FINA 1082 Principles of Finance - Project NPV and Stock DDM

VerifiedAdded on 2022/08/09

|16

|3463

|14

Report

AI Summary

This report addresses key concepts in finance, including project evaluation using Net Present Value (NPV) analysis and stock valuation using the Dividend Discount Model (DDM). The first question explores the appropriate cost of capital for a project, comparing the cost of debt and the Weighted Average Cost of Capital (WACC), and conducts a sensitivity analysis to assess the impact of changes in investment capital, projected sales value, and WACC on the project's NPV. The second question applies the DDM to value stocks, using Hormel Food Products and AT&T as examples, and discusses the assumptions underlying the model, including beta calculation, market rate of return, risk-free rate, and growth rate. Finally, it provides investment recommendations based on the comparison of intrinsic value and market price, considering the mean reversion property of stock prices. The report emphasizes the importance of considering various factors and assumptions in financial decision-making.

Running head: QUESTION AND ANSWERS

Question and Answers

Name of the Student:

Name of the University:

Author Note:

Question and Answers

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1QUESTION AND ANSWERS

Table of Contents

Answer to Question 1:................................................................................................................2

Part 1:.....................................................................................................................................2

Part 2:.....................................................................................................................................3

Part 3:.....................................................................................................................................5

Part a: Change in the Investment Capital:..........................................................................5

Part b: Change in the projected sale value of the project:..................................................6

Part c: Change in the WACC of the company:..................................................................7

Answer to Question 2:................................................................................................................8

Part 1:.................................................................................................................................8

Part 2:.................................................................................................................................9

Part 3:...............................................................................................................................10

Answer to Question 3:..............................................................................................................11

Bibliographies:.........................................................................................................................13

Table of Contents

Answer to Question 1:................................................................................................................2

Part 1:.....................................................................................................................................2

Part 2:.....................................................................................................................................3

Part 3:.....................................................................................................................................5

Part a: Change in the Investment Capital:..........................................................................5

Part b: Change in the projected sale value of the project:..................................................6

Part c: Change in the WACC of the company:..................................................................7

Answer to Question 2:................................................................................................................8

Part 1:.................................................................................................................................8

Part 2:.................................................................................................................................9

Part 3:...............................................................................................................................10

Answer to Question 3:..............................................................................................................11

Bibliographies:.........................................................................................................................13

2QUESTION AND ANSWERS

Answer to Question 1:

Part 1:

The cost of capital of a project depends on various factors which needs to be

considered by the company management before selecting one for a project. The cost of

capital of debt as highlighted by the CEO wants to take as 6%, which is the cost of debt since

the project would be financed with debt. At first sight this seems to be appropriate, however

the debt would be recorded in the balance sheet of the company and would affect the credit

worthiness of the company. Thus, taking the cost of debt as the cost of capital for a project

would be incorrect as it would not highlight the true measure of risk which is present in the

project (Marcu and et.al 2017).

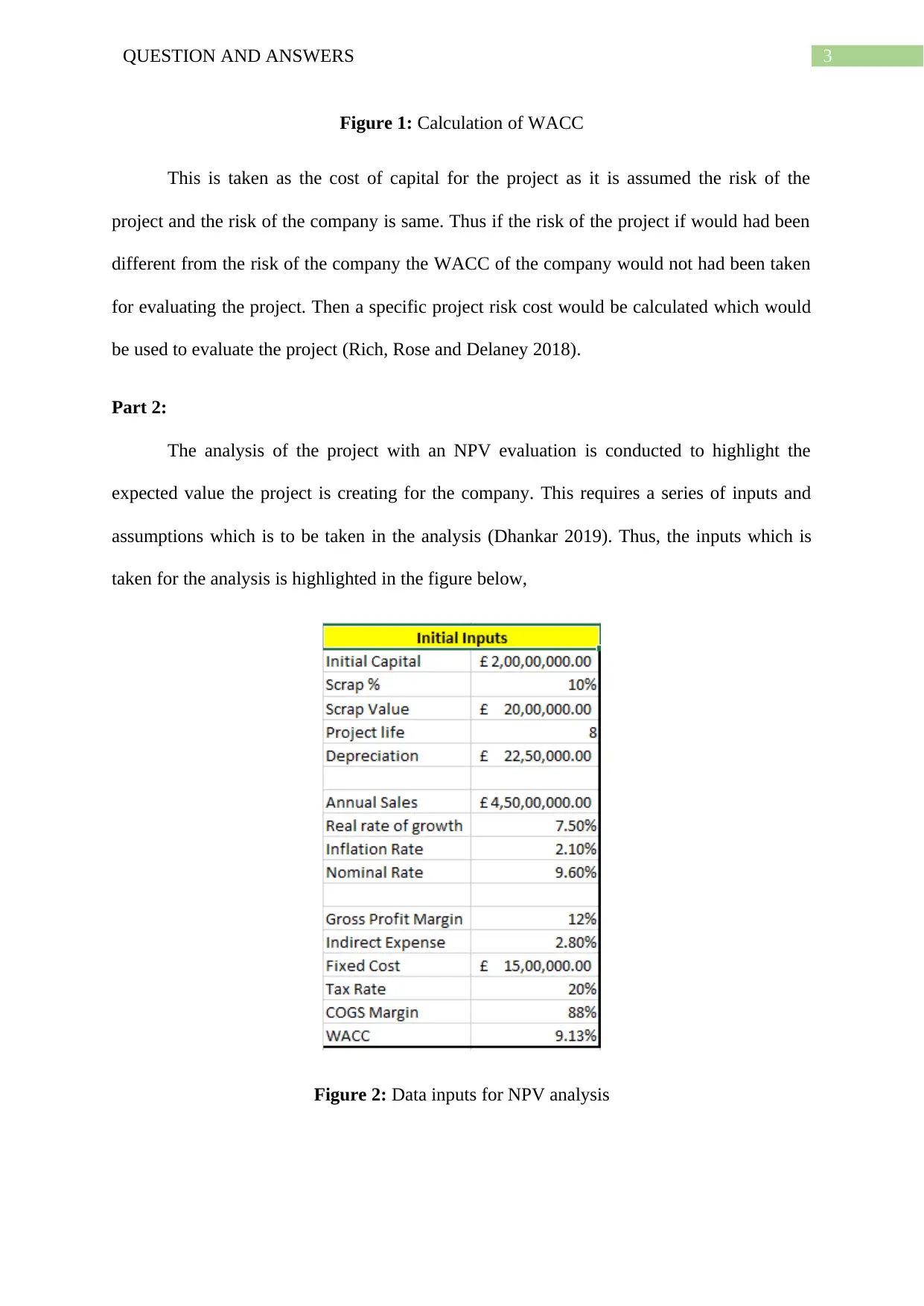

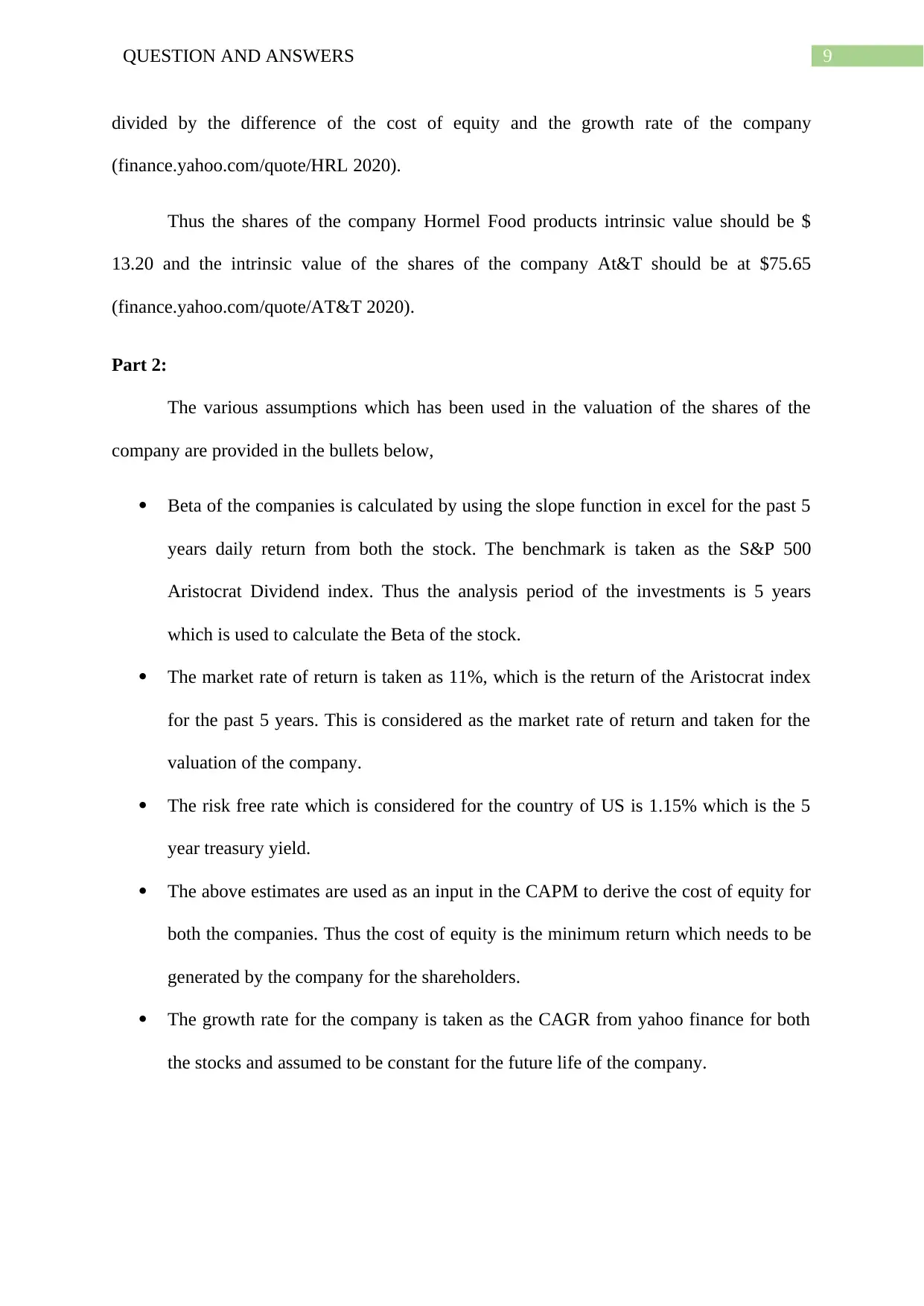

The project manager advised to take on the WACC of the company as the cost of

capital of the project. This is a correct measure only if the risk which is present in the project

is same as the risk of the company. Hence, if the risk is the same then the WACC of the

company which is 9.13% and is calculated in the figure below can be taken as the cost of

capital of the project.

Answer to Question 1:

Part 1:

The cost of capital of a project depends on various factors which needs to be

considered by the company management before selecting one for a project. The cost of

capital of debt as highlighted by the CEO wants to take as 6%, which is the cost of debt since

the project would be financed with debt. At first sight this seems to be appropriate, however

the debt would be recorded in the balance sheet of the company and would affect the credit

worthiness of the company. Thus, taking the cost of debt as the cost of capital for a project

would be incorrect as it would not highlight the true measure of risk which is present in the

project (Marcu and et.al 2017).

The project manager advised to take on the WACC of the company as the cost of

capital of the project. This is a correct measure only if the risk which is present in the project

is same as the risk of the company. Hence, if the risk is the same then the WACC of the

company which is 9.13% and is calculated in the figure below can be taken as the cost of

capital of the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3QUESTION AND ANSWERS

Figure 1: Calculation of WACC

This is taken as the cost of capital for the project as it is assumed the risk of the

project and the risk of the company is same. Thus if the risk of the project if would had been

different from the risk of the company the WACC of the company would not had been taken

for evaluating the project. Then a specific project risk cost would be calculated which would

be used to evaluate the project (Rich, Rose and Delaney 2018).

Part 2:

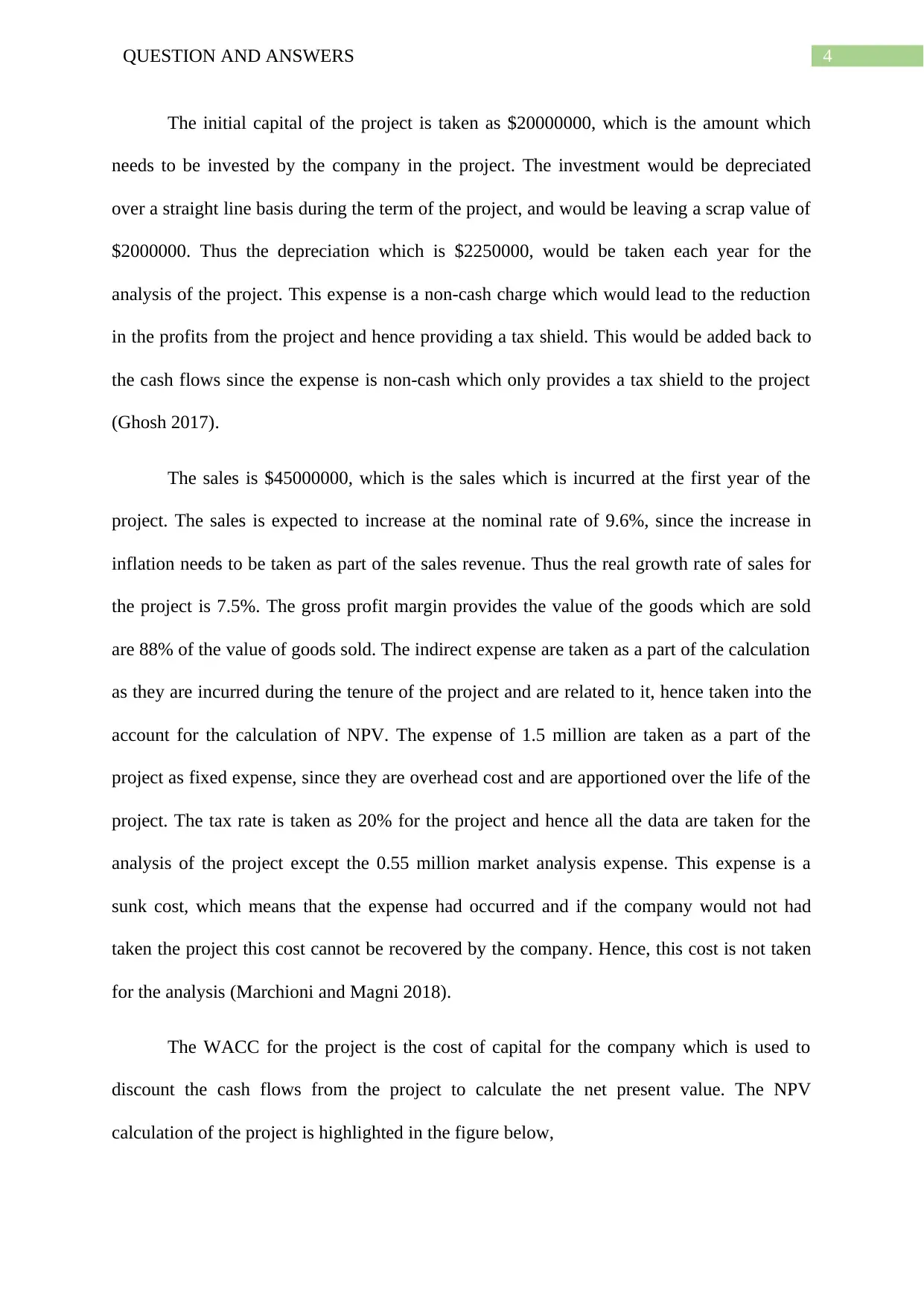

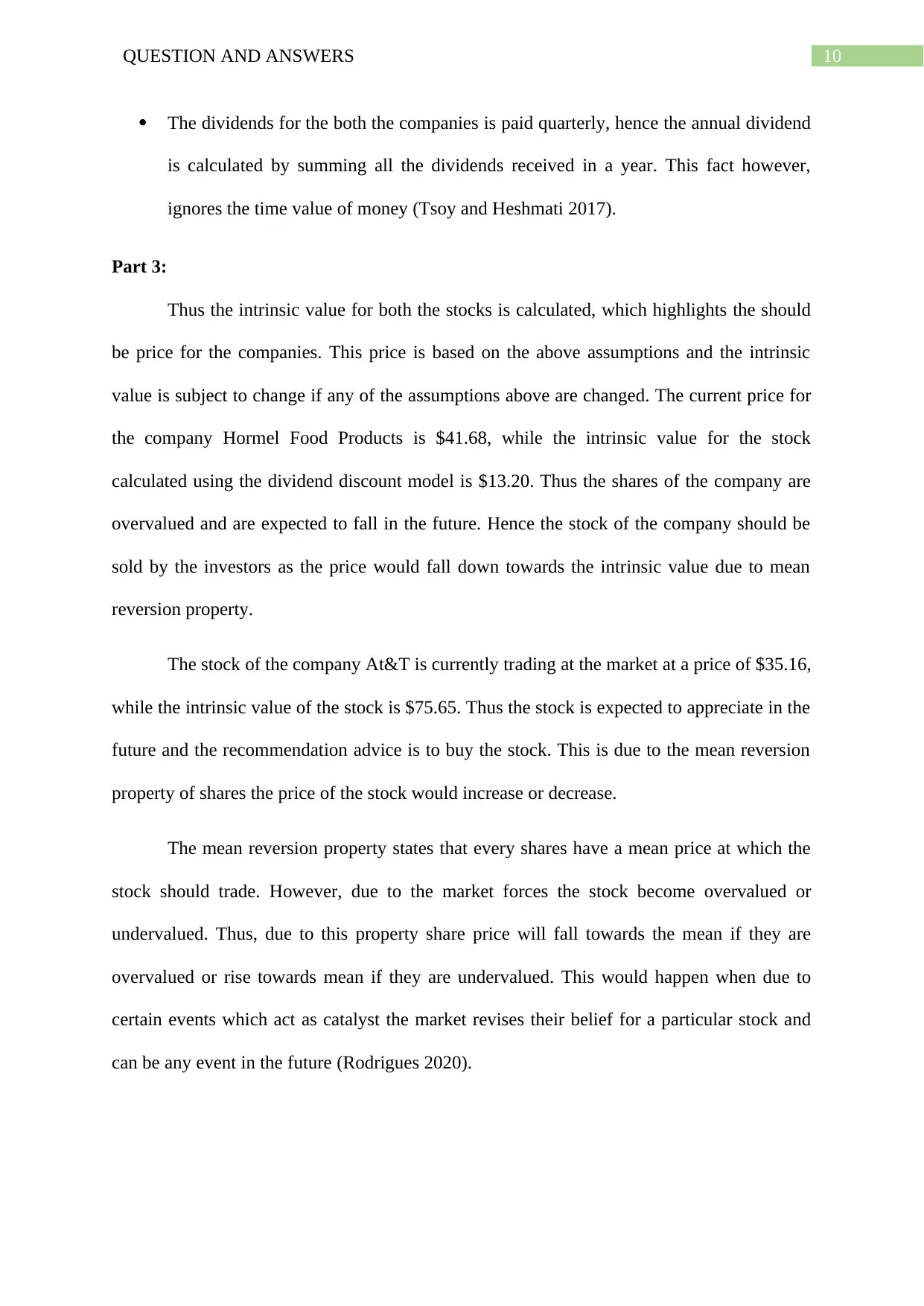

The analysis of the project with an NPV evaluation is conducted to highlight the

expected value the project is creating for the company. This requires a series of inputs and

assumptions which is to be taken in the analysis (Dhankar 2019). Thus, the inputs which is

taken for the analysis is highlighted in the figure below,

Figure 2: Data inputs for NPV analysis

Figure 1: Calculation of WACC

This is taken as the cost of capital for the project as it is assumed the risk of the

project and the risk of the company is same. Thus if the risk of the project if would had been

different from the risk of the company the WACC of the company would not had been taken

for evaluating the project. Then a specific project risk cost would be calculated which would

be used to evaluate the project (Rich, Rose and Delaney 2018).

Part 2:

The analysis of the project with an NPV evaluation is conducted to highlight the

expected value the project is creating for the company. This requires a series of inputs and

assumptions which is to be taken in the analysis (Dhankar 2019). Thus, the inputs which is

taken for the analysis is highlighted in the figure below,

Figure 2: Data inputs for NPV analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4QUESTION AND ANSWERS

The initial capital of the project is taken as $20000000, which is the amount which

needs to be invested by the company in the project. The investment would be depreciated

over a straight line basis during the term of the project, and would be leaving a scrap value of

$2000000. Thus the depreciation which is $2250000, would be taken each year for the

analysis of the project. This expense is a non-cash charge which would lead to the reduction

in the profits from the project and hence providing a tax shield. This would be added back to

the cash flows since the expense is non-cash which only provides a tax shield to the project

(Ghosh 2017).

The sales is $45000000, which is the sales which is incurred at the first year of the

project. The sales is expected to increase at the nominal rate of 9.6%, since the increase in

inflation needs to be taken as part of the sales revenue. Thus the real growth rate of sales for

the project is 7.5%. The gross profit margin provides the value of the goods which are sold

are 88% of the value of goods sold. The indirect expense are taken as a part of the calculation

as they are incurred during the tenure of the project and are related to it, hence taken into the

account for the calculation of NPV. The expense of 1.5 million are taken as a part of the

project as fixed expense, since they are overhead cost and are apportioned over the life of the

project. The tax rate is taken as 20% for the project and hence all the data are taken for the

analysis of the project except the 0.55 million market analysis expense. This expense is a

sunk cost, which means that the expense had occurred and if the company would not had

taken the project this cost cannot be recovered by the company. Hence, this cost is not taken

for the analysis (Marchioni and Magni 2018).

The WACC for the project is the cost of capital for the company which is used to

discount the cash flows from the project to calculate the net present value. The NPV

calculation of the project is highlighted in the figure below,

The initial capital of the project is taken as $20000000, which is the amount which

needs to be invested by the company in the project. The investment would be depreciated

over a straight line basis during the term of the project, and would be leaving a scrap value of

$2000000. Thus the depreciation which is $2250000, would be taken each year for the

analysis of the project. This expense is a non-cash charge which would lead to the reduction

in the profits from the project and hence providing a tax shield. This would be added back to

the cash flows since the expense is non-cash which only provides a tax shield to the project

(Ghosh 2017).

The sales is $45000000, which is the sales which is incurred at the first year of the

project. The sales is expected to increase at the nominal rate of 9.6%, since the increase in

inflation needs to be taken as part of the sales revenue. Thus the real growth rate of sales for

the project is 7.5%. The gross profit margin provides the value of the goods which are sold

are 88% of the value of goods sold. The indirect expense are taken as a part of the calculation

as they are incurred during the tenure of the project and are related to it, hence taken into the

account for the calculation of NPV. The expense of 1.5 million are taken as a part of the

project as fixed expense, since they are overhead cost and are apportioned over the life of the

project. The tax rate is taken as 20% for the project and hence all the data are taken for the

analysis of the project except the 0.55 million market analysis expense. This expense is a

sunk cost, which means that the expense had occurred and if the company would not had

taken the project this cost cannot be recovered by the company. Hence, this cost is not taken

for the analysis (Marchioni and Magni 2018).

The WACC for the project is the cost of capital for the company which is used to

discount the cash flows from the project to calculate the net present value. The NPV

calculation of the project is highlighted in the figure below,

5QUESTION AND ANSWERS

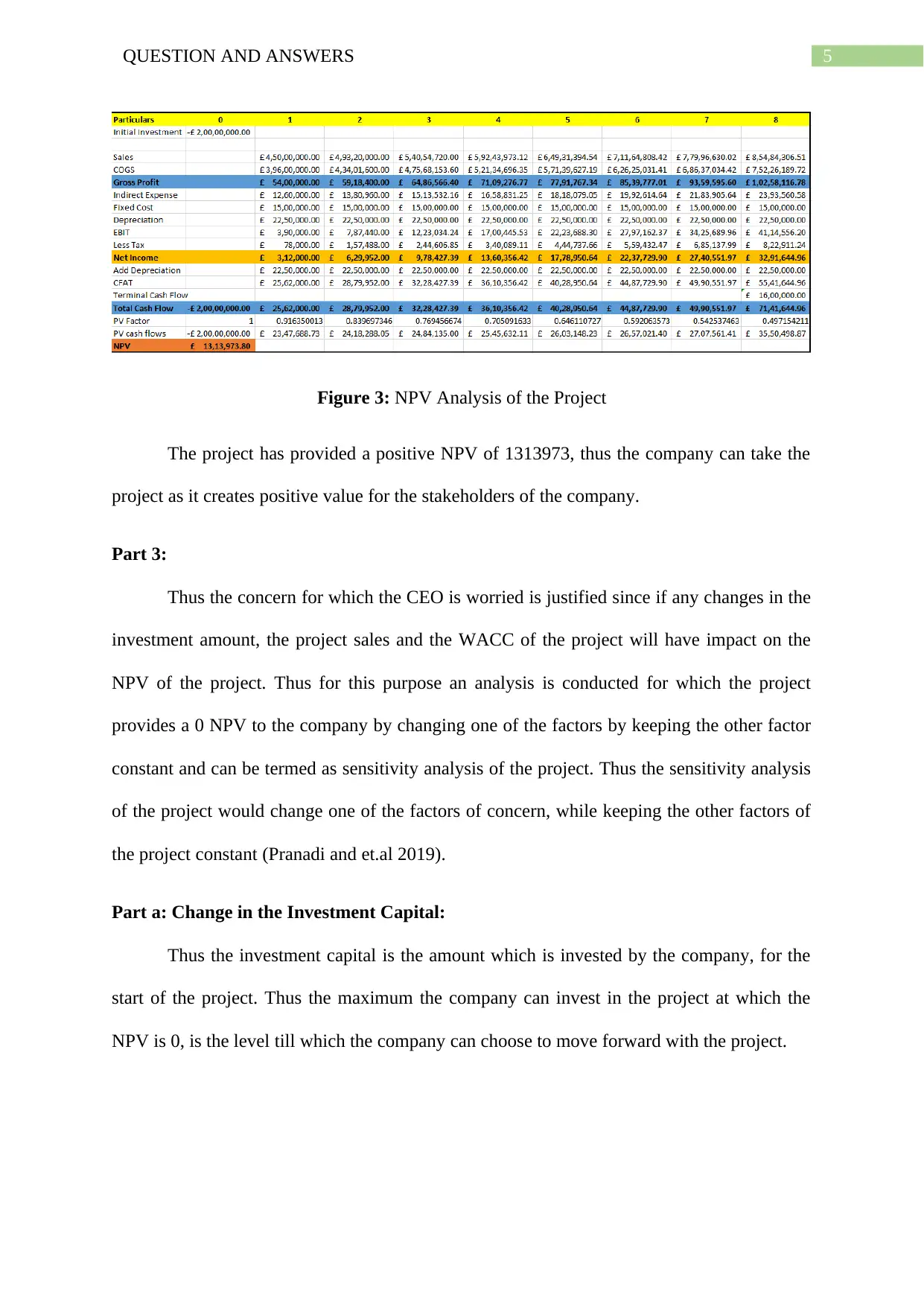

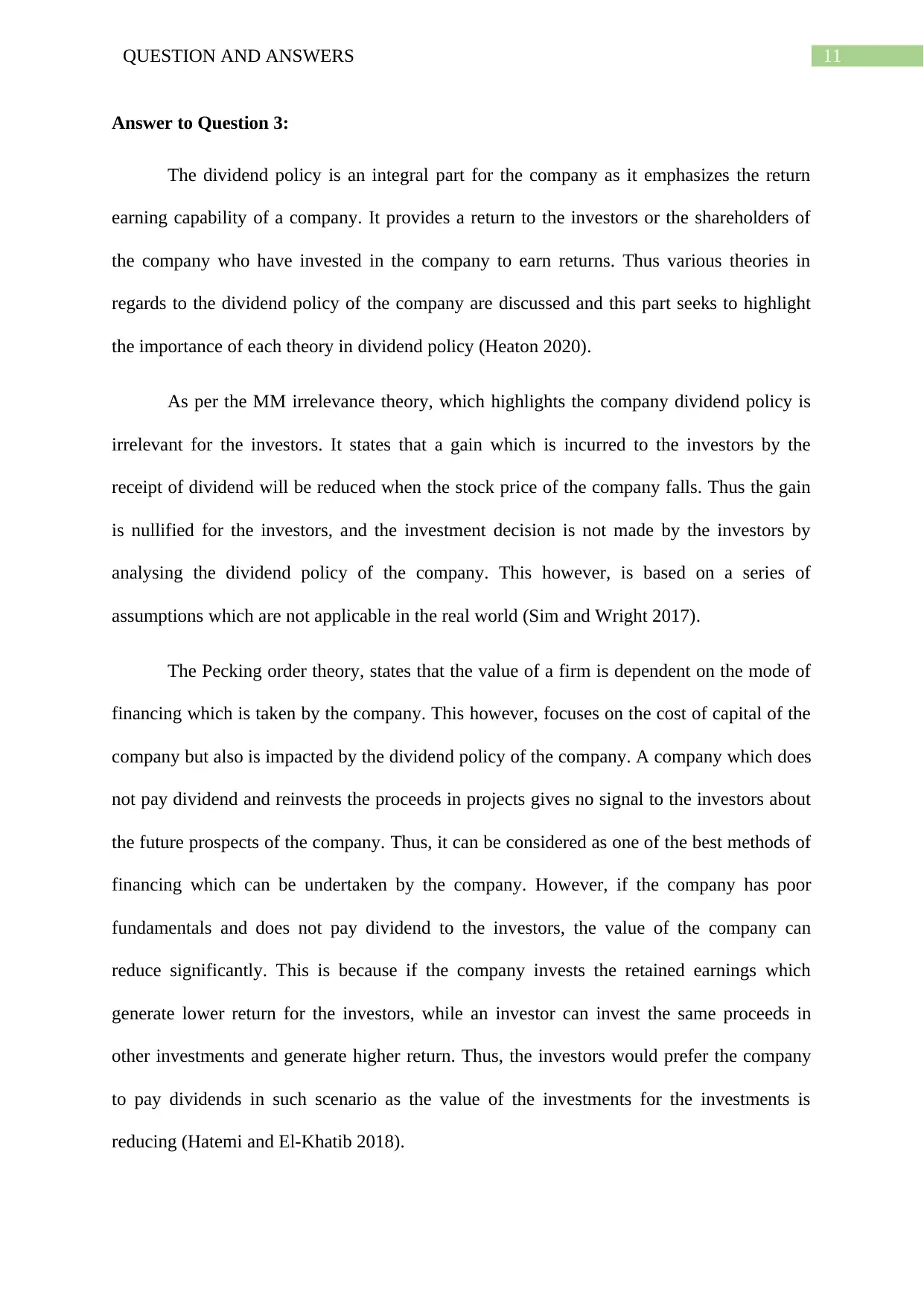

Figure 3: NPV Analysis of the Project

The project has provided a positive NPV of 1313973, thus the company can take the

project as it creates positive value for the stakeholders of the company.

Part 3:

Thus the concern for which the CEO is worried is justified since if any changes in the

investment amount, the project sales and the WACC of the project will have impact on the

NPV of the project. Thus for this purpose an analysis is conducted for which the project

provides a 0 NPV to the company by changing one of the factors by keeping the other factor

constant and can be termed as sensitivity analysis of the project. Thus the sensitivity analysis

of the project would change one of the factors of concern, while keeping the other factors of

the project constant (Pranadi and et.al 2019).

Part a: Change in the Investment Capital:

Thus the investment capital is the amount which is invested by the company, for the

start of the project. Thus the maximum the company can invest in the project at which the

NPV is 0, is the level till which the company can choose to move forward with the project.

Figure 3: NPV Analysis of the Project

The project has provided a positive NPV of 1313973, thus the company can take the

project as it creates positive value for the stakeholders of the company.

Part 3:

Thus the concern for which the CEO is worried is justified since if any changes in the

investment amount, the project sales and the WACC of the project will have impact on the

NPV of the project. Thus for this purpose an analysis is conducted for which the project

provides a 0 NPV to the company by changing one of the factors by keeping the other factor

constant and can be termed as sensitivity analysis of the project. Thus the sensitivity analysis

of the project would change one of the factors of concern, while keeping the other factors of

the project constant (Pranadi and et.al 2019).

Part a: Change in the Investment Capital:

Thus the investment capital is the amount which is invested by the company, for the

start of the project. Thus the maximum the company can invest in the project at which the

NPV is 0, is the level till which the company can choose to move forward with the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6QUESTION AND ANSWERS

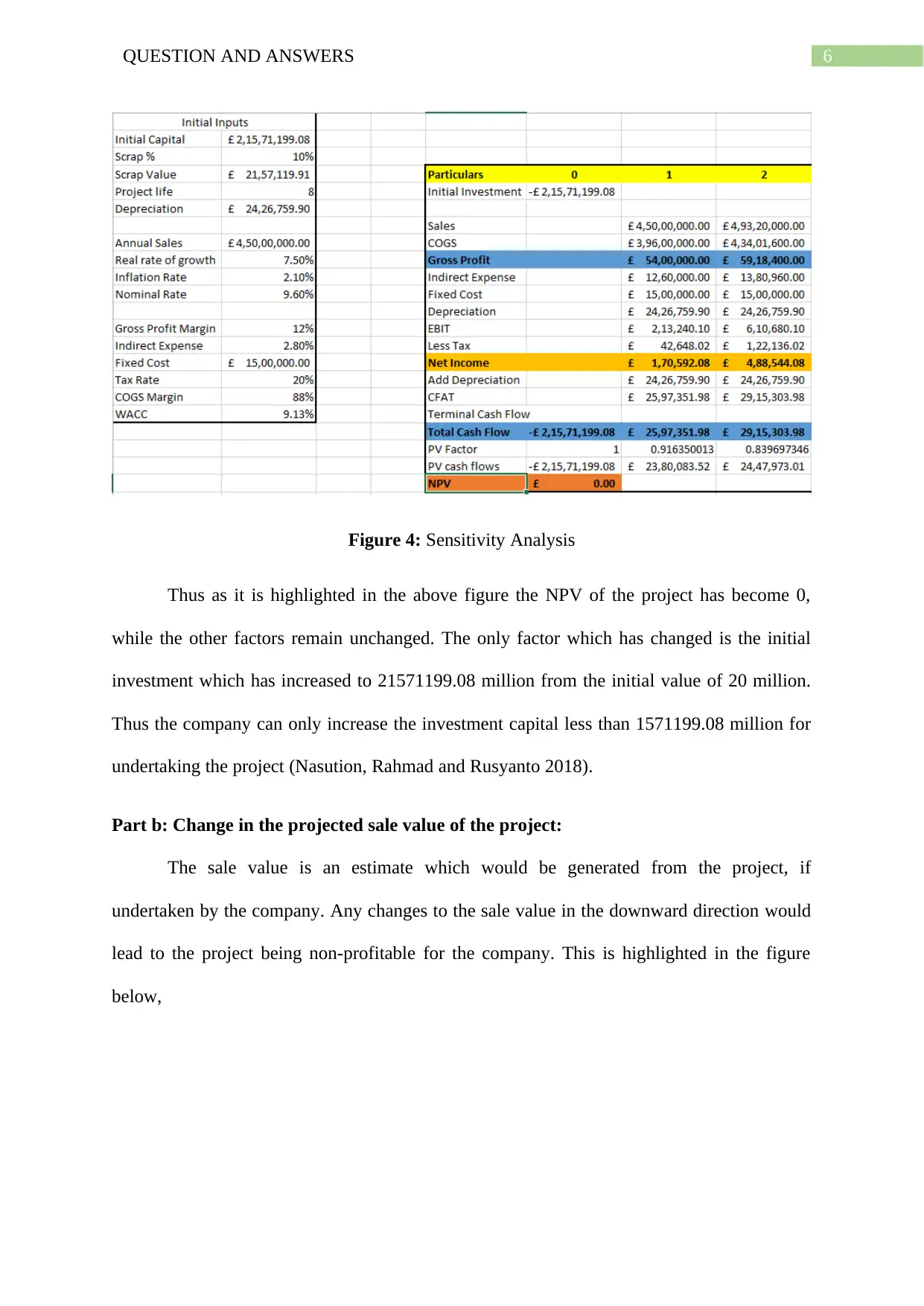

Figure 4: Sensitivity Analysis

Thus as it is highlighted in the above figure the NPV of the project has become 0,

while the other factors remain unchanged. The only factor which has changed is the initial

investment which has increased to 21571199.08 million from the initial value of 20 million.

Thus the company can only increase the investment capital less than 1571199.08 million for

undertaking the project (Nasution, Rahmad and Rusyanto 2018).

Part b: Change in the projected sale value of the project:

The sale value is an estimate which would be generated from the project, if

undertaken by the company. Any changes to the sale value in the downward direction would

lead to the project being non-profitable for the company. This is highlighted in the figure

below,

Figure 4: Sensitivity Analysis

Thus as it is highlighted in the above figure the NPV of the project has become 0,

while the other factors remain unchanged. The only factor which has changed is the initial

investment which has increased to 21571199.08 million from the initial value of 20 million.

Thus the company can only increase the investment capital less than 1571199.08 million for

undertaking the project (Nasution, Rahmad and Rusyanto 2018).

Part b: Change in the projected sale value of the project:

The sale value is an estimate which would be generated from the project, if

undertaken by the company. Any changes to the sale value in the downward direction would

lead to the project being non-profitable for the company. This is highlighted in the figure

below,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7QUESTION AND ANSWERS

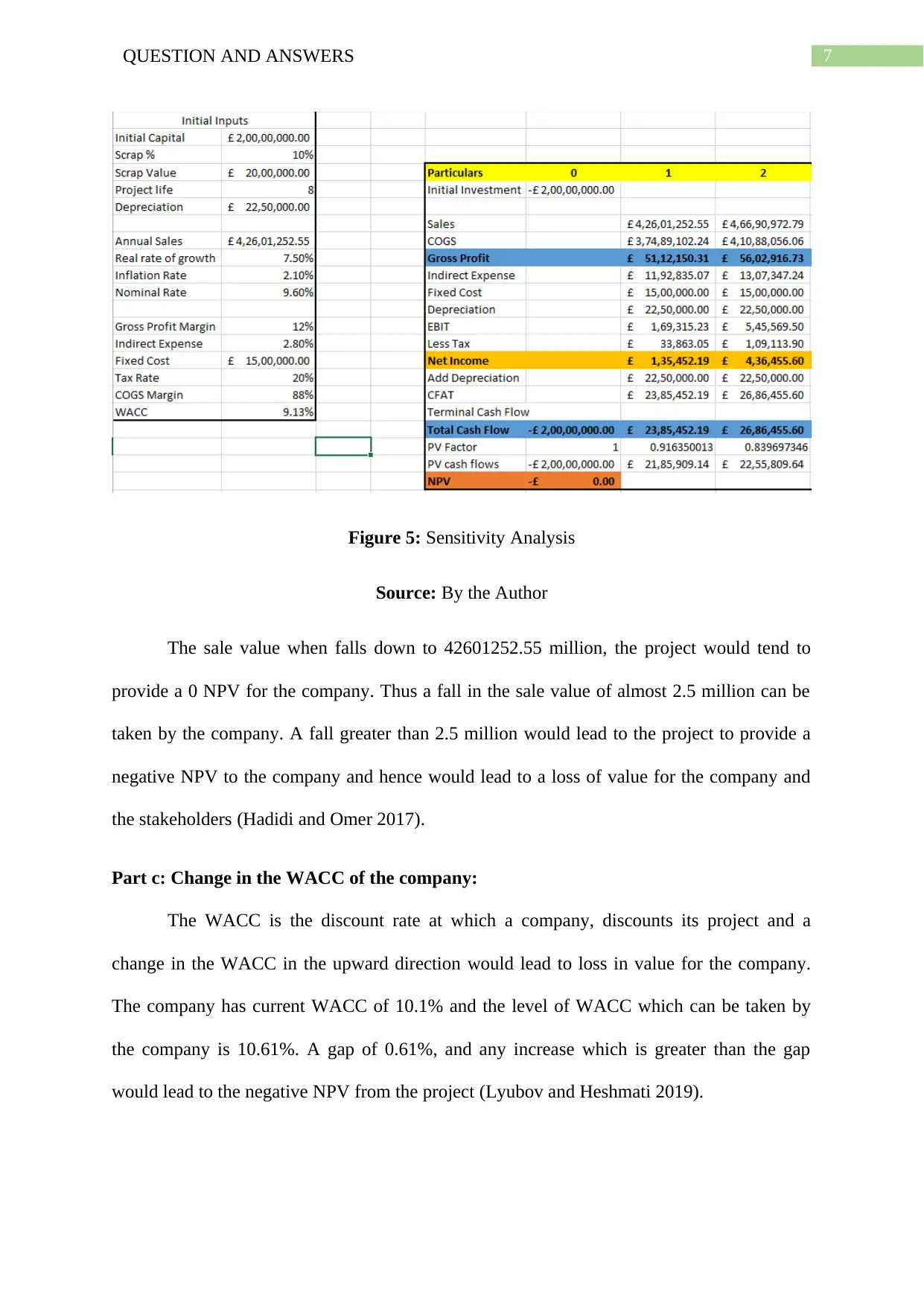

Figure 5: Sensitivity Analysis

Source: By the Author

The sale value when falls down to 42601252.55 million, the project would tend to

provide a 0 NPV for the company. Thus a fall in the sale value of almost 2.5 million can be

taken by the company. A fall greater than 2.5 million would lead to the project to provide a

negative NPV to the company and hence would lead to a loss of value for the company and

the stakeholders (Hadidi and Omer 2017).

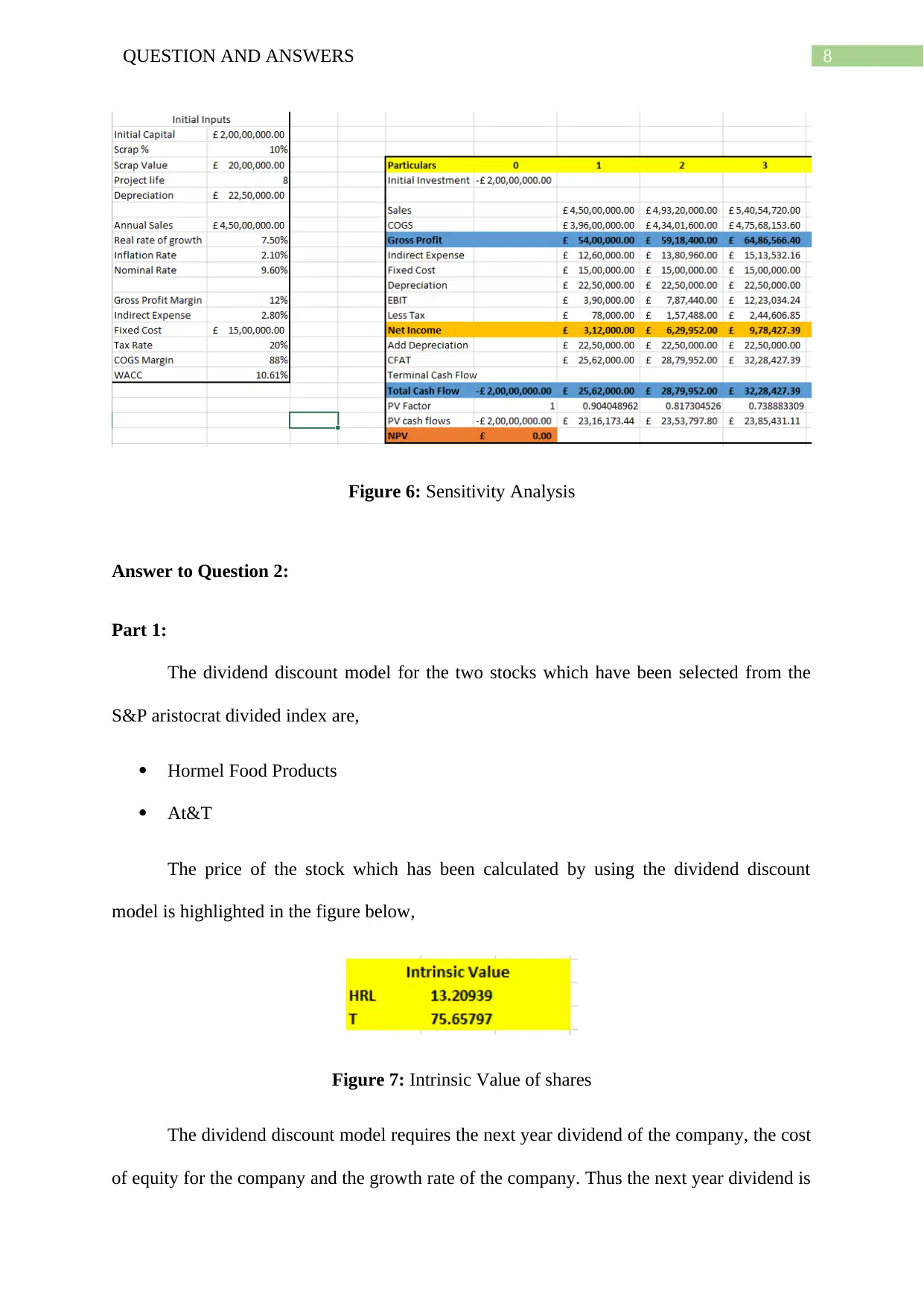

Part c: Change in the WACC of the company:

The WACC is the discount rate at which a company, discounts its project and a

change in the WACC in the upward direction would lead to loss in value for the company.

The company has current WACC of 10.1% and the level of WACC which can be taken by

the company is 10.61%. A gap of 0.61%, and any increase which is greater than the gap

would lead to the negative NPV from the project (Lyubov and Heshmati 2019).

Figure 5: Sensitivity Analysis

Source: By the Author

The sale value when falls down to 42601252.55 million, the project would tend to

provide a 0 NPV for the company. Thus a fall in the sale value of almost 2.5 million can be

taken by the company. A fall greater than 2.5 million would lead to the project to provide a

negative NPV to the company and hence would lead to a loss of value for the company and

the stakeholders (Hadidi and Omer 2017).

Part c: Change in the WACC of the company:

The WACC is the discount rate at which a company, discounts its project and a

change in the WACC in the upward direction would lead to loss in value for the company.

The company has current WACC of 10.1% and the level of WACC which can be taken by

the company is 10.61%. A gap of 0.61%, and any increase which is greater than the gap

would lead to the negative NPV from the project (Lyubov and Heshmati 2019).

8QUESTION AND ANSWERS

Figure 6: Sensitivity Analysis

Answer to Question 2:

Part 1:

The dividend discount model for the two stocks which have been selected from the

S&P aristocrat divided index are,

Hormel Food Products

At&T

The price of the stock which has been calculated by using the dividend discount

model is highlighted in the figure below,

Figure 7: Intrinsic Value of shares

The dividend discount model requires the next year dividend of the company, the cost

of equity for the company and the growth rate of the company. Thus the next year dividend is

Figure 6: Sensitivity Analysis

Answer to Question 2:

Part 1:

The dividend discount model for the two stocks which have been selected from the

S&P aristocrat divided index are,

Hormel Food Products

At&T

The price of the stock which has been calculated by using the dividend discount

model is highlighted in the figure below,

Figure 7: Intrinsic Value of shares

The dividend discount model requires the next year dividend of the company, the cost

of equity for the company and the growth rate of the company. Thus the next year dividend is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9QUESTION AND ANSWERS

divided by the difference of the cost of equity and the growth rate of the company

(finance.yahoo.com/quote/HRL 2020).

Thus the shares of the company Hormel Food products intrinsic value should be $

13.20 and the intrinsic value of the shares of the company At&T should be at $75.65

(finance.yahoo.com/quote/AT&T 2020).

Part 2:

The various assumptions which has been used in the valuation of the shares of the

company are provided in the bullets below,

Beta of the companies is calculated by using the slope function in excel for the past 5

years daily return from both the stock. The benchmark is taken as the S&P 500

Aristocrat Dividend index. Thus the analysis period of the investments is 5 years

which is used to calculate the Beta of the stock.

The market rate of return is taken as 11%, which is the return of the Aristocrat index

for the past 5 years. This is considered as the market rate of return and taken for the

valuation of the company.

The risk free rate which is considered for the country of US is 1.15% which is the 5

year treasury yield.

The above estimates are used as an input in the CAPM to derive the cost of equity for

both the companies. Thus the cost of equity is the minimum return which needs to be

generated by the company for the shareholders.

The growth rate for the company is taken as the CAGR from yahoo finance for both

the stocks and assumed to be constant for the future life of the company.

divided by the difference of the cost of equity and the growth rate of the company

(finance.yahoo.com/quote/HRL 2020).

Thus the shares of the company Hormel Food products intrinsic value should be $

13.20 and the intrinsic value of the shares of the company At&T should be at $75.65

(finance.yahoo.com/quote/AT&T 2020).

Part 2:

The various assumptions which has been used in the valuation of the shares of the

company are provided in the bullets below,

Beta of the companies is calculated by using the slope function in excel for the past 5

years daily return from both the stock. The benchmark is taken as the S&P 500

Aristocrat Dividend index. Thus the analysis period of the investments is 5 years

which is used to calculate the Beta of the stock.

The market rate of return is taken as 11%, which is the return of the Aristocrat index

for the past 5 years. This is considered as the market rate of return and taken for the

valuation of the company.

The risk free rate which is considered for the country of US is 1.15% which is the 5

year treasury yield.

The above estimates are used as an input in the CAPM to derive the cost of equity for

both the companies. Thus the cost of equity is the minimum return which needs to be

generated by the company for the shareholders.

The growth rate for the company is taken as the CAGR from yahoo finance for both

the stocks and assumed to be constant for the future life of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10QUESTION AND ANSWERS

The dividends for the both the companies is paid quarterly, hence the annual dividend

is calculated by summing all the dividends received in a year. This fact however,

ignores the time value of money (Tsoy and Heshmati 2017).

Part 3:

Thus the intrinsic value for both the stocks is calculated, which highlights the should

be price for the companies. This price is based on the above assumptions and the intrinsic

value is subject to change if any of the assumptions above are changed. The current price for

the company Hormel Food Products is $41.68, while the intrinsic value for the stock

calculated using the dividend discount model is $13.20. Thus the shares of the company are

overvalued and are expected to fall in the future. Hence the stock of the company should be

sold by the investors as the price would fall down towards the intrinsic value due to mean

reversion property.

The stock of the company At&T is currently trading at the market at a price of $35.16,

while the intrinsic value of the stock is $75.65. Thus the stock is expected to appreciate in the

future and the recommendation advice is to buy the stock. This is due to the mean reversion

property of shares the price of the stock would increase or decrease.

The mean reversion property states that every shares have a mean price at which the

stock should trade. However, due to the market forces the stock become overvalued or

undervalued. Thus, due to this property share price will fall towards the mean if they are

overvalued or rise towards mean if they are undervalued. This would happen when due to

certain events which act as catalyst the market revises their belief for a particular stock and

can be any event in the future (Rodrigues 2020).

The dividends for the both the companies is paid quarterly, hence the annual dividend

is calculated by summing all the dividends received in a year. This fact however,

ignores the time value of money (Tsoy and Heshmati 2017).

Part 3:

Thus the intrinsic value for both the stocks is calculated, which highlights the should

be price for the companies. This price is based on the above assumptions and the intrinsic

value is subject to change if any of the assumptions above are changed. The current price for

the company Hormel Food Products is $41.68, while the intrinsic value for the stock

calculated using the dividend discount model is $13.20. Thus the shares of the company are

overvalued and are expected to fall in the future. Hence the stock of the company should be

sold by the investors as the price would fall down towards the intrinsic value due to mean

reversion property.

The stock of the company At&T is currently trading at the market at a price of $35.16,

while the intrinsic value of the stock is $75.65. Thus the stock is expected to appreciate in the

future and the recommendation advice is to buy the stock. This is due to the mean reversion

property of shares the price of the stock would increase or decrease.

The mean reversion property states that every shares have a mean price at which the

stock should trade. However, due to the market forces the stock become overvalued or

undervalued. Thus, due to this property share price will fall towards the mean if they are

overvalued or rise towards mean if they are undervalued. This would happen when due to

certain events which act as catalyst the market revises their belief for a particular stock and

can be any event in the future (Rodrigues 2020).

11QUESTION AND ANSWERS

Answer to Question 3:

The dividend policy is an integral part for the company as it emphasizes the return

earning capability of a company. It provides a return to the investors or the shareholders of

the company who have invested in the company to earn returns. Thus various theories in

regards to the dividend policy of the company are discussed and this part seeks to highlight

the importance of each theory in dividend policy (Heaton 2020).

As per the MM irrelevance theory, which highlights the company dividend policy is

irrelevant for the investors. It states that a gain which is incurred to the investors by the

receipt of dividend will be reduced when the stock price of the company falls. Thus the gain

is nullified for the investors, and the investment decision is not made by the investors by

analysing the dividend policy of the company. This however, is based on a series of

assumptions which are not applicable in the real world (Sim and Wright 2017).

The Pecking order theory, states that the value of a firm is dependent on the mode of

financing which is taken by the company. This however, focuses on the cost of capital of the

company but also is impacted by the dividend policy of the company. A company which does

not pay dividend and reinvests the proceeds in projects gives no signal to the investors about

the future prospects of the company. Thus, it can be considered as one of the best methods of

financing which can be undertaken by the company. However, if the company has poor

fundamentals and does not pay dividend to the investors, the value of the company can

reduce significantly. This is because if the company invests the retained earnings which

generate lower return for the investors, while an investor can invest the same proceeds in

other investments and generate higher return. Thus, the investors would prefer the company

to pay dividends in such scenario as the value of the investments for the investments is

reducing (Hatemi and El-Khatib 2018).

Answer to Question 3:

The dividend policy is an integral part for the company as it emphasizes the return

earning capability of a company. It provides a return to the investors or the shareholders of

the company who have invested in the company to earn returns. Thus various theories in

regards to the dividend policy of the company are discussed and this part seeks to highlight

the importance of each theory in dividend policy (Heaton 2020).

As per the MM irrelevance theory, which highlights the company dividend policy is

irrelevant for the investors. It states that a gain which is incurred to the investors by the

receipt of dividend will be reduced when the stock price of the company falls. Thus the gain

is nullified for the investors, and the investment decision is not made by the investors by

analysing the dividend policy of the company. This however, is based on a series of

assumptions which are not applicable in the real world (Sim and Wright 2017).

The Pecking order theory, states that the value of a firm is dependent on the mode of

financing which is taken by the company. This however, focuses on the cost of capital of the

company but also is impacted by the dividend policy of the company. A company which does

not pay dividend and reinvests the proceeds in projects gives no signal to the investors about

the future prospects of the company. Thus, it can be considered as one of the best methods of

financing which can be undertaken by the company. However, if the company has poor

fundamentals and does not pay dividend to the investors, the value of the company can

reduce significantly. This is because if the company invests the retained earnings which

generate lower return for the investors, while an investor can invest the same proceeds in

other investments and generate higher return. Thus, the investors would prefer the company

to pay dividends in such scenario as the value of the investments for the investments is

reducing (Hatemi and El-Khatib 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.