Capital Budgeting Decision Making: Replacement Analysis - Safa Motors

VerifiedAdded on 2023/06/10

|47

|6903

|211

Report

AI Summary

This report analyzes Safa Motors Ltd.'s decision to replace its old plant with a new one for manufacturing electric vehicles, motivated by environmental regulations and the Volkswagen scandal. The analysis employs capital budgeting techniques such as payback period, net present value (NPV), and sensitivity analysis to assess the feasibility of the replacement. The report identifies relevant and irrelevant costs, forecasts cash flows and profits for both old and new car manufacturing scenarios, and performs a cost-volume-profit (CVP) analysis to determine the breakeven point. The application of capital budgeting techniques indicates a positive NPV, suggesting the replacement is profitable, although the payback period is longer than desired. Sensitivity analysis explores the impact of changes in sales volume, selling price, and required rate of return on the project's NPV. The report concludes with a critical analysis of the capital budgeting techniques used and considers non-financial factors influencing the replacement decision.

Running Head: Capital Budgeting Decision Making

REPLACEMENT DECISIONS UNDER CAPITAL BUDGETING

REPLACEMENT DECISIONS UNDER CAPITAL BUDGETING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital Budgeting Decision Making 1

Executive summary:

Safa Motors Ltd. is the company that is engaged in the business of manufacturing of vehicles.

Currently the company is manufacturing only petrol and diesel vehicles. However, after the

occurrence of Volkswagen Scandal, the company has started considering the proposal of

replacing its manufacturing its old plant with the new plant that produces the electrical vehicles

in place of petrol and diesel vehicles. This decision is being proposed in order to meet the

environmental laws and regulation of the country. To replace the old plant with a new one, the

different capital budgeting techniques have been applied in the report such as payback period,

net present value analysis, sensitivity analysis to estimate the worth of replacement decision.

Executive summary:

Safa Motors Ltd. is the company that is engaged in the business of manufacturing of vehicles.

Currently the company is manufacturing only petrol and diesel vehicles. However, after the

occurrence of Volkswagen Scandal, the company has started considering the proposal of

replacing its manufacturing its old plant with the new plant that produces the electrical vehicles

in place of petrol and diesel vehicles. This decision is being proposed in order to meet the

environmental laws and regulation of the country. To replace the old plant with a new one, the

different capital budgeting techniques have been applied in the report such as payback period,

net present value analysis, sensitivity analysis to estimate the worth of replacement decision.

Capital Budgeting Decision Making 2

Table of Contents

Executive summary:....................................................................................................................................1

Introduction:...............................................................................................................................................4

Relevant and Non-Relevant Costs of the proposed project:........................................................................4

The total cash flows and the profits for the next five years:.......................................................................5

Total incremental (net) profits and cash flows:...........................................................................................6

Cost Volume Profit Analysis:........................................................................................................................7

Application of various capital budgeting techniques...................................................................................8

Sensitivity Analysis:.....................................................................................................................................8

Change in sales volume...........................................................................................................................9

Change in selling price.............................................................................................................................9

Change in required rate of return............................................................................................................9

Change in useful life of project................................................................................................................9

Critical analysis of capital budgeting techniques:......................................................................................10

Payback period:.....................................................................................................................................10

Net present value:.................................................................................................................................11

Accounting rate of return:.....................................................................................................................12

Internal rate of return:..........................................................................................................................13

Non-financial factors of Replacement Decision:........................................................................................14

Conclusion:................................................................................................................................................15

References:................................................................................................................................................16

Appendices................................................................................................................................................19

Appendix 1: Forecasted total cash flows and total profits:....................................................................19

Appendix 2: Forecasted net cash flows and profits:..............................................................................23

Appendix 3: CVP Analysis.......................................................................................................................24

Appendix 4: Capital investment appraisal:............................................................................................25

Appendix 5: Sensitivity Analysis.............................................................................................................27

Table of Contents

Executive summary:....................................................................................................................................1

Introduction:...............................................................................................................................................4

Relevant and Non-Relevant Costs of the proposed project:........................................................................4

The total cash flows and the profits for the next five years:.......................................................................5

Total incremental (net) profits and cash flows:...........................................................................................6

Cost Volume Profit Analysis:........................................................................................................................7

Application of various capital budgeting techniques...................................................................................8

Sensitivity Analysis:.....................................................................................................................................8

Change in sales volume...........................................................................................................................9

Change in selling price.............................................................................................................................9

Change in required rate of return............................................................................................................9

Change in useful life of project................................................................................................................9

Critical analysis of capital budgeting techniques:......................................................................................10

Payback period:.....................................................................................................................................10

Net present value:.................................................................................................................................11

Accounting rate of return:.....................................................................................................................12

Internal rate of return:..........................................................................................................................13

Non-financial factors of Replacement Decision:........................................................................................14

Conclusion:................................................................................................................................................15

References:................................................................................................................................................16

Appendices................................................................................................................................................19

Appendix 1: Forecasted total cash flows and total profits:....................................................................19

Appendix 2: Forecasted net cash flows and profits:..............................................................................23

Appendix 3: CVP Analysis.......................................................................................................................24

Appendix 4: Capital investment appraisal:............................................................................................25

Appendix 5: Sensitivity Analysis.............................................................................................................27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital Budgeting Decision Making 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital Budgeting Decision Making 4

Introduction:

This report is being prepared to analyze the decision of Safa Motors Ltd in regards to the

replacement of old plant and equipment that is currently being used in the manufacturing of

petrol and diesel cars with the new plant that will manufacture the electrical vehicles. If the new

plant is implemented then the production of petrol and diesel car be abandoned and hence the old

plant and equipment will run out of use and hence it will be disposed in the market and funds

from it will be used to acquire the new machine that is more technical in nature. Since the

investment in new plant requires huge amount of funds, such replacement decision must be

carefully evaluated by applying various techniques of capital budgeting such as net present value

analysis, payback period analysis, sensitivity analysis .etc. The incremental cash flows approach

has been used to evaluate the replacement decision.

Relevant and Non-Relevant Costs of the proposed project:

While determining the worthiness of any project, the project manager has to undertake the cost

benefit analysis of the project under which all the costs and benefits of the project are separately

and jointly considered to understand their impact on the overall value of the project. Primarily,

the cost is divided into two categories i.e. the relevant cost and irrelevant cost. Relevant costs are

those costs that are useful to be given consideration while taking the decisions about project’s

acceptance or rejection. However relevant costs are those costs that do not affect the further cash

flows of the project and are the common part of all the alternative projects under considerations.

These costs are either sunk costs that have already been incurred or the costs that forms part in

all the alternative options of investment.

Introduction:

This report is being prepared to analyze the decision of Safa Motors Ltd in regards to the

replacement of old plant and equipment that is currently being used in the manufacturing of

petrol and diesel cars with the new plant that will manufacture the electrical vehicles. If the new

plant is implemented then the production of petrol and diesel car be abandoned and hence the old

plant and equipment will run out of use and hence it will be disposed in the market and funds

from it will be used to acquire the new machine that is more technical in nature. Since the

investment in new plant requires huge amount of funds, such replacement decision must be

carefully evaluated by applying various techniques of capital budgeting such as net present value

analysis, payback period analysis, sensitivity analysis .etc. The incremental cash flows approach

has been used to evaluate the replacement decision.

Relevant and Non-Relevant Costs of the proposed project:

While determining the worthiness of any project, the project manager has to undertake the cost

benefit analysis of the project under which all the costs and benefits of the project are separately

and jointly considered to understand their impact on the overall value of the project. Primarily,

the cost is divided into two categories i.e. the relevant cost and irrelevant cost. Relevant costs are

those costs that are useful to be given consideration while taking the decisions about project’s

acceptance or rejection. However relevant costs are those costs that do not affect the further cash

flows of the project and are the common part of all the alternative projects under considerations.

These costs are either sunk costs that have already been incurred or the costs that forms part in

all the alternative options of investment.

Capital Budgeting Decision Making 5

In the present case, the cost of research carried for the diesel and petrol cars is a sunk cost as it

has already been incurred and hence it cannot be recovered under any circumstance. Therefore

this cost of £250000 is irrelevant in nature and thus it must be ignored while making the

evaluation of equipment decision. Further, the cost of acquisition of old equipment used to

manufacture the petrol and diesel cars is not to be taken into consideration while making the

calculation of incremental initial investment as it has already been incurred. But, the same must

be considered to calculate the depreciation on the equipment. However, the depreciation expense

on both the equipment is also irrelevant in nature since the present question has asked to ignore

the tax impact of the cash flows and hence the depreciation is not relevant to be considered in

such as it does not amount to flow of cash (Chen, 2008). The relevant costs of the replacement

decision under consideration are all other costs that are taken into consideration while calculating

the net present value of the project. These costs are: Cost of acquisition of new investment,

material cost, labor cost, variable cost, fixed cost such as research and development cost, selling ,

savings in the cost of components of old car, increase in the cost of new components.

The total cash flows and the profits for the next five years:

The total cash flows and the profits for the next five years under both the projects i.e.

manufacturing the old cars only and the new cars only are shown in the tables below:

Refer Appendix 1:

Old car:

Year 1 2 3 4 5

Profit £ £ £ £ £

In the present case, the cost of research carried for the diesel and petrol cars is a sunk cost as it

has already been incurred and hence it cannot be recovered under any circumstance. Therefore

this cost of £250000 is irrelevant in nature and thus it must be ignored while making the

evaluation of equipment decision. Further, the cost of acquisition of old equipment used to

manufacture the petrol and diesel cars is not to be taken into consideration while making the

calculation of incremental initial investment as it has already been incurred. But, the same must

be considered to calculate the depreciation on the equipment. However, the depreciation expense

on both the equipment is also irrelevant in nature since the present question has asked to ignore

the tax impact of the cash flows and hence the depreciation is not relevant to be considered in

such as it does not amount to flow of cash (Chen, 2008). The relevant costs of the replacement

decision under consideration are all other costs that are taken into consideration while calculating

the net present value of the project. These costs are: Cost of acquisition of new investment,

material cost, labor cost, variable cost, fixed cost such as research and development cost, selling ,

savings in the cost of components of old car, increase in the cost of new components.

The total cash flows and the profits for the next five years:

The total cash flows and the profits for the next five years under both the projects i.e.

manufacturing the old cars only and the new cars only are shown in the tables below:

Refer Appendix 1:

Old car:

Year 1 2 3 4 5

Profit £ £ £ £ £

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

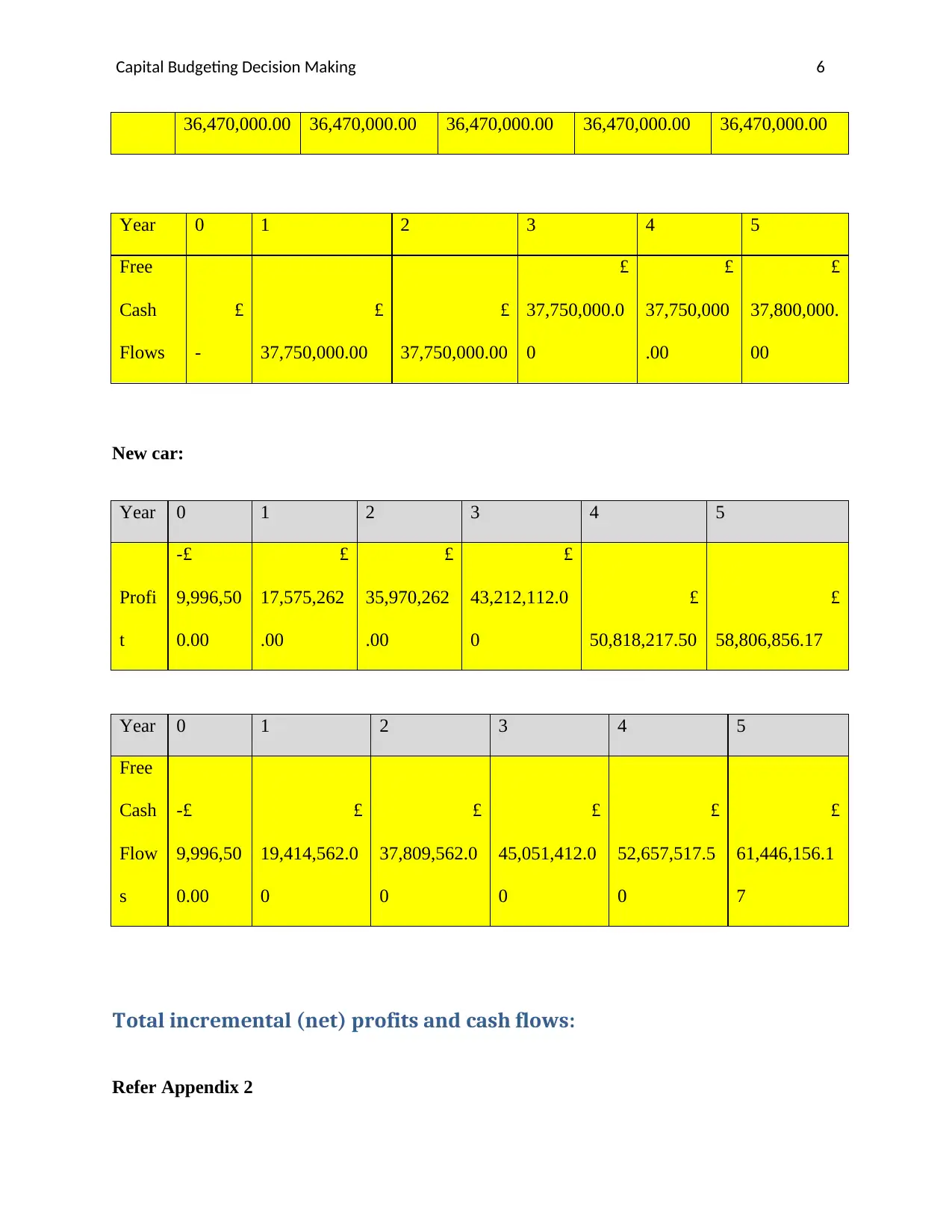

Capital Budgeting Decision Making 6

36,470,000.00 36,470,000.00 36,470,000.00 36,470,000.00 36,470,000.00

Year 0 1 2 3 4 5

Free

Cash

Flows

£

-

£

37,750,000.00

£

37,750,000.00

£

37,750,000.0

0

£

37,750,000

.00

£

37,800,000.

00

New car:

Year 0 1 2 3 4 5

Profi

t

-£

9,996,50

0.00

£

17,575,262

.00

£

35,970,262

.00

£

43,212,112.0

0

£

50,818,217.50

£

58,806,856.17

Year 0 1 2 3 4 5

Free

Cash

Flow

s

-£

9,996,50

0.00

£

19,414,562.0

0

£

37,809,562.0

0

£

45,051,412.0

0

£

52,657,517.5

0

£

61,446,156.1

7

Total incremental (net) profits and cash flows:

Refer Appendix 2

36,470,000.00 36,470,000.00 36,470,000.00 36,470,000.00 36,470,000.00

Year 0 1 2 3 4 5

Free

Cash

Flows

£

-

£

37,750,000.00

£

37,750,000.00

£

37,750,000.0

0

£

37,750,000

.00

£

37,800,000.

00

New car:

Year 0 1 2 3 4 5

Profi

t

-£

9,996,50

0.00

£

17,575,262

.00

£

35,970,262

.00

£

43,212,112.0

0

£

50,818,217.50

£

58,806,856.17

Year 0 1 2 3 4 5

Free

Cash

Flow

s

-£

9,996,50

0.00

£

19,414,562.0

0

£

37,809,562.0

0

£

45,051,412.0

0

£

52,657,517.5

0

£

61,446,156.1

7

Total incremental (net) profits and cash flows:

Refer Appendix 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

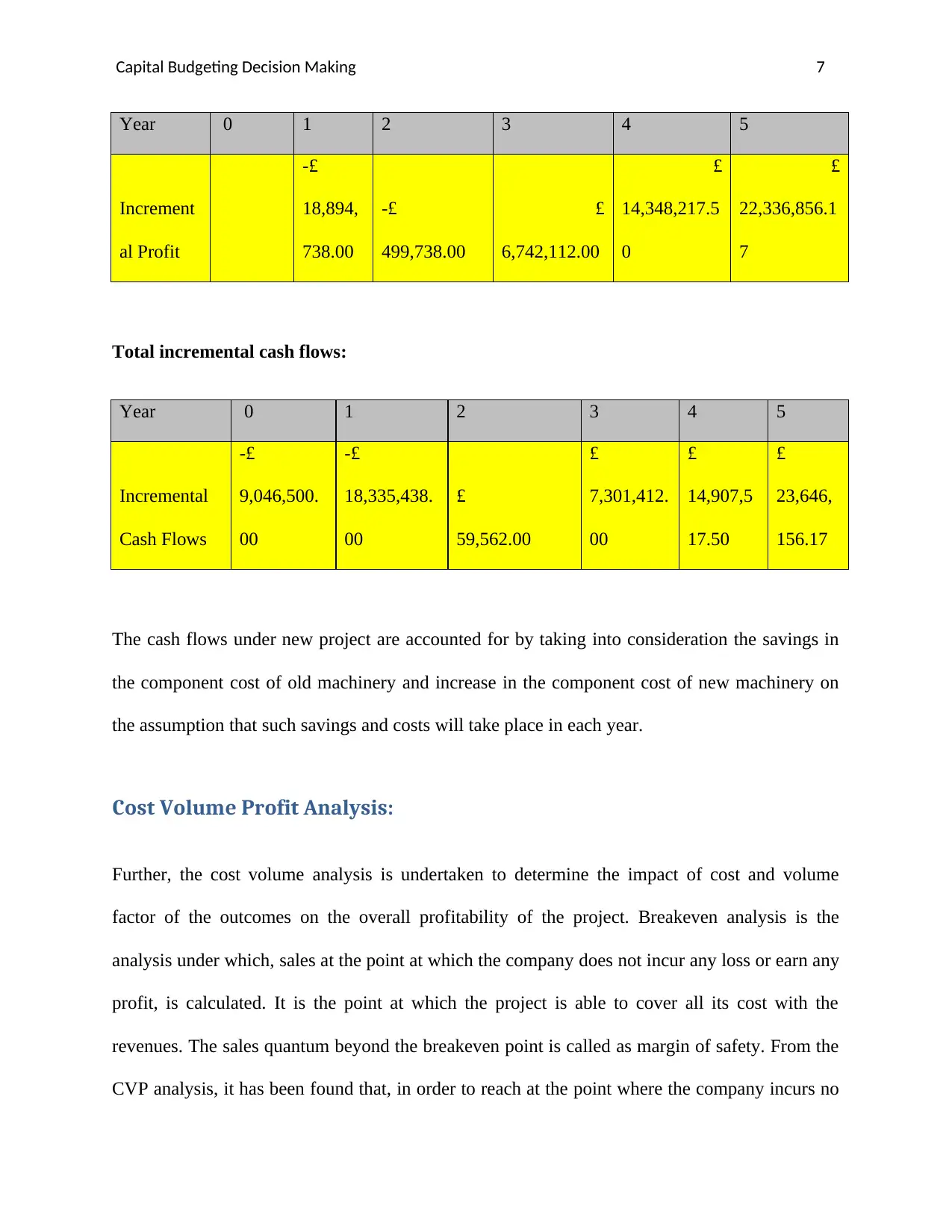

Capital Budgeting Decision Making 7

Year 0 1 2 3 4 5

Increment

al Profit

-£

18,894,

738.00

-£

499,738.00

£

6,742,112.00

£

14,348,217.5

0

£

22,336,856.1

7

Total incremental cash flows:

Year 0 1 2 3 4 5

Incremental

Cash Flows

-£

9,046,500.

00

-£

18,335,438.

00

£

59,562.00

£

7,301,412.

00

£

14,907,5

17.50

£

23,646,

156.17

The cash flows under new project are accounted for by taking into consideration the savings in

the component cost of old machinery and increase in the component cost of new machinery on

the assumption that such savings and costs will take place in each year.

Cost Volume Profit Analysis:

Further, the cost volume analysis is undertaken to determine the impact of cost and volume

factor of the outcomes on the overall profitability of the project. Breakeven analysis is the

analysis under which, sales at the point at which the company does not incur any loss or earn any

profit, is calculated. It is the point at which the project is able to cover all its cost with the

revenues. The sales quantum beyond the breakeven point is called as margin of safety. From the

CVP analysis, it has been found that, in order to reach at the point where the company incurs no

Year 0 1 2 3 4 5

Increment

al Profit

-£

18,894,

738.00

-£

499,738.00

£

6,742,112.00

£

14,348,217.5

0

£

22,336,856.1

7

Total incremental cash flows:

Year 0 1 2 3 4 5

Incremental

Cash Flows

-£

9,046,500.

00

-£

18,335,438.

00

£

59,562.00

£

7,301,412.

00

£

14,907,5

17.50

£

23,646,

156.17

The cash flows under new project are accounted for by taking into consideration the savings in

the component cost of old machinery and increase in the component cost of new machinery on

the assumption that such savings and costs will take place in each year.

Cost Volume Profit Analysis:

Further, the cost volume analysis is undertaken to determine the impact of cost and volume

factor of the outcomes on the overall profitability of the project. Breakeven analysis is the

analysis under which, sales at the point at which the company does not incur any loss or earn any

profit, is calculated. It is the point at which the project is able to cover all its cost with the

revenues. The sales quantum beyond the breakeven point is called as margin of safety. From the

CVP analysis, it has been found that, in order to reach at the point where the company incurs no

Capital Budgeting Decision Making 8

loss and earns no profit, it is required to sell 43723 units of new electric vehicles and after this

point it will start earning profits (Refer Appendix 3).

Application of various capital budgeting techniques:

Further in the report various techniques of capital budgeting are applied to evaluate the

replacement decision. For this purpose, NPV, IRR, ARR and Payback Period are calculated. The

NPV of the replacement decision is positive and hence it indicates that it will be profitable to

accept the decision of manufacturing the electric vehicles only in place of diesel cars. However,

the desirable payback period of the project is 3.5 years while the calculations have shown that

the old machinery replacement will result in the payback period of around 4.34 years which is

higher than the desirable period of time (Refer Appendix 4). Therefore, it is necessary to identify

the objective of company behind such investment. If the company is expecting to earn maximum

returns within the minimum time then it must not accept the proposed project. But, if the main

aim of the project is to earn maximum returns irrespective of the time period it must accept the

new plant implementation project as the calculation of Annual rate of return is found to be quite

higher (85%) than the desirable results (35%). Further, the internal rate of return of the project is

15.17% and it is higher than the cost of capital of the project (12%). It signifies that the project

has higher return potential. Therefore it must be accepted.

Sensitivity Analysis:

loss and earns no profit, it is required to sell 43723 units of new electric vehicles and after this

point it will start earning profits (Refer Appendix 3).

Application of various capital budgeting techniques:

Further in the report various techniques of capital budgeting are applied to evaluate the

replacement decision. For this purpose, NPV, IRR, ARR and Payback Period are calculated. The

NPV of the replacement decision is positive and hence it indicates that it will be profitable to

accept the decision of manufacturing the electric vehicles only in place of diesel cars. However,

the desirable payback period of the project is 3.5 years while the calculations have shown that

the old machinery replacement will result in the payback period of around 4.34 years which is

higher than the desirable period of time (Refer Appendix 4). Therefore, it is necessary to identify

the objective of company behind such investment. If the company is expecting to earn maximum

returns within the minimum time then it must not accept the proposed project. But, if the main

aim of the project is to earn maximum returns irrespective of the time period it must accept the

new plant implementation project as the calculation of Annual rate of return is found to be quite

higher (85%) than the desirable results (35%). Further, the internal rate of return of the project is

15.17% and it is higher than the cost of capital of the project (12%). It signifies that the project

has higher return potential. Therefore it must be accepted.

Sensitivity Analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital Budgeting Decision Making 9

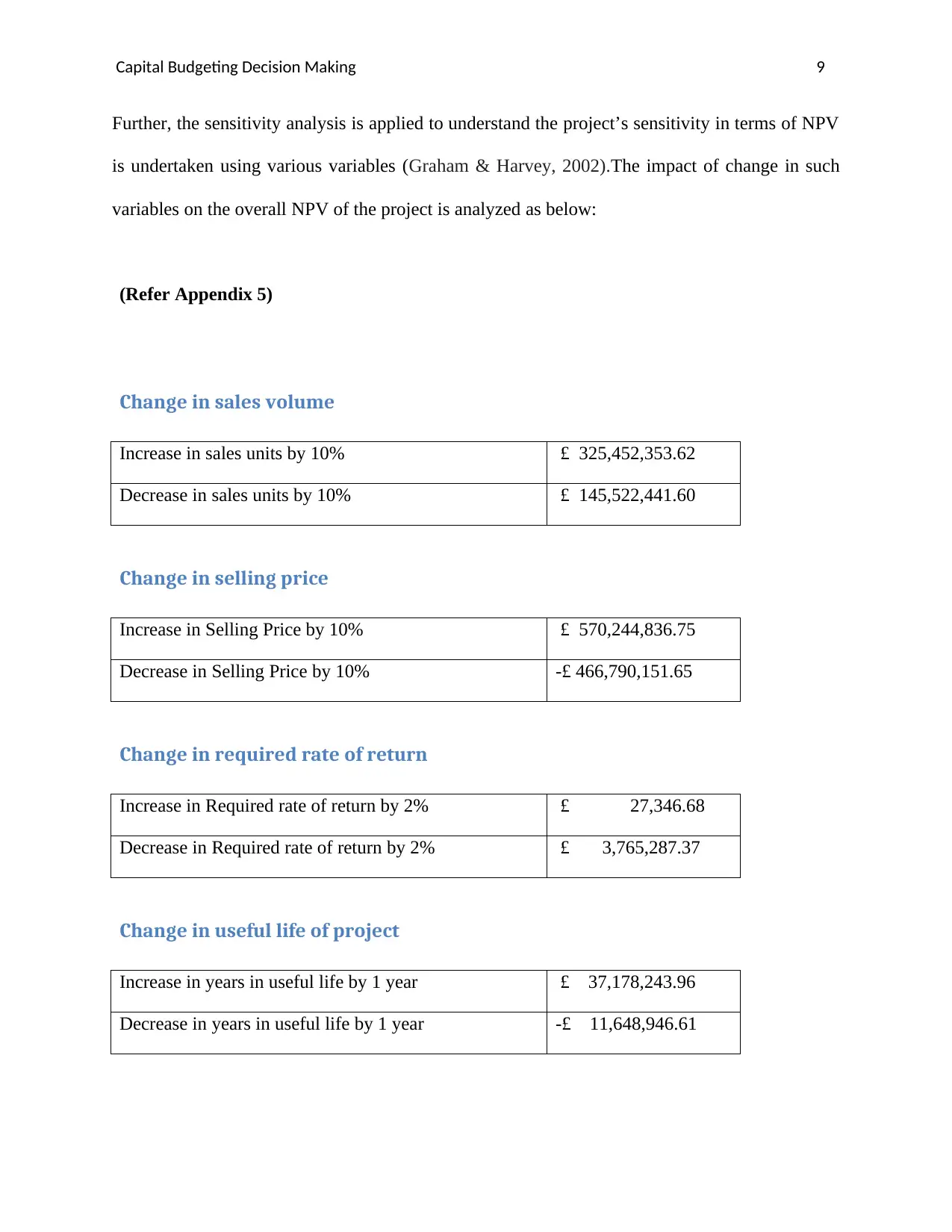

Further, the sensitivity analysis is applied to understand the project’s sensitivity in terms of NPV

is undertaken using various variables (Graham & Harvey, 2002).The impact of change in such

variables on the overall NPV of the project is analyzed as below:

(Refer Appendix 5)

Change in sales volume

Increase in sales units by 10% £ 325,452,353.62

Decrease in sales units by 10% £ 145,522,441.60

Change in selling price

Increase in Selling Price by 10% £ 570,244,836.75

Decrease in Selling Price by 10% -£ 466,790,151.65

Change in required rate of return

Increase in Required rate of return by 2% £ 27,346.68

Decrease in Required rate of return by 2% £ 3,765,287.37

Change in useful life of project

Increase in years in useful life by 1 year £ 37,178,243.96

Decrease in years in useful life by 1 year -£ 11,648,946.61

Further, the sensitivity analysis is applied to understand the project’s sensitivity in terms of NPV

is undertaken using various variables (Graham & Harvey, 2002).The impact of change in such

variables on the overall NPV of the project is analyzed as below:

(Refer Appendix 5)

Change in sales volume

Increase in sales units by 10% £ 325,452,353.62

Decrease in sales units by 10% £ 145,522,441.60

Change in selling price

Increase in Selling Price by 10% £ 570,244,836.75

Decrease in Selling Price by 10% -£ 466,790,151.65

Change in required rate of return

Increase in Required rate of return by 2% £ 27,346.68

Decrease in Required rate of return by 2% £ 3,765,287.37

Change in useful life of project

Increase in years in useful life by 1 year £ 37,178,243.96

Decrease in years in useful life by 1 year -£ 11,648,946.61

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital Budgeting Decision Making 10

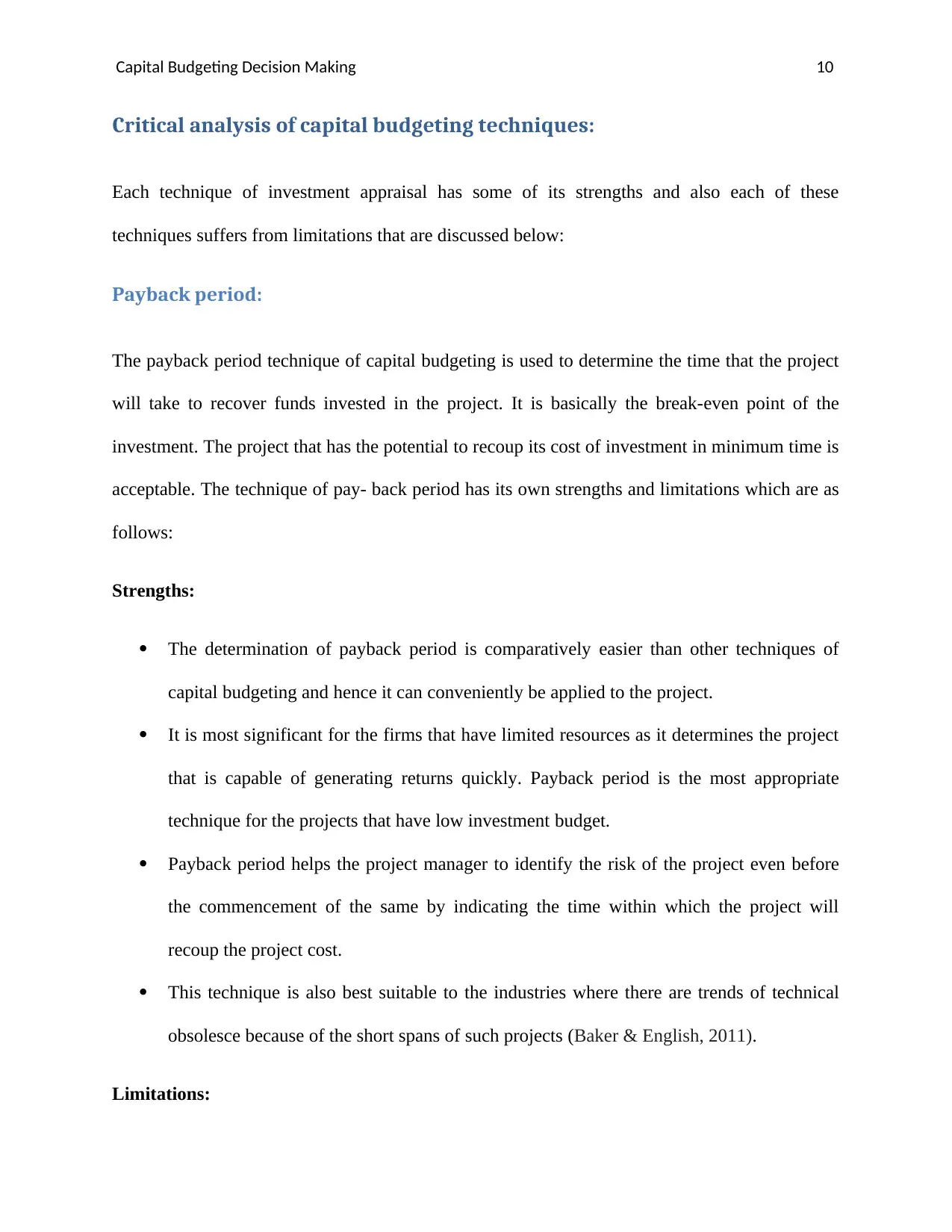

Critical analysis of capital budgeting techniques:

Each technique of investment appraisal has some of its strengths and also each of these

techniques suffers from limitations that are discussed below:

Payback period:

The payback period technique of capital budgeting is used to determine the time that the project

will take to recover funds invested in the project. It is basically the break-even point of the

investment. The project that has the potential to recoup its cost of investment in minimum time is

acceptable. The technique of pay- back period has its own strengths and limitations which are as

follows:

Strengths:

The determination of payback period is comparatively easier than other techniques of

capital budgeting and hence it can conveniently be applied to the project.

It is most significant for the firms that have limited resources as it determines the project

that is capable of generating returns quickly. Payback period is the most appropriate

technique for the projects that have low investment budget.

Payback period helps the project manager to identify the risk of the project even before

the commencement of the same by indicating the time within which the project will

recoup the project cost.

This technique is also best suitable to the industries where there are trends of technical

obsolesce because of the short spans of such projects (Baker & English, 2011).

Limitations:

Critical analysis of capital budgeting techniques:

Each technique of investment appraisal has some of its strengths and also each of these

techniques suffers from limitations that are discussed below:

Payback period:

The payback period technique of capital budgeting is used to determine the time that the project

will take to recover funds invested in the project. It is basically the break-even point of the

investment. The project that has the potential to recoup its cost of investment in minimum time is

acceptable. The technique of pay- back period has its own strengths and limitations which are as

follows:

Strengths:

The determination of payback period is comparatively easier than other techniques of

capital budgeting and hence it can conveniently be applied to the project.

It is most significant for the firms that have limited resources as it determines the project

that is capable of generating returns quickly. Payback period is the most appropriate

technique for the projects that have low investment budget.

Payback period helps the project manager to identify the risk of the project even before

the commencement of the same by indicating the time within which the project will

recoup the project cost.

This technique is also best suitable to the industries where there are trends of technical

obsolesce because of the short spans of such projects (Baker & English, 2011).

Limitations:

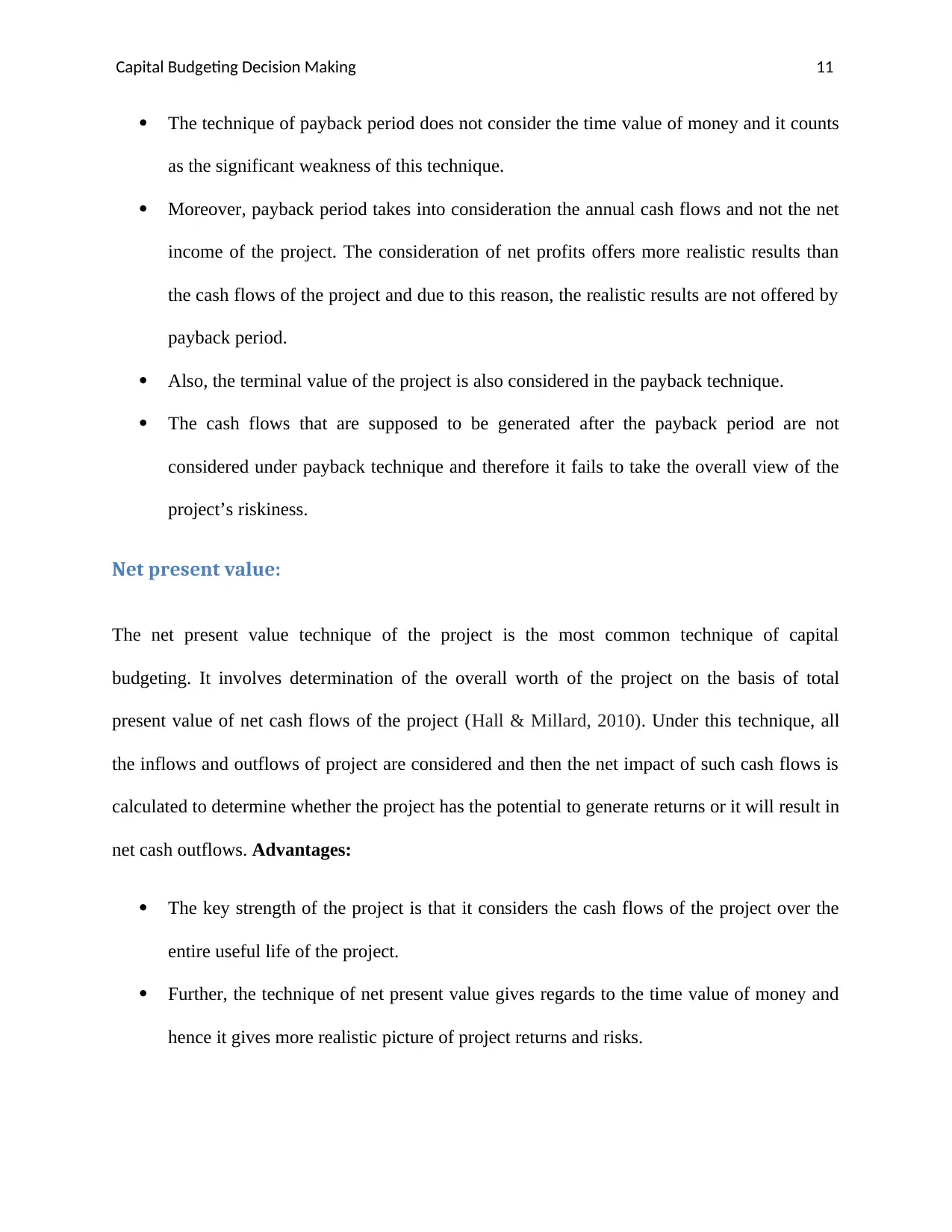

Capital Budgeting Decision Making 11

The technique of payback period does not consider the time value of money and it counts

as the significant weakness of this technique.

Moreover, payback period takes into consideration the annual cash flows and not the net

income of the project. The consideration of net profits offers more realistic results than

the cash flows of the project and due to this reason, the realistic results are not offered by

payback period.

Also, the terminal value of the project is also considered in the payback technique.

The cash flows that are supposed to be generated after the payback period are not

considered under payback technique and therefore it fails to take the overall view of the

project’s riskiness.

Net present value:

The net present value technique of the project is the most common technique of capital

budgeting. It involves determination of the overall worth of the project on the basis of total

present value of net cash flows of the project (Hall & Millard, 2010). Under this technique, all

the inflows and outflows of project are considered and then the net impact of such cash flows is

calculated to determine whether the project has the potential to generate returns or it will result in

net cash outflows. Advantages:

The key strength of the project is that it considers the cash flows of the project over the

entire useful life of the project.

Further, the technique of net present value gives regards to the time value of money and

hence it gives more realistic picture of project returns and risks.

The technique of payback period does not consider the time value of money and it counts

as the significant weakness of this technique.

Moreover, payback period takes into consideration the annual cash flows and not the net

income of the project. The consideration of net profits offers more realistic results than

the cash flows of the project and due to this reason, the realistic results are not offered by

payback period.

Also, the terminal value of the project is also considered in the payback technique.

The cash flows that are supposed to be generated after the payback period are not

considered under payback technique and therefore it fails to take the overall view of the

project’s riskiness.

Net present value:

The net present value technique of the project is the most common technique of capital

budgeting. It involves determination of the overall worth of the project on the basis of total

present value of net cash flows of the project (Hall & Millard, 2010). Under this technique, all

the inflows and outflows of project are considered and then the net impact of such cash flows is

calculated to determine whether the project has the potential to generate returns or it will result in

net cash outflows. Advantages:

The key strength of the project is that it considers the cash flows of the project over the

entire useful life of the project.

Further, the technique of net present value gives regards to the time value of money and

hence it gives more realistic picture of project returns and risks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 47

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.