Investment Decisions: Capital Budgeting for Sooner Clinics

VerifiedAdded on 2023/05/28

|14

|1766

|268

Case Study

AI Summary

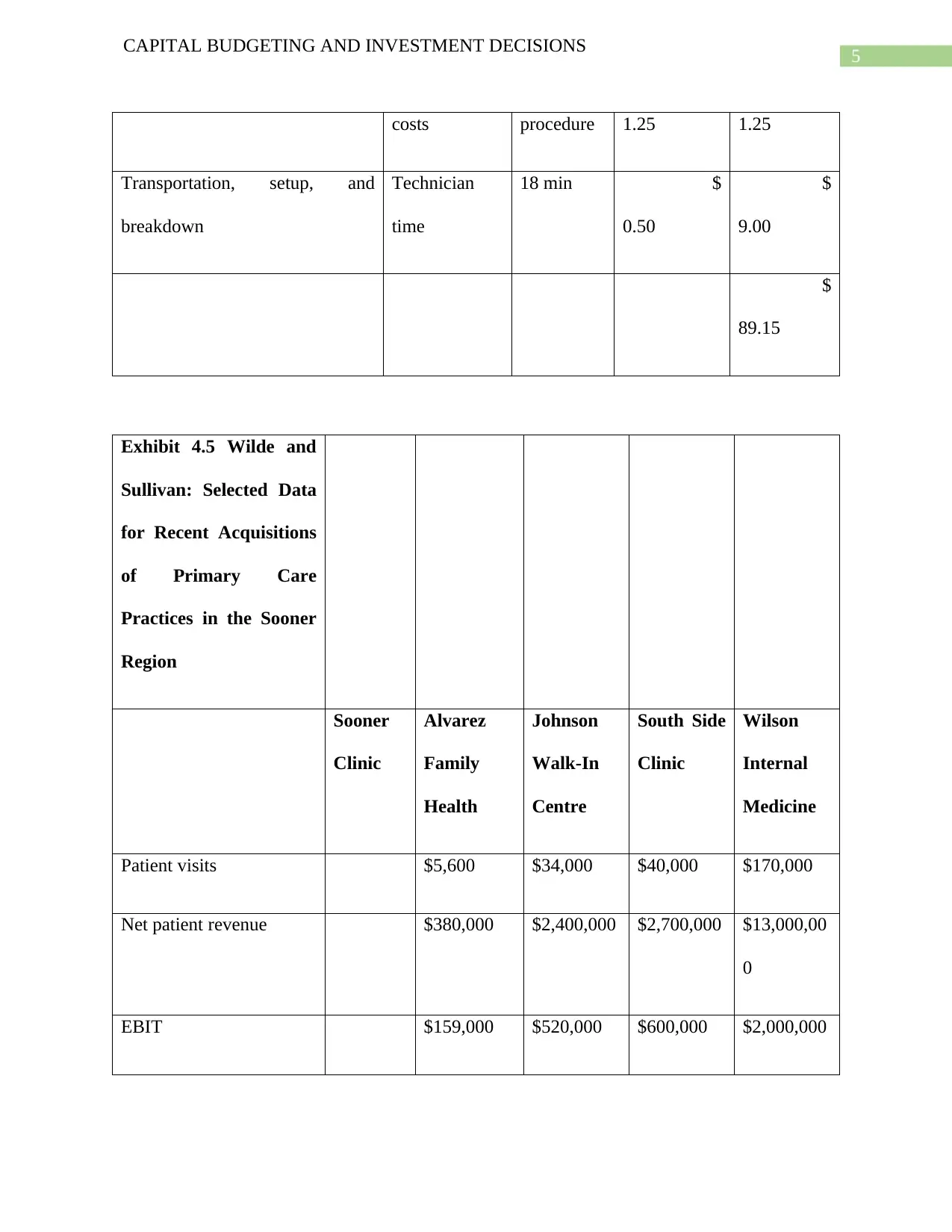

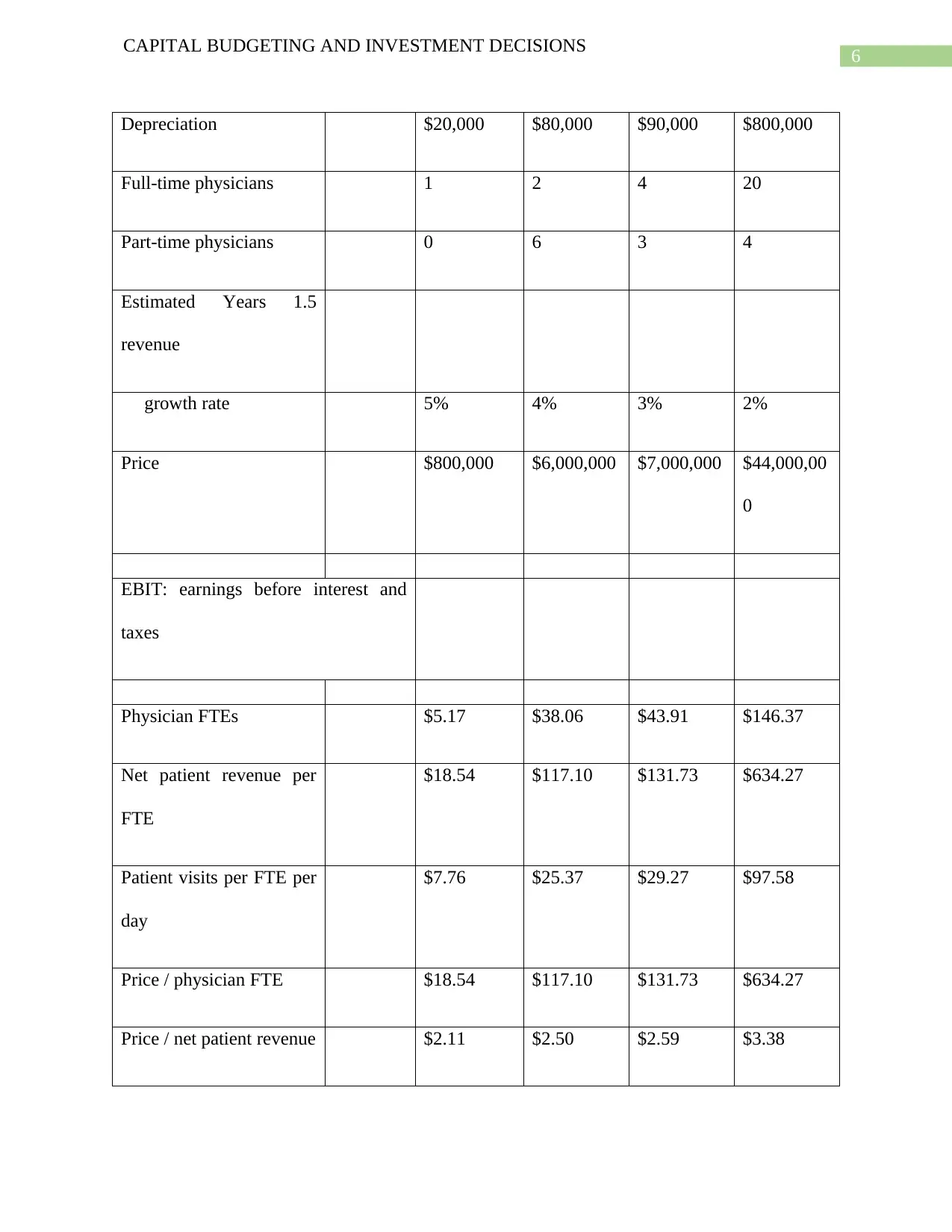

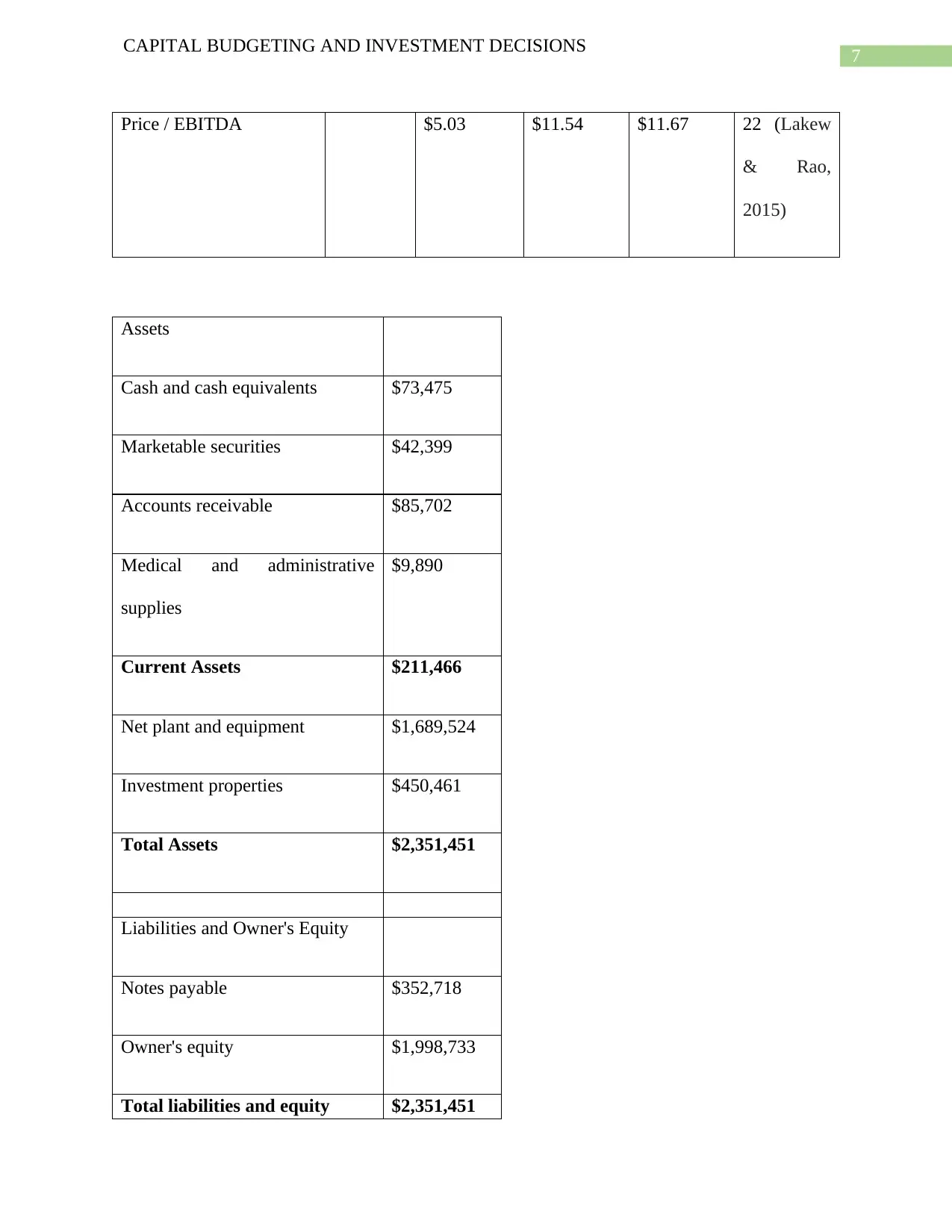

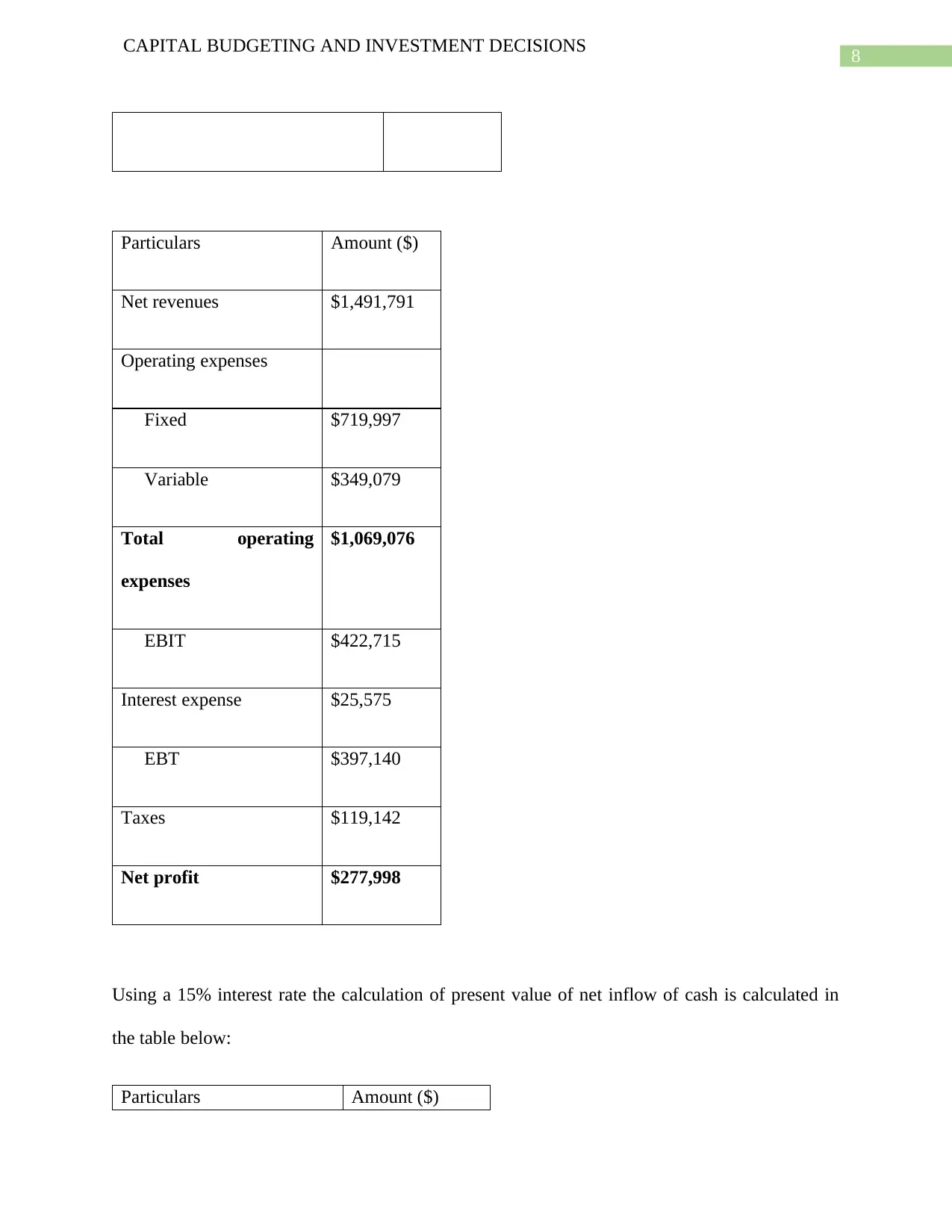

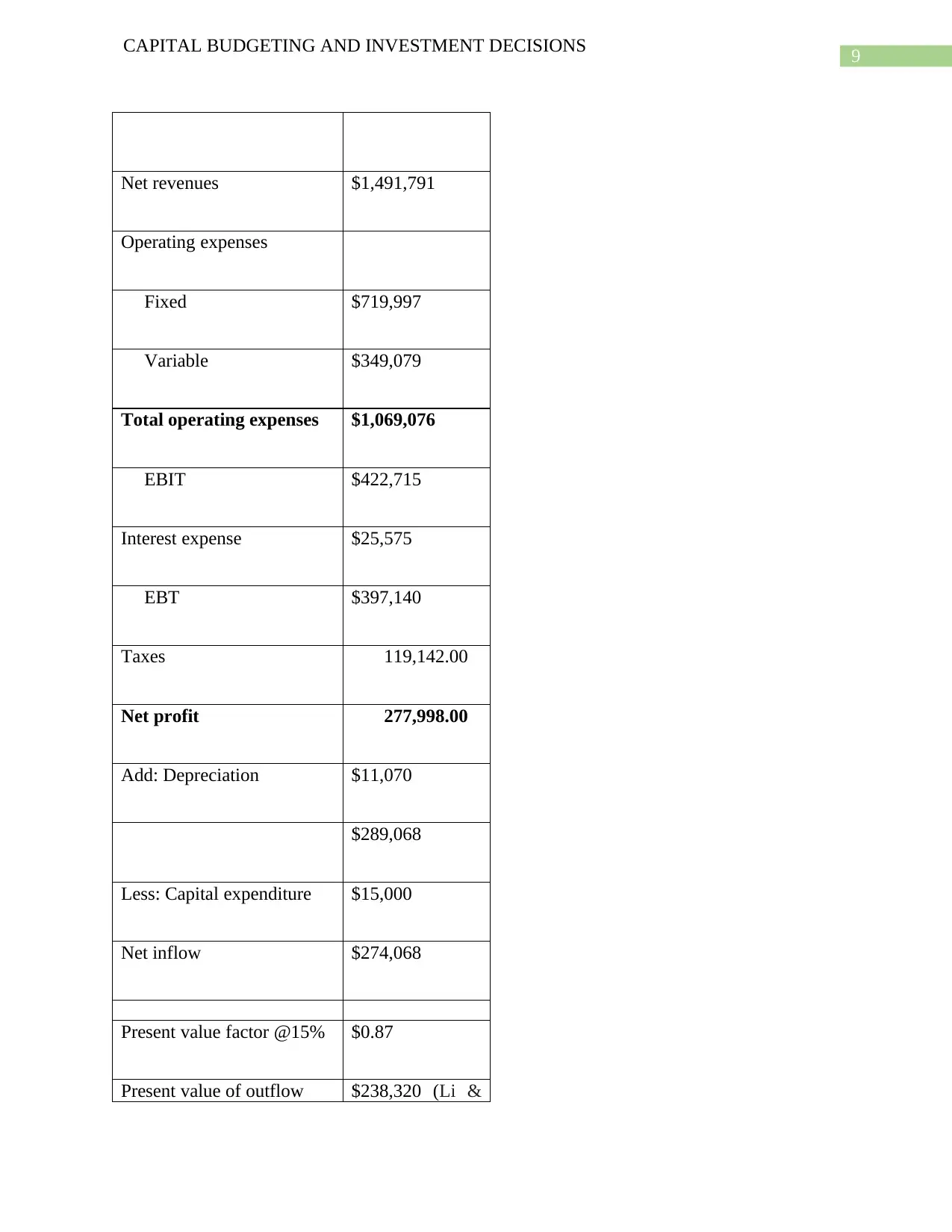

This case study delves into the capital budgeting and investment decisions facing Sooner Clinics, a subsidiary of Sooner Health System. It examines various financial aspects, including activity-based costing, revenue analysis, and balance sheet assessment. The analysis includes calculations of present value of cash flows, EBIT, and the overall valuation of the organization for potential acquisition. It considers different operational alternatives, cost drivers, and market data from comparable acquisitions. Using a 15% interest rate, the present value of net cash inflow is calculated and compared to the annual cash outflow. The study also estimates the organization's value based on future growth and cost of capital. The recommendation is for UHSC to acquire Sooner Clinics, given that the calculated value significantly exceeds the acquisition cost. This study provides a comprehensive financial overview and strategic recommendation based on thorough analysis and calculations.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.