Finance Report: Capital Budgeting Analysis for Pinto Limited Project

VerifiedAdded on 2021/05/31

|7

|1424

|115

Report

AI Summary

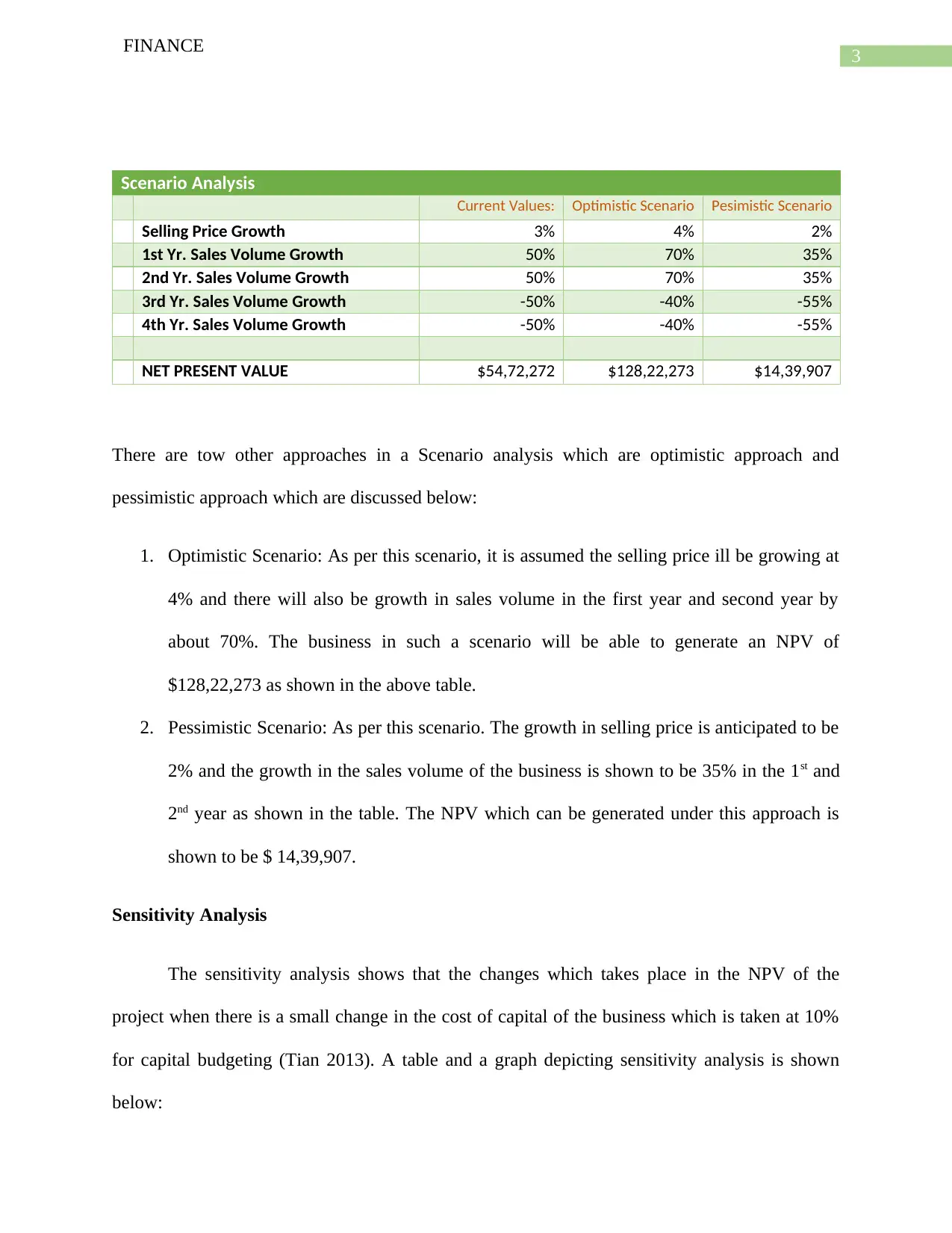

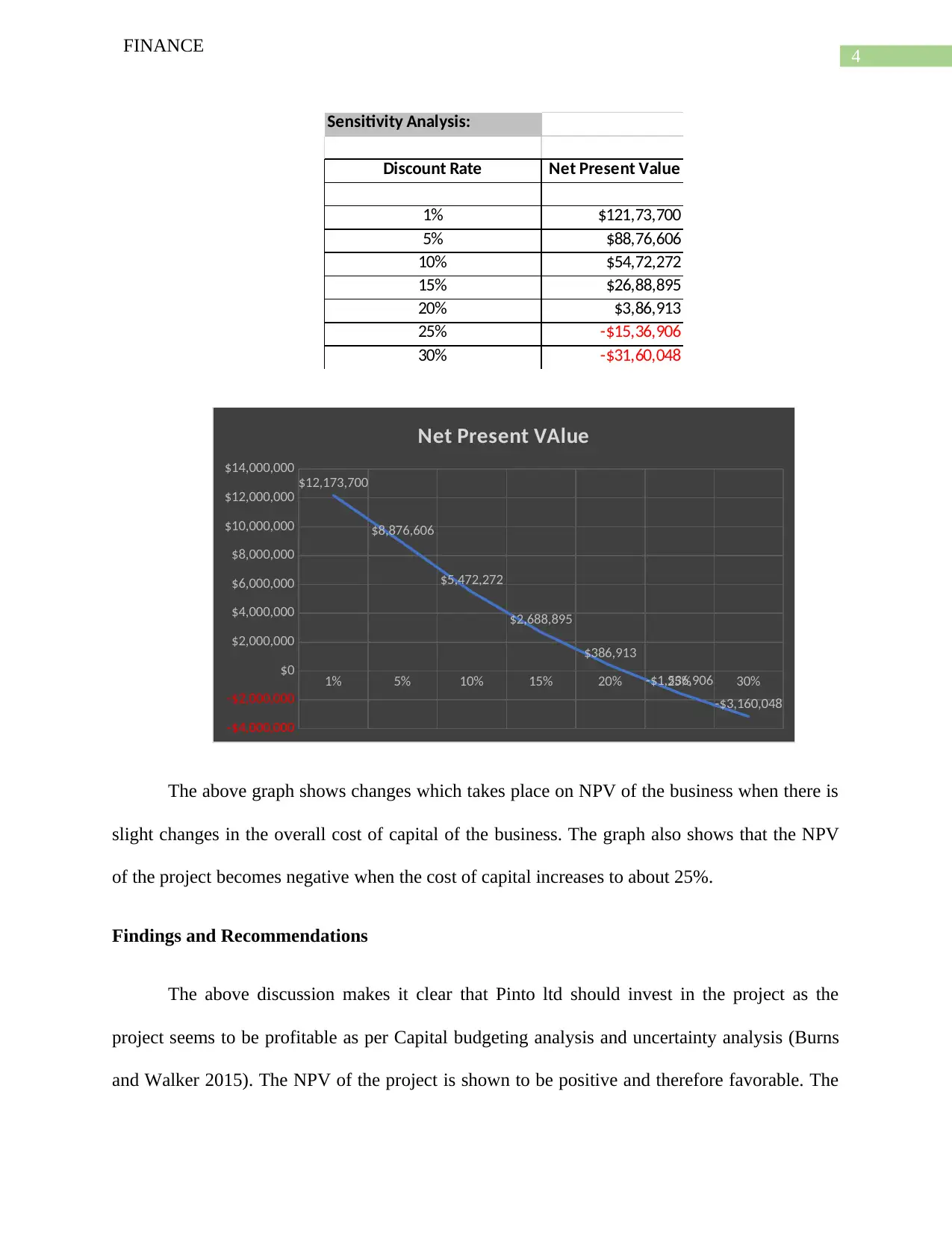

This report analyzes a capital budgeting project for Pinto Limited, evaluating the viability of a new product market investment. The report uses several capital budgeting techniques, including Net Present Value (NPV), Profitability Index, Payback Period, Discounted Payback Period, and Internal Rate of Return (IRR). The initial investment is estimated at $180,00,000, and the analysis is conducted over five years. The report also incorporates uncertainty analysis through scenario and sensitivity analysis to assess the project's risks and potential returns under optimistic and pessimistic scenarios, including changes in sales volume and selling price. The findings suggest that the project is profitable, with positive NPV, a profitability index greater than 1, and a favorable IRR compared to the cost of capital. The report recommends that Pinto Ltd. reduce operational costs, maximize sales, and maintain a proper capital structure. The report concludes that the project is a favorable investment opportunity.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.