Financial Analysis: Capital Budgeting for Printer Replacement at CQU

VerifiedAdded on 2020/05/16

|23

|3336

|151

Report

AI Summary

This report provides a comprehensive analysis of capital budgeting techniques applied to the decision of replacing printers at CQU Printing. The report evaluates two printer options (Printer A and Printer B) using Net Present Value (NPV), Payback Period, and Internal Rate of Return (IRR) methods. It includes detailed calculations of initial investments, operating cash flows, and terminal cash flows for each printer. The analysis compares the financial performance of each printer based on the different capital budgeting techniques, and provides a graphical representation of the IRR profiles with NPVs. The report concludes that Printer B is the more favorable investment option, as it demonstrates more positive outcomes across the various financial metrics. The report also addresses decision-making under different scenarios, such as unlimited funds.

Running Head: Appraisal of Capital Investments

Capital Budgeting Decisions

Capital Budgeting Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments 1

Executive summary:

In this report, various capital budgeting techniques have been discussed and applied to reach at a

conclusion regarding the decision of replacement of printers held as asset by CQU printing firm

which is engaged in the business of commercial printing. The firm is considering the

replacement the old printer with the new printer to improve the quality of printing and the

operational efficiency. However, there are two choices of printer available in the market and the

firm has to select the best suitable option on the basis of rankings given using various capital

budgeting techniques such as Net present value, Payback period, Internal rate of return etc. In

this report each of these capital investment proposals have been critically evaluated and it is

observed that the firm must go with the option of Printer B as it has more favorable results than

Printer A.

Executive summary:

In this report, various capital budgeting techniques have been discussed and applied to reach at a

conclusion regarding the decision of replacement of printers held as asset by CQU printing firm

which is engaged in the business of commercial printing. The firm is considering the

replacement the old printer with the new printer to improve the quality of printing and the

operational efficiency. However, there are two choices of printer available in the market and the

firm has to select the best suitable option on the basis of rankings given using various capital

budgeting techniques such as Net present value, Payback period, Internal rate of return etc. In

this report each of these capital investment proposals have been critically evaluated and it is

observed that the firm must go with the option of Printer B as it has more favorable results than

Printer A.

Appraisal of Capital Investments 2

Table of Contents

Executive summary.....................................................................................................................................1

Introduction.................................................................................................................................................3

Part A..........................................................................................................................................................3

1. Initial investment.............................................................................................................................3

2. Operating cash flows.......................................................................................................................5

3. Terminal cash flows.........................................................................................................................7

Part B...........................................................................................................................................................8

Cash flow streams....................................................................................................................................8

Part C.........................................................................................................................................................10

1. Payback Period..............................................................................................................................10

2. Net Present Value..........................................................................................................................11

3. Internal Rate of return....................................................................................................................13

Part d.........................................................................................................................................................15

Graphical representation of IRR profiles with NPVs.............................................................................15

Part e......................................................................................................................................................17

i. Conflicts of results.....................................................................................................................17

ii. Decision making under the different situations..........................................................................17

Part f..........................................................................................................................................................18

Conclusion.................................................................................................................................................19

References.................................................................................................................................................20

Appendices................................................................................................................................................22

Table of Contents

Executive summary.....................................................................................................................................1

Introduction.................................................................................................................................................3

Part A..........................................................................................................................................................3

1. Initial investment.............................................................................................................................3

2. Operating cash flows.......................................................................................................................5

3. Terminal cash flows.........................................................................................................................7

Part B...........................................................................................................................................................8

Cash flow streams....................................................................................................................................8

Part C.........................................................................................................................................................10

1. Payback Period..............................................................................................................................10

2. Net Present Value..........................................................................................................................11

3. Internal Rate of return....................................................................................................................13

Part d.........................................................................................................................................................15

Graphical representation of IRR profiles with NPVs.............................................................................15

Part e......................................................................................................................................................17

i. Conflicts of results.....................................................................................................................17

ii. Decision making under the different situations..........................................................................17

Part f..........................................................................................................................................................18

Conclusion.................................................................................................................................................19

References.................................................................................................................................................20

Appendices................................................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appraisal of Capital Investments 3

Introduction:

Capital budgeting is the most important part of financial management as it involves evaluation of

decisions regarding the capital investment in any business or project. As a large sum of capital

funds of the firm is investment in these decisions for generally longer terms and it is not easily

possible to reverse the decision once made, such decisions are required to be made after

assessing all the potential benefits and risks involved in the possible investment plans. To

evaluate each proposal of capital investment the project or business managers must use various

techniques of capital budgeting such as Net present value, Payback period or Internal rate of

return etc.

In the instant case of CQU Printers, the firm has to critically evaluate the replacement decision

and the year in which such decision must be implemented. Also, the firm has to select the most

appropriate investment option between Printer A or Printer B so as to increase its profitability

with the efficient utilization of resources available with it.

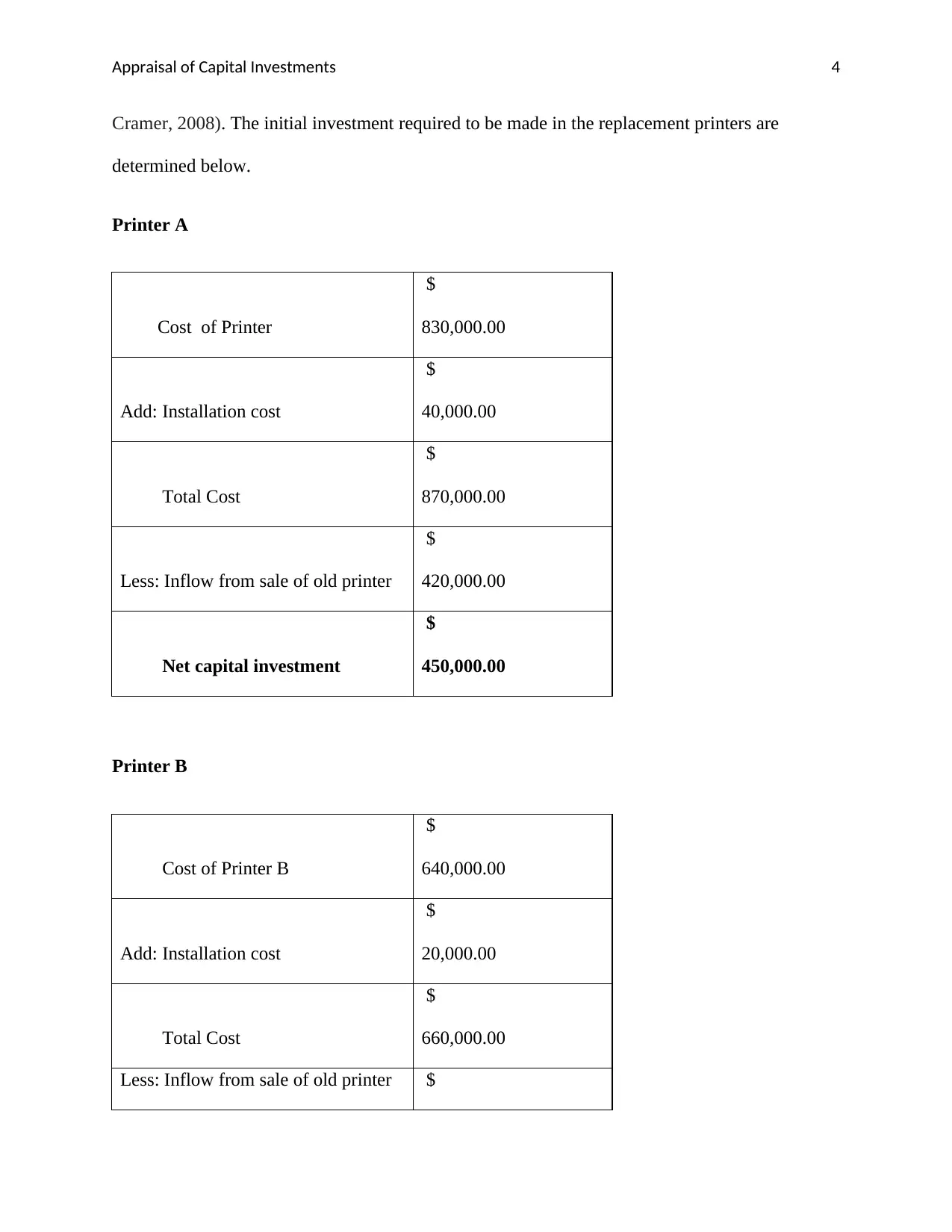

Part A

1. Initial investment:

Initial investment is the deployment of capital funds in the acquisition and installation of an asset

to the business or to undertake any project. It is made in the base year. In the given case, the firm

is selling the old printer and the value realized on its sale will be deducted from the cost of new

printer. Cost of new printer will include both the acquisition and installation cost (Correia &

Introduction:

Capital budgeting is the most important part of financial management as it involves evaluation of

decisions regarding the capital investment in any business or project. As a large sum of capital

funds of the firm is investment in these decisions for generally longer terms and it is not easily

possible to reverse the decision once made, such decisions are required to be made after

assessing all the potential benefits and risks involved in the possible investment plans. To

evaluate each proposal of capital investment the project or business managers must use various

techniques of capital budgeting such as Net present value, Payback period or Internal rate of

return etc.

In the instant case of CQU Printers, the firm has to critically evaluate the replacement decision

and the year in which such decision must be implemented. Also, the firm has to select the most

appropriate investment option between Printer A or Printer B so as to increase its profitability

with the efficient utilization of resources available with it.

Part A

1. Initial investment:

Initial investment is the deployment of capital funds in the acquisition and installation of an asset

to the business or to undertake any project. It is made in the base year. In the given case, the firm

is selling the old printer and the value realized on its sale will be deducted from the cost of new

printer. Cost of new printer will include both the acquisition and installation cost (Correia &

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments 4

Cramer, 2008). The initial investment required to be made in the replacement printers are

determined below.

Printer A

Cost of Printer

$

830,000.00

Add: Installation cost

$

40,000.00

Total Cost

$

870,000.00

Less: Inflow from sale of old printer

$

420,000.00

Net capital investment

$

450,000.00

Printer B

Cost of Printer B

$

640,000.00

Add: Installation cost

$

20,000.00

Total Cost

$

660,000.00

Less: Inflow from sale of old printer $

Cramer, 2008). The initial investment required to be made in the replacement printers are

determined below.

Printer A

Cost of Printer

$

830,000.00

Add: Installation cost

$

40,000.00

Total Cost

$

870,000.00

Less: Inflow from sale of old printer

$

420,000.00

Net capital investment

$

450,000.00

Printer B

Cost of Printer B

$

640,000.00

Add: Installation cost

$

20,000.00

Total Cost

$

660,000.00

Less: Inflow from sale of old printer $

Appraisal of Capital Investments 5

420,000.00

Net capital investment

$

240,000.00

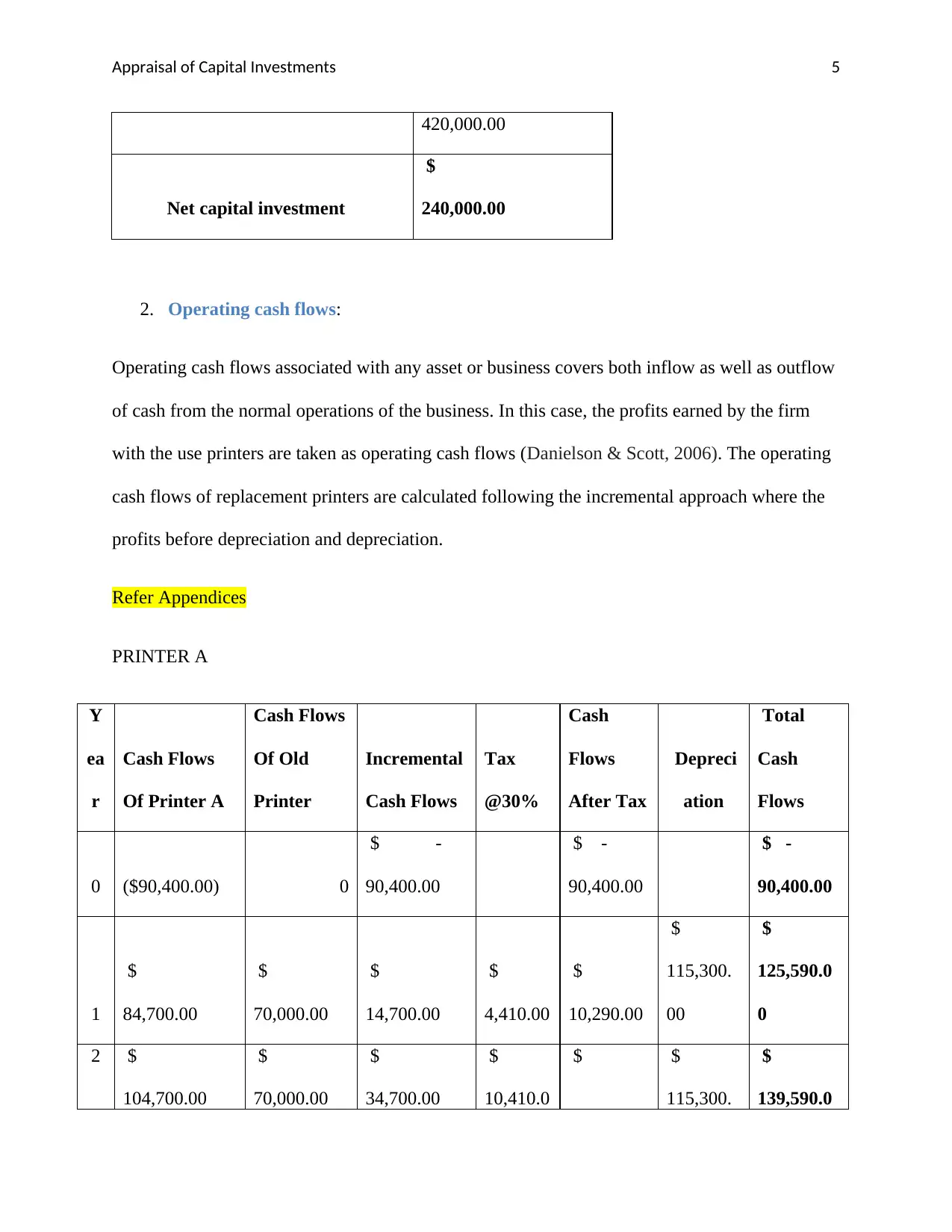

2. Operating cash flows:

Operating cash flows associated with any asset or business covers both inflow as well as outflow

of cash from the normal operations of the business. In this case, the profits earned by the firm

with the use printers are taken as operating cash flows (Danielson & Scott, 2006). The operating

cash flows of replacement printers are calculated following the incremental approach where the

profits before depreciation and depreciation.

Refer Appendices

PRINTER A

Y

ea

r

Cash Flows

Of Printer A

Cash Flows

Of Old

Printer

Incremental

Cash Flows

Tax

@30%

Cash

Flows

After Tax

Depreci

ation

Total

Cash

Flows

0 ($90,400.00) 0

$ -

90,400.00

$ -

90,400.00

$ -

90,400.00

1

$

84,700.00

$

70,000.00

$

14,700.00

$

4,410.00

$

10,290.00

$

115,300.

00

$

125,590.0

0

2 $

104,700.00

$

70,000.00

$

34,700.00

$

10,410.0

$ $

115,300.

$

139,590.0

420,000.00

Net capital investment

$

240,000.00

2. Operating cash flows:

Operating cash flows associated with any asset or business covers both inflow as well as outflow

of cash from the normal operations of the business. In this case, the profits earned by the firm

with the use printers are taken as operating cash flows (Danielson & Scott, 2006). The operating

cash flows of replacement printers are calculated following the incremental approach where the

profits before depreciation and depreciation.

Refer Appendices

PRINTER A

Y

ea

r

Cash Flows

Of Printer A

Cash Flows

Of Old

Printer

Incremental

Cash Flows

Tax

@30%

Cash

Flows

After Tax

Depreci

ation

Total

Cash

Flows

0 ($90,400.00) 0

$ -

90,400.00

$ -

90,400.00

$ -

90,400.00

1

$

84,700.00

$

70,000.00

$

14,700.00

$

4,410.00

$

10,290.00

$

115,300.

00

$

125,590.0

0

2 $

104,700.00

$

70,000.00

$

34,700.00

$

10,410.0

$ $

115,300.

$

139,590.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appraisal of Capital Investments 6

0 24,290.00 00 0

3

$

134,700.00

$

70,000.00

$

64,700.00

$

19,410.0

0

$

45,290.00

$

115,300.

00

$

160,590.0

0

4

$

164,700.00

$

70,000.00

$

94,700.00

$

28,410.0

0

$

66,290.00

$

115,300.

00

$

181,590.0

0

5

$

204,700.00

$

70,000.00

$

134,700.00

$

40,410.0

0

$

94,290.00

$

115,300.

00

$

209,590.0

0

PRINTER B

Ye

ar

Cash Flows

Of Printer B

Cash Flows

Of Old

Printer

Incremental

Cash Flows

Tax

@30%

Cash

Flows

After Tax

Deprecia

tion

Total

Cash

Flows

0 $0.00 0

$

-

$

-

$

-

1

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

2

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

3 $ $ $ $ $ $ $

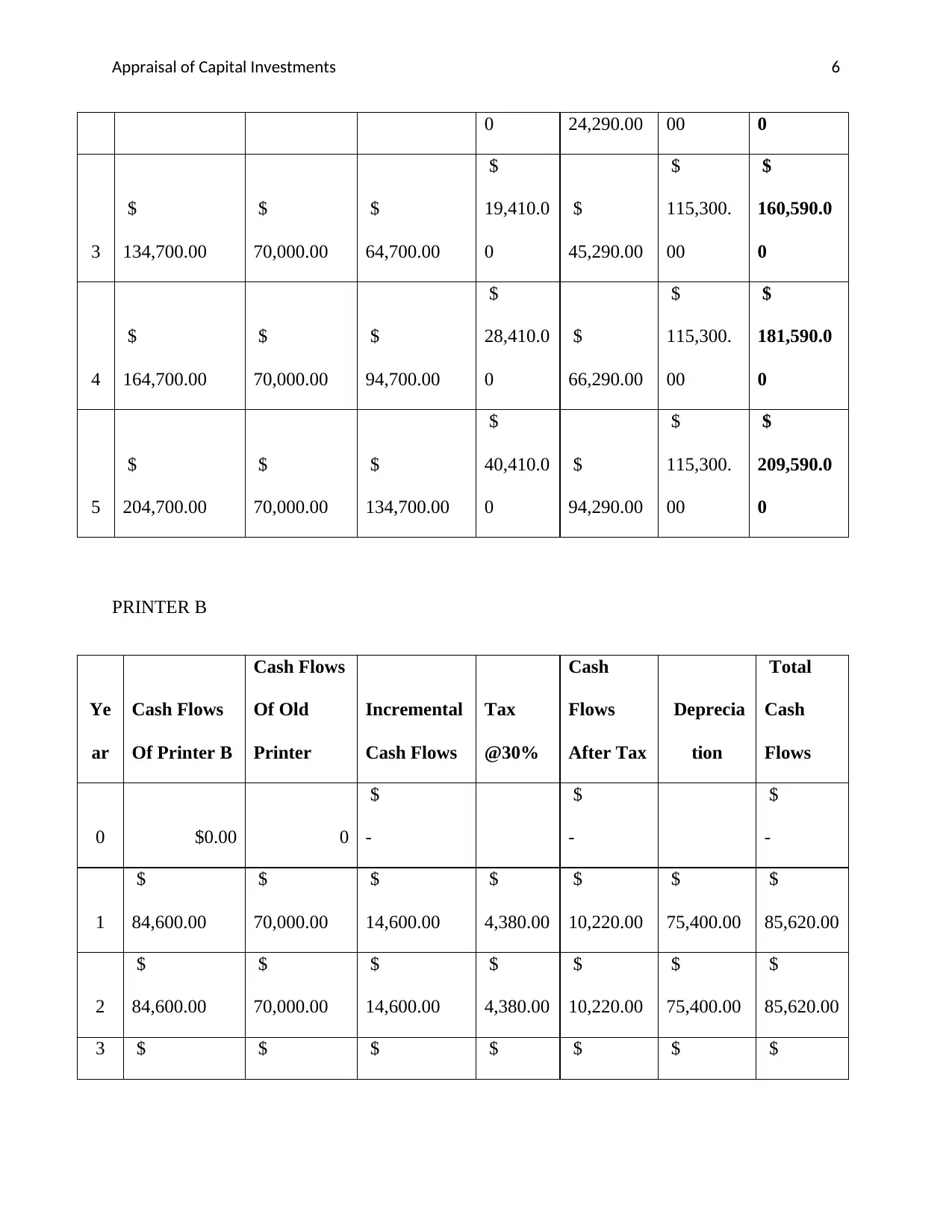

0 24,290.00 00 0

3

$

134,700.00

$

70,000.00

$

64,700.00

$

19,410.0

0

$

45,290.00

$

115,300.

00

$

160,590.0

0

4

$

164,700.00

$

70,000.00

$

94,700.00

$

28,410.0

0

$

66,290.00

$

115,300.

00

$

181,590.0

0

5

$

204,700.00

$

70,000.00

$

134,700.00

$

40,410.0

0

$

94,290.00

$

115,300.

00

$

209,590.0

0

PRINTER B

Ye

ar

Cash Flows

Of Printer B

Cash Flows

Of Old

Printer

Incremental

Cash Flows

Tax

@30%

Cash

Flows

After Tax

Deprecia

tion

Total

Cash

Flows

0 $0.00 0

$

-

$

-

$

-

1

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

2

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

3 $ $ $ $ $ $ $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments 7

84,600.00 70,000.00 14,600.00 4,380.00 10,220.00 75,400.00 85,620.00

4

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

5

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

Therefore total incremental operating cash flows of printer A are $725550 and that of printer B

are $ 428100.

3. Terminal cash flows:

The cash flows from activities other than operating and that occur in the last year of project

duration or useful life of the concerned asset, are the terminal cash flows of the project or

business. In the given case, the useful life of all the printers is 5 years and at the end of 5th year

the new printers are expected to be sold out by the firm. Therefore, the value realized on sale of

printers will be the terminal cash flows of the business. The capital gain taxation has been

ignored while calculating the terminal cash flows as per the requirement of the case.

Particular PRINTER A PRINTER B

Salvage value (at 5th yearend)

$

400,000.00 $ 330,000.00

84,600.00 70,000.00 14,600.00 4,380.00 10,220.00 75,400.00 85,620.00

4

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

5

$

84,600.00

$

70,000.00

$

14,600.00

$

4,380.00

$

10,220.00

$

75,400.00

$

85,620.00

Therefore total incremental operating cash flows of printer A are $725550 and that of printer B

are $ 428100.

3. Terminal cash flows:

The cash flows from activities other than operating and that occur in the last year of project

duration or useful life of the concerned asset, are the terminal cash flows of the project or

business. In the given case, the useful life of all the printers is 5 years and at the end of 5th year

the new printers are expected to be sold out by the firm. Therefore, the value realized on sale of

printers will be the terminal cash flows of the business. The capital gain taxation has been

ignored while calculating the terminal cash flows as per the requirement of the case.

Particular PRINTER A PRINTER B

Salvage value (at 5th yearend)

$

400,000.00 $ 330,000.00

Appraisal of Capital Investments 8

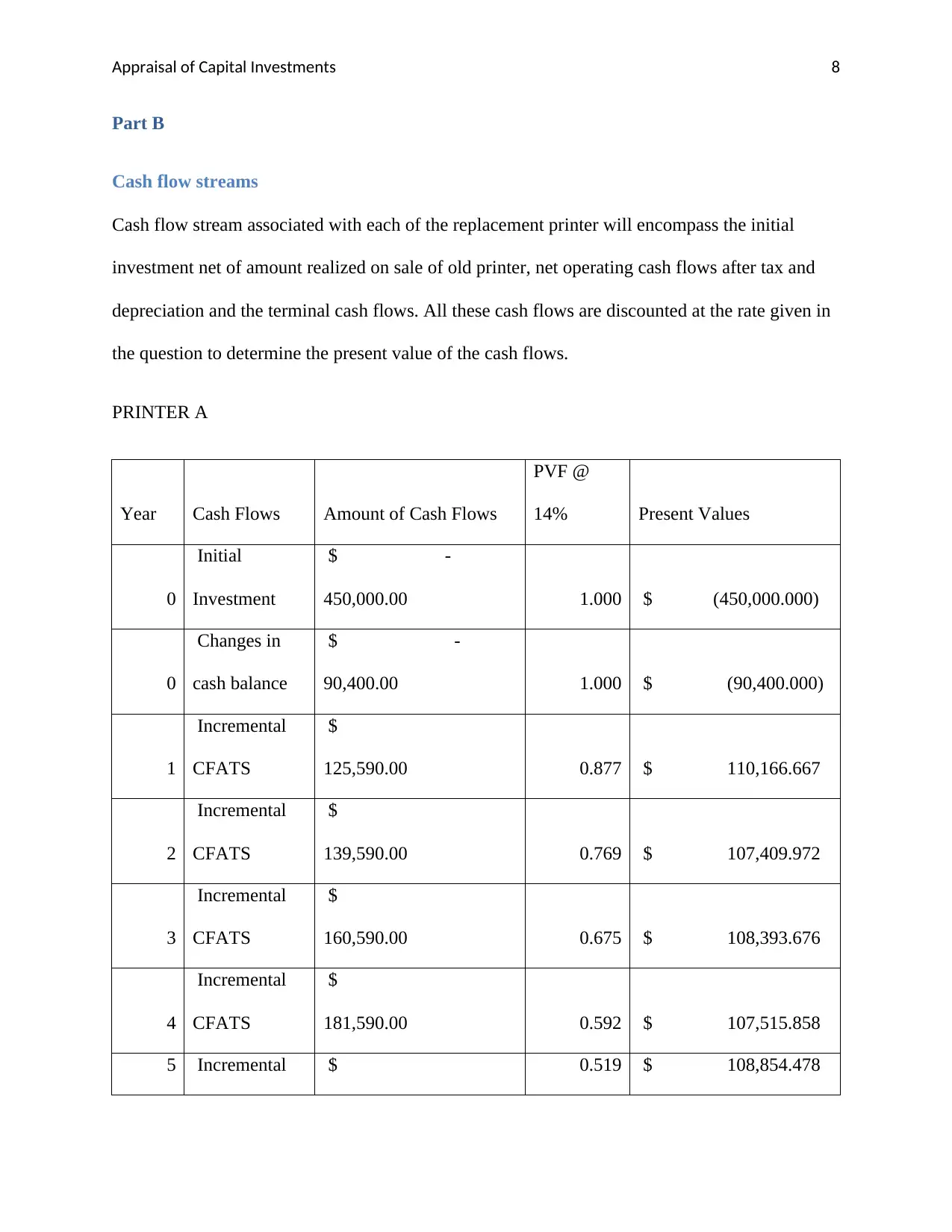

Part B

Cash flow streams

Cash flow stream associated with each of the replacement printer will encompass the initial

investment net of amount realized on sale of old printer, net operating cash flows after tax and

depreciation and the terminal cash flows. All these cash flows are discounted at the rate given in

the question to determine the present value of the cash flows.

PRINTER A

Year Cash Flows Amount of Cash Flows

PVF @

14% Present Values

0

Initial

Investment

$ -

450,000.00 1.000 $ (450,000.000)

0

Changes in

cash balance

$ -

90,400.00 1.000 $ (90,400.000)

1

Incremental

CFATS

$

125,590.00 0.877 $ 110,166.667

2

Incremental

CFATS

$

139,590.00 0.769 $ 107,409.972

3

Incremental

CFATS

$

160,590.00 0.675 $ 108,393.676

4

Incremental

CFATS

$

181,590.00 0.592 $ 107,515.858

5 Incremental $ 0.519 $ 108,854.478

Part B

Cash flow streams

Cash flow stream associated with each of the replacement printer will encompass the initial

investment net of amount realized on sale of old printer, net operating cash flows after tax and

depreciation and the terminal cash flows. All these cash flows are discounted at the rate given in

the question to determine the present value of the cash flows.

PRINTER A

Year Cash Flows Amount of Cash Flows

PVF @

14% Present Values

0

Initial

Investment

$ -

450,000.00 1.000 $ (450,000.000)

0

Changes in

cash balance

$ -

90,400.00 1.000 $ (90,400.000)

1

Incremental

CFATS

$

125,590.00 0.877 $ 110,166.667

2

Incremental

CFATS

$

139,590.00 0.769 $ 107,409.972

3

Incremental

CFATS

$

160,590.00 0.675 $ 108,393.676

4

Incremental

CFATS

$

181,590.00 0.592 $ 107,515.858

5 Incremental $ 0.519 $ 108,854.478

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

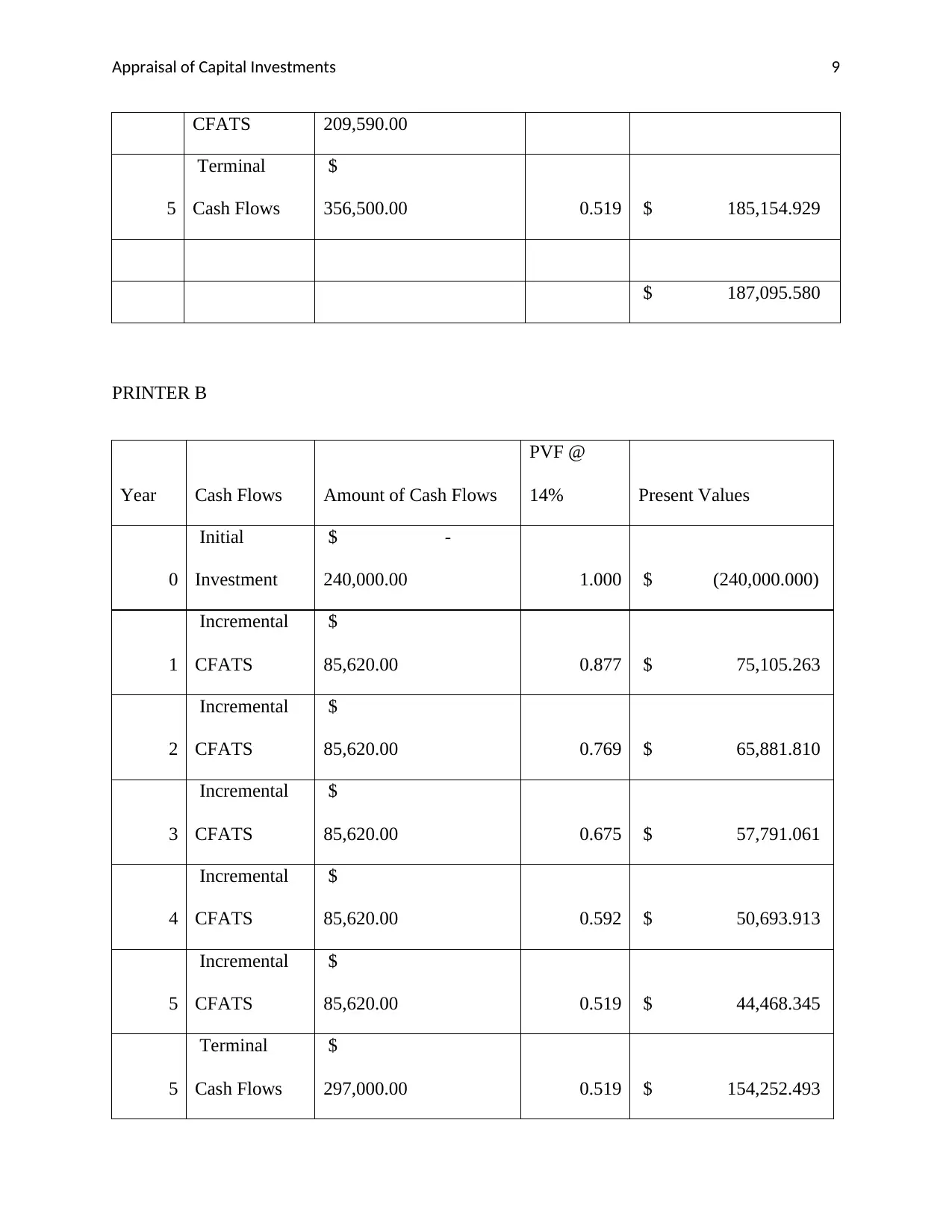

Appraisal of Capital Investments 9

CFATS 209,590.00

5

Terminal

Cash Flows

$

356,500.00 0.519 $ 185,154.929

$ 187,095.580

PRINTER B

Year Cash Flows Amount of Cash Flows

PVF @

14% Present Values

0

Initial

Investment

$ -

240,000.00 1.000 $ (240,000.000)

1

Incremental

CFATS

$

85,620.00 0.877 $ 75,105.263

2

Incremental

CFATS

$

85,620.00 0.769 $ 65,881.810

3

Incremental

CFATS

$

85,620.00 0.675 $ 57,791.061

4

Incremental

CFATS

$

85,620.00 0.592 $ 50,693.913

5

Incremental

CFATS

$

85,620.00 0.519 $ 44,468.345

5

Terminal

Cash Flows

$

297,000.00 0.519 $ 154,252.493

CFATS 209,590.00

5

Terminal

Cash Flows

$

356,500.00 0.519 $ 185,154.929

$ 187,095.580

PRINTER B

Year Cash Flows Amount of Cash Flows

PVF @

14% Present Values

0

Initial

Investment

$ -

240,000.00 1.000 $ (240,000.000)

1

Incremental

CFATS

$

85,620.00 0.877 $ 75,105.263

2

Incremental

CFATS

$

85,620.00 0.769 $ 65,881.810

3

Incremental

CFATS

$

85,620.00 0.675 $ 57,791.061

4

Incremental

CFATS

$

85,620.00 0.592 $ 50,693.913

5

Incremental

CFATS

$

85,620.00 0.519 $ 44,468.345

5

Terminal

Cash Flows

$

297,000.00 0.519 $ 154,252.493

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appraisal of Capital Investments 10

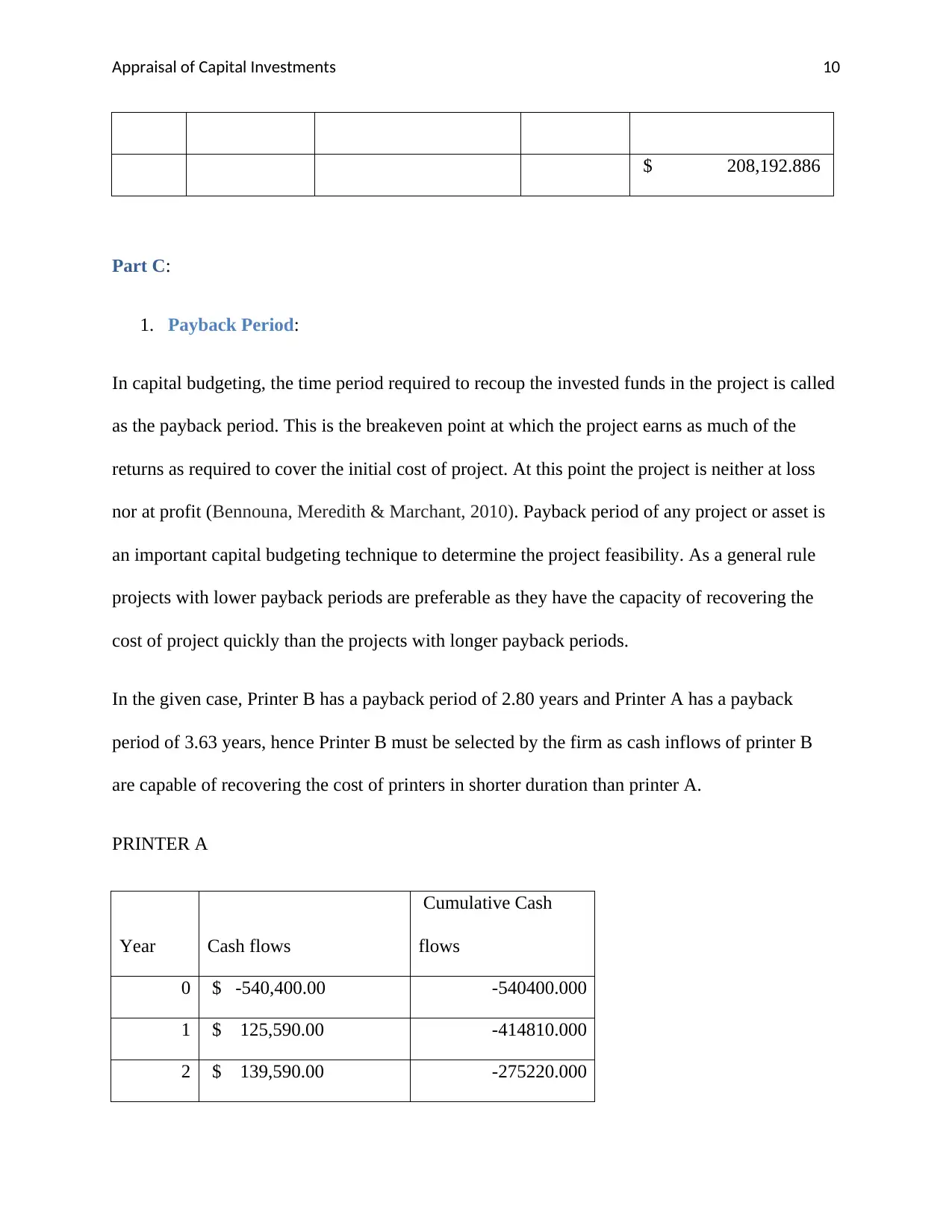

$ 208,192.886

Part C:

1. Payback Period:

In capital budgeting, the time period required to recoup the invested funds in the project is called

as the payback period. This is the breakeven point at which the project earns as much of the

returns as required to cover the initial cost of project. At this point the project is neither at loss

nor at profit (Bennouna, Meredith & Marchant, 2010). Payback period of any project or asset is

an important capital budgeting technique to determine the project feasibility. As a general rule

projects with lower payback periods are preferable as they have the capacity of recovering the

cost of project quickly than the projects with longer payback periods.

In the given case, Printer B has a payback period of 2.80 years and Printer A has a payback

period of 3.63 years, hence Printer B must be selected by the firm as cash inflows of printer B

are capable of recovering the cost of printers in shorter duration than printer A.

PRINTER A

Year Cash flows

Cumulative Cash

flows

0 $ -540,400.00 -540400.000

1 $ 125,590.00 -414810.000

2 $ 139,590.00 -275220.000

$ 208,192.886

Part C:

1. Payback Period:

In capital budgeting, the time period required to recoup the invested funds in the project is called

as the payback period. This is the breakeven point at which the project earns as much of the

returns as required to cover the initial cost of project. At this point the project is neither at loss

nor at profit (Bennouna, Meredith & Marchant, 2010). Payback period of any project or asset is

an important capital budgeting technique to determine the project feasibility. As a general rule

projects with lower payback periods are preferable as they have the capacity of recovering the

cost of project quickly than the projects with longer payback periods.

In the given case, Printer B has a payback period of 2.80 years and Printer A has a payback

period of 3.63 years, hence Printer B must be selected by the firm as cash inflows of printer B

are capable of recovering the cost of printers in shorter duration than printer A.

PRINTER A

Year Cash flows

Cumulative Cash

flows

0 $ -540,400.00 -540400.000

1 $ 125,590.00 -414810.000

2 $ 139,590.00 -275220.000

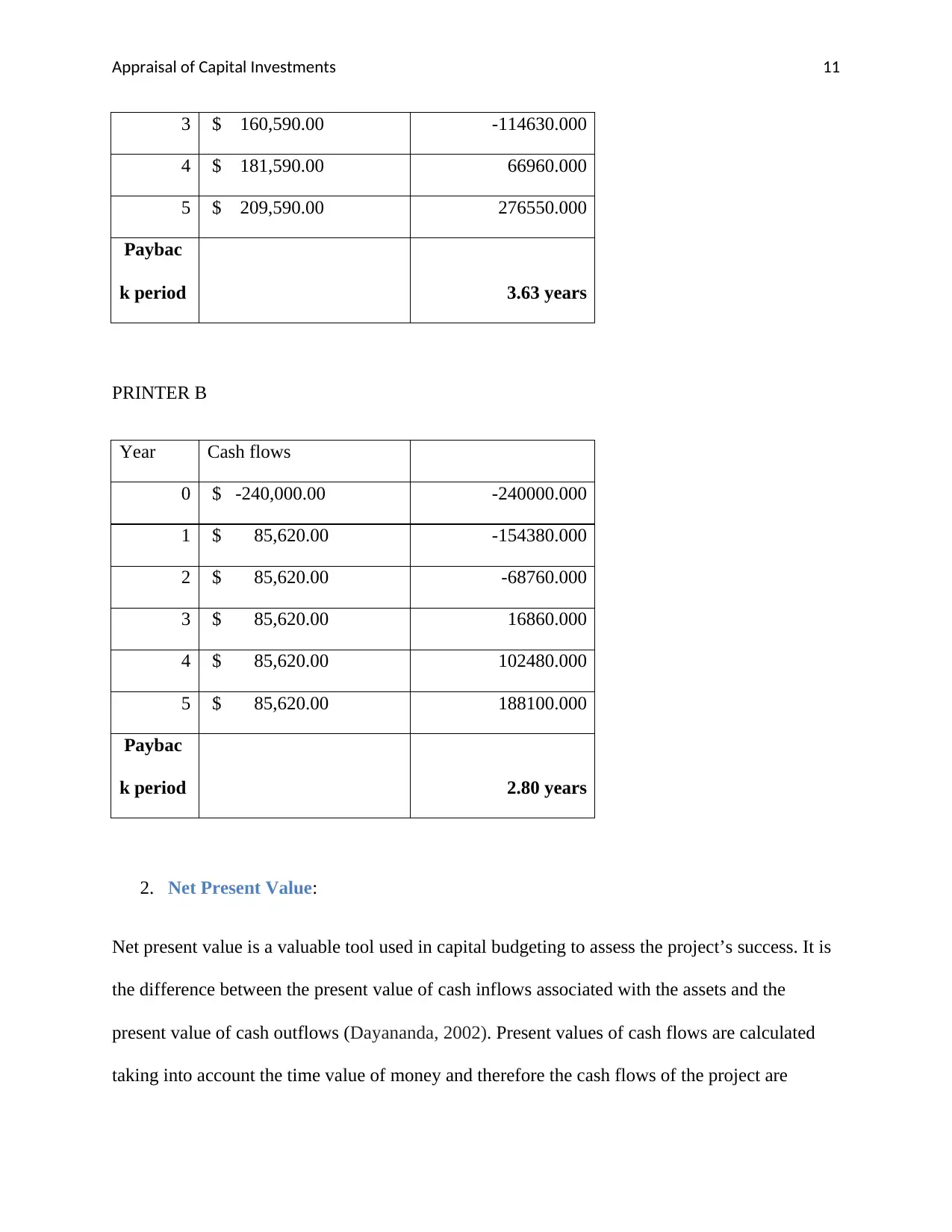

Appraisal of Capital Investments 11

3 $ 160,590.00 -114630.000

4 $ 181,590.00 66960.000

5 $ 209,590.00 276550.000

Paybac

k period 3.63 years

PRINTER B

Year Cash flows

0 $ -240,000.00 -240000.000

1 $ 85,620.00 -154380.000

2 $ 85,620.00 -68760.000

3 $ 85,620.00 16860.000

4 $ 85,620.00 102480.000

5 $ 85,620.00 188100.000

Paybac

k period 2.80 years

2. Net Present Value:

Net present value is a valuable tool used in capital budgeting to assess the project’s success. It is

the difference between the present value of cash inflows associated with the assets and the

present value of cash outflows (Dayananda, 2002). Present values of cash flows are calculated

taking into account the time value of money and therefore the cash flows of the project are

3 $ 160,590.00 -114630.000

4 $ 181,590.00 66960.000

5 $ 209,590.00 276550.000

Paybac

k period 3.63 years

PRINTER B

Year Cash flows

0 $ -240,000.00 -240000.000

1 $ 85,620.00 -154380.000

2 $ 85,620.00 -68760.000

3 $ 85,620.00 16860.000

4 $ 85,620.00 102480.000

5 $ 85,620.00 188100.000

Paybac

k period 2.80 years

2. Net Present Value:

Net present value is a valuable tool used in capital budgeting to assess the project’s success. It is

the difference between the present value of cash inflows associated with the assets and the

present value of cash outflows (Dayananda, 2002). Present values of cash flows are calculated

taking into account the time value of money and therefore the cash flows of the project are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.