Capital Budgeting and Project Evaluation: Risk Analysis and Cash Flow

VerifiedAdded on 2021/06/22

|13

|3612

|26

Report

AI Summary

This report delves into the core concepts of capital budgeting and project evaluation, essential for sound financial decision-making within organizations. It begins with an introduction to capital budgeting, outlining its significance in assessing project investments and estimating key financial metrics. The report then explores incremental and operating cash flows, along with depreciation methods and working capital considerations. A significant portion of the report is dedicated to risk analysis and project evaluation, including scenario analysis with cash flow projections, and sensitivity analyses under base, best, and worst-case scenarios. The report also incorporates a comparative analysis to highlight the impact of different scenarios on project outcomes. Overall, the report provides a practical application of financial tools to assess project feasibility and profitability, with specific examples related to a production unit.

[Due Date]

Business Finance

Capital Budgeting and

Project Evaluation

[Student Name]

Business Finance

Capital Budgeting and

Project Evaluation

[Student Name]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Index Title Page No

1 Introduction 1

2 Part 1 - Capital budgeting 1

3 Part 2: Risk Analysis and Project Evaluation 3

3.1 Scenario Analysis with Cash Flow 3

3.2 Sensitivity of the project 6

3.2.1 Case 1: Base Case 6

3.2.2 Case 2: Best Case 7

3.2.3 Case 3: Worst Case 8

4 Comparative Analysis 9

5 Conclusion 10

Reference 11

1 Introduction 1

2 Part 1 - Capital budgeting 1

3 Part 2: Risk Analysis and Project Evaluation 3

3.1 Scenario Analysis with Cash Flow 3

3.2 Sensitivity of the project 6

3.2.1 Case 1: Base Case 6

3.2.2 Case 2: Best Case 7

3.2.3 Case 3: Worst Case 8

4 Comparative Analysis 9

5 Conclusion 10

Reference 11

1

CAPITAL BUDGETING AND PROJECT EVALUATION

1. Introduction

In any organization, project analysis is considered an important factor involved in

the evaluation of project investment. Based on the project analysis companies able to

decide reasonably and comprehensively [1]. In this scenario, capital budgeting is

considered as the major factor for the evaluation of projects and investments with the

estimation of metrics involved in the project. Capital budgeting is a set of processes

involved in the analysis of cash inflow and cash outflow for the determination of

expected returns in the project [2]. Based on capital budgeting companies decides the

acceptance/rejection of a particular project. This provides a systematic evaluation of

the project about the resources and goals of the organization involved in the project

[3]. This report about information about capital budgeting and project evaluation.

Further, this report provides the scenario analysis of the production unit through

sensitivity analysis in terms of the best and worst cases. Finally, the overall

implication of research concerning the production industry is provided.

2. Part 1 - Capital budgeting

Q 1.1 Incremental Cash Flow: 1.1 Incremental cash flow is considered an important

factor for developing the new project by the company as it provides additional cash

flow acquired by the company [4]. In other words, Incremental Cash Flow provides

the cash flow received by the company in the future with acceptance of new projects

[5].

The financial manager makes a decision upon acceptance or rejection of a

particular project based on incremental cash flow since it relies on the profitability of

investors. As incremental cash flow involved in cash inflows and cash outflows for a

specified period in the project. Usually, incremental cash flow is estimated based on

the net present value (NPV) with consideration of NPV financial manager either

accept or reject the project based on the following decision into consideration:

If NPV > 0 ; then the project is accepted which leads to profitability

If NPV < 0 ; then the project is not accepted which does not provides adequate

profitability to investors.

Q 1.2 Operating Cash Flow: Operating Cash Flow provides information about the

amount of cash utilized by the company for normal/main operation [6]. It provides

CAPITAL BUDGETING AND PROJECT EVALUATION

1. Introduction

In any organization, project analysis is considered an important factor involved in

the evaluation of project investment. Based on the project analysis companies able to

decide reasonably and comprehensively [1]. In this scenario, capital budgeting is

considered as the major factor for the evaluation of projects and investments with the

estimation of metrics involved in the project. Capital budgeting is a set of processes

involved in the analysis of cash inflow and cash outflow for the determination of

expected returns in the project [2]. Based on capital budgeting companies decides the

acceptance/rejection of a particular project. This provides a systematic evaluation of

the project about the resources and goals of the organization involved in the project

[3]. This report about information about capital budgeting and project evaluation.

Further, this report provides the scenario analysis of the production unit through

sensitivity analysis in terms of the best and worst cases. Finally, the overall

implication of research concerning the production industry is provided.

2. Part 1 - Capital budgeting

Q 1.1 Incremental Cash Flow: 1.1 Incremental cash flow is considered an important

factor for developing the new project by the company as it provides additional cash

flow acquired by the company [4]. In other words, Incremental Cash Flow provides

the cash flow received by the company in the future with acceptance of new projects

[5].

The financial manager makes a decision upon acceptance or rejection of a

particular project based on incremental cash flow since it relies on the profitability of

investors. As incremental cash flow involved in cash inflows and cash outflows for a

specified period in the project. Usually, incremental cash flow is estimated based on

the net present value (NPV) with consideration of NPV financial manager either

accept or reject the project based on the following decision into consideration:

If NPV > 0 ; then the project is accepted which leads to profitability

If NPV < 0 ; then the project is not accepted which does not provides adequate

profitability to investors.

Q 1.2 Operating Cash Flow: Operating Cash Flow provides information about the

amount of cash utilized by the company for normal/main operation [6]. It provides

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2

information about the utility of cash at regular intervals of time for the particular

project. For investment project, the operating cash flow is calculated using equation

(1):

Operating Cash Flow = Operating Income + Depreciation – Taxes + Change in

Working Capital (1)

Annual Free Cash Flow: Usually, Free Cash Flow is defined as the amount of fund

left with the company after utilization of funds for operating expenses and capital

expenditures [7].

Q 1.3 a) Depreciation Expenses: Depreciation Expenses are purchased long-term

assets instead of including in accounting period included in capital factor [8].

In this, depreciation expenses do not have a direct impact on annual free cash flow but

indirectly impact on liabilities of tax. In the case of the investment project, annual free

cash flow is calculated using equation (2)

Annual Free Cash Flow = Net Income + Non -Cash expenses - Increase in Working

Capital - Capital Expenditure (2)

Usually, investment project assets are considered as an economic factor and generate

accounting period and overstate expenses are utilized for the future accounting period.

To overcome this limitation, depreciation expenses are utilized on investment project

for the generation of revenues.

Depreciation Methods are categorized in to three scenarios such as [9]:

1. Straight - line

2. Accelerated

3. Units of Production

Straight line depreciation is calculated using equation (3)

Depreciation = (Fair Value - Residual Value)/ Life of Asset (3)

Accelerated depreciation is calculated using equation (4)

Depreciation = Initial Value of Asset* Factor/Useful Life (4)

Units of Production is calculated using equation (5)

Depreciation = (Fair Value - Residual Value)/ Useful Life (5)

information about the utility of cash at regular intervals of time for the particular

project. For investment project, the operating cash flow is calculated using equation

(1):

Operating Cash Flow = Operating Income + Depreciation – Taxes + Change in

Working Capital (1)

Annual Free Cash Flow: Usually, Free Cash Flow is defined as the amount of fund

left with the company after utilization of funds for operating expenses and capital

expenditures [7].

Q 1.3 a) Depreciation Expenses: Depreciation Expenses are purchased long-term

assets instead of including in accounting period included in capital factor [8].

In this, depreciation expenses do not have a direct impact on annual free cash flow but

indirectly impact on liabilities of tax. In the case of the investment project, annual free

cash flow is calculated using equation (2)

Annual Free Cash Flow = Net Income + Non -Cash expenses - Increase in Working

Capital - Capital Expenditure (2)

Usually, investment project assets are considered as an economic factor and generate

accounting period and overstate expenses are utilized for the future accounting period.

To overcome this limitation, depreciation expenses are utilized on investment project

for the generation of revenues.

Depreciation Methods are categorized in to three scenarios such as [9]:

1. Straight - line

2. Accelerated

3. Units of Production

Straight line depreciation is calculated using equation (3)

Depreciation = (Fair Value - Residual Value)/ Life of Asset (3)

Accelerated depreciation is calculated using equation (4)

Depreciation = Initial Value of Asset* Factor/Useful Life (4)

Units of Production is calculated using equation (5)

Depreciation = (Fair Value - Residual Value)/ Useful Life (5)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3

Q 1.3 b) Working Capital: Change in working capital of the firm reflects the cash

flow statement of the company about the project focused. In the cash flow statement

change in working capital is estimated based on the following equation (6)

Working Capital = Previous Working Capital - Present Working Capital (6)

Where, Working capital is computed as Working Capital = Present Operational Assets

- Present Operational Liabilities

Q 1.3 b) Residual Value: It provides the salvage value of the asset deployed with the

owner received for asset value. Also, this can be stated as an asset can be estimated

based on the amount obtained for future profitability of the company.

3. Part 2: Risk Analysis and Project Evaluation

In second part details of project is presented and asked to perform cash flow,

sensitivity analysis and scenario analysis. The analysis is conducted under two parts

such as cash flow estimation and scenario analysis. In this section general information

are presented.

Given

Initial Investment/Cost of Asset = $2500000

Selling Average Price = $30/unit

Residual Value = $400,000 for 4 years

Selling Unit = 250,000/year

Variable Cost = $10/unit

Fixed Cost = $250000/year

Depreciation method: straight line

Discount rate: 15%

Tax Rate: 30%

Solution

3.1 Scenario Analysis with Cash Flow:

Initially, cash flow analysis is asked to perform for estimation of project

investment. Usually, cash flow is a major factor to estimate the functioning of the

project which is based on consideration of cash in and cash out for effective

functioning of the particular project.

Q 1.3 b) Working Capital: Change in working capital of the firm reflects the cash

flow statement of the company about the project focused. In the cash flow statement

change in working capital is estimated based on the following equation (6)

Working Capital = Previous Working Capital - Present Working Capital (6)

Where, Working capital is computed as Working Capital = Present Operational Assets

- Present Operational Liabilities

Q 1.3 b) Residual Value: It provides the salvage value of the asset deployed with the

owner received for asset value. Also, this can be stated as an asset can be estimated

based on the amount obtained for future profitability of the company.

3. Part 2: Risk Analysis and Project Evaluation

In second part details of project is presented and asked to perform cash flow,

sensitivity analysis and scenario analysis. The analysis is conducted under two parts

such as cash flow estimation and scenario analysis. In this section general information

are presented.

Given

Initial Investment/Cost of Asset = $2500000

Selling Average Price = $30/unit

Residual Value = $400,000 for 4 years

Selling Unit = 250,000/year

Variable Cost = $10/unit

Fixed Cost = $250000/year

Depreciation method: straight line

Discount rate: 15%

Tax Rate: 30%

Solution

3.1 Scenario Analysis with Cash Flow:

Initially, cash flow analysis is asked to perform for estimation of project

investment. Usually, cash flow is a major factor to estimate the functioning of the

project which is based on consideration of cash in and cash out for effective

functioning of the particular project.

4

Cost of asset = $2500,000

Residual value = $400,000

Life of Asset = 4 years

Depreciation Cost = Cost of Asset - Residual Value/Life of Asset

Depreciation cost = (2500,000 - 400,000)/4

Depreciation Cost = $525,000

For the given values depreciation cost is estimated for 4 years with consideration

of residual value and cost of asset as $2500,000. Based on estimation depreciation

cost is calculated as $525,000.

3.2 Sensitivity of the project

Sensitivity analysis of project provides the risk assessment with estimation

changes associated with specific variables in the model. In the present case, for the

given production project three cases are derived those are stated as follows:

1. Base Case

2. Best Case

3. Worst Case

3.2.1 Case 1: Base Case

To conduct scenario analysis at first base cases are evaluated for analysis those

are presented as follows. Based on the estimated base values best and worst cases are

estimated for analysis.

Average Sales prices per unit = 30

Variable Cost per unit = 10

Fixed Cost per year = 250000

Target Profit = 400000

For the given scenario, sales is estimated based on consideration of fixed cost and

average price. The calculation is presented in equation (7) as follows:

Sales = Sells unit x Average Price (7)

Sales = 250000 x 30 = $7,500,000

The variable cost of project is calculated using equation (8) as follows:

Variable Cost = Sales x Variable Cost (8)

Variable Cost = 250000 x 10 = 2500000

Cost of asset = $2500,000

Residual value = $400,000

Life of Asset = 4 years

Depreciation Cost = Cost of Asset - Residual Value/Life of Asset

Depreciation cost = (2500,000 - 400,000)/4

Depreciation Cost = $525,000

For the given values depreciation cost is estimated for 4 years with consideration

of residual value and cost of asset as $2500,000. Based on estimation depreciation

cost is calculated as $525,000.

3.2 Sensitivity of the project

Sensitivity analysis of project provides the risk assessment with estimation

changes associated with specific variables in the model. In the present case, for the

given production project three cases are derived those are stated as follows:

1. Base Case

2. Best Case

3. Worst Case

3.2.1 Case 1: Base Case

To conduct scenario analysis at first base cases are evaluated for analysis those

are presented as follows. Based on the estimated base values best and worst cases are

estimated for analysis.

Average Sales prices per unit = 30

Variable Cost per unit = 10

Fixed Cost per year = 250000

Target Profit = 400000

For the given scenario, sales is estimated based on consideration of fixed cost and

average price. The calculation is presented in equation (7) as follows:

Sales = Sells unit x Average Price (7)

Sales = 250000 x 30 = $7,500,000

The variable cost of project is calculated using equation (8) as follows:

Variable Cost = Sales x Variable Cost (8)

Variable Cost = 250000 x 10 = 2500000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5

In the given scenario tax is considered hence earning before tax is computed

using equation (9)

Earning Before Tax = Sales - Total Variable Cost - Fixed Cost-Depreciation Cost

(9)

Earning Before Tax = $ 7,500,000 - $2500000 - $250000 - $525,000 = $ 4,225,000

Tax expenses are calculated using equation (10)

Tax Expenses = Earning Before Tax - Tax Rate (10)

Tax Expenses = $4,225,000 x 30% = $1,425,000

Net Income is calculated using equation (11)

Net Income = Earning before tax - Tax Expenses (11)

Net income = $ 4,225,000 - $1,267,000 = $2,957,000

Net cash flow = Net Income +Depreciation Expenses - Change in Working Capital =

$3,325,000 + $525,000 - $ 250,000 = $3,232,000

Discounted Net Cash Flow (DNCF) = $3,232,000/(1+0.15)1+$3,232,000/(1+0.15)2+

$3,232,000/(1+0.15)3+$3,232,000/(1+0.15)4 = $3,347,826.09

Baseline NPV = $3,347,826.09 - $2500000 = $6728,547

Based on the baseline value best and worst cases are computed for the project

flow is evaluated.

3.2.2 Case 2: Worst Case

The worst-case scenario analysis provides the information about project flow is

not as per the goal of the organization. For the given task, the worst case

scenario Unit sales decrease by 10%, and Price per unit decreases by 10%.

Average unit Sales price = 250000

Price per unit = $30

10% decrease in unit sale = 250000 - 25000 = $247,000

Sale = $247,000 x $30 = $247,500

In table 1 worst case scenario 10% reduction in price sales is presented.

Table 1: Worst Case Scenario for 10% decrease in sales

Base Case 10% decrease in

sales per unit

Sales $7,500,000 $7,425,000

Total Variable Cost $ 2500000 $247,5000

Earning before tax $4,225,000 $4175000

Tax Expenses $1,267,000 $1,252,500

Net Income $2,957,000 $2,922,500

Net Cash Flow $3,232,000 $3197500

In the given scenario tax is considered hence earning before tax is computed

using equation (9)

Earning Before Tax = Sales - Total Variable Cost - Fixed Cost-Depreciation Cost

(9)

Earning Before Tax = $ 7,500,000 - $2500000 - $250000 - $525,000 = $ 4,225,000

Tax expenses are calculated using equation (10)

Tax Expenses = Earning Before Tax - Tax Rate (10)

Tax Expenses = $4,225,000 x 30% = $1,425,000

Net Income is calculated using equation (11)

Net Income = Earning before tax - Tax Expenses (11)

Net income = $ 4,225,000 - $1,267,000 = $2,957,000

Net cash flow = Net Income +Depreciation Expenses - Change in Working Capital =

$3,325,000 + $525,000 - $ 250,000 = $3,232,000

Discounted Net Cash Flow (DNCF) = $3,232,000/(1+0.15)1+$3,232,000/(1+0.15)2+

$3,232,000/(1+0.15)3+$3,232,000/(1+0.15)4 = $3,347,826.09

Baseline NPV = $3,347,826.09 - $2500000 = $6728,547

Based on the baseline value best and worst cases are computed for the project

flow is evaluated.

3.2.2 Case 2: Worst Case

The worst-case scenario analysis provides the information about project flow is

not as per the goal of the organization. For the given task, the worst case

scenario Unit sales decrease by 10%, and Price per unit decreases by 10%.

Average unit Sales price = 250000

Price per unit = $30

10% decrease in unit sale = 250000 - 25000 = $247,000

Sale = $247,000 x $30 = $247,500

In table 1 worst case scenario 10% reduction in price sales is presented.

Table 1: Worst Case Scenario for 10% decrease in sales

Base Case 10% decrease in

sales per unit

Sales $7,500,000 $7,425,000

Total Variable Cost $ 2500000 $247,5000

Earning before tax $4,225,000 $4175000

Tax Expenses $1,267,000 $1,252,500

Net Income $2,957,000 $2,922,500

Net Cash Flow $3,232,000 $3197500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

Discounted Net

Cash Flow

(DNCF)

$9228547 $9133542

Baseline NPV $6728,547 $6,633542

Sensitivity % 35%

In the above table 1 comparison of 10% decrease in sales of the project is

comparatively presented with baseline value. In worst case scenario DNCF is

observed as $9133542 which is significantly minimal than baseline value. This

implies that competitor project is effective and sales of the project is significantly

reduced. The observed sensitivity is estimated as 35% for 4 years. In table 2 10% in

price unit is presented for worst case

Table 2: Worst Case Scenario for 10% decrease in price per unit

Base Case 10% decrease in

price per unit

Sales $7,500,000 $6,750,000

Total Variable Cost $ 2500000 $2500000

Earning before tax $4,225,000 -$525000

Tax Expenses $1,267,000 -$157,500

Net Income $2,957,000 -$682,500

Net Cash Flow $3,232,000 -$407,500

Discounted Net

Cash Flow

(DNCF)

$9228547 -$1164008

Baseline NPV for 1

year

$6728,547 -$3664008

Sensitivity % -15%

The worst case analysis of project flow in comparison with competitor 10%

reduction in price contribute effective sensitivity value. The analysis illustrated that

DNCF is significantly higher than that of baseline value as it is observed as -

$1164008. Similarly the sensitivity analysis for 4 year NPV is observed as -15% for 4

years.

3.1.3 Case 3: Best Case

Discounted Net

Cash Flow

(DNCF)

$9228547 $9133542

Baseline NPV $6728,547 $6,633542

Sensitivity % 35%

In the above table 1 comparison of 10% decrease in sales of the project is

comparatively presented with baseline value. In worst case scenario DNCF is

observed as $9133542 which is significantly minimal than baseline value. This

implies that competitor project is effective and sales of the project is significantly

reduced. The observed sensitivity is estimated as 35% for 4 years. In table 2 10% in

price unit is presented for worst case

Table 2: Worst Case Scenario for 10% decrease in price per unit

Base Case 10% decrease in

price per unit

Sales $7,500,000 $6,750,000

Total Variable Cost $ 2500000 $2500000

Earning before tax $4,225,000 -$525000

Tax Expenses $1,267,000 -$157,500

Net Income $2,957,000 -$682,500

Net Cash Flow $3,232,000 -$407,500

Discounted Net

Cash Flow

(DNCF)

$9228547 -$1164008

Baseline NPV for 1

year

$6728,547 -$3664008

Sensitivity % -15%

The worst case analysis of project flow in comparison with competitor 10%

reduction in price contribute effective sensitivity value. The analysis illustrated that

DNCF is significantly higher than that of baseline value as it is observed as -

$1164008. Similarly the sensitivity analysis for 4 year NPV is observed as -15% for 4

years.

3.1.3 Case 3: Best Case

7

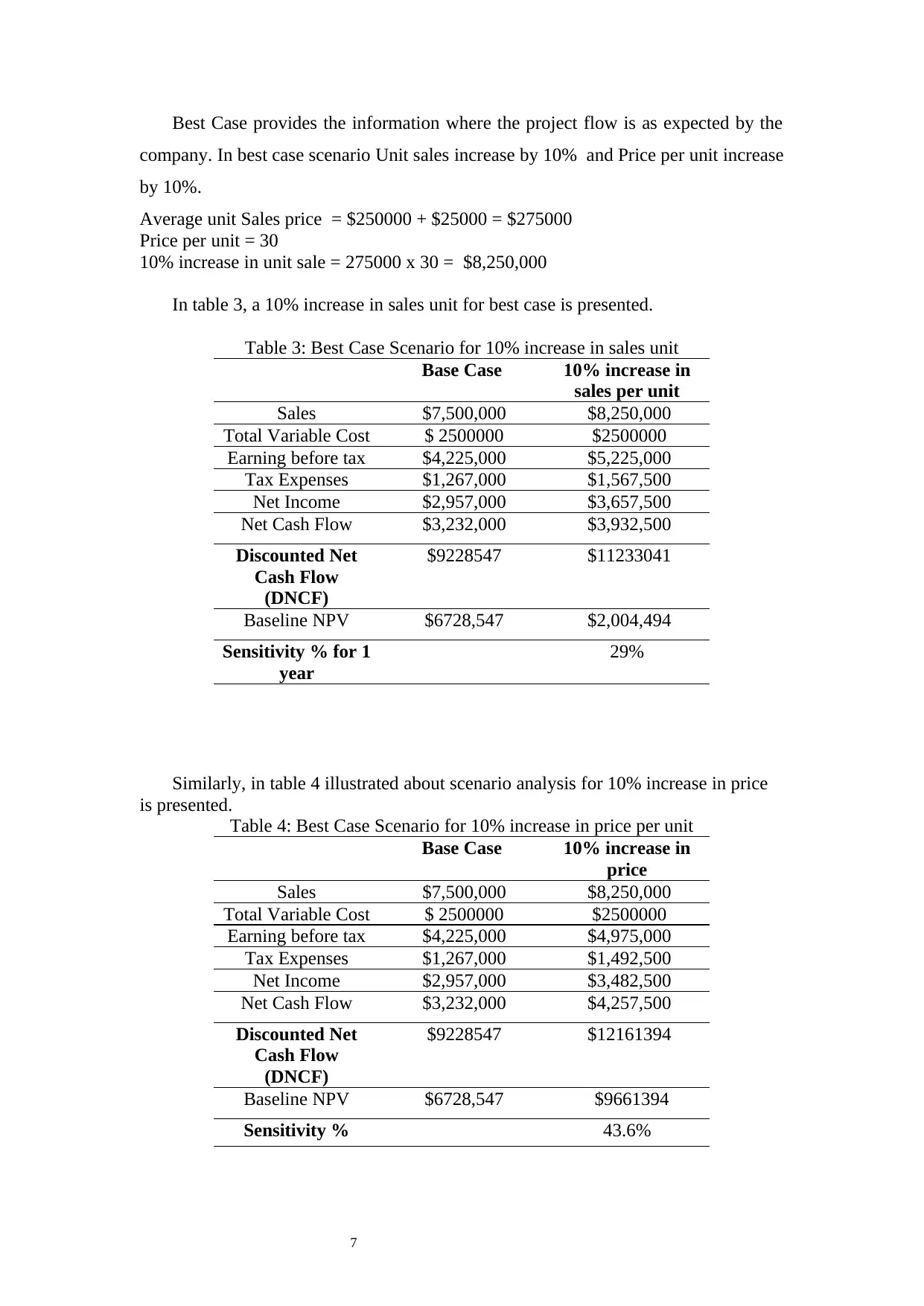

Best Case provides the information where the project flow is as expected by the

company. In best case scenario Unit sales increase by 10% and Price per unit increase

by 10%.

Average unit Sales price = $250000 + $25000 = $275000

Price per unit = 30

10% increase in unit sale = 275000 x 30 = $8,250,000

In table 3, a 10% increase in sales unit for best case is presented.

Table 3: Best Case Scenario for 10% increase in sales unit

Base Case 10% increase in

sales per unit

Sales $7,500,000 $8,250,000

Total Variable Cost $ 2500000 $2500000

Earning before tax $4,225,000 $5,225,000

Tax Expenses $1,267,000 $1,567,500

Net Income $2,957,000 $3,657,500

Net Cash Flow $3,232,000 $3,932,500

Discounted Net

Cash Flow

(DNCF)

$9228547 $11233041

Baseline NPV $6728,547 $2,004,494

Sensitivity % for 1

year

29%

Similarly, in table 4 illustrated about scenario analysis for 10% increase in price

is presented.

Table 4: Best Case Scenario for 10% increase in price per unit

Base Case 10% increase in

price

Sales $7,500,000 $8,250,000

Total Variable Cost $ 2500000 $2500000

Earning before tax $4,225,000 $4,975,000

Tax Expenses $1,267,000 $1,492,500

Net Income $2,957,000 $3,482,500

Net Cash Flow $3,232,000 $4,257,500

Discounted Net

Cash Flow

(DNCF)

$9228547 $12161394

Baseline NPV $6728,547 $9661394

Sensitivity % 43.6%

Best Case provides the information where the project flow is as expected by the

company. In best case scenario Unit sales increase by 10% and Price per unit increase

by 10%.

Average unit Sales price = $250000 + $25000 = $275000

Price per unit = 30

10% increase in unit sale = 275000 x 30 = $8,250,000

In table 3, a 10% increase in sales unit for best case is presented.

Table 3: Best Case Scenario for 10% increase in sales unit

Base Case 10% increase in

sales per unit

Sales $7,500,000 $8,250,000

Total Variable Cost $ 2500000 $2500000

Earning before tax $4,225,000 $5,225,000

Tax Expenses $1,267,000 $1,567,500

Net Income $2,957,000 $3,657,500

Net Cash Flow $3,232,000 $3,932,500

Discounted Net

Cash Flow

(DNCF)

$9228547 $11233041

Baseline NPV $6728,547 $2,004,494

Sensitivity % for 1

year

29%

Similarly, in table 4 illustrated about scenario analysis for 10% increase in price

is presented.

Table 4: Best Case Scenario for 10% increase in price per unit

Base Case 10% increase in

price

Sales $7,500,000 $8,250,000

Total Variable Cost $ 2500000 $2500000

Earning before tax $4,225,000 $4,975,000

Tax Expenses $1,267,000 $1,492,500

Net Income $2,957,000 $3,482,500

Net Cash Flow $3,232,000 $4,257,500

Discounted Net

Cash Flow

(DNCF)

$9228547 $12161394

Baseline NPV $6728,547 $9661394

Sensitivity % 43.6%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

The analysis illustrated that best case provides increase in unit price by 10% leads to

significant DNCF value of $12161394 which is significantly higher than base value.

The best case scenario illustrated that increase in price of unit leads to effective

sensitivity value rate of 43.6%.

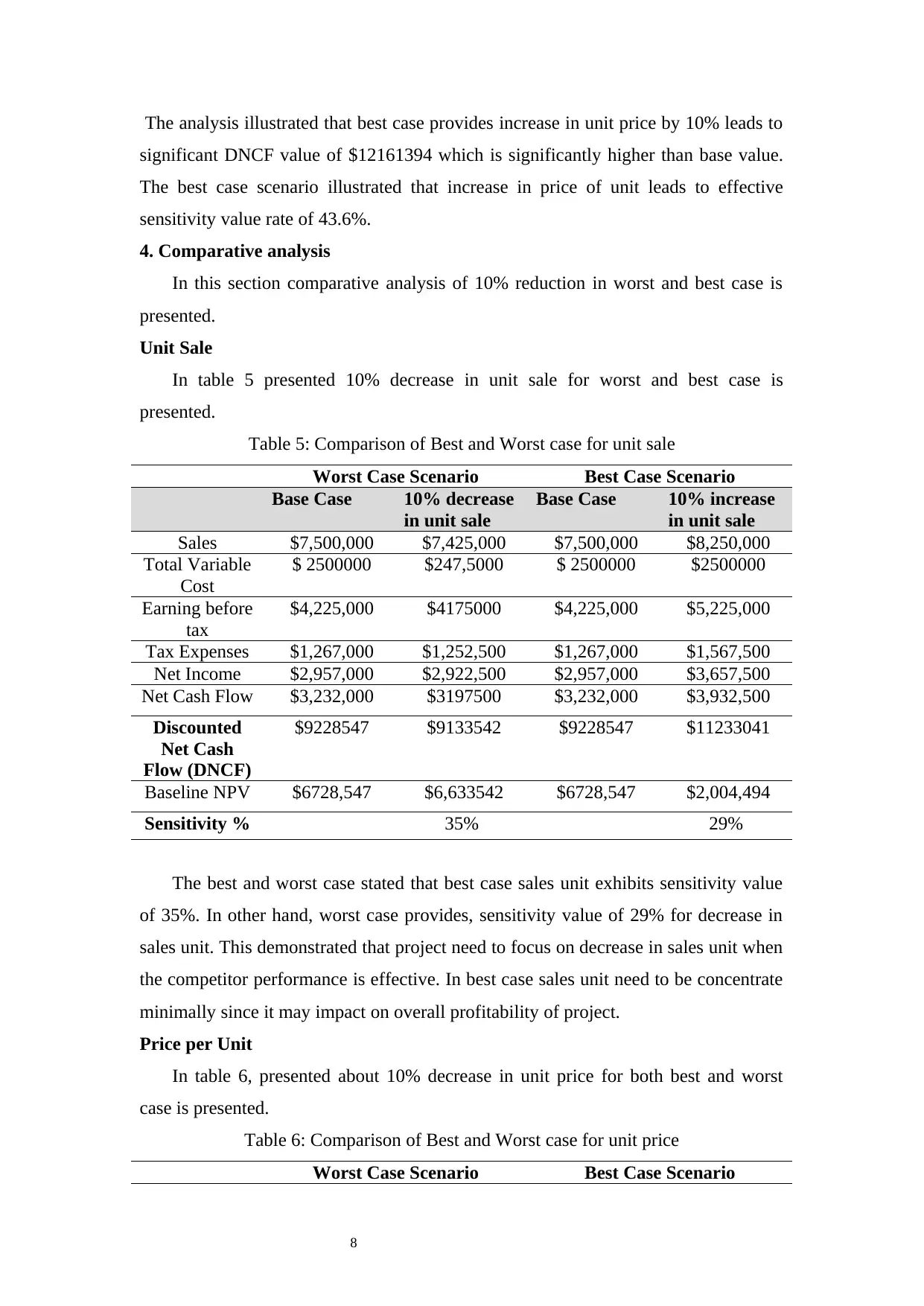

4. Comparative analysis

In this section comparative analysis of 10% reduction in worst and best case is

presented.

Unit Sale

In table 5 presented 10% decrease in unit sale for worst and best case is

presented.

Table 5: Comparison of Best and Worst case for unit sale

Worst Case Scenario Best Case Scenario

Base Case 10% decrease

in unit sale

Base Case 10% increase

in unit sale

Sales $7,500,000 $7,425,000 $7,500,000 $8,250,000

Total Variable

Cost

$ 2500000 $247,5000 $ 2500000 $2500000

Earning before

tax

$4,225,000 $4175000 $4,225,000 $5,225,000

Tax Expenses $1,267,000 $1,252,500 $1,267,000 $1,567,500

Net Income $2,957,000 $2,922,500 $2,957,000 $3,657,500

Net Cash Flow $3,232,000 $3197500 $3,232,000 $3,932,500

Discounted

Net Cash

Flow (DNCF)

$9228547 $9133542 $9228547 $11233041

Baseline NPV $6728,547 $6,633542 $6728,547 $2,004,494

Sensitivity % 35% 29%

The best and worst case stated that best case sales unit exhibits sensitivity value

of 35%. In other hand, worst case provides, sensitivity value of 29% for decrease in

sales unit. This demonstrated that project need to focus on decrease in sales unit when

the competitor performance is effective. In best case sales unit need to be concentrate

minimally since it may impact on overall profitability of project.

Price per Unit

In table 6, presented about 10% decrease in unit price for both best and worst

case is presented.

Table 6: Comparison of Best and Worst case for unit price

Worst Case Scenario Best Case Scenario

The analysis illustrated that best case provides increase in unit price by 10% leads to

significant DNCF value of $12161394 which is significantly higher than base value.

The best case scenario illustrated that increase in price of unit leads to effective

sensitivity value rate of 43.6%.

4. Comparative analysis

In this section comparative analysis of 10% reduction in worst and best case is

presented.

Unit Sale

In table 5 presented 10% decrease in unit sale for worst and best case is

presented.

Table 5: Comparison of Best and Worst case for unit sale

Worst Case Scenario Best Case Scenario

Base Case 10% decrease

in unit sale

Base Case 10% increase

in unit sale

Sales $7,500,000 $7,425,000 $7,500,000 $8,250,000

Total Variable

Cost

$ 2500000 $247,5000 $ 2500000 $2500000

Earning before

tax

$4,225,000 $4175000 $4,225,000 $5,225,000

Tax Expenses $1,267,000 $1,252,500 $1,267,000 $1,567,500

Net Income $2,957,000 $2,922,500 $2,957,000 $3,657,500

Net Cash Flow $3,232,000 $3197500 $3,232,000 $3,932,500

Discounted

Net Cash

Flow (DNCF)

$9228547 $9133542 $9228547 $11233041

Baseline NPV $6728,547 $6,633542 $6728,547 $2,004,494

Sensitivity % 35% 29%

The best and worst case stated that best case sales unit exhibits sensitivity value

of 35%. In other hand, worst case provides, sensitivity value of 29% for decrease in

sales unit. This demonstrated that project need to focus on decrease in sales unit when

the competitor performance is effective. In best case sales unit need to be concentrate

minimally since it may impact on overall profitability of project.

Price per Unit

In table 6, presented about 10% decrease in unit price for both best and worst

case is presented.

Table 6: Comparison of Best and Worst case for unit price

Worst Case Scenario Best Case Scenario

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

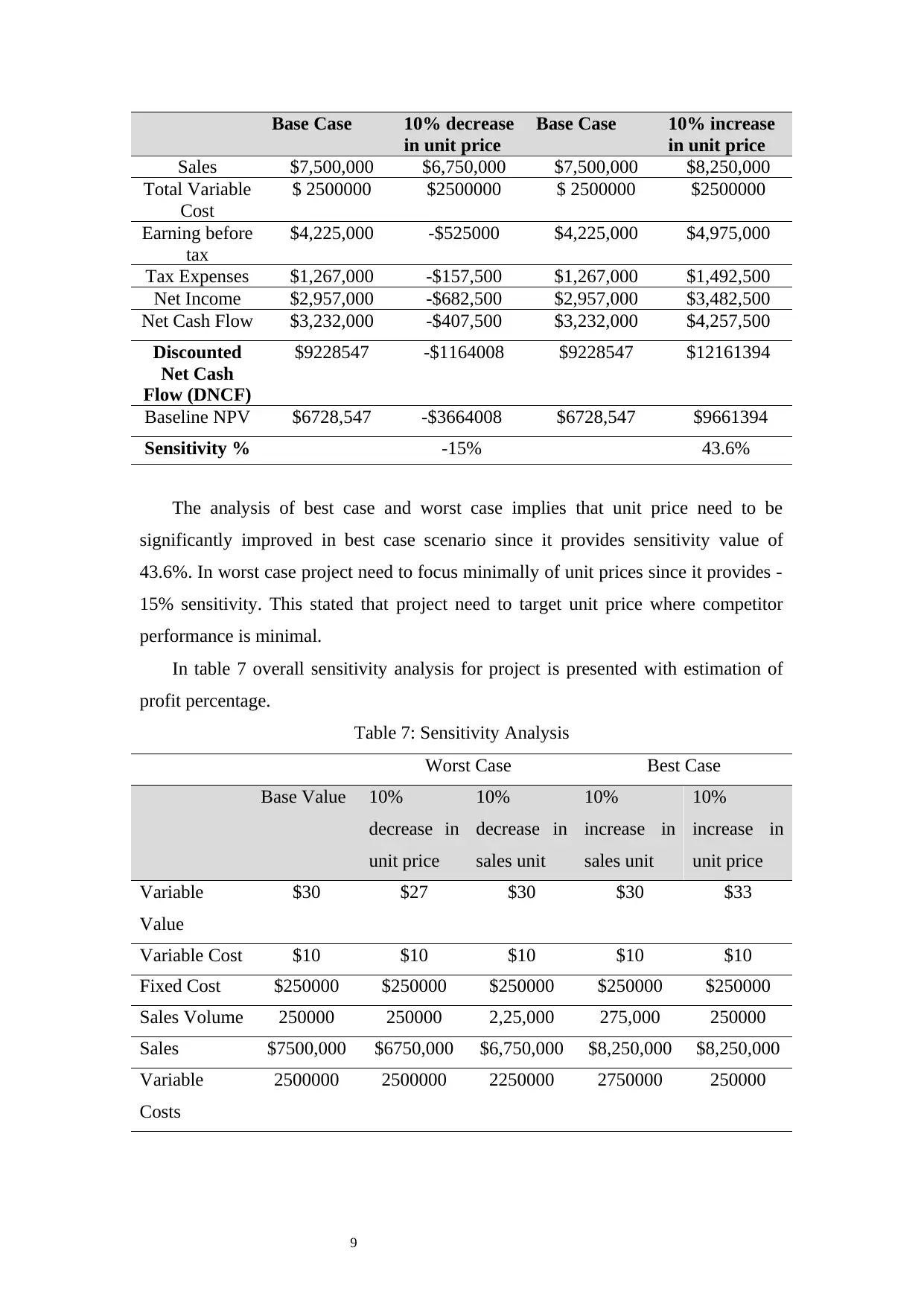

Base Case 10% decrease

in unit price

Base Case 10% increase

in unit price

Sales $7,500,000 $6,750,000 $7,500,000 $8,250,000

Total Variable

Cost

$ 2500000 $2500000 $ 2500000 $2500000

Earning before

tax

$4,225,000 -$525000 $4,225,000 $4,975,000

Tax Expenses $1,267,000 -$157,500 $1,267,000 $1,492,500

Net Income $2,957,000 -$682,500 $2,957,000 $3,482,500

Net Cash Flow $3,232,000 -$407,500 $3,232,000 $4,257,500

Discounted

Net Cash

Flow (DNCF)

$9228547 -$1164008 $9228547 $12161394

Baseline NPV $6728,547 -$3664008 $6728,547 $9661394

Sensitivity % -15% 43.6%

The analysis of best case and worst case implies that unit price need to be

significantly improved in best case scenario since it provides sensitivity value of

43.6%. In worst case project need to focus minimally of unit prices since it provides -

15% sensitivity. This stated that project need to target unit price where competitor

performance is minimal.

In table 7 overall sensitivity analysis for project is presented with estimation of

profit percentage.

Table 7: Sensitivity Analysis

Worst Case Best Case

Base Value 10%

decrease in

unit price

10%

decrease in

sales unit

10%

increase in

sales unit

10%

increase in

unit price

Variable

Value

$30 $27 $30 $30 $33

Variable Cost $10 $10 $10 $10 $10

Fixed Cost $250000 $250000 $250000 $250000 $250000

Sales Volume 250000 250000 2,25,000 275,000 250000

Sales $7500,000 $6750,000 $6,750,000 $8,250,000 $8,250,000

Variable

Costs

2500000 2500000 2250000 2750000 250000

Base Case 10% decrease

in unit price

Base Case 10% increase

in unit price

Sales $7,500,000 $6,750,000 $7,500,000 $8,250,000

Total Variable

Cost

$ 2500000 $2500000 $ 2500000 $2500000

Earning before

tax

$4,225,000 -$525000 $4,225,000 $4,975,000

Tax Expenses $1,267,000 -$157,500 $1,267,000 $1,492,500

Net Income $2,957,000 -$682,500 $2,957,000 $3,482,500

Net Cash Flow $3,232,000 -$407,500 $3,232,000 $4,257,500

Discounted

Net Cash

Flow (DNCF)

$9228547 -$1164008 $9228547 $12161394

Baseline NPV $6728,547 -$3664008 $6728,547 $9661394

Sensitivity % -15% 43.6%

The analysis of best case and worst case implies that unit price need to be

significantly improved in best case scenario since it provides sensitivity value of

43.6%. In worst case project need to focus minimally of unit prices since it provides -

15% sensitivity. This stated that project need to target unit price where competitor

performance is minimal.

In table 7 overall sensitivity analysis for project is presented with estimation of

profit percentage.

Table 7: Sensitivity Analysis

Worst Case Best Case

Base Value 10%

decrease in

unit price

10%

decrease in

sales unit

10%

increase in

sales unit

10%

increase in

unit price

Variable

Value

$30 $27 $30 $30 $33

Variable Cost $10 $10 $10 $10 $10

Fixed Cost $250000 $250000 $250000 $250000 $250000

Sales Volume 250000 250000 2,25,000 275,000 250000

Sales $7500,000 $6750,000 $6,750,000 $8,250,000 $8,250,000

Variable

Costs

2500000 2500000 2250000 2750000 250000

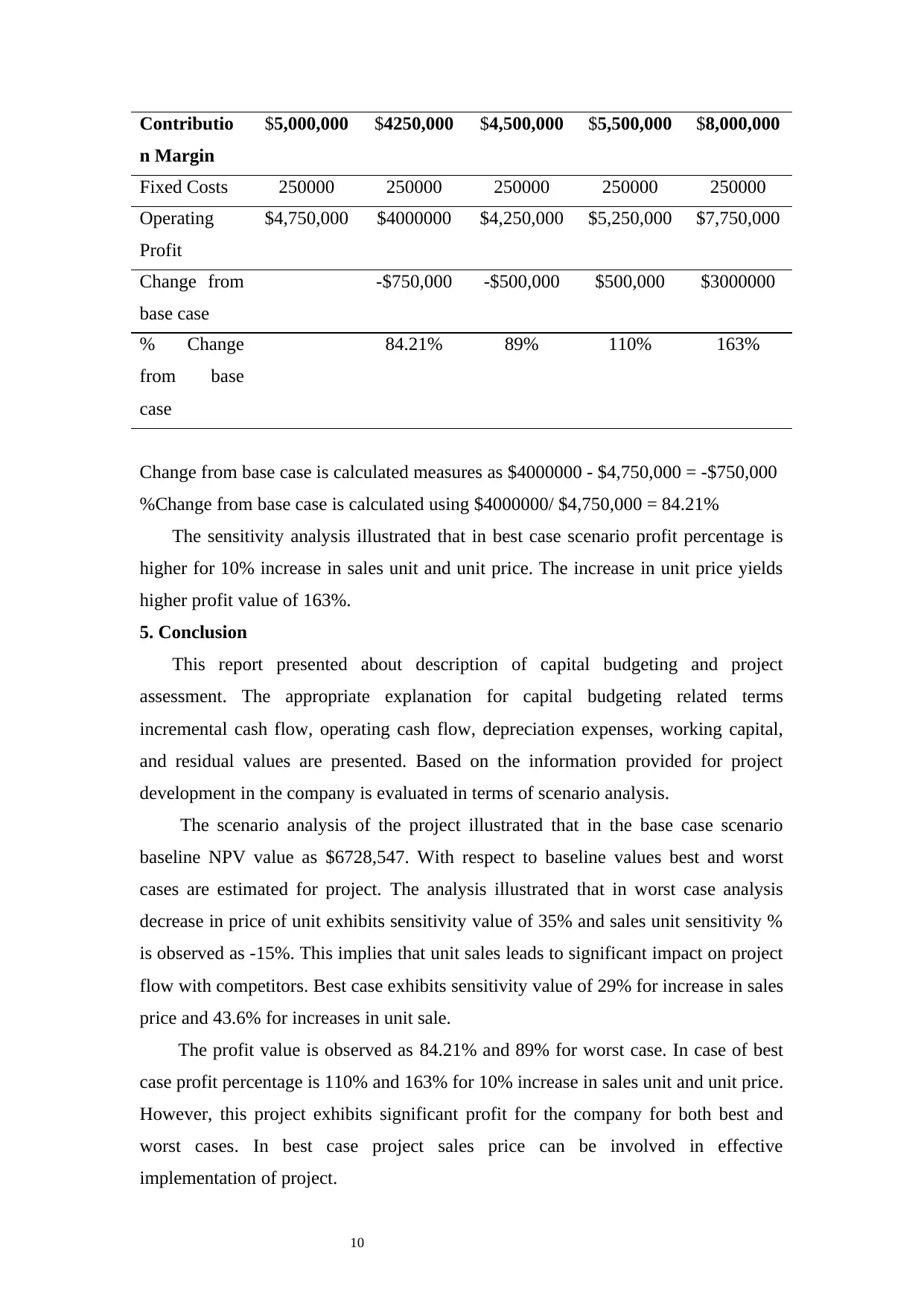

10

Contributio

n Margin

$5,000,000 $4250,000 $4,500,000 $5,500,000 $8,000,000

Fixed Costs 250000 250000 250000 250000 250000

Operating

Profit

$4,750,000 $4000000 $4,250,000 $5,250,000 $7,750,000

Change from

base case

-$750,000 -$500,000 $500,000 $3000000

% Change

from base

case

84.21% 89% 110% 163%

Change from base case is calculated measures as $4000000 - $4,750,000 = -$750,000

%Change from base case is calculated using $4000000/ $4,750,000 = 84.21%

The sensitivity analysis illustrated that in best case scenario profit percentage is

higher for 10% increase in sales unit and unit price. The increase in unit price yields

higher profit value of 163%.

5. Conclusion

This report presented about description of capital budgeting and project

assessment. The appropriate explanation for capital budgeting related terms

incremental cash flow, operating cash flow, depreciation expenses, working capital,

and residual values are presented. Based on the information provided for project

development in the company is evaluated in terms of scenario analysis.

The scenario analysis of the project illustrated that in the base case scenario

baseline NPV value as $6728,547. With respect to baseline values best and worst

cases are estimated for project. The analysis illustrated that in worst case analysis

decrease in price of unit exhibits sensitivity value of 35% and sales unit sensitivity %

is observed as -15%. This implies that unit sales leads to significant impact on project

flow with competitors. Best case exhibits sensitivity value of 29% for increase in sales

price and 43.6% for increases in unit sale.

The profit value is observed as 84.21% and 89% for worst case. In case of best

case profit percentage is 110% and 163% for 10% increase in sales unit and unit price.

However, this project exhibits significant profit for the company for both best and

worst cases. In best case project sales price can be involved in effective

implementation of project.

Contributio

n Margin

$5,000,000 $4250,000 $4,500,000 $5,500,000 $8,000,000

Fixed Costs 250000 250000 250000 250000 250000

Operating

Profit

$4,750,000 $4000000 $4,250,000 $5,250,000 $7,750,000

Change from

base case

-$750,000 -$500,000 $500,000 $3000000

% Change

from base

case

84.21% 89% 110% 163%

Change from base case is calculated measures as $4000000 - $4,750,000 = -$750,000

%Change from base case is calculated using $4000000/ $4,750,000 = 84.21%

The sensitivity analysis illustrated that in best case scenario profit percentage is

higher for 10% increase in sales unit and unit price. The increase in unit price yields

higher profit value of 163%.

5. Conclusion

This report presented about description of capital budgeting and project

assessment. The appropriate explanation for capital budgeting related terms

incremental cash flow, operating cash flow, depreciation expenses, working capital,

and residual values are presented. Based on the information provided for project

development in the company is evaluated in terms of scenario analysis.

The scenario analysis of the project illustrated that in the base case scenario

baseline NPV value as $6728,547. With respect to baseline values best and worst

cases are estimated for project. The analysis illustrated that in worst case analysis

decrease in price of unit exhibits sensitivity value of 35% and sales unit sensitivity %

is observed as -15%. This implies that unit sales leads to significant impact on project

flow with competitors. Best case exhibits sensitivity value of 29% for increase in sales

price and 43.6% for increases in unit sale.

The profit value is observed as 84.21% and 89% for worst case. In case of best

case profit percentage is 110% and 163% for 10% increase in sales unit and unit price.

However, this project exhibits significant profit for the company for both best and

worst cases. In best case project sales price can be involved in effective

implementation of project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.