Capital Budgeting Analysis: NPV, Payback Period, and Project Appraisal

VerifiedAdded on 2022/10/08

|6

|722

|45

Homework Assignment

AI Summary

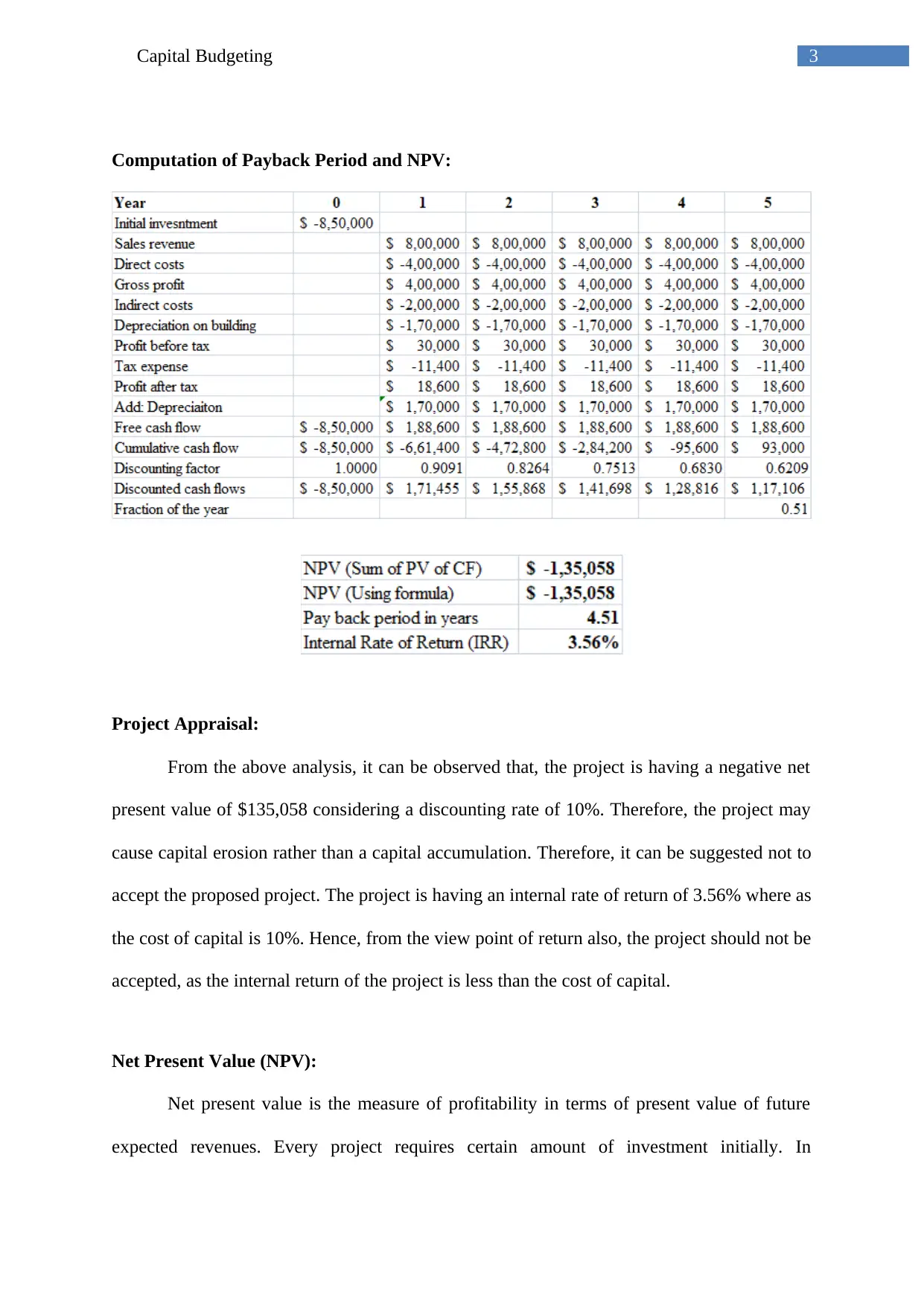

This assignment provides a comprehensive analysis of capital budgeting techniques, focusing on Net Present Value (NPV) and payback period calculations. The student analyzes a project, concluding that it has a negative NPV and an extended payback period, suggesting the project should not be accepted. The analysis includes detailed explanations of both NPV and payback period methods, emphasizing their roles in project appraisal and investment decision-making. The document also includes references to academic sources. The analysis suggests that the project may cause capital erosion rather than capital accumulation. The project is also having an internal rate of return of 3.56% where as the cost of capital is 10%. Hence, from the view point of return also, the project should not be accepted, as the internal return of the project is less than the cost of capital.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.