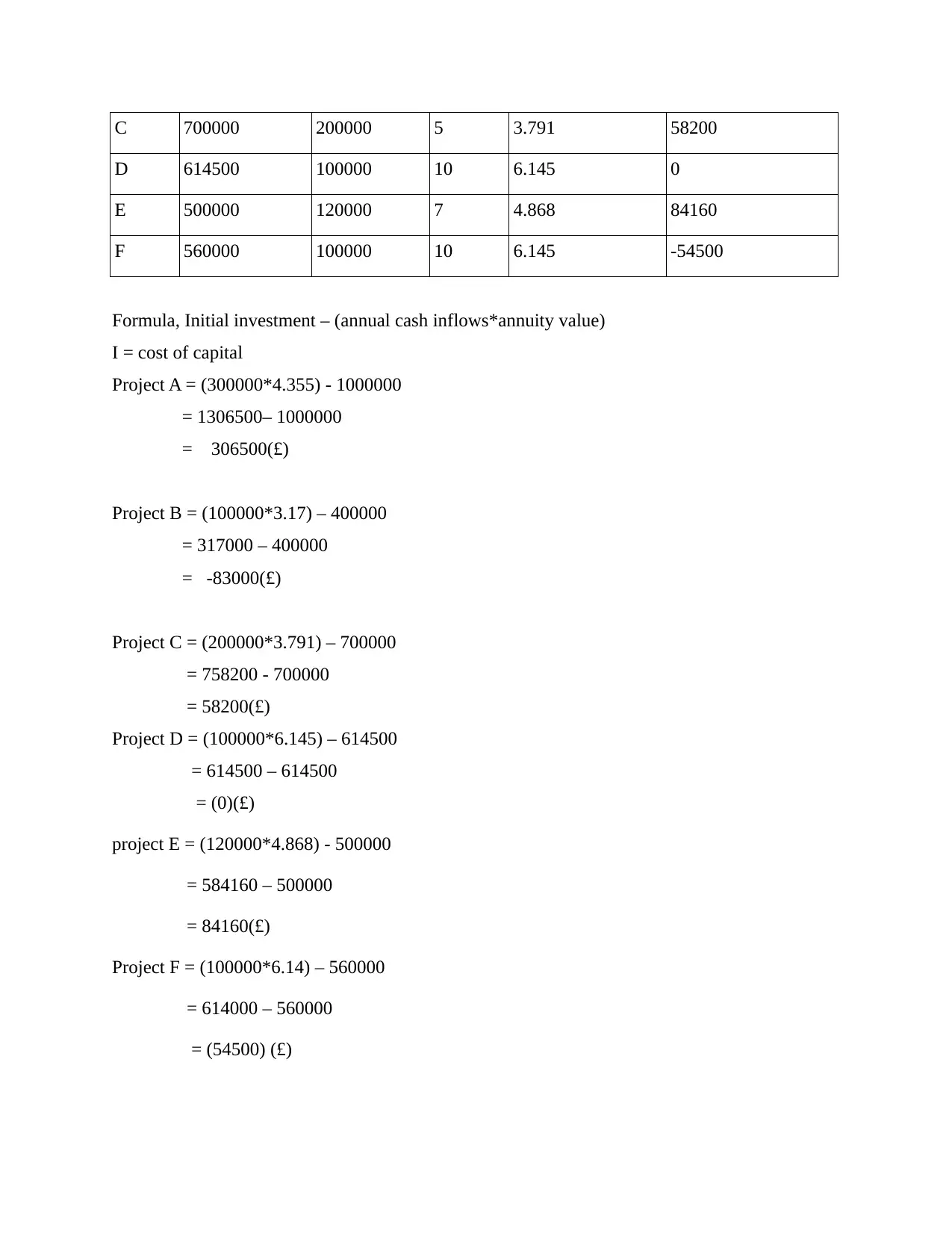

C 700000 200000 5 3.791 58200

D 614500 100000 10 6.145 0

E 500000 120000 7 4.868 84160

F 560000 100000 10 6.145 -54500

Formula, Initial investment – (annual cash inflows*annuity value)

I = cost of capital

Project A = (300000*4.355) - 1000000

= 1306500– 1000000

= 306500(£)

Project B = (100000*3.17) – 400000

= 317000 – 400000

= -83000(£)

Project C = (200000*3.791) – 700000

= 758200 - 700000

= 58200(£)

Project D = (100000*6.145) – 614500

= 614500 – 614500

= (0)(£)

project E = (120000*4.868) - 500000

= 584160 – 500000

= 84160(£)

Project F = (100000*6.14) – 560000

= 614000 – 560000

= (54500) (£)

D 614500 100000 10 6.145 0

E 500000 120000 7 4.868 84160

F 560000 100000 10 6.145 -54500

Formula, Initial investment – (annual cash inflows*annuity value)

I = cost of capital

Project A = (300000*4.355) - 1000000

= 1306500– 1000000

= 306500(£)

Project B = (100000*3.17) – 400000

= 317000 – 400000

= -83000(£)

Project C = (200000*3.791) – 700000

= 758200 - 700000

= 58200(£)

Project D = (100000*6.145) – 614500

= 614500 – 614500

= (0)(£)

project E = (120000*4.868) - 500000

= 584160 – 500000

= 84160(£)

Project F = (100000*6.14) – 560000

= 614000 – 560000

= (54500) (£)

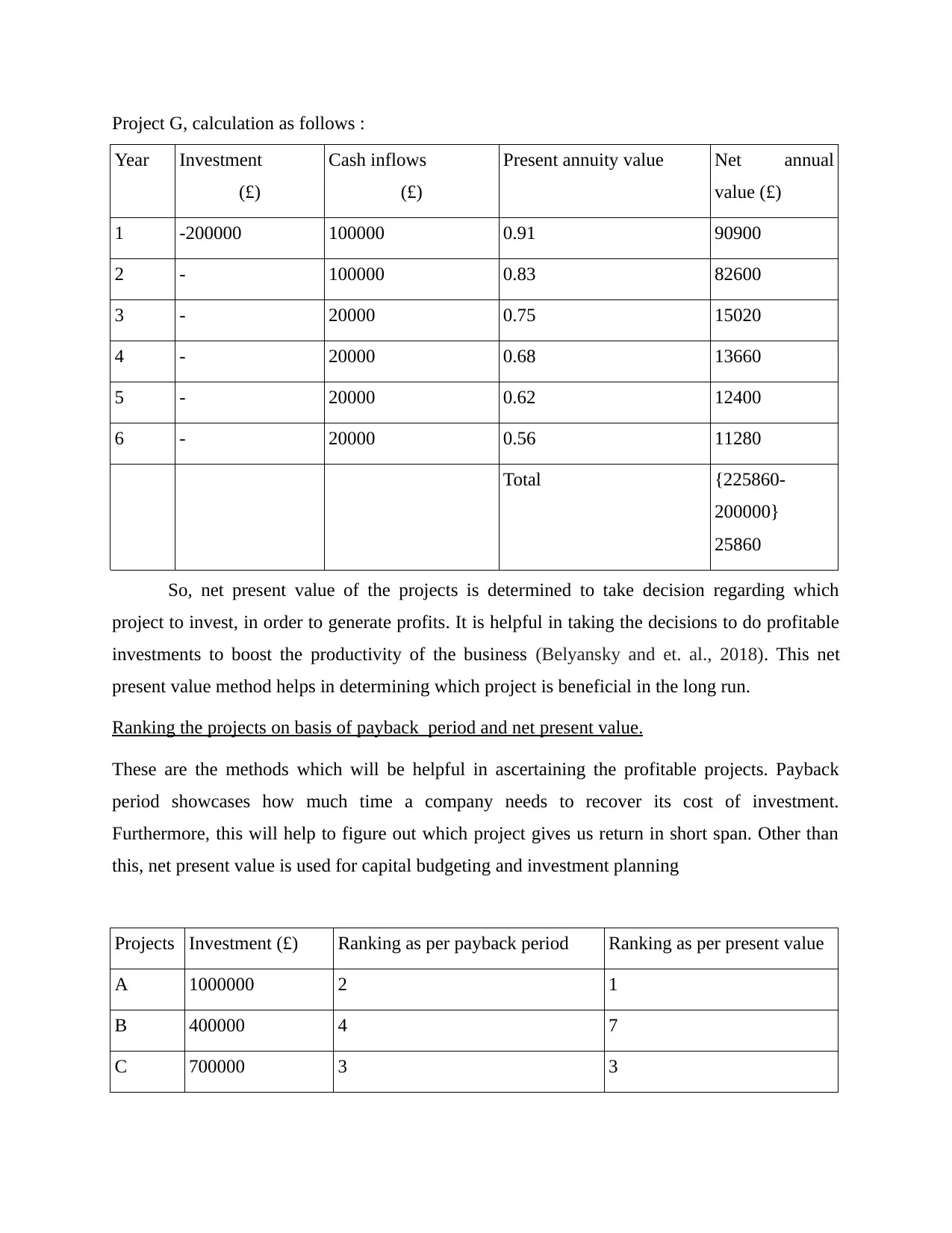

Project G, calculation as follows :

Year Investment

(£)

Cash inflows

(£)

Present annuity value Net annual

value (£)

1 -200000 100000 0.91 90900

2 - 100000 0.83 82600

3 - 20000 0.75 15020

4 - 20000 0.68 13660

5 - 20000 0.62 12400

6 - 20000 0.56 11280

Total {225860-

200000}

25860

So, net present value of the projects is determined to take decision regarding which

project to invest, in order to generate profits. It is helpful in taking the decisions to do profitable

investments to boost the productivity of the business (Belyansky and et. al., 2018). This net

present value method helps in determining which project is beneficial in the long run.

Ranking the projects on basis of payback period and net present value.

These are the methods which will be helpful in ascertaining the profitable projects. Payback

period showcases how much time a company needs to recover its cost of investment.

Furthermore, this will help to figure out which project gives us return in short span. Other than

this, net present value is used for capital budgeting and investment planning

Projects Investment (£) Ranking as per payback period Ranking as per present value

A 1000000 2 1

B 400000 4 7

C 700000 3 3

Year Investment

(£)

Cash inflows

(£)

Present annuity value Net annual

value (£)

1 -200000 100000 0.91 90900

2 - 100000 0.83 82600

3 - 20000 0.75 15020

4 - 20000 0.68 13660

5 - 20000 0.62 12400

6 - 20000 0.56 11280

Total {225860-

200000}

25860

So, net present value of the projects is determined to take decision regarding which

project to invest, in order to generate profits. It is helpful in taking the decisions to do profitable

investments to boost the productivity of the business (Belyansky and et. al., 2018). This net

present value method helps in determining which project is beneficial in the long run.

Ranking the projects on basis of payback period and net present value.

These are the methods which will be helpful in ascertaining the profitable projects. Payback

period showcases how much time a company needs to recover its cost of investment.

Furthermore, this will help to figure out which project gives us return in short span. Other than

this, net present value is used for capital budgeting and investment planning

Projects Investment (£) Ranking as per payback period Ranking as per present value

A 1000000 2 1

B 400000 4 7

C 700000 3 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

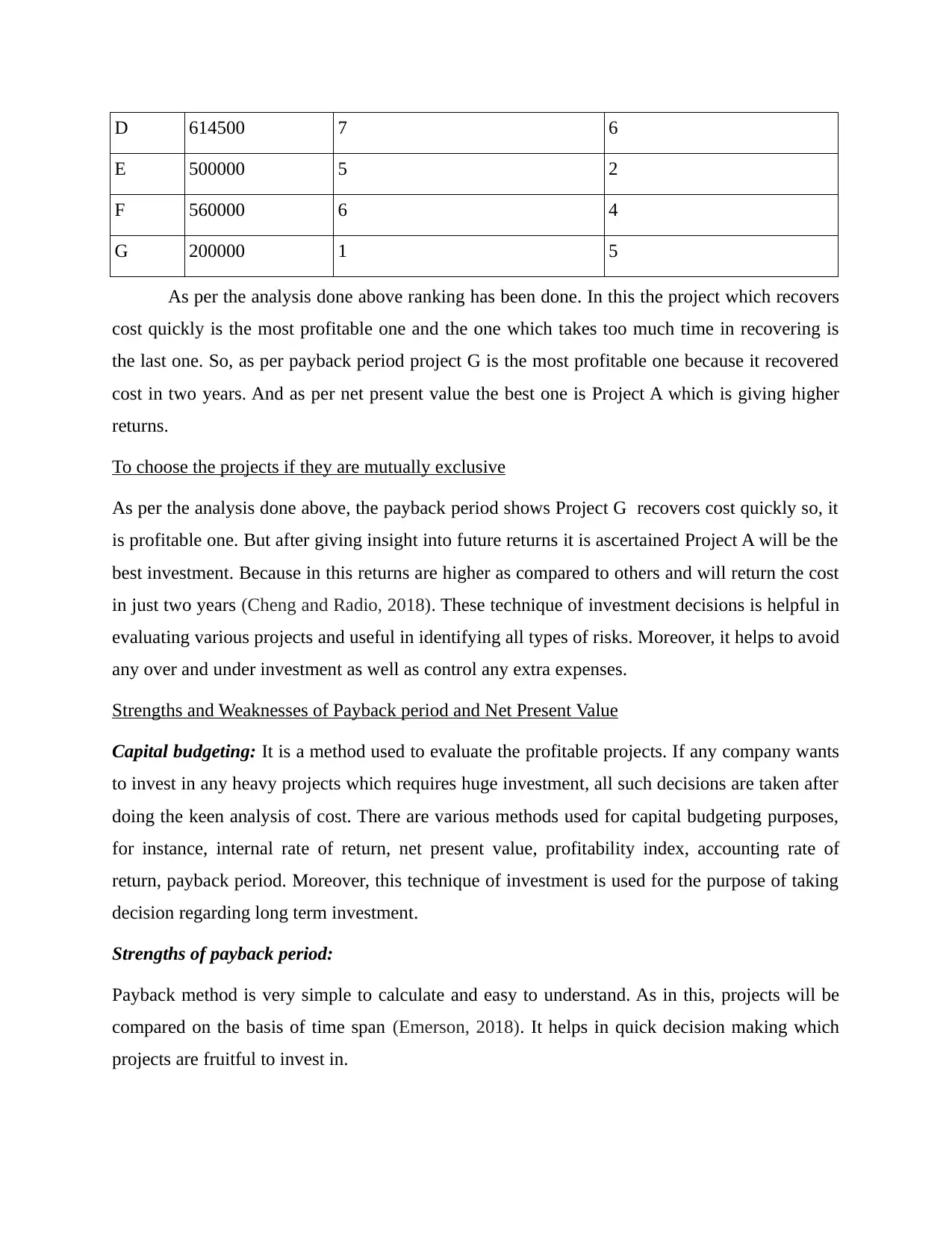

D 614500 7 6

E 500000 5 2

F 560000 6 4

G 200000 1 5

As per the analysis done above ranking has been done. In this the project which recovers

cost quickly is the most profitable one and the one which takes too much time in recovering is

the last one. So, as per payback period project G is the most profitable one because it recovered

cost in two years. And as per net present value the best one is Project A which is giving higher

returns.

To choose the projects if they are mutually exclusive

As per the analysis done above, the payback period shows Project G recovers cost quickly so, it

is profitable one. But after giving insight into future returns it is ascertained Project A will be the

best investment. Because in this returns are higher as compared to others and will return the cost

in just two years (Cheng and Radio, 2018). These technique of investment decisions is helpful in

evaluating various projects and useful in identifying all types of risks. Moreover, it helps to avoid

any over and under investment as well as control any extra expenses.

Strengths and Weaknesses of Payback period and Net Present Value

Capital budgeting: It is a method used to evaluate the profitable projects. If any company wants

to invest in any heavy projects which requires huge investment, all such decisions are taken after

doing the keen analysis of cost. There are various methods used for capital budgeting purposes,

for instance, internal rate of return, net present value, profitability index, accounting rate of

return, payback period. Moreover, this technique of investment is used for the purpose of taking

decision regarding long term investment.

Strengths of payback period:

Payback method is very simple to calculate and easy to understand. As in this, projects will be

compared on the basis of time span (Emerson, 2018). It helps in quick decision making which

projects are fruitful to invest in.

E 500000 5 2

F 560000 6 4

G 200000 1 5

As per the analysis done above ranking has been done. In this the project which recovers

cost quickly is the most profitable one and the one which takes too much time in recovering is

the last one. So, as per payback period project G is the most profitable one because it recovered

cost in two years. And as per net present value the best one is Project A which is giving higher

returns.

To choose the projects if they are mutually exclusive

As per the analysis done above, the payback period shows Project G recovers cost quickly so, it

is profitable one. But after giving insight into future returns it is ascertained Project A will be the

best investment. Because in this returns are higher as compared to others and will return the cost

in just two years (Cheng and Radio, 2018). These technique of investment decisions is helpful in

evaluating various projects and useful in identifying all types of risks. Moreover, it helps to avoid

any over and under investment as well as control any extra expenses.

Strengths and Weaknesses of Payback period and Net Present Value

Capital budgeting: It is a method used to evaluate the profitable projects. If any company wants

to invest in any heavy projects which requires huge investment, all such decisions are taken after

doing the keen analysis of cost. There are various methods used for capital budgeting purposes,

for instance, internal rate of return, net present value, profitability index, accounting rate of

return, payback period. Moreover, this technique of investment is used for the purpose of taking

decision regarding long term investment.

Strengths of payback period:

Payback method is very simple to calculate and easy to understand. As in this, projects will be

compared on the basis of time span (Emerson, 2018). It helps in quick decision making which

projects are fruitful to invest in.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

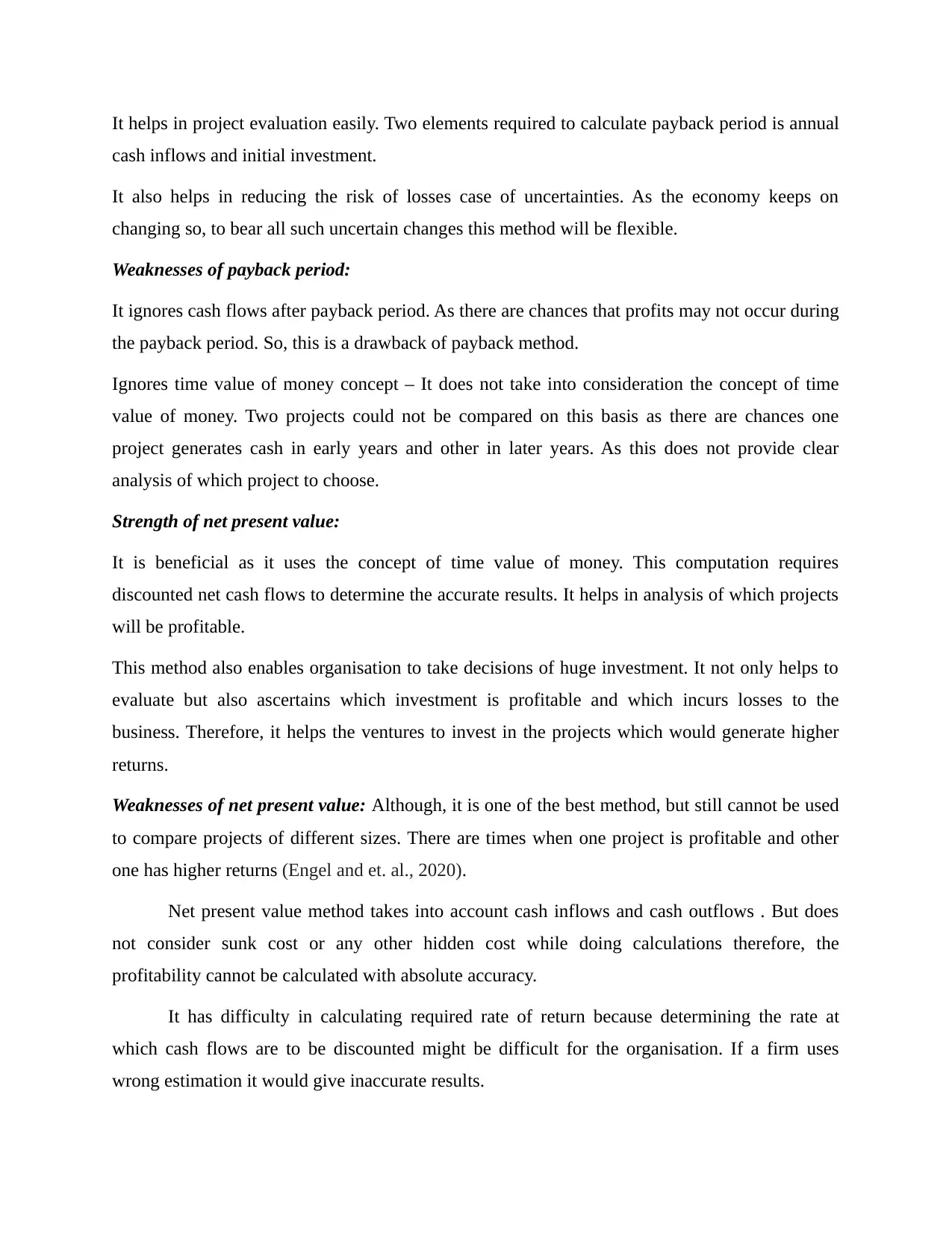

It helps in project evaluation easily. Two elements required to calculate payback period is annual

cash inflows and initial investment.

It also helps in reducing the risk of losses case of uncertainties. As the economy keeps on

changing so, to bear all such uncertain changes this method will be flexible.

Weaknesses of payback period:

It ignores cash flows after payback period. As there are chances that profits may not occur during

the payback period. So, this is a drawback of payback method.

Ignores time value of money concept – It does not take into consideration the concept of time

value of money. Two projects could not be compared on this basis as there are chances one

project generates cash in early years and other in later years. As this does not provide clear

analysis of which project to choose.

Strength of net present value:

It is beneficial as it uses the concept of time value of money. This computation requires

discounted net cash flows to determine the accurate results. It helps in analysis of which projects

will be profitable.

This method also enables organisation to take decisions of huge investment. It not only helps to

evaluate but also ascertains which investment is profitable and which incurs losses to the

business. Therefore, it helps the ventures to invest in the projects which would generate higher

returns.

Weaknesses of net present value: Although, it is one of the best method, but still cannot be used

to compare projects of different sizes. There are times when one project is profitable and other

one has higher returns (Engel and et. al., 2020).

Net present value method takes into account cash inflows and cash outflows . But does

not consider sunk cost or any other hidden cost while doing calculations therefore, the

profitability cannot be calculated with absolute accuracy.

It has difficulty in calculating required rate of return because determining the rate at

which cash flows are to be discounted might be difficult for the organisation. If a firm uses

wrong estimation it would give inaccurate results.

cash inflows and initial investment.

It also helps in reducing the risk of losses case of uncertainties. As the economy keeps on

changing so, to bear all such uncertain changes this method will be flexible.

Weaknesses of payback period:

It ignores cash flows after payback period. As there are chances that profits may not occur during

the payback period. So, this is a drawback of payback method.

Ignores time value of money concept – It does not take into consideration the concept of time

value of money. Two projects could not be compared on this basis as there are chances one

project generates cash in early years and other in later years. As this does not provide clear

analysis of which project to choose.

Strength of net present value:

It is beneficial as it uses the concept of time value of money. This computation requires

discounted net cash flows to determine the accurate results. It helps in analysis of which projects

will be profitable.

This method also enables organisation to take decisions of huge investment. It not only helps to

evaluate but also ascertains which investment is profitable and which incurs losses to the

business. Therefore, it helps the ventures to invest in the projects which would generate higher

returns.

Weaknesses of net present value: Although, it is one of the best method, but still cannot be used

to compare projects of different sizes. There are times when one project is profitable and other

one has higher returns (Engel and et. al., 2020).

Net present value method takes into account cash inflows and cash outflows . But does

not consider sunk cost or any other hidden cost while doing calculations therefore, the

profitability cannot be calculated with absolute accuracy.

It has difficulty in calculating required rate of return because determining the rate at

which cash flows are to be discounted might be difficult for the organisation. If a firm uses

wrong estimation it would give inaccurate results.

So, these two methods are used to ascertain in which project to invest. Both has its

advantages and disadvantages. Therefore, an organisation has to conduct deep analysis while

taking the decisions of investment.

Qualitative Factors of Capital Budgeting

Various qualitative factors to be considered before making any decision of capital budgeting. It is

the most important factor to be considered while making decisions as they are responsible for

shaping any business. Moreover, it helps in resolving many critical issues due to economic,

political or any other changes. It affects the operations and profitability of the concern.

Therefore, these decisions are to be considered before making any huge investment.

• Existing competition in markets: This factor is most important to be considered as it

affect the cash flow due to uncertainties in the prevailing market. There are lot of

uncertain actions which competitors took for instance, reduction in cost or coming with

the updated technology and so on (Helms, Salm and Wüstenhagen, 2020). Therefore,

these uncertain changes can cause serious issues and affect the cash flows of the

company.

• Human errors: This focuses on the errors committed by management in estimating

discount rates which are needed to be considered in capital budgeting decisions. It has

high importance in the success and failure of the concern. Moreover, time scheduling

issues, prices of the resources and other materials are major considerations which led to

success or failure of the business concern.

• Social trends: changes of the societal trends are an important qualitative factor to be

considered while making investment decisions. These trends keeps on changing with time

so, company's have to keep themselves updated as per the current market conditions in

order to make profits. In these organisations has to monitor what are the likes and dislikes

of the target audience, what are their goals and missions and how they keep on changing

with time. So, businesses have to do investments after a deep insight into customers

needs and wants.

• Environmental factors: as with growing concerns of society, businesses have started

taking societal responsibilities. Companies who have recognition and awards for

advantages and disadvantages. Therefore, an organisation has to conduct deep analysis while

taking the decisions of investment.

Qualitative Factors of Capital Budgeting

Various qualitative factors to be considered before making any decision of capital budgeting. It is

the most important factor to be considered while making decisions as they are responsible for

shaping any business. Moreover, it helps in resolving many critical issues due to economic,

political or any other changes. It affects the operations and profitability of the concern.

Therefore, these decisions are to be considered before making any huge investment.

• Existing competition in markets: This factor is most important to be considered as it

affect the cash flow due to uncertainties in the prevailing market. There are lot of

uncertain actions which competitors took for instance, reduction in cost or coming with

the updated technology and so on (Helms, Salm and Wüstenhagen, 2020). Therefore,

these uncertain changes can cause serious issues and affect the cash flows of the

company.

• Human errors: This focuses on the errors committed by management in estimating

discount rates which are needed to be considered in capital budgeting decisions. It has

high importance in the success and failure of the concern. Moreover, time scheduling

issues, prices of the resources and other materials are major considerations which led to

success or failure of the business concern.

• Social trends: changes of the societal trends are an important qualitative factor to be

considered while making investment decisions. These trends keeps on changing with time

so, company's have to keep themselves updated as per the current market conditions in

order to make profits. In these organisations has to monitor what are the likes and dislikes

of the target audience, what are their goals and missions and how they keep on changing

with time. So, businesses have to do investments after a deep insight into customers

needs and wants.

• Environmental factors: as with growing concerns of society, businesses have started

taking societal responsibilities. Companies who have recognition and awards for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

environmental stewardship stand apart from its competitors. It positively influences

stakeholders and customers as well as helps in acquiring new customers and creates

loyalty from existing customers.

So, these qualitative factors are considered while making capital budgeting decisions as these

investments are expected to generate long term benefits. This improves the efficiency,

productivity, revenues of the business concern. Not only the financial factors are rather all these

other factors considered before making any expenditure in order to capture large market share.

Task B

There are various external sources available to K PLC for the purpose of raising the funds.

• Bank loans: this is an external source which a business can use to raise funds. For

obtaining the funds having a good credit history is important for the concern. It

showcases the financial position of the company and provides assurance to the bank

regarding the payment of debts. So, banks ask for the financial statements before issuing

the loan to see the ability of the company to pay of its debts. These statements reflect the

profits and losses of the business concern and the current financial condition of the

company. Furthermore, this allows lenders to see whether your company would able to

make payment of the debts on time.

• Government loans and grants: this is another external source to raise the funds in order

to expand the business. In this government provide capital to the business in the form of

grant for the purpose of expansion. These grants are provided to promote the economic

growth of the industries. Alternatively, businesses can raise funds through micro loans

from government agencies. These will help the businesses to keep going and non profit

organisations provide help to the owners in boosting the growth of local economic

system. For the purpose of raising loans through grants businesses have to provide details

regarding the project description, a detailed plan with full costs, completed application

forms and all the relevant procedures are need to be fulfilled.

• Venture capital: Venture capitalist looks for the businesses with high growth potential to

invest in. This includes sectors such as information technology, communication,

stakeholders and customers as well as helps in acquiring new customers and creates

loyalty from existing customers.

So, these qualitative factors are considered while making capital budgeting decisions as these

investments are expected to generate long term benefits. This improves the efficiency,

productivity, revenues of the business concern. Not only the financial factors are rather all these

other factors considered before making any expenditure in order to capture large market share.

Task B

There are various external sources available to K PLC for the purpose of raising the funds.

• Bank loans: this is an external source which a business can use to raise funds. For

obtaining the funds having a good credit history is important for the concern. It

showcases the financial position of the company and provides assurance to the bank

regarding the payment of debts. So, banks ask for the financial statements before issuing

the loan to see the ability of the company to pay of its debts. These statements reflect the

profits and losses of the business concern and the current financial condition of the

company. Furthermore, this allows lenders to see whether your company would able to

make payment of the debts on time.

• Government loans and grants: this is another external source to raise the funds in order

to expand the business. In this government provide capital to the business in the form of

grant for the purpose of expansion. These grants are provided to promote the economic

growth of the industries. Alternatively, businesses can raise funds through micro loans

from government agencies. These will help the businesses to keep going and non profit

organisations provide help to the owners in boosting the growth of local economic

system. For the purpose of raising loans through grants businesses have to provide details

regarding the project description, a detailed plan with full costs, completed application

forms and all the relevant procedures are need to be fulfilled.

• Venture capital: Venture capitalist looks for the businesses with high growth potential to

invest in. This includes sectors such as information technology, communication,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

biotechnology and so on. These take ownership position in the company and expect

higher return on their investments. So, this source not only brings funds for the expansion

but also, relevant experience and knowledge of the investors.

Therefore, these are the external source which businesses can opt for the purpose of its

expansion. Although it is expensive source because businesses have to pay high rate of interest

on the raised funds.

Link between investing and financing activity :

Financing and investing are two different activities of financial management to raise the

funds in the organisation. Financing is an act of raising funds through internal and external

sources. Internal sources are equity, retained earnings and so on which cost less to the businesses.

Alternatively, external sources are debenture, loans from banks and government etc. cost high to

the owners. It increases the risk of the organisation. On the other hand, investing is an act of

obtaining money by investing in the profitable projects. These are important for the long term

success of the organisation. To conduct financial planning these activities are considered. Or for

framing future corporate strategies various decisions are considered regarding from which source

to raise funds and whether that would be profitable for the business concern or not. So, these

decisions are taken with regard to finances of the company. These decisions are regarding the

acquisition of the assets, raising funds from different sources, investing in the profitable projects

and so on. This affect the assets and liabilities of the business concern. So, financing will help k

plc to raise the funds from various sources and later, invest the raised funds in profitable projects.

TASK C

Standard costing system

It is the process of estimating the expenses of production process. It is used by the

manufacturer to plan their future expenses in advance for instance, direct material, direct labour,

overheads and so on. It helps the management to control the expenses of day to day operations.

Moreover, it is system of cost control in which standard cost is compared with actual cost and

variances are identified by comparing the two. It can be used by any industry to make budgetary

control effective.

higher return on their investments. So, this source not only brings funds for the expansion

but also, relevant experience and knowledge of the investors.

Therefore, these are the external source which businesses can opt for the purpose of its

expansion. Although it is expensive source because businesses have to pay high rate of interest

on the raised funds.

Link between investing and financing activity :

Financing and investing are two different activities of financial management to raise the

funds in the organisation. Financing is an act of raising funds through internal and external

sources. Internal sources are equity, retained earnings and so on which cost less to the businesses.

Alternatively, external sources are debenture, loans from banks and government etc. cost high to

the owners. It increases the risk of the organisation. On the other hand, investing is an act of

obtaining money by investing in the profitable projects. These are important for the long term

success of the organisation. To conduct financial planning these activities are considered. Or for

framing future corporate strategies various decisions are considered regarding from which source

to raise funds and whether that would be profitable for the business concern or not. So, these

decisions are taken with regard to finances of the company. These decisions are regarding the

acquisition of the assets, raising funds from different sources, investing in the profitable projects

and so on. This affect the assets and liabilities of the business concern. So, financing will help k

plc to raise the funds from various sources and later, invest the raised funds in profitable projects.

TASK C

Standard costing system

It is the process of estimating the expenses of production process. It is used by the

manufacturer to plan their future expenses in advance for instance, direct material, direct labour,

overheads and so on. It helps the management to control the expenses of day to day operations.

Moreover, it is system of cost control in which standard cost is compared with actual cost and

variances are identified by comparing the two. It can be used by any industry to make budgetary

control effective.

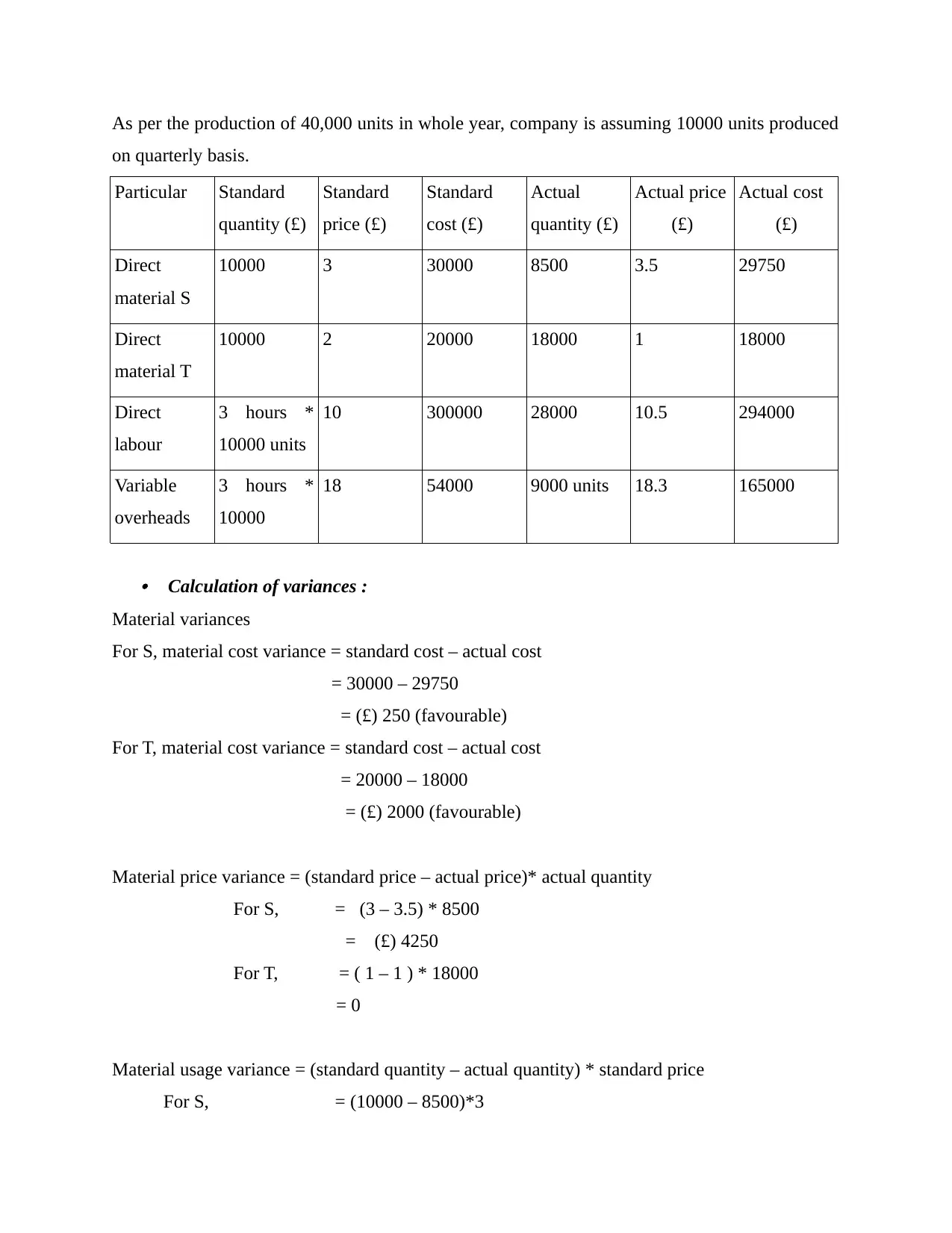

As per the production of 40,000 units in whole year, company is assuming 10000 units produced

on quarterly basis.

Particular Standard

quantity (£)

Standard

price (£)

Standard

cost (£)

Actual

quantity (£)

Actual price

(£)

Actual cost

(£)

Direct

material S

10000 3 30000 8500 3.5 29750

Direct

material T

10000 2 20000 18000 1 18000

Direct

labour

3 hours *

10000 units

10 300000 28000 10.5 294000

Variable

overheads

3 hours *

10000

18 54000 9000 units 18.3 165000

• Calculation of variances :

Material variances

For S, material cost variance = standard cost – actual cost

= 30000 – 29750

= (£) 250 (favourable)

For T, material cost variance = standard cost – actual cost

= 20000 – 18000

= (£) 2000 (favourable)

Material price variance = (standard price – actual price)* actual quantity

For S, = (3 – 3.5) * 8500

= (£) 4250

For T, = ( 1 – 1 ) * 18000

= 0

Material usage variance = (standard quantity – actual quantity) * standard price

For S, = (10000 – 8500)*3

on quarterly basis.

Particular Standard

quantity (£)

Standard

price (£)

Standard

cost (£)

Actual

quantity (£)

Actual price

(£)

Actual cost

(£)

Direct

material S

10000 3 30000 8500 3.5 29750

Direct

material T

10000 2 20000 18000 1 18000

Direct

labour

3 hours *

10000 units

10 300000 28000 10.5 294000

Variable

overheads

3 hours *

10000

18 54000 9000 units 18.3 165000

• Calculation of variances :

Material variances

For S, material cost variance = standard cost – actual cost

= 30000 – 29750

= (£) 250 (favourable)

For T, material cost variance = standard cost – actual cost

= 20000 – 18000

= (£) 2000 (favourable)

Material price variance = (standard price – actual price)* actual quantity

For S, = (3 – 3.5) * 8500

= (£) 4250

For T, = ( 1 – 1 ) * 18000

= 0

Material usage variance = (standard quantity – actual quantity) * standard price

For S, = (10000 – 8500)*3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.