Capital Project Evaluation: NPV, ARR, and Payback Analysis

VerifiedAdded on 2023/03/20

|4

|495

|32

Project

AI Summary

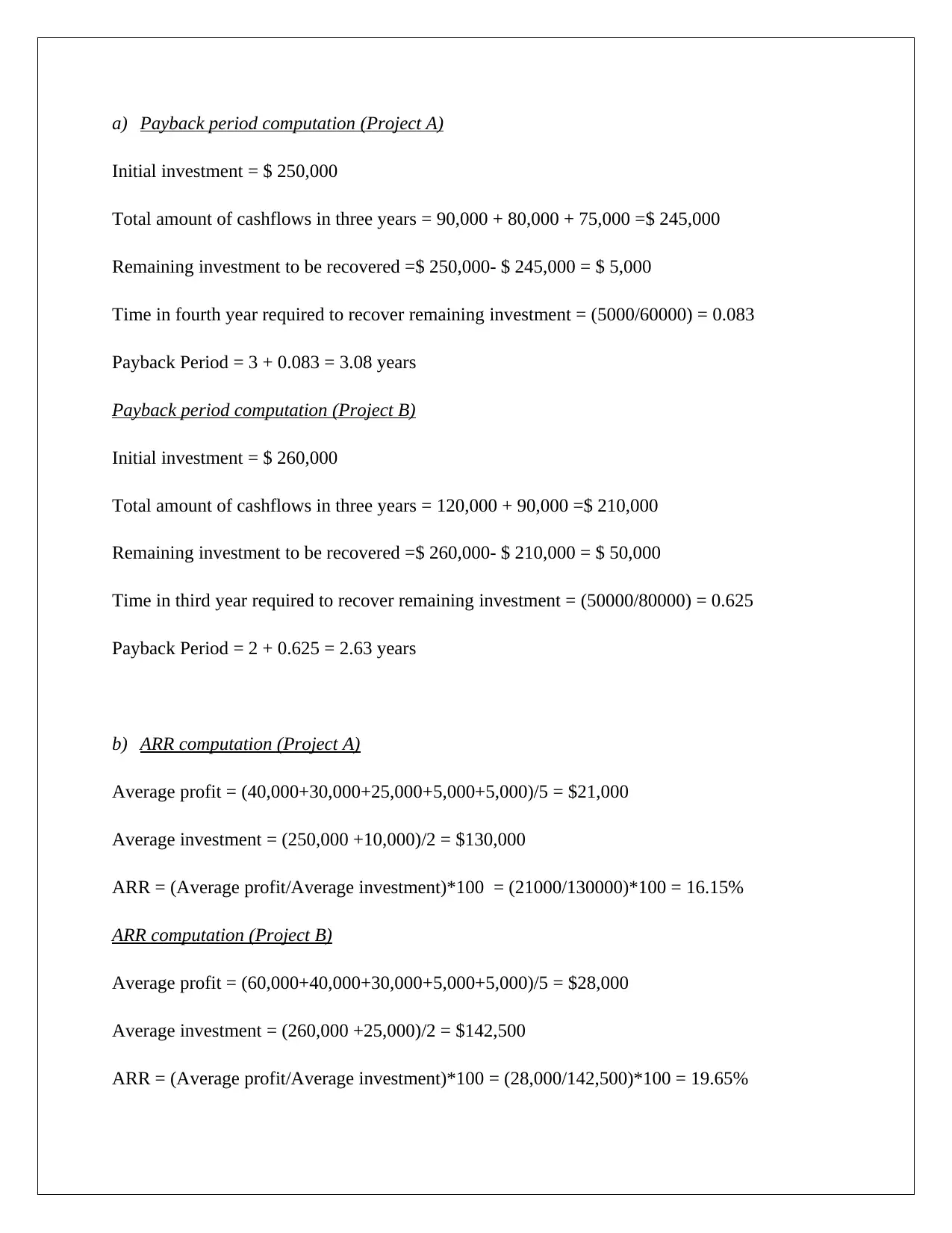

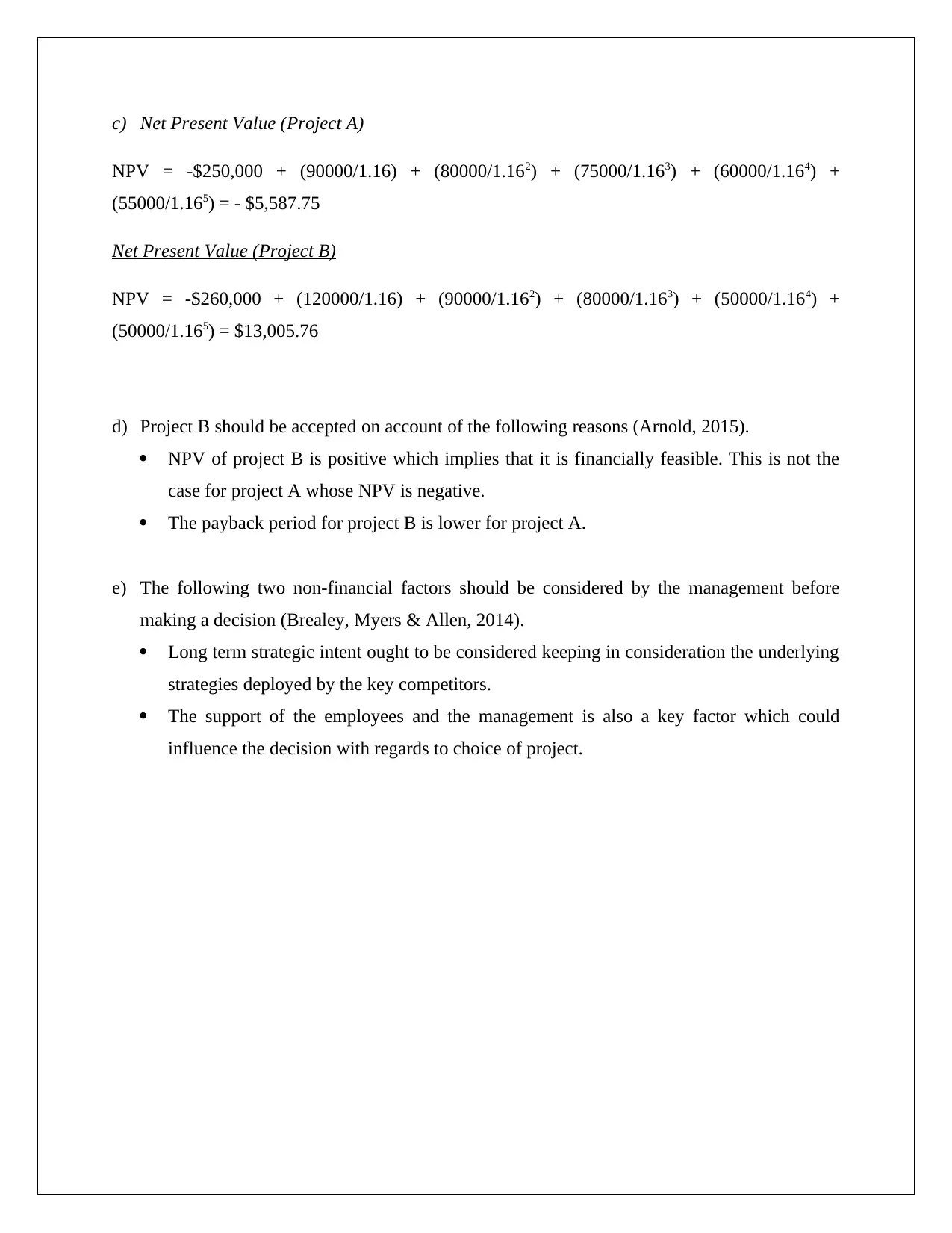

This finance project evaluates two capital projects (A and B) for Te Runanganui o Ngati Porou (TRNP). The analysis includes calculating the payback period, accounting rate of return (ARR), and net present value (NPV) for each project. The solution demonstrates the step-by-step calculations for each method, considering initial costs, cash inflows, profits, and the company's cost of capital (16%). The project concludes with a recommendation on which project to accept, supported by financial reasons, and also explores non-financial factors that management should consider before making a final decision, such as long-term strategic intent and employee support. References from Arnold (2015) and Brealey, Myers & Allen (2014) are included to support the analysis.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.