University Finance Report: Capital Budgeting, Ethics, and WACC

VerifiedAdded on 2020/02/03

|9

|1574

|79

Report

AI Summary

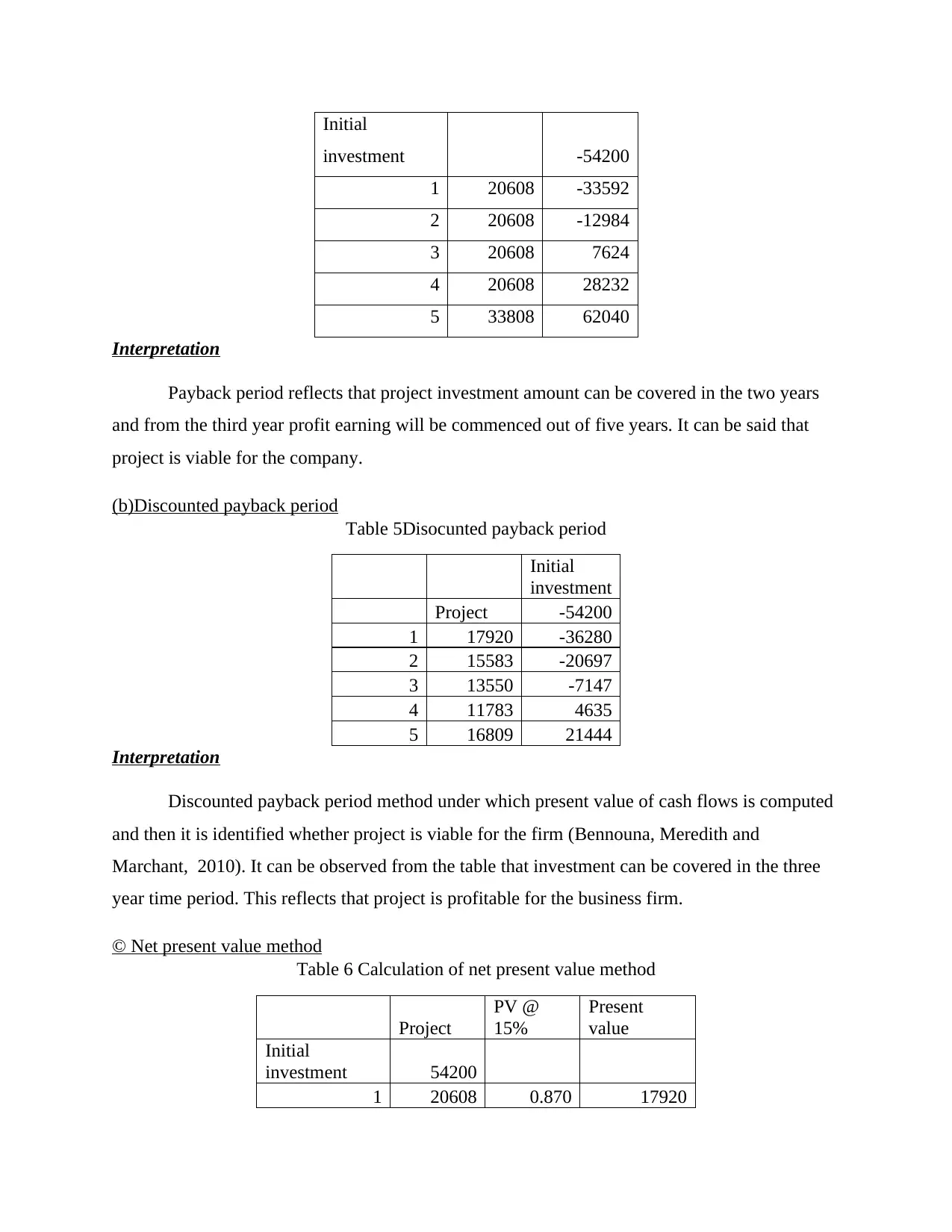

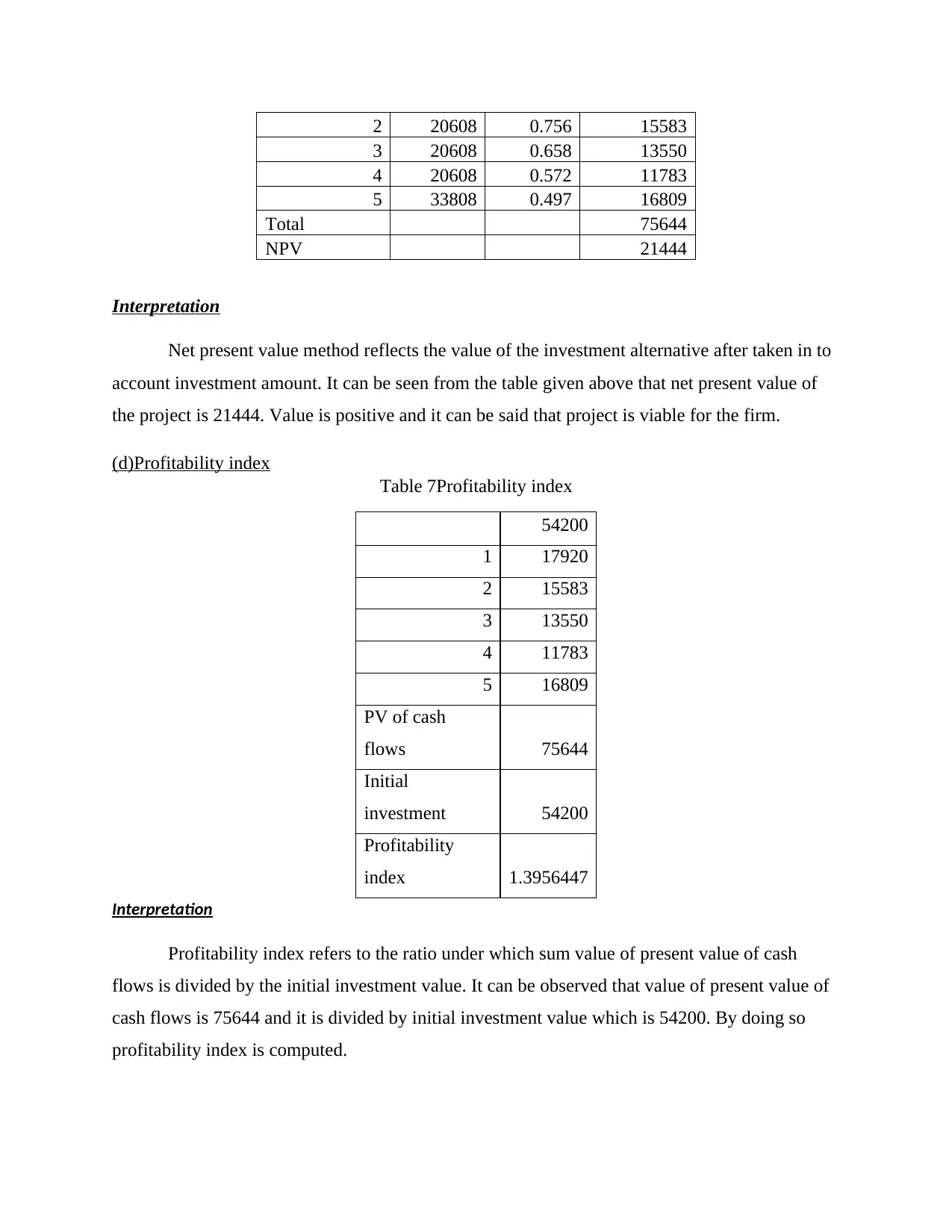

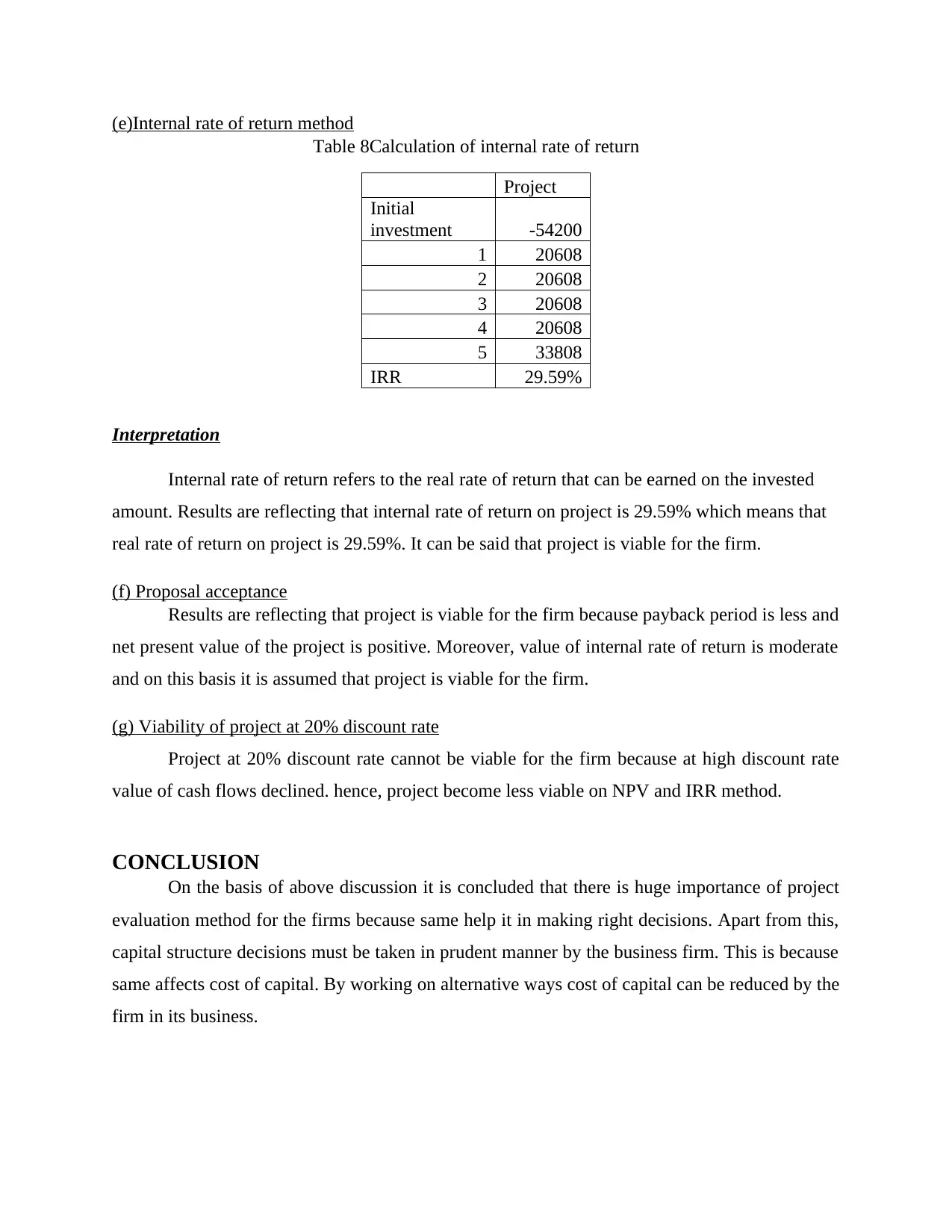

This report provides a comprehensive analysis of capital budgeting techniques and financial concepts. It begins by highlighting the ethical considerations essential in the capital budgeting process, emphasizing the importance of accurate cash flow projections and stakeholder interests. The report then delves into the calculation of the weighted average cost of capital (WACC) and explores alternative capital structures to manage costs. Furthermore, it evaluates a sample project using various capital budgeting methods, including payback period, discounted payback period, net present value (NPV), profitability index, and internal rate of return (IRR). The analysis includes detailed calculations and interpretations of the results, concluding with a proposal acceptance decision based on the project's viability and a discussion on the impact of a higher discount rate. The report underscores the importance of project evaluation methods and prudent capital structure decisions for effective financial management.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.