Financial Report: Capital Budgeting Analysis for Powerboat Projects

VerifiedAdded on 2021/06/15

|4

|1108

|27

Report

AI Summary

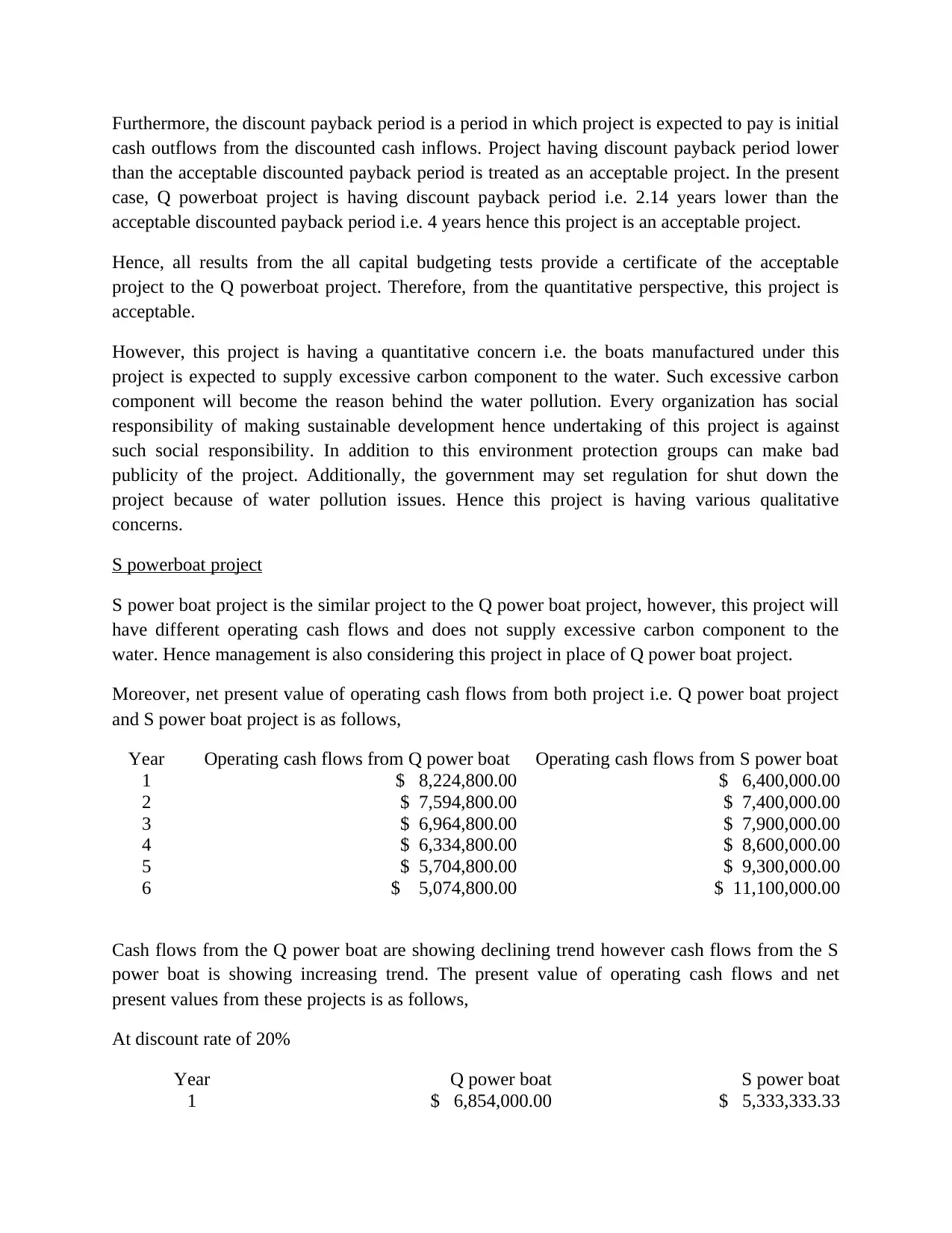

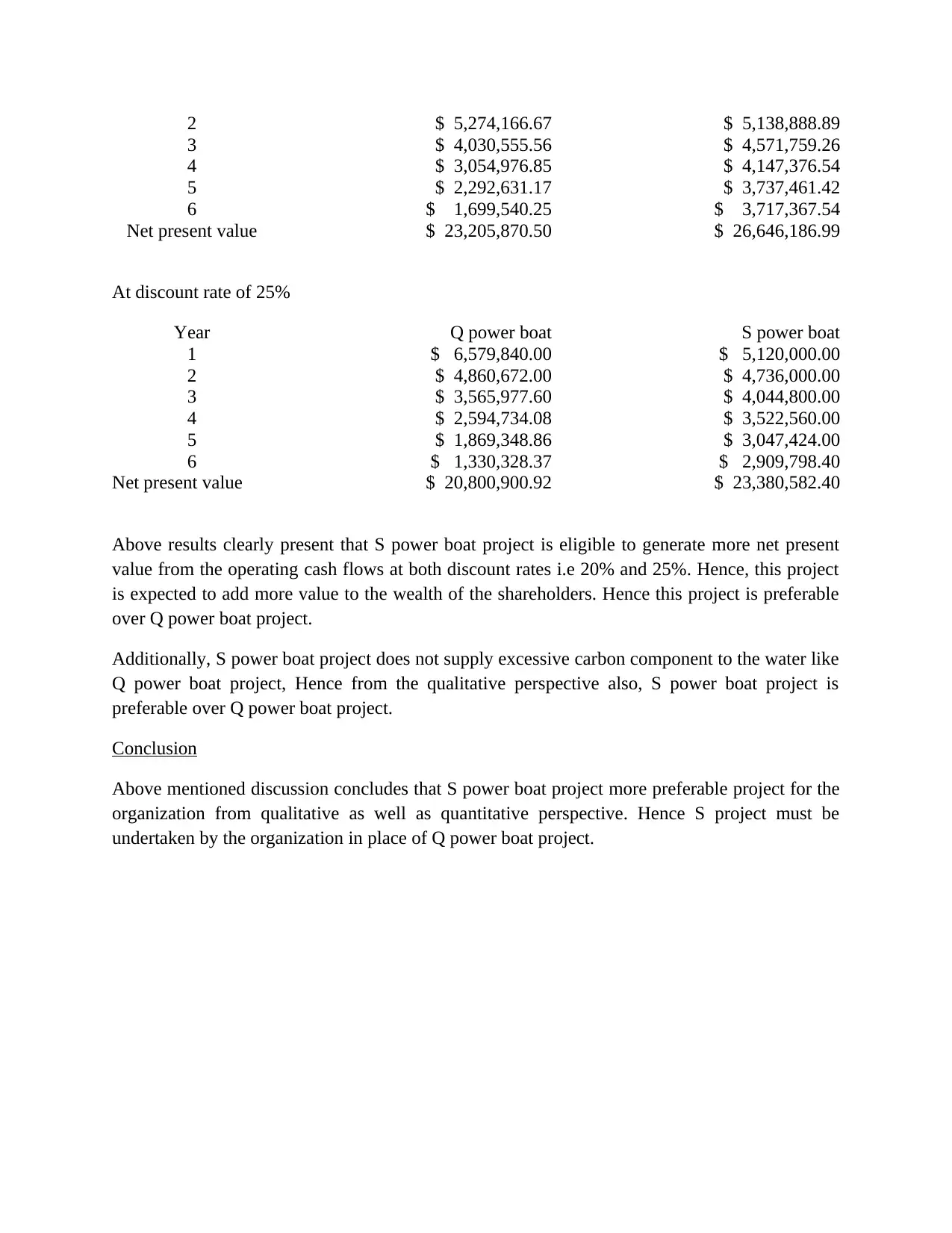

This report provides a capital budgeting analysis comparing two powerboat projects, Q and S, to determine which is a more viable investment. The analysis utilizes various capital budgeting techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), and discounted payback period to assess the financial feasibility of each project. The Q powerboat project initially appears acceptable based on its positive NPV, high IRR, and short discounted payback period. However, the report also considers qualitative factors, particularly the environmental impact of the Q project due to its contribution to water pollution, which leads to concerns regarding social responsibility and potential government regulations. The S powerboat project is then introduced as an alternative, with a comparative analysis showing that it generates a higher NPV at both 20% and 25% discount rates and does not pose the same environmental risks. Consequently, the report concludes that the S powerboat project is the more favorable choice from both quantitative and qualitative standpoints, recommending its implementation over the Q powerboat project.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.