Financial Viability: Capital Budgeting and Ratio Analysis Methods

VerifiedAdded on 2023/06/18

|16

|2669

|105

Report

AI Summary

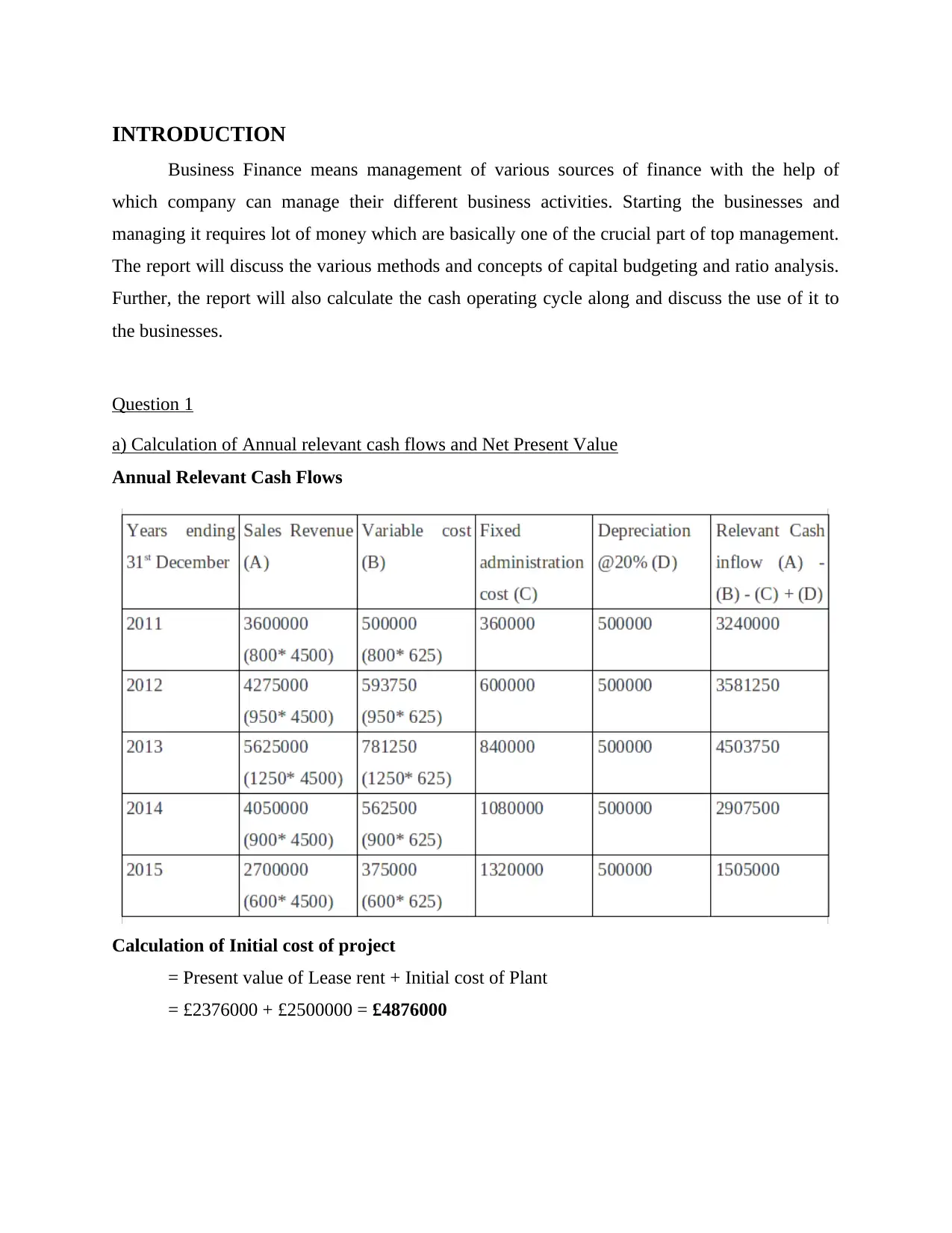

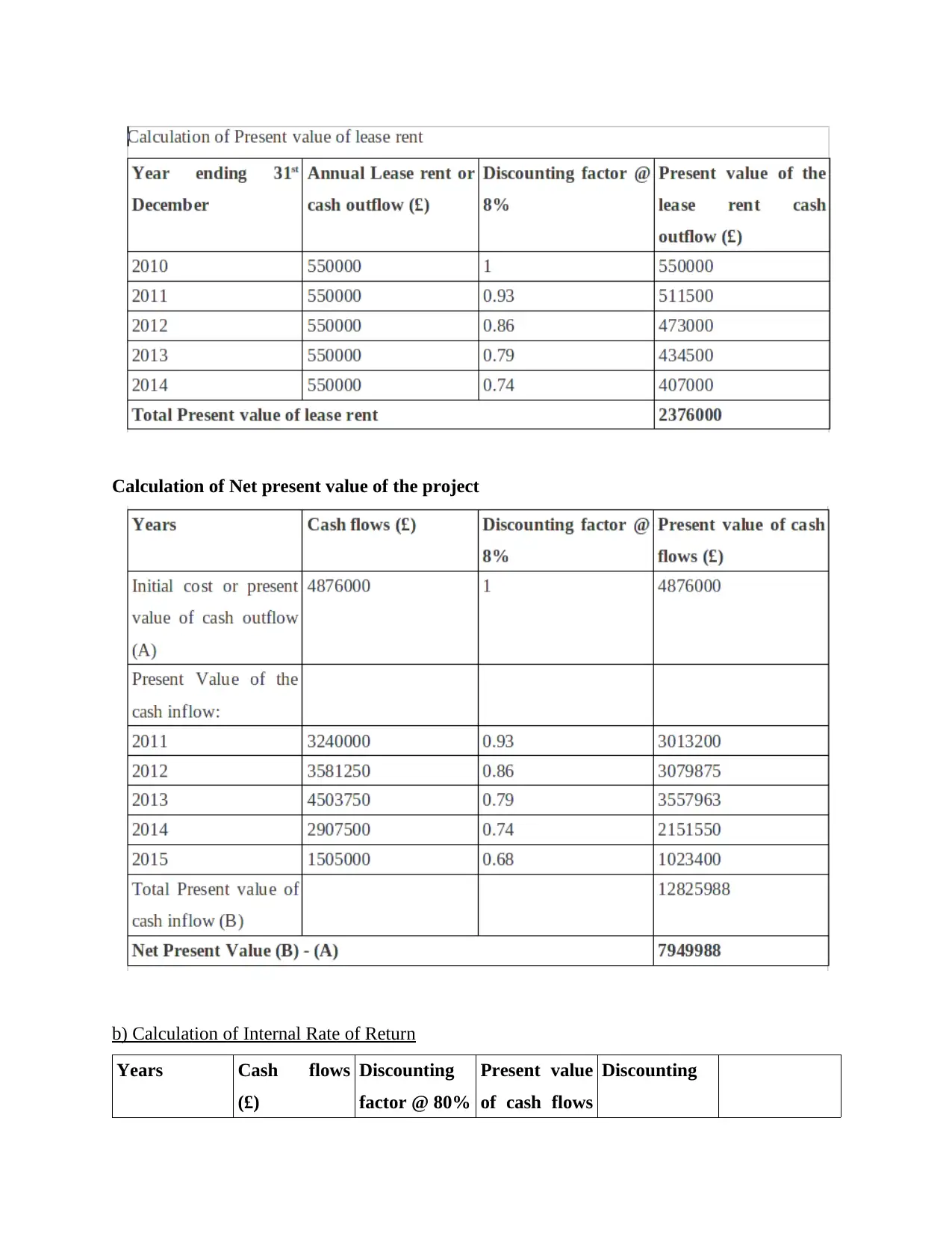

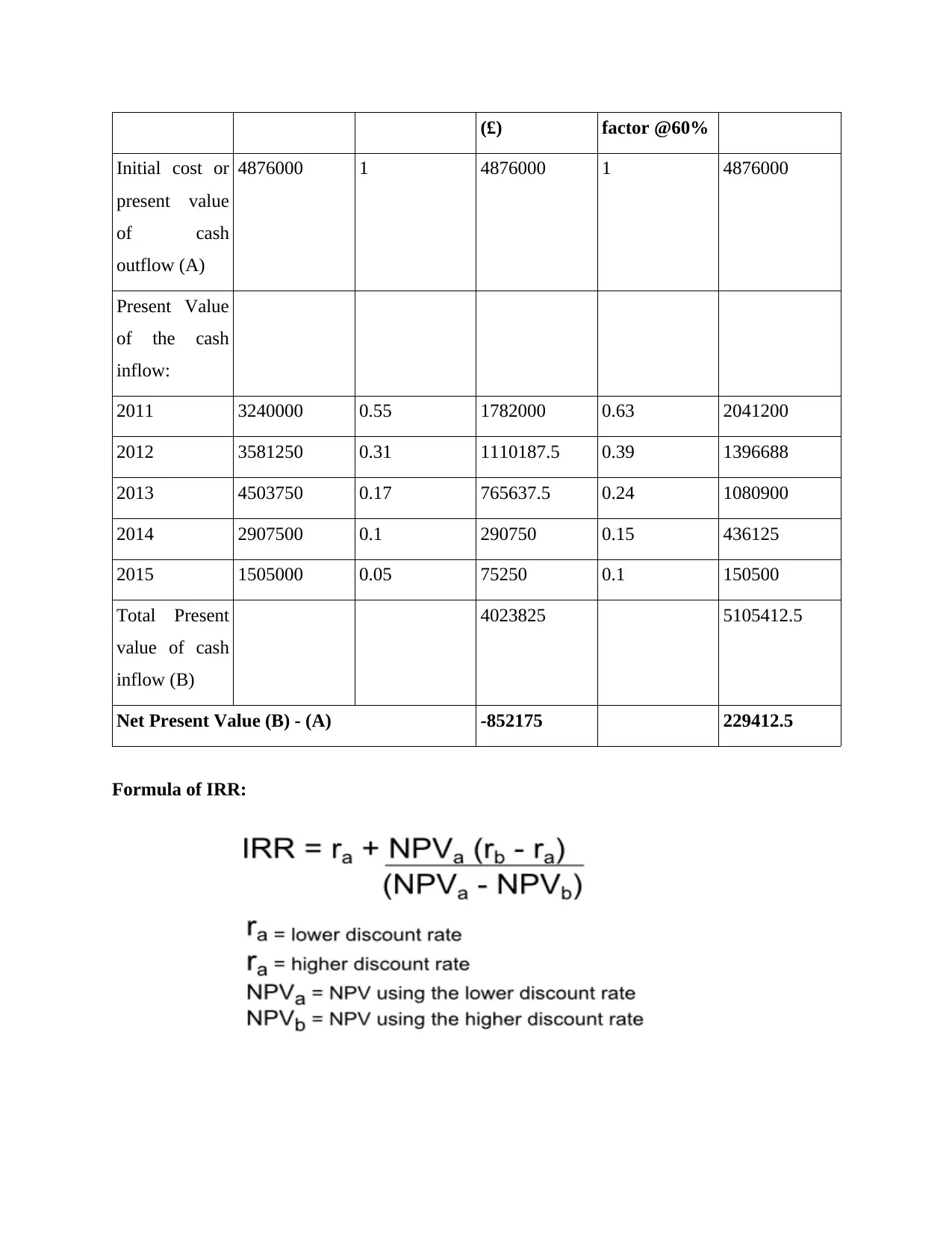

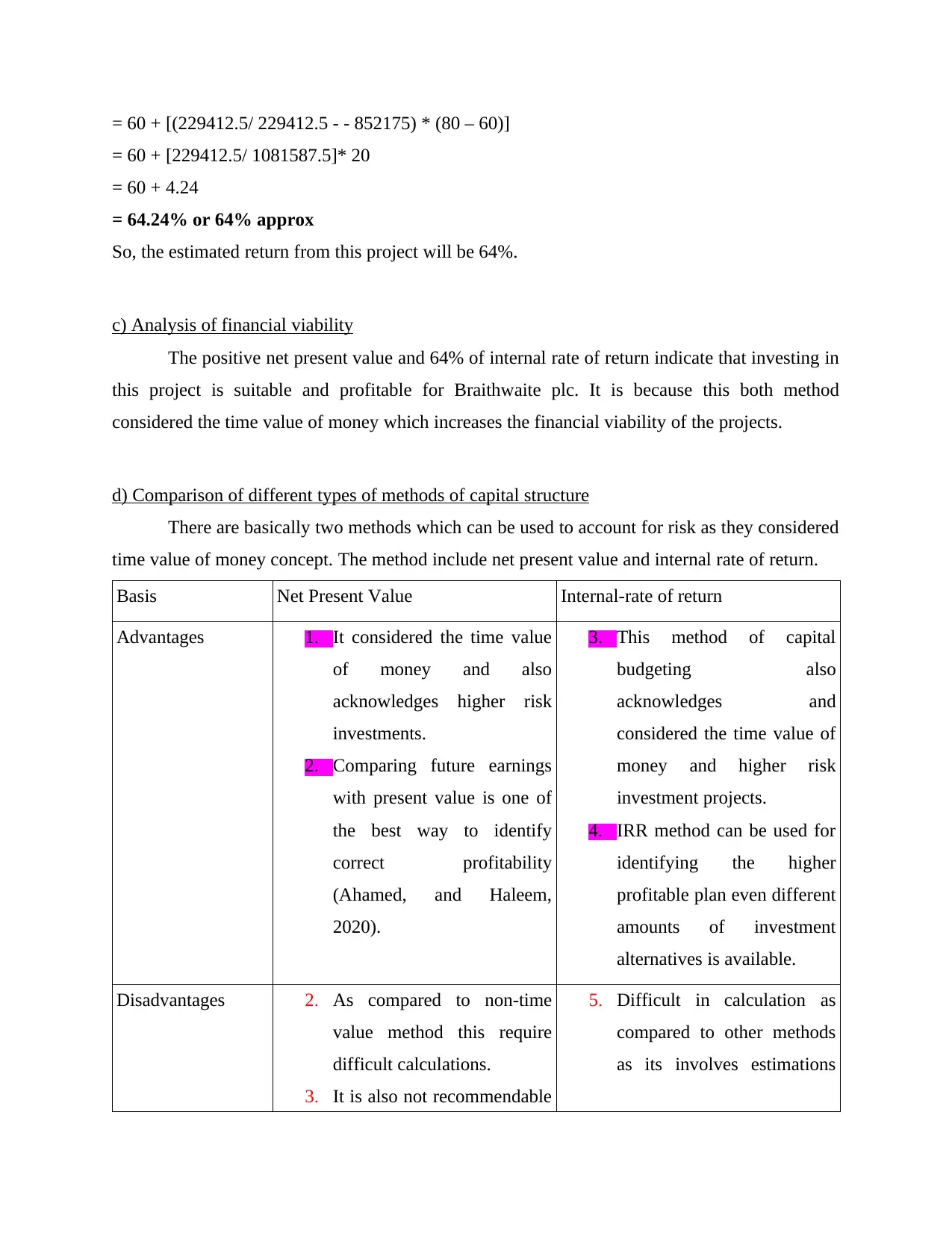

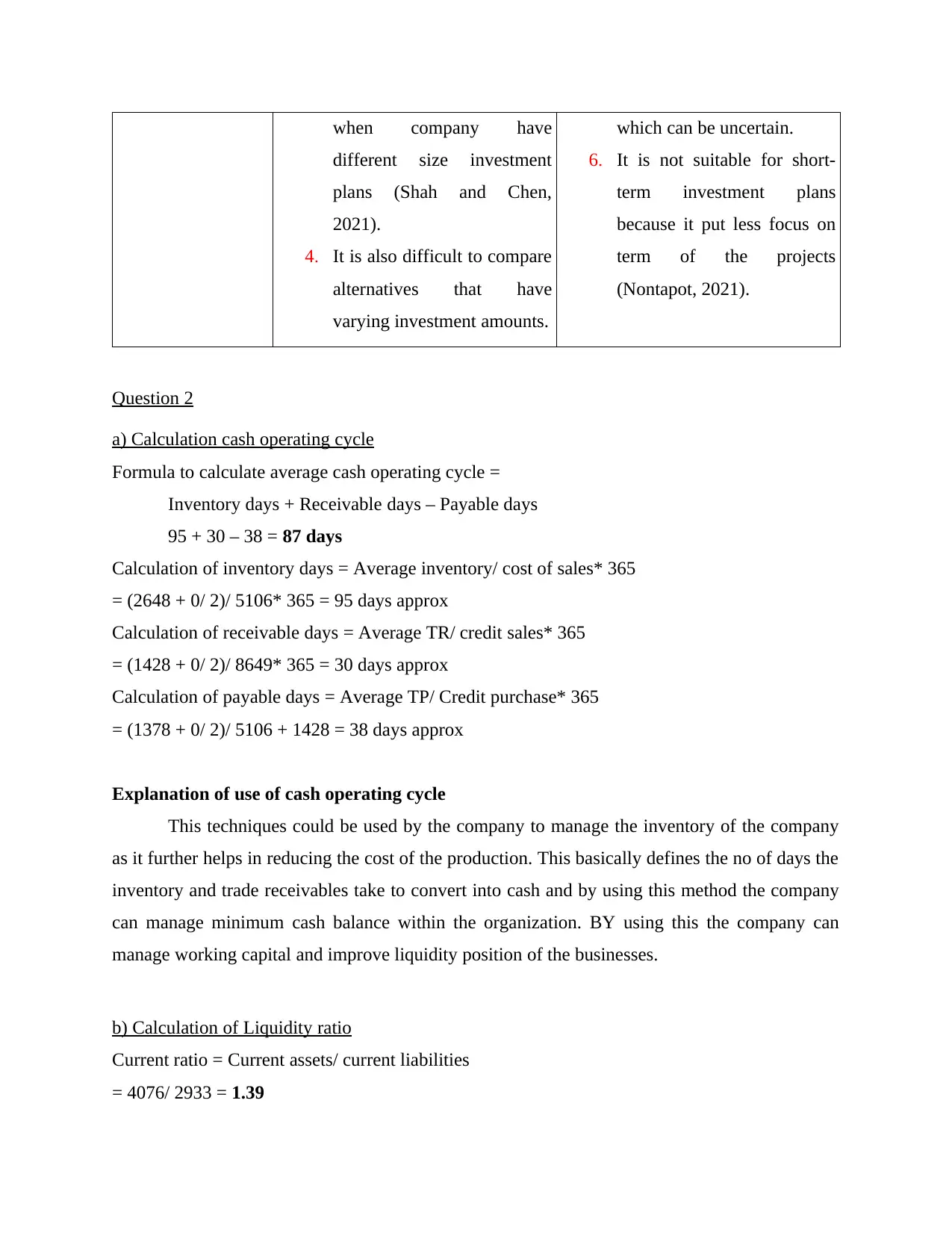

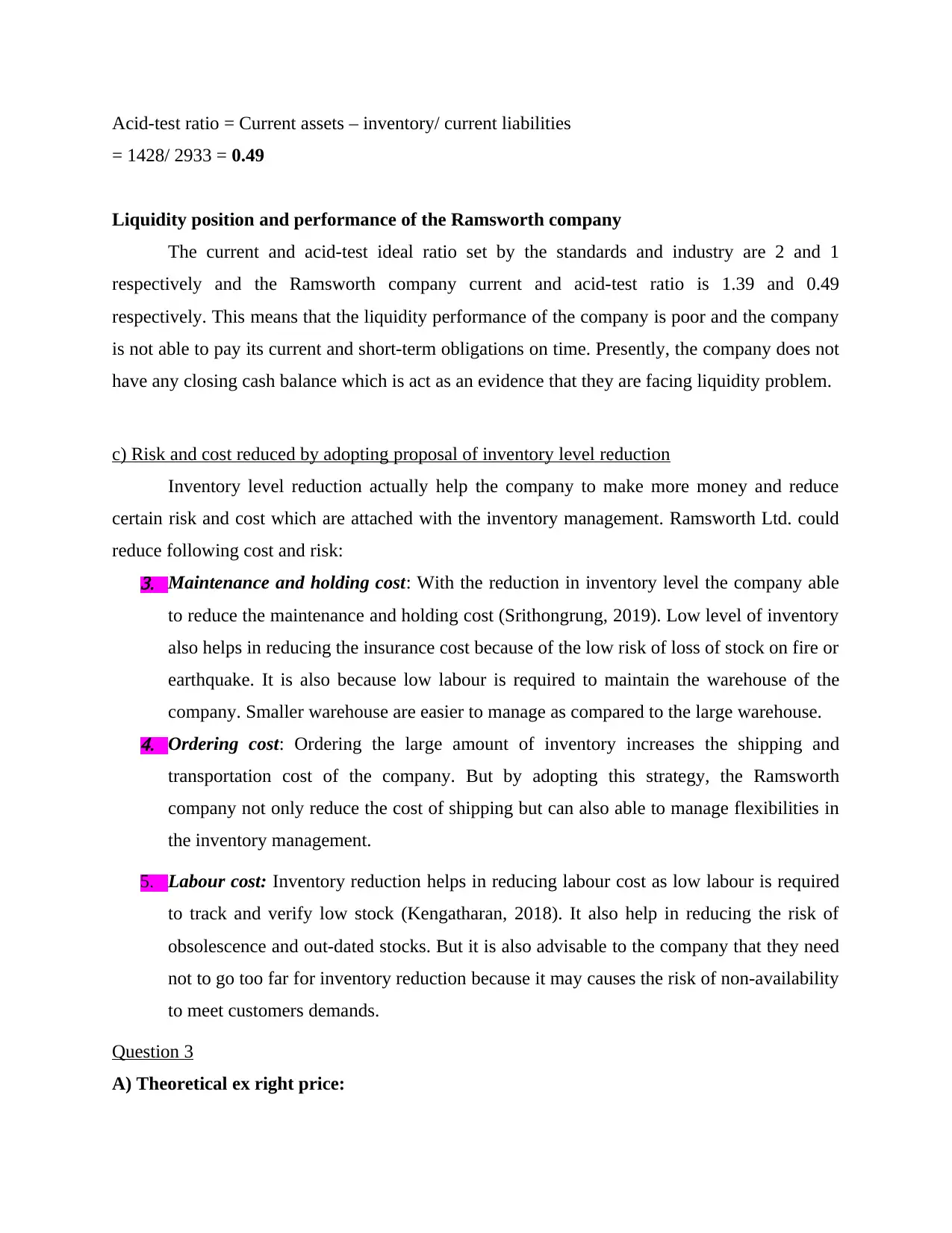

This assignment provides a detailed analysis of business finance concepts, focusing on capital budgeting and ratio analysis. It begins with calculating annual relevant cash flows and net present value for a project, followed by determining the internal rate of return (IRR) and assessing the project's financial viability. The report also compares different capital structure methods, including net present value and internal rate of return, highlighting their advantages and disadvantages. Furthermore, the assignment calculates the cash operating cycle, liquidity ratios (current and acid-test ratios), and discusses how reducing inventory levels can lower costs and risks for a company. Finally, it evaluates right share options for investors and analyzes various financial ratios to assess a company's financial position, including return on capital employed, gross profit margin, operating profit margin, inventory turnover period, trade receivable period, trade payable period, current ratio, acid test ratio, gearing ratio, interest cover ratio, earning per share, and dividend cover ratio.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.